S&P Futures Hit Record High Above 3,800 Ahead Of Dismal Payrolls Report

S&P Futures Hit Record High Above 3,800 Ahead Of Dismal Payrolls Report

While there is broad consensus that today’s payrolls report will be ugly, with economists expecting a sharp slowdown in December job growth in the U.S. due to the…

S&P Futures Hit Record High Above 3,800 Ahead Of Dismal Payrolls Report

While there is broad consensus that today's payrolls report will be ugly, with economists expecting a sharp slowdown in December job growth in the U.S. due to the second wave of covid lockdowns and a quarter of those surveyed (including Goldman) predicting a negative print when the data is published at 8:30 a.m. ET, that did not dent the euphoric sentiment unleashed with the Democrats' blue wave victory in Georgia, and as traders walked into their basement offices on Friday the Emini was trading up 13 pts ot 0.3%, to 3,808 having hit a record high of 3,817.75 earlier. The dollar erased gains and 10-year Treasury yields were flat.

Among individual stocks, hedge fund hotel Sarepta sank 46% in premarket trading after a trial for its gene therapy missed investor expectations. Micron Technology Inc rose 4.5% after the chipmaker forecast second-quarter revenue above estimates as a global shift to remote work and a recent uptick in 5G smartphone adoption drove demand for its chips. U.S.-listed shares of Baidu Inc jumped 5.2% on plans to form a company to make smart electric vehicles, according to two sources familiar with the matter.

Late on Thursday, President Trump finally conceded and pledged to pursue a smooth transition of power and condemned the earlier unrest at the Capitol. Trump is under siege from some Republicans as well as Democrats and from inside his own administration as top officials announce resignations.

The Dow and the Nasdaq are on track for fourth straight weekly gains even as Democrats on Friday weighed impeaching President Donald Trump for a second time. While normally a dismal jobs report would be risk negative, today it is the other way around with investors betting Democrat control of the Senate will give President-elect Joe Biden greater power to battle the economic slowdown spurred by the pandemic, including with stimulus checks.

“A unified government as the result of the ‘blue sweep’ victory will smooth the path to more fiscal stimulus,” said Mark Haefele, chief investment officer of UBS Global Wealth Management. “This points to the reflation trade remaining intact, which we think has further to run.”

The situation is “close to ideal” for stocks, as a lack of a strong majority will also make it difficult for Democrats to implement tax rises, according to Alexandre Tavazzi, global strategist at Pictet Wealth Management.

The euphoria was global with European stocks headed for their best week since November, led higher by tech shares which were boosted by earnings reports from U.S. and Asia chipmakers. Banks slumped, with Credit Suisse Group AG and Commerzbank AG among the biggest laggards. European stocks are on track to start 2021 with their biggest weekly gain for almost two months as investors predict government stimulus and coronavirus vaccination programs will drive an economic rebound. The Stoxx Europe 600 Index added 0.6%, taking the week’s rise to 3%. Technology and consumer discretionary were among the best performers on Friday, with the former boosted by earnings reports from U.S. and Asia chip bellwethers. Consumer staples and communications underperformed, while energy stocks were steady as oil edged up after Saudi Arabia’s unilateral output cut eased over-supply fears.

A gauge of Asia-Pacific equities jumped the most in about two months: Asian stocks climbed to new highs on the familiar hopes for U.S. stimulus and investor demand for shares tied to electric vehicles and semiconductors. Shares of EV-related companies gained after Tesla jumped to a fresh record. Hyundai Motor surged 19% even as it backed away from a statement confirming it’s in talks with Apple Inc. on developing self-driving car. In Hong Kong, Geely Automobile jumped 20% after the company is said to form an EV tie-up with Baidu. South Korea’s Kospi climbed 4%, the most among Asian benchmarks, powered by gains in Hyundai and Samsung Electronics, which rose after reporting results. Key equity gauges rose more than 1% in markets including Japan, Hong Kong, Taiwan, Singapore, Malaysia, the Philippines and Indonesia,

The MSCI gauge of emerging-market stocks headed for its highest ever close, surpassing levels seen before the 2008 global financial crisis. Technology stocks continued to lead the advance even as MSCI said it will remove China’s three major telecommunications companies from its indexes on Friday. The ruble fell most among currencies as traders returned from holidays in Russia with the Turkish lira also paring a fourth straight week of gains. South Africa’s rand rose from recent declines that were fueled by spiraling coronavirus cases.

On the virus front, more U.S. states reported their first cases of the variant that helped trigger a U.K. lockdown amid concern that Covid-19 deaths in the U.S. are likely to maintain a near-record pace at least through January. Mounting hospitalizations are offsetting any positive effect from the halting start to inoculations.

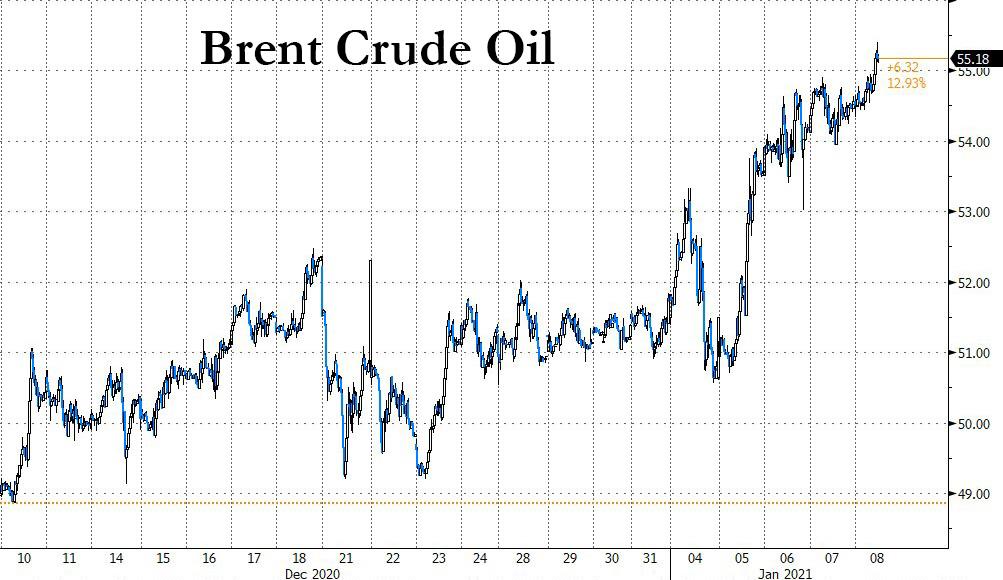

Elsewhere, Brent oil topped $55 a barrel sending energy stocks higher, while gold dipped.

Bitcoin did not follow gold, and again jumped to a record.

In FX, the Bloomberg Dollar Index was little changed at 1120.62; the pound outperformed Group-of-10 peers, rising 0.2% to $1.36. “The U.S. payrolls report might be viewed as a potential litmus test for U.S. dollar bears,” TD Securities strategists including Jim O’Sullivan wrote in a note on Thursday. “Positioning is stretched and the backup in U.S. yields has some investors nervous.”

In rates, the yield on 10-year U.S. Treasuries was steady at 1.08%, after rising as much as 2bps to 1.10%, the highest since March. Yields are within a basis point of Thursday’s closing levels with 10-year around 1.085%, broadly in line with bunds and gilts during European session. Gains for Asia bourses and U.S. stock index futures weighed and regional dip-buyers remained sidelined. Supply will be in sharper focus after 8:30am ET jobs data, with 3-, 10-, 30-year auction cycle starting Monday.

To the day ahead now, the main highlight will likely be the aforementioned US jobs report. Other data releases from Europe include November’s industrial production readings from France and Germany, along with the Euro Area’s unemployment rate in November. Finally from central banks, we’ll hear from Fed Vice Chair Clarida.

Market Snapshot

S&P 500 futures up 0.3% to 3,807.25

STOXX Europe 600 up 0.5% to 410.48

German 10Y yield fell 0.3 bps to -0.525%

Euro down 0.3% to $1.2231

Italian 10Y yield fell 0.9 bps to 0.447%

Spanish 10Y yield fell 1.9 bps to 0.025%

MXAP up 1.7% to 207.33

MXAPJ up 1.7% to 691.30

Nikkei up 2.4% to 28,139.03

Topix up 1.6% to 1,854.94

Hang Seng Index up 1.2% to 27,878.22

Shanghai Composite down 0.2% to 3,570.11

Sensex up 1.4% to 48,749.73

Australia S&P/ASX 200 up 0.7% to 6,757.87

Kospi up 4% to 3,152.18

Brent futures up 0.9% to $54.89/bbl

Gold spot down 1.2% to $1,890.36

U.S. Dollar Index up 0.2% to 89.98

Top Overnight News from Bloomberg

President Donald Trump, in a video message on Thursday night, condemned the storming of the U.S. Capitol -- which occurred after he urged his angry supporters to take action -- and said he would prepare for the administration of President-elect Joe Biden.

The rapidly growing calls among Democrats to oust President Donald Trump either by his own cabinet taking action or by another impeachment is running quickly up against the limits of time and Republican Party politics.

The vaccine developed by Pfizer Inc. and BioNTech SE may offer some protection against a mutation in the new fast-spreading variants of the coronavirus that have emerged from the U.K. and South Africa, according to a recent study.

A quick look at global markets courtesy of Newsquawk

Asian equity markets traded mostly positive on momentum from the fresh all-time highs on Wall St where the Nasdaq led the advances as large-cap tech names clawed back losses after the dust settled from the blue sweep and with better-than-expected data adding to the constructive mood. ASX 200 (+0.7%) and Nikkei 225 (+2.4%) were higher with outperformance seen in Australia’s tech and financials but with gains in the index capped by weakness in miners and after the Queensland Premier announced a 3-day lockdown in Greater Brisbane due to COVID-19, while Japanese exporters benefitted from favourable currency effects which have offset the headwinds from the State of Emergency declaration for Tokyo and neighbouring prefectures, as well as mixed Household Spending figures. KOSPI (+4.0%) was the biggest gainer with index heavyweight Samsung Electronics underpinned after its preliminary Q4 results in which oper. profit slightly missed expectations at KRW 9.0tln vs exp. KRW 9.1tln but still showed a 25% increase Y/Y and Hyundai Motor shares were in 5th gear with gains of nearly 20% following reports the Co. could partner with Apple for self-driving cars, despite the automaker confirming nothing has been decided yet and that the US tech giant was in discussions with various car manufacturers. Hang Seng (+1.2%) and Shanghai Comp. (-0.2%) were mixed with the mainland faltering after the PBoC’s operations resulted to a net weekly liquidity drain of CNY 505bln and due to ongoing tensions with US after MSCI and FTSE Russell announced to delete the Chinese telco giants from their indexes, while Beijing also warned that Washington will pay a heavy price if it proceeds with an Ambassador visit to Taiwan scheduled for next week. Finally, 10yr JGBs were subdued and languished at the prior day's lows amid gains in stocks and after continued pressure in USTs, with mixed 30yr JGB auction results also keeping price action drab.

Top Asian News

Global Demand for Taiwan Tech Sends Exports to Record High

SoftBank Clashes Again With Moody’s Over Credit Rating

South Korea ‘Comfort Women’ Compensation Verdict Angers Japan

European bourses trade somewhat mixed (Euro Stoxx 50 +0.6%), after opening with gains across the board following a similarly mixed APAC handover. US future meanwhile trade off best levels but remain in modest positive territory ahead of the US labour market report, although it is worth noting that further fiscal support for Americans was rubber-stamped after the payroll survey period, and will therefore not be reflected in the employment situation report (full preview available in the Newsquawk Research Suite). The narrative across the market seems to remain fixated on stimulus anticipation under the incoming Biden administration coupled with mass vaccine rollouts throughout the year in a bid to return to normality. That being said, downside scenarios for stocks prevail in the form of further COVID mutations (possibly rendering vaccines ineffective) and sooner-than-expected unwind of loose policy. Regarding the former, Pfizer said its COVID-19 vaccine appears to be effective against the UK & South African variants of the virus in lab tests. However, other reports noted that study was conducted on blood taken from people who had been given the vaccine and that its findings are limited because it does not look at the full set of mutations found in either of the new variants. Back to Europe, sectors are mostly higher with underperformance seen in financials amid losses in Credit Suisse (see below) and a pullback in yields - also contributing to the underperformance in the FTSE 100 (Unch) on account of its heavy bank exposure alongside unfavourable Sterling dynamics. On the other side of the spectrum, the Tech sector outpaces peers and notably outperforms amid a number of potential factors. 1) Samsung Electronics said its operating profit for the three months that ended in December likely rose 26% - shares closed higher by over 7%, 2) STMicroelectronics (+1.5%) reported net prelim revenue above the prior guidance due to "significantly better than expected market dynamics throughout the quarter", 3) Taiwanese chip-maker TSMC reported an improvement in revenue, 4) Micron beating on top and bottom lines which supported shares after the close. As such, regional chip-makers cheer the wave of bullish updates with Infineon (+6.7%) and ASML (+3.1%) among the top gainers in Europe. In terms of other movers, Credit Suisse (-3%) is pressured as it expects to increase provisions for the MBIA case and other RMBS-related cases by a total of USD 850mln vs prior provisions of USD 300mln. This charge will be reflected in 4Q20 financial results and thus the group is expected to report a net loss in the period. Conversely, Sodexo (+6.5%) sees gains after upping its guidance.

Top European News

EU Secures an Additional 300 Million Pfizer Vaccine Doses

Mercedes Meets CO2 Targets With Year-End Surge in EV Sales

Fiscal Policy Key for Czech Interest-Rate Path, Minutes Show

In FX, the USD has bounced further, with the index now eyeing pre-New Year highs having scaled 90.000 to print a new recovery high at 90.132, so far. It may be just symbolic, but the fact that the Greenback has extended its recovery from 89.206 to break a losing streak is encouraging, and if it can end the week without suffering a major set-back then the omens and technical picture will look even brighter. However, NFP looms and could be more of a wildcard than usual given COVID-19 restrictive measures impacting the labour data, and anecdotal evidence carrying a downside bias to consensus, which could spark a retracement in US Treasury yields alongside curve re-flattening on a big payrolls disappointment. On the flip-side, any Buck retreat may be viewed as another opportunity to cover shorts or take profit on bearish Biden Blue sweep bets.

XAU/CHF/EUR - As noted above, the main victims of the Dollar revival, as Gold finally folded after fending off multiple attempts to take out Usd 1900/oz and then succumbed to a stop-driven collapse when the 100 DMA around Usd 1893 was breached in what some described as a flash crash. Meanwhile, the Franc only found refuge from support into 0.8900 after mixed Swiss unemployment rates and the Euro is trying to regain composure following a slide through 10 and 21 DMAs (1.2256 and 1.2222 respectively) that only came to a halt circa 1.2214.

AUD/NZD/CAD/JPY - All narrowly mixed vs their US counterpart having weathered an early EU storm, with the Aussie gleaning some support from still firm iron ore prices to reclaim 0.7750+ status even though Queensland has been forced into a 3 day lockdown due to a case of the coronavirus. Similarly, the Kiwi has clambered back from the low 0.7200 area, but seems to be facing stronger headwinds via the Aud/Nzd cross that has climbed over 1.0700 again. Elsewhere, the Loonie has rebounded quite firmly from sub-1.2730 levels in the run up to the Canadian-US jobs showdown and the Yen is paring declines from just under 104.00.

GBP - Sterling is ‘outperforming’, though marginally and more on the back of retrenchment rather than anything fundamental or a change in fortunes for the Pound that remains hampered by the Brexit hangover and battle to stop the pandemic in its new and increasingly infectious guise. Hence, Cable has not been able to convincingly regain grip of the 1.3600 handle and Eur/Gbp extend beyond 0.9000.

SCANDI/EM - Simmering oil prices are still a source of power for the Nok, while the Zar has found some much needed support to unwind some recent heavy losses from vaccine approval in SA.

South Africa's Eskom says it has suspended loadshedding as demand has declined ahead of the weekend. (Newswires)

In commodities, WTI and Brent front month futures eke mild gains but trade at session highs, with the former around USD 51.30/bbl and the latter meandering just under USD 55/bbl after briefly topping the level. Oil-specific newsflow remains light but the complex continues to be supported by Saudi's voluntary decision to cut 1mln additional barrels of production in February and March. Looking ahead, prices are likely to eye sentiment alongside COVID-related headlines, namely further lockdowns and travel bans. On the flip side, desks not that the cold weather has previously proved to be bullish for the energy complex, with the cold streak seen in North Asia currently helping to reduce middle distillate stocks in the region, according to ING. Elsewhere precious metals saw a bout of downside in during European trade in what seemed to be technically driven amidst a lack of fresh fundamentals at the time. Spot gold slumped below USD 1900/oz after tripping suspected stops and fell to a current low of ~USD 1877/oz (vs. high 1917/oz) while spot silver similarly relinquished the USD 27/oz handle to a low of almost USD 26/oz. In terms of base metals, Shanghai copper hit levels last seen in over nine years on reflationary play, whilst similar omens were felt by Dalian iron ore futures which rose for a sixth consecutive session as it also gains impetus on firmer demand prospects ahead of the Lunar New Year holiday.

US Event Calendar

8:30am: Change in Nonfarm Payrolls, est. 50,000, prior 245,000

Change in Private Payrolls, est. 13,000, prior 344,000

Unemployment Rate, est. 6.8%, prior 6.7%

Average Hourly Earnings MoM, est. 0.2%, prior 0.3%

Average Hourly Earnings YoY, est. 4.5%, prior 4.4%; Average Weekly Hours All Employees, est. 34.8, prior 34.8

Labor Force Participation Rate, est. 61.5%, prior 61.5%

I attended my first school assembly since 1992 yesterday. Back then it was a rowdy affair as a bunch of rebellious leaving 6th formers tried to play a prank on the whole school which for good taste I won’t go into here. This was a zoom assembly for 5 year olds so the tone was slightly different. The headmistress said one of the most important thing to do was to listen to Mummy and Daddy. That fell on deaf ears. Talking of ears I had to cover home schooling for an hour or so yesterday for the first time as one of the twins was having an operation to fit two grommets in his ears. Hopefully if he can hear more clearly now he won’t be so loud. Fingers crossed.

The only noise in markets yesterday was a bullish stampede as markets continued their strong start to 2021 yesterday as investors brushed off the violence in Washington to look forward to the prospect of more stimulus and less political volatility under a new administration in less than two weeks’ time. Ahead of payrolls today, US equities hit fresh highs, with the S&P 500 (+1.48%), the Dow Jones (+0.69%) and the NASDAQ (+2.56%) all reaching new records. The latter was helped by the large rally in tech, with the biggest highlight being Tesla gaining +7.94% on the day. That means the electric car company’s market cap rose by $56.9bn, or nearly the entire market cap of GM ($62bn) on the day! Meanwhile in fixed income, there was a significant bear-steepening in US Treasuries as attention focused on what united Democratic control in Washington will mean for markets and the economy.

Our US economics team, put out an update to their outlook yesterday (link here ) after the Democratic sweep. They see the new administration passing another stimulus bill of approximately $900bn, built around further stimulus checks, funds for state and local governments, and enhancements to unemployment benefits. They have now lifted their growth forecast for 2021 by about 2 percentage points to 6.3% (Q4/Q4) and lowered the year-end forecast for the US unemployment rate to 4.3% from 5% previously. This would mean that real GDP would return to its pre-virus level in Q2 and converge towards the pre-virus path by year-end. This faster pace to the recovery could also affect the Fed, and the US economic team could see the Fed’s QE tapering by the end of this year. The Fed could begin signaling its tapering intentions during the June FOMC meeting if they are convinced that the vaccine rollout is proceeding well and growth is getting back on track before a gradual taper in December. So a far cry from where we were even a few weeks ago.

This change in sentiment is certainly impacting US fixed income and by the close, yields on 10yr Treasuries had risen +4.4bps to 1.08% (and are up a further +1.8bps overnight), with the bulk of that increase coming from rising inflation expectations, as breakevens rose a further +2.6bps to 2.10%, their highest level since late-2018. In fact they are approaching the top of their 6 year range which is remarkable given all the perceived deflationary forces in the system and the fears over permanent Japanification. There is no Japanification coming if you look at breakevens. Meanwhile the steepening in the curve saw the 2s10s slope rise +4.2bps to a fresh 3-year high, as the 5s30s reached a fresh 4-year high.

A couple of hours after we went to press yesterday, President-elect Biden’s victory was officially certified by the Joint Session of Congress, marking the last formal stage of the election process before inauguration day on January 20. Though President Trump has still not conceded defeat in the election, he issued a statement via an aide which said that in spite of his disagreements over the outcome of the election, “there will be an orderly transition on January 20”. However, there were further resignations in the aftermath of Wednesday’s political turmoil, with Trump’s former chief of staff Mick Mulvaney announcing his resignation as the Special Envoy for Northern Ireland. Transportation Secretary Elaine Chao, who is also the wife of Senate Majority Leader McConnell, became the first member of the cabinet to resign following the events at the Capitol and the President’s remarks. Notably, Facebook also announced that they were extending the block on the President’s Facebook and Instagram accounts indefinitely, and at least until after the inauguration. Speaker Pelosi and Senate Democratic Leader Schumer asked Vice President Pence and the cabinet to remove the President under the 25th amendment, indicating that the House could issue articles of impeachment otherwise. Given that there is less than a fortnight left in the President term, this would be mostly signalling, but an impeached and removed president could be barred from seeking the office again in 2024. Late last night the President released a video message pledging to a smooth transition to the Biden administration and condemning the violence at the Capitol the day before.

Asian markets are following Wall Street’s lead this morning with the Nikkei (+1.89%), Hang Seng (+1.32%) and Kospi (+2.92%) all up. The outperformance of the Kopsi is on the back of news that Hyundai Motor Co. is in talks with Apple Inc. over electric vehicles. Bucking the trend, the Shanghai Comp (-0.62%) is down likely due to MSCI saying that it will remove China’s three major telecommunications companies from its benchmark indexes after the close today thereby giving global funds just one day to adjust billions of dollars of passive investments. Shares of China Unicom are down -7.87% today after being down -11.35% yesterday, while China Mobile and China Telecom have declined by -12.8% and -16.5% over the last two days. Meanwhile, futures on the S&P and Nasdaq are up +0.49% and +0.32% respectively.

Risk assets outside the US also performed strongly throughout yesterday’s session, with the STOXX 600 rising +0.51% to hit its own post-pandemic high, while the German DAX (+0.55%) rose to a new all-time high but note it is a total return index. Brent crude (+0.15%) and WTI (+0.40%) oil prices reached their highest levels since the pandemic began, at $54.38/bbl and $50.83/bbl respectively, on the back of rising optimism over future economic demand. They are up similar amounts overnight. Over in sovereign bond markets, yields on ten-year bunds (-0.2bps) saw little movement and are in a different world to Treasuries at the moment, though there was a further narrowing in spreads, with the gap between Italian ten-year yields and bunds tightening to a fresh 4-year low of 1.08%, as the Greek spread fell to its lowest in over a decade, at 1.1%. The European five-year, five-year inflation swap rate rose +1.8bps to 1.32%, which is the highest level since January 20, 2020, just prior to the pandemic. Finally bitcoin rose above $40,000 intraday before settling at $39,733 – a new all-time high. It is trading at $38,340 this morning bringing its YTD gains to +32.22% after just a single week.

On the coronavirus, a state of emergency was declared for the Tokyo area by the Japanese PM as the number of cases continued to rise in the capital. It’ll be in place until February 2, with restaurants having to close by 8pm. Meanwhile in China, the city of Shijiazhuang was locked down, and people and vehicles banned from leaving, after more than 90 confirmed cases of the virus were reported since January 2nd. There was also news that China’s Sinovac vaccine was shown to be 78% effective in a late-stage Brazilian trial, offering more optimism for developing markets. In Europe, France announced that the government plans to extend aid to companies in sectors most affected by the pandemic as the lockdowns in the country are set to continue, but there was no indication of the exact level of fiscal support. Meanwhile, the UK has said overnight that it will require all international passengers to prove they do not have coronavirus and show a negative test result within 72 hours of the start of their journey while travellers arriving from countries that are not on the government’s open travel corridor list will be required to isolate at home for 10 days, regardless of their test results. Elsewhere Portugal’s Prime Minister Costa announced that restrictions may be tightened next week at a press conference yesterday after a record one day rise in cases on Wednesday. In the US, Connecticut, Pennsylvania and Texas all reported cases of the new more virulent strain of the virus – making it eight states so far. Overnight, there was more positive news on the vaccine front as a study by Pfizer and the University of Texas Medical Branch showed that Pfizer/BioNTech’s vaccine possibly works against a key mutation of the highly transmissible variants of the coronavirus discovered in the U.K. and South Africa.

Attention today will remain on the US thanks to the release of the December jobs report, which coincides with further rises in coronavirus cases throughout the country. In terms of what to expect, DB’s US economists are looking for nonfarm payrolls to grow by just +50k, in line with the consensus. That would be the slowest pace of monthly job growth since the massive -20.787m decline back in April, and they think that should see the unemployment rate tick up a tenth to 6.8%, which would be the first time its risen since April, marking an end to the labour market progress there’s been since the recovery from the pandemic began back in May. The jobs report later comes after yesterday’s ISM services index from the US, which rose to 57.2 (vs. 54.5 expected) in December. However, the employment index fell back to 48.2, its lowest since August.

To the day ahead now, and the main highlight will likely be the aforementioned US jobs report. Other data releases from Europe include November’s industrial production readings from France and Germany, along with the Euro Area’s unemployment rate in November. Finally from central banks, we’ll hear from Fed Vice Chair Clarida.dd

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}