Nasdaq Futures Surge On Wave Of Upgrades Ahead Of Crazy Earnings Week; EMini Flat

Nasdaq Futures Surge On Wave Of Upgrades Ahead Of Crazy Earnings Week; EMini Flat

Stocks fluctuated in early Monday trading, with US equity futures and global stocks rising back to all time highs before fading some gains, as optimism over…

Nasdaq Futures Surge On Wave Of Upgrades Ahead Of Crazy Earnings Week; EMini Flat

Stocks fluctuated in early Monday trading, with US equity futures and global stocks rising back to all time highs before fading some gains, as optimism over the $1.9 trillion U.S. stimulus plan fizzled modestly following a WaPo report that a bipartisan group was seeking to cut back on the proposed dollar amount while rising COVID-19 cases and delays in vaccine supplies muted some of the market's recent euphoria.

While E-Mini S&P futures were up "just" 7 points, or 0.20% to 3,842, Nasdaq futures soared on Monday, up 130 points or more than 1%, and outperforming contracts on the Russell 2000 Index of small-cap shares. After ending on a cautious note last Friday, global stocks resumed their march upward. Key for the market this week will be the parade of earnings, with the biggest U.S. tech giants including Apple, Tesla and Facebook scheduled to release results.

"The Federal Reserve, continued string of earnings with big techs ahead and the fear of missing out are driving the equity market,” said Sebastien Galy, a senior strategist at Nordea Investment Funds. "We expect the Fed to push back against the notion of tapering and that should be supportive of risky assets.”

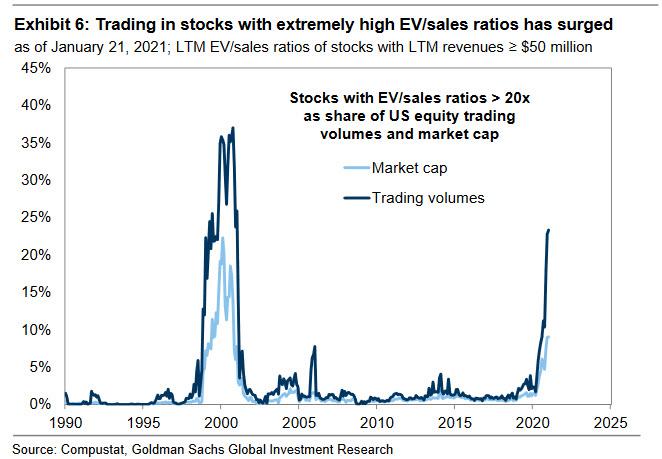

The combination of record stock prices, steep rallies in everything from Bitcoin to GameStop Corp. shares and Tencent, along with investor exuberance is reviving the debate over whether lavish central bank stimulus has created asset bubbles. Over the weekend, Goldman joined the chorus of warnings about a (contained) bubble, cautioning that the surge in SPAC, prices of tech companies without profits and companies with extremely high EV/sales ratios is troubling.

“Pockets of the market have recently appeared to demonstrate investor behavior consistent with bubble-like sentiment,” wrote strategists including David Kostin wrote in a note Friday. “But these excesses present low systemic risk to the broader market given their modest share of market cap.”

Goldman's warning did not trouble investors too much, and overnight, giga caps such as Microsoft, Facebook and Apple rose between 1.4% and 2.2% in premarket trading, with Apple surging to a new all time high after its stock price target was raised to $150 from $140 at Raymond James ahead of the iPhone maker’s results due Jan. 27, with the broker raising estimates as consumers move toward higher-end models. Apple shares rise 2% in U.S. premarket trading, set to open at a fresh record. Elsewhere, Microsoft, scheduled to report results on Tuesday, rose 1.5% as Wedbush raised its price target on the software maker’s stock on expectations of further growth in its cloud business for 2021.

Additionally, AMD added 1.5% after RBC raised its price target on the chipmaker’s stock on expectations of upbeat fourth-quarter earnings, helped by upside from PC demand, GPU demand and improving server trends. Merck Inc fell 1.2% after the drugmaker said it will end development of its two COVID-19 vaccines and focus pandemic research on treatments, with initial efficacy data on an experimental oral antiviral expected by the end of March. GameStop extended its massive short squeeze, surging as much as 46% in premarket trading.

On the political front, officials in President Joe Biden’s administration tried to head off Republican concerns that his $1.9 trillion pandemic relief proposal was too expensive, even as lawmakers from both parties agreed that getting the COVID-19 vaccine to Americans should be a priority.

“Expectations of substantial fiscal aid are keeping the bulls in charge,” said Hussein Sayed, chief market strategist at FXTM. “Some investors remain concerned about the surge in COVID-19 mutations, but it’s fiscal and monetary policies along with earnings that will determine the next move in equities.”

Sentiment was more mixed in Europe, with equity benchmarks in France, Spain and the U.K. turning modestly lower after opening higher. The Stoxx Europe 600 slipped 0.3%, giving up gains of as much as 0.6% as the travel and banking sectors weigh heaviest on the market. Travel industry gauge tumbles 1.8%, banks are 1.6% lower; Autos lose 1.4%; Personal care, telecoms, health care and tech outperform. European stocks slipped to session lows following news that Merck is discontinuing development of its two experimental Covid-19 vaccines. The euro reversed a modest gain after German Ifo business confidence stood at 90.1 vs 92.2 in December, missing an estimate of 91.4.

Earlier in the session, Asian stocks rose to a new record as benchmark gauges in Hong Kong and South Korea climbed more than 2% each. Tencent was the biggest boost to the MSCI Asia Pacific Index, which was headed for a fresh all-time high. Tencent climbed as a company it backs, Kuaishou Technology, announced plans for a $5.4 billion IPO in Hong Kong. Hong Kong stocks rebounded from a two-day loss after the government lifted its first lockdown, which was successful in detecting 13 new cases of coronavirus. Samsung Electronics also helped bolster gains in the Asian benchmark, as well as South Korea’s Kospi. Indonesia’s key stock index tumbled after Jakarta confirmed that it’s extending virus-related restrictions by two weeks to Feb. 8.

With pricey stock market valuations, investors are keeping an eye out for corporate forecasts to justify it, given the expectation of an economic rebound this year. Earnings are expected to rise 23.7% this year after falling 14.1% in 2020, according to Refinitiv.

Of the 122 companies in the S&P 500 reporting this week, the highlights are Microsoft, Johnson & Johnson, Verizon Communications, NextEra Energy, Texas Instruments, Starbucks, American Express, General Electric, Lockheed Martin and UBS (tomorrow). Then on Wednesday we’ll hear from Apple, Tesla, Facebook, AT&T, Abbott Laboratories and Boeing. Thursday brings Visa, Mastercard, Comcast, Danaher, McDonald’s and Samsung. And finally Friday sees reports from Eli Lilly, Chevron, SAP, Charter Communications, Honeywell and Caterpillar.

“Small/Mid (SMID) cap earnings were more impacted by the pandemic, and we project an earnings rebound more than 2x larger than the S&P 500,” said BoFA strategists in a note. “Historically, when Democrats control both the White House and Congress, SMID-cap returns have exceeded large cap. Also, SMID-caps are more domestically-oriented, which should benefit from on-shoring and infrastructure spending.”

In rates, Treasuries were higher as U.S. trading began after erasing Asia-session losses, led by bunds and gilts during European morning after soft German IFO data and as Italian bonds outperform. Treasury yields were lower by ~2bp across long-end of the curve, with 2s01s, 5s30s spreads flatter by 0.8bp and 1.6bp; 10-year yields around 1.075% with bunds, gilts outperforming by ~1bp and Italian bonds by ~4bp. This week's auction cycle returns with $60bn 2-year note, $61bn 5-year Tuesday and $62bn 7-year Thursday.

Bunds advanced, outperforming Treasuries, ahead of a large line-up of ECB speakers; Italian bonds rallied higher as the nation’s prime minister is sizing up his options ahead of a crucial Senate vote this week and could decide to resign in a tactical move to position himself to lead a new government if he’s set to fall short

In FX, the Bloomberg Dollar Spot Index bounced in early European hours to erase an earlier decline, and the dollar was mixed versus its Group-of-10 currencies; the FOMC rate decision on Wednesday is this week’s main risk event for currency markets and options are pricing in a dovish stance. The Swedish krona and commodity currencies lead gains, while the Swiss franc edged lower along with the euro, which reversed a modest gain after German Ifo business confidence stood at 90.1 vs 92.2 in December, missing an estimate of 91.4. The yen was steady after swinging between losses gains versus the dollar; Australian and New Zealand dollars pared gains in European hours after earlier advancing in Asian session amid risk-on price action spurred by gains in the yuan and regional stock indexes after a partial lockdown in Hong Kong was lifted.

In commodities, Brent gained 0.65% to $55.77 a barrel and U.S. crude rose 0.75% to $52.66 with investors assessing the impact of supply curbs from Iraq and Libya on the near-term demand outlook. Bitcoin rebounded above $34,000 following the latest JPMorgan hitpiece. Gold was flat at $1,862 an ounce.

On today's calendar, we get the December Chicago Fed national activity index and the Dallas Fed index. ECB President Lagarde, ECB’s Panetta, Lane, PBoC Governor Yi Gang speak.

Market Snapshot

S&P 500 futures up 0.3% to 3,847.00

MXAP up 0.9% to 215.03

MXAPJ up 1.2% to 727.13

Nikkei up 0.7% to 28,822.29

Topix up 0.3% to 1,862.00

Hang Seng Index up 2.4% to 30,159.01

Shanghai Composite up 0.5% to 3,624.24

Sensex down 0.9% to 48,462.24

Australia S&P/ASX 200 up 0.4% to 6,824.71

Kospi up 2.2% to 3,208.99

Brent Futures up 0.7% to $55.82/bbl

Gold spot little changed at $1,856.05

U.S. Dollar Index up 0.1% to 90.32

STOXX Europe 600 up 0.2% to 409.43

German 10Y yield fell 2.1 bps to -0.533%

Euro down 0.1% to $1.2158

Italian 10Y yield rose 6.5 bps to 0.639%

Spanish 10Y yield fell 3.3 bps to 0.09%

Top Overnight News from Bloomberg

The White House is at work pitching wary Republican senators the $1.9 trillion stimulus plan

Cryptocurrency enthusiasts counting on Bitcoin to bounce back above the $40,000 level face a challenge due to faltering demand for the biggest fund tracking the digital asset, according to JPMorgan Chase & Co. The pace of flows into the $20 billion Grayscale Bitcoin Trust “appears to have peaked” based on four-week rolling averages

Bank of England Governor Andrew Bailey is missing an opportunity to fight climate change by buying the debt of polluting companies with no green strings attached, a panel of lawmakers warned

Prospects for convicting President Donald Trump in his impeachment trial are waning as more Republicans embrace the argument that a conviction would be divisive, unwarranted or even unconstitutional

Bank of Japan Governor Haruhiko Kuroda says Japan’s economy will probably return to its pre-pandemic level by the end of fiscal 2021 or early in the following year

A 3-minute recap of the overnight action courtesy of Amplify Trading

A quick look at global markets courtesy of Newsquawk

Asian equity markets began the week with a mildly positive tilt and US equity futures also rebounded from Friday’s losses although upside was limited amid a lack of significant bullish catalysts with weekend newsflow dominated by COVID-19 headlines and as participants look ahead with the FOMC meeting and month-end on the horizon. ASX 200 (+0.4%) was led higher by consumer stocks amid an easing of restrictions after Western Australia and Victoria relaxed some lockdown policies concerning neighbouring states, while trade data was also encouraging as it showed a 16% M/M jump in exports. Nikkei 225 (+0.4%) was kept afloat as exporters benefitted from mild currency outflows and with Toshiba shares the stellar performer in Tokyo after its approval to return to the first section of the exchange. Hang Seng (+2.4%) and Shanghai Comp. (+0.5%) were also positive amid recent speculation the PBoC could potentially utilize the contingent reserve arrangement ahead of the Lunar New Year which allows banks to dip into their reserves to plug any shortfalls in liquidity, with the gains in Hong Kong exacerbated by southbound Stock Connect flows and after the city’s authorities lifted the weekend lockdown that was imposed in Kowloon. Finally, 10yr JGBs treaded water overnight following recent upside in USTs and with the BoJ also in the market for nearly JPY 1.4tln of JGBs in up to 10yr maturities, although upside was restricted with some analysts recently suggesting that JGB purchases could weaken in the current quarter as participants await further clarity regarding the BoJ’s March review given that potential tweaks could steepen the curve.

Top Asian News

Tencent’s $251 Billion Rally Triggers Frenzy in Shares, Options

ByteDance Foe Seeks $5.4 Billion in Biggest Tech IPO Since Uber

Kuroda Says Economy Likely to Reach Pre-Crisis Level in FY2021

Kazakh Central Bank Keeps Rates Unchanged to Curb Inflation

European bourses see a mixed start to week (Euro Stoxx 50 Unch) as the optimism seen during the APAC session petered out in light of a downbeat German Ifo release, and ahead of a slew of high-profile speakers and the first FOMC policy decision of the year. US equity futures meanwhile see similarly mixed, but somewhat more resilient trade with the NQ (+0.9%) remaining the outperformer vs the RTY (-0.1%) ahead of a flood of large-cap tech earnings later this week, including from the likes of Apple, Microsoft, Tesla, Facebook, SAP alongside McDonalds, Boeing, 3M and Caterpillar. Back to Europe, bourses vary in performance with Italy’s FTSE MIB (+0.5%) supported by reports PM Conte is reportedly close to resigning and is looking to form a new government which would have a more substantial majority – albeit this was downplayed by sources. Meanwhile, the CAC 40 (-0.4%) narrowly underperforms its peers with the index pressure by banks and its COVID-exposed aeronautical sector amid chatter of an imminent third national lockdown – with Airbus (-2.3%) and Safran (-2%) also hit by reports that China Southern Airlines, China Eastern Airlines and Air China held off on a total of 58 planes from Boeing and 53 from Airbus last year, whilst Bahrain Gulf Air is reportedly in talks to delay plan orders from Airbus and Boeing. Sectors in Europe are also mixed with no clear risk bias. Energy stands as the straddler following Friday’s losses in the crude complex, whilst financials bear the brunt of a lower yield environment and healthcare sees some defensive inflows. The IT sector stands as the gainer with some potential tailwinds emanating from reports that chipmakers including STMicroelectronics (+2.8%) and NXP Semiconductor (+4.5% pre-mkt) are raising prices on chips that go into cars and telecom equipment in a bid to manoeuvre out of a squeeze created by soaring demand and limited foundry capacity. The chipmakers have reportedly demanded that clients pay 10-20% more, according to sources. In terms of individual movers, Deutsche Bank (-0.2%) is relatively stable with reports over the weekend stating the Co. is looking into whether staff members mis-sold investment banking projects in breach of EU rules.

Top European News

Italy Premier Weighs Tactical Retreat Before Vote This Week

Philips Sees Sustained Growth After Profit Meets Target

Renewables Beat Fossil Fuels in EU for First Time Last Year

German Business Mood Darkens as Virus Lockdowns Delay Recovery

In FX, another rise in weekly Swiss bank sight deposits suggests that direct action to curb Franc strength amidst renewed political instability in Italy has been stepped up again, and Eur/Chf has taken some heed along with Usd/Chf as the respective pairs hover off lows within 1.0771-87 and 0.8848-73 ranges. However, the Euro is suffering a bit of a set-back in its own right following a weaker than expected German Ifo survey, as all key metrics missed consensus in contrast to ZEW findings, albeit with both institutes reporting improvements in the outlook for exports. Eur/Usd has retreated further from post-ECB peaks to sub-1.2150, and giving the Dollar a lift indirectly with the DXY eclipsing last Friday’s high having held just above 90.000 again between 90.361-079 parameters. Nevertheless, the Buck and index remain prone to further downside pressure while under 90.500 ahead of the FOMC, US data and month end.

NZD/AUD/CAD/GBP/JPY - The Kiwi continues to benefit from repositioning for a less RBNZ, and more so than the RBA that cut rates and ramped up QE in November. Hence, Nzd/Usd is clinging to 0.7200 as the Aud/Nzd cross retraces towards 1.0700 from just over 1.0750 and Aud/Usd fades after falling a few pips shy of 0.7750 in wake of Aussie trade data revealing an encouraging 16% jump in exports. Elsewhere, the Loonie has probed 1.2700 again with the aid of a rebound in oil prices, but remains well off post-BoC highs after US President Biden’s executive order cancelling the Keystone XL pipeline transit permit and the Pound had another brief look above 1.3700 before yielding to the general Greenback revival. Meanwhile, the Yen is still keeping its head above 104.00 with little reaction to relatively run of the mill rhetoric from BoJ Governor Kuroda – see headline feed at 8.14GMT for details.

SCANDI/EM -The Sek and Nok are both taking advantage of the aforementioned Eur reversal irrespective of the fact that Sweden and Norway are both taking stricter measures to combat COVID-19, as the latter also gleans some traction from crude, but the Try is also outperforming after a marginal rise in Turkish manufacturing sentiment and S&P reaffirming its rating with a stable outlook.

In commodities, WTI and Brent front-month futures kicked off the European week with gains following a similarly firm APAC session, as markets retrace some of Friday’s losses as the complex continues to be underpinned by vaccines, stimulus and recovery hopes alongside OPEC+ flexibility and some geopolitical risks in the face of more stringent near-term lockdown and travel restriction measures due to the rising variants. Further supportive factors for the complex includes reports that Iraq will compensate for its prior overproduction by reducing oil output in January and February, in which it will produce 3.60mln BPD vs 3.85mln BPD in December, also lifting sentiment surrounding OPEC. Geopolitical risks cannot be discounted as Taiwan’s air defence identification zone was breached multiple times by Chinese military aircrafts over the weekend, whilst the Friday saw the passing of a law that would allow Chinese coast guards to fire on foreign vessels – with eyes on the contested South China sea. There were also reports that China and India had a clash, although the severity of the situation was downplayed by both sides. On the demand side, reports noted that France may enter a national lockdown whilst Norway is to widen its lockdown in the capital region. Brent March'21 resides just above USD 56.50/bbl (vs low USD 55.18/bbl) while its WTI counterpart hovers around USD 52.50/bbl (vs low USD 52.05/bbl). Elsewhere, spot gold has gained traction in recent trade to print fresh session highs after declining from its USD 1860/oz overnight higher and dipping below its 50 DMA (USD 1858/oz) to test its USD 1850/oz psychological level ahead of its 200 DMA (USD 1848/oz). In terms of base metals, LME copper edges higher amid the softer Buck and reflationary hopes. Dalian iron ore maintained a narrow range overnight as tighter steel margins countered falling shipments of the base metal from Australia.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0.1, prior 0.3

10:30am: Dallas Fed Manf. Activity, est. 12, prior 9.7

DB's Jim Reid concludes the overnight wrap

Given there is nothing much to do at the moment the snowman and snowwomen population of the U.K. must have grown exponentially yesterday. We welcomed in an identical set of snowman twins to the world before Bronte the dog mauled them both so as to eat the carrots and chew the sticks that were for a short while their arms. Yes we had our one day of snow every c.3 years here in the south of England. At least the lockdown has spared us a few days of chaos on the roads and trains.

So winter is truly with us and the hopes of a celebratory summer ahead seems a long way off at the moment. Reflecting of this, given we published our 2021 credit outlook in the first half of November it is interesting to assess what is different now from when we published. Back then we were full of optimism that the vaccine would deliver conditions relatively close to normality by mid-year and that Q2 would likely be a quarter of increasing re-openings of developed market economies. As such it was hard to be anything other than bullish on risk, especially in H1. However c.10 weeks later what has changed? Well credit spreads are already very close to what we thought were bullish H1 targets but it’s fair to say the news on the virus isn’t as optimistic as we’d hoped.

Vaccinations are slower than what we’d expected in virtually all large countries and even in countries where it’s been quicker, eg the U.K., the one dose first strategy means that full protection will be slower to materialise. It also doesn’t seem to be the case that just vaccinating the vulnerable will be enough to lift most restrictions as I’d expected. This is partly due to increasing concerns around mutations from various parts of the world. Until scientists rule that each will be covered by the current vaccines there will likely be reluctance to lift restrictions. So it now seems we will be constantly worried about mutations until covid has been largely eradicated even if none of them ever evade vaccines. So although I still think there’s going to be a huge surge of economic activity by the summer, there is probably a bit more doubt in my mind now than there was back in November.

However how do you trade that? The longer economies stay highly restricted the longer central banks and governments will be all in. Plus we have Biden’s extra stimulus to come. Ironically it was always the normalisation of economies that was going to pose the greatest risk to markets as that was where there was a larger risk of rates rising sharply and also the biggest risk of any tech bubble bursting due to a desire to rotate out of this winning pandemic sector and back into the normal economy. I would say there’s been no rotation away from tech since November only less buying than in cyclicals. If we actually saw the market net selling tech then that could cause big problems given their size and influence. Anyway in conclusion there are higher levels of uncertainty now than back in November and tighter spreads/ higher markets. It seems like a more asymmetric risk set up.

Importantly there was some positive news on vaccinations overnight with Israel’s second-largest health network, Maccabi Health Services, saying that its study of a sample group of 50,777 people over the age of 60 inoculated in late December and then again in mid-January, showed that 2 days after the second shot, the number of new infections and hospitalisations were both down about 60% from their peak. This could literally be a shot in the arm in the fight against Covid-19. For how different countries vaccination drives are progressing see the table below.

Moving to the week ahead, we have an eventful calendar once again, with the Fed’s latest monetary policy decision on Wednesday expected to be a highlight. Indeed Wednesday is a blockbuster day with Apple, Tesla and Facebook reporting to add to the fun. 122 S&P 500 companies report in total over the coming 5 days in the first blockbuster week for earnings. In terms of economic data releases, a number of countries release their Q4 GDP readings for the first time. In politics Congress will start the high level negotiations on Biden’s proposed stimulus package. House speaker Pelosi has suggested she wants to pass something through reconciliation within two weeks. However the realities will likely extend this timeline. Nonetheless plenty of opportunities for headlines now. Staying with politics, the Italian government has a Senate vote this week (likely Wednesday or Thursday) on the annual report of its justice minister. A loss would raise the stakes for PM Conte and although we still don’t think fresh elections are likely, the uncertainty is building as to what happens next to his administration. Indeed, Italian daily Corriere della Sera has reported that Mr. Conte may quit if he loses.

Elsewhere, although the annual meeting of the World Economic Forum at Davos won’t be taking place as normal this week, and I won’t have to be embarrassed by a lack of a Canada Goose jacket at the shindig, a virtual event will see a number of global leaders and central bankers gather to discuss important policy issues. Attendees include Chinese President Xi Jinping, German Chancellor Merkel, French President Macron, BoJ Governor Kuroda, ECB President Lagarde and BoE Governor Bailey.

In more detail on some of the upcoming events, in terms of the Fed, in their preview (link here), our US economists do not anticipate any material changes to the policy settings and message from the FOMC, after they adopted outcome-based forward guidance for asset purchases in December. Furthermore, they expect the statement to be untouched, aside from acknowledging a recent softening in the data. The big question on investors’ minds will be any timetable for tapering purchases, though Powell is likely to adopt a dovish tone on this, and reiterate that it’s premature to contemplate a potential timeline given the challenging near-term outlook and remaining uncertainties.

On the data side, the main highlight will be the first look at the Q4 GDP numbers for a number of countries, including the US (Thursday), France and Germany (both Friday). Given the lockdowns that were imposed in a number of European countries late last year, our economists are forecasting a Q4 contraction in the key European economies, including a -1.5% quarter-on-quarter decline in Germany, and a -6.2% decline for France. The US should fare relatively better however, with our economists forecasting Q4 growth at an annualised rate of +4.5%. As well as these, next week will also see the release of the Ifo Institute’s business climate indicator from Germany (this morning).

Of the 122 companies in the S&P 500 and the 42 in the STOXX 600, the highlights are Microsoft, Johnson & Johnson, LVMH, Novartis, Verizon Communications, NextEra Energy, Texas Instruments, Starbucks, American Express, General Electric, Lockheed Martin and UBS (tomorrow). Then on Wednesday we’ll hear from Apple, Tesla, Facebook, AT&T, Abbott Laboratories and Boeing. Thursday brings Visa, Mastercard, Comcast, Danaher, McDonald’s and Samsung. And finally Friday sees reports from Eli Lilly, Chevron, SAP, Charter Communications, Honeywell and Caterpillar.

Asian markets have started the week on the front foot with the Nikkei (+0.37%), Hang Seng (+2.11%), Shanghai Comp (+0.74%) and Kospi (+2.03%) all up. The outperformance of the Hang Seng is being helped by the news that the city has lifted lockdown restrictions in Kowloon. Futures on the S&P 500 are also up +0.40% while the US dollar index is down -0.11%.

Recapping last week now and equity markets rose to new all-time highs in the US and new pandemic highs in Europe. However as earnings season kicked into gear and concerns over the virus impact lingering for longer than expected in 2021, the cyclical-over-growth trade seems to have taken a pause with large cap tech outperforming on the week at the expense of sectors such as banks and energy. The S&P 500 gained +1.94% (-0.30% Friday), while the NASDAQ composite rose an even greater +4.19% (+0.09% Friday). Bank stocks on both sides of the Atlantic fell sharply as the sharp rise in core rates reversed slightly, with US banks dropping -3.06% while European Banks were down a slightly lesser -2.91%. European equities underperformed as the STOXX 600 ended the week just +0.17% higher (-0.57% Friday) while the Italian FTSE MIB (-1.31%) and Spanish IBEX (-2.36%) notably lost ground.

Following President Biden’s inauguration midweek, the new administration went about further explaining and drumming up support for the new rescue stimulus bill of $1.9 trillion. The substantial selloff in US Treasuries slowed, with 10yr yields broadly unchanged (+0.2bps) at 1.086%. Yield curves resumed steepening however with the US 2s10s curve up another +1.4bps to 96.1bps, while the same curve steepened +1.6bps in Germany. Yields in Europe rose with 10Yr Bund yields +3.1bps (-1.6bps Friday) to -0.51% and 10yr Gilt yields +2.0ps (-2.3bps Friday) to 0.31%. Following the political fallout of the realignment of the Italian government, and even after Prime Minister Conte won his vote of confidence mid-week, the spread of 10yr Italian BTPs over German bunds widened +10.7bps to 126bps, while BTP yields themselves rose to their highest level since mid-November.

On the data front the highlight from Friday was the January flash PMIs from around the world. PMIs slid across Europe, with the composite Euro Area PMI falling to 47.5, remaining beneath the 50-mark that separates expansion from contraction. Germany’s composite PMI came in at 50.8 (vs. 50.0 expected), a stark difference to the below-expansion numbers in France (47.0 vs 49.0 expected) and the UK (40.6 vs 45.5 expected). The latter data point shows just how much the lockdowns are affecting the British economy, with the services PMIs coming in at 38.8 (vs. 45.0 expected) which was the lowest since May. The US numbers on the other hand were stronger than expected, with the services PMI just over 4pts higher than expected at 57.5 and manufacturing PMI 2.6pts higher at 59.1. The composite level of 58.0 is just 0.6pts lower than this past November’s level, which makes it the second-highest reading since 2015.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}