Uncategorized

Private Equity Firms Expect Middle-Market Dominance in 2023 as Monetary Tightening Drives Deal Volumes and Values Down, Yet Fundraising Still Outstrips Pre-Pandemic Levels

Private Equity Firms Expect Middle-Market Dominance in 2023 as Monetary Tightening Drives Deal Volumes and Values Down, Yet Fundraising Still Outstrips Pre-Pandemic Levels

PR Newswire

NEW YORK, Nov. 28, 2022

Increasing interest rates and cost of le…

Share this:

Private Equity Firms Expect Middle-Market Dominance in 2023 as Monetary Tightening Drives Deal Volumes and Values Down, Yet Fundraising Still Outstrips Pre-Pandemic Levels

PR Newswire

NEW YORK, Nov. 28, 2022

Increasing interest rates and cost of leverage amid monetary tightening is the top challenge facing the US PE market, according to Dechert's "Global Private Equity Outlook Report"— but dealmakers continue to find creative solutions for growth

Highlights

Global PE deal activity experienced a significant slowdown in the first three quarters of 2022, with the number of deals falling 18% and value nearly halving from US$1.2 trillion to US$685 billion compared to the same period in 2021. However, the market share of private equity transactions as a proportion of global M&A activity has continued to steadily grow, reaching a record 23% as of Q3 2022, according to Refinitiv.

- PE fundraising dropped 16% by value and 30.6% in the number of funds closed through Q3 2022, compared with the same period in last year.

- 2021 was an outlier for PE dealmaking, but 2022 has already seen 2,081 buyouts in the US worth US$333.4bn in the first three quarters of the year— above the total value and volume of any full-year period in the decade before 2021.

- 37% of respondents believe retail access to PE vehicles will expand as an after effect of the COVID-19 crisis.

- 50% of respondents are now very likely to consider GP-led secondary transactions, a trend that 65% of respondents also see growing as an offshoot of the pandemic.

- 63% of PE firms are planning to make a GP-stake divestiture in the next 24 months.

- Take privates were the least favored deal choice among respondents, with over half either not very likely to consider a public-to-private option (26%), or reservedly saying it depends on the specific deal (26%). This in large part stems from the difficulty of financing these transactions despite the attractive valuations of many public companies.

- 51% of the respondents have increased their use of private credit to finance buyouts in the last three years.

- Divergence in market sentiment over liquidity in the next 12 months was shown. 82% of those from North America and 80% of respondents from EMEA have a favorable view, with only 45% of APAC respondents sharing a similar outlook.

NEW YORK, Nov. 28, 2022 /PRNewswire/ -- Rising leverage costs and volatile valuations driven by economic downturns and increasingly tight monetary policy are the greatest challenges facing the private equity industry, according to the 2023 Dechert Global Private Equity Outlook report.

The US, like other regions in 2022, saw the PE buyout market shift down a gear, with the number of transactions in the region declining by 15% and their aggregate value sinking 43% in the first nine months of the year, compared to the same period in 2021. In the US, the number of buyouts across this period totaled 2,081 with a value of US$333.4bn. Among PE leaders, this trajectory is expected to continue into 2023 and beyond, driven by tightening credit conditions and broader economic dislocation. On the bright side, the market share of buyouts as a proportion of overall M&A activity continues to grow with the percentage share approaching 25% in the Americas through Q3 2022, according to data from Refinitiv.

More than 40% of US respondents said valuation and economic uncertainties were among the top two challenges the PE industry faced. The data, published today, in association with Mergermarket, surveyed more than 100 senior-level executives within PE firms based in North America, EMEA, and Asia-Pacific (APAC). This is Dechert's 5th annual Global Private Equity report.

Despite this, the global volume of transactions remained surprisingly robust. General Partners (GP) remained highly active on all but the largest transactions: "There is always something going on in the middle market, whether it is new platform deals or add-on acquisitions. Even though the amount of capital being invested has fallen, private equity has really demonstrated its resilience," said Dr. Markus P. Bolsinger, co-head of Dechert's global private equity practice and partner in the firm's New York and Munich offices.

The current environment does provide opportunities, being particularly highly favorable to those sitting on dry powder, having access to private credit financings and taking a prudent approach. As bid levels are reined in, new transactions are being more honestly priced in comparison to the last decade where cheap debt and a superabundance of equity capital have made for frothy valuations.

Dechert is a leading global law firm with 22 offices around the world. Our global team advises private equity, private credit and other alternative asset managers on flexible solutions at every phase of the investment life cycle. We form funds structured for market terms and tax efficiency; negotiate investments and advise on transactions and financings that maximize value; and structure and execute exits accomplished at the right time and delivering the best returns.

Methodology: Mergermarket, on behalf of Dechert LLP, surveyed 100 senior-level executives within private equity (PE) firms based in North America (45%), EMEA (35%), and Asia-Pacific (20%). In order to qualify for inclusion, the firms all needed to have US$1bn or more in assets under management. The survey included a combination of qualitative and quantitative questions.

View original content to download multimedia:https://www.prnewswire.com/news-releases/private-equity-firms-expect-middle-market-dominance-in-2023-as-monetary-tightening-drives-deal-volumes-and-values-down-yet-fundraising-still-outstrips-pre-pandemic-levels-301687946.html

SOURCE Dechert LLP

Uncategorized

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

Share this:

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

vaccine pandemic covid-19Uncategorized

Q4 Update: Delinquencies, Foreclosures and REO

Today, in the Calculated Risk Real Estate Newsletter: Q4 Update: Delinquencies, Foreclosures and REO

A brief excerpt: I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened followi…

Share this:

A brief excerpt:

I’ve argued repeatedly that we would NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble). The two key reasons are mortgage lending has been solid, and most homeowners have substantial equity in their homes..There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ mortgage rates real estate mortgages pandemic interest rates

...

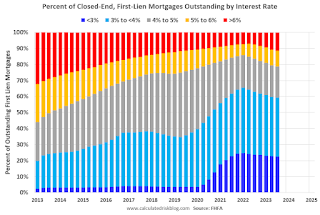

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q3 2023 (Q4 2023 data will be released in a two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 22.6% of loans are under 3%, 59.4% are under 4%, and 78.7% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Uncategorized

‘Bougie Broke’ – The Financial Reality Behind The Facade

‘Bougie Broke’ – The Financial Reality Behind The Facade

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming…

Share this:

{kind=link}

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

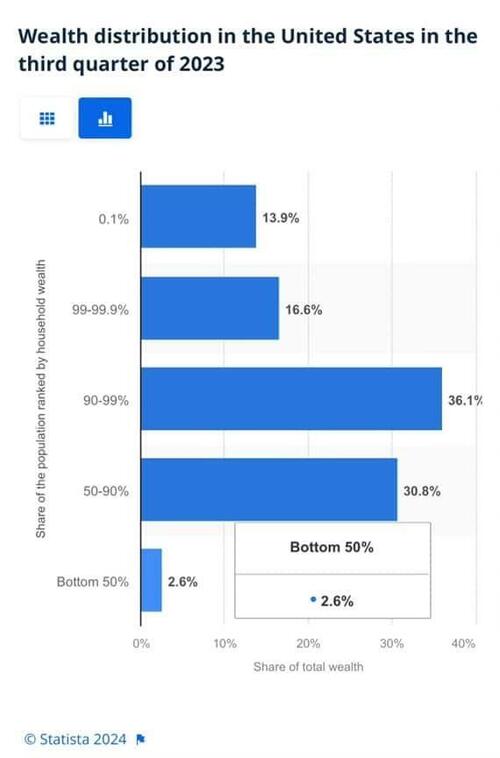

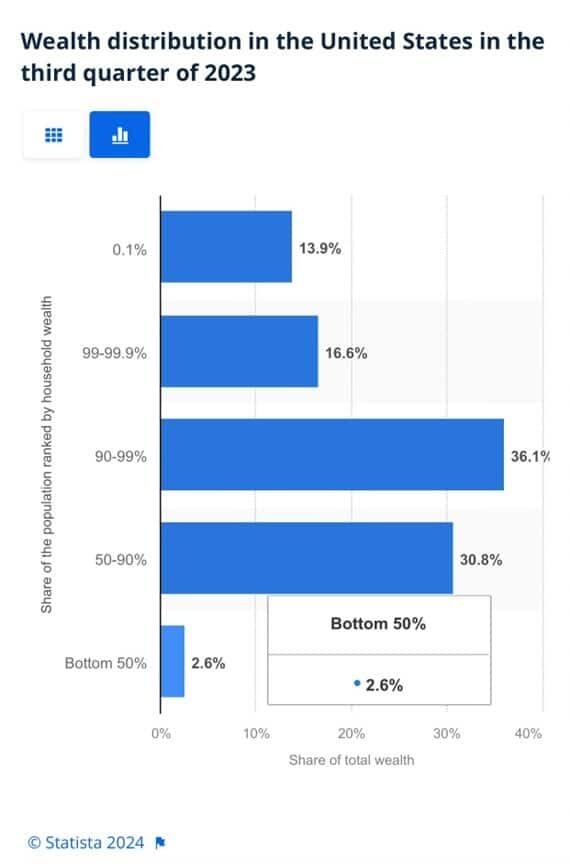

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottom half of the population accounts for less than 3% of the wealth.

{kind=link}

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

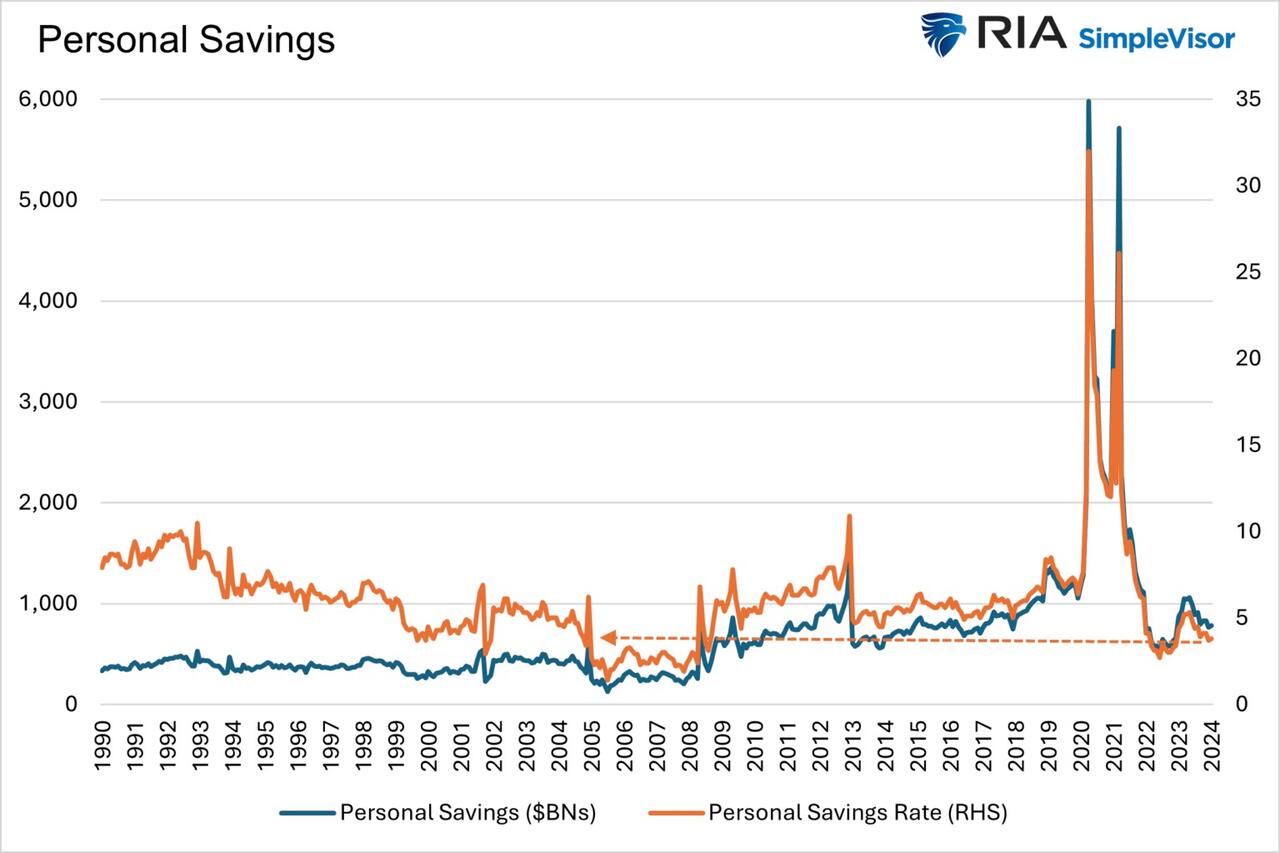

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

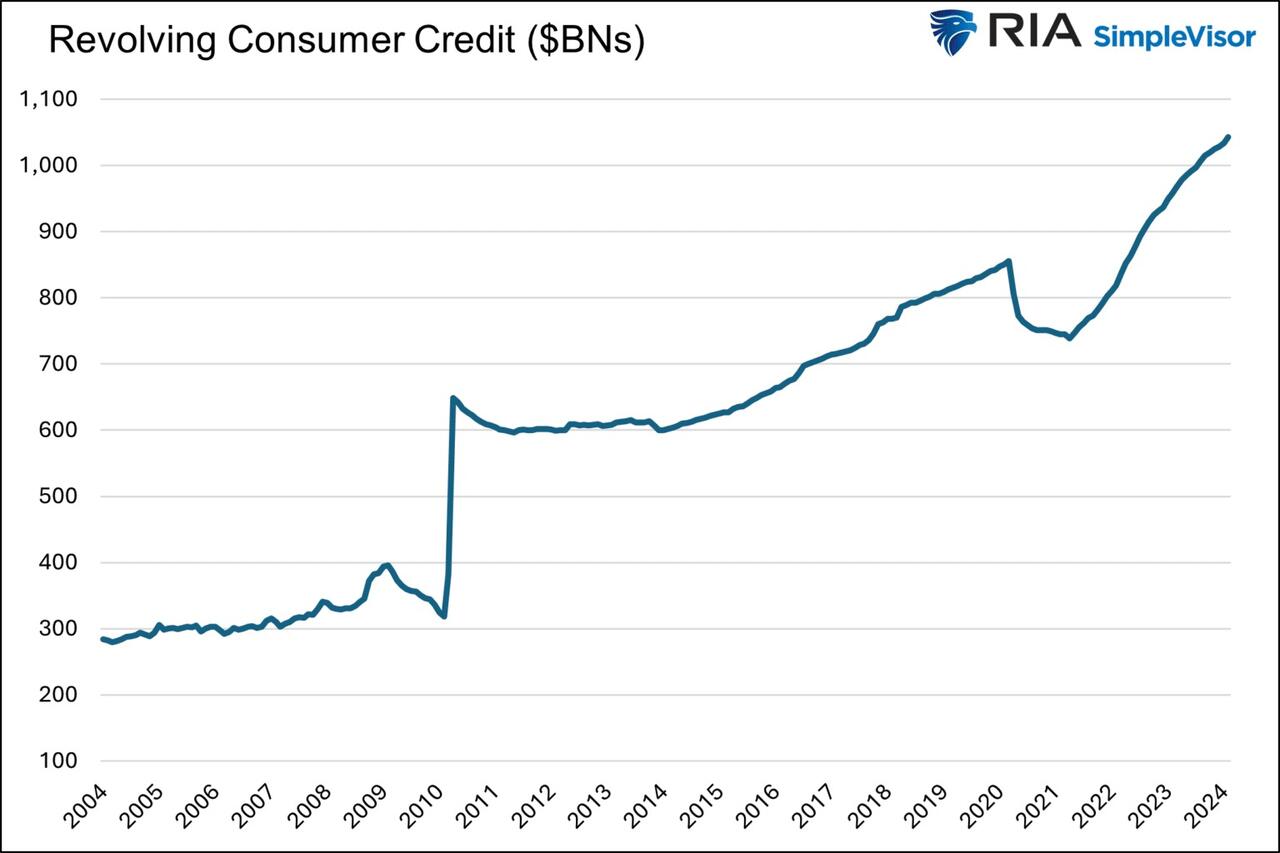

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

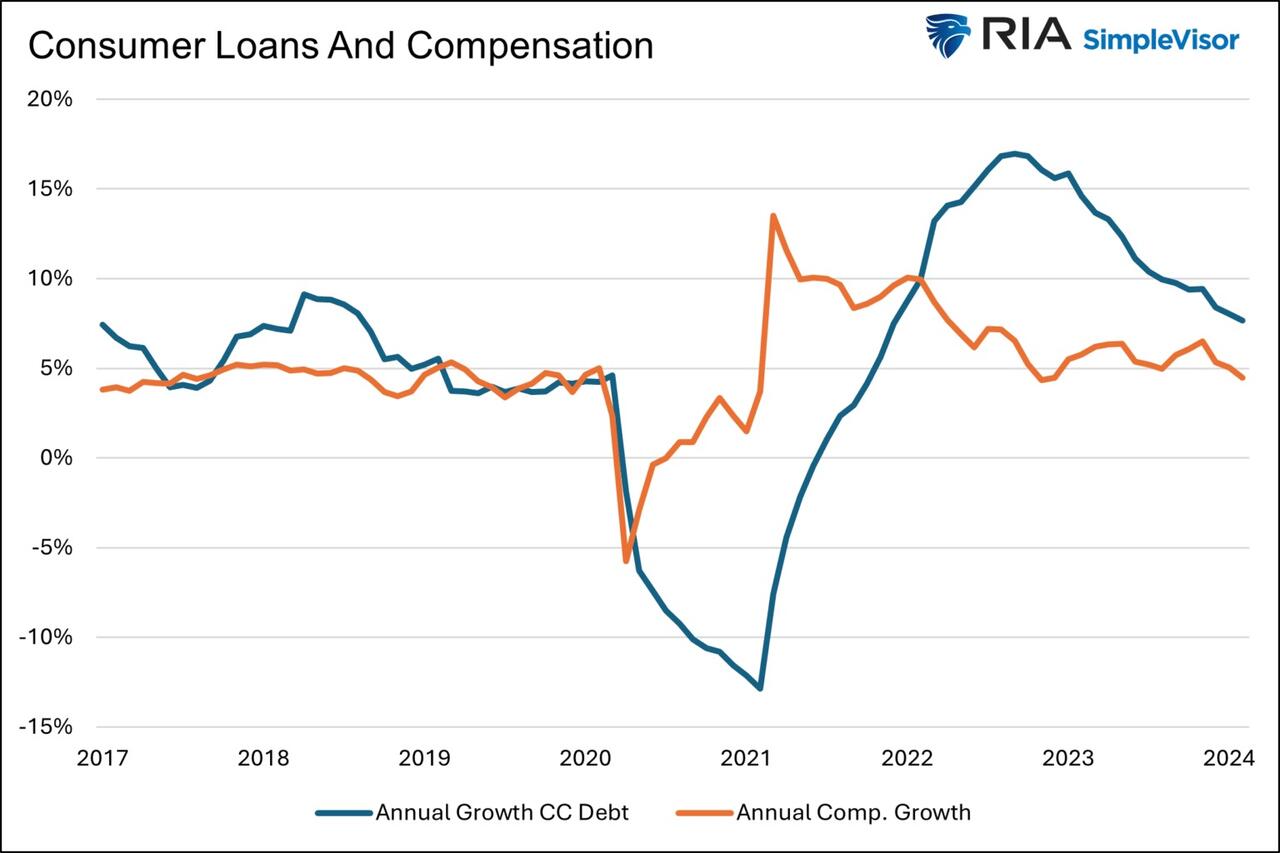

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

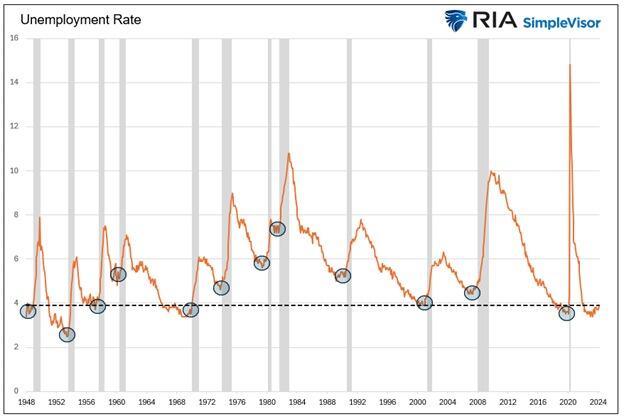

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

Q4 Update: Delinquencies, Foreclosures and REO

Digital Currency And Gold As Speculative Warnings

Bougie Broke The Financial Reality Behind The Facade

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Aging at AACR Annual Meeting 2024

Bitcoin on Wheels: The Story of Bitcoinetas

Futures Flat At All-Time High As Bitcoin Surges To Record, Oil Rises

The most potent labor market indicator of all is still strongly positive

‘Bougie Broke’ – The Financial Reality Behind The Facade

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges