Government

Futures Surge On Even More “Optimism” Ahead Of Payrolls

Futures Surge On Even More "Optimism" Ahead Of Payrolls

Share this:

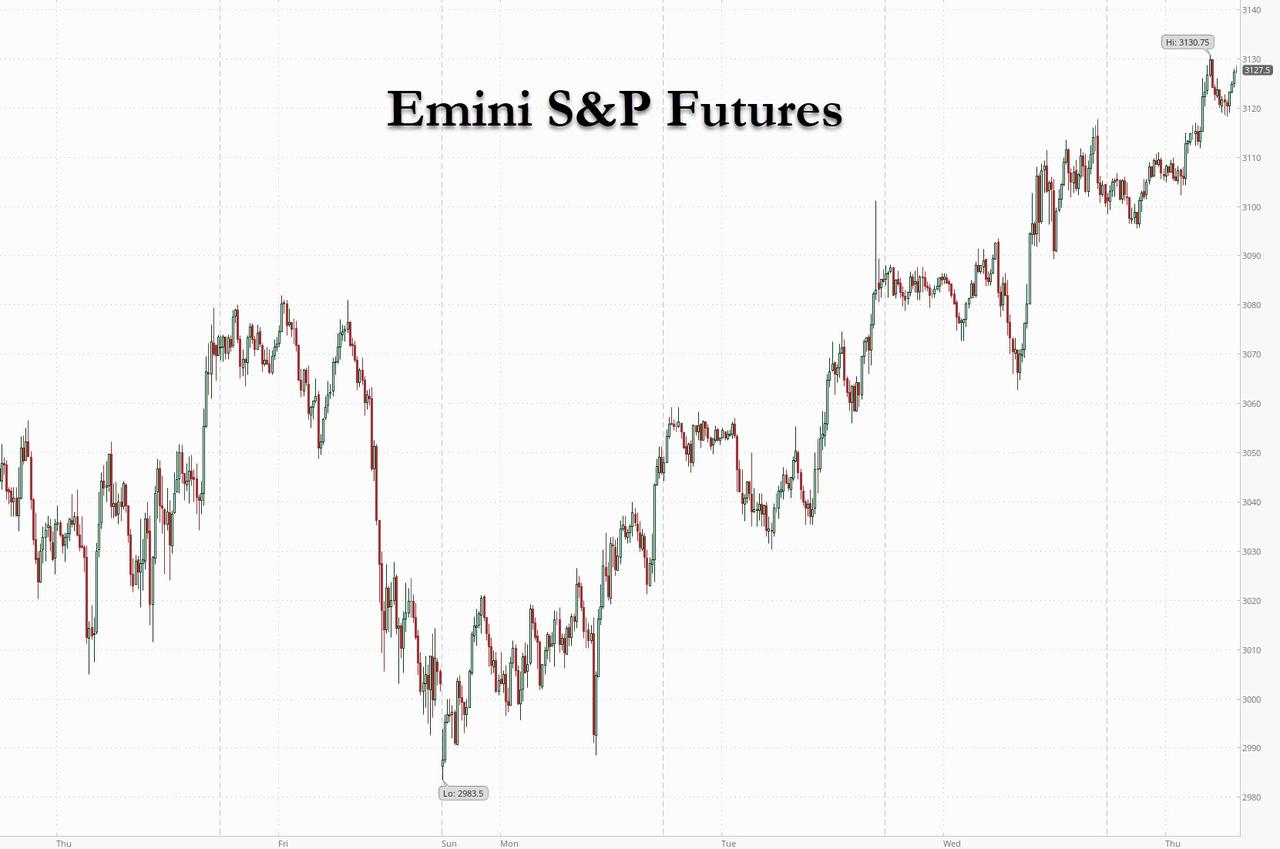

After sliding to 2,983.5 in early Sunday trading on fears of a second wave of covid infections, futures have completely forgotten what they were concerned about at the start of the week, and have since levitated in largely linear fashion some 150 points higher, rising to 3,130.75 overnight, on even more hope and optimism, this time for a reassuring job report coupled with yesterday's hopes for positive vaccine developments. The dollar slipped and 10Y yields rose.

At 7:20 a.m. ET, Dow e-minis were up 275 points, or just over 1%, S&P 500 e-minis were up 25 points to 3,128, and Nasdaq 100 e-minis were up 52 points to 10320. Travel-related stocks were among the biggest gainers in premarket trade, with cruise line operators Carnival, Royal Caribbean Cruises and Norwegian Cruise Line Holdings rising between 3% and 4%, while economically-sensitive stocks including Morgan Stanley, Goldman Sachs, Citigroup, JPMorgan Chase and Bank of America up between 1% and 3%. Tesla was up another $100 overnight, rising to a new record high above 1,200.

Indeed, as Reuters writes this morning, "optimism about a post-pandemic rebound in business activity, aggressive U.S. stimulus and hopes of a COVID-19 vaccine" have fueled a Wall Street rally since April, with the tech-heavy Nasdaq notching up its sixth record closing high since early June on Wednesday.

After the latest ISM data showed U.S. manufacturing unexpectedly hit its highest level in June in more than a year, the Labor Department’s jobs report due later in the day is expected to show record job growth last month, signaling that a COVID-19-driven recession was probably over, at least until its returns next month when government stimulus checks run out. Meanwhile, with several states scaling back or pausing reopenings to tackle a recent surge in coronavirus infections, analysts have warned of another selloff in financial markets if the damage to Corporate America mounts.

Third-quarter earnings for S&P 500 companies are now expected to tumble 25%, compared with a forecast of a 2.7% drop on April 1, according to Refinitiv. In the second quarter, earnings are forecast to have plunged 43%.

Europe's Stoxx 600 Index extended its initial gains on advances in banks and automakers with the Eurostoxx 50 rallying as much as 1.9% to fresh highs for the week; IBEX outperforms, gaining over 2.5%. Europe's Stoxx 600 Travel & Leisure index rose as much as 3.6%, the most since June 16, led by airlines and gaming stocks. IAG was up as much as 7.4% and EasyJet advances 6.6%; the U.K. is planning to lift quarantine rules for 75 countries, according to a report in the Telegraph. Gaming stocks including GVC (+3.1%) and Flutter (+2.9%) also higher after brushing off a U.K. House of Lords report calling for the introduction of new rules to reduce gambling-related harm.

Asian stocks also gained, led by communications and energy, after ending flat in the last session. Hong Kong shares outperformed after traders returned from a holiday, despite the recent tensions over China’s new national security law over the city. The Shanghai Composite turned positive for the year to date, with Zhangjiagang Freetrade Science & Technology Group and Xinjiang Tianye posting the biggest advances. Stocks in Australia, China, Japan and South Korea also rose. The Topix gained 0.3%, with Retail Partners and GungHo Online rising the most. Trading volume for MSCI Asia Pacific Index members was 62% above the monthly average for this time of the day.

"The rally for equities could survive even if the U.S. jobs data disappoint, after the Fed’s signal of sustained low rates,” said Stephen Gallo, a foreign-exchange strategist at the Bank of Montreal. “Bad numbers could extend that outlook for cheap money." Translation: a good jobs number will be good, a bad jobs number will be better.

In rates, Treasuries were little changed on light volume in futures ahead of the June jobs report and the early close in the bond market (Sifma-recommended 2pm ET close before U.S. holiday Friday). Narrow yield ranges have prevailed so far with risk-takers sidelined before the pandemic-inflected data. Yields slightly cheaper across long-end of the curve, still within ~1bp of Wednesday’s close; 10-year ~0.68%, cheaper by 0.5bp, while bunds, gilts outperform by 2bp and 1.5bp. Core European bonds were aided by French debt rally after the oversubscription rate for sale of 10-year bonds rose to highest since May 2019.

In FX, the dollar dropped as haven bids waned after the abovementioned optimism bolstered bets for a global economic recovery, with market focus shifting to an upcoming U.S. jobs report. The euro touched a one-week high versus the greenback, with options pointing to more upside for the common currency. Three-month EUR/USD risk reversals are the most bullish since mid- March, while the six-month measure rose above parity for the first time since the pandemic panic four month ago. Norway’s krone saw the biggest gains against the dollar among Group-of-10 peers, partly boosted by the climb in oil prices.

In commodities, oil futures climbed for a second session, helped by a strong drawdown in crude stockpiles, while gold rebounded to session highs, silver was trading back over $18/oz.

Market Snapshot

- S&P 500 futures up 0.8% to 3,126.75

- STOXX Europe 600 up 1.3% to 365.79

- MXAP up 1.5% to 160.15

- MXAPJ up 1.9% to 525.40

- Nikkei up 0.1% to 22,145.96

- Topix up 0.3% to 1,542.76

- Hang Seng Index up 2.9% to 25,124.19

- Shanghai Composite up 2.1% to 3,090.57

- Sensex up 1.7% to 36,008.91

- Australia S&P/ASX 200 up 1.7% to 6,032.71

- Kospi up 1.4% to 2,135.37

- German 10Y yield fell 0.4 bps to -0.399%

- Euro up 0.4% to $1.1294

- Brent Futures up 0.9% to $42.42/bbl

- Italian 10Y yield rose 1.2 bps to 1.143%

- Spanish 10Y yield fell 2.5 bps to 0.477%

- Brent Futures up 0.9% to $42.42/bbl

- Gold spot up 0.06% to $1,771.08

- U.S. Dollar Index down 0.3% to 96.86

Top Overnight News from Bloomberg

- Russian President Vladimir Putin won a resounding endorsement of his bid to extend his two-decade-long rule potentially to 2036, even as some polls show his approval ratings near historic lows

- U.S. daily coronavirus cases topped 50,000 for the first time. Oxford’s vaccine project is currently ahead of others, but the world needs more than one type of shot to tackle the new coronavirus, said U.S. infectious-disease expert Anthony Fauci

- Sovereign borrowers including Germany, Ireland, Italy, Spain and the U.K. helped the SSA sector to lead a record setting second quarter as marketwide sales reached EU607.92b, according to data analyzed by Bloomberg

- Ukraine canceled a $1.75 billion Eurobond sale after the head of its central bank unexpectedly stepped down citing sustained political pressure against him and his colleagues

- China warned of strong countermeasures if the U.S., Australia and the U.K. continued taking actions in response to Beijing’s tough national security law in Hong Kong, saying foreign pressure would “never succeed”

- Yuan trading is the calmest since January as investors evaluate the virus pandemic and China-U.S. tensions

Asian equity markets traded positively after the region took advantage of the mild tailwinds from Wall St where stocks finished mostly higher on vaccine hopes and equity inflows as Q3 trading got underway, although gains were mild in the absence of any improvement to the increasing COVID-19 infections narrative stateside, where new cases surpassed 50k for the first time. ASX 200 (+1.7%) was lifted by strength in tech with the sector inspired following the recent outperformance of the Nasdaq which posted a record close in the preceding session, while Nikkei 225 (+0.1%) shrugged off the early choppy price action which had been at the whim of an indecisive currency. Hang Seng (+2.9%) and Shanghai Comp. (+2.1%) were also upbeat as the constructive tone seen across the continent helped participants overlook another PBoC liquidity drain, as well as the continued US-China tensions after the China Foreign Ministry announced fresh actions against US media and the US House passed China sanctions in response to the HK national security law. Finally, 10yr JGBs were subdued amid gains in stocks and with yields extending to the upside as observed in the 30yr yield which rose to its highest since January last year, while a bout of strength seen on return from the Tokyo lunch break was short-lived due to the mixed results from the 10yr JGB auction.

Top Asian News

- U.S. Readies ‘Harsh’ Sanctions on China Over Abuses in Xinjiang

- China-Sanctions Bill on Hong Kong Law Passed by U.S. House

- South Indian Bank Proposes Former ICICI Banker as Next CEO

- Landslide in Myanmar’s Jade Mining Hub Leaves 113 People Dead

European equities continue to march higher as the second trading session in H2 is underway (Euro Stoxx 50 +1.5%) following on from a similarly stellar APAC performance – with gains in stocks attributed to COVID-19 vaccine optimism coupled with Q3 inflows. The fundamental landscape has not shifted much but the narrative of rising case counts has not subsided, with US cases topping 50k additions for the first time whilst a record increase was also reported in Indonesia. Furthermore, the Hong National Security Law keeps tensions riled up between China and G10 nations, with US House passing the China sanctions bill in response to the HK national security law through unanimous consent. Nonetheless, Europe extends on gains seen at the open with Spain’s IBEX (+2%) outperforming as the index is propped up by outperformance in Banks and Travel & Leisure. Meanwhile, Autos, construction and insurance sectors also reside near the top of the pile whilst Healthcare and consumer staples trade on the other side of the spectrum. Cyclicals clearly outpace defensives. In terms of individual movers, Wirecard (-27%) shares are on the backfoot amid reports Softbank is to end its partnership with the Co. Meanwhile, Associated British Foods (+5.3%) holds onto a bulk of its gains after reporting that almost all of its Primark stores have reopened and the group continues to expect strong progress in aggregate adjusted operating profit in sugar, grocery, agriculture and ingredients businesses.

Top European News

- Ukraine Cancels Eurobond Sale After Central Bank Chief Quits

- China Strongly Condemns U.K. Offer to Hong Kong Citizens

- Novartis to Pay $678m to Settle Fraud Lawsuit, U.S. DOJ says

- Blast at Glencore Oil Refinery in Cape Town Leaves Three Dead

In FX, the Dollar continues to depreciate amidst rather contradictory or juxtaposed impulses via more signs that the US and global economy has turned the corner from initial coronavirus-related shutdowns vs concerns about the impact of re-opening and a 2nd wave. Hence, a double whammy for the Buck as fresh COVID-19 outbreaks spread to more states that have lifted restrictions, but the overall risk environment remains positive and the DXY loses grip of the 97.000 handle ahead of NFP, the more timely weekly jobless claims update, trade data and factory orders, all truncated due to Friday’s market closure for Independence Day.

- NZD/EUR/GBP/AUD/CHF - The Kiwi is back above 0.6500, thanks in part to general Greenback weakness, but also deriving momentum from closer to home as the Aussie lags in wake of weaker than forecast trade data overnight. In response, Aud/Nzd has retreated from circa 1.0675 to sub-1.0640 and Aud/Usd has not been able to revisit 0.6950 against the backdrop of heavy option expiry interest at 0.6895 (1.8 bn) and in the Aud/Jpy cross close to current levels, at 74.50 (1 bn). Similarly, the Euro and Pound are both making more headway against the Dollar, with Eur/Usd probing above 1.1300 and Cable now over 1.2500 as Eur/Gbp eyes 0.9000 to the downside on reports of real money Sterling buyers. Note, the single currency may also be capped by significant expiries at 1.1300 (2 bn), but should glean support from slightly bigger options rolling off at 1.1250 (2.2 bn). Elsewhere, the Franc has extended gains vs the Buck towards 0.9425 in contrast to marginal underperformance against the Euro around 1.0650 following slightly softer than expected Swiss CPI metrics.

- JPY/CAD - Both narrowly mixed vs the Usd, as the Yen weighs up bullish risk sentiment alongside latest Greenback declines and treads a fine line between 107.55-35 with a decent 107.50 expiry (1 bn) also in contention for the NY cut pending reaction to US data. Conversely, the Loonie has reversed further from recent highs to pivot 1.3600 in advance of Canadian trade and manufacturing PMI, as underlying traction from crude stalls somewhat.

- SCANDI/EM - Broad strength on the ongoing risk-friendly start to July, Q3 and H2, and with the Zar also benefiting from another upside SA data surprise in the form of a Q1 current account surplus, while the Rub is underpinned by reduced political uncertainty on the domestic front after more than ¾ of the country voted in favour of Russia’s new constitution. However, the Try remains hampered due to renewed geopolitical jitters, albeit still stemming losses with the aid of Turkish bank intervention.

In commodities, WTI and Brent front-month futures hold onto earlier gains, albeit have drifted off highs in recent trade with little by way of fresh fundamental drivers as the oil complex piggybacks on risk sentiment. On the OPEC front, interesting reports overnight from delegates noted that Saudi Arabia threatened to re-ignited an oil price war in past weeks if other OPEC countries do not adhere to their quotas. The headline, however, gained little traction as OPEC laggards have, at face value, been taking steps to improve compliance in line with the OPEC+ pact. Meanwhile, Russian Energy Minister Novak hopes the global oil market reaches a balance/shortage in July but noted a second wave of COVID-19 could impact on oil demand. WTI trades on either side of USD 40/bbl (39.50-40.40/bbl range) whilst Brent Sep holds its head above USD 42/bbl (41.73-42.66/bbl).Price action today will likely be dictated by pandemic-related headlines alongside the US labour market report, whilst the Baker Hughes Rig Count will be released today on account of tomorrow’s Independence Day market holiday. Elsewhere, spot gold remains contained around recent ranges on either side of USD 1770/oz as the yellow metal bides its time ahead of NFP. Copper prices meanwhile are experiencing a day of correction after its recent supply-led gains.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 1.35m, prior 1.48m; Continuing Claims, est. 19m, prior 19.5m

- 8:30am: Change in Nonfarm Payrolls, est. 3.06m, prior 2.51m

- Change in Private Payrolls, est. 3m, prior 3.09m

- Change in Manufact. Payrolls, est. 437,500, prior 225,000

- Unemployment Rate, est. 12.5%, prior 13.3%

- Underemployment Rate, prior 21.2%

- Labor Force Participation Rate, est. 61.2%, prior 60.8%

- Average Weekly Hours All Employees, est. 34.5, prior 34.7;

- Average Hourly Earnings MoM, est. -0.7%, prior -1.0%; Average Hourly Earnings YoY, est. 5.3%, prior 6.7%

- 8:30am: Trade Balance, est. $53.2b deficit, prior $49.4b deficit

- 9:45am: Bloomberg Consumer Comfort, prior 41.4

- 10am: Factory Orders, est. 8.65%, prior -13.0%; Factory Orders Ex Trans, est. 6.5%, prior -8.5%

- 10am: Durable Goods Orders, est. 15.8%, prior 15.8%; Durables Ex Transportation, est. 4.0%, prior 4.0%

- 10am: Cap Goods Orders Nondef Ex Air, est. 2.3%, prior 2.3%; Cap Goods Ship Nondef Ex Air, prior 1.8%

DB's Jim Reid concludes the overnight wrap

After the market’s batteries were fully charged after an incredibly strong Q2, the second half started off on a mixed note yesterday, but positivity again won out in the end. After a soft start in Europe, risk assets were boosted early in the US session by some promising developments in a vaccine trial. However we gave back all of the early US session gains as Arizona saw a record rise in new cases late morning US time. The US regained its poise into the close though with the S&P 500 ending +0.50%.

The vaccine specific news came through from Pfizer (+3.18%) and BioNTech (-3.90%, though opened +18.9%), who announced that those patients who’d received two doses of their vaccine candidate had “significantly elevated” antibodies, raising hopes among investors that we could see a vaccine later this year if further tests prove successful. Both stocks saw late losses though, possibly on a Bloomberg report that the Food and Drug Administration’s new standards on Covid-19 vaccine development may mean a longer roll out than anticipated. The standard, published on Tuesday, said that any potential vaccine would need to prove itself at least 50% more effective than a placebo to earn an approval. Merely showing immune response data would not be enough to be administered.

In terms of the virus, Arizona reported a record daily increase in cases of 4,865 (6.2% vs the 7-day average of 4.5%). Arizona has had some reporting issues over the last few days so single day data is dangerous to over analyse. Their fatality number hit a new high of 80, above the 7-day average of 36 and exceeding the previous high of 71 last Wednesday. However our back of the envelope calculations suggest that with the 7-day lag between cases and fatalities we saw globally in the first wave, the 7 day run rate of Arizona deaths would now be in the 130 (using Germany) to 160 (using New York) range if the pattern and case fatality rates had stayed the same. In 7 days’ time it should be in the 250 to 300 range, given current case increases. So one to watch and whilst fatalities will of course go up they are still not yet seeing the pickup consistent with first wave trends.

The US overall has now seen over 41,000 new cases on average over the last week, well above the 32,000 peak seen in April. Florida saw numbers rise by 4.3% vs 5.7% over the past 7 days, while the positive test rate grew to a high of 15%, indicating that the real case count in the state is likely much higher. California saw another record with over 9740 new infections, the 5.0% rise compared to a 2.8% average rise over the last week. See the latest from around the world and the four troubled US states in the pdf today.

The recent rise in California cases has caused Governor Newsom to shutdown indoor businesses including restaurants, bars, museums and movie theaters in 19 counties. Citing a small pickup in cases within Pennsylvania (5th largest US state) and the caseload of the country overall, Governor Wolf mandated that masks be worn at all times when leaving the house. Elsewhere yesterday saw New York City Mayor de Blasio announce that the planned reopening of indoor dining next week would be postponed, given the rising numbers of cases in the US. New York State overall is now opening testing to all residents, as capacity has increased sufficiently. Overnight, Bloomberg has reported that McDonald’s is pausing the resumption of all dine-in services in its US restaurants with the halt likely to last 21 days.

Staying with lockdowns, we have also published the latest Exit Strategy Tracker (Link here) which compares exits across the world. In this edition we preview holiday season by assessing which countries seem the most sensible places to have break in this summer given various criteria. We’re not quite branching out into travel guides yet but it will give you a guide to openness.

Back to markets and thanks to the initial vaccine developments, global equity markets recovered from their early declines, with the STOXX 600 paring back its intraday low of -1.02% to close +0.24% higher. In the US, the market was boosted by a +11.72% gain for FedEx after the company announced much stronger than expected earnings, while tech stocks outperformed with the NASDAQ up +0.95%. The other big company news yesterday was that Tesla overtook Toyota to become the world’s most valuable automaker, following more than a five-fold increase in the company’s share price over the last 12 months. At the end of last May the stock was trading at just under 180 while yesterday it closed at 1119.6. In that time the stock gained +412%, and then lost over -60% during the pandemic selloff in March before soaring (+210%) off the pandemic lows.

Overnight, Asian markets have tracked gains on Wall Street with the Nikkei (+0.49%), Hang Seng (+1.49%), Shanghai Comp (+1.16%), Kospi (+0.83%) and ASX (+1.35%) all advancing. Futures on the S&P 500 are also up +0.11%.

Today, market attention will turn to the US jobs report for June, which is out on a Thursday this month because of the Independence Day holiday. In terms of what to expect, our US economists are looking for a gain in nonfarm payrolls of another +2.5m, following last month’s +2.509m reading, along with a reduction in the unemployment rate to 12.5%. However given the persistent misclassification issues, the U-6 rate (19.4% vs. 20.2%) will provide a more-accurate picture with respect to the underlying state of the labour market. In addition it’s worth remembering that given the US shed over 22m jobs in March and April, even another 2.5m boost would still mean that less than a quarter of the total jobs have been recovered, so there’s still a long way to go before the labour market gets back to something approaching normality. Also bear in mind that this data is backward-looking, so any positive developments won’t necessarily be sustained if a further worsening of the pandemic leads more states to roll back reopening measures.

While we’re on the data theme, another factor that helped to boost markets yesterday was the continued recovery of both the ISM manufacturing reading along with the PMIs from their April lows. Starting with the ISM, that came in at 52.6 (vs. 49.8 expected), above the crucial 50-mark that separates expansion from contraction, and its highest level since April 2019. The positive news extended to Europe too, where the final Euro Area manufacturing PMI was revised up half a point from the flash reading to 47.4, while the French (52.3) and the German (45.2) numbers also saw upward revisions. However, the recovery we’ve seen in activity shouldn’t be overstated, and to some extent this is pent-up demand. The big question as the virus accelerates in many countries again is whether this new found recovery can be sustained.

Fed minutes from the June meeting were released last night, with the biggest point of interest seeing how officials responded to discussions around yield-curve control. The transcript revealed that the FOMC is clearly leaning toward forward guidance over committing to YCC, saying that “many participants remarked that, as long as the committee’s forward guidance remained credible on its own, it was not clear that there would be a need for the committee to reinforce its forward guidance with the adoption of a YCT policy.” On the topic of inflation a “number” of officials favoured the idea of making future policy moves conditional on inflation. This could mean waiting for “a modest temporary overshooting of the committee’s longer-run inflation goal” of 2%.

Elsewhere in markets, sovereign bonds sold off in line with the broader move away from havens into risk assets, and yields on 10yr bunds rose by +5.9bps in their largest daily move upwards in over a month. Yields on US Treasuries (+2.0bps) and gilts (+3.9bps) similarly rose, though peripheral spreads in Europe tightened, with the gap between 10yr BTPs over bunds falling by -4.6bps to its narrowest in over 3 months. Gold came off its 7-year high with a -0.61% move lower, and oil rallied with Brent crude up +2.14%.

Wrapping up with yesterday’s other data, and in advance of today’s US jobs report, the ADP’s report of private payrolls showed a +2.369m increase in June (vs. 2.9m expected) though the previous month’s reading was revised up by +5.8m! In Germany however, unemployment jumped to 2.943m, its highest level in six-and-a-half years. Also in Germany, data showed retail sales in May rebounded by 13.9%, well above expectations for a 3.5% rise and a significant rebound from last month’s -5.3 drop.

To the day ahead now, and the highlight is likely to be the aforementioned jobs report for June from the US. Otherwise, we’ll also get the weekly initial jobless claims reading, along with data on factory orders and the trade balance for May. Otherwise, we’ll get the Euro Area unemployment rate for May and the manufacturing PMI for Canada. There’ll also be remarks from the ECB’s Mersch and Schnabel.

Government

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canadaInternational

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Authored by Zachary Stieber via The Epoch Times (emphasis…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

People who recovered from COVID-19 and received a COVID-19 shot were more likely to suffer adverse reactions, researchers in Europe are reporting.

Participants in the study were more likely to experience an adverse reaction after vaccination regardless of the type of shot, with one exception, the researchers found.

Across all vaccine brands, people with prior COVID-19 were 2.6 times as likely after dose one to suffer an adverse reaction, according to the new study. Such people are commonly known as having a type of protection known as natural immunity after recovery.

People with previous COVID-19 were also 1.25 times as likely after dose 2 to experience an adverse reaction.

The findings held true across all vaccine types following dose one.

Of the female participants who received the Pfizer-BioNTech vaccine, for instance, 82 percent who had COVID-19 previously experienced an adverse reaction after their first dose, compared to 59 percent of females who did not have prior COVID-19.

The only exception to the trend was among males who received a second AstraZeneca dose. The percentage of males who suffered an adverse reaction was higher, 33 percent to 24 percent, among those without a COVID-19 history.

“Participants who had a prior SARS-CoV-2 infection (confirmed with a positive test) experienced at least one adverse reaction more often after the 1st dose compared to participants who did not have prior COVID-19. This pattern was observed in both men and women and across vaccine brands,” Florence van Hunsel, an epidemiologist with the Netherlands Pharmacovigilance Centre Lareb, and her co-authors wrote.

There were only slightly higher odds of the naturally immune suffering an adverse reaction following receipt of a Pfizer or Moderna booster, the researchers also found.

The researchers performed what’s known as a cohort event monitoring study, following 29,387 participants as they received at least one dose of a COVID-19 vaccine. The participants live in a European country such as Belgium, France, or Slovakia.

Overall, three-quarters of the participants reported at least one adverse reaction, although some were minor such as injection site pain.

Adverse reactions described as serious were reported by 0.24 percent of people who received a first or second dose and 0.26 percent for people who received a booster. Different examples of serious reactions were not listed in the study.

Participants were only specifically asked to record a range of minor adverse reactions (ADRs). They could provide details of other reactions in free text form.

“The unsolicited events were manually assessed and coded, and the seriousness was classified based on international criteria,” researchers said.

The free text answers were not provided by researchers in the paper.

“The authors note, ‘In this manuscript, the focus was not on serious ADRs and adverse events of special interest.’” Yet, in their highlights section they state, “The percentage of serious ADRs in the study is low for 1st and 2nd vaccination and booster.”

Dr. Joel Wallskog, co-chair of the group React19, which advocates for people who were injured by vaccines, told The Epoch Times: “It is intellectually dishonest to set out to study minor adverse events after COVID-19 vaccination then make conclusions about the frequency of serious adverse events. They also fail to provide the free text data.” He added that the paper showed “yet another study that is in my opinion, deficient by design.”

Ms. Hunsel did not respond to a request for comment.

She and other researchers listed limitations in the paper, including how they did not provide data broken down by country.

The paper was published by the journal Vaccine on March 6.

The study was funded by the European Medicines Agency and the Dutch government.

No authors declared conflicts of interest.

Some previous papers have also found that people with prior COVID-19 infection had more adverse events following COVID-19 vaccination, including a 2021 paper from French researchers. A U.S. study identified prior COVID-19 as a predictor of the severity of side effects.

Some other studies have determined COVID-19 vaccines confer little or no benefit to people with a history of infection, including those who had received a primary series.

The U.S. Centers for Disease Control and Prevention still recommends people who recovered from COVID-19 receive a COVID-19 vaccine, although a number of other health authorities have stopped recommending the shot for people who have prior COVID-19.

Another New Study

In another new paper, South Korean researchers outlined how they found people were more likely to report certain adverse reactions after COVID-19 vaccination than after receipt of another vaccine.

The reporting of myocarditis, a form of heart inflammation, or pericarditis, a related condition, was nearly 20 times as high among children as the reporting odds following receipt of all other vaccines, the researchers found.

The reporting odds were also much higher for multisystem inflammatory syndrome or Kawasaki disease among adolescent COVID-19 recipients.

Researchers analyzed reports made to VigiBase, which is run by the World Health Organization.

“Based on our results, close monitoring for these rare but serious inflammatory reactions after COVID-19 vaccination among adolescents until definitive causal relationship can be established,” the researchers wrote.

The study was published by the Journal of Korean Medical Science in its March edition.

Limitations include VigiBase receiving reports of problems, with some reports going unconfirmed.

Funding came from the South Korean government. One author reported receiving grants from pharmaceutical companies, including Pfizer.

International

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

As the global pandemic unfolded, government-funded…

Share this:

{kind=link}

As the global pandemic unfolded, government-funded experimental vaccines were hastily developed for a virus which primarily killed the old and fat (and those with other obvious comorbidities), and an aggressive, global campaign to coerce billions into injecting them ensued.

{kind=link}

Then there were the lockdowns - with some countries (New Zealand, for example) building internment camps for those who tested positive for Covid-19, and others such as China welding entire apartment buildings shut to trap people inside.

It was an egregious and unnecessary response to a virus that, while highly virulent, was survivable by the vast majority of the general population.

Oh, and the vaccines, which governments are still pushing, didn't work as advertised to the point where health officials changed the definition of "vaccine" multiple times.

Tucker Carlson recently sat down with Dr. Pierre Kory, a critical care specialist and vocal critic of vaccines. The two had a wide-ranging discussion, which included vaccine safety and efficacy, excess mortality, demographic impacts of the virus, big pharma, and the professional price Kory has paid for speaking out.

Keep reading below, or if you have roughly 50 minutes, watch it in its entirety for free on X:

Ep. 81 They’re still claiming the Covid vax is safe and effective. Yet somehow Dr. Pierre Kory treats hundreds of patients who’ve been badly injured by it. Why is no one in the public health establishment paying attention? pic.twitter.com/IekW4Brhoy

— Tucker Carlson (@TuckerCarlson) March 13, 2024

"Do we have any real sense of what the cost, the physical cost to the country and world has been of those vaccines?" Carlson asked, kicking off the interview.

"I do think we have some understanding of the cost. I mean, I think, you know, you're aware of the work of of Ed Dowd, who's put together a team and looked, analytically at a lot of the epidemiologic data," Kory replied. "I mean, time with that vaccination rollout is when all of the numbers started going sideways, the excess mortality started to skyrocket."

When asked "what kind of death toll are we looking at?", Kory responded "...in 2023 alone, in the first nine months, we had what's called an excess mortality of 158,000 Americans," adding "But this is in 2023. I mean, we've had Omicron now for two years, which is a mild variant. Not that many go to the hospital."

'Safe and Effective'

Tucker also asked Kory why the people who claimed the vaccine were "safe and effective" aren't being held criminally liable for abetting the "killing of all these Americans," to which Kory replied: "It’s my kind of belief, looking back, that [safe and effective] was a predetermined conclusion. There was no data to support that, but it was agreed upon that it would be presented as safe and effective."

Tucker Carlson Asks the Forbidden Question

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

He wants to know why the people who made the claim “safe and effective” aren’t being held to criminal liability for abetting the “killing of all these Americans.”

DR. PIERRE KORY: “It’s my kind of belief, looking back, that [safe and… pic.twitter.com/Icnge18Rtz

Carlson and Kory then discussed the different segments of the population that experienced vaccine side effects, with Kory noting an "explosion in dying in the youngest and healthiest sectors of society," adding "And why did the employed fare far worse than those that weren't? And this particularly white collar, white collar, more than gray collar, more than blue collar."

Kory also said that Big Pharma is 'terrified' of Vitamin D because it "threatens the disease model." As journalist The Vigilant Fox notes on X, "Vitamin D showed about a 60% effectiveness against the incidence of COVID-19 in randomized control trials," and "showed about 40-50% effectiveness in reducing the incidence of COVID-19 in observational studies."

Dr. Pierre Kory: Big Pharma is ‘TERRIFIED’ of Vitamin D

— The Vigilant Fox ???? (@VigilantFox) March 14, 2024

Why?

Because “It threatens the DISEASE MODEL.”

A new meta-analysis out of Italy, published in the journal, Nutrients, has unearthed some shocking data about Vitamin D.

Looking at data from 16 different studies and 1.26… pic.twitter.com/q5CsMqgVju

Professional costs

Kory - while risking professional suicide by speaking out, has undoubtedly helped save countless lives by advocating for alternate treatments such as Ivermectin.

Kory shared his own experiences of job loss and censorship, highlighting the challenges of advocating for a more nuanced understanding of vaccine safety in an environment often resistant to dissenting voices.

"I wrote a book called The War on Ivermectin and the the genesis of that book," he said, adding "Not only is my expertise on Ivermectin and my vast clinical experience, but and I tell the story before, but I got an email, during this journey from a guy named William B Grant, who's a professor out in California, and he wrote to me this email just one day, my life was going totally sideways because our protocols focused on Ivermectin. I was using a lot in my practice, as were tens of thousands of doctors around the world, to really good benefits. And I was getting attacked, hit jobs in the media, and he wrote me this email on and he said, Dear Dr. Kory, what they're doing to Ivermectin, they've been doing to vitamin D for decades..."

"And it's got five tactics. And these are the five tactics that all industries employ when science emerges, that's inconvenient to their interests. And so I'm just going to give you an example. Ivermectin science was extremely inconvenient to the interests of the pharmaceutical industrial complex. I mean, it threatened the vaccine campaign. It threatened vaccine hesitancy, which was public enemy number one. We know that, that everything, all the propaganda censorship was literally going after something called vaccine hesitancy."

Money makes the world go 'round

Carlson then hit on perhaps the most devious aspect of the relationship between drug companies and the medical establishment, and how special interests completely taint science to the point where public distrust of institutions has spiked in recent years.

"I think all of it starts at the level the medical journals," said Kory. "Because once you have something established in the medical journals as a, let's say, a proven fact or a generally accepted consensus, consensus comes out of the journals."

"I have dozens of rejection letters from investigators around the world who did good trials on ivermectin, tried to publish it. No thank you, no thank you, no thank you. And then the ones that do get in all purportedly prove that ivermectin didn't work," Kory continued.

"So and then when you look at the ones that actually got in and this is where like probably my biggest estrangement and why I don't recognize science and don't trust it anymore, is the trials that flew to publication in the top journals in the world were so brazenly manipulated and corrupted in the design and conduct in, many of us wrote about it. But they flew to publication, and then every time they were published, you saw these huge PR campaigns in the media. New York Times, Boston Globe, L.A. times, ivermectin doesn't work. Latest high quality, rigorous study says. I'm sitting here in my office watching these lies just ripple throughout the media sphere based on fraudulent studies published in the top journals. And that's that's that has changed. Now that's why I say I'm estranged and I don't know what to trust anymore."

Vaccine Injuries

Carlson asked Kory about his clinical experience with vaccine injuries.

"So how this is how I divide, this is just kind of my perception of vaccine injury is that when I use the term vaccine injury, I'm usually referring to what I call a single organ problem, like pericarditis, myocarditis, stroke, something like that. An autoimmune disease," he replied.

"What I specialize in my practice, is I treat patients with what we call a long Covid long vaxx. It's the same disease, just different triggers, right? One is triggered by Covid, the other one is triggered by the spike protein from the vaccine. Much more common is long vax. The only real differences between the two conditions is that the vaccinated are, on average, sicker and more disabled than the long Covids, with some pretty prominent exceptions to that."

Watch the entire interview above, and you can support Tucker Carlson's endeavors by joining the Tucker Carlson Network here...

Net Zero, The Digital Panopticon, & The Future Of Food

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Looking Back At COVID’s Authoritarian Regimes

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Health Officials: Man Dies From Bubonic Plague In New Mexico

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

The SNF Institute for Global Infectious Disease Research announces new advisory board

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A