East Hanover, NJ – November 4, 2022 – Employment remains at historic highs for people with disabilities, but whether these gains will persist is a topic of today’s National Trends in Disability Employment – Monthly Update (nTIDE), issued by Kessler Foundation and the University of New Hampshire’s Institute on Disability (UNH-IOD). The COVID-19 pandemic prompted a marked increase in flexible business practices that benefit workers with disabilities, and a new survey indicates that many of these changes are likely to be here to stay.

Month-to-Month nTIDE Numbers (comparing September 2022 to October 2022)

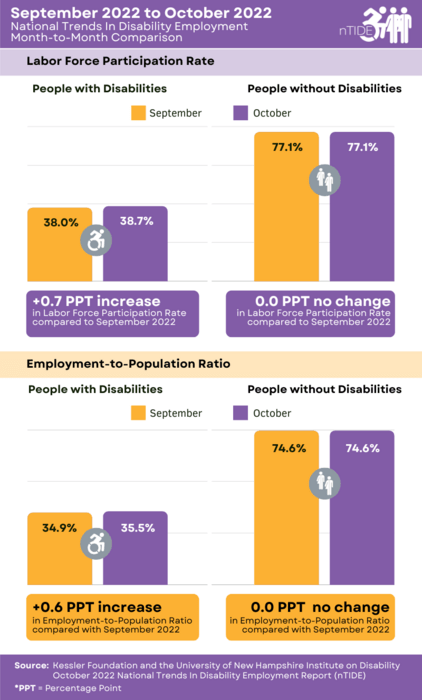

Based on data from the U.S. Bureau of Labor Statistics (BLS) Jobs Report released today, the employment-to-population ratio for people with disabilities (ages 16-64) increased from 34.9 percent in September to 35.5 percent in October (up 1.7 percent or 0.6 percentage points). For people without disabilities (ages 16-64), the employment-to-population ratio remained the same at 74.6 percent in September and October. The employment-to-population ratio, a key indicator, reflects the percentage of people who are working relative to the total population (the number of people working divided by the number of people in the total population multiplied by 100).

“The employment-to-population ratio for people with disabilities not only increased but remains steadily above historic highs. This contrasts with the lag we have seen for their counterparts without disabilities, whose ratio is just reaching its pre-pandemic levels,” said John O’Neill, PhD, director of the Center for Employment and Disability Research at Kessler Foundation. “Efforts to combat inflation continue, however, with this week’s major rate hike the latest in a series by the Federal Reserve,” he cautioned. “While these moves may dampen the future labor market, there are other positive factors for people with disabilities who are striving to work.”

Findings were similar for October’s labor force participation rate. For people with disabilities (ages 16-64), the labor force participation rate increased from 38.0 percent in September to 38.7 percent in October (up 1.8 percent or 0.7 percentage points). For people without disabilities (ages 16-64), the labor force participation rate remained the same, 77.1 percent in September and October. The labor force participation rate is the percentage of the population that is working, not working, and on temporary layoff, or not working and actively looking for work.

“The employment gains we’re seeing among people with disabilities are very encouraging,” remarked Andrew Houtenville, PhD, professor of economics and the research director of the UNH-IOD. “These may lead to long-term improvements in the workplace integration of people with disabilities,” explained Dr. Houtenville. “From our latest employment and disability survey, we’ve seen that supervisors indicate these positive changes are here to stay.”

Read more about the 2022 National Employment & Disability Survey: Effects of COVID-19 Pandemic Supervisor Perspectives. This new survey compares the workplaces of 2017 and 2022, revealing gains in recruiting, hiring, accommodating, and retaining employees with disabilities

Year-to-Year nTIDE Numbers (Comparing October 2021 to October 2022)

The employment-to-population ratio for working-age people with disabilities (ages 16-64) increased from 33.2 percent in October 2021, to 35.5 percent in October 2022 (up 6.9 percent or 2.3 percentage points). For working-age people without disabilities (ages 16-64), the employment-to-population ratio also increased from 73.5 percent in October 2021 to 74.6 percent in October 2022 (up 1.5 percent or 1.1 percentage points).

Similarly, for people with disabilities (ages 16-64), the labor force participation rate increased from 36.8 percent in October 2021 to 38.7 percent in October 2022 (up 5.2 percent or 1.9 percentage points). For people without disabilities (ages 16-64), the labor force participation rate also increased from 76.6 percent in October 2021 to 77.1 percent in October 2022 (up 0.7 percent or 0.5 percentage points).

In October 2022 among workers ages 16-64, the 5,883,000 workers with disabilities represented 4.0 percent of the total 148,031,000 workers in the U.S.

Ask Questions about Disability and Employment

Each nTIDE release is followed by an nTIDE Lunch & Learn online webinar. This live broadcast, hosted via Zoom Webinar, offers attendees Q&A on the latest nTIDE findings, provides news and updates from the field, as well as invited panelists to discuss current disability-related findings and events. On November 4, 2022 at 12:00 pm Eastern, Jhillika Kumar, founder and CEO of Mentra, the world’s largest neurodiversity employment network, joins Drs. Houtenville and O’Neill, and Denise Rozell, Policy Strategist at Association of University Centers on Disabilities (AUCD). Join our Lunch & Learns live or visit the nTIDE archives at: ResearchonDisability.org/nTIDE.

NOTE: The statistics in the nTIDE are based on Bureau of Labor Statistics numbers but are not identical. They are customized by UNH to combine the statistics for men and women of working age (16 to 64). nTIDE is funded, in part, by grants from the National Institute on Disability, Independent Living and Rehabilitation Research (NIDILRR) (90RT5037) and Kessler Foundation.

About the Institute on Disability at the University of New Hampshire

The Institute on Disability (IOD) at the University of New Hampshire (UNH) was established in 1987 to provide a university-based focus for the improvement of knowledge, policies, and practices related to the lives of persons with disabilities and their families. For information on the NIDILRR-funded Research and Training Center on Disability Statistics, visit ResearchOnDisability.org.

About Kessler Foundation

Kessler Foundation, a major nonprofit organization in the field of disability, is a global leader in rehabilitation research that seeks to improve cognition, mobility, and long-term outcomes – including employment – for people with neurological disabilities caused by diseases and injuries of the brain and spinal cord. Kessler Foundation leads the nation in funding innovative programs that expand opportunities for employment for people with disabilities. For more information, visit KesslerFoundation.org.

Stay Connected with Kessler Foundation

Twitter | Facebook | YouTube | Instagram | iTunes & SoundCloud

To interview an expert, contact:

Deborah Hauss, DHauss@kesslerfoundation.org;

Carolann Murphy, CMurphy@KesslerFoundation.org.

{kind=link}