Uncategorized

Sam Bankman-Fried trial [Day 17] — latest update: Live coverage

The former FTX CEO faces seven counts of conspiracy and fraud. A New York court will decide his fate.

Cointelegraph reporters are on…

Share this:

The former FTX CEO faces seven counts of conspiracy and fraud. A New York court will decide his fate.

Cointelegraph reporters are on the ground in New York bringing you live coverage of the trial of former FTX CEO Sam “SBF” Bankman-Fried. As the saga unfolds, check below for the latest SBF updates.

Nov. 2: Prosecution makes closing arguments, jurors request dinner and transportation

The month-long trial of Sam Bankman-Fried is nearing its end after Assistant Attorney Danielle Sassoon laid out the government's closing arguments against the former FTX executive.

Sassoon told the New York court that prosecutors "met the burden" of proving Bankman-Fried's guilt related to seven counts of fraud and conspiracy to commit fraud. She said the prosecution exposed Bankman-Fried's lies and false impressions, including misleading FTX customers about the safety of their funds.

Sassoon described Bankman-Fried as an ambitious executive who even had his eye on the White House, and "lied to get customers' trust." In addition, he used customer funds as his own personal "piggy bank."

The Assistant Attorney said the failings of former FTX executives, including Caroline Ellison, Gary Wang and Nishad Sign, couldn't be separated from Bankman-Fried. "They were acting at the defendant's direction," she said.

U.S. Southern District of New York Judge Lewis Kaplan briefed the 12-person jury Thursday afternoon as they began deliberations. He explained that charges related to defrauding FTX customers and using interstate wires to defraud lenders were substantive, meaning the alleged crimes do not depend on one another.

They've back.

— Inner City Press (@innercitypress) November 2, 2023

Judge Kaplan: The jurors have said they want dinner and transportation.

[A beat]

Judge Kaplan: No one in hear wants to ask for a car?

[Laughter]

Judge Kaplan: It seems that the evidence thumb drive does not have the whole "all-hands" meeting

Shortly after 4:00 p.m. ET (8;00 p.m. UTC), Judge Kaplan confirmed that the jurors had requested dinner and transportation, meaning that more deliberations were expected. Jury deliberations may last until Monday.

Nov. 1: US attorneys deliver closing arguments at the SBF trial

Sam “SBF” Bankman-Fried’s trial has entered the final stages, with the prosecution delivering its closing arguments in the case on Nov. 1.

“That’s fraud. It’s stealing, plain and simple. Before FTX, there was Alameda,” Assistant United States Attorney Nicolas Roos reportedly told jurors, presenting one of the many charts the government used as evidence.

The former CEO of FTX is facing seven counts of fraud and conspiracy to commit fraud. Bankman-Fried could serve up to 115 years in prison if convicted. A jury of 12 will decide his fate in the coming days.

Bankman-Fried’s defense faces a tough challenge in persuading jurors that he is innocent of the charges, as the government presented extensive evidence, including testimony from officials and law enforcement agents involved in the case. Check out the full story here.

Oct. 31: Trial heads toward closing remarks

Bankman-Fried resumed his testimony on Oct. 31, with prosecutor Danielle Sassoon of the Southern District of New York asking the former FTX CEO about whether he believed it was permissible to spend $8 billion in customer deposits.

"I thought it was folded into risk management,” he reportedly said. “As CEO of Alameda, I was concerned with their portfolio. At FTX, I was paying attention but not as much as I should have been.“

“You said it [regulations] was P.R. [public relations]?” Sassoon reportedly asked. Bankman-Fried responded: “I said something like that.”

Lead defense attorney Mark Cohen’s request to have Bankman-Fried acquitted was denied by Judge Lewis Kaplan, opening the door for closing arguments to be heard on Nov. 1. Neither the defense nor the prosecution intend to call any additional witnesses.

Oct. 30: “Fuck regulators,” said SBF behind closed doors

Despite publicly supporting drafting crypto regulation to protect customers, Bankman-Fried appears to have shared a deep disdain for regulators.

During SBF’s ongoing criminal trial, Assistant U.S. Prosecutor Danielle Sassoon inquired if the crypto executive could recall his previous Twitter statements regarding his support of blockchain regulation to protect customers. “I don’t remember,” SBF said. Sassoon asked, “But in private, you said, fuck regulators, right?”

“I said that once,” SBF replied. Among other profanities, the former crypto executive also stated that he viewed a “subset of people” on Crypto Twitter as “dumb motherfuckers.” Before his arrest, SBF testified in a 2021 hearing before the U.S. House Financial Services Committee on crypto regulation.

“You said it [regulations] was P.R. [public relations]?” asked Sassoon. SBF responded, “I said something like that.”

During additional questioning, SBF also claimed that the benefits of helping draft crypto regulation included assisting in FTX taking market share from competitor exchange Binance. Before FTX’s collapse last November, SBF revealed that the exchange, along with sister hedge fund Alameda Research, held close to $15 billion in customers’ deposits, with $10 billion reported missing.

On Nov. 8, 2022, Binance founder Changpeng Zhao signed a letter of intent to acquire FTX. The deal fell apart just a day later after Binance reportedly viewed FTX’s books and discovered the asset discrepancy. SBF recalled that on Nov. 7, 2022, customer net withdrawals amounted to $4 billion, or 100 times the volume of an average trading day, sending the company into a deep liquidity crisis.

Oct. 27: Bankman-Fried faces jurors

Bankman-Fried recognized that a “lot of people got hurt” due to FTX’s collapse but denied any wrongdoing in the exchange’s relationship with Alameda Research.

“I made a number of small mistakes and a number of big mistakes,” he told jurors in the first minutes of his testimony on Oct. 27. Jurors are listening to Bankman-Fried’s testimony for the first time. A hearing was held with him on Oct. 26 without the jurors present.

Compared with the previous day, Bankman-Fried appeared to be much better prepared for questions this morning. He delivered the jurors a narrative of FTX’s inception, its first months in business and its relationship with Alameda. According to him, Alameda was the primary market maker and liquidity provider of FTX, which meant it would be responsible for covering customer losses if FTX’s risk engine failed.

Due to Alameda’s role in FTX, it received customized features in FTX code, such as the ability to go negative without activating the risk engine. The exemption, according to him, was necessary to avoid Alameda’s potential liquidation, which would have an adverse impact on the crypto markets.

Bankman-Fried also noted that as a customer and liquidity provider for FTX, Alameda was able to borrow funds from the exchange if collateral was provided. As per FTX’s terms of use, borrowers would not have any restrictions on using borrowed funds, meaning Alameda could use the funds for trading purposes.

FTX’s former CEO also noted that Alameda handled wire transactions on behalf of FTX, acting as a payment processor for the platform.

In response to a question regarding whether he knew how FTX’s customer deposits on Alameda’s account were traced, he replied, “I wish I had a better understanding than I did.”

Bankman-Fried also pointed out that the exchange’s terms of use had a provision regarding the clawback of funds. According to the document, margin trading and futures would fall under the provision stating:

"Your account balance may be subject to claw back due to losses suffered by other users.”

The provision was intended to ensure that if FTX was unable to cover losses related to spot margin and futures, damages could be shared among all customers.

Overall, his testimony argued that the company’s relationship was protected by legal documents, though mistakes were made during the bull market’s speedy expansion. Bankman-Fried will continue to be examined by the defense, followed by a cross-examination by the prosecution.

Oct. 26: Prosecutors rest their case

Attendees of Sam Bankman-Fried’s trial on Oct. 26 had a disappointing morning as attorneys from both sides kept an endless cycle of repeated questions, sidebars and objections, prompting District Court Judge Kaplan to interrupt witness testimony and urge attorneys to move forward.

Prosecutors rested their case early this morning after FBI Agent Mark Troiano briefly testified as the last government witness. In his analysis, more than 300 Signal groups with Bankman-Fried were examined. Most of these groups had enabled the auto-delete feature, which deletes messages after a specified period.

Following a short break, the defense called as a witness Bahamas attorney Krystal Rolle, who represented Bankman-Fried and FTX in November 2022. Rolle said that she was part of a group that met with the Securities Commission of the Bahamas on Nov. 12 related to the collapse of FTX.

Although her testimony did not offer much new information, she shared with the jury that FTX transferred all digital assets held in its custody to the Bahamas regulator the same day a court order was issued.

Joseph Pimbley, a financial consultant with a Ph.D. in physics, was the second witness presented by the defense. His work on the case included an analysis of FTX’s code and database.

According to Pimbley’s findings, in November last year, FTX had over $5.8 billion in assets from accounts with spot margin, lending or futures trading enabled. The amount does not include balances of FTX entities or Alameda Research. During the cross-examination, prosecutors pointed out that the FTX database did not accurately reflect its bank accounts at that time.

Oct. 19: Former FTX legal counsel presents spreadsheet used to track $2.1 billion in loans to SBF, other execs

FTX’s former general counsel Can Sun was unaware of the exchange’s commingling of funds with Alameda Research, he told jurors on Oct. 19 as part of his testimony in Sam Bankman-Fried’s criminal trial.

Sun said he learned about Alameda’s exemption from the liquidation engine system from other employees in August 2022. Normally, the system would liquidate loss-making trades, but Alameda reportedly bypassed the mechanism due to its exception.

Upon learning about the problem, Sun allegedly worked on a plan to fix the issue. The plan would include a delay-liquidation mechanism to replace the non-exemption on Alameda’s account. According to the plan, the delayed mechanism would later be applied to other market makers on FTX, which also sought to notify customers and regulators about the issue. According to San, the plan was stalled by other FTX departments and was never implemented.

Furthermore, Sun acknowledged that he relied on Bankman-Fried’s statements about segregating customer funds to develop the company’s terms of service and answer regulators’ inquiries. FTX’s terms of services said that “none of the Digital Assets in your account are the property of, or shall or may be loaned to, FTX Trading” — in opposition to what was apparently happening between the sister companies. The same terms would apply to fiat assets, Sun noted in his testimony.

Additionally, the former FTX attorney disclosed a spreadsheet he used to trace loans made by Alameda to Bankman-Fried, Gary Wang, Ryan Salame and Nishad Singh. According to the spreadsheet, Alameda loaned them $2.1 billion across 35 loans.

These loans were used to fund other venture investments by FTX. While this process wasn’t the most transparent way of carrying out investments, it was a legal option at the time, Sun said.

According to prosecutors, the spreadsheet did not include millions of dollars transferred to Salame and Bankman-Fried. Sun said he was unaware of the additional transactions.

Sun traveled from Japan to testify in court as part of his non-prosecution agreement with the Department of Justice.

The trial of Bankman-Fried will resume on Oct. 26. The prosecution expects to rest its case on that date. The defense counsel has not yet confirmed whether a case will be brought.

Oct. 18: “Lawyers should do better than this” — Judge Kaplan

District Judge Lewis Kaplan ran out of patience during Sam Bankman-Fried’s trial on Oct. 18, calling out on lawyers representing both parties in the criminal court case. The judge’s comments came after a witness fleeing Texas for the trial testified for roughly 15 minutes.

Cory Gaddis, a policy specialist at Google, spent over three hours flying only to confirm that Google’s metadata indicates Caroline Ellison and Bankman-Fried owned a fabricated balance sheet of Alameda Research. According to Ellison’s testimony from last week, she developed seven alternative spreadsheets to mislead Alameda’s lenders about its financial health in 2022.

In cross-examination, Bankman-Fried’s defense counsel ended Gaddis’ testimony at the third question after realizing he wasn’t a technical expert.

“Lawyers should do better than this,” Judge Kaplan said, complaining about prosecutors and the defense counsel’s witness strategies.

For example, in the morning, former FTX lobbyist Eliora Kats took a short test just to confirm FTX had publicly advocated in Washington, D.C. for crypto regulation, which was already public knowledge, noted Judge Kaplan.

“These people [jurors] are giving up weeks of their lives, and I care about it,” he noted.

Prosecutors are expected to rest their case on Oct. 25. The defense counsel has not yet confirmed it hasa case.

Oct. 18: Forensic analysis of Alameda and FTX accounts

Accounting professor Peter Easton provided a breakdown of the alleged commingling of funds between FTX and Alameda Research since 2021. Easton is an accounting specialist working on forensic financial analysis and testified on Oct. 18 at the Southern District Court of New York as part of Bankman-Fried’s criminal trial.

According to Easton’s analysis, Alameda invested in Genesis Capital, K5 Global Holdings, Anthropic PBC, Dave Inc, Modulo Capital and other ventures, partially using funds from FTX customers. In June 2022, Alameda had a negative balance of $11.3 billion with FTX, while the companies’ liquid assets stood at $2.3 billion, meaning a gap of $9 billion between the sister firms.

Another critical point from the analysis: Alameda has 57 accounts with FTX that could have negative balances, whereas no other customer could do so. The analysis challenges Bankman-Fried’s defense argument that Alameda had similar privileges as other market makers on FTX.

Another finding of the analysis is that Alameda repaid $6.6 billion in loans to crypto lenders during the bear market in 2022. Of these funds, 68% ($4.5 billion) were traced as customer assets, while 32% ($2.1 billion) came from its own funds.

At least 35 properties in the Bahamas were purchased with customer funds totaling $228.5 million, according to Easton.

Oct. 13: BlockFi would not have filed for bankruptcy without the FTX debacle

The BlockFi team warned its leadership about the crypto lender’s over-exposure to FTX Token (FTT) in August 2021, according to evidence presented in court on Oct. 13 during Sam Bankman-Fried’s trial.

A credit memo prepared by BlockFi’s team in August 2021 recommended against a loan of 10,000 Bitcoin (BTC) to Alameda Research, worth nearly $470 million at the time.

Zac Prince, founder and former CEO of BlockFi, said the loan was denied, but Alameda increased its borrowings with BlockFi in the following months, reaching $1 billion in the second quarter of 2022. Prince testified that Alameda had always paid its loans on time until the collapse of FTX in November 2022, and that the loans had always been overcollateralized. He was unfamiliar with the fact that Alameda was paying the loans using funds from FTX customers.

One of the stress scenarios presented by BlockFi’s team in 2021 observed that if Alameda entered into default, with all lenders calling for repayment at the same time, the price of FTT would drop 60% to 75% in a day (or more).

Another stress evaluation during the same period noted that even in a scenario in which all collaterals decline 100%, FTX would still have a positive balance of $638 million in assets. The projections were made based on consolidated balance sheets presented by Alameda.

The connection between Alameda and BlockFi started at the end of 2021, when the first $15 million was lent to Alameda. Prince noted that Alameda went through due diligence processes across many departments on BlockFi, but the financial documents provided were unaudited.

Alameda was lent capital under open-term loans, which allowed borrowers such as BlockFi to call for repayment of funds at any time. In June 2022, following the collapse of the Terra ecosystem, BlockFi called back millions in loans owned by Alameda.

According to Prince, the loans were paid, and the companies deepened their relationship amid the bear market.

Seeking capital from investors during the same period, BlockFi entered into an agreement with FTX US that included $400 million in credit and a potential acquisition of BlockFi in July 2023, which never happened since both companies went bankrupt as a result of last November’s events.

Alameda offered FTT, SOL (SOL) and SRM as collateral for loans. According to Prince’s testimony, those tokens were held on BlockFi’s account on FTX. BlockFi also used FTX as a trading platform for its clients’ orders. At the time of FTX bankruptcy, the crypto lending platform had $650 million lent to Alameda and $350 million in funds available for trading.

Once it became clear that funds were impaired and loans wouldn’t be repaid, BlockFi filed for bankruptcy. Prince noted that despite the challenges of the bear market, BlockFi would not have filed for bankruptcy without the FTX debacle.

Oct. 12: Ellison’s testimony continues, with further focus on relationship with Sam Bankman-Fried

Caroline Ellison alleges #SBF utilized Thai sex worker IDs in a bid to unfreeze $1B in Alameda funds before resorting to bribery. pic.twitter.com/COPHbaECz6

— Cointelegraph (@Cointelegraph) October 12, 2023

The cross-examination of Caroline Ellison started in the Southern District Court of New York on Oct. 12, with the former CEO of Alameda Research discussing the decision-making process between Alameda and FTX, as well as how her romantic relationship with Bankman-Fried played a role in the events leading up to the exchange’s collapse.

The defense counsel first explored the capital lent to Alameda by crypto lenders Genesis and Voyager. According to Ellison’s testimony, funds borrowed by Alameda could be legally used for a range of purposes, including trading activities and covering the company’s operating expenses. The defense used her remarks to show that Alameda’s lenders knew the capital was being used for undefined purposes.

She also reported that communication with Bankman-Fried deteriorated after their last breakup in April 2022, with her avoiding meeting with the former partner one-on-one and preferring to communicate via Signal or group meetings instead. The communication challenges a her concerns about FTX venture investments made Ellison consider resigning as CEO of Alameda in early 2022.

In response to questions from Bankman-Fried’s defense attorney, Ellison acknowledged having held at least 20 meetings with prosecutors since December 2022 as part of her cooperation agreement, including a review of her answers on Oct. 9, one day prior to her testifying as a witness in the case. In December, before an agreement was in place with the U.S. government, she acknowledged the Federal Bureau of Investigation searched her house.

During the bear market, Ellison also created financial forecasts of how much money would be needed to hedge Alameda against market downturns, according to her testimony. She discovered that Alameda would have to sell billions of dollars in assets to have an appropriate hedge.

Additionally, Ellison discussed Alameda’s Northern Dimension bank account, which FTX used while it had difficulty opening its own. Later on, around the end of 2021 and the beginning of 2022, FTX was able to get its account and began redirecting users’ funds. However, legacy customers still sent funds to Northern Dimension’s account. As evidence, the defense pointed to one of her meetings with prosecutors in December 2022, in which she suggested that Bankman-Fried was unaware that FTX customers’ funds were still being sent to Alameda.

Oct. 11: Caroline Ellison details the final months of FTX

On her second day of testimony at the trial of Sam “SBF” Bankman-Fried trial on Oct. 11, Caroline Ellison provided more information about the months leading up to the FTX debacle in November 2022. Lenders required Alameda Research to repay millions in loans in mid-June following the market downturn in May, according to Ellison. “I was very stressed out,” she said.

Genesis Capital was one of these lenders, recalling $500 million in loans, according to screenshots taken from conversations between Ellison, Bankman-Fried and Genesis employees via Telegram.

At the time, Alameda had over $13 billion of debt on its credit line with FTX, while its open-term loans exceeded $1.3 billion. As per Ellison’s testimony, Bankman-Fried instructed her to devise “alternative ways” to disclose Alameda’s financial information to lenders, specifically Genesis.

According to Ellison, Genesis could recall all loans to Alameda if it were aware of Alameda’s true financial status, as well as damage its reputation. “I didn’t want Genesis to know that,” she stated about Alameda’s multibillion-dollar liability toward FTX.

As per prosecutors’ evidence, Ellison worked on at least seven alternative spreadsheets for Genesis. A spreadsheet sent by Alameda to Genesis in June listed $10.3 billion in total liabilities, whereas the actual amount was approximately $15 billion at the time.

Bankman-Fried’s plans to survive the storm included raising capital from Mohammed bin Salman, the crown prince of Saudi Arabia. According to evidence presented in court, Ellison made a list of “things Sam is freaking out about” months before the exchange collapsed.

The list featured raising capital from “the MBS,” borrowing more capital from BlockFi, which had already lent Alameda over $660 million, as well as “getting regulators to crack down on Binance,” in an effort by Bankman-Fried to expand FTX’s market share, Ellison said.

She also mentioned a $150 million bribe that FTX allegedly paid to a Chinese official in 2021 to release funds frozen there as part of an investigation into money laundering. The alleged bribe is not included in the trial.

Oct. 10: Gary Wang is cross-examined, star witness Ellison enters

The fourth day of the trial began with Gary Wang concluding his testimony. He was cross-examined by one of SBF’s lawyers, Christian Everdell.

During the cross-examination, Wang was asked about Bankman-Fried’s intention to shut down Alameda, to which Wang responded that SBF thought there was a “30% chance” it should be shut down. He also said he wasn’t sure whether the tweet by Binance CEO Changpeng Zhao or leaked financials caused the FTX bank run.

After Wang was dismissed by Judge Lewis Kaplan, Ellison, the former CEO of Alameda and an ex-girlfriend of Bankman-Fried, was called to the witness stand.

In the opening questions, Ellison was asked why she was guilty of the crimes for which she was accused and responded that “Alameda took several billions of dollars from FTX customers and used it for investments.”

She reportedly placed the entire blame for the misuse of FTX user funds on Bankman-Fried. Ellison claimed he “set up the systems” that allowed Alameda to take $14 billion from the exchange.

Ellison also revealed personal information about her relationship with the defendant, including his aspirations to be U.S. president and that he considered paying former U.S. President Donald Trump not to run for reelection.

Additionally, she testified on the firm buying back FTX Tokens (FTT) from Binance or else “Binance would cause trouble,” along with using loans from Genesis in 2021 as a funding source.

“Alameda took several billions of dollars from FTX customers and used it for investments,” said Ellison, according to reports. “I sent balance sheets that made Alameda look less risky than it was.”

Ellison admitted to not feeling qualified for the CEO role at Alameda, though she was encouraged by SBF, and said she took a $3.5 million loan from the firm “for a gambling company people at FTX wanted to put in my name” and for political contributions.

Oct. 6 Gary Wang’s testimony continues admits to “special privileges” given to FTX on Alameda

The trial continued for the fourth day on Friday, Oct. 6, with a shorter session ending at 2:00 pm Eastern Time because jurors opted not to take a lunch break.

Wang, the former chief technology officer of FTX, continued to testify after a brief stint the previous afternoon. On this day, Wang testified that the back-end code and the database for FTX.com kept track of many coins a user had and the availability of a feature called “allow negative.”

According to Inner City Press, the prosecutor asked Wang what would happen if that feature was checked to which Wang said, “Then you are allowed to go beyond. “

He then said that Alameda’s account was allowed this special privilege and could, therefore, “trade more than it had in its account. They had a large line of credit. And it could trade faster than others.”

“It withdrew more than it had in its account, like $8 billion in fiat and crypto,” Wang said. When asked where the money came from, he said, “from FTX customers.”

According to Wang’s testimony, he overheard Bankman-Fried saying Alameda could withdraw up to $50–$100 million from FTX. He said that after a 2020 database query, he saw Alameda’s balance was negative to an amount greater than the revenue of FTX itself.

Wang pleaded guilty to four charges in December 2022, one of which was wire fraud. Like Ellison, Wang has agreed to cooperate with officials via a plea deal that could see him avoid up to 50 years in prison.

Oct. 5: Wang details relationship between FTX and Alameda Research

In over four hours of testimony, Wang provided in-depth details about the relationship between the companies and how the crypto empire ended up with an $8 billion hole in customer assets.

According to Wang, a few months after FTX’s inception, in 2019, Alameda received special privileges from FTX. Prosecutors used screenshots of FTX’s database and code available on GitHub to show that Alameda was allowed to have an unlimited negative balance at FTX, a special line of credit of $65 billion in 2022 and an exemption from the liquidation engine.

The commingling of funds and problems between companies evolved over time. In 2020, Bankman-Fried instructed Wang that Alameda’s negative balance should not exceed FTX’s revenue — a rule that changed over the years, according to Wang’s testimony. In late 2021, for example, Alameda’s liability to FTX stood at $3 billion, up from $300 million in 2020.

“I trusted his judgment,” Wang said when asked why he agreed to Alameda’s privileges.

However, these alleged privileges were part of Alameda’s role as a primary market maker for FTX, the defense argued later during Wang’s testimony. The defense counsel also noted that other market makers had similar privileges at FTX, and being able to go negative was a key feature of any market maker.

Another point emphasized by prosecutors was the MobileCoin exploit in 2021. Bankman-Fried allegedly told Wang and Ellison to add the multimillion-dollar deficit to Alameda’s balance sheet instead of keeping it on FTX to hide the loss from FTX investors.

Months before FTX’s collapse, Bankman-Fried, Wang and former engineering director Nishad Singh discussed shutting down Alameda and replacing its role with other market makers. The company’s liabilities, however, were too high at the time, sitting at $14 billion. Alameda remained in operation until November 2022.

Wang’s testimony will continue on Oct. 10, the same day Ellison’s will be heard.

Oct. 5: Yedidia cross-examination, witness testimonies in focus

Day 3 of the #SBF trial, we’re here bright and early! ☀️ pic.twitter.com/PQ1rQV38Px

— Cointelegraph (@Cointelegraph) October 5, 2023

A liability of $8 billion from Alameda to FTX was at the center of prosecutors’ cross-examination of Adam Yedidia on Oct. 5. Yedidia is a close friend of Bankman-Fried and was a developer at FTX. He was also one of ten people to live in Bankman-Fried’s $35 million luxury resort in the Bahamas.

According to Yedidia’s testimony, since early 2021, FTX used an Alameda account labeled North Dimension to deposit users’ funds while facing difficulties opening its own bank account. Funds would be considered Alameda’s liability toward FTX, which reached $8 billion in June 2022.

While Yedidia was aware of the funds sent to Alameda’s account, he didn’t see it as a concern when he first heard about it in 2021. However, after learning about the liability amount in 2022, he voiced his concerns to Bankman-Fried during a tennis game. According to Yedidia, Bankman-Fried said the debt should be settled between the companies within six months to three years.

“I trusted Sam, Caroline, and others in Alameda to handle the situation,” he said, answering questions from prosecutors. Upon learning that Alameda was not only holding the funds but using them to pay its debtors, Yedidia resigned in November 2022.

While prosecutors used the case to illustrate how the companies were commingling funds, Bankman-Fried’s defense counsel sought to share a broader picture of FTX and Alameda’s relationship with the jury.

The defense highlighted that FTX was growing fast, with its leadership working over 10 hours a day during the 2021 bull market, including Bankman-Fried, who oversaw several parts of the company at the time.

The defense counsel also pointed out that Yedidia had been under several inquiries from prosecutors under an immunity order, meaning cooperation with prosecutors would protect him from facing any charges regarding his role at FTX.

Also, according to Bankman-Fried’s defense, FTX’s difficulties opening a bank account and its reliance on Alameda’s North Dimension to deposit funds were well known. Yedidia’s cross-examination will resume this afternoon in the federal courtroom in lower Manhattan.

Two witnesses testified during the second part of the Bankman-Fried trial on Oct. 5: Matthew Huang, co-founder of Paradigm and Wang, co-founder of FTX and Alameda Research.

Paradigm invested a total of $278 million in FTX in two funding rounds between 2021 and 2022. According to Huang, the venture capital firm was not aware of the commingling of funds between FTX and Alameda, nor of the privileges that Alameda had with the crypto exchange.

Such privileges included Alameda’s exemption from FTX’s liquidation engine (a tool that closes positions at risk of liquidation). With the exemption, Alameda was able to leverage its position and maintain a negative balance with FTX.

The Paradigm co-founder also acknowledged that the firm did not conduct deeper due diligence on FTX, instead relying on information provided by Bankman-Fried.

Another concern for Paradigm was FTX not having a board of directors. According to Huang, Bankman-Fried was “very resistant” to the idea of having investors on FTX’s board of directors but promised to build one and appoint experienced executives to serve on it.

During his brief testimony, Wang acknowledged that he, along with Bankman-fried and Ellison, had committed wire fraud, securities fraud and commodities fraud.

Wang also noted that Alameda had special privileges with FTX, such as the ability to withdraw unlimited funds from the exchange, as well as a line of credit of $65 billion. To illustrate these privileges, Wang pointed out that any other market maker would have a credit line in the millions, while Alameda had a credit line in the billions.

A loan of approximately $200 million to $300 million from Alameda was also mentioned by Wang, allegedly as part of the purchase of other crypto firms. However, the loans were never credited to his account. His testimony will continue on Oct. 6.

Oct. 4: DOJ and Bankman-Fried’s defense state their arguments

The first hours of SBF’s trial have offered a glimpse of the arguments the U.S. Department of Justice (DOJ) and the former FTX CEO’s defense will bring to court in the coming weeks.

After a jury selection in the morning, both parties gave opening statements to the 12-person jury present in the court.

The DOJ took a tough stance against Bankman-Fried in its first statement, portraying the FTX founder as someone who deliberately lied to investors to enrich himself and expand his crypto empire.

According to the DOJ, Bankman-Fried lied to FTX customers and investors, using Alameda as a key partner to “steal customers’ funds,” a phrase that was frequently used during the opening statements.

As per the trial preview, the DOJ will focus its arguments on allegations that Bankman-Fried misled customers, investors and lenders regarding the safety of their funds while using Alameda to steal their money and influence politicians in Washington.

The defense, meanwhile, brought arguments about Bankman-Fried being a young entrepreneur who made business decisions that “didn’t work out.” The defense denied the existence of secret transactions between Alameda and FTX or a backdoor used to steal customer funds. According to the previous arguments presented, all transactions were legitimate or made in good faith by Bankman-Fried during the crypto market downturn and the subsequent collapse of FTX in November 2022.

The defense also highlighted the role of Binance in the bank run that led to FTX’s collapse. Testimonies will continue throughout the day.

According to the defense, Bankman-Fried assumed FTX was allowed to loan funds to Alameda as part of a business relationship with the market maker, and there was no secret door for transactions between the companies.

Prosecutors also noted that Ellison, Wang and Singh would offer the jury insider details about Bankman-Fried’s role in FTX’s operations and alleged crimes. However, the defense pointed out that as part of the cooperation agreement with the government, they were supposed to give testimony against Bankman-Fried, raising doubts about their credibility.

The defense also downplayed the accusations against the nature of the relationship between FTX and Alameda, arguing that FTX margin traders were aware of the risks associated with transactions.

“There was no theft,” the defense claimed. “It’s not a crime to be the CEO of a company that files for bankruptcy.”

In the second half of the first day of the trial, the jury heard from two witnesses: Mark Julliard, a French trader and former client of FTX, and Adam Yedidia, a friend of Sam Bankman-Fried and former employee at Alameda Research and FTX.

In his testimony, Julliard said he had four Bitcoin (BTC) held at FTX at the time of the exchange’s collapse, worth nearly $100,000. He admitted that FTX and Bankman-Fried’s marketing efforts, as well as the notable venture capital companies backing FTX, gave him the confidence to use the exchange for crypto trading. He assumed that venture capital firms had done due diligence on FTX and its leadership.

During the questioning, prosecutors emphasized that the trader used FTX exclusively for spot trading and was unaware that the exchange used client funds for crypto trading with Alameda Research.

Questions for Yedidia were focused on his educational background at the Massachusetts Institute of Technology, where he first met Bankman-Fried and had two professional experiences with the FTX founder. Yedidia worked at Alameda briefly in 2017 as a trader and then returned to work for FTX in 2021 as a developer. He was among 10 people living in the Bahamas on FTX’s $30 million real estate.

In Yedidia’s testimony, prosecutors used former FTX ads as evidence that the company was always positioning itself as a safe, trusted and easy way to invest in cryptocurrency, including marketing campaigns with NFL player Tom Brady and comedian Larry David. The trial will resume Oct. 5.

Oct. 3: SBF trial begins

The trial of Bankman-Fried began on Oct. 3 with jury selection. Bankman-Fried is charged with seven counts of conspiracy and fraud in connection with the collapse of FTX, the cryptocurrency exchange he co-founded. He has pleaded not guilty to all charges. The case is being heard by Judge Lewis Kaplan, who has presided over a long list of other high-profile cases, including ones involving detainees at Guantanamo Bay, the Gambino crime family, Prince Andrew and Donald Trump.

Bankman-Fried was ordered to be jailed on Aug. 11 after Kaplan found that his sharing of former Alameda Research CEO Caroline Ellison’s personal papers amounted to witness intimidation. Alameda Research was a trading house also founded by Bankman-Fried. Previously, he had been under house arrest in his parents’ home in Stanford, California, on a $250-million bond.

December: SBF arrested

Bankman-Fried was arrested in the United States on his arrival from the Bahamas on Dec. 21, 2022. He had been arrested in the Bahamas on Dec. 12 after the U.S. government formally notified the country of charges the U.S. was filing against him. He declared his intention to fight extradition from the Caribbean nation but changed his mind after a week in Bahaman jail and consented to extradition.

Meanwhile, FTX co-founder Gary Wang and Alameda Research CEO (and reportedly sometime SBF girlfriend) Ellison agreed to plead guilty in the burgeoning case.

November: FTX collapses

Bankman-Fried’s troubles began when reports emerged on Nov. 2 that Alameda Research had a large holding of FTX Token (FTT), FTX’s utility token. That revelation led to questions about the relationship between the two entities. On Nov. 6, Changpeng Zhao, CEO of rival exchange Binance, announced that his exchange would liquidate its FTT holdings, which were estimated to be worth $2.1 billion. Zhao turned down an offer tweeted by Ellison to buy Binance’s FTT.

A run began on FTX. Bankman-Fried gave reassurances on Twitter (now X) that the exchange’s “assets are fine” and accused “a competitor” of spreading rumors. By Nov. 8, the price of FTT had fallen from $22 to $15.40.

It’s only been one week since SBF’s notorious “FTX is fine. Assets are fine.” pic.twitter.com/zKoILqquHF

— Robert Smith (@BondHack) November 14, 2022

Also on Nov. 8, Bankman-Fried announced on Twitter that he had come to an agreement with Zhao “on a strategic transaction.” He wrote, “Our teams are working on clearing out the withdrawal backlog as is. This will clear out liquidity crunches; all assets will be covered 1:1.”

On Nov. 9, Zhao announced that Binance would not pursue the acquisition of FTX after due diligence and more reports of mishandled funds. The price of Bitcoin (BTC) plummeted to $15,600. The FTX and Alameda Research websites went dark for a few hours. When the FTX website came back, it bore a warning against making deposits and was unable to process withdrawals.

On Nov. 10, Bankman-Fried posted a 22-part Twitter thread that began with “I’m sorry.” It was the first of a long string of public statements he made about the exchange’s fall. The following day, the entire staff of Alameda Research quit, and FTX, FTX US and Alameda Research filed for bankruptcy in the United States. Bankman-Fried resigned as FTX CEO and was replaced by John J. Ray III, who was best known for his role in the Enron bankruptcy.

SBF and FTX before the fall

At the beginning of 2022, FTX had a $32-billion valuation and was thought to be in enviable financial condition. Bankman-Fried was seen as a respected business leader by much of the crypto community and the world at large. He was photographed with political leaders and spoke at congressional hearings.

Maxine Waters is chairing the investigation into FTX https://t.co/oFMctH4rRh pic.twitter.com/Ox6O5w4nOl

— Jordan Schachtel @ dossier.today (@JordanSchachtel) November 17, 2022

He had gained a reputation as a philanthropist, pursuing a philosophy popular among academics known as “effective altruism.” Part of his implementation of that philosophy was political activism in the form of financial support for candidates.

As the crypto winter set in, Bankman-Fried spoke of FTX and Alameda Research’s “responsibility to seriously consider stepping in, even if it is at a loss to ourselves, to stem contagion.” The companies made a bid for Voyager Digital that was rebuffed.

FTX made a deal with Visa to introduce its own debit card in 40 countries.

Bankman-Fried, Ellison and other alumni of Jane Street Capital founded Alameda Research in 2017. Bankman-Fried went on to found FTX with Wang in 2019. Zhao was an early investor in the exchange.

This is a developing story, and further information will be added as it becomes available.

cryptocurrency bitcoin blockchain crypto btc real estate crypto commoditiesUncategorized

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Authored by Sam Bourgi via CreditNews.com,

Homeownership…

Share this:

Authored by Sam Bourgi via CreditNews.com,

Homeownership is one of the key pillars of the American dream. But for many families, the idyllic fantasy of a picket fence and backyard barbecues remains just that—a fantasy.

Thanks to elevated mortgage rates, sky-high house prices, and scarce inventory, millions of American families have been locked out of the opportunity to buy a home in many cities.

To shed light on America’s housing affordability crisis, Creditnews Research ranked the 50 most populous cities by the percentage of neighborhoods within reach for the typical married-couple household to buy a home in.

The study reveals a stark reality, with many cities completely out of reach for the most affluent household type. Not only that, the unaffordability has radically worsened in recent years.

Comparing how affordability has changed since Covid, Creditnews Research discovered an alarming pattern—indicating consistently more unaffordable housing in all but three cities.

Fortunately, there’s still hope for households seeking to put down roots in more affordable cities—especially for those looking beyond Los Angeles, New York, Boston, San Jone, and Miami.

The typical American family has a hard time putting down roots in many parts of the country. In 11 of the top 50 cities, at least 50% of neighborhoods are out of reach for the average married-couple household. The affordability gap has widened significantly since Covid; in fact, no major city has reported an improvement in affordability post-pandemic.

Sam Bourgi, Senior Analyst at Creditnews

Key findings

-

The most unaffordable cities are Los Angeles, Boston, St. Louis, and San Jose; in each city, 100% of neighborhoods are out of reach for for married-couple households earning a median income;

-

The most affordable cities are Cleveland, Hartford, and Memphis—in these cities, the typical family can afford all neighborhoods;

-

None of the top 50 cities by population saw an improvement in affordable neighborhoods post-pandemic;

-

California recorded the biggest spike in unaffordable neighborhoods since pre-Covid;

-

The share of unaffordable neighborhoods has increased the most since pre-Covid in San Jose (70 percentage points), San Diego (from 57.8 percentage points), and Riverside-San Bernardino (51.9 percentage points);

-

Only three cities have seen no change in housing affordability since pre-Covid: Cleveland, Memphis, and Hartford. They’re also the only cities that had 0% of unaffordable neighborhoods before Covid.

Cities with the highest share of unaffordable neighborhoods

With few exceptions, the most unaffordable cities for married-couple households tend to be located in some of the nation’s most expensive housing markets.

Four cities in the ranking have an unaffordability percentage of 100%—indicating that the median married-couple household couldn’t qualify for an average home in any neighborhood.

The following are the cities ranked from the least affordable to the most:

-

Los Angeles, CA: Housing affordability in Los Angeles has deteriorated over the last five years, as average incomes have failed to keep pace with rising property values and elevated mortgage rates. The median household income of married-couple families in LA is $117,056, but even at that rate, 100% of the city’s neighborhoods are unaffordable.

-

St. Louis, MO: It may be surprising to see St. Louis ranking among the most unaffordable housing markets for married-couple households. But a closer look reveals that the Mound City was unaffordable even before Covid. In 2019, 98% of the city’s neighborhoods were unaffordable—way worse than Los Angeles, Boston, or San Jose.

-

Boston, MA: Boston’s housing affordability challenges began long before Covid but accelerated after the pandemic. Before Covid, married couples earning a median income were priced out of 90.7% of Boston’s neighborhoods. But that figure has since jumped to 100%, despite a comfortable median household income of $172,223.

-

San Jose, CA: Nestled in Silicon Valley, San Jose has long been one of the most expensive cities for housing in America. But things have gotten far worse since Covid, as 100% of its neighborhoods are now out of reach for the average family. Perhaps the most shocking part is that the median household income for married-couple families is $188,403—much higher than the national average.

-

San Diego, CA: Another California city, San Diego, is among the most unaffordable places in the country. Despite boasting a median married-couple household income of $136,297, 95.6% of the city’s neighborhoods are unaffordable.

-

San Francisco, CA: San Francisco is another California city with a high married-couple median income ($211,585) but low affordability. The percentage of unaffordable neighborhoods for these homebuyers stands at 89.2%.

-

New York, NY: As one of the most expensive cities in America, New York is a difficult housing market for married couples with dual income. New York City’s share of unaffordable neighborhoods is 85.9%, marking a 33.4% rise from pre-Covid times.

-

Miami, FL: Partly due to a population boom post-Covid, Miami is now one of the most unaffordable cities for homebuyers. Roughly four out of five (79.4%) of Miami’s neighborhoods are out of reach price-wise for married-couple families. That’s a 34.7% increase from 2019.

-

Nashville, TN: With Nashville’s population growth rebounding to pre-pandemic levels, the city has also seen greater affordability challenges. In the Music City, 73.7% of neighborhoods are considered unaffordable for married-couple households—an increase of 11.9% from pre-Covid levels.

-

Richmond, VA: Rounding out the bottom 10 is Richmond, where 55.9% of the city’s 161 neighborhoods are unaffordable for married-couple households. That’s an 11.9% increase from pre-Covid levels.

Cities with the lowest share of unaffordable neighborhoods

All the cities in our top-10 ranking have less than 10% unaffordable neighborhoods—meaning the average family can qualify for a home in at least 90% of the city.

Interestingly, these cities are also outside the top 15 cities by population, and eight are in the bottom half.

The following are the cities ranked from the most affordable to the least:

-

Hartford, CT: Hartford ranks first with the percentage of unaffordable neighborhoods at 0%, unchanged since pre-Covid times. Married couples earning a median income of $135,612 can afford to live in any of the city’s 16 neighborhoods. Interestingly, Hartford is the smallest city to rank in the top 10.

-

Memphis, TN: Like Hartford, Memphis has 0% unaffordable neighborhoods, meaning any married couple earning a median income of $101,734 can afford an average homes in any of the city’s 12 neighborhoods. The percentage of unaffordable neighborhoods also stood at 0% before Covid.

-

Cleveland, OH: The Midwestern city of Cleveland is also tied for first, with the percentage of unaffordable neighborhoods at 0%. That means households with a median-couple income of $89,066 can qualify for an average home in all of the city’s neighborhoods. Cleveland is also among the three cities that have seen no change in unaffordability compared to 2019.

-

Minneapolis, MN: The largest city in the top 10, Minneapolis’ share of unaffordable neighborhoods stood at 2.41%, up slightly from 2019. Married couples earning the median income ($149,214) have access to the vast majority of the city’s 83 neighborhoods.

-

Baltimore, MD: Married-couple households in Baltimore earn a median income of $141,634. At that rate, they can afford to live in 97.3% of the city’s 222 neighborhoods, making only 2.7% of neighborhoods unaffordable. That’s up from 0% pre-Covid.

-

Louisville, KY: Louisville is a highly competitive market for married households. For married-couple households earning a median wage, only 3.6% of neighborhoods are unaffordable, up 11.9% from pre-Covid times.

-

Cincinnati, OH: The second Ohio city in the top 10 ranks close to Cleveland in population but has a much higher median married-couple household income of $129,324. Only 3.6% of the city’s neighborhoods are unaffordable, up slightly from pre-pandemic levels.

-

Indianapolis, IN: Another competitive Midwestern market, only 4.4% of Indianapolis is unaffordable, making the vast majority of the city’s 92 neighborhoods accessible to the average married couple. Still, the percentage of unaffordable neighborhoods before Covid was less than 1%.

-

Oklahoma City, OK: Before Covid, Oklahoma City had 0% neighborhoods unaffordable for married-couple households earning the median wage. It has since increased to 4.69%, which is still tiny compared to the national average.

-

Kansas City, MO: Kansas City has one of the largest numbers of neighborhoods in the top 50 cities. Its married-couple residents can afford to live in nearly 95% of them, making only 5.6% of neighborhoods out of reach. Like Indiana, Kansas City’s share of unaffordable neighborhoods was less than 1% before Covid.

The biggest COVID losers

What's particularly astonishing about the current housing market is just how quickly affordability has declined since Covid.

Even factoring in the market correction after the 2022 peak, the price of existing homes is still nearly one-third higher than before Covid. Mortgage rates have also more than doubled since early 2022.

Combined, the rising home prices and interest rates led to the worst mortgage affordability in more than 40 years.

Against this backdrop, it’s hardly surprising that unaffordability increased in 47 of the 50 cities studied and remained flat in the other three. No city reported improved affordability in 2024 compared to 2019.

The biggest increases are led by San Jose (70 percentage points), San Diego (57.8 percentage points), Riverside-San Bernardino (51.9 percentage points), Sacramento (43 percentage points), Orlando (37.4 percentage points), Miami (34.7 percentage points), and New York City (33.4 percentage points).

The following cities in our study are ranked by the largest percentage point change in unaffordable neighborhoods since pre-Covid:

Uncategorized

Your financial plan may be riskier without bitcoin

It might actually be riskier to not have bitcoin in your portfolio than it is to have a small allocation.

Share this:

This article originally appeared in the Sound Advisory blog. Sound Advisory provide financial advisory services and are specialize in educating and guiding clients to thrive financially in a bitcoin-powered world. Click here to learn more.

“Belief is a wise wager. Granted that faith cannot be proved, what harm will come to you if you gamble on its truth and it proves false? If you gain, you gain all; if you lose, you lose nothing. Wager, then, without hesitation, that He exists.”

- Blaise Pascal

Blaise Pascal only lived to age 39 but became world-famous for many contributions in the fields of mathematics, physics, and theology. The above quote encapsulates Pascal’s wager—a philosophical argument for the Christian belief in the existence of God.

The argument's conclusion states that a rational person should live as though God exists. Even if the probability is low, the reward is worth the risk.

Pascal’s wager as a justification for bitcoin? Yes, I’m aware of the fallacies: false dichotomy, appeal to emotion, begging the question, etc. That is not the point. The point is that binary outcomes instigate extreme results, and the game theory of money suggests that it’s a winner-take-all game.

The Pascalian investor: A rational approach to bitcoin

Humanity’s adoption of “the best money over time” mimics a series of binary outcomes—A/B tests.

Throughout history, inferior forms of money have faded as better alternatives emerged (see India’s failed transition to a gold standard). And if bitcoin is trying to be the premier money of the future, it will either succeed or it won’t.

“If you ain’t first, you’re last.” -Ricky Bobby, Talladega Nights, on which monies succeed over time.

So, we can look at bitcoin success similarly to Pascal’s wager—let’s call it Satoshi’s wager. The translated points would go something like this:

- If you own bitcoin early and it becomes a globally valuable money, you gain immensely. ????

- If you own bitcoin and it fails, you’ve lost that value. ????

- If you don’t own bitcoin and it goes to zero, no pain and no gain. ????

- If you don’t own bitcoin and it succeeds, you will have missed out on the significant financial revolution of our lifetimes and fall comparatively behind. ????

If bitcoin is successful, it will be worth far more than it is today and have a massive impact on your financial future. If it fails, the losses are only limited to your exposure. The most that you could lose is the money that you invested.

It is hypothetically possible that bitcoin could be worth 100x more than it is today, but it can only possibly lose 1x its value as it goes to zero. The concept we’re discussing here is asymmetric upside - significant gains with relatively limited downside. In other words, the potential rewards of the investment outweigh the potential risks.

Bitcoin offers an asymmetric upside that makes it a wise investment for most portfolios. Even a small allocation provides potential protection against extreme currency debasement.

Salt, gasoline, and insurance

“Don’t over salt your steak, pour too much gas on the fire, or buy too much insurance.”

A little bit goes a long way, and you can easily overdo it. The same applies when looking at bitcoin in the context of a financial plan.

Bitcoin’s asymmetric upside gives it “insurance-like” qualities, and that insurance pays off very well in times of money printing. This was exemplified in 2020 when bitcoin's value increased over 300% in response to pandemic money printing, far outpacing stocks, gold, and bonds.

Bitcoin offers a similar asymmetric upside today. Bitcoin's supply is capped at 21 million coins, making it resistant to inflationary debasement. In contrast, the dollar's purchasing power consistently declines through unrestrained money printing. History has shown that societies prefer money that is hard to inflate.

If recent rampant inflation is uncontainable and the dollar system falters, bitcoin is well-positioned as a successor. This global monetary A/B test is still early, but given their respective sizes, a little bitcoin can go a long way. If it succeeds, early adopters will benefit enormously compared to latecomers. Of course, there are no guarantees, but the potential reward justifies reasonable exposure despite the risks.

Let’s imagine Nervous Nancy, an extremely conservative investor. She wants to invest but also take the least risk possible. She invests 100% of her money in short-term cash equivalents (short-term treasuries, money markets, CDs, maybe some cash in the coffee can). With this investment allocation, she’s nearly certain to get her initial investment back and receive a modest amount of interest as a gain. However, she has no guarantees that the investment returned to her will purchase the same amount as it used to. Inflation and money printing cause each dollar to be able to purchase less and less over time. Depending on the severity of the inflation, it might not buy anything at all. In other words, she didn’t lose any dollars, but the dollar lost purchasing power.

Now, let’s salt her portfolio with bitcoin.

99% short-term treasuries. 1% bitcoin.

With a 1% allocation, if bitcoin goes to zero overnight, she’ll have only lost a penny on the dollar, and her treasury interest will quickly fill the gap. Not at all catastrophic to her financial future.

However, if the hypothetical hyperinflationary scenario from above plays out and bitcoin grows 100x in purchasing power, she’s saved everything. Metaphorically, her entire dollar house burned down, and “bitcoin insurance” made her whole. Powerful. A little bitcoin salt goes a long way.

(When protecting against the existing system, it’s important to remember that you need to get your bitcoin out of the system. Keeping bitcoin on an exchange or with a counterparty will do you no good if that entity fails. If you view bitcoin as insurance, it’s essential to keep your bitcoin in cold storage and hold your keys. Otherwise, it’s someone else’s insurance.)

When all you have a hammer, everything looks like a…

A construction joke:

There are only three rules to construction: 1.) Always use the right tool for the job! 2.) A hammer is always the right tool! 3.) Anything can be a hammer!

Yeah. That’s what I thought, too. Slightly funny and mostly useless.

But if you spend enough time swinging a hammer, you’ll eventually realize it can be more than it first appears. Not everything is a nail. A hammer can tear down walls, break concrete, tap objects into place, and wiggle other things out. A hammer can create and destroy; it builds tall towers and humbles novice fingers. The use cases expand with the skill of the carpenter.

Like hammers, bitcoin is a monetary tool. And a 1-5% allocator to the asset typically sees a “speculative insurance” use case - valid. Bitcoin is speculative insurance, but it is not only speculative insurance. People invest and save in bitcoin for many different reasons.

I’ve seen people use bitcoin to pursue all of the following use cases:

- Hedging against a financial collapse (speculative insurance)

- Saving for family and future (long-term general savings and safety net)

- Growing a downpayment for a house (medium-term specific savings)

- Shooting for the moon in a manner equivalent to winning the lottery (gambling)

- Opting out of government-run, bank-controlled financial systems (financial optionality)

- Making a quick buck (short-term trading)

- Escaping a hostile country (wealth evacuation)

- Locking away wealth that can’t be confiscated (wealth preservation)

- As a means to influence opinions and gain followers (social status)

- Fix the money and fix the world (mission and purpose)

Keep this in mind when taking other people’s financial advice. They are often playing a different game than you. They have different goals, upbringings, worldviews, family dynamics, and circumstances. Even though they might use the same hammer as you, it could be for a completely different job.

Wrapping Up

A massive allocation to bitcoin may seem crazy to some people, yet perfectly reasonable to others. The same goes for having a 1% allocation.

But, given today’s macroeconomic environment and bitcoin’s trajectory, I find very few use cases where 0% bitcoin makes sense. By not owning bitcoin, you implicitly say that you are 100% certain it will fail and go to zero. Given its 14-year history so far, I’d recommend reducing your confidence. Nobody is 100% right forever. A little salt goes a long way. Your financial plan may be riskier without bitcoin. Diversify accordingly.

“We must learn our limits. We are all something, but none of us are everything.” - Blaise Pascal.

bonds pandemic stocks bitcoin link goldContact

Office: (208)-254-0142

Ste. 205

Eagle, ID 83616

Check the background of your financial professional on FINRA's BrokerCheck.The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Some of this material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named representative, broker - dealer, state - or SEC - registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

Copyright 2024 FMG Suite.

Sound Advisory, LLC (“SA”) is a registered investment advisor offering advisory services in the State of Idaho and in other jurisdictions where exempt. Registration does not imply a certain level of skill or training. The information on this site is not intended as tax, accounting, or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This information should not be relied upon as the sole factor in an investment-making decision. Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal any performance noted on this site.

The information on this site is provided “AS IS” and without warranties of any kind, either express or implied. To the fullest extent permissible pursuant to applicable laws, Sound Advisory LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

SA does not warrant that the information on this site will be free from error. Your use of the information is at your sole risk. Under no circumstances shall SA be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided on this site, even if SA or an SA authorized representative has been advised of the possibility of such damages. Information contained on this site should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Uncategorized

The Question You Should Ask Whenever You’re Wrong

“Never bet on the end of the world. It only comes once, which is pretty long odds.” — Arthur Cashin, New York Stock Exchange Floor Manager (“Maxims…

Share this:

{kind=link}

“Never bet on the end of the world. It only comes once, which is pretty long odds.” — Arthur Cashin, New York Stock Exchange Floor Manager (“Maxims of Wall Street,” p. 110)

Since Joe Biden gave his State of the Union (or shall we say “Disunion”) speech last week, I’ve encountered a plethora of negative comments about the future of America.

Is the American Dream Over?

“If Biden is re-elected, it will be the end of the American Dream as we know it,” said one pundit on Fox News.

The critics are out in force. Supply-side economist Steve Moore writes, “Biden is intentionally trying to dismantle the American economy with his imbecile energy, climate change, crime, border, inflation, debt and high tax policies.”

Glenn Beck, the host of Blaze TV, recently warned that America may face multiple terrorist attacks in one day, similar to 9/11, given the open borders policy of the Biden Administration.

Recently, I attended a private meeting of political leaders and pundits who thought that President Biden’s address was the most polemical, shrill and divisive talk they had ever heard.

I’ve been watching State of the Union addresses all my adult life, by both Republicans and Democrats, and in many ways they are always polemical and divisive. What was amazing to me is how “sleepy” Joe Biden performed. He must have been well rested and jacked up with some pretty incredible drugs to do as well as he did.

President Biden did say some things that were crazy, such as when he asserted that voting for former president Donald Trump is a “vote against democracy.”

Hey, wasn’t it the Democrats who want to remove Trump from the November ballot in Colorado and other states? Talk about anti-democratic! I was glad to see the Supreme Court ruled 9-0 against the Colorado decision. Let the people decide. Isn’t that what democracy is all about?

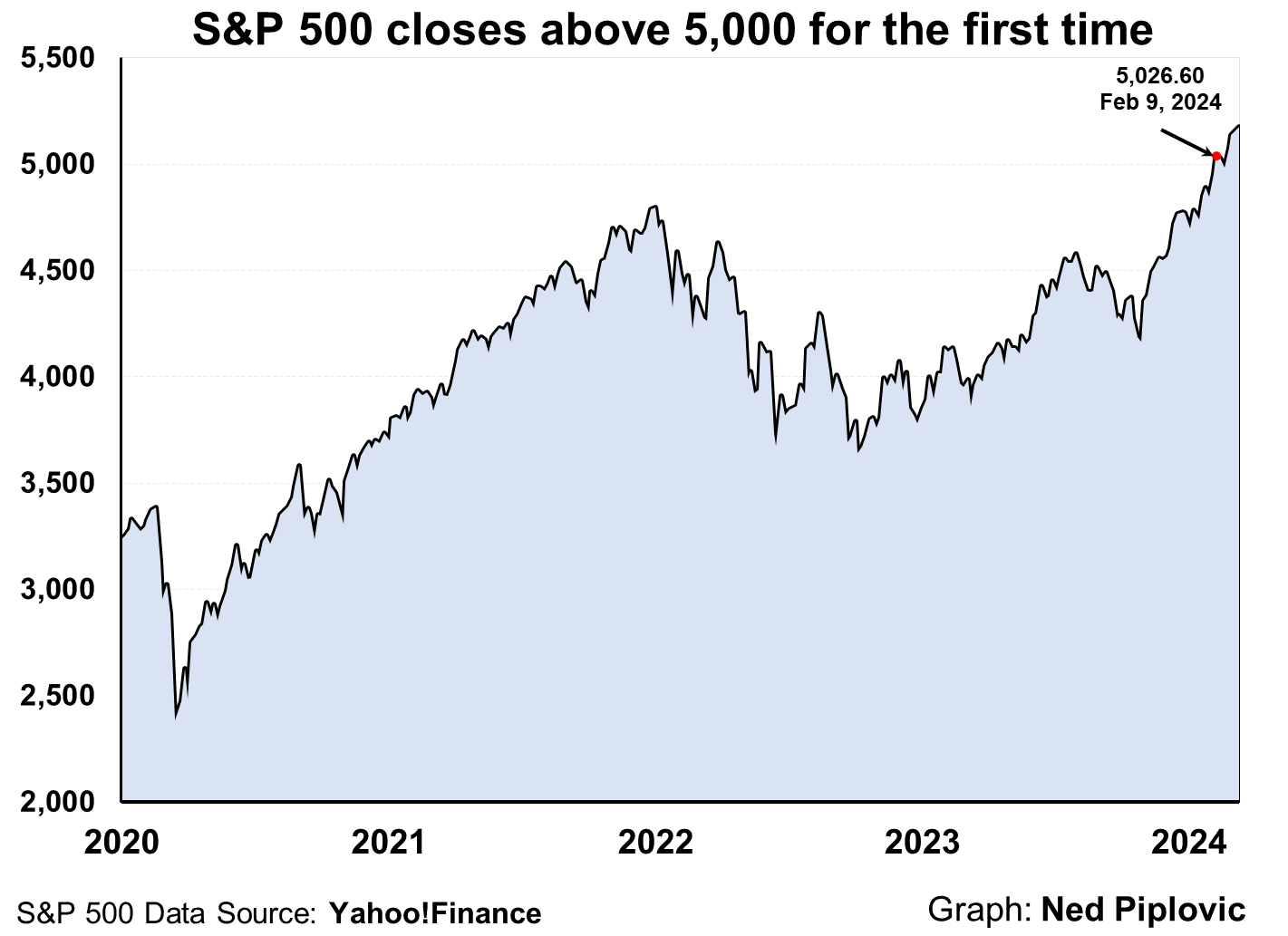

Why Then Is the Stock Market at an All-Time High?

Kevin Roberts, the new president of the Heritage Foundation, recently declared, “The American Dream is being threatened as never before!”

If that is true, why is the stock market at or near an all-time high? What are the prophets of doom and gloom missing?

That’s the question I always ask when I’m wrong about something:

“What am I missing?”

Wall Street is a good bellwether of what is going on the country. So far, the benefits outweigh the costs. The economy is recovering from the Covid pandemic, inflation is coming down, corporate profits are strong, new technologies are being introduced and there’s a strong movement to reverse the “cancel” and “woke” culture in the United States.

We have gridlock on Capitol Hill that is keeping a lot of bad legislation from becoming law. The Supreme Court has reversed many bad decisions by the lower courts.

We Remain Fully Invested

So, all is not lost after all. In my newsletter, Forecasts & Strategies, we remain fully invested, despite occasional corrections in the market.

We are also well diversified in some “contrarian” investments such as Bitcoin and gold, both of which continue to outperform and offset any selloffs in the stock market.

By remaining positive and fully invested, we have made good money in 2024.

The American Obituary Has Been Written Many Times

The American economy has been left for dead many times, only to be resuscitated with renewed vigor. We have survived civil and world wars, the Great Depression, the inflationary 1970s, terrorist attacks and more.

As J.P. Morgan once said, “The man who is a bear on the United States will eventually go broke” (“Maxims,” p. 111).

I encourage you to read my favorite J.P. Morgan story found on pp. 218-219 in “The Maxims of Wall Street.” See www.skousenbooks.com.

American exceptionalism is alive and well. We are still the Promised Land with millions wanting to live and work here.

Solving Our Unfunded Liability Problem: Look to Canada!

One serious problem in America is the irresponsible, out-of-control deficit spending and national debt, created by both Republican and Democratic leaders over the years. The trouble is getting worse, with rising interest rates to pay the debt and the growing unfunded liabilities from Social Security and Medicare.

Robert Poole of the Reason Foundation warns:

“The Congressional Budget Office (CBO)’s latest 10-year projection is frightening. CBO projects annual federal budget deficits to increase steadily, exceeding $2.5 trillion by 2034, assuming current policies continue… The federal government is projected to borrow an additional $20 trillion over the next decade, the CBO estimates.

“One driving factor is the impact of higher interest rates on the current $34 trillion (and growing) national debt… By 2034, annual interest expense is projected to be $1.6 trillion — more than one-fourth of all federal tax revenue.

“The Penn Wharton Budget Model suggests that the United States has about 20 years to fix this debt/deficit problem — ‘after which no amount of future tax increases or spending cuts could avoid the government defaulting on its debt.’

“On August 2, 2023, Fitch Ratings downgraded the federal government’s long-term debt rating from AAA to AA+. And on November 10, 2023, Moody’s Investors Service reduced its outlook on the U.S. credit rating from ‘stable’ to ‘negative.’ Standard & Poor’s did its downgrade in 2011. These are warning shots across the ship of state’s bow.”

Sounds ominous. What to do?

Canada faced a similar problem back in the mid-1990s. Deficits were getting out of hand, and the Canadian dollar was sinking. The Conservative Party and the Liberty Party of Canada worked together and resolved to cut government spending, lay off federal workers and then went on a supply-side tax-cutting program that resulted in economic growth and deficit reduction.

What about the unfunded liability problem, which causes national bankruptcy? Again, Canada offers an incredible example of solving the issue.

Last week, Andy Puzder and Terrence Keeley wrote an op-ed in The Wall Street Journal on the success of the Canadian social security system, which has earned a 9.3% annualized return over the past 10 years (versus almost zero return in our Social Security Trust Fund). They wrote:

“The Canada Pension Plan’s superiority stems from its asset allocation. The fund invests about 57% of its assets in equities and 12% in bonds; the rest is divided among real estate, infrastructure and credit. Over the past 10 years, the Canada Pension Plan has realized a 9.3% annualized net return. Similarly to how Social Security works, Canadian citizens pay into the program and are guaranteed lifetime benefits.”

At some point, the United States will need to imitate the Canadian model. Here is a chart on the difference between the two:

In sum, there are solutions to all of our problems — if we know where to look and remain optimistic.

Sound Advice from the ‘Investment Bible’

In my home, I have a whole section of my library devoted to dozens of books written by doomsayers and Cassandras, such as “The Coming Deflation”…. “How to Prosper During the Coming Bad Years”… “Bankruptcy 1995”… “The End of Inflation” and so on.

I’ve also collected a bunch of quotes on doomsayers and Cassandras in “The Maxims of Wall Street.”

Jim Woods, my colleague at Eagle Publishing, is a big fan.

Jim states, “I’ve always felt that a collection of wisdom from the best brains in that industry has been most special to me. And on this front, there is no better ‘how to’ anthology than the one by my friend, fellow Fast Money Alert co-editor and brilliant economist, Dr. Mark Skousen. The ‘Maxims of Wall Street’ is a collection of some of the greatest wisdom ever to flow from the biggest and brightest names on Wall Street. Great investors such as Jesse Livermore, Baron Rothschild, J.P. Morgan, Benjamin Graham, Warren Buffett, Peter Lynch and John Templeton are just a sneak peek at some of the names you’ll discover in this fantastic collection. Then, there is profundity from the likes of Ben Franklin, John D. Rockefeller, Joe Kennedy, Bernard Baruch, John Maynard Keynes, Steve Forbes and numerous other luminaries too copious to mention.”

If you don’t have an autographed copy of my collection of quotes, stories and wisdom of the world’s top traders and investors, please order a copy now.

It is in its 10th edition, having sold nearly 50,000 copies. It has been endorsed by Warren Buffett, Kevin O’Leary, Jack Bogle, Kim Githler, Bert Dohmen, Richard Band and Gene Epstein in Barron’s.

I offer it cheaply to my Skousen CAFÉ readers: Only $21 for the first copy, and all additional copies are $11 each (they make a great gift to clients, friends, relatives and your favorite broker or money manager). I sign and number each one, then mail it at no extra charge if you live in the United States. If you order an entire box (32 copies), the price is only $327. As Hetty Green, the first female millionaire, once said, “When I see a good thing going cheap, I buy a lot of it!”

To order, go to www.skousenbooks.com.

You Nailed it!

Friedrich Hayek Won the Nobel Prize 50 Years Ago

“Mises and Hayek articulated and vastly enriched the principles of Adam Smith at a crucial time in this century.” — Vernon Smith (2002 Nobel prize in economics)

March 23 is the anniversary of the passing of a giant in economics — the Austrian economist Friedrich Hayek (1899-1992).

He is most famous for his bestselling book “The Road to Serfdom,” written near the end of World War II, an admittedly a pessimistic book, warning the West that its move toward socialism, fascism and communism was indeed a “road to serfdom.”

Then, when he won the Nobel prize in economics in 1974, he warned again of the dangers of “accelerating inflation,” which he said, were “brought about by policies which the majority of economists recommended and even urged governments to pursue. We have indeed at the moment little cause for pride: as a profession we have made a mess of things.”

Fortunately, we have moved away from the road to serfdom, especially after the collapse of the Berlin Wall and the Soviet socialist central planning model.

But the road to freedom has been a checkered one, and we must always be alert to losing our liberties in the name of inequality, fairness and social justice.

Last month, Tom Woods interviewed me in honor of the 50th anniversary of Hayek’s winning the Nobel prize. Watch the interview here.

Mark Skousen, Friedrich Hayek and Gary North in Austria, 1985

I had the pleasure of interviewing Hayek for three hours in the Austrian alps in 1985. He was especially happy to hear I resurrected his macroeconomic model in developing gross output (GO). See www.grossoutput.com, a measure of Hayek’s triangles.

This week, Larry Reed, former president of the Foundation for Economic Education, wrote this wonderful tribute to Hayek.

Highly recommended.

Good investing, AEIOU,

Mark Skousen

The post The Question You Should Ask Whenever You’re Wrong appeared first on Stock Investor.

bonds pandemic equities bitcoin real estate canadian dollar gold

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Part 1: Current State of the Housing Market; Overview for mid-March 2024

The Question You Should Ask Whenever You’re Wrong

Walmart and Target make key self-checkout changes to fight theft

The best real estate coaching programs for 2024

Your financial plan may be riskier without bitcoin

Futures Rise To New Record High Ahead Of Data Deluge

Bougie Broke The Financial Reality Behind The Facade

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International6 days ago

International6 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International6 days ago

International6 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges