Government

S&P Futures Inexplicably Dip As “Magical, Non-Stop Rally” Reverses

S&P Futures Inexplicably Dip As "Magical, Non-Stop Rally" Reverses

Share this:

After nine consecutive days of record highs and after closing higher on Wednesday for the ninth time in the past 10 sessions, S&P futures have done something they haven't done in a long time: following a "magical, non-stop rally in stocks continues" as Adam Button of ForexLive dubbed it, futures are down this morning, trading down 0.5% at session lows as of 730am at 3,564, down some 20 points from their all time high hit yesterday.

Chip makers including Nvidia fell in the premarket while banks like JPMorgan Chase and Bank of America on the back of a Deutsche Bank upgrade and as the rotation away from tech stocks looked set to extend. Shares of Apple, Adobe, Nvidia and Netflix, all of which have soared more than 70% this year, slipped about 2% each in premarket trading, following yesterday's declines as the gamma trade appears to be unwinding. Tesla tumbled 6.6%, falling for the third session after announcing a $5 billion stock offering. PVH Corp rose 2.5% after Calvin Klein owner posted a surprise quarterly profit, boosted by strong online demand for comfortable and casual clothing during the coronavirus-led shift to work from home.

"What we are seeing is a little bit of profit-taking now in the big tech sector as people look to rebalance their portfolios going into the last part of this year," Ann Berry, partner at Cornell Capital LLC, said on Bloomberg TV. "Folks are trying to go back to basics a little bit as we continue to see these surges and the topping out in the value of the market right now."

The perplexing decline in Emini futures took place even as European shares jumped the most in a month on the back of continued EURUSD weakness (the pair dipped to 1,1790 after hitting 1.20 two days ago) and after France introduced new stimulus measures to drive the economy and spur job creation.

France plans to spend €100 billion to pull its economy out of a deep coronavirus-induced slump, signalling renewed efforts by President Emmanuel Macron to push through a pro-business reform agenda. The stimulus equates to 4% of GDP, meaning France is plowing more public cash into its economy than any other big European country as a percentage of GDP, an official said ahead of its formal launch later on Thursday. France’s recession, marked by a 13.8% second quarter GDP contraction that coincided with the country’s COVID-19 lockdown and is set to generate an 11% drop in 2020 as a whole, has also been one of Europe’s deepest.

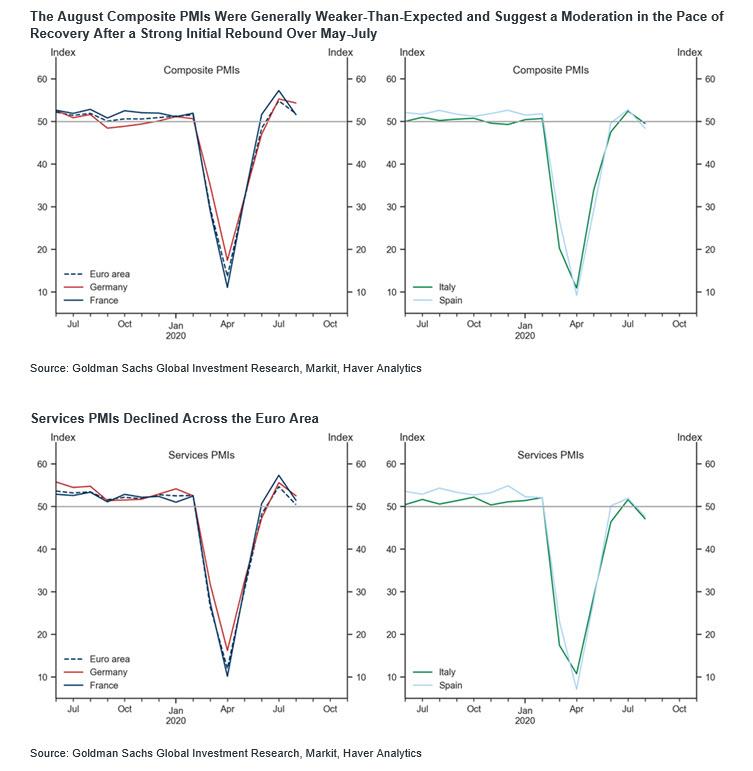

As a result, France’s CAC 40 Index surged as much as 2% amid a broad rally in Europe that showed the stock market advance is continuing to expand beyond the tech sector, while the euro dipped for a third day on signals the European Central Bank is concerned about the currency’s strength (see "With A Record Number Of Bulls, The Euro Is Ripe To Tumble After "Euphoric Run"). Meanwhile, the French Service PMI dipped from 51.9 in July to 51.5 in August, missing expectations of 51.9, even as Germany posted a modest beat (51.9 vs exp. 51.6, last 51.6).

Commenting on the European PMIs, Goldman said that the Euro area composite PMI was revised up by 0.3pt from its flash estimate of 51.6 for August. This reflected a sizeable upward revision to the German composite PMI (concentrated in the service sector), which more than offset the downward flash-to-final revision in France and (implicitly) elsewhere in the Euro area. Both the Italian and Spanish composite PMIs came in below expectations, especially the latter, declining by 3.0 and 4.4pt respectively. The August PMIs across the Euro area indicate a slowdown in the pace of recovery—with a potential contraction in Spain, but also Italy—after a notably stronger-than-expected initial rebound from the April trough.

The Stoxx 600 Travel & Leisure Index climbed to the highest since June 10, while the Auto & Parts Index reaches best level since June 8, amid optimism surrounding the quest for a Covid-19 vaccine, fresh economic stimulus in France, and a weaker euro boosting exporters. SXTP up 2.7% leading the Stoxx 600; IAG (+6%), Carnival (+5.7%) and Easyjet (+5.7%) lead SXTP; Peugeot (+4.9%), Renault (+4.8%), Fiat Chrysler (+3.8%) lead SXAP; The first results showing whether a vaccine can stop people from getting the virus could come by mid-September from AstraZeneca, according to Airfinity, an analytics company that tracks drug trials, while two other contenders may also have initial data before a key FDA meeting on Oct. 22

Earlier in the session, Asian stocks were little changed, with energy falling and IT rising, after rising in the last session. Markets in the region were mixed, with South Korea's Kospi Index and Australia's S&P/ASX 200 rising, and Jakarta Composite and Shanghai Composite falling. The Topix gained 0.5%, with Fukushima Bank and Solxyz rising the most. China's Shanghai Composite Index retreated 0.6%, with Bohai Ferry Group Ltd and Jilin Forest Ind posting the biggest slides.

Global stock have been rising on continued central bank stimulus as well as renewed hopes for a coronavirus vaccine, fueling a catch-up trade in markets that had lagged the U.S. The S&P 500 jumped 1.5% yesterday to hit another record and Japanese stocks are trading at the highest since February. Data on Thursday is likely to show the number of Americans filing for weekly jobless claims remained elevated in the latest week, but dipped below the 1 million mark. Separately, reading on ISM’s services index probably edged lower to 57 in August from 58.1. The critical monthly payrolls report by the Labor Department is set for release on Friday. Signs that the U.S. economic recovery is faltering has raised concerns about depleting federal aid. At the same time, investors are hopeful that the next fiscal coronavirus relief bill could be unveiled in the coming days.

“Markets continue to show unrestrained faith in the capacity of central bank liquidity to chart a relatively smooth path for the global economy out of the Covid challenges,” said Stephen Miller, investment strategist at GSFM.

The U.S. Centers for Disease Control and Prevention - after halting eviction - told states to prepare for a Covid-19 vaccine to be ready by Nov. 1, an aggressive goal that suggests availability just before the presidential election. Anthony Fauci warned of a potential surge in American cases from the coming long holiday weekend.

In FX, the dollar rose against G-10 peers, with the Bloomberg Dollar Spot Index climbing a third day. The euro headed for the biggest three-day decline since June following signals that the ECB is concerned about the strength of the common currency. The pound dropped a second day against the greenback. Norway’s krone and the New Zealand dollar led losses among G-10 currencies.

In rates, Treasury yields were little changed across a steeper curve, off session highs reached during European morning. Yields were cheaper by less than 1bp across the curve, with 2s10s and 5s30s curves marginally steeper; 10-year yields around 0.655% with bunds outperforming and gilts lagging, each by ~1bp. At 11am, the Treasury Department will announce sizes of next week’s three coupon auctions; based on its forecasts in Aug. 5 refunding announcement, expectation is for $50b 3-year new issue (vs $48b last month), $35b 10-year reopening (vs $29b in previous cycle) and $23b 30-year reopening (vs $19b).

In commodities, WTI and Brent continued to drift lower, with Brent down more than 1%, partly weighed on by the firmer USD, while traders kept an eye on the supply side of the equation as Gulf of Mexico production comes back online, while comments from Russian Energy Minister Novak yesterday, regarding oil demand at ~90% of pre-pandemic levels and calling on OPEC to take this into account, hinted at a potential proposal of early tapering of the OPEC+ output curbs. Gold dropped for the third day on the back of continued dollar strength, further decoupling from real rates.

Looking at the day ahead, the ISM services index from the US will be the highlight, as well as the weekly initial jobless claims and the July trade balance from the US. Central bank speakers today include BoE Governor Bailey as well as Deputy Governor Ramsden, along with the ECB’s Schnabel and the Fed’s Evans. Campbell Soup, Ciena, Broadcom and DocuSign are among companies reporting earnings.

Market Wrap

- S&P 500 futures down 0.1% to 3,575.50

- STOXX Europe 600 up 1.1% to 375.28

- MXAP up 0.08% to 174.30

- MXAPJ down 0.1% to 577.19

- Nikkei up 0.9% to 23,465.53

- Topix up 0.5% to 1,631.24

- Hang Seng Index down 0.5% to 25,007.60

- Shanghai Composite down 0.6% to 3,384.98

- Sensex up 0.02% to 39,093.85

- Australia S&P/ASX 200 up 0.8% to 6,112.61

- Kospi up 1.3% to 2,395.90

- German 10Y yield rose 0.5 bps to -0.468%

- Euro down 0.3% to $1.1823

- Italian 10Y yield fell 6.3 bps to 0.846%

- Spanish 10Y yield rose 1.5 bps to 0.346%

- Brent futures down 1.4% to $43.81/bbl

- Gold spot down 0.4% to $1,934.71

- U.S. Dollar Index little changedat at 92.87

Top Overnight News from Bloomberg

- The euro area’s recovery ran out of steam midway through the third quarter, with gauges of activity pointing to contractions in Italy and Spain. While manufacturing output rose markedly in August, the larger services sectors aw only marginal growth, according to an IHS Markit report. Orders increased at a slower pace, job cuts continued and confidence about the outlook eased

- Boris Johnson’s officials are urgently working to avert a major border crisis when the U.K. leaves the European Union’s trade regime. According to a leaked document, ministers are asking hauliers and other industry groups for help to avoid chaos at the border when the Brexit transition period expires at the end of the year

- The U.S. Centers for Disease Control and Prevention told states to get ready for coronavirus vaccine distribution as early as November 1 -- days before the presidential election

- Coronavirus cases surpass 26 million globally while deaths exceed 863,000

- Sanofi started human trials for its vaccine, aiming for results in December and planning to then move on quickly to late-state trials

- French President Emmanuel Macron unveiled a 100 billion-euro ($118 billion) stimulus plan to restart the country’s economy after the pandemic, including wage subsidies, tax cuts for businesses and funding for green projects

A quick stroll across global markets, courtesy of NewsSquawk

Asian equity markets ultimately closed mixed after a predominantly positive session following the firm handover from US peers in which the S&P 500 and Nasdaq extended on record highs and DJIA climbed back above 29,000 amid dovish central bank rhetoric and vaccine optimism. ASX 200 (+0.8%) gained from the open with the index led by its top-weighted financials sector and sentiment underpinned by tax cut hopes after Treasurer Frydenberg announced that the government plans to bring forward tax reductions. Nikkei 225 (+0.9%) found support from a favourable currency and after Japan's Chief Cabinet Secretary Suga confirmed he will run in the party leadership race and will continue with Abenomics policies, while index heavyweight Fast Retailing was also buoyed after its domestic same-store sales surged 29.8% last month. Hang Seng (-0.5%) and Shanghai Comp. (-0.6%) were initially positive after stronger than expected data in which Caixin Services PMI topped estimates and Caixin Composite PMI improved, although upside was later reversed following a relatively tepid liquidity effort by the PBoC which resulted to a daily net injection of CNY 20bln and due to US-China tensions after the US imposed fresh restrictions on Chinese diplomats in the US. Finally, 10yr JGBs were higher as they tracked recent gains in T-notes despite the strength seen in equity markets, with prices kept afloat amid declining yields and following marginal improvement in the 30yr JGB auction results.

Top Asian News

- Investors Pile Into OCBC’s Biggest Dollar Bond in Six Years

- Hong Kong Media Mogul Jimmy Lai Acquitted in Intimidation Case

- China Affirms Right to Approve Tech Deals as TikTok Sale Looms

- Singapore’s MAS to Boost Access to Dollar Funding for Banks

European equity markets continue on their upwards trajectory (Euro Stoxx 50 +1.2%) in a continuation of yesterday’s price action and following a firm handover from Wall Street, although a divergence is seen between European and US equity futures, with the latter potentially weighed on by the stalemate on Capitol Hill, whilst NQ underperforms in what seems to be an unwind of the recent tech rally. Note: some have attributed the upside in Europe to a piece via the FT noting that ECB members are likely to cut their inflation projections at next week’s meeting amid the recent EUR strength. However, it is worth keeping in mind that price action does not correlate with the timing of the piece, with futures stable until the European cash open, almost three hours after markets picked up on the FT report. Nonetheless, the region experiences a sea of green with some underperformance seen in UK’s FTSE (+0.6) – weighed on by some large-cap miners as metals succumb to the Dollar. Sectors also reside in positive territory across the board with no clear risk bias to be extracted. Basic resources are the laggards whilst Travel & Leisure top the charts, possibly underpinned by vaccine hopes after NIH’s Fauci said there could be a vaccine ready by November or December. The IT sector meanwhile failed to garner much traction from reports that China is said to be mulling broader chip-sector support to battle US President Trump. In terms of individual movers, Sanofi (+0.7%) and GSK (+0.5%) have not deviated much since the cash open despite initiating its Phase 1/2 trial for its protein-based COVID-19 vaccine candidate, with pre-clinical studies showing promising safety and immunogenicity. Iliad (-3.1%) shares have tumbled after reporting a mixed bag of earnings. Finally, Siemens Healthineers (-3.6%) stand as one of the laggards after the group commenced a cash capital increase.

Top European News

- Europe’s Rebound Lost Momentum With Italy, Spain Shrinking Again

- Merkel Bloc Backs Plan for Extra Deficit Spending Next Year

- Merkel Faces Pressure to Drop Russian Pipeline to Punish Putin

- BOE Talks Up Prospect of Easing as U.K. Faces Triple Threat

In FX, the great Greenback revival seems to have stalled around 93.000 in DXY terms, albeit with the Euro rebounding on the back of a German boost to the pan Eurozone services and composite PMIs after disappointing prints from the periphery and France. Indeed, the Dollar may yet regain the initiative and upward momentum if the services ISM emulates the feats of Tuesday’s manufacturing survey and/or initial claims return to a declining trend. For now, the index is maintaining an underlying bid within a 93.074-92.688 band and taking cues from major counterparts in the main, while US Treasury yields and the curve continue to tick higher and steepen against the backdrop of positive risk sentiment in global stocks vs softer crude and commodity prices.

- GBP - Sterling has slipped towards the bottom of the G10 ranks, with Cable struggling to keep sight of 1.3300 and Eur/Gbp eyeing 0.8900 after downward revisions to UK services and composite PMIs, but also amidst some re-pricing for zero or negative rates along the Short Sterling strip. However, BoE Governor Bailey may reiterate that NIRP is unlikely to happen anytime soon and MPC member Saunders rounds off this week’s heavy speaker’s schedule tomorrow.

- AUD/NZD/CAD - Also weaker vs their US rival as the Aussie teeters just above 0.7300 in wake of weak trade data hot on the heels of the record Q2 GDP contraction, the Kiwi pivots 0.6750 and Loonie meanders between 1.3100-1.3040 parameters awaiting Canadian trade and Friday’s labour report.

- EUR/CHF/JPY - As noted above, the Euro has gleaned some traction from upgrades to final German PMIs that more than offset misses elsewhere, with Eur/Usd back over 1.1800 and within striking distance of the 21 DMA (1.1835), while the Franc has pared declines from circa 0.9142 even though Swiss CPI came in slightly softer than expected and will likely harden the resolve of the SNB to keep rates negative and actively intervening. Similarly, the Yen is trying to contain losses below 106.00 despite more dovish BoJ commentary overnight and Japanese services and composite PMIs staying sub-50.

- SCANDI/EM - The aforementioned downturn in oil has pushed the Norwegian Crown back under 10.5000 against the Euro and the Yuan is finally succumbing to the Buck’s persistent efforts to recover, but the Lira is underperforming again and sliding to new all time lows following weaker than forecast Turkish inflation and more intense investor anxiety about the nation’s increasingly strained international relations.

In commodities, WTI and Brent front month futures continue to drift lower in early European hours, partly weighed on by the firmer USD, although participants must keep an eye on the supply side of the equation as Gulf of Mexico production comes back online (BSEE estimate 19.9% production shuttered in vs. Prev. 28.4%), whilst comments from Russian Energy Minister Novak yesterday, regarding oil demand at ~90% of pre-pandemic levels and calling on OPEC to take this into account, hinted at a potential proposal of early tapering of the OPEC+ output curbs. Meanwhile, the demand side of the equations continues to eye COVID-19 developments, with the European Centre for Disease Prevention and Control suggesting COVID-19 infections in Europe are "almost back" to March levels. Of course, airline fuel demand will be in focus on this front given the implementation of quarantine rules in the continent, whilst lockdowns are likely to be targeted to specific regions of cluster outbreaks. WTI Oct just below USD 41/bbl (vs. high 41.79/bbl) and Brent Nov under USD 44/bbl (vs. high 44.65/bbl), with the latter approaching USD 43.50/bbl to the downside. Elsewhere, precious metals remain subdued as a function of the Dollar – spot gold found overnight resistance at 1950/oz before trundling lower to ~1925/oz. Spot silver saw losses accelerate after a downwards breach of 27/oz, albeit the metal has since reclaimed the level. In terms of base metals, copper prices eased as disruptions ease in Chile, alongside an overall downbeat performance in China.

US Event Calendar:

- 7:30am: Challenger Job Cuts 115.762K, vs 262.649K last

- 8:30am: Nonfarm Productivity, est. 7.5%, prior 7.3%; Unit Labor Costs, est. 12.0%, prior 12.2%

- 8:30am: Initial Jobless Claims, est. 950,000, prior 1.01m; Continuing Claims, est. 14m, prior 14.5m

- 8:30am: Trade Balance, est. $58.0b deficit, prior $50.7b deficit

- 9:45am: Markit US Services PMI, est. 54.7, prior 54.8; Markit US Composite PMI, prior 54.7

- 10am: ISM Services Index, est. 57, prior 58.1

DB's Jim Reid concludes the overnight wrap

On the subject of vaccines there are a few questions on this in our monthly survey. We’ve been very happy with the number of responses (very many thanks) so far and as a result we are going to close it a day early this lunchtime. So last few hours to fill it in. Link is here. Results hopefully tomorrow once we count all the ballots up!!

It’s a landmark day at home as my daughter Maisie migrates from nursery to school today and the twin boys start their first day at nursery at the same school. So cue lots of tears from everyone apart from me. Although I was a little upset to find that nursery didn’t have a boarding option. We plan to take a group photo in uniform at our front door this morning. I suspect there is no chance of them 1) all looking at the camera, 2) all smiling and 3) not fighting. However we may as well make the photos as authentic as possible. The twins do absolutely everything together (including wild fighting) but they are being separated into two classes today so goodness knows how that will turn out. Not our problem. We’ll just leave them at the gates and run.

Even if today is the first day of school for many, global equity markets have been at the top of the class this month already. US equities again hit fresh highs, with the S&P 500 jumping +1.54% as the index remains on track to close higher for the 9th week out of the last 10. It was the largest one day gain for the index since July 6th. The Dow Jones (+1.59%) hit a post-pandemic high as well, though unusually tech stocks lagged behind as the NASDAQ ‘only’ rose +0.98%. 22 of 24 S&P industries were higher with Autos and Utilities up over +3%, while Tech Hardware fell back -1.37% as Apple (-2.07%) retreated after rallying over +7% following its stock split back on Monday.

In Europe the moves were even stronger, with the STOXX 600 up +1.66%, though banks struggled (-0.65%) as bond yields took a sharp turn lower. The DAX (+2.07%) was another to reach a post-pandemic high, though it fell just -0.04% shy of being in positive territory on a YTD basis. Staying with Europe, a reminder that on Tuesday, 8 September at 2pm BST/3pm CET/9am ET, DB’s Mark Wall will be hosting a conversation with Peter Praet, Former Executive Board Member and Chief Economist of the ECB (2011-2019) on ECB policy through the pandemic and beyond. To register for the event, please click here.

Back now to those moves in fixed income yesterday. Yields on 10yr bunds (-5.3bps), OATs (-6.1bps) and BTPs (-6.3bps) fell throughout the session. Even in the US, where Treasury yields had climbed at the start of the day, they finished -1.6bps lower at 0.653%. Elsewhere, it was a pretty mixed performance for other safe havens, with the dollar index (+0.38%) strengthening for a second day running, whilst gold (-1.38%) and silver (-2.36%) saw noticeable falls. The stronger dollar weighed on oil as well, as WTI (-2.92%) and Brent (-2.52%) fell. The other factor pushing crude lower was news of OPEC+ beginning to taper cuts.

Overnight in Asia markets are mostly higher with the Nikkei (+1.31%) and Kospi (+1.41%) both posting strong advances while the Asx is up a more modest +0.77%. The Hang Seng -0.31% and Shanghai Comp -0.06% are down though. In FX, most G-10 and emerging market currencies are trading weak against the US dollar this morning with the euro down -0.35% to 1.1814. Futures on the S&P 500 are -0.08% this morning while yields on 10y USTs are back up +1.2bps.

Looking forward, attention today will turn to the release of the services and composite PMIs from around the world. Overnight we’ve already had the numbers in from Japan/China/Australia, which showed China’s Caixin services PMI stabilising at 54.0 (vs. 54.1 last month and 53.9 expected) while the composite reading moved up to 55.1 (vs. 54.5 last month). Japan’s final services PMI printed in line with the flash at 45.0 while the composite stood at 45.2 (vs. 44.9 in flash). Lastly Australia’s services reading was confirmed at 49.0 (vs. 48.1 in flash). So certainly no nasty data surprises in Asia as we head into European PMIs.

In other overnight news, the US State Department said in a statement that Chinese diplomats in the US will now face new limits on travel and meetings in the US. Under the new rules, senior Chinese diplomats must get approval to visit university campuses or meet with local officials and any Chinese-hosted cultural events outside of consular posts will need approval if the audience is larger than 50 people. The statement also added that the State Department will require that Chinese diplomatic social media accounts are identified as government-controlled. The moves are aimed at matching Communist Party restrictions on American diplomats and impose costs for what it calls unfair treatment.

On the coronavirus, Dr Fauci warned yesterday that the Labor Day holiday coming up could lead to a rise in cases as other summer holidays have in the US. Cases are currently rising at a rate of 290,000 per week in the US, the lowest since just before the July 4th holiday weekend in the states. While new cases are declining in the summer hot spots like Texas, Florida, and Arizona the concern has shifted to states that were less affected in both the first (Northeast) and second waves such as Iowa and the Dakotas, which have seen sharp rises over the past 2 weeks. Back to the topic of vaccines, the CDC in the US told health officials in all 50 states that they should be ready to distribute a vaccine by November 1 to at-risk individuals including healthcare workers and the elderly. As outlined in the vaccine piece linked above, the timeline puts a potential rollout right before the US election and already over 75% of Americans believe the approval process is driven by politics (according to a Stat/Harris poll). This could hamper the initial uptake and politicise it as discussed in our piece.

In the UK, the government had to step back from easing restrictions in some areas of northwest England after pushback from local leaders. On the continent, France reported over 7000 cases in the last day and along with Spain are now seeing more confirmed cases on a weekly basis than they did during their original outbreaks. Hospitalisations continue to lag as countries continue to cite younger populations as being infected in larger quantities. There is also a matter of greater testing, but the increasing numbers before the weather gets cold will mean the probability of some form of restrictions returning in the next few months is high. The question for governments remain how to balance restrictions with the economic impacts.

Ahead of tomorrow’s US jobs report, the ADP’s private payrolls report showed that firms added +428k jobs, which was beneath the +1m reading expected. However as our US economists wrote last week, given their miss last month, this release may be discounted somewhat. As a reminder, their forecast is still for a +1.2m increase in nonfarm payrolls tomorrow. In terms of other data out yesterday, US factory orders in July were up +6.4% (vs. +6.1% expected), though German retail sales in July unexpected fell by -0.9% (vs. +0.5% expected).

Overnight, Fed’s Daly became the latest official to speak on the need for fiscal stimulus in the US. She said “at this point more fiscal would be appropriate” and added if support isn't restored to its previous levels, it could be a "headwind" to growth with a "disproportionate" effect on those who are struggling the most. She also said, “I think there’s more to do in that Main Street lending program, and we’re actively trying to do it”. On the other hand, Senate Majority Leader Mitch McConnell raised concerns over whether the Congress can get a deal at all after lawmakers return to Capitol post a month long recess. He said, “I don’t know if there will be another package in the next few weeks or not,” while adding that talks between top administration officials and House Speaker Nancy Pelosi haven’t been fruitful, and that any embrace of bipartisanship in the Capitol has “descended” as the elections near.

Here in the UK we actually had a number of headlines yesterday, including an array of Bank of England speakers. On the possibility of further stimulus, Deputy Governor Ramsden said that the BoE had “headroom to do materially more QE if we need to add to it”, though Governor Bailey also said that the BoE’s “best guess” was that inflation probably wouldn’t go negative, since the pass-through of the VAT cut was less than anticipated. Meanwhile on the UK-EU trade negotiations, the EU’s chief negotiator Michel Barnier gave a speech yesterday in which he criticised the UK’s stance on multiple points. He said that “the UK has refused to engage on credible guarantees for open and fair competition”, that they have “not shown any willingness to seek compromises on fisheries”, and that “the UK has been extremely reluctant to include any meaningful horizontal dispute settlement mechanisms in our future agreement”. We’ll likely get some more headlines on this front next week when the next negotiating round takes place in London.

To the day ahead now, and the aforementioned services and composite PMIs from around the world are likely to be the main data highlight, along with the ISM services index from the US. Otherwise, there’s Euro Area retail sales for July, as well as the weekly initial jobless claims and the July trade balance from the US. Central bank speakers today include BoE Governor Bailey as well as Deputy Governor Ramsden, along with the ECB’s Schnabel and the Fed’s Evans.

Government

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Government

Low Iron Levels In Blood Could Trigger Long COVID: Study

Low Iron Levels In Blood Could Trigger Long COVID: Study

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate…

Share this:

{kind=link}

{kind=link}

Authored by Amie Dahnke via The Epoch Times (emphasis ours),

People with inadequate iron levels in their blood due to a COVID-19 infection could be at greater risk of long COVID.

{kind=link}

A new study indicates that problems with iron levels in the bloodstream likely trigger chronic inflammation and other conditions associated with the post-COVID phenomenon. The findings, published on March 1 in Nature Immunology, could offer new ways to treat or prevent the condition.

Long COVID Patients Have Low Iron Levels

Researchers at the University of Cambridge pinpointed low iron as a potential link to long-COVID symptoms thanks to a study they initiated shortly after the start of the pandemic. They recruited people who tested positive for the virus to provide blood samples for analysis over a year, which allowed the researchers to look for post-infection changes in the blood. The researchers looked at 214 samples and found that 45 percent of patients reported symptoms of long COVID that lasted between three and 10 months.

In analyzing the blood samples, the research team noticed that people experiencing long COVID had low iron levels, contributing to anemia and low red blood cell production, just two weeks after they were diagnosed with COVID-19. This was true for patients regardless of age, sex, or the initial severity of their infection.

According to one of the study co-authors, the removal of iron from the bloodstream is a natural process and defense mechanism of the body.

But it can jeopardize a person’s recovery.

“When the body has an infection, it responds by removing iron from the bloodstream. This protects us from potentially lethal bacteria that capture the iron in the bloodstream and grow rapidly. It’s an evolutionary response that redistributes iron in the body, and the blood plasma becomes an iron desert,” University of Oxford professor Hal Drakesmith said in a press release. “However, if this goes on for a long time, there is less iron for red blood cells, so oxygen is transported less efficiently affecting metabolism and energy production, and for white blood cells, which need iron to work properly. The protective mechanism ends up becoming a problem.”

The research team believes that consistently low iron levels could explain why individuals with long COVID continue to experience fatigue and difficulty exercising. As such, the researchers suggested iron supplementation to help regulate and prevent the often debilitating symptoms associated with long COVID.

“It isn’t necessarily the case that individuals don’t have enough iron in their body, it’s just that it’s trapped in the wrong place,” Aimee Hanson, a postdoctoral researcher at the University of Cambridge who worked on the study, said in the press release. “What we need is a way to remobilize the iron and pull it back into the bloodstream, where it becomes more useful to the red blood cells.”

The research team pointed out that iron supplementation isn’t always straightforward. Achieving the right level of iron varies from person to person. Too much iron can cause stomach issues, ranging from constipation, nausea, and abdominal pain to gastritis and gastric lesions.

1 in 5 Still Affected by Long COVID

COVID-19 has affected nearly 40 percent of Americans, with one in five of those still suffering from symptoms of long COVID, according to the U.S. Centers for Disease Control and Prevention (CDC). Long COVID is marked by health issues that continue at least four weeks after an individual was initially diagnosed with COVID-19. Symptoms can last for days, weeks, months, or years and may include fatigue, cough or chest pain, headache, brain fog, depression or anxiety, digestive issues, and joint or muscle pain.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

When Military Rule Supplants Democracy

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

Walmart joins Costco in sharing key pricing news

Angry Shouting Aside, Here’s What Biden Is Running On

Are Voters Recoiling Against Disorder?

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex