Futures Surge, Dollar Crumbles Ahead Of Pivotal CPI Print

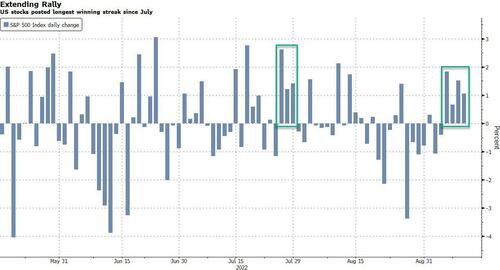

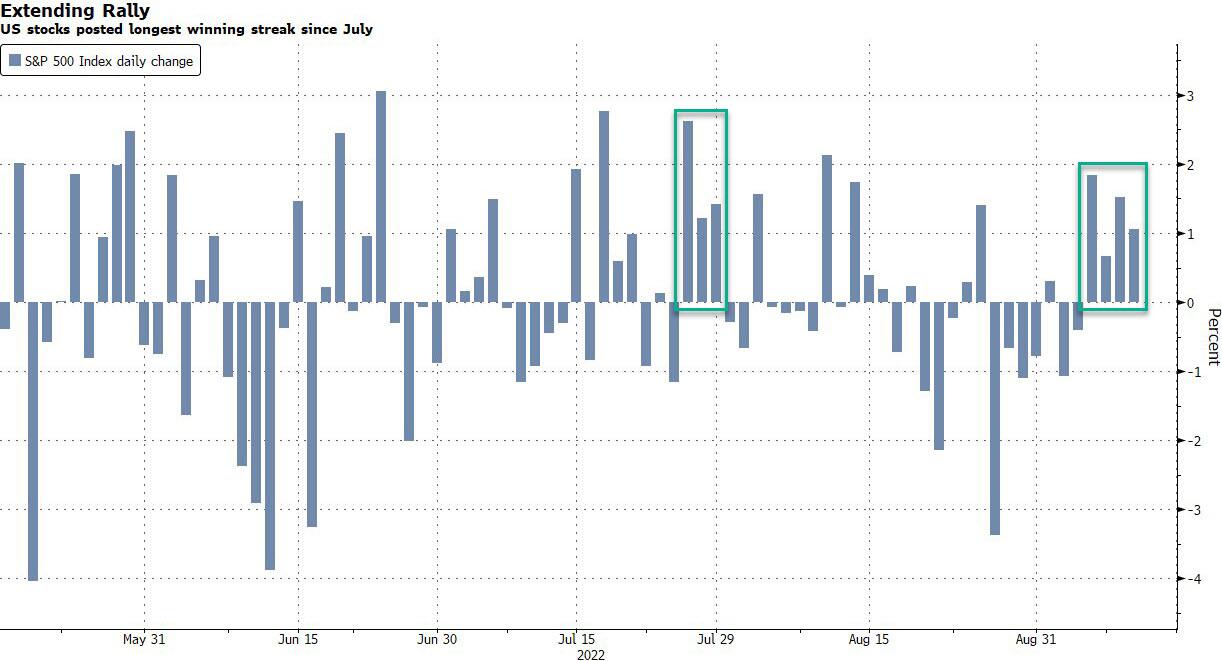

US futures extended their gains for fifth consecutive day - their longest winning streak since July - rising ahead of today's "pivotal" CPI data.

Futures on the S&P 500 and Nasdaq 100 gained 0.7% at 7:45 a.m. in New York ahead of the data that’s due at 8:30 a.m. The underlying gauges advanced Monday for a fourth straight day amid hopes that inflation will show further signs of cooling with the headline print actually declining for the first time in two years, before the Fed’s decision on interest rates next week. Treasury yields dipped while the Bloomberg dollar index extended its recent decline, sliding 0.3% to a two week low as traders bet that US inflation is near peaking, therefore challenging the dollar-dominance narrative, in the process pushing oil and bitcoin higher.

In premarket trading, tech giants including Apple and Microsoft climbed. Satellite-imaging company Planet Labs shares gained as much as 12% in US premarket session after raising full year forecasts for both revenue and adjusted gross margin. Oracle shares rose 1.9% as analysts are positive on the company’s 1Q top-line growth amid accelerating cloud revenue expansion. More bearish commentators, however, highlight a drop in operating margin as the integration of health records provider Cerner pushes up costs. Here are some other notable premarket movers:

Rent the Runway (RENT US) shares slump 23% in premarket trading after reporting a drop in subscribers in the second-quarter and announcing a restructuring of the company.

Dow (DOW US) shares declined 0.7% in premarket trading as Jefferies downgraded the stock to hold, saying that it is likely to be range-bound in the near term, with downside risk as rising interest rates further hit customer confidence.

Peloton (PTON US) shares may be in focus as Citi analysts say that the departure of the company’s founders, including Executive Chairman John Foley, completes the organizational changes at Peloton and should improve its free cash flow picture.

Keep an eye on Innovid (CTV US) shares as Morgan Stanley initiates coverage with an underweight rating, saying that the company has good positioning in connected TV, but the stock appears to be “more than fully valued”.

Previewing the CPI (our full preview here), UBS chief economist Paul Donovan writes that while US August consumer price inflation is due "Consumer prices do not measure the cost of living. Fantasy numbers in US CPI calculation further divorce this price measure from the cost of living. However, the Fed’s June policy error elevated the importance of consumer price inflation. Disinflation and deflation in durable goods, the longest period of gasoline price deflation for years, and some evidence of squeezing profit margins all suggest a lower reading."

“It’s way to early to expect the Fed to react to the fact that we’re past peak inflation,” Nannette Hechler-Fayd’Herbe, chief investment officer at Credit Suisse International Wealth Management, told Bloomberg TV. “When you look at S&P 500 we have seen very big support levels from a technical point of view, so I can very well envisage that volatility takes us down to these levels once the market finally realizes the Fed will not cut rates as early as 2023.”

The government’s report is expected to show that consumer inflation increased 8.1% in August from the same month last year, down from 8.5% in July yet still historically elevated. The figures aren’t likely to sway the Fed’s September decision, with traders almost fully expecting another 75-basis-point increase next week, taking their cue from officials supporting that view. Still, solid signs of peaking inflation can affect the US central bank’s policy in later meetings.

“With a lot of US policymakers calling for a front-loading approach, the odds appear to favor a 75 basis-point move if markets are to be convinced the US central bank is serious about driving inflation lower on a ‘sustainable basis'," said Michael Hewson, chief market analyst at CMC Markets UK. That “means today’s inflation numbers may not be terribly instructive.”

Meanwhile, JPMorgan permabullish strategists Marko Kolanovic and Nikolaos Panigirtzoglou said a soft landing is becoming the more likely scenario for the global economy, which will continue to provide tailwinds for risky assets. As a reminder, Marko has said to buy the dip pretty much every single week in 2022. Recent data pointing to moderating inflation and wage pressures, rebounding growth and stabilizing consumer confidence suggest the world will avoid a recession, they said. Not confirming their optimism, a Bank of America survey showed investors are fleeing equities en masse amid the specter of a recession, with allocations to stocks at record lows and cash exposure at all-time highs.

“The fact is that two consecutive reports showing a sharp deceleration combined with last month’s goldilocks jobs report will be a really encouraging sign and could trigger a broader risk rebound in the markets,” said Craig Erlam, a senior market analyst at Oanda Europe Ltd. “It may not be enough to tip the Fed balance in favor of a more modest 50 basis point rate hike next week but it may slow the pace of tightening thereafter.”

In Europe, corporate news helped buoy the Stoxx Europe 600 index, with UBS Group AG rising after raising its dividend and share-buyback target, and Bayer AG jumping more than 2% after starting the search for a new chief executive. Retailers and grocers pared some of their recent rally after Ocado Group Plc said inflation and energy costs will weigh on profit. The FTSE MIB outperformed peers, adding 0.3%. Utilities, consumer products and miners are the strongest performing sectors.

Earlier in the session, Asian stocks extended their recent rally as several markets returned from holidays, and as traders awaited a key US inflation data release due later Tuesday. The MSCI Asia Pacific Index rose as much as 0.7%, poised for a fourth-straight day of gains, driven by technology shares. South Korean stocks led advances among regional benchmarks in a catch-up rally following a four-day weekend. The US CPI report is expected to show a mixed picture, hinting that inflation may have peaked but remained elevated. This could provide more clues to the Federal Reserve’s rate decision next week, with traders currently expecting another 75-basis-point increase.

“Further pushback from the Fed could be likely but for now, with the Fed blackout period in place, market bulls may be hoping to see underperformance in the upcoming inflation data,” Jun Rong Yeap, a market strategist at IG Asia Pte, wrote in a note. How to trade dollar, bonds or equities ahead of the Fed decision? This week’s MLIV Pulse survey asks about the best trades going into the FOMC meeting. Please click here to share your views anonymously. Chinese equities edged higher as traders returned from a holiday. President Xi Jinping plans to travel to Central Asia this week in what would be his first trip abroad since the Covid pandemic began. Shares in Hong Kong fell.

Japanese equities rose for a fourth day, driven by optimism that inflation is close to the peak as investors await US CPI data to be announced late Tuesday. The Topix Index rose 0.3% to 1,986.57 as of market close Tokyo time, while the Nikkei advanced 0.3% to 28,614.63. Nintendo Co. contributed the most to the Topix Index gain, increasing 5.5%. Out of 2,169 stocks in the index, 1,126 rose and 903 fell, while 140 were unchanged. “Consumer surveys released by the New York Fed show that inflation expectations have receded, supporting stock prices to some extent,” said Masahiro Ichikawa, chief market strategist at Sumitomo Mitsui DS Asset Management.

In Australia, the S&P/ASX 200 index rose 0.7% to close at 7,009.70, boosted by gains in banks and mining shares. The benchmark reached the highest level since Aug. 26. Ramsay Health Care tumbled more than 10% after a consortium led by KKR & Co. indicated it won’t improve the terms of a takeover proposal, indicating the end of a A$20.1 billion ($14 billion) pursuit. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,762.15

Key equity gauges in India advanced for fourth consecutive session to edge closer to peaks seen in October as shares in the heavily weighted finance sector rebound following the resumption of inflows from foreigners. The S&P BSE Sensex gained 0.8% to 60,571.08 in Mumbai, while the NSE Nifty 50 Index rose by a similar measure. Both gauges are less than 3% short of their record highs after climbing more than 14% since the end of June. The rally in stocks comes despite surging consumer prices in the country. Retail inflation accelerated to 7% in August, slightly above the consensus estimate, data released Monday evening showed. Foreign investors have net bought more than $8 billion of local equities since end of June, with a large proportion going into shares of financial firms. “The current market buoyancy globally, including in India, is based on the expectation that inflation has peaked along with softening crude prices,” said Naveen Kulkarni, chief investment officer of Axis Securities’ PMS business. With the onset of winter, investors should watch energy prices in Europe and the US, which can re-ignite inflation, he added. HDFC Bank Ltd contributed the most to the Sensex’s gain, increasing 1.3%. Out of 30 shares in the benchmark index, 24 rose and 6 fell.

In FX, the Bloomberg Dollar Spot Index extended its recent losses, and after hitting an all time high at the start of the month, fell to a two-week low as the greenback weakened against all of its Group-of-10 peers apart from the Norwegian krone. CAD and NZD were the weakest performers in G-10 FX, SEK and JPY outperform.

The euro rose a third day, to touch a day high of 1.0155 versus the greenback. European bonds traded mostly lower. German yields rose up to 4bps as they underperformed Italian bonds and with both countries tapping the market today

The Norwegian krone posted a small drop versus the euro after a key survey of business sentiment by Norges Bank showed that the economy faces worsening prospects amid a “sharp” rise in prices.

The yen reversed an Asia-session loss while the Australian and New Zealand dollars swung between modest gains and losses

In fixed income, Treasuries held gains into early US session, having pared most of Monday afternoon’s slide that followed weak 10-year note auction. US yields are richer by 4bp-5bp across the curve; the long-end lags, steepening 5s30s by about 1bp. The 10-year yield eased 4bps to near 3.31%. Bunds 10-year yield is up 1bp to around 1.66% and gilts 10-year yield is little changed. Treasuries outperform bunds and gilts as stock futures reach highest levels this month. The US auction cycle concludes with $18b 30-year bond reopening at 1pm. WI 30-year yield around 3.475% is above auction stops since 2014 and ~37bp cheaper than August’s, which tailed by 1.1bp. IG dollar issuance slate empty so far; Monday saw eight borrowers price $11.7b; activity expected to be lighter Tuesday with focus on August inflation data. Focal points of US session include CPI inflation and 30-year bond auction; Monday’s 3-year sale also tailed.

In commodities, WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary of short-term upward moves as China continues with strings of lockdowns. WTI trades within Monday’s range, adding 1.1% to near $88.71. Spot gold trades on either side of the flat mark in the run-up to US CPI, under its 50 and 21 DMAs at 1,740.82/oz and USD 1,731.05/oz respectively. Base metals are mostly firmer amid the weaker Buck and upside across stocks.

Bitcoin trades on either side of USD 22,500, whilst Ethereum pulled back after reaching levels close to 1,800.

Looking to the day ahead, along with August CPI in the US, American data will include NFIB Small Business optimism (came in at 91.8, higher than the 90.8 expeected) and average hourly earnings, German and Eurozone ZEW survey results, UK August jobless claims, July average weekly earnings, and unemployment rate, Japanese August PPI, and Italian 2Q unemployment rate.

Market Snapshot

S&P 500 futures up 0.5% to 4,129.25

STOXX Europe 600 up 0.3% to 429.10

MXAP up 0.5% to 156.38

MXAPJ up 0.6% to 513.28

Nikkei up 0.3% to 28,614.63

Topix up 0.3% to 1,986.57

Hang Seng Index down 0.2% to 19,326.86

Shanghai Composite little changed at 3,263.80

Sensex up 0.8% to 60,577.61

Australia S&P/ASX 200 up 0.6% to 7,009.69

Kospi up 2.7% to 2,449.54

Gold spot down 0.1% to $1,723.41

U.S. Dollar Index down 0.22% to 108.09

German 10Y yield little changed at 1.67%

Euro up 0.2% to $1.0140

Top Overnight News from Bloomberg

Pacific Investment Management Co. is advocating a radical solution to fix the liquidity woes plaguing the world of bonds: The entire $23.7 trillion Treasury market should move to a model where investors can transact directly with each other -- reducing their unhealthy dependence on balance-sheet-constrained banks

The euro is up by almost 3% from two-decade lows hit a week ago against the dollar, and option markets suggest the rally has more room to run. The bet is that US consumer price data due later Tuesday will show inflation is near peaking, therefore challenging the dollar-dominance narrative. That view is behind the greenback’s recent retreat versus its major peers

Germany is set to use a fund created to help companies cope with the economic hit from the pandemic to provide loan guarantees for struggling energy firms, according to a person familiar with the plan. The volume of loan guarantees available would be around 67 billion euros ($68 billion)

China’s Premier Li Keqiang called for more policies to drive up consumption in the economy as latest figures show a further plunge in travel and spending over a three-day public holiday amid tight Covid controls

For the better part of a decade, a US hedge-fund manager who has never even set foot in China has been patiently betting that the yuan will stage a massive collapse, one so deep that its value could be cut in half

It’s not a common sight for euro overnight volatility to trade above 20% on non-central bank decision days. Yet this is what investors face this morning as everyone is on the lookout for the release of the US inflation report

Britain’s unemployment rate fell to the lowest since 1974 as more people dropped out of the workforce, fanning upward pressure on wages. The government said 3.6% of adults were out of work and looking for jobs in the three months through July, lower than the 3.8% pace in the previous months. Economists had expected no change

Secretary of State Antony Blinken said it was ‘unlikely’ the US and Iran would reach a new nuclear deal anytime soon, adding to Western officials’ downbeat assessment over the prospects for reviving an accord that President Donald Trump abandoned in 2018

Japan has more firepower in its foreign exchange reserves than it did the last time it intervened in markets to support its currency, though a unilateral move is seen as unlikely to succeed without US support

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded positive after the advances in global peers including on Wall St. where sentiment was helped by slowing inflation expectations, although gains were capped ahead of US CPI data and amid further China COVID woes. ASX 200 reclaimed the 7,000 level with advances led by the commodity-related sectors and with the risk tone also helped by an improvement in business and consumer sentiment data. Nikkei 225 marginally gained amid hopes of further supportive measures with Japan to potentially implement a nationwide travel incentive this month. Hang Seng and Shanghai Comp were slightly firmer but with upside contained after fresh COVID restrictions including in Sanhe near Beijing and with Shijiazhuang city in Hebei also locking down a district due to coronavirus.

Top Asian News

Emmys for Netflix’s Squid Game Boost ‘K-Drama’ Stocks in Seoul

Fosun Chief Says Many Overseas Units Resilient Amid Pandemic

Holders of Fosun’s 2b Yuan Bond Request Early Repayment in Full

Netflix’s Megahit ‘Squid Game’ Wins Top Emmy Awards

Woodford Administrator Faces Possible £306 Million Hit, UK Says

European bourses tread water with modest gains following a relatively mixed APAC lead. European sectors are mostly higher with no overarching theme or bias. Stateside, futures are edging higher in early European trade with a broad-based performance seen across the ES, NQ, YM, and RTY.

Top European News

UK Chancellor Kwarteng told Treasury officials to adapt to a new approach focused on boosting GDP to 2.5%, the long-term average pre-GFC, ahead of the mini-Budget announcement next week which includes tax cuts and increased borrowing, according to FT.

UK and EU are reportedly seeking to avoid a September 15th legal deadline over ‘grace periods’ becoming a flashpoint in talks, according to officials from both sides cited by the FT.

The EU is delaying plans to cut the use of pesticides amid food production fears and subsequent price increases as a result, according to the FT.

UK's Felixstowe port has received notice from union of further strike action from 27th Sept to 5th Oct; collective bargaining process has been exhausted - no prospect of an agreement being reached with union.

EU Commission President is to call another energy meeting by end-September, according to the Spanish Energy Minister, according Reuters.

German Economy Ministry report says early indicators and polls point to a rising number of insolvencies in H2, but there is no 'insolvency wave' in sight, via Reuters.

EU is reportedly mulling a EUR 180-200 price cap from lower-cost sources (vs guided EUR 200); eyes taking 33% of extra profits from fossil fuel companies, according to Bloomberg sources.

Ocado Plummets as Shoppers Cut Back and Energy Costs Bite

Mercedes-Benz Wins Dismissal of German Climate Lawsuit

Some 17 Million in Europe Got Long Covid in First Pandemic Years

FX

DXY is softer and trades on either side of 108.00, ahead of yesterday's 107.80 low and the 50 DMA at 107.52.

EUR/USD faded at 1.0160 with decent option expiry interest between 1.0170-80 (1.21bn).

The JPY continued its correction to almost 142.00 against the Greenback, irrespective of mixed Japanese PPI prints.

Fixed Income

Choppy and divergent price action in debt futures as EZ bonds digest decent auction results from Germany and Italy.

Gilts regroup after underperformance on the back of better than expected UK data.

Bunds are holding above 144.00 having fallen to a marginal new Eurex low at 143.86

US Treasuries are firmer across the board pre-US CPI, irrespective of Monday’s poorly received 3 and 10 year offerings.

Commodities

WTI and Brent are firmer intraday as a function of the receding Dollar, but traders are wary of short-term upward moves as China continues with strings of lockdowns.

Spot gold trades on either side of the flat mark in the run-up to US CPI, under its 50 and 21 DMAs at 1,740.82/oz and USD 1,731.05/oz respectively

Base metals are mostly firmer amid the weaker Buck and upside across stocks.

Crypto

Bitcoin trades on either side of USD 22,500, whilst Ethereum pulled back after reaching levels close to 1,800.

US Event Calendar

06:00: Aug. SMALL BUSINESS OPTIMISM, 91.8, est. 90.8, prior 89.9

08:30: Aug. Real Avg Hourly Earning YoY, prior -3.0%

08:30: Aug. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

08:30: Aug. CPI Core Index SA, est. 296.250, prior 295.275

08:30: Aug. CPI Index NSA, est. 295.588, prior 296.276

08:30: Aug. CPI Ex Food and Energy YoY, est. 6.1%, prior 5.9%

08:30: Aug. CPI YoY, est. 8.1%, prior 8.5%

08:30: Aug. Real Avg Weekly Earnings YoY, prior -3.6%

08:30: Aug. CPI MoM, est. -0.1%, prior 0%

14:00: Aug. Monthly Budget Statement, est. -$217b, prior -$170.6b

DB's Jim Reid concludes the overnight wrap

It’s that time again. US CPI will clearly be the major focus today and could shape next week’s FOMC and the rest of the month’s trading. Or, of course, it could be a damp squib but I’m sure they’ll be something in it to move markets.

Our economists are expecting a slight decline in the headline number, (-0.09% MoM) but for core to pick up (+0.30%). On a YoY basis, headline CPI should fall five-tenths to 8.0% while core should increase a tenth to 6.0%. With the market pricing a near certainty of a 75bp move next week (now at 73.4bps), that profile above won’t be enough to meaningfully reduce chances of a 75bp hike, and markets will turn to this Friday’s inflation expectations data as the last hurdle to clear before the Fed delivers (barring any late breaking news stories to the contrary). On that front, the New York Fed’s 3-year inflation expectations measure fell to its lowest level in 2 years yesterday, clocking in at 2.8% in August from 3.2% in July. For context, it’s retreated from a high of 4.2% in October of last year. Uncertainty remains near record highs, though, which will continue to give policymakers pause even as the 75th and 25th percentile of survey responses have also fallen.

Ahead of CPI, the S&P 500 rallied (+1.06% and a 5-day rally for the first time since late-January/early-February) alongside the global risk complex, led by energy and big tech stocks, with the NASDAQ outperforming, up +1.27%. Apple (+3.85%) led the way in the first full trading day since their new iPhone went on sale on Friday. Orders have been strong so far. I upgrade every year but this time I decided not to.... until one minute before the virtual shop opened for the new products. As with every year I got seduced.

While European sovereign curves rallied and flattened, the Treasury curve steepened, and yields climbed ahead of today’s inflation data. 2yr yields climbed +1.5bps while 10yr yields were +4.8bps higher, but some +9.8bps higher than their lunchtime lows. Much of that was after the Europe close as 10yr Bunds and BTP rallied -4.4bps and -5.7bps, respectively. One theory for the US yield sell-off was the fact that yesterday brought the first batch of US Treasury coupon auctions since the Fed doubled the size of their monthly QT runoff, with yields marching higher after both the 3yr and 10yr auction, as the market has to absorb additional collateral. There’s been a partial pullback in Asia this morning with yields on 10yr USTs down -2.12bps to 3.34%.

The initial risk appetite yesterday was led by Europe, as most of the early focus was on the news we discussed 24 hours ago, namely Ukraine’s successful counter-offensive operation over the weekend. Risk sentiment enjoyed a boost, with the Euro also having its best day against the US dollar in a month, appreciating +0.80%. The wider implications of this success are still up for debate though. In particular, it seems like this pushes out the timeline on any potential peace talks, as Ukraine will be emboldened to double down on their red lines. In that vein, the Kremlin said yesterday there were no prospects for talks at the moment. On the downside, this potentially raises the spectre of escalation as well, whether it’s on the battlefield via unconventional weapons or a mass mobilisation from Russia, or on the economic front with Russia applying more pressure through natural gas markets through the remaining pipeline to Europe. European natural gas futures were trading in line with the broader risk sentiment yesterday though, rather than on potential tail risk scenarios, falling another -8.0%, closing below EUR 200 for the first time in a month. We peaked at EUR 342 eleven days ago, so down -44.23% since then. As hinted, European equities rallied strongly, with the STOXX 600 climbing +1.76%, the DAX +2.40% higher, and the CAC increasing +1.95%.

Sticking with the theme of the war and energy, a draft EU proposal, to be officially unveiled this week, included mandatory power cut targets, bringing the bloc closer to rationing. The draft also includes a levy on extra profits at energy producers used to fund relief to consumers. These are still merely draft proposals, which would ultimately need member state buy-in to be implemented, so the negotiation process may wind up watering down the proposal. Nevertheless, as mentioned, natural gas futures fell on the news, with German and French power prices also falling -8.10% and -3.60%, respectively.

The UK’s own energy support plan that we’ve recently covered is due to take effect come October. Whilst US CPI out later today will gain the lion’s share of attention over the near term, the UK has its own CPI print out tomorrow, as well. Our economists are expecting headline inflation to stay put at 10.1% yoy and core to increase to 6.4% yoy. With the new Energy Price Guarantee program in place, they’re lowering their peak forecast for CPI from 14% to 10.5%.

Asian equity markets are firmly in the green while extending a global rally this morning on optimism that inflation is peaking. Across the region, the Kospi (+2.56%) is leading gains with the CSI (+0.70%), the Shanghai Composite (+0.33%) and the Hang Seng (+0.44%) catching up after reopening following a public holiday. Elsewhere, the Nikkei (+0.16%) is trading in positive territory in early trade.

In overnight trading, US stock futures are pointing to slightly higher with the S&P 500 (+0.11%) and NASDAQ 100 (+0.10%).

Early morning data indicated that pipeline prices in Japan appear to have stabilised as factory gate inflation (+9.0% y/y) in August remained unchanged (vs +9.4% in June), albeit a tenth above expectations. Looking at the data, the decline in global oil prices seems to have led the way despite the weakening in the Japanese yen.

Oil prices are slightly lower in early Asian trade with Brent crude futures -0.18% at $93.83/bbl as China’s harsh zero-Covid policy continues to negatively impact the demand from the world’s top oil importer.

To the day ahead, along with August CPI in the US, American data will include NFIB Small Business optimism and average hourly earnings, German and Eurozone ZEW survey results, UK August jobless claims, July average weekly earnings, and unemployment rate, Japanese August PPI, and Italian 2Q unemployment rate.

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

Former Project Veritas & O’Keefe Media Group operative and Pfizer formulation analyst scientist Justin Leslie revealed previously unpublished recordings showing Pfizer’s top vaccine researchers discussing major concerns surrounding COVID-19 vaccines. Leslie delivered these recordings to Veritas in late 2021, but they were never published:

Principal scientist at Pfizer, Kanwall Gill in 2021:

“We had no idea how it’s going to look like. MRNA vaccines have been there for 50 years, but nothing went to clinical trial because MRNA have been known to have side effects.”

Featured in Leslie’s footage is Kanwal Gill, a principal scientist at Pfizer. Gill was weary of MRNA technology given its long research history yet lack of approved commercial products. She called the vaccines “sneaky,” suggesting latent side effects could emerge in time.

Gill goes on to illustrate how the vaccine formulation process was dramatically rushed under the FDA’s Emergency Use Authorization and adds that profit incentives likely played a role:

Pfizer's principal scientist in 2021:

“It takes 10 year for a vaccine to come out. It takes years of observations... we are doing everything at the same time."

"It’s going to affect my heart, and I’m going to die. And nobody’s talking about that."

Leslie recorded another colleague, Pfizer’s pharmaceutical formulation scientist Ramin Darvari, who raised the since-validated concern that repeat booster intake could damage the cardiovascular system:

Pfizer's pharmaceutical formulation scientist, Ramin Darvari, in 2021:

“They’re engineering it specifically for me to take the next one, so increasing my consumption."

“It’s going to affect my heart, and I’m going to die. And nobody’s talking about that.”

None of these claims will be shocking to hear in 2024, but it is telling that high-level Pfizer researchers were discussing these topics in private while the company assured the public of “no serious safety concerns” upon the jab’s release:

Vaccine for Children is a Different Formulation

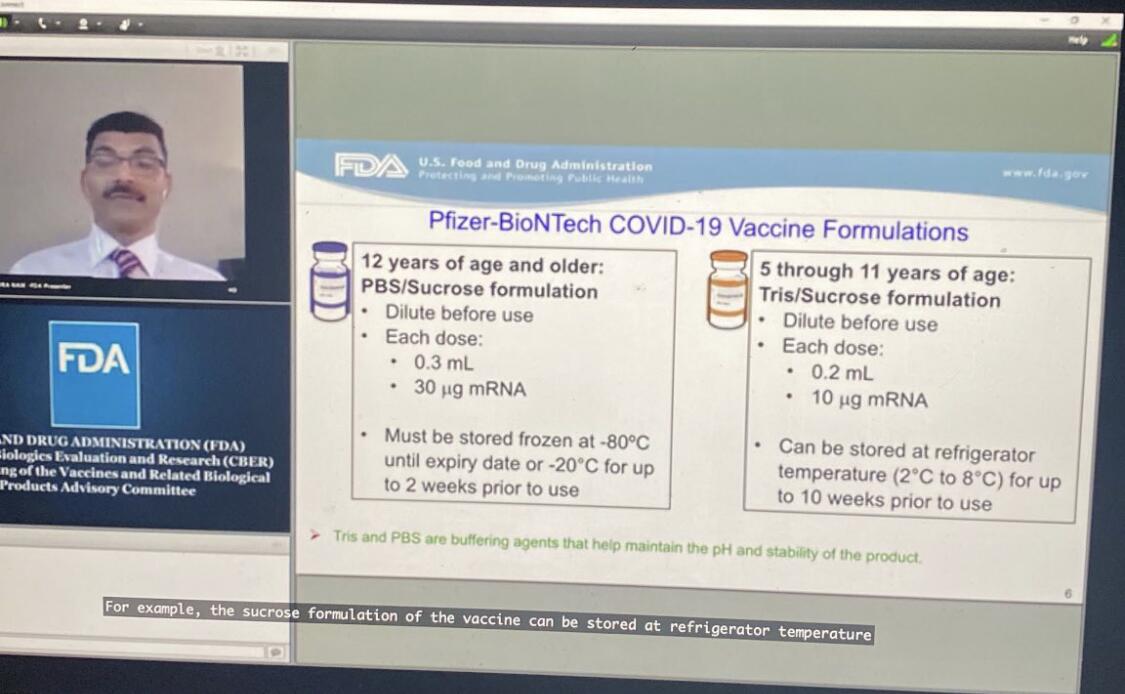

Leslie sent me a little-known FDA-Pfizer conference — a 7-hour Zoom meeting published in tandem with the approval of the vaccine for 5 – 11 year-olds — during which Pfizer’s vice presidents of vaccine research and development, Nicholas Warne and William Gruber, discussed a last-minute change to the vaccine’s “buffer” — from “PBS” to “Tris” — to improve its shelf life. For about 30 seconds of these 7 hours, Gruber acknowledged that the new formula was NOT the one used in clinical trials (emphasis mine):

“The studies were done using the same volume… but contained the PBS buffer. We obviously had extensive consultations with the FDA and it was determined that the clinical studies were not required because, again, the LNP and the MRNA are the same and the behavior — in terms of reactogenicity and efficacy — are expected to be the same.”

According to Leslie, the tweaked “buffer” dramatically changed the temperature needed for storage: “Before they changed this last step of the formulation, the formula was to be kept at -80 degrees Celsius. After they changed the last step, we kept them at 2 to 8 degrees celsius,” Leslie told me.

The claims are backed up in the referenced video presentation:

I’m no vaccinologist but an 80-degree temperature delta — and a 5x shelf-life in a warmer climate — seems like a significant change that might warrant clinical trials before commercial release.

Despite this information technically being public, there has been virtually no media scrutiny or even coverage — and in fact, most were told the vaccine for children was the same formula but just a smaller dose — which is perhaps due to a combination of the information being buried within a 7-hour jargon-filled presentation and our media being totally dysfunctional.

Bohemian Grove?

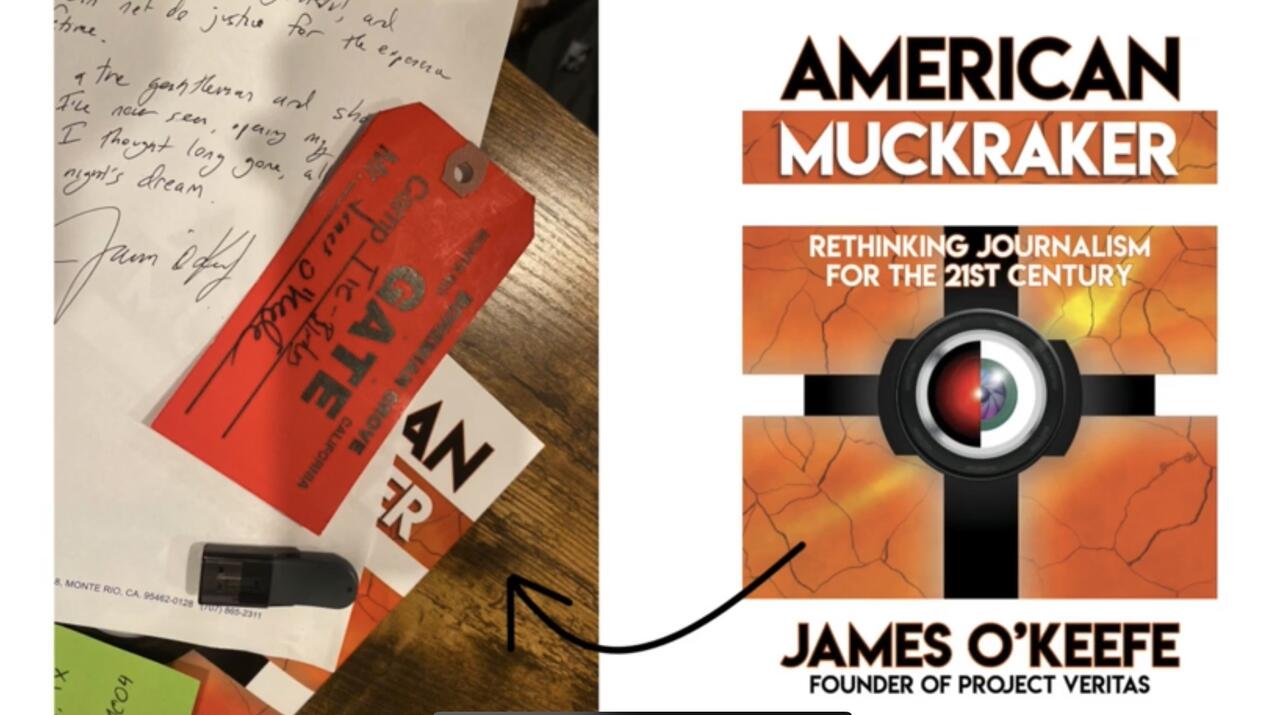

Leslie’s 2-hour long documentary on his experience at both Pfizer and O’Keefe’s companies concludes on an interesting note: James O’Keefe attended an outing at the Bohemian Grove.

Leslie offers this photo of James’ Bohemian Grove “GATE” slip as evidence, left on his work desk atop a copy of his book, “American Muckraker”:

My thoughts on the Bohemian Grove: my good friend’s dad was its general manager for several decades. From what I have gathered through that connection, the Bohemian Grove is not some version of the Illuminati, at least not in the institutional sense.

Do powerful elites hangout there? Absolutely. Do they discuss their plans for the world while hanging out there? I’m sure it has happened. Do they have a weird ritual with a giant owl? Yep, Alex Jones showed that to the world.

My perspective is based on conversations with my friend and my belief that his father is not lying to him. I could be wrong and am open to evidence — like if boxer Ryan Garcia decides to produce evidence regarding his rape claims — and I do find it a bit strange the club would invite O’Keefe who is notorious for covertly filming, but Occam’s razor would lead me to believe the club is — as it was under my friend’s dad — run by boomer conservatives the extent of whose politics include disliking wokeness, immigration, and Biden (common subjects of O’Keefe’s work).

Therefore, I don’t find O’Keefe’s visit to the club indicative that he is some sort of Operation Mockingbird asset as Leslie tries to depict (however Mockingbird is a 100% legitimate conspiracy). I have also met James several times and even came close to joining OMG. While I disagreed with James on the significance of many of his stories — finding some to be overhyped and showy — I never doubted his conviction in them.

As for why Leslie’s story was squashed… all my sources told me it was to avoid jail time for Veritas executives.

Feel free to watch Leslie’s full documentary here and decide for yourself.

Fun fact — Justin Leslie was also the operative behind this mega-viral Project Veritas story where Pfizer’s director of R&D claimed the company was privately mutating COVID-19 behind closed doors:

BREAKING: @Pfizer Exploring "Mutating" COVID-19 Virus For New Vaccines

"Don't tell anyone this...There is a risk...have to be very controlled to make sure this virus you mutate doesn't create something...the way that the virus started in Wuhan, to be honest."#DirectedEvolutionpic.twitter.com/xaRvlD5qTo

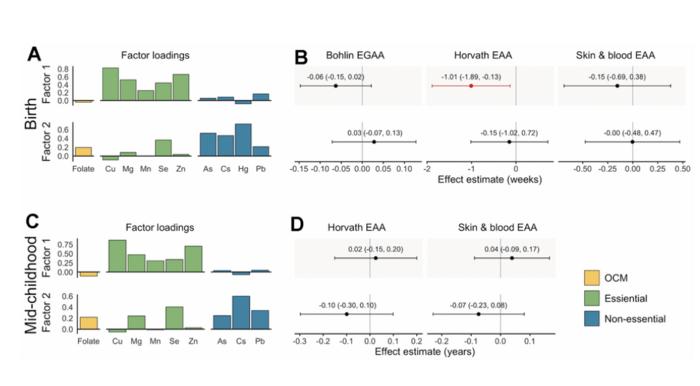

“[…] our findings support the hypothesis that the intrauterine environment, particularly essential and non-essential metals, affect epigenetic aging biomarkers across the life course.”

Credit: 2024 Bozack et al.

“[…] our findings support the hypothesis that the intrauterine environment, particularly essential and non-essential metals, affect epigenetic aging biomarkers across the life course.”

BUFFALO, NY- March 12, 2024 – A new research paper was published inAging (listed by MEDLINE/PubMed as “Aging (Albany NY)” and “Aging-US” by Web of Science) Volume 16, Issue 4, entitled, “Associations of prenatal one-carbon metabolism nutrients and metals with epigenetic aging biomarkers at birth and in childhood in a US cohort.”

Epigenetic gestational age acceleration (EGAA) at birth and epigenetic age acceleration (EAA) in childhood may be biomarkers of the intrauterine environment. In this new study, researchers Anne K. Bozack, Sheryl L. Rifas-Shiman, Andrea A. Baccarelli, Robert O. Wright, Diane R. Gold, Emily Oken, Marie-France Hivert, and Andres Cardenas from Stanford University School of Medicine, Harvard Medical School, Harvard T.H. Chan School of Public Health, Columbia University, and Icahn School of Medicine at Mount Sinai investigated the extent to which first-trimester folate, B12, 5 essential and 7 non-essential metals in maternal circulation are associated with EGAA and EAA in early life.

“[…] we hypothesized that OCM [one-carbon metabolism] nutrients and essential metals would be positively associated with EGAA and non-essential metals would be negatively associated with EGAA. We also investigated nonlinear associations and associations with mixtures of micronutrients and metals.”

Bohlin EGAA and Horvath pan-tissue and skin and blood EAA were calculated using DNA methylation measured in cord blood (N=351) and mid-childhood blood (N=326; median age = 7.7 years) in the Project Viva pre-birth cohort. A one standard deviation increase in individual essential metals (copper, manganese, and zinc) was associated with 0.94-1.2 weeks lower Horvath EAA at birth, and patterns of exposures identified by exploratory factor analysis suggested that a common source of essential metals was associated with Horvath EAA. The researchers also observed evidence of nonlinear associations of zinc with Bohlin EGAA, magnesium and lead with Horvath EAA, and cesium with skin and blood EAA at birth. Overall, associations at birth did not persist in mid-childhood; however, arsenic was associated with greater EAA at birth and in childhood.

“Prenatal metals, including essential metals and arsenic, are associated with epigenetic aging in early life, which might be associated with future health.”

Read the full paper: DOI:https://doi.org/10.18632/aging.205602

Corresponding Author: Andres Cardenas

Corresponding Email:andres.cardenas@stanford.edu

Keywords: epigenetic age acceleration, metals, folate, B12, prenatal exposures

Click here to sign up for free Altmetric alerts about this article.

About Aging:

Launched in 2009, Aging publishes papers of general interest and biological significance in all fields of aging research and age-related diseases, including cancer—and now, with a special focus on COVID-19 vulnerability as an age-dependent syndrome. Topics in Aging go beyond traditional gerontology, including, but not limited to, cellular and molecular biology, human age-related diseases, pathology in model organisms, signal transduction pathways (e.g., p53, sirtuins, and PI-3K/AKT/mTOR, among others), and approaches to modulating these signaling pathways.

Please visit our website at www.Aging-US.com and connect with us:

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}