Government

Much Ado, but Barring Significant Downside Surprise, August Jobs Report will not Stand in the Way of Fed Tapering

Overview: The US dollar was sold ahead of today’s employment report, falling to around three-four week lows against most major currencies. Follow-through dollar selling today has been minimal, and the Antiopdeans continue to lead the move. Emerging…

Share this:

Overview: The US dollar was sold ahead of today's employment report, falling to around three-four week lows against most major currencies. Follow-through dollar selling today has been minimal, and the Antiopdeans continue to lead the move. Emerging market currencies are mixed, and the JP Morgan EM FX index is stalling after rising for the past five sessions. Asia Pacific equities rallied, led by the 2% advance in the Nikkei on news that Prime Minister Suga will not stand at the LDP leadership contest later this month, effectively stepping down. The yen has barely budged. European shares are trading slightly softer as service PMIs coming in softer. Still, the Dow Jones Stoxx 600 may eke out its sixth gain in the past seven weeks. US futures are trading firmer but seem almost meaningless ahead of the US employment report. The US 10-year yield is steady, slightly below 1.30%. European benchmark yields are slightly firmer. Ten-year rates have risen faster in Europe this week than in the US. Separately oil gushed higher yesterday. The 2.1% rally lifted October WTI above $70 a barrel for the first time in a month. Trading is subdued today and the October contract continues to straddle the $70-level. Gold too remains within the well-worn ranges seen this week, mostly between $1800 and $1820. China's iron ore contract eased for the fourth consecutive session and finished the week with a 6.6% cumulative loss. It is the sixth decline in the past seven weeks. Copper has edged higher but is still nursing a small loss for the week. The CRB Index begins today with a 0.4% gain for the week after a nearly 6% advance last week.

Asia Pacific

Speculation in the press yesterday that Japan Prime Minister was going to dissolve the lower house shortly to arrange an election next month proved for naught. Instead, Suga announced that he would not contest the leadership challenge later this month. Since the leader of the LDP becomes the prime minister, given its representation, Suga's announcement is tantamount to resignation. As we have argued, finding an alternative to Suga is one thing; devising a substantially different programmatic approach is quite another. The LDP's thrust is fiscal and monetary stimulus.

China, Australia, and Japan reported disappointing August service and composite PMIs. China's Caixin service PMI fell below the 50 boom/bust level (46.7 vs. 54.9), which drove the composite reading to 47.2 from 53.1. This confirms what the market already accepted. The world's second-largest economy has slowed considerably, and that officials will likely provide more support formally and informally. Japan remains the only G7 country whose PMI is below the 50-level. The service PMI was revised to 42.9 from the preliminary reading of 43.5 and 47.4 in July. The composite got chopped to 45.5. It was at 48.8 in July. Expectations for a recovery in the world's third-largest economy had already been pushed into Q4. Australia's final PMI reading confirmed the fourth consecutive monthly decline, and there has been further deterioration since the preliminary report. The service PMI stands at 42.9 (43.3 flash) and 44.2 in July. The composite slipped to 43.3 (43.5 flash) from 45.2 previously.

Yesterday, the dollar was confined to a 20-pip range against the yen, and today, the range is only slightly wider. The session low has been JPY109.80, and the high is slightly above JPY110.05. A three-week high was set on Wednesday near JPY110.40. It found support this week a little ahead of last week's low (~JPY109.40). In the bigger picture, for the better part of two months, the dollar has been mostly in a JPY109 to JPY111 range. The $1.3 bln options expiring today at JPY110 have likely been neutralized. The Australian dollar is extended its gains for the fourth consecutive session and eight of the past 10. It is at its best level since July 16 as it pushes near $0.7440. The $0.7450 area corresponds to the (38.2%) retracement of this year's decline (from the last February high slightly above $0.8000. The dollar drifted lower against the Chinese yuan for the sixth consecutive session. In only one of those days (last Friday) was the next change more than 0.1%. Still, the dollar has eased to the lower end of the CNY6.45-CNY6.50 range that has mostly confined the dollar since mid-June. It is the greenback's long losing streak since May. The PBOC set the dollar's reference rate at CNY6.4577, close to the median projection in Bloomberg's survey for CNY6.4574.

Europe

The eurozone final PMIs disappointed. German and French services PMIs were revised lower. This dragged the German composite lower (60.0 vs. 60.6 preliminary and 62.4 in July). In France, the composite PMI was steady (at the flash reading of 55.9) but down from 56.6 in July. Italy's service PMI stands at 58.0, unchanged from July but below the 58.5 forecasts. Due to the strength of the manufacturing PMI, the composite rose to 59.1 from 58.6. Italy's resilience is notable. Spain service PMI softened to 60.1 from 61.9, undershooting forecast, while the composite met expectations at 60.6, down from 61.2 in July. This turns into a 59.0 service reading on the aggregate level, down from the 59.7 preliminary estimates and 59.8 in July. The composite stands at 59.0 (59.5 flash) and 60.2 previously. While the precise numbers are new, the general signal that some momentum was lost in August does not surprise. Nor does it shed much light on next week's ECB's decision.

The UK's preliminary service and composite PMI were also revised lower, confirming the third consecutive monthly slowing. The services PMI was revised to 55.0 from 55.5 and 59.6 in July. It is the lowest reading since February. The composite stands at 54.8, not 55.3 of the flash estimate, and down from the 59.2 reading in July. Meanwhile, during last year's crisis, the Chancellor of the Exchequer was well-liked as he opened the purse strings in the face of the unprecedented pandemic. However, now as he is at the forefront of efforts to rein in spending, his star has dimmed. Today's reports suggest he has the state pensions in view. Local papers see an announcement as early as next week that will abrogate the 2019 election manifesto by seeking a cap on pension increases and boost the national insurance payments on some 25 million people. Prime Minister Johnson had promised to preserve the "triple lock" on pensions and foreswore an increase in income, value-added, and national insurance taxes. The tension between the Prime Minister and the Chancellor is set to increase.

The euro made a marginal new high for the move near $1.1885 in Asia and was sold to session lows near $1.1870 in the European morning. We are most confident that the narrow range will not hold. A 655 mln euro option at $1.1875 that expires today may be part of the battle. The euro had risen in nine of the past 10 sessions coming into today. The euro continues to flirt with the upper Bollinger Band (slightly below $1.1875). The market appears vulnerable to "buy the rumor, sell the fact on today's US employment report. The two-week uptrend line comes in a little above $1.1800, where an option for nearly 800 mln euros is struck that also expires today. Sterling closed above its 200-day moving average (~$1.3815) yesterday for the first time since mid-August and was bid to $1.3845 today. Some of the buying may have been linked to the GBP1.01 bln options expiring today in the $1.3815-$1.3820 area. Sterling is kissing the trendline drawn from the June 1 high (~$1.4250) and the late July high (~$1.3985). It caught the early August highs and is at about $1.3840 today.

America

It is all about the US jobs report today. After two months of more than 900k growth of non-farm payrolls and on the back of most high-frequency data points coming in below expectations, a softer number has been anticipated, even before the ADP miss. The median forecast in Bloomberg's survey now stands at 725k. Recall that July's 943k increase was flattered by a rise of 240k government workers, primarily related to the re-opening of schools. The private sector added 703k jobs in July. Economists in the Bloomberg survey looked for 700k private-sector jobs a week ago, but the new forecasts have driven the median guesstimate to 610k. The unemployment rate is expected to slipe to 5.2% from 5.4%, and the participation rate may tick up to 61.8% from 61.7%. The key issue is not so much the details, but will it impact the Fed's signal about tapering in Q4. And here, barring a significant downside surprise, the answer is negative. Even if the June-July non-farm payroll pace is not maintained, there is no doubt that the labor market is healing and significant progress has been made, even if it is not complete. Headline risk, yes, after all, the non-farm payroll report remains one of the hardest high-frequency data points to forecast.

The ISM services index is also due today. It is expected to have pulled back to 61.7 from 64.1, still elevated. Meanwhile, Senator Manchin has underscored the sense in the market that while the Democrats can push through more of its agenda over Republican opposition through the reconciliation measures, the main hurdle is within the Democratic Party itself. Manchin's speeches and op-ed pieces argue against the $3.5 trillion spending programs that the Biden administration and House of Representatives seek. Lastly, the debt ceiling issue, which has yet to be resolved, appears to have impacted the four and eight-week bill auctions as participants seek to avoid bills expiring around when the Treasury's ability to maneuver is exhausted, which is now seen next month.

The US dollar narrowly posted an outside down day against the Canadian dollar, and follow-through selling has seen it test the 200-day moving average (~CAD1.2535). There is an unusually large option expiry today for $1.6 bln at CAD1.2550. Another set of options for nearly $1.2 bln are struck at CAD1.2500. On the top side, resistance is seen initially around CAD1.2570 and then a band that extends from CAD1.2600 to CAD1.2640. The dollar's downside momentum against the Mexican peso that carried it from MXN20.20 at the start of the week to MXN19.93 yesterday stalled. Only a marginal new low was recorded yesterday, and it is consolidating in a narrow range ahead of the US employment report. The first area of important resistance is seen around MXN20.12, where the 200-day moving average is found, and it corresponds to the (38.2%) retracement objective of the decline since last week's MXN20.4275 high was posted.

Disclaimer

unemployment pandemic stimulus dow jones equities fed currencies us dollar canadian dollar euro yuan house of representatives recovery unemployment gold oil japan european europe uk france spain italy china

Government

Young People Aren’t Nearly Angry Enough About Government Debt

Young People Aren’t Nearly Angry Enough About Government Debt

Authored by The American Institute for Economic Research,

Young people sometimes…

Share this:

Authored by The American Institute for Economic Research,

Young people sometimes seem to wake up in the morning in search of something to be outraged about. We are among the wealthiest and most educated humans in history. But we’re increasingly convinced that we’re worse off than our parents were, that the planet is in crisis, and that it’s probably not worth having kids.

I’ll generalize here about my own cohort (people born after 1981 but before 2010), commonly referred to as Millennials and Gen Z, as that shorthand corresponds to survey and demographic data. Millennials and Gen Z have valid economic complaints, and the conditions of our young adulthood perceptibly weakened traditional bridges to economic independence. We graduated with record amounts of student debt after President Obama nationalized that lending. Housing prices doubled during our household formation years due to zoning impediments and chronic underbuilding. Young Americans say economic issues are important to us, and candidates are courting our votes by promising student debt relief and cheaper housing (which they will never be able to deliver).

Young people, in our idealism and our rational ignorance of the actual appropriations process, typically support more government intervention, more spending programs, and more of every other burden that has landed us in such untenable economic circumstances to begin with. Perhaps not coincidentally, young people who’ve spent the most years in the increasingly partisan bubble of higher education are also the most likely to favor expanded government programs as a “solution” to those complaints.

It’s Your Debt, Boomer

What most young people don’t yet understand is that we are sacrificing our young adulthood and our financial security to pay for debts run up by Baby Boomers. Part of every Millennial and Gen-Z paycheck is payable to people the same age as the members of Congress currently milking this system and miring us further in debt.

Our government spends more than it can extract from taxpayers. Social Security, which represents 20 percent of government spending, has run an annual deficit for 15 years. Last year Social Security alone overspent by $22.1 billion. To keep sending out checks to retirees, Social Security goes begging to the Treasury Department, and the Treasury borrows from the public by issuing bonds. Bonds allow investors (who are often also taxpayers) to pay for some retirees’ benefits now, and be paid back later. But investors only volunteer to lend Social Security the money it needs to cover its bills because the (younger) taxpayers will eventually repay the debt — with interest.

In other words, both Social Security and Medicare, along with various smaller federal entitlement programs, together comprising almost half of the federal budget, have been operating for a decade on the principle of “give us the money now, and stick the next generation with the check.” We saddle future generations with debt for present-day consumption.

The second largest item in the budget after Social Security is interest on the national debt — largely on Social Security and other entitlements that have already been spent. These mandatory benefits now consume three quarters of the federal budget: even Congress is not answerable for these programs. We never had the chance for our votes to impact that spending (not that older generations were much better represented) and it’s unclear if we ever will.

Young Americans probably don’t think much about the budget deficit (each year’s overspending) or the national debt (many years’ deficits put together, plus interest) much at all. And why should we? For our entire political memory, the federal government, as well as most of our state governments, have been steadily piling “public” debt upon our individual and collective heads. That’s just how it is. We are the frogs trying to make our way in the watery world as the temperature ticks imperceptibly higher. We have been swimming in debt forever, unaware that we’re being economically boiled alive.

Millennials have somewhat modest non-mortgage debt of around $27,000 (some self-reports say twice that much), including car notes, student loans, and credit cards. But we each owe more than $100,000 as a share of the national debt. And we don’t even know it.

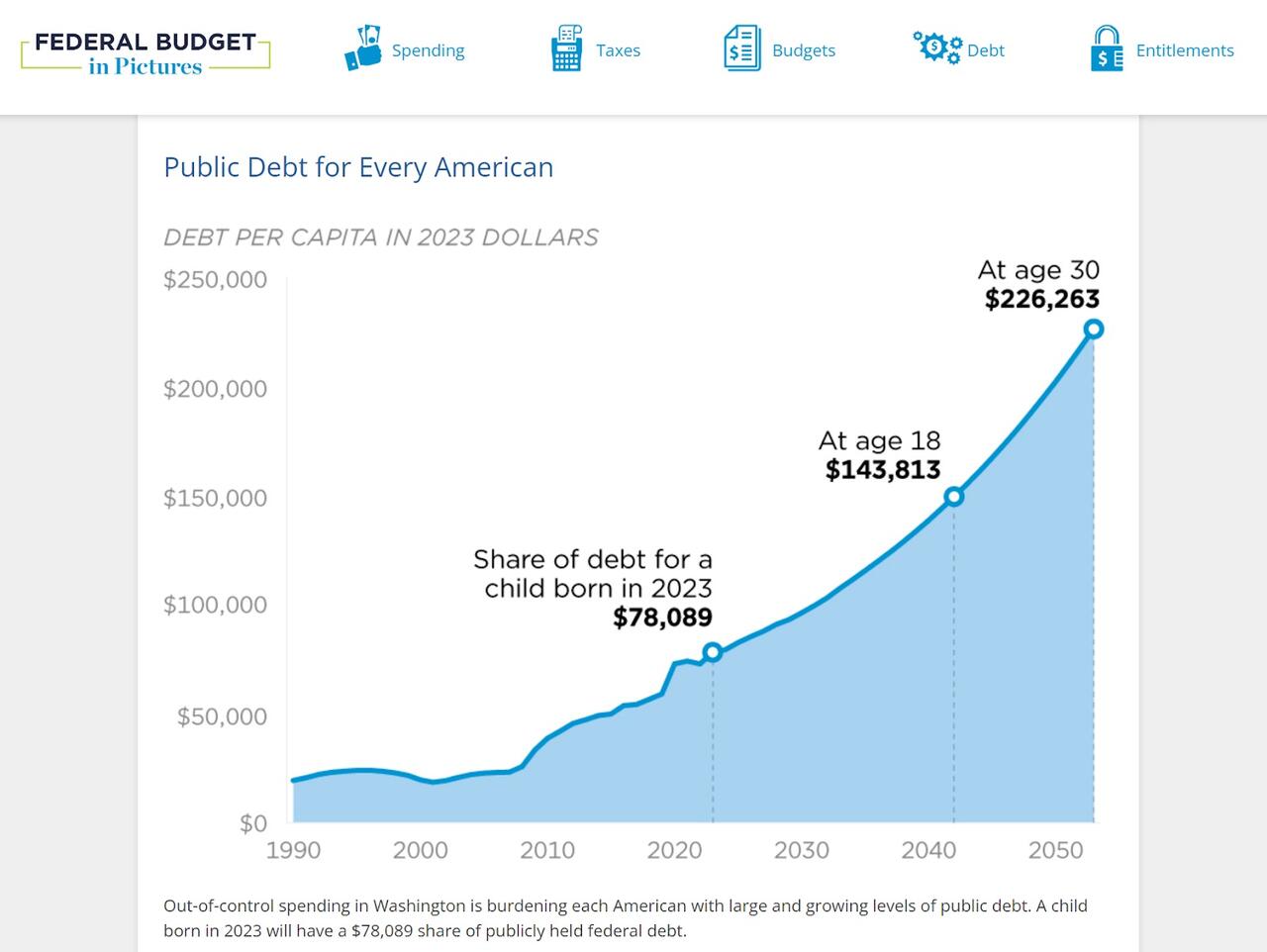

When Millennials finally do have babies (and we are!) that infant born in 2024 will enter the world with a newly minted Social Security Number and $78,089 credit card bill for Granddad’s heart surgery and the interest on a benefit check that was mailed when her parents were in middle school.

Headlines and comments sections love to sneer at “snowflakes” who’ve just hit the “real world,” and can’t figure out how to make ends meet, but the kids are onto something. A full 15 percent of our earnings are confiscated to pay into retirement and healthcare programs that will be insolvent by the time we’re old enough to enjoy them. The Federal Reserve and government debt are eating the economy. The same interest rates that are pushing mortgages out of reach are driving up the cost of interest to maintain the debt going forward. As we learn to save and invest, our dollars are slowly devalued. We’re right to feel trapped.

Sure, if we’re alive and own a smartphone, we’re among the one percent of the wealthiest humans who’ve ever lived. Older generations could argue (persuasively!) that we have no idea what “poverty” is anymore. But with the state of government spending and debt…we are likely to find out.

Despite being richer than Rockefeller, Millennials are right to say that the previous ways of building income security have been pushed out of reach. Our earning years are subsidizing not our own economic coming-of-age, but bank bailouts, wars abroad, and retirement and medical benefits for people who navigated a less-challenging wealth-building landscape.

Redistribution goes both ways. Boomers are expected to pass on tens of trillions in unprecedented wealth to their children (if it isn’t eaten up by medical costs, despite heavy federal subsidies) and older generations’ financial support of the younger has had palpable lifting effects. Half of college costs are paid by families, and the trope of young people moving back home is only possible if mom and dad have the spare room and groceries to make that feasible.

Government “help” during COVID-19 resulted in the worst inflation in 40 years, as the federal government spent $42,000 per citizen on “stimulus” efforts, right around a Millennial’s average salary at that time. An absurd amount of fraud was perpetrated in the stimulus to save an economy from the lockdown that nearly ruined it. Trillions in earmarked goodies were rubber stamped, carelessly added to young people’s growing bill. Government lenders deliberately removed fraud controls, fearing they couldn’t hand out $800 billion in young people’s future wages away fast enough. Important lessons were taught by those programs. The importance of self-sufficiency and the dignity of hard work weren’t top of the list.

Boomer Benefits are Stagnating Hiring, Wages, and Investment for Young People

Even if our workplace engagement suffered under government distortions, Millennials continue to work more hours than other generations and invest in side hustles and self employment at higher rates. Working hard and winning higher wages almost doesn’t matter, though, when our purchasing power is eaten from the other side. Buying power has dropped 20 percent in just five years. Life is $11,400/year more expensive than it was two years ago and deficit spending is the reason why.

We’re having trouble getting hired for what we’re worth, because it costs employers 30 percent more than just our wages to employ us. The federal tax code both requires and incentivizes our employers to transfer a bunch of what we earned directly to insurance companies and those same Boomer-busted federal benefits, via tax-deductible benefits and payroll taxes. And the regulatory compliance costs of ravenous bureaucratic state. The price paid by each employer to keep each employee continues to rise — but Congress says your boss has to give most of the increase to someone other than you.

Federal spending programs that many people consider good government, including Social Security, Medicare, Medicaid, and health insurance for children (CHIP) aren’t a small amount of the federal budget. Government spends on these programs because people support and demand them, and because cutting those benefits would be a re-election death sentence. That’s why they call cutting Social Security the “third rail of politics.” If you touch those benefits, you die. Congress is held hostage by Baby Boomers who are running up the bill with no sign of slowing down.

Young people generally support Social Security and the public health insurance programs, even though a 2021 poll by Nationwide Financial found 47 percent of Millennials agree with the statement “I will not get a dime of the Social Security benefits I have earned.”

In the same survey, Millennials were the most likely of any generation to believe that Social Security benefits should be enough to live on as a sole income, and guessed the retirement age was 52 (it’s 67 for anyone born after 1959 — and that’s likely to rise). Young people are the most likely to see government guarantees as a valid way to live — even though we seem to understand that those promises aren’t guarantees at all.

Healthcare costs tied to an aging population and wonderful-but-expensive growth in medical technologies and medications will balloon over the next few years, and so will the deficits in Boomer benefit programs. Newly developed obesity drugs alone are expected to add $13.6 billion to Medicare spending. By 2030, every single Baby Boomer will be 65, eligible for publicly funded healthcare.

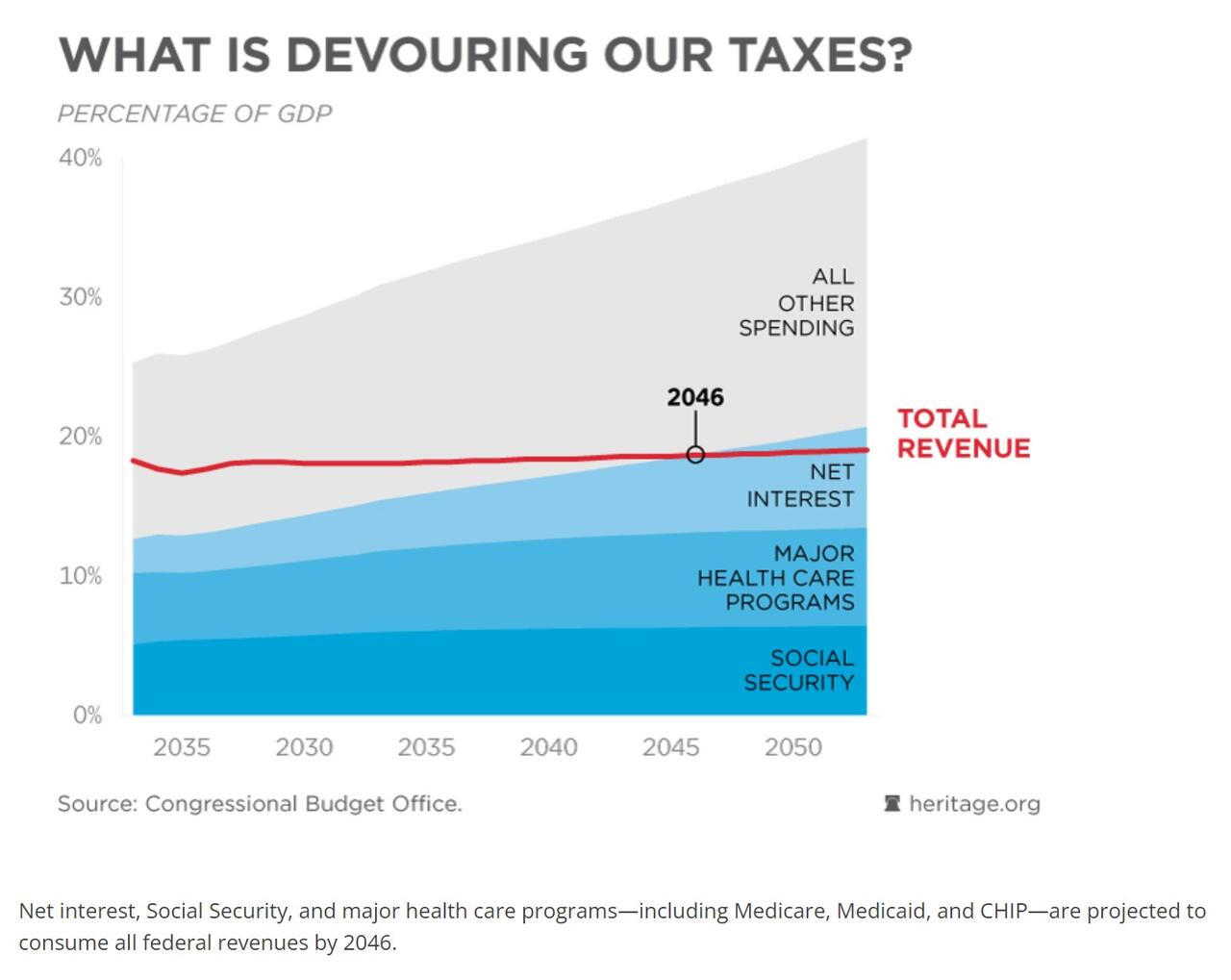

The first Millennial will be eligible to claim Medicare (assuming the program exists and the qualifying age is still 65, both of which are improbable) in 2046. As it happens, that’s also the year that the Boomer benefits programs (which will then be bloated with Gen Xers) and the interest payments we’re incurring to provide those benefits now, are projected to consume 100 percent of federal tax revenue.

Government spending is being transferred to bureaucrats and then to the beneficiaries of government spending who are, in some sense, your diabetic grandma who needs a Medicare-paid dialysis treatment, but in a much more immediate sense, are the insurance companies, pharma giants, and hospital corporations who wrote the healthcare legislation. Some percentage of every college graduate’s paycheck buys bullets that get fired at nothing and inflating the private investment portfolios of government contractors, with dubious, wasteful outcomes from the prison-industrial complex to the perpetual war machine.

No bank or nation in the world can lend the kind of money the American government needs to borrow to fulfill its obligations to citizens. Someone will have to bite the bullet. Even some of the co-authors of the current disaster are wrestling with the truth.

Forget avocado toast and streaming subscriptions. We’re already sensing it, but we haven’t yet seen it. Young people are not well-informed, and often actively misled, about what’s rotten in this economic system. But we are seeing the consequences on store shelves and mortgage contracts and we can sense disaster is coming. We’re about to get stuck with the bill.

Government

Student loan borrowers may finally get answers to loan forgiveness issues

A major student loan service company has been invited to face Congress over its alleged servicing failures.

Share this:

U.S. Sen. Elizabeth Warren (D-MA) wants answers from one of the top student loan service companies in the country for allegedly botching its student loan forgiveness process involving the federal Public Service Loan Forgiveness program, leaving borrowers confused and without answers.

The senator sent a letter to Mohela CEO Scott Giles on March 18 inviting him to testify before Congress at a hearing on April 10 titled “MOHELA’s Performance as a Student Loan Servicer.” During the hearing, Giles will have to answer for why his company allegedly failed to send billing statements to student loan borrowers in a timely manner and miscalculated monthly payments for borrowers when it was time for them to repay their loans in September last year.

Related: Here's who qualifies for Biden's student loan debt relief starting next month

Also, in the letter, Warren highlighted a report that claimed that Mohela failed to perform basic servicing functions for borrowers eligible for PSLF, which led to over 800,000 public service workers facing delays in receiving student debt relief. The report also accuses the company of using a “‘call deflection’ scheme” to keep customers away from speaking to a customer service representative and instead redirecting them to parts of their website.

“Your company has contributed to student loan borrowers’ difficulties by mishandling borrowers’ return to repayment following the COVID-19 pandemic-related pause on payments, interest, and collections and by impeding public servants’ access to PSLF relief,” wrote Warren in the letter.

The move from Warren comes after the U.S. Department of Education withheld $7.2 million in payments to its servicer Mohela in October as punishment because it failed to issue timely billing statements to 2.5 million borrowers which resulted in 800,000 borrowers becoming delinquent on their loans. The department ordered Mohela to put those affected by the issues into forbearance until the mess was resolved.

Mohela is also currently facing two class-action lawsuits, one filed in December last year and another in January this year, for its alleged “failure to timely process and render decisions for student loan borrowers enrolled in the Public Service Loan Forgiveness program.”

In response to recent criticism surrounding its alleged issues and failures regarding the PSLF program, Mohela claimed in a statement to the Missouri Independent that it “does not have authority to process loan forgiveness until authorization is provided by FSA, which can take months to occur.”

The company also claimed that there are “false accusations” inside of the bombshell report, which was released in February, that details the company’s servicing failures.

“It is unfortunate and irresponsible that information is being spun to create a false narrative in an attempt to mislead the public. False accusations are being disingenuously branded as an investigative report,” said Mohela.

white house congress pandemic covid-19International

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

Federal police in Brazil have indicted former President Jair…

Share this:

{kind=link}

{kind=link}

Federal police in Brazil have indicted former President Jair Bolsonaro for falsifying his Covid-19 vaccine card in order to travel to the United States and elsewhere during the pandemic.

{kind=link}

Federal prosecutors will review the indictment and decide whether to pursue the case - which would be the first time the former president has faced criminal charges.

According to the indictment, Bolsonaro ordered a top deputy to obtain falsified Covid-19 vaccine records of himself and his 13-year-old daughter in late 2022, right before he flew to Florida for a three-month stay following his election loss.

Brazilian police are also waiting to hear back from the US DOJ on whether Bolsonaro used said cards to enter the United States, which would open him up to further criminal charges, the NY Times reports.

Bolsonaro has repeatedly claimed not to have received the Covid-19 vaccine, but denies any involvement in a plan to falsify his vaccination records. A previous investigation by Brazil's comptroller general concluded that Bolsonaro's vaccination records were false.

The records show that Bolsonaro, a COVID-19 skeptic who publicly opposed the vaccine, received a dose of the immunizer in a public healthcare center in Sao Paulo in July 2021. [ZH: hilarious, Reuters calling the vaccine an 'immunizer.']

The investigation concluded, however, that the former president had left the city the previous day and didn't leave Brasilia until three days later, according to a statement.

The nurse listed in the records as having applied the vaccine on Bolsonaro denied doing so and was no longer working at the center. The listed vaccine lot was also not available on that date, the comptroller general's office said. -Reuters

"It's a selective investigation. I'm calm, I don't owe anything," Bolsonaro told Reuters. "The world knows that I didn't take the vaccine."

During the pandemic, Bolsonaro panned the vaccine - and instead insisted on alternative treatments such as Ivermectin, which has antiviral properties against Covid-19. For this, he was investigated by Brazil's congress, which recommended that the former president be charged with "crimes against humanity," among other things, for his actions during the pandemic.

In May, Brazilian police raided Bolsonaro's home, confiscating his cell phone and arresting one of his closest aides and two of his security cards in connection to the vaccine record investigation.

Brazil's electoral court ruled that Bolsonaro can't run for public office until 2030 after he suggested that the country's voting system was rigged. For that, he has to sit out the 2026 election.

Google’s A.I. Fiasco Exposes Deeper Infowarp

Greenback Surges after BOJ Hikes and Ends YCC and RBA Delivers a Dovish Hold

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Student loan borrowers may finally get answers to loan forgiveness issues

You can strike gold and silver investment opportunities at Costco

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

TikTok Ban Obscures Chinese Stock Gold Rush

Bolsonaro Indicted By Brazilian Police For Falsifying Covid-19 Vaccine Records

Report Criticizes ‘Catastrophic Errors’ Of COVID Lockdowns, Warns Of Repeat

Anti-Semitism As The Harbinger Of Global Chaos

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex