Uncategorized

HS Management Partners, LLC Looks to the Next 15 Years

HS Management Partners, LLC Looks to the Next 15 Years

PR Newswire

NEW YORK, March 2, 2023

NEW YORK, March 2, 2023 /PRNewswire/ — HS Management Partners, LLC (HSMP), a boutique equity investment advisor, is proud to announce several milestones as …

Share this:

HS Management Partners, LLC Looks to the Next 15 Years

PR Newswire

NEW YORK, March 2, 2023

NEW YORK, March 2, 2023 /PRNewswire/ -- HS Management Partners, LLC (HSMP), a boutique equity investment advisor, is proud to announce several milestones as we near completion of year 16 of our performance track record, ending March 31st, 2023 for its sole investment strategy, the HSMP Concentrated Quality Growth Equity portfolio.

The Firm, located at 640 Fifth Avenue in New York City, was established in 2007 and currently advises assets approaching $2.5 billion applying a focused, bottom-up fundamentals-first approach to portfolio construction.

HSMP Composite Performance as of 12/31/22 | |||||||

4Q22 | 2022 | 3 Years | 5 Years | 10 Years | Since Inception | Since Inception | |

HSMP Composite (Net) | 13.5 % | -17.7 % | 6.9 % | 9.7 % | 13.1 % | 11.4 % | 448.3 % |

S&P 500® Index | 7.6 % | -18.1 % | 7.7 % | 9.4 % | 12.6 % | 8.7 % | 271.7 % |

Russell 1000® Growth Index | 2.2 % | -29.1 % | 7.8 % | 11.0 % | 14.1 % | 10.5 % | 382.0 % |

Performance results are net of fees and include the reinvestment of dividends and other earnings. Past performance is not indicative of future results. | |||||||

Harry Segalas, Managing Partner & Chief Investment Officer, remarks, "Since inception, our Composite has annualized compounded returns at a 11.4% annual post-fee rate (net-of-fees) (4/1/2007 through 12/31/2022). The power of this compounding shows that cumulative returns (net-of-fees) amounted to 448.3% in that period and that $1 million invested at our start (4/1/2007) is now worth $5,482,900 (see Performance table above). We believe this represents a strong track record during that period, even in the face of three Black Swan events in the past 15 years (the Global Financial Crisis in 2008, the Pandemic in 2020, and the Russian Invasion of Ukraine in 2022).

Continuing forward, we remain committed to our sole concentrated quality growth methodology. This includes a strong valuation discipline and active management. Undoubtedly, we will face many challenges but believe this approach will serve clients well in our drive toward absolute returns in the years ahead. Many thanks to the incredible HS Management Partners team that has been assembled over the years, and thanks most of all to our clients, entrusting us with the management of their valuable assets. It is a responsibility that we take with utmost seriousness."

Greg Nejmeh, Partner, President & Investment Strategist, adds, "The key to our future is the same as the key to our past – our culture. When asked by a client along the way what was the best decision we'd made, and after some reflection, I offered our best decision was to model HS Management Partners in a manner consistent with the criteria we prize among our portfolio holdings: a long-term market perspective, a highly focused approach, and a relentless emphasis on quality in people, processes, products, and services. We invested behind the core of our convictions, and that has made, and will continue to make, all the difference."

"As we move forward, we are proud of the inclusive and diverse team of professionals we have assembled, and we have continued to invest in our capabilities (investment, client, and operational) with an intent to grow Firm assets. We view ourselves as a "QARP" manager – quality at a reasonable price – and our benchmark agnostic approach has served clients well (see our latest Thought Piece, entitled "The Market Square…The HSMP Circle"). We are proud to have been recently recognized by Zephyr's PSN as a "Top Gun" in their latest quarterly rankings and having been identified by Nasdaq eVestment in recent quarters of their Brand Awareness Rankings. We hope to build on our internal initiatives and external recognition to grow the Firm while maintaining focus on our singular strategy."

With David Altman, Partner and Director of Research and Bart Buxbaum, Partner and Chief Administrative Officer, the four Partners have over 160 years of combined industry experience. In total, HSMP consists of 18 professionals with an average of 28 years of experience. The entire HSMP team is determined to continue to manage and service client assets with the same purpose, resolve and integrity that have served as the blueprint for past success.

For HSMP market commentary and quarterly updates, follow the HSMP LinkedIn page or #HSPerspectives. For additional information on HSMP, visit the Firm's website at www.hsmanage.com which includes a Firm video or contact Tom Bylaitis or Patti Norton at 212-888-0060 or info@hsmanage.com.

Important Disclosures

This piece represents our opinion as of 3/2/23 based on our understanding of market conditions and publicly available information and is intended for Institutional and High-Net-Worth investors only. This piece is written from the perspective of our investment philosophy and strategy, Composite holdings, performance, and estimated outlook and metrics, and it does not refer to any specific client account (client accounts can have higher or lower performance than that shown here). The performance shown here should not be taken as an indication of how the Composite or a client account will perform in the future; past performance is not indicative of and does not guarantee future results.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; "believe,", "anticipate," "estimated," and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio's operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of HSMP, its affiliates, principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.

Investing in securities involves significant risks, including the risk of loss of the original amount invested.

Refer to our Firm Brochure (at http://www.hsmanage.com/documents/ or upon request at 212-888-0060) for material risks applicable to our strategy and information regarding our Firm. The information here is solely for illustration or discussion, is subject to change without notice, should not be construed as a recommendation to buy or sell any particular security, and should not be used as basis for making investment decisions.

The Composite is compared to the Russell 1000® Growth Index and the S&P 500® Index as benchmarks for market context only. The Russell 1000 Growth Index is an unmanaged index that measures the performance of those Russell 1000® Index companies (largest 1,000 U.S. companies based on market capitalization) with higher price-to-book ratios and higher forecasted growth values. The S&P 500® Index is an unmanaged market capitalization-weighted index designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. There are meaningful differences between the Composite and each index that should be considered when comparing performance, such as in terms of composition, concentration and volatility (e.g., the Composite contains securities not represented in either or both indices and is much more concentrated than either index in terms of companies and sectors; the average market capitalization of companies in the Composite will likely differ from that of either index; and market or economic conditions can affect positively/negatively the Composite's performance but not the indices to the same extent). Neither index bears fees and expenses and investors cannot invest directly in either of them. We do not seek to mimic any market index in our investment approach and do not maintain limits on industry or sector weightings. For these and other reasons the Composite does not directly relate to an index. Although most discretionary client accounts are included in the Composite and dispersion is typically low over time, not all client accounts are in the Composite, and even for those in the Composite, there can be dispersion, particularly for small client accounts and also when viewed over narrow time periods. Client account holdings and performance can deviate from our Composite and/or from other client accounts, and also from the representative portfolio, for several reasons, such as: client restrictions, account type and size, timing and market conditions at an account's inception and contributions/withdrawals, timing and terms of trades, actual client investment advisory fees (or the lack thereof), and client directed brokerage/commission recapture instructions.

eVestment Alliance, LLC and its affiliated entities (collectively, "eVestment") collect information directly from investment management firms and other sources. Performance results may be provided with additional disclosures available on eVestment's systems and other important considerations such as fees that may be applicable. Not for general distribution and limited distribution may only be made pursuant to client's agreement terms. Zephyr is a subsidiary of Informa plc and publishes their PSN Top Guns List on PSN, an investment manager database and a division of Informa (collectively, "PSN Informa"). PSN Top Guns relies on data provided by third-party sources. The peer groups were created using the information collected through the PSN investment manager questionnaire and uses only gross of fee returns. PSN Top Guns investment managers must claim that they are GIPs compliant. These top performers are strictly based on current quarter returns. Copyright 2012-2023 eVestment Alliance, LLC. Copyright 2023 Informa Intelligence, Inc. All Rights Reserved. eVestment and PSN Informa do not guarantee or warrant the accuracy, adequacy, timeliness, or completeness or availability of the information provided, and neither is responsible for any errors or omissions or for the results obtained from the use of such information.

HSMP pays eVestment and PSN Informa to collect our data that is used to provide data and other to information to qualified investment professionals and financial institutions. HSMP does not compensate eVestment or PSN Informa directly for their rankings. HSMP has been ranked in the Top 20 of the Nasdaq eVestment Brand Awareness Rankings in the Single Product Firm category among both Consultants and Asset Owners for the prior three quarters in 2022. HSMP has been ranked in the PSN Top Guns list for both the Large Growth Universe and US Growth Universe categories.

This document includes general information and has not been tailored for any specific recipient or recipients. Accordingly, the information here is not intended to cause HSMP to become a fiduciary within the meaning of Section 3(21)(A)(ii) of the Employee Retirement Income Security Act of 1974, as amended, or Section 4975(e)(3)(B) of the Internal Revenue Code of 1986, as amended.

Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell 1000® Growth Index. Russell® is a trademark of Russell Investment Group. S&P 500® Index is a registered trademark of Standard and Poor's Financial Services LLC, a division of the McGraw-Hill Companies, Inc. Standard & Poor's is the owner of the trademarks, service marks, and copyrights related to its indexes. GIPS® is a registered trademark of the CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein. Neither Standard and Poor's nor Russell Investment Group endorses, promotes, or sponsors HSMP. The marks, trade names, or copyrighted work included in this document are mentioned for identification purposes only and are the property of their respective owners.

HS Management Partners, LLC ("HSMP", "HS Management Partners", or the "Firm"). For information or questions contact us at 212-888-0060.

View original content to download multimedia:https://www.prnewswire.com/news-releases/hs-management-partners-llc-looks-to-the-next-15-years-301761062.html

SOURCE HS MANAGEMENT PARTNERS, LLC

Uncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

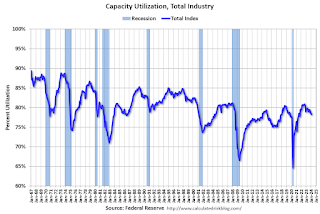

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Uncategorized

Southwest and United Airlines have bad news for passengers

Both airlines are facing the same problem, one that could lead to higher airfares and fewer flight options.

Share this:

{kind=link}

Airlines operate in a market that's dictated by supply and demand: If more people want to fly a specific route than there are available seats, then tickets on those flights cost more.

That makes scheduling and predicting demand a huge part of maximizing revenue for airlines. There are, however, numerous factors that go into how airlines decide which flights to put on the schedule.

Related: Major airline faces Chapter 11 bankruptcy concerns

Every airport has only a certain number of gates, flight slots and runway capacity, limiting carriers' flexibility. That's why during times of high demand — like flights to Las Vegas during Super Bowl week — do not usually translate to airlines sending more planes to and from that destination.

Airlines generally do try to add capacity every year. That's become challenging as Boeing has struggled to keep up with demand for new airplanes. If you can't add airplanes, you can't grow your business. That's caused problems for the entire industry.

Every airline retires planes each year. In general, those get replaced by newer, better models that offer more efficiency and, in most cases, better passenger amenities.

If an airline can't get the planes it had hoped to add to its fleet in a given year, it can face capacity problems. And it's a problem that both Southwest Airlines (LUV) and United Airlines have addressed in a way that's inevitable but bad for passengers.

Image source: Kevin Dietsch/Getty Images

Southwest slows down its pilot hiring

In 2023, Southwest made a huge push to hire pilots. The airline lost thousands of pilots to retirement during the covid pandemic and it needed to replace them in order to build back to its 2019 capacity.

The airline successfully did that but will not continue that trend in 2024.

"Southwest plans to hire approximately 350 pilots this year, and no new-hire classes are scheduled after this month," Travel Weekly reported. "Last year, Southwest hired 1,916 pilots, according to pilot recruitment advisory firm Future & Active Pilot Advisors. The airline hired 1,140 pilots in 2022."

The slowdown in hiring directly relates to the airline expecting to grow capacity only in the low-single-digits percent in 2024.

"Moving into 2024, there is continued uncertainty around the timing of expected Boeing deliveries and the certification of the Max 7 aircraft. Our fleet plans remain nimble and currently differs from our contractual order book with Boeing," Southwest Airlines Chief Financial Officer Tammy Romo said during the airline's fourth-quarter-earnings call.

"We are planning for 79 aircraft deliveries this year and expect to retire roughly 45 700 and 4 800, resulting in a net expected increase of 30 aircraft this year."

That's very modest growth, which should not be enough of an increase in capacity to lower prices in any significant way.

United Airlines pauses pilot hiring

Boeing's (BA) struggles have had wide impact across the industry. United Airlines has also said it was going to pause hiring new pilots through the end of May.

United (UAL) Fight Operations Vice President Marc Champion explained the situation in a memo to the airline's staff.

"As you know, United has hundreds of new planes on order, and while we remain on path to be the fastest-growing airline in the industry, we just won't grow as fast as we thought we would in 2024 due to continued delays at Boeing," he said.

"For example, we had contractual deliveries for 80 Max 10s this year alone, but those aircraft aren't even certified yet, and it's impossible to know when they will arrive."

That's another blow to consumers hoping that multiple major carriers would grow capacity, putting pressure on fares. Until Boeing can get back on track, it's unlikely that competition between the large airlines will lead to lower fares.

In fact, it's possible that consumer demand will grow more than airline capacity which could push prices higher.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic stocks

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

The best real estate coaching programs for 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex