Spread & Containment

On the hunt for the next Moderna, investors have pumped ‘platform plays’ with cash. Can anything slow the runaway train?

It didn’t take an expert to see that mRNA platforms could be huge.

Julie Sunderland partnered with both Moderna and BioNTech about a decade ago while she was running program-related investments for the Bill & Melinda Gates Foundation — and even…

Share this:

It didn’t take an expert to see that mRNA platforms could be huge.

Julie Sunderland partnered with both Moderna and BioNTech about a decade ago while she was running program-related investments for the Bill & Melinda Gates Foundation — and even then the potential for their platforms was obvious despite some well-founded concerns about whether the next-gen tech would ever cross the finish line.

“If you looked at the mRNA technology, it was very obvious that it had the potential to be transformative for vaccines,” said Sunderland, who splintered off from the Gates Foundation in 2016 to co-found Biomatics Capital Partners and is now its managing director.

She was right: After getting approval for the world’s first two mRNA vaccines, Moderna and BioNTech each pulled in more than a billion dollars in Q1. Moderna’s $MRNA stock, which sold for under $20 for most of 2019, is now flying at more than $200 apiece.

For possibly the first time, hundreds of millions of people are experiencing platform biotechnology first-hand. But for those who have been paying attention, the excitement around platform plays is nothing new. In fact, even before Moderna and BioNTech’s runaway wins with the Covid-19 vaccines, investors watched the fundamentals for this market build for years.

Platform companies have gone in and out of style over the last few decades, marked by periods when the market favored more asset-centric approaches. It used to be one of biotech investing’s big debates: Is it better to nurture the goose or focus on a few golden eggs?

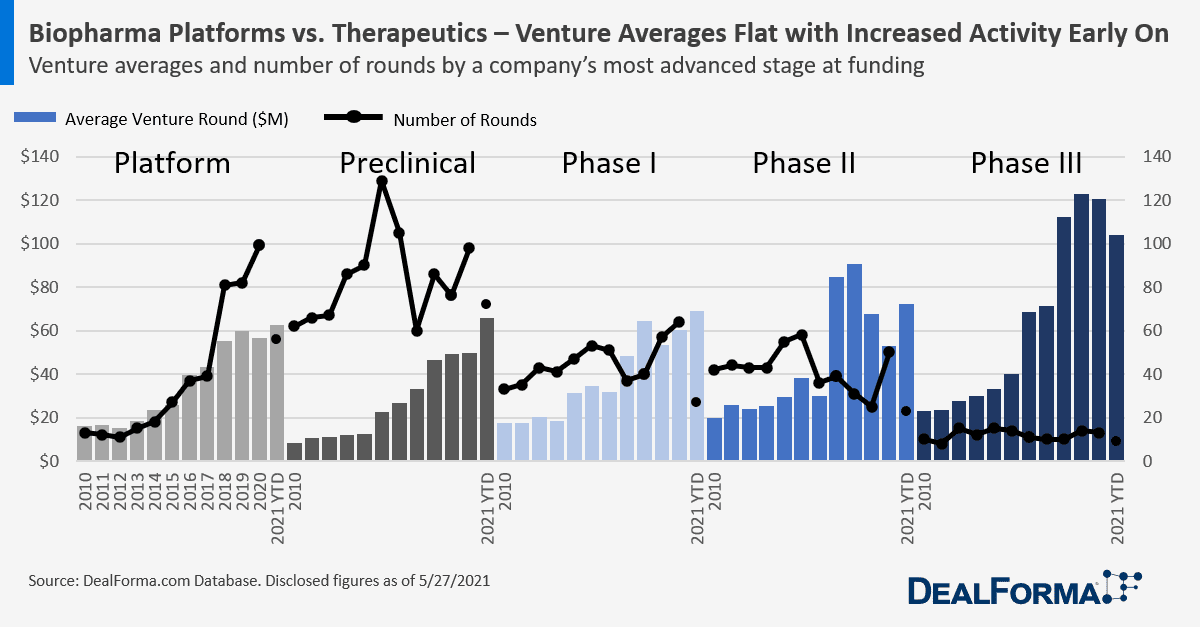

In the past several years, money has been flowing increasingly to the geese. Venture funding for platforms has been on the rise since about 2012, according to figures from DealForma, which defines “platform companies” as those that don’t yet have a compound discovered or are only developing the tech to discover new therapies. And since 2017, the number of IPOs going to platform plays has skyrocketed. According to DealForma, the average amount raised in platform company IPOs so far this year has been nearly $250 million.

Back in February, Sana Biotechnology’s cell engineering platform landed the company a whopping $587.5 million IPO, bringing its market value to roughly $4.6 billion — the highest market cap in history for a biotech without any programs in the clinic. And just last week, Lyell Immunopharma priced its shares at $17 apiece, pulling in a $425 million IPO to advance its platform tech for improving patients’ responses to cell therapies.

Simeon George

Simeon George“We didn’t need Moderna and BioNTech to tell us how exciting this was,” SR One Capital CEO Simeon George told Endpoints News. “For, you know, dyed in the wool investors or folks that are in life sciences, we’ve known this for a while now. It hasn’t changed our direction of travel at all.”

But the road hasn’t been without a few potholes. Platform companies can fail if they’re too slow to generate products, or if the platform becomes established by other companies, according to Stelios Papadopoulos, who co-founded Exelixis back in 1994 and now serves as the chairman of Biogen. He pointed to Deltagen, which went public in April 2000 with its database of mammalian gene functions, only to file for bankruptcy two years later. Sienna Biopharmaceuticals went public in 2017 to develop topicals for skin problems like acne through two tech platforms. But after a drug-device combo for acne flopped in pivotal testing, the company’s story ended with a Chapter 11.

As with everything else in biopharma, trends come and go. But with so much institutional investment in platforms, is there anything that could slow this runaway train?

Varying definitions

What does it mean to be a platform company these days? The answer depends on who you ask, and it goes far beyond the traditional goose versus golden egg debate.

Atlas Venture partner Bruce Booth describes platform and asset-centric companies as two poles. On one end, you have drug discovery engines that produce a portfolio of products. At the other end, you have product plays. These could be collections of products that have been in-licensed or brought in, but you’re still missing that engine that’s going to keep producing new medicines.

Bruce Booth

Bruce BoothWhere it gets complicated, Booth said, is that there’s plenty of space in between these two poles.

“We’ve played up and down that continuum the whole time,” he said of Atlas.

Geoffrey von Maltzahn, general partner at Flagship Pioneering and CEO of Tessera, would break it down even further: “I think every biotech company would state they have a platform of some kind,” he said.

Within the platform realm, he sees two distinct models. There are companies boasting a technological capability, and those with what he calls a “biological inquiry capability.” Tech platforms are straightforward — think Moderna’s mRNA platform, or Sana’s engineered-cell platform. On the latter end, you have companies like Cygnal Therapeutics — a startup out of Flagship, the same incubator from whence Moderna sprang — where the platform is its exploration of the exoneural biology.

Laronde CEO Diego Miralles said “programmable platforms” are up-and-coming. These are platforms like his company’s eRNA work or Moderna’s mRNA programs, in which all you need to do is “change the code” to get new products. He compared the model to CDs, where the CD player is the body, and the platform is the CD.

Diego Miralles

Diego Miralles“All the CDs look the same — effectively, all you need to do is change the code and sometimes you can have one song, sometimes you can have two songs on the same CD,” he said.

In the 1990s, there was a trend toward platforms that were drug development tools. These are what Booth calls “picks and shovels platforms,” like ArQule, which was doing combinatorial chemistry and selling its libraries to Big Pharma.

“The tools platforms (of) the 90s, you tend not to see as much of anymore. You see folks applying tools to make drugs,” he said. It’s all about that pathway to a product.

If you ask Sunderland, platform technologies don’t exist. And while some consider Moderna a shining example of what platforms have to offer, she sees the company as a product play.

Geoffrey von Maltzahn

Geoffrey von Maltzahn“I really dislike the platform versus product framing, because I think it’s a little bit of a false dichotomy,” she said. “A platform is at the end of the day, potentially a series of products, but it’s always products … To me there’s no such thing as a platform technology, because we’re always developing products.”

Moderna isn’t valuable because it’s a platform, Sunderland argues. It’s valuable because Stéphane Bancel and his team worked hard to develop useful products for patients.

For our purposes, von Maltzahn distilled his idea of a platform down to this: some capability that allows you to repeatedly create products of value, where a single success increases your probability of success across future endeavors.

In and out of style — then back in again

In the mid-1990s, platform companies were “almost everything in biotech,” Booth told Endpoints. There was genetics work being done at deCODE, combinatorial chemistry at ArQule, and functional genomics at Exelixis. Platforms eat up lots of cash, so in order to flourish, they need equity capital markets to be open and flowing into those kinds of ventures. And in the ’90s, that was certainly the case.

The Human Genome Project launched in 1990, and new genomics firms began cropping up shortly after that. Private funding for biomedical R&D skyrocketed, surpassing public and nonprofit funding in the early ’90s — and in genomics, that rise was even more pronounced, according to a publication in Genome Medicine. There was also a general excitement around lots of then-new technologies, like high-throughput screening, combinatorial chemistry and transgenic models, Booth said. Biotechnology was looking to some investors like the next Internet, according to a piece Papadopoulos wrote in Nature.

“Biotech also moved increasingly into the limelight with investors in the 1990s,” Booth said.

By 2000, the global market cap for public genomics companies topped $84 billion. That year was a record one for biotech financing, with 63 IPOs completed. But what goes up must come down. The genomics bubble burst, knocking down valuations of the top 15 firms five-fold. Things tightened for the whole industry, and those “picks and shovels” platform companies like ArQule had to retool as product companies, Booth said.

This coincided with the rise of the specialty pharma model — “spec pharma” for short — around in-licensing drugs or reformulating and repurposing older compounds.

“It was really about a drug in Phase II or III, and that’s what the capital markets got excited by,” Booth said.

Prices started collapsing at the end of 2000, and into 2001 and 2002, according to Papadopoulos. And they went down even more for platform companies, compared to product companies, he said. The market was recalibrating itself, and because platform companies had the most exaggerated valuations in the year 2000, they corrected proportionately more than the others.

Stelios Papadapoulos

Stelios Papadapoulos“That probably told people, as the market came back in 2003, that they’d be better off investing in product-related companies rather than platform companies,” he added.

Along with fanny packs and low-rise jeans, drug discovery platforms went out of style. deCODE, which first hit Wall Street in 2000, filed for bankruptcy protection in 2009 and re-emerged as a private company before getting snapped up by Amgen in 2012. Merck struck a $2.7 billion deal for ArQule in 2019, with its eyes on ARQ 531, a BTK inhibitor that showed early-stage promise in patients with B cell malignancies.

Papadopoulos called this period the “lost decade.” By the end of 2002, many companies that had gone public in 2000 were trading below the IPO price, he said. And there were hardly any aspirational companies making the jump to Wall Street.

“The vast majority of companies trying to go public were some kind of a repurposed drug, or you know, some Phase II, some drug delivery methodology on top of an old drug,” he said.

In 2009, there were just three biotech IPOs, all of which occurred in the second half of the year. In 2020, it wasn’t uncommon to see that many in a week.

Add to that the financial crisis starting in 2007, and that sums up the “lost decade,” Papadopoulos said: “Nothing really exciting happened.”

Though not much platform work was being done between 2002 and 2012, some VC firms continued to build those models, including Atlas, which put together Alnylam — the “quintessential biotech platform story,” according to Booth. That company, which was founded in 2002 to explore the realm of RNA interference, developed the first approved drugs in the class.

Then around 2012-13, the equity markets opened back up. And in the past seven years or so, Booth has noticed a climbing interest in platform companies. The majority of companies that went public in 2012 had Phase II, III or even marketed products, Booth said. Whereas today, IPOs are increasingly going to Phase I or preclinical stage companies, most of which are big platform companies selling the promise of making lots of new medicines, he observed.

“I’d say it’s been a crescendo that has happened because of years of just increasing volume around the enthusiasm for innovation,” Booth said. “This isn’t something that a 2020 switch was flipped and all of a sudden biotech was interesting. This has really, really been eight-plus years of just an amazing bull market.”

von Maltzahn put it this way: “The past 10 years has certainly been the start of the heyday of biotech platforms.” Note his use of the word “start.”

What are investors looking for?

For investors, it’s all about a path to market, Papadopoulos says. Does the platform readily generate a product? Can you sell a billion dollars worth of goods based on what you have? Or is it just a tool?

If it’s a tool, that’s okay, Sunderland said. But “you damn well better be enabling or partnering with somebody who knows how to develop drugs for patients,” she added.

“There are companies that are using computer technology, data tools to enhance the R&D process and that is a good thing, because there’s a ton of inefficiencies in the R&D process that can be enhanced by data and analytics,” she said. “However, just doing that for the sake of doing it is not useful.”

Julie Sunderland

Julie SunderlandEven then, you run the risk of that service becoming irrelevant. “No one’s going to want to put a whole lot of money in a tool, which by the way the tool, mathematically certainly again will become redundant and irrelevant at some point,” Papadopoulos said.

Remember restriction fragment length polymorphisms, or RFLPs? Probably not unless you’re 60 or older, Papadopoulos joked, adding that the early molecular markers developed for genetic mapping were phased out once whole exome sequencing became available.

The distinction between tool and product grows more complicated when you get into gene therapies, Sunderland said. The product could be an edit, a payload, or a way to insert the cell. It’s a new way to understand biology, or a better way to discover therapeutics.

Sunderland cited Tillman Gerngross’ Adimab as a “classic business model” that’s fueled by partnerships rather than an internal pipeline. The company, founded in 2007, has inked more than 80 partnerships for its antibody discovery and engineering services, from Big Pharmas — like Merck, GlaxoSmithKline and Eli Lilly — to small startups. According to Gerngross, 2020 was the third year in a row that saw more than 10 Adimab antibodies enter the clinic.

“Antibody discovery is cheap compared to the cost of manufacturing and clinical development. Why build an entire development program on a questionable foundation?” Guy Van Meter, Adimab’s chief business officer, said in a statement back in February.

Part of the reason why platforms are so popular now is because we’re in a long investment horizon, and people can dream, Papadopoulos said. A perfect example of that is Laronde, which formally launched in May with a $50 million check from Flagship and a mission to make eRNA therapeutics.

eRNA — that’s “e” for “endless” — traces back to a circular class of naturally occurring RNA called lncRNA, or long non-coding RNA. Unlike mRNA, which can only produce proteins that last days, Laronde thinks eRNA can produce the same proteins for weeks to months without tripping the innate immune system or exonuclease enzymes over time. And it’s making some big promises. By 2031, Laronde says it can use its platform to create 100 drugs across a broad range of diseases. But does it have a clear path to market?

Miralles says the team will first set out to best other protein-based therapeutics, which may be suboptimal because they need to be administered frequently or are difficult to manufacture. They haven’t yet announced when they plan to enter the clinic.

“When you have a platform of the breadth of eRNA, you want to build that platform, so then you start selecting the many things you can do rather than rushing to the clinic with one program,” he said. “Because remember the value that you are creating is around the possibility of doing so many different things. ”

To Booth, the key is finding that first “killer application.” What will be truly distinctive, either because it’s first-in-class, or because it tops other existing drugs?

“Target selection is just a huge part of the future success,” he said. “You can think about it like you’re coding the early DNA of the company. And you don’t want to put a bunch of mutations into the DNA early on, because they can express themselves in bad ways. You waste a lot of money chasing things you shouldn’t.”

When Venrock partner Racquel Bracken was helping build Federation Bio, she didn’t pull the trigger until she was sure the team had an interesting platform — in this case, designing engineered or naturally occurring microbial communities to treat diseases like secondary hyperoxaluria — and a couple indications to focus on.

Racquel Bracken

Racquel Bracken“We think there’s a straightforward clinical development plan and we think there’s a big population, kind of at the end of the rainbow that matters,” she said. “And it wasn’t until we kind of landed on those key diseases and indications and built a plan around that that we said, ‘Okay, we’re ready to launch.’”

What about Alnylam, the RNAi company that launched during the platform dark period? They’ve now got three approved drugs on the market, and a potential fourth on the way. The company’s shares $ALNY, which priced at $6 apiece when it went public in 2004, are now selling for around $170.

“The reality of biotech is it takes a long time. And no matter what you work on, you’re gonna put thousands and thousands of hours of your life into it,” von Maltzahn said. “The virtue of building a platform where you have conviction that it can create very valuable products, do so repeatedly, and the essence of your platform empowers you with a rate of innovation that is very advantaged, is that the probability that you’re using your time wisely, and then you’ll have an impact on the world … is markedly increased relative to the one program at a time risk.”

Fad or here to stay?

Booth doesn’t see platforms going anywhere — at least not anytime soon.

“I think we’re going to continue to see ample funding flows into platform companies, especially because even if the IPO markets are cooling off, the private markets remain very, very strong,” he said. “It’s a great time to start platform companies.”

George says the popularity of platform plays will be dependent on a few things, including continued innovation that’s “pushing the envelope” with respect to new platforms or new ways to adopt existing platforms. And platforms will have to prove their worth through clinical data.

“It’s a self-fulfilling prophecy,” he said, adding that there could be an ebb and flow in the market’s receptiveness to platform plays. “If those novel technologies don’t translate into meaningful clinical innovation, ultimately, the markets and investors and pharma companies will not reward that.”

One thing is for certain, though, von Maltzahn said: “Many of the best and most impactful biotech companies, life science companies, have not been started yet.”

bankruptcy covid-19 testing preclinical genome genetic antibodies rna dnaInternational

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

The crisis in NHS dentistry is driving increasing numbers abroad for treatment. Here are some of their stories.

Share this:

It’s a hot summer day in the Turkish city of Antalya, a Mediterranean resort with golden beaches, deep blue sea and vibrant nightlife. The pool area of the all-inclusive resort is crammed with British people on sun loungers – but they aren’t here for a holiday. This hotel is linked to a dental clinic that organises treatment packages, and most of these guests are here to see a dentist.

From Norwich, two women talk about gums and injections. A man from Wales holds a tissue close to his mouth and spits blood – he has just had two molars extracted.

The dental clinic organises everything for these dental “tourists” throughout their treatment, which typically lasts from three to 15 days. The stories I hear of what has caused them to travel to Turkey are strikingly similar: all have struggled to secure dental treatment at home on the NHS.

“The hotel is nice and some days I go to the beach,” says Susan*, a hairdresser in her mid-30s from Norwich. “But really, we aren’t tourists like in a proper holiday. We come here because we have no choice. I couldn’t stand the pain.”

This is Susan’s second visit to Antalya. She explains that her ordeal started two years earlier:

I went to an NHS dentist who told me I had gum disease … She did some cleaning to my teeth and gums but it got worse. When I ate, my teeth were moving … the gums were bleeding and it was very painful. I called to say I was in pain but the clinic was not accepting NHS patients any more.

The only option the dentist offered Susan was to register as a private patient:

I asked how much. They said £50 for x-rays and then if the gum disease got worse, £300 or so for extraction. Four of them were moving – imagine: £1,200 for losing your teeth! Without teeth I’d lose my clients, but I didn’t have the money. I’m a single mum. I called my mum and cried.

Susan’s mother told her about a friend of hers who had been to Turkey for treatment, then together they found a suitable clinic:

The prices are so much cheaper! Tooth extraction, x-rays, consultations – it all comes included. The flight and hotel for seven days cost the same as losing four teeth in Norwich … I had my lower teeth removed here six months ago, now I’ve got implants … £2,800 for everything – hotel, transfer, treatments. I only paid the flights separately.

In the UK, roughly half the adult population suffers from periodontitis – inflammation of the gums caused by plaque bacteria that can lead to irreversible loss of gums, teeth, and bone. Regular reviews by a dentist or hygienist are required to manage this condition. But nine out of ten dental practices cannot offer NHS appointments to new adult patients, while eight in ten are not accepting new child patients.

Some UK dentists argue that Britons who travel abroad for treatment do so mainly for cosmetic procedures. They warn that dental tourism is dangerous, and that if their treatment goes wrong, dentists in the UK will be unable to help because they don’t want to be responsible for further damage. Susan shrugs this off:

Dentists in England say: ‘If you go to Turkey, we won’t touch you [afterwards].’ But I don’t worry because there are no appointments at home anyway. They couldn’t help in the first place, and this is why we are in Turkey.

‘How can we pay all this money?’

As a social anthropologist, I travelled to Turkey a number of times in 2023 to investigate the crisis of NHS dentistry, and the journeys abroad that UK patients are increasingly making as a result. I have relatives in Istanbul and have been researching migration and trading patterns in Turkey’s largest city since 2016.

In August 2023, I visited the resort in Antalya, nearly 400 miles south of Istanbul. As well as Susan, I met a group from a village in Wales who said there was no provision of NHS dentistry back home. They had organised a two-week trip to Turkey: the 12-strong group included a middle-aged couple with two sons in their early 20s, and two couples who were pensioners. By going together, Anya tells me, they could support each other through their different treatments:

I’ve had many cavities since I was little … Before, you could see a dentist regularly – you didn’t even think about it. If you had pain or wanted a regular visit, you phoned and you went … That was in the 1990s, when I went to the dentist maybe every year.

Anya says that once she had children, her family and work commitments meant she had no time to go to the dentist. Then, years later, she started having serious toothache:

Every time I chewed something, it hurt. I ate soups and soft food, and I also lost weight … Even drinking was painful – tea: pain, cold water: pain. I was taking paracetamol all the time! I went to the dentist to fix all this, but there were no appointments.

Anya was told she would have to wait months, or find a dentist elsewhere:

A private clinic gave me a list of things I needed done. Oh my God, almost £6,000. My husband went too – same story. How can we pay all this money? So we decided to come to Turkey. Some people we know had been here, and others in the village wanted to come too. We’ve brought our sons too – they also need to be checked and fixed. Our whole family could be fixed for less than £6,000.

By the time they travelled, Anya’s dental problems had turned into a dental emergency. She says she could not live with the pain anymore, and was relying on paracetamol.

In 2023, about 6 million adults in the UK experienced protracted pain (lasting more than two weeks) caused by toothache. Unintentional paracetamol overdose due to dental pain is a significant cause of admissions to acute medical units. If left untreated, tooth infections can spread to other parts of the body and cause life-threatening complications – and on rare occasions, death.

In February 2024, police were called to manage hundreds of people queuing outside a newly opened dental clinic in Bristol, all hoping to be registered or seen by an NHS dentist. One in ten Britons have admitted to performing “DIY dentistry”, of which 20% did so because they could not find a timely appointment. This includes people pulling out their teeth with pliers and using superglue to repair their teeth.

In the 1990s, dentistry was almost entirely provided through NHS services, with only around 500 solely private dentists registered. Today, NHS dentist numbers in England are at their lowest level in a decade, with 23,577 dentists registered to perform NHS work in 2022-23, down 695 on the previous year. Furthermore, the precise division of NHS and private work that each dentist provides is not measured.

The COVID pandemic created longer waiting lists for NHS treatment in an already stretched public service. In Bridlington, Yorkshire, people are now reportedly having to wait eight-to-nine years to get an NHS dental appointment with the only remaining NHS dentist in the town.

In his book Patients of the State (2012), Argentine sociologist Javier Auyero describes the “indignities of waiting”. It is the poor who are mostly forced to wait, he writes. Queues for state benefits and public services constitute a tangible form of power over the marginalised. There is an ethnic dimension to this story, too. Data suggests that in the UK, patients less likely to be effective in booking an NHS dental appointment are non-white ethnic groups and Gypsy or Irish travellers, and that it is particularly challenging for refugees and asylum-seekers to access dental care.

This article is part of Conversation Insights

The Insights team generates long-form journalism derived from interdisciplinary research. The team is working with academics from different backgrounds who have been engaged in projects aimed at tackling societal and scientific challenges.

In 2022, I experienced my own dental emergency. An infected tooth was causing me debilitating pain, and needed root canal treatment. I was advised this would cost £71 on the NHS, plus £307 for a follow-up crown – but that I would have to wait months for an appointment. The pain became excruciating – I could not sleep, let alone wait for months. In the same clinic, privately, I was quoted £1,300 for the treatment (more than half my monthly income at the time), or £295 for a tooth extraction.

I did not want to lose my tooth because of lack of money. So I bought a flight to Istanbul immediately for the price of the extraction in the UK, and my tooth was treated with root canal therapy by a private dentist there for £80. Including the costs of travelling, the total was a third of what I was quoted to be treated privately in the UK. Two years on, my treated tooth hasn’t given me any more problems.

A better quality of life

Not everyone is in Antalya for emergency procedures. The pensioners from Wales had contacted numerous clinics they found on the internet, comparing prices, treatments and hotel packages at least a year in advance, in a carefully planned trip to get dental implants – artificial replacements for tooth roots that help support dentures, crowns and bridges.

In Turkey, all the dentists I speak to (most of whom cater mainly for foreigners, including UK nationals) consider implants not a cosmetic or luxurious treatment, but a development in dentistry that gives patients who are able to have the procedure a much better quality of life. This procedure is not available on the NHS for most of the UK population, and the patients I meet in Turkey could not afford implants in private clinics back home.

Paul is in Antalya to replace his dentures, which have become uncomfortable and irritating to his gums, with implants. He says he couldn’t find an appointment to see an NHS dentist. His wife Sonia went through a similar procedure the year before and is very satisfied with the results, telling me: “Why have dentures that you need to put in a glass overnight, in the old style? If you can have implants, I say, you’re better off having them.”

Most of the dental tourists I meet in Antalya are white British: this city, known as the Turkish Riviera, has developed an entire economy catering to English-speaking tourists. In 2023, more than 1.3 million people visited the city from the UK, up almost 15% on the previous year.

Read more: NHS dentistry is in crisis – are overseas dentists the answer?

In contrast, the Britons I meet in Istanbul are predominantly from a non-white ethnic background. Omar, a pensioner of Pakistani origin in his early 70s, has come here after waiting “half a year” for an NHS appointment to fix the dental bridge that is causing him pain. Omar’s son had been previously for a hair transplant, and was offered a free dental checkup by the same clinic, so he suggested it to his father. Having worked as a driver for a manufacturing company for two decades in Birmingham, Omar says he feels disappointed to have contributed to the British economy for so long, only to be “let down” by the NHS:

At home, I must wait and wait and wait to get a bridge – and then I had many problems with it. I couldn’t eat because the bridge was uncomfortable and I was in pain, but there were no appointments on the NHS. I asked a private dentist and they recommended implants, but they are far too expensive [in the UK]. I started losing weight, which is not a bad thing at the beginning, but then I was worrying because I couldn’t chew and eat well and was losing more weight … Here in Istanbul, I got dental implants – US$500 each, problem solved! In England, each implant is maybe £2,000 or £3,000.

In the waiting area of another clinic in Istanbul, I meet Mariam, a British woman of Iraqi background in her late 40s, who is making her second visit to the dentist here. Initially, she needed root canal therapy after experiencing severe pain for weeks. Having been quoted £1,200 in a private clinic in outer London, Mariam decided to fly to Istanbul instead, where she was quoted £150 by a dentist she knew through her large family. Even considering the cost of the flight, Mariam says the decision was obvious:

Dentists in England are so expensive and NHS appointments so difficult to find. It’s awful there, isn’t it? Dentists there blamed me for my rotten teeth. They say it’s my fault: I don’t clean or I ate sugar, or this or that. I grew up in a village in Iraq and didn’t go to the dentist – we were very poor. Then we left because of war, so we didn’t go to a dentist … When I arrived in London more than 20 years ago, I didn’t speak English, so I still didn’t go to the dentist … I think when you move from one place to another, you don’t go to the dentist unless you are in real, real pain.

In Istanbul, Mariam has opted not only for the urgent root canal treatment but also a longer and more complex treatment suggested by her consultant, who she says is a renowned doctor from Syria. This will include several extractions and implants of back and front teeth, and when I ask what she thinks of achieving a “Hollywood smile”, Mariam says:

Who doesn’t want a nice smile? I didn’t come here to be a model. I came because I was in pain, but I know this doctor is the best for implants, and my front teeth were rotten anyway.

Dentists in the UK warn about the risks of “overtreatment” abroad, but Mariam appears confident that this is her opportunity to solve all her oral health problems. Two of her sisters have already been through a similar treatment, so they all trust this doctor.

The UK’s ‘dental deserts’

To get a fuller understanding of the NHS dental crisis, I’ve also conducted 20 interviews in the UK with people who have travelled or were considering travelling abroad for dental treatment.

Joan, a 50-year-old woman from Exeter, tells me she considered going to Turkey and could have afforded it, but that her back and knee problems meant she could not brave the trip. She has lost all her lower front teeth due to gum disease and, when I meet her, has been waiting 13 months for an NHS dental appointment. Joan tells me she is living in “shame”, unable to smile.

In the UK, areas with extremely limited provision of NHS dental services – known as as “dental deserts” – include densely populated urban areas such as Portsmouth and Greater Manchester, as well as many rural and coastal areas.

In Felixstowe, the last dentist taking NHS patients went private in 2023, despite the efforts of the activist group Toothless in Suffolk to secure better access to NHS dentists in the area. It’s a similar story in Ripon, Yorkshire, and in Dumfries & Galloway, Scotland, where nearly 25,000 patients have been de-registered from NHS dentists since 2021.

Data shows that 2 million adults must travel at least 40 miles within the UK to access dental care. Branding travel for dental care as “tourism” carries the risk of disguising the elements of duress under which patients move to restore their oral health – nationally and internationally. It also hides the immobility of those who cannot undertake such journeys.

The 90-year-old woman in Dumfries & Galloway who now faces travelling for hours by bus to see an NHS dentist can hardly be considered “tourism” – nor the Ukrainian war refugees who travelled back from West Sussex and Norwich to Ukraine, rather than face the long wait to see an NHS dentist.

Many people I have spoken to cannot afford the cost of transport to attend dental appointments two hours away – or they have care responsibilities that make it impossible. Instead, they are forced to wait in pain, in the hope of one day securing an appointment closer to home.

‘Your crisis is our business’

The indignities of waiting in the UK are having a big impact on the lives of some local and foreign dentists in Turkey. Some neighbourhoods are rapidly changing as dental and other health clinics, usually in luxurious multi-storey glass buildings, mushroom. In the office of one large Istanbul medical complex with sections for hair transplants and dentistry (plus one linked to a hospital for more extensive cosmetic surgery), its Turkish owner and main investor tells me:

Your crisis is our business, but this is a bazaar. There are good clinics and bad clinics, and unfortunately sometimes foreign patients do not know which one to choose. But for us, the business is very good.

This clinic only caters to foreign patients. The owner, an architect by profession who also developed medical clinics in Brazil, describes how COVID had a major impact on his business:

When in Europe you had COVID lockdowns, Turkey allowed foreigners to come. Many people came for ‘medical tourism’ – we had many patients for cosmetic surgery and hair transplants. And that was when the dental business started, because our patients couldn’t see a dentist in Germany or England. Then more and more patients started to come for dental treatments, especially from the UK and Ireland. For them, it’s very, very cheap here.

The reasons include the value of the Turkish lira relative to the British pound, the low cost of labour, the increasing competition among Turkish clinics, and the sheer motivation of dentists here. While most dentists catering to foreign patients are from Turkey, others have arrived seeking refuge from war and violence in Syria, Iraq, Afghanistan, Iran and beyond. They work diligently to rebuild their lives, careers and lost wealth.

Regardless of their origin, all dentists in Turkey must be registered and certified. Hamed, a Syrian dentist and co-owner of a new clinic in Istanbul catering to European and North American patients, tells me:

I know that you say ‘Syrian’ and people think ‘migrant’, ‘refugee’, and maybe think ‘how can this dentist be good?’ – but Syria, before the war, had very good doctors and dentists. Many of us came to Turkey and now I have a Turkish passport. I had to pass the exams to practise dentistry here – I study hard. The exams are in Turkish and they are difficult, so you cannot say that Syrian doctors are stupid.

Hamed talks excitedly about the latest technology that is coming to his profession: “There are always new materials and techniques, and we cannot stop learning.” He is about to travel to Paris to an international conference:

I can say my techniques are very advanced … I bet I put more implants and do more bone grafting and surgeries every week than any dentist you know in England. A good dentist is about practice and hand skills and experience. I work hard, very hard, because more and more patients are arriving to my clinic, because in England they don’t find dentists.

While there is no official data about the number of people travelling from the UK to Turkey for dental treatment, investors and dentists I speak to consider that numbers are rocketing. From all over the world, Turkey received 1.2 million visitors for “medical tourism” in 2022, an increase of 308% on the previous year. Of these, about 250,000 patients went for dentistry. One of the most renowned dental clinics in Istanbul had only 15 British patients in 2019, but that number increased to 2,200 in 2023 and is expected to reach 5,500 in 2024.

Like all forms of medical care, dental treatments carry risks. Most clinics in Turkey offer a ten-year guarantee for treatments and a printed clinical history of procedures carried out, so patients can show this to their local dentists and continue their regular annual care in the UK. Dental treatments, checkups and maintaining a good oral health is a life-time process, not a one-off event.

Many UK patients, however, are caught between a rock and a hard place – criticised for going abroad, yet unable to get affordable dental care in the UK before and after their return. The British Dental Association has called for more action to inform these patients about the risks of getting treated overseas – and has warned UK dentists about the legal implications of treating these patients on their return. But this does not address the difficulties faced by British patients who are being forced to go abroad in search of affordable, often urgent dental care.

A global emergency

The World Health Organization states that the explosion of oral disease around the world is a result of the “negligent attitude” that governments, policymakers and insurance companies have towards including oral healthcare under the umbrella of universal healthcare. It as if the health of our teeth and mouth is optional; somehow less important than treatment to the rest of our body. Yet complications from untreated tooth decay can lead to hospitalisation.

The main causes of oral health diseases are untreated tooth decay, severe gum disease, toothlessness, and cancers of the lip and oral cavity. Cases grew during the pandemic, when little or no attention was paid to oral health. Meanwhile, the global cosmetic dentistry market is predicted to continue growing at an annual rate of 13% for the rest of this decade, confirming the strong relationship between socioeconomic status and access to oral healthcare.

In the UK since 2018, there have been more than 218,000 admissions to hospital for rotting teeth, of which more than 100,000 were children. Some 40% of children in the UK have not seen a dentist in the past 12 months. The role of dentists in prevention of tooth decay and its complications, and in the early detection of mouth cancer, is vital. While there is a 90% survival rate for mouth cancer if spotted early, the lack of access to dental appointments is causing cases to go undetected.

The reasons for the crisis in NHS dentistry are complex, but include: the real-term cuts in funding to NHS dentistry; the challenges of recruitment and retention of dentists in rural and coastal areas; pay inequalities facing dental nurses, most of them women, who are being badly hit by the cost of living crisis; and, in England, the 2006 Dental Contract that does not remunerate dentists in a way that encourages them to continue seeing NHS patients.

The UK is suffering a mass exodus of the public dentistry workforce, with workers leaving the profession entirely or shifting to the private sector, where payments and life-work balance are better, bureaucracy is reduced, and prospects for career development look much better. A survey of general dental practitioners found that around half have reduced their NHS work since the pandemic – with 43% saying they were likely to go fully private, and 42% considering a career change or taking early retirement.

Reversing the UK’s dental crisis requires more commitment to substantial reform and funding than the “recovery plan” announced by Victoria Atkins, the secretary of state for health and social care, on February 7.

The stories I have gathered show that people travelling abroad for dental treatment don’t see themselves as “tourists” or vanity-driven consumers of the “Hollywood smile”. Rather, they have been forced by the crisis in NHS dentistry to seek out a service 1,500 miles away in Turkey that should be a basic, affordable right for all, on their own doorstep.

*Names in this article have been changed to protect the anonymity of the interviewees.

For you: more from our Insights series:

GP crisis: how did things go so wrong, and what needs to change?

Insomnia: how chronic sleep problems can lead to a spiralling decline in mental health

To hear about new Insights articles, join the hundreds of thousands of people who value The Conversation’s evidence-based news. Subscribe to our newsletter.

Diana Ibanez Tirado receives funding from the School of Global Studies, University of Sussex.

pound pandemic treatment therapy spread recovery iran brazil european europe uk germany ukraine world health organizationSpread & Containment

The Coming Of The Police State In America

The Coming Of The Police State In America

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now…

Share this:

Authored by Jeffrey Tucker via The Epoch Times,

The National Guard and the State Police are now patrolling the New York City subway system in an attempt to do something about the explosion of crime. As part of this, there are bag checks and new surveillance of all passengers. No legislation, no debate, just an edict from the mayor.

Many citizens who rely on this system for transportation might welcome this. It’s a city of strict gun control, and no one knows for sure if they have the right to defend themselves. Merchants have been harassed and even arrested for trying to stop looting and pillaging in their own shops.

The message has been sent: Only the police can do this job. Whether they do it or not is another matter.

Things on the subway system have gotten crazy. If you know it well, you can manage to travel safely, but visitors to the city who take the wrong train at the wrong time are taking grave risks.

In actual fact, it’s guaranteed that this will only end in confiscating knives and other things that people carry in order to protect themselves while leaving the actual criminals even more free to prey on citizens.

The law-abiding will suffer and the criminals will grow more numerous. It will not end well.

When you step back from the details, what we have is the dawning of a genuine police state in the United States. It only starts in New York City. Where is the Guard going to be deployed next? Anywhere is possible.

If the crime is bad enough, citizens will welcome it. It must have been this way in most times and places that when the police state arrives, the people cheer.

We will all have our own stories of how this came to be. Some might begin with the passage of the Patriot Act and the establishment of the Department of Homeland Security in 2001. Some will focus on gun control and the taking away of citizens’ rights to defend themselves.

My own version of events is closer in time. It began four years ago this month with lockdowns. That’s what shattered the capacity of civil society to function in the United States. Everything that has happened since follows like one domino tumbling after another.

It goes like this:

1) lockdown,

2) loss of moral compass and spreading of loneliness and nihilism,

3) rioting resulting from citizen frustration, 4) police absent because of ideological hectoring,

5) a rise in uncontrolled immigration/refugees,

6) an epidemic of ill health from substance abuse and otherwise,

7) businesses flee the city

8) cities fall into decay, and that results in

9) more surveillance and police state.

The 10th stage is the sacking of liberty and civilization itself.

It doesn’t fall out this way at every point in history, but this seems like a solid outline of what happened in this case. Four years is a very short period of time to see all of this unfold. But it is a fact that New York City was more-or-less civilized only four years ago. No one could have predicted that it would come to this so quickly.

But once the lockdowns happened, all bets were off. Here we had a policy that most directly trampled on all freedoms that we had taken for granted. Schools, businesses, and churches were slammed shut, with various levels of enforcement. The entire workforce was divided between essential and nonessential, and there was widespread confusion about who precisely was in charge of designating and enforcing this.

It felt like martial law at the time, as if all normal civilian law had been displaced by something else. That something had to do with public health, but there was clearly more going on, because suddenly our social media posts were censored and we were being asked to do things that made no sense, such as mask up for a virus that evaded mask protection and walk in only one direction in grocery aisles.

Vast amounts of the white-collar workforce stayed home—and their kids, too—until it became too much to bear. The city became a ghost town. Most U.S. cities were the same.

As the months of disaster rolled on, the captives were let out of their houses for the summer in order to protest racism but no other reason. As a way of excusing this, the same public health authorities said that racism was a virus as bad as COVID-19, so therefore it was permitted.

The protests had turned to riots in many cities, and the police were being defunded and discouraged to do anything about the problem. Citizens watched in horror as downtowns burned and drug-crazed freaks took over whole sections of cities. It was like every standard of decency had been zapped out of an entire swath of the population.

Meanwhile, large checks were arriving in people’s bank accounts, defying every normal economic expectation. How could people not be working and get their bank accounts more flush with cash than ever? There was a new law that didn’t even require that people pay rent. How weird was that? Even student loans didn’t need to be paid.

By the fall, recess from lockdown was over and everyone was told to go home again. But this time they had a job to do: They were supposed to vote. Not at the polling places, because going there would only spread germs, or so the media said. When the voting results finally came in, it was the absentee ballots that swung the election in favor of the opposition party that actually wanted more lockdowns and eventually pushed vaccine mandates on the whole population.

The new party in control took note of the large population movements out of cities and states that they controlled. This would have a large effect on voting patterns in the future. But they had a plan. They would open the borders to millions of people in the guise of caring for refugees. These new warm bodies would become voters in time and certainly count on the census when it came time to reapportion political power.

Meanwhile, the native population had begun to swim in ill health from substance abuse, widespread depression, and demoralization, plus vaccine injury. This increased dependency on the very institutions that had caused the problem in the first place: the medical/scientific establishment.

The rise of crime drove the small businesses out of the city. They had barely survived the lockdowns, but they certainly could not survive the crime epidemic. This undermined the tax base of the city and allowed the criminals to take further control.

The same cities became sanctuaries for the waves of migrants sacking the country, and partisan mayors actually used tax dollars to house these invaders in high-end hotels in the name of having compassion for the stranger. Citizens were pushed out to make way for rampaging migrant hordes, as incredible as this seems.

But with that, of course, crime rose ever further, inciting citizen anger and providing a pretext to bring in the police state in the form of the National Guard, now tasked with cracking down on crime in the transportation system.

What’s the next step? It’s probably already here: mass surveillance and censorship, plus ever-expanding police power. This will be accompanied by further population movements, as those with the means to do so flee the city and even the country and leave it for everyone else to suffer.

As I tell the story, all of this seems inevitable. It is not. It could have been stopped at any point. A wise and prudent political leadership could have admitted the error from the beginning and called on the country to rediscover freedom, decency, and the difference between right and wrong. But ego and pride stopped that from happening, and we are left with the consequences.

The government grows ever bigger and civil society ever less capable of managing itself in large urban centers. Disaster is unfolding in real time, mitigated only by a rising stock market and a financial system that has yet to fall apart completely.

Are we at the middle stages of total collapse, or at the point where the population and people in leadership positions wise up and decide to put an end to the downward slide? It’s hard to know. But this much we do know: There is a growing pocket of resistance out there that is fed up and refuses to sit by and watch this great country be sacked and taken over by everything it was set up to prevent.

Spread & Containment

Another beloved brewery files Chapter 11 bankruptcy

The beer industry has been devastated by covid, changing tastes, and maybe fallout from the Bud Light scandal.

Share this:

{kind=link}

Before the covid pandemic, craft beer was having a moment. Most cities had multiple breweries and taprooms with some having so many that people put together the brewery version of a pub crawl.

It was a period where beer snobbery ruled the day and it was not uncommon to hear bar patrons discuss the makeup of the beer the beer they were drinking. This boom period always seemed destined for failure, or at least a retraction as many markets seemed to have more craft breweries than they could support.

Related: Fast-food chain closes more stores after Chapter 11 bankruptcy

The pandemic, however, hastened that downfall. Many of these local and regional craft breweries counted on in-person sales to drive their business.

And while many had local and regional distribution, selling through a third party comes with much lower margins. Direct sales drove their business and the pandemic forced many breweries to shut down their taprooms during the period where social distancing rules were in effect.

During those months the breweries still had rent and employees to pay while little money was coming in. That led to a number of popular beermakers including San Francisco's nationally-known Anchor Brewing as well as many regional favorites including Chicago’s Metropolitan Brewing, New Jersey’s Flying Fish, Denver’s Joyride Brewing, Tampa’s Zydeco Brew Werks, and Cleveland’s Terrestrial Brewing filing bankruptcy.

Some of these brands hope to survive, but others, including Anchor Brewing, fell into Chapter 7 liquidation. Now, another domino has fallen as a popular regional brewery has filed for Chapter 11 bankruptcy protection.

Image source: Shutterstock

Covid is not the only reason for brewery bankruptcies

While covid deserves some of the blame for brewery failures, it's not the only reason why so many have filed for bankruptcy protection. Overall beer sales have fallen driven by younger people embracing non-alcoholic cocktails, and the rise in popularity of non-beer alcoholic offerings,

Beer sales have fallen to their lowest levels since 1999 and some industry analysts

"Sales declined by more than 5% in the first nine months of the year, dragged down not only by the backlash and boycotts against Anheuser-Busch-owned Bud Light but the changing habits of younger drinkers," according to data from Beer Marketer’s Insights published by the New York Post.

Bud Light parent Anheuser Busch InBev (BUD) faced massive boycotts after it partnered with transgender social media influencer Dylan Mulvaney. It was a very small partnership but it led to a right-wing backlash spurred on by Kid Rock, who posted a video on social media where he chastised the company before shooting up cases of Bud Light with an automatic weapon.

Another brewery files Chapter 11 bankruptcy

Gizmo Brew Works, which does business under the name Roth Brewing Company LLC, filed for Chapter 11 bankruptcy protection on March 8. In its filing, the company checked the box that indicates that its debts are less than $7.5 million and it chooses to proceed under Subchapter V of Chapter 11.

"Both small business and subchapter V cases are treated differently than a traditional chapter 11 case primarily due to accelerated deadlines and the speed with which the plan is confirmed," USCourts.gov explained.

Roth Brewing/Gizmo Brew Works shared that it has 50-99 creditors and assets $100,000 and $500,000. The filing noted that the company does expect to have funds available for unsecured creditors.

The popular brewery operates three taprooms and sells its beer to go at those locations.

"Join us at Gizmo Brew Works Craft Brewery and Taprooms located in Raleigh, Durham, and Chapel Hill, North Carolina. Find us for entertainment, live music, food trucks, beer specials, and most importantly, great-tasting craft beer by Gizmo Brew Works," the company shared on its website.

The company estimates that it has between $1 and $10 million in liabilities (a broad range as the bankruptcy form does not provide a space to be more specific).

Gizmo Brew Works/Roth Brewing did not share a reorganization or funding plan in its bankruptcy filing. An email request for comment sent through the company's contact page was not immediately returned.

bankruptcy pandemic social distancing

The Coming Of The Police State In America

Another beloved brewery files Chapter 11 bankruptcy

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex