Futures Surge After Stimulus Pessimism Turns To Stimulus OptimismTyler DurdenThu, 10/01/2020 - 08:09

Narratives used to explain market moves have become so simple enough even 16-year-old Robinhood traders can understand them: if markets are down, it's due to stimulus pessimism, rising covid cases and/or a fading economic recovery; if markets are up, it's due to stimulus optimism, covid vaccine hopes and/or a stronger economic recovery.

Case in point, yesterday we for the former, when late in the session news out of McConnell and Mnuchin hit market sentiment late in the session. However, all that reversed overnight, when Roll Call reported that Mnuchin had proposed a $1.62 trillion compromise proposal including more state and local aid and $400 a week in unemployment insurance. Talks continue today after the House delayed a vote on its $2.2 trillion plan to give Mnuchin and Nancy Pelosi more time to try to thrash out a deal

That was enough to boost market sentiment, while allowing traders to ignore the latest flood of mass layoff announcements as American Air and United said they'll start laying off a combined 32,000 workers (but said they would reverse the move if the government agrees to additional support in the coming days, adding more pressure on policy makers to reach an eleventh-hour stimulus deal, according to Bloomberg). Also overnight, President Trump signed a stopgap spending legislation early Thursday to avert a government shutdown weeks before the presidential election.

As a result futures S&P 500 E-mini futures breached Wednesday’s highs, gaining as much as 1%, and the dollar weakened as investors "remained hopeful" - as Reuters put it - of a new coronavirus fiscal aid package ahead of a clutch of economic data including consumer spending and weekly jobless claims. European stocks advanced, led by technology firms.

Shares of American Airlines Group, Delta Air Lines, United Airlines and JetBlue rose all between 1.3% and 3.6% in thin premarket tradin, after the White House proposed a new stimulus bill to House Democrats worth more than $1.5 trillion that includes a $20 billion extension in aid for the battered airline industry. U.S. airlines have been pleading for more payroll support to protect jobs after the current package expired at midnight on Thursday.

Boeing rose 2.7% a day after Federal Aviation Administration Chief Steve Dickson conducted a 737 MAX test flight, a milestone for the jet to win approval to resume flying after two fatal crashes. PepsiCo gained 2.2% after it forecast full-year profit above estimates as consumers bought more of its snacks such as Doritos and Cheetos, while staying indoors due to the COVID-19 pandemic. Nasdaq futures also rose as tech giga-caps including Apple, Nvidia, Microsoft and Alphabet all rose between 1.3% and 2.4%.

Europe's Stoxx 600 pared its advance to 0.1%, with FTSE 100 also relinquishing some gains on Brexit concern as the EU started the first step of legal action against the U.K. for breaching the terms of the Withdrawal Agreement. Travel and leisure shares fare worst on Stoxx 600, while chip stocks rallied after STMicroelectronics N.V. raised its revenue guidance. The French-Italian chipmaker jumped 6.4% after it saw a sharp rise in automotive and microcontrollers demand in the third quarter, setting it on course to top its 2020 forecast. Bayer AG shares fell as much as 13% in Frankfurt after the agriculture and pharma giant issued a profit warning. Engine maker Rolls-Royce Holdings Plc dropped after announcing a share sale. The UK's FTSE 100 trims advance even as GBP falls; midcap FTSE 250 almost wipes gains of as much as 0.6%.

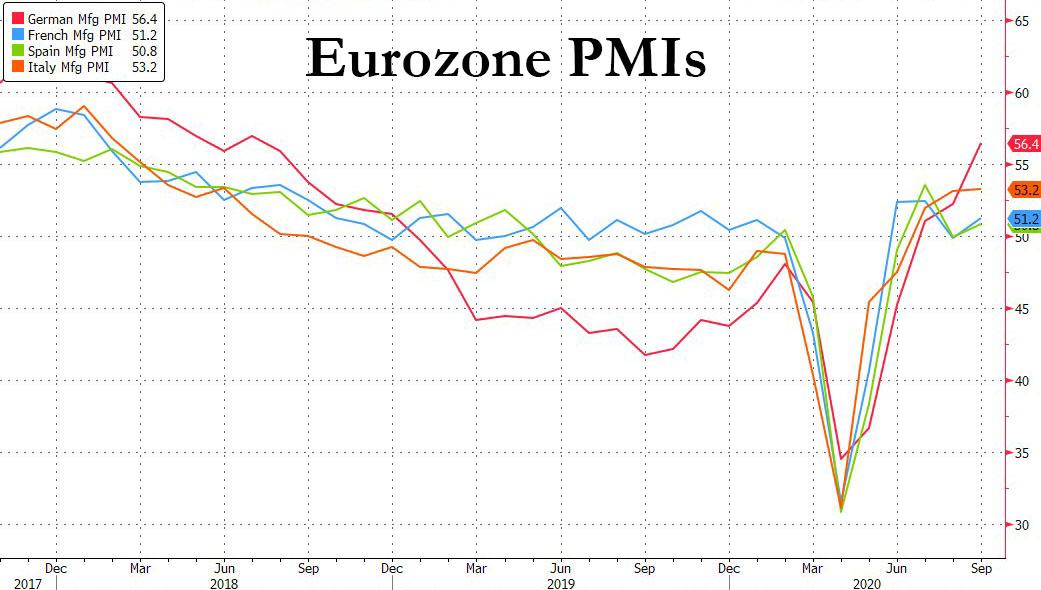

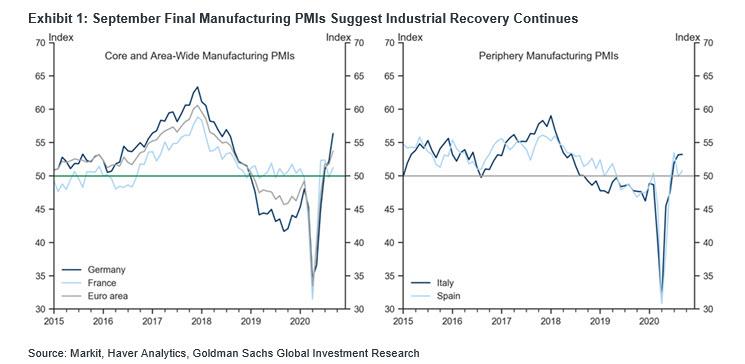

The recovery in euro zone manufacturing activity gathered pace last month but it was largely driven by strength in powerhouse Germany, and rising coronavirus cases across the region may yet reverse the upturn, a survey showed. The Euro area manufacturing PMI for September was unrevised from its flash estimate of 53.7, primarily reflecting partially offsetting revisions to the German (-0.2pt) and French (+0.3pt) counterparts, and somewhat stronger PMIs elsewhere than initially implied. The Italian manufacturing PMI rose only modestly further (below expectations), whereas the Spanish counterpart rose more notably (above expectations). The composition of both the Italian and Spanish readings was mixed, with some commonalities such as (i) weaker domestic but stronger foreign demand, and (ii) relative weakness in consumer goods and strength in investment goods.

Commenting on the data, Goldman said that "the September manufacturing PMI readings across the Euro area suggest the recovery in the industrial sector has continued, reflecting a net positive impulse despite (primarily domestic) headwinds amid a recovery in global industrial activity."

Earlier in the session, the Tokyo Stock Exchange halted trading for the entire day Thursday. Japan Exchange Group, the operator of the TSE, said the problem occurred due to a failed switchover to backups following a hardware breakdown. The exchange will replace hardware and restart its system, aiming to resume trading as normal on Friday. Elsewhere, Asian stocks gained, led by materials and finance, after falling in the last session. The Topix was little changed, with Kyokuyo rising and Kyokuyo falling the most.

In rates, US Treasuries have been under modest selling pressure after S&P 500 E-mini futures breached Wednesday’s highs, gaining as much as 1%. The long-end yields are cheaper by ~2bp, steepening 2s10s, 5s30s by ~1bp each; 10-year, higher by 1.7bp at 0.70%, trails bunds and gilts by ~1bp. 30-year rose as much as 2.7bp to 1.482% in European trading.

In FX, the dollar slipped against most of its G-10 peers even though trading was muted in Asian session with Hong Kong and China shut for a holiday. The weakness continue what was the worst quarter for the dollar in more than three years.

The Bloomberg Dollar Spot Index slipped, yet came off a an early London session low as a rally in equities lost steam. The pound sank versus the euro after the European Union started legal proceedings against the U.K. over Prime Minister Boris Johnson’s plan to breach terms of its Brexit divorce deal. However, pound options traders are in no rush to hedge the risk of a sharp decline in the U.K. currency due to Brexit risks, according to Bloomberg. The Australian and New Zealand dollars rose to a one-week high as gains in U.S. stock futures and China’s yuan lift sentiment.

In commodities, crude futures continued to decline in tandem with sentiment in Europe as Brexit remains in the doldrums while crude-specific news-flow for the complex remains light; as participants look towards the day’s European Council gathering & key US data. WTI Nov trades on either side of USD 40/bbl (vs. high 40.47/bbl) whilst Brent Dec oscillates around the USD 42/bbl mark (vs. high 42.55/bbl). Elsewhere, spot gold remains capped by the USD 1900/oz mark as the yellow metal failed another jab at the psychosocial levels, whilst spot silver retraces some of yesterday’s losses and sees itself north of 23.50/oz.

With a clutch of better-than-expected data also boosting sentiment in the previous session, investors will turn to consumer spending figures for August and the latest batch of weekly jobless claims on Thursday to gauge the pace of the domestic economic recovery. Initial jobless claims are not expected to show much improvement from last week's 870,000 total when the data is released at 8:30 a.m. Eastern Time. The number comes as more companies announce they are going to move ahead with layoffs with American Airlines Group and United Airlines Holdings cutting a combined 32,000 positions. Goldman Sachs Group is also swinging the ax. Increasingly, signs are pointing to the rapid rebound in activity in the third quarter grinding to a near halt, according to Bloomberg. September data on the manufacturing sector is also due at 10 a.m. ET, while the Labor Department’s jobs report is scheduled for release on Friday.

Looking at today's session, U.S. economic data includes initial jobless claims and August personal income and spending (includes PCE deflator) at 8:30am, final September Markit manufacturing PMI (9:45am), August construction spending and September ISM manufacturing (10am); jobs report is ahead Friday.

Market Snapshot

S&P 500 futures up 0.6% to 3,372.75

STOXX Europe 600 up 0.3% to 362.31

MXAP up 0.4% to 170.66

MXAPJ up 0.6% to 560.29

Nikkei unchanged at 23,185.12

Topix unchanged at 1,625.49

Hang Seng Index up 0.8% to 23,459.05

Shanghai Composite down 0.2% to 3,218.05

Sensex up 1.6% to 38,668.04

Australia S&P/ASX 200 up 1% to 5,872.93

Kospi up 0.9% to 2,327.89

German 10Y yield rose 0.3 bps to -0.519%

Euro up 0.03% to $1.1725

Brent Futures down 0.8% to $41.98/bbl

Italian 10Y yield rose 1.4 bps to 0.662%

Spanish 10Y yield rose 0.3 bps to 0.251%

Brent Futures down 0.8% to $41.98/bbl

Gold spot up 0.5% to $1,894.65

U.S. Dollar Index down 0.02% to 93.86

Top Overnight News from Bloomberg

President Donald Trump signed stopgap spending legislation early Thursday to avert a government shutdown weeks before the presidential election, the White House said

U.S. Treasury Secretary Steven Mnuchin and House Speaker Nancy Pelosi plan to resume discussions Thursday on a new pandemic relief package, racing against the clock to resolve their differences on another round of coronavirus stimulus

The European Commission will on Thursday send a “letter of formal notice” to the U.K. for breaching the terms of the Withdrawal Agreement, a person familiar with the matter says

The ECB’s emergency stimulus has propelled excess cash sloshing around the euro area’s economy past 3 trillion euros ($3.5 trillion) for the first time

The Tokyo Stock Exchange halted trading for the entire day Thursday, freezing buying and selling in thousands of companies in the worst-ever outage for the world’s third-largest bourse

Sweden’s Riksbank said in the minutes of its latest monetary policy meeting that if there is a need for more monetary policy stimulus, further expansion of the balance sheet remains an important tool

A quick look at global markets courtesy of NewsSquawk

European cash indices trade with modest gains (Eurostoxx 50 +0.3%), albeit off best levels as Q4 gets underway. Direction is potentially in part due to gains in US equity index futures, which remain elevated near yesterday’s best levels as policymakers in Capitol Hill continue to attempt to broker some form of agreement on COVID-19 stimulus. Focus ahead, will likely be on whether the administration and Democrats can bridge the gap between their respective USD 1.62trl and USD 2.2trl offers respectively and then ultimately whether any agreed deal can make its way through Congress; failure to do so at this juncture will likely mean that the US will not receive a fiscal boost until after the November election. From a European perspective, the DAX (+0.2%) has been a modest laggard throughout the session amid losses in index-heavyweight Bayer (-10.5%) after the Co. announced it is intending to cut around EUR 1.5bln in annual costs whilst citing weakness in the agricultural sector, which desks suggest further undermines the efficacy of the Co.s’ purchase of Monsanto. From a sector standpoint, retail names have been underpinned by upside in H&M (+6.6%) after its Q3 update posted a beat on expectations and revealed plans to lower its store count by 250 in 2021. IT names are also firmer this morning after prelim Q3 earnings from STMicroelectronics (+5.8%) saw the Co. raise its net revenue outlook for the quarter to USD 2.67bln from USD 2.45bln whilst nothing that Q3 was fuelled by “significantly better than expected market conditions throughout the quarter”; peers such as Infineon (+5.7%) and Dialog Semiconductor (+4.1%) have been seen higher in sympathy. Elsewhere, travel & leisure names are the clear laggard in the region with losses in airline names such as IAG (-3.9%), easyJet (-2.3%) and Ryanair (-2%). Finally, Rolls-Royce (-9.5%) have faced heavy selling pressure throughout the session after the Co. announced a GBP 2bln rights issue alongside the intention to begin a bond offering raising at a minimum of GBP 1bln.

Top European News

Brexit Prompts 7,500 City Jobs, $1.6 Trillion to Leave U.K.

H&M German Unit Fined $41.4 Million for Snooping on Staff

ECB’s Overnight Funding Rate Falls to Record Low Amid Cash Glut

UniCredit CEO Says M&A Isn’t a ‘Panacea’ for His Bank

Asia-Pac markets were quiet, owing to the closures in key bourses across the region with China, Hong Kong, Taiwan and South Korea all observing holidays, while trade in Japan was also mired by system issues for the Tokyo Stock Exchange which forced JPX to announce a halt of trade for the entire day. The lack of participants resulted in an uneventful overnight session; however, the mood was still positive as US equity futures extended on gains which had been attributed to month-end flows, strong data and increased stimulus hopes. This was after attempts by US Treasury Secretary Mnuchin and House Speaker Pelosi to reach an agreement on COVID relief and although progress was said to have been made, an actual deal remained elusive and House Democrats were forced to postpone the vote on their USD 2.2tln bill to Thursday to allow more time for talks with the White House. ASX 200 (+1.0%) traded with firm gains and surged above the 5,900 level with the index underpinned as miners led the broad strength in all its sectors, while Nikkei 225 remained suspended alongside Tokyo trade but Osaka futures were higher by 0.2% with a mild lift provided by the tailwinds from US and amid reports Japan is to consider further stimulus to address the pandemic. There was also mixed Tankan data which despite mostly missing expectations including on the headline Large Manufacturers Index, it still showed an improvement of the index for the first time in 11 quarters and Large All Industry Capex also topped estimates. Finally, 10yr JGBs futures were steady just above the 152.00 psychological level with price action contained as firmer results in the 10yr JGB auction was nullified by the system issues in Tokyo.

Top Asian News

Rare Ouster of Indian Bank CEOs to Spur Drive to Find Suitors

Top India Carmaker’s Sales Soar to 2-Year High After Lockdown

Global Investors Sell Record Japanese Debt as FX Swaps Sour

Korea Exports Rise in September for First Time Since Pandemic

In FX, sterling stands as the marked underperformer with initial downside sparked by source reports that the UK and EU have failed to narrow differences on State Aid in trade talks, whilst notably, a senior diplomat said the final agreement will be contingent on the UK withdrawing the Internal Market Bill – a move the UK PM previously rejected, citing UK safeguards. Thereafter, the European Commission President announced that Brussels will begin infringement proceedings against the UK for the breach of the Withdrawal Agreement, again in relation to the IMB. As such, Cable slid from an overnight high of 1.2950 to print a base at 1.2820 before stabilising, whilst EUR/GBP was propelled from 0.9070 to a high just shy of 0.9150. EUR/USD meanwhile has been under some pressure, potentially on Dollar-follow-through from the Sterling weakness as final manufacturing PMIs and an in-line EZ unemployment rate were brushed aside, with the pair briefly dipping below 1.1725 (vs. high 1.1758), whilst today’s NY cut sees a raft of large EUR/USD opex including some EUR 1.175bln rolling off between 1.1700-50 and EUR 2bln between 1.1680-85.

DXY - The broader Dollar and index remain within a tight range but off worst levels with the aid of the aforementioned Sterling weakness, with overnight losses a function of the then upbeat sentiment across markets, with talks on State-side stimulus still in limbo but the two sides seemingly in tense negotiations for an agreement. DXY resides around the middle of its current 93.614-876 intraday band, with downside levels including the 50 DMA at the 93.50 psychological level. The Buck now eyes US PCE Price Index and ISM Manufacturing PMI, alongside another wave of Fed speakers, relief bill talks and the fallout from the Special European Council Summit.

AUD, NZD, CAD - The non-US Dollars stand as the G10 gainers and hold onto APAC upside which was fuelled by overnight sentiment coupled with a firm CNH performance in the absence of the PBoC, and amidst a lack of pertinent data. AUD/USD trades just below 0.7200 having had tested the level to the upside overnight. A breach to the upside would open the door to the 50 and 21 DMAs at 0.7206 and 0.7211 respectively. The Kiwi similarly remains buoyed with a 0.6600+ status but just shy of the 0.6650 psychological level vs. the USD which lines up with the 21DMA. The Loonie’s gains meanwhile are to a lesser extent as the decline in oil prices weigh on the currency, but nonetheless USD/CAD meanders around 1.3300 having printed a current range of 1.3280-3327.

JPY - Shallow losses for the JPY but seemingly on Dollar-dynamics after the technical glitch in Tokyo stock markets. USD/JPY sees itself a touch above 105.50 as it eyes Tuesday’s high at 105.73 and the 50 DMA at 105.75. Note: today’s notable option expiries see USD 1.6bln at 105, USD 1.1bln between 105.30-35 and USD 1.4bln between 105.70-80.

In Commodities, WTI and Brent futures continue to decline in tandem with sentiment in Europe as Brexit remains in the doldrums with the EU readying legal actions against the UK on breaches of “good faith”, whilst crude-specific news-flow for the complex remains light; as participants look towards the day’s European Council gathering & key US data. WTI Nov trades on either side of USD 40/bbl (vs. high 40.47/bbl) whilst Brent Dec oscillates around the USD 42/bbl mark (vs. high 42.55/bbl). Elsewhere, spot gold remains capped by the USD 1900/oz mark as the yellow metal failed another jab at the psychosocial levels, whilst spot silver retraces some of yesterday’s losses and sees itself north of 23.50/oz. Finally, LME copper prices have retreated from earlier highs as the red metal tracks losses in stock markets, Dollar dynamics and overall sentiment.

US Event Calendar

8:30am: Initial Jobless Claims, est. 850,000, prior 870,000; Continuing Claims, est. 12.2m, prior 12.6m

8:30am: Personal Income, est. -2.5%, prior 0.4%; Personal Spending, est. 0.8%, prior 1.9%

9:45am: Markit US Manufacturing PMI, est. 53.5, prior 53.5;

10am: Construction Spending MoM, est. 0.7%, prior 0.1%

10am: ISM Manufacturing, est. 56.4, prior 56; New Orders, est. 65.2, prior 67.6; Prices Paid, est. 58.8, prior 59.5

Wards Total Vehicle Sales, est. 15.7m, prior 15.2m

DB's Jim Reid concludes the overnight wrap

Welcome to October and the last quarter of what has been a decidedly strange year. Markets rounded off a fairly solid Q3 yesterday, even if September was more difficult. The quarter ended on a decent note though, as hopes rose among investors that a US stimulus deal might finally be reached between Republicans and Democrats, even if we were off the highs for the session as nothing materialised from talks. Henry is publishing the latest monthly, quarterly and YTD performance numbers in the next hour so watch out for that. As a spoiler the worst performer in September was the best in Q3. I’ll let you guess what that was before the note hits your inbox.

In terms of yesterday’s developments, the day started with higher expectations on the US fiscal front as Treasury Secretary Mnuchin said on CNBC that he hoped to have an “understanding” worked out with Speaker Pelosi by today. However after having met Pelosi for around 90 minutes yesterday, Mnuchin said that there was no agreement on an additional stimulus package. He tried to keep the mood upbeat, saying “we’ve made progress in a lot of areas.” Pelosi agreed in her own statement, “we found areas where we are seeking further clarification. Our conversations will continue.” The House was supposed to vote on the most recent Democratic proposal for a $2.2 trillion package overnight but it seems that’s now today’s business. That bill will likely be dead on arrival in the Republican Senate, where Senate Majority Leader McConnell called it “outlandish”. McConnell has tempered expectations quite a bit, saying the two sides were “very, very far apart on a deal." Overnight, the Roll Call has reported that Mnuchin has offered a $1.62t relief proposal to Pelosi which includes more state and local assistance than Republican negotiators had previously offered and $400 per week in unemployment insurance.

The earlier initial hopes that a stimulus deal might soon be reached were a boon for risk assets, as the S&P 500 was up +1.74% intra-day. However after Mnuchin and McConnell’s comments the broad index retraced over 1.5% before a slight rally into the close saw the S&P finish +0.83%. Elsewhere the NASDAQ followed a similar pattern, finishing well off its highs, but closing up +0.74%. In Europe, the STOXX 600 fell -0.11% as fiscal stimulus was an issue as well, with Germany warning that delays to the European Union’s Recovery Fund were inevitable given disputes between member countries.

The net positive sentiment in the US was further supported by some positive data surprises. To start with, the ADP’s report of private payrolls in September showed a +749k increase (vs. +649k expected), while the previous month’s figure was revised up by +53k. Furthermore, pending home sales in August saw an +8.8% increase (vs. +3.1% expected), and the MNI Chicago PMI rose to 62.4 in September (vs. 52.0 expected), which was its highest level since December 2018.

Overnight in Asia, the markets which are open are mostly trading up including the Asx (+1.58%) and India’s Nifty (+1.14%). Futures on the S&P 500 are also up +0.51%. Japanese bourses have halted trading for the whole session following a serious hardware breakdown at the Tokyo Stock Exchange. This is the worst breakdown that the world’s third-largest bourse has ever suffered. Currently, there is no guidance on if trading will resume tomorrow. Meanwhile markets in China, Hong Kong and South Korea are closed for a holiday. Chinese markets will remain closed for a week. In Fx, the US dollar index is trading down -0.21%. Elsewhere, spot gold and silver prices are up +0.36% and +1.33% respectively.

In overnight news, President Donald Trump signed an executive order aimed at expanding domestic production of rare-earth minerals vital to most manufacturing sectors and reducing dependence on China. Meanwhile, the Fed has extended through the rest of the year its constraints on dividend payments and share buybacks for the biggest US banks citing “economic uncertainty from the coronavirus response” and the need for the banking industry to preserve capital. Elsewhere, Bloomberg has reported the White House is planning to announce an investigation into Vietnam’s currency practices, under section 301 of the 1974 Trade Act, after the Departments of Commerce and Treasury in August determined that Vietnam had manipulated its currency in a specific trade case involving tires.

The main data highlight of the day ahead will be the manufacturing PMIs from major economies. We have already seen the Jibun Bank Japan PMI come in at 47.7 (vs flash 47.3). In the West, the flash readings generally showed global manufacturing PMIs in expansion territory and roughly in line with expectations, whereas the services readings disappointed. In the Euro Area, the flash manufacturing PMI rose to 53.7, the highest reading since August 2018. While Germany’s flash manufacturing PMI rose to 56.6, not every region saw robust momentum with France (50.9) closer to the 50pt line that divides expansion and contraction. The US ISM manufacturing reading was quite strong last month at 56.0 and the market is expecting 56.4 today. It will be key to see if a recent pickup of covid-19 cases in the Midwest (particularly towards the latter end of the month) affect any momentum. Similarly if the rising coronavirus cases and reintroduction of some restrictions in Europe have affected data there.

In terms of the coronavirus itself, Spain became the most recent country to order restrictions on movement and social gatherings. Spanish Health Minister Illa indicated that a majority of the 17 regions of Spain agreed to the new rules which will limit public services and retail to 50% capacity and install a 10pm closing hour. The measures are meant to target regions with more than 50 infections per 10,000 people or where ICU capacity is strained, currently including Madrid. In the UK, the government reached a compromise with rebel Conservative MPs, as the Health Secretary announced that MPs would be able to have a vote on national regulations before they come into force “wherever possible”. It came as a further 7,121 cases were reported yesterday, pushing the 7-day average up to 6,220. Elsewhere in New York City, the positivity rate fell back to 0.94%, a day after it had been above the 3% threshold which if maintained over a 7-day rolling average could trigger school closures. At the moment, the 7-day rolling average is at 1.46%. See our table below for all the latest Covid cases numbers. The rolling 7-day number remains our focus. Also as we showed in our CoTD link here yesterday, covid has moved up to 20th in the list of the worst pandemics in history. Find out in the note how far it could end up going by looking at other pandemics through history.

Overnight we also saw some vaccine related news, with the CEO of Moderna saying that the company would not be ready to seek emergency use authorisation from the US FDA before November 25 at the earliest. He also added that the company doesn’t expect to have full approval to distribute the drug to all sections of the population until next spring. On the positive side, Bloomberg reported that the European Medicines Agency is expected to announce an accelerated “rolling review” for the University of Oxford and AstraZeneca Plc vaccine candidate as soon as this week to grant it an emergency approval. Such reviews allow regulators to see trial data while the development is ongoing to speed up approvals of drugs and vaccines. The move comes even as the US FDA widened its investigation of a serious illness in AstraZeneca’s vaccine study by asking for data from earlier trials of similar vaccines developed by the same scientists.

As investors moved away from safe havens, the dollar index (-0.01%) fell for a 3rd consecutive session, which concluded a quarter in which the greenback had weakened -3.51% in its worst performance since Q2 2017. And sovereign bonds also sold off on both sides of the Atlantic, with 10yr Treasury yields climbing +2.79bps to reach 0.684%, while in Europe 10yr bunds (+2.3bps), OATs (+2.4bps) and BTPs (+1.5bps) all saw yields rise.

Staying on Europe, following the weak German inflation print on Tuesday, both the French and Italian readings similarly showed readings that were below expectations. In Italy, inflation fell to -0.9% (vs. -0.4% expected), while over in France, inflation came in at 0.0% (vs. +0.2% expected), which was the lowest since April 2016. We’ll get the flash reading for the whole Euro Area on Friday, but given the Euro’s +4.34% appreciation against the US dollar over Q3, the figures will represent yet more unwelcome news for ECB policymakers.

On the US election, there wasn’t a lot of news yesterday following the raucous presidential debate we covered yesterday, and we won’t find out if there’s been any impact on the polls for a few days yet. Nevertheless, the betting/prediction markets have shifted somewhat in Biden’s favour in the last 24 hours, probably because there is little that’s likely to jolt the race out of the current dynamic with a persistent Biden lead in the mid-to-high single digits. The next set-piece event is on Wednesday, with the Vice-Presidential Debate between incumbent VP Mike Pence and California Senator Kamala Harris.

To the day ahead now, and as mentioned earlier the manufacturing PMIs from around the world will be the main data highlight. Otherwise, there’s also the Euro Area unemployment rate for August, the weekly initial jobless claims from the US, as well as US data on personal income, personal spending and construction spending for August. From central banks, we’ll hear from the ECB’s Lane and Hernandez de Cos, the BoE’s Haldane, and the Fed’s Williams and Bowman. Finally, EU leaders will gather in Brussels for a Special European Council summit.

As the industrial market sees some cooling from pandemic-era highs and financing tightens, what should owners and investors expect over the next 12-18…

As the industrial market sees some cooling from pandemic-era highs and financing tightens, what should owners and investors expect over the next 12-18 months? Four national experts took the stage at I.CON West to discuss what lies ahead for this popular asset class.

Capital Raising is Down, Cash is King

Overall, institutional capital raising was down 30-40% in 2023. Institutional investors have been wary of open-ended funds, portfolios have been trimmed and deals are happening increasingly in cash. Considering the current lending environment, more investors prefer unlevered deals.

“I’m always surprised how many groups out there are willing to buy all cash,” said Christy Gahr, director of capital markets, North America, Realterm. “It’s taken off over the last year, especially when the cost of debt is 6%.”

The private equity market is active, and panelists said they see more investment coming from end users. On the debt side, banks are shying away from speculative development projects and focused on smaller transactions last year. Some investors are taking more of a “rifle shot” approach by focusing on targeted, specific projects rather than casting a wide net. There is also interest from life companies that have some liquidity to invest in stabilized industrial product in first-tier markets.

Not Much Distress, But More Scrutiny

PJ Charlton, chief investment officer, CenterPoint Properties, commented he wasn’t seeing much distress and certainly not at 2009 levels. However, there are motivated sellers. It is a suitable time to sell assets out of a fund due to the high leasing rates and spectacular rent growth. “Most sellers today have a reason,” said Tim Walsh, chief investment officer, Dermody, “whether it’s a balance sheet-motivated, whether it’s related to some sort of tax structuring or promises they’ve made to investors.”

What has changed over the past 2-3 years is the approach of investment committees. “Back then it was about aggregation,” said Charlton. “It was all in on industrial… rents were growing 15% a year, cap rates are down another 50 basis points. Interest rates are 3%… Investment committees are reading every page and scrutinizing every word now. It’s a much more discerning buyer than it was three years ago,” he said. Investment committees are focusing on projects in healthy rent growth markets such as New Jersey, Los Angeles and Miami with $50-$150 million deal ranges.

“There is a thesis that there’s a slowdown in developments in all our markets,” said Walsh. “Everyone sees it. There are some submarkets where there weren’t any groundbreakings in the first quarter.” However, there will be an overall return to a balanced supply and demand dynamic.

Embracing ESG

Investors and tenants are increasingly recognizing the importance of ESG, and the panel agreed bigger credit and quality tenants tend to be more environmentally focused. Dermody has increased its environmental standards, making sure each of their building roofs can structurally support solar panels and installing piping and wiring the parking lots for electric charging. “There is a lot of noise out there when it comes to NIMBYism,” said Walsh, “And I think we need to do more to promote the modern environmentally sensitive product that we’re all building.”

Additionally, power supply is becoming more of a concern. “Several years ago, everyone was talking about having the right amount of parking. Now the hot topic is having access to power supply,” said Charlton. Several Fortune 500 companies, including FedEx, have promised to reduce their carbon footprint quickly and that means access to electrified parking. “What we’re seeing is that parking is even more important because now you have fleets that need to be able to charge two or three times a day in last-mile distribution facilities,” said Gahr. “It will change aspects of how we invest and how we underwrite and think about what our properties need to be able to provide our users.”

Nearshoring and Onshoring

Jack Fraker, president and global head of industrial and logistics capital markets for Newmark, turned the discussion to what is happening near the U.S.-Mexico border and asked the panelists what they are seeing in terms of nearshoring. Gahr commented that so much has changed in a short period and cited several statistics. For example, since 2019, China alone has invested in more than 120 projects in Mexico and in over 18 million square feet of industrial space. U.S.-Mexico trade is now outpacing U.S.-China trade by more than 40%.

“During the first half of 2023, $461 billion of goods passed through the U.S.-Mexico border, which is 44% higher than the value of goods between U.S. and China,” said Gahr. More than 150 foreign companies said in 2023 that they will open a new operation or expand into Mexico. These sectors include automotive, energy, manufacturing and IT.

Texas cities Laredo and El Paso were identified as active border markets, and the panelists agreed the best-performing assets are going to be as close to the border as possible. In 2023, El Paso had over three million square feet in total net absorption with a market wide vacancy of less than 4%, according to CBRE. The panelists also discussed the tremendous amount of opportunity in Mexico, although many U.S. development companies have not yet chosen to invest there. Onshoring activity, such as a Samsung project in Austin, is also on the rise.

Overall, the panel remained optimistic about investments, the economy and interest rates. Unemployment is below 4% and the economy is still growing. Additionally, the level of capital that’s sitting in money markets right now is “at $6 trillion – and that’s $2 trillion higher than it was five years ago,” according to Walsh. “So, the giant pile of money persists. And it’s available as soon as people are comfortable coming off the sidelines.”

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

Centre for Doctoral Training in Diversity in Data Visualization awarded over £9m funding from the EPSRC

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research…

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research Council (EPSRC) to help train the next, diverse generation of research leaders in data visualization.

A collaboration between City, University of London and the University of Warwick, the EPSRC Centre for Doctoral Training in Diversity in Data Visualization (DIVERSE CDT) will train 60 PhD students, in cohorts of 12 students, beginning in October 2025. The set-up phase will begin in July 2024.

The funding announcement is part of a wider UK Research & Innovation (UKRI) announcement of the UK’s biggest-ever investment in engineering and physical sciences postgraduate skills, totalling more than £1 billion.

DIVERSE CDT will be supported by 19 partner organisations, including the Natural History Museum, the Ordnance Survey, and the Centre for Applied Education Research.

Data Visualization is the practice of designing, developing and evaluating representations of complex data – the kinds of data that lie at the heart of every organization – to enable more people to make real-world use of a source of information which is otherwise challenging to access.

Data visualization can be used to synthesise complex data into a clear story upon which actions can be based. From illustrating how the Covid-19 pandemic made countries poorer, to showing how the processing-power of cryptocurrencies may have driven up the price of high-street graphics cards; data visualization is crucial to society obtaining meaning from data.

However, no current CDT focuses upon training its students in data visualization. This is despite government’s Department of Digital, Media, Culture and Sport listing data visualization as one of the top five skills needed by businesses – with 23% of businesses saying that their sector has insufficient capacity. Likewise, Wiley’s Digital Skills Gap Index, 2021, listed data visualization as the third most needed business and organisational skill for employees to succeed in the workplace in the next five years.

Key innovations of DIVERSE CDT will include students:

Credit: Alex Kachkaev and Jo Wood, City, University of London

Announced today, a new Centre for Doctoral Training (CDT) has been funded by a grant of over £9 million from the Engineering and Physical Sciences Research Council (EPSRC) to help train the next, diverse generation of research leaders in data visualization.

A collaboration between City, University of London and the University of Warwick, the EPSRC Centre for Doctoral Training in Diversity in Data Visualization (DIVERSE CDT) will train 60 PhD students, in cohorts of 12 students, beginning in October 2025. The set-up phase will begin in July 2024.

The funding announcement is part of a wider UK Research & Innovation (UKRI) announcement of the UK’s biggest-ever investment in engineering and physical sciences postgraduate skills, totalling more than £1 billion.

DIVERSE CDT will be supported by 19 partner organisations, including the Natural History Museum, the Ordnance Survey, and the Centre for Applied Education Research.

Data Visualization is the practice of designing, developing and evaluating representations of complex data – the kinds of data that lie at the heart of every organization – to enable more people to make real-world use of a source of information which is otherwise challenging to access.

Data visualization can be used to synthesise complex data into a clear story upon which actions can be based. From illustrating how the Covid-19 pandemic made countries poorer, to showing how the processing-power of cryptocurrencies may have driven up the price of high-street graphics cards; data visualization is crucial to society obtaining meaning from data.

However, no current CDT focuses upon training its students in data visualization. This is despite government’s Department of Digital, Media, Culture and Sport listing data visualization as one of the top five skills needed by businesses – with 23% of businesses saying that their sector has insufficient capacity. Likewise, Wiley’s Digital Skills Gap Index, 2021, listed data visualization as the third most needed business and organisational skill for employees to succeed in the workplace in the next five years.

Key innovations of DIVERSE CDT will include students:

undertaking and relating a series of applied studies with world-leading industrial and academic partners through a structured internship programme and an exchange programme with 18 leading international labs

using an interactive digital notebook for recording, reflection and reporting which becomes a “thesis” for examination, in lieu of the traditional doctoral thesis, and in line with current best practice in data visualization methodology

being provided with tools that mitigate against the dreaded isolation that PhD students fear, including opportunities for cohort reflection and supportive inclusion via enriching and inclusive processes for admissions, support, and a research environment that addresses barriers for students from under-represented backgrounds; specifically students who identify as female, students from ethnic minority backgrounds and students from lower socio-economic groups.

DIVERSE CDT will be led by Professor Stephanie Wilson, Co-Director of the Centre for HCI Design (HCID) and Professor Jason Dykes, Professor of Visualization and Co-Director of the giCentre, both of the School of Science & Technology at City, University of London.

Members of DIVERSE CDT’s interdisciplinary team include:

Professor Cagatay Turkay and Dr Gregory McInerny from the Centre for Interdisciplinary Methodologies, University of Warwick

Dr Sara Jones, Reader in Creative Interactive System Design, Bayes Business School at City

Professor Rachel Cohen, Professor in Sociology, Work and Employment, School of Policy & Global Affairs at City

Professor Jo Wood, Professor of Visual Analytics, and Dr Marjahan Begum, Lecturer in Computer Science, School of Science & Technology at City

Ian Gibbs, Head of Academic Enterprise at City.

Reflecting on DIVERSE CDT, Co-Principal Investigator, Professor Stephanie Wilson said:

“This funding represents a significant investment from the EPSRC and partner organisations in our vision of an innovative approach to doctoral training. We are delighted to have the opportunity to train a new and diverse generation of PhD students to become future leaders in data visualization.”

Professor Cagatay Turkay said:

“I am thrilled to see this investment for this exciting initiative that brings City and Warwick together to train the next generation of data visualization leaders. Together with our stellar partner organisations, DIVERSE CDT will deliver a transformative training programme that will underpin pioneering interdisciplinary data visualization research that not only innovates in methods and techniques but also delivers meaningful change in the world.”

Dr Sara Jones said:

“I’m really excited to be part of this great new initiative, sharing some of the innovative approaches we’ve developed through the interdisciplinary Centre for Creativity in Professional Practice and Masters in Innovation, Creativity and Leadership, and applying them in this important field.”

Professor Rachel Cohen said:

“DIVERSE CDT puts City at the heart of interdisciplinary data visualization. Data are increasingly part of the social science and policy agenda and it is imperative that those charged with visualizing data understand both the technical and social implications of visualization”

“The CDT is committed to developing and widening the group of people who have the cutting-edge skills needed to visualize, interpret and represent key aspects of our everyday lives. As such it marks a huge step forward both in terms of skill development and representation.”

Professor Leanne Aitken, Vice-President (Research), City, University of London, said:

“Growing the number of doctoral students we prepare in the interdisciplinary field of data visualization is core to our research strategy at City. Doctoral students represent the future of research and expand the capacity and impact of our research. The strength of the DIVERSE CDT is that it draws together our commitment to providing a supportive environment for students from all backgrounds to undertake applied research that challenges current practices in partnership with a range of commercial, public and third sector organisations. This represents an exciting expansion in our doctoral training provision.”

Professor Charlotte Deane, Executive Chair of the EPSRC, part of UKRI, said:

“The Centres for Doctoral Training announced today will help to prepare the next generation of researchers, specialists and industry experts across a wide range of sectors and industries.

“Spanning locations across the UK and a wide range of disciplines, the new centres are a vivid illustration of the UK’s depth of expertise and potential, which will help us to tackle large-scale, complex challenges and benefit society and the economy.

“The high calibre of both the new centres and applicants is a testament to the abundance of research excellence across the UK, and EPSRC’s role as part of UKRI is to invest in this excellence to advance knowledge and deliver a sustainable, resilient and prosperous nation.”

Science and Technology Secretary, Michelle Donelan, said:

“As innovators across the world break new ground faster than ever, it is vital that government, business and academia invests in ambitious UK talent, giving them the tools to pioneer new discoveries that benefit all our lives while creating new jobs and growing the economy.

“By targeting critical technologies including artificial intelligence and future telecoms, we are supporting world class universities across the UK to build the skills base we need to unleash the potential of future tech and maintain our country’s reputation as a hub of cutting-edge research and development.”

ENDS

Notes to editors

Contact details:

To speak to City, University of London collaborators, contact Dr Shamim Quadir, Senior Communications Officer, School of Science & Technology, City, University of London. Tel: +44(0) 207 040 8782 Email: shamim.quadir@city.ac.uk.

To speak to University of Warwick collaborators contact Annie Slinn, Communications Officer, University of Warwick. Tel: +44 (0)7392 125 605 Email: annie.slinn@warwick.ac.uk

Further information

Example data visualization (image)

Bridges – Alex Kachaev and Jo Wood.

Link to image:bit.ly/3Iy3BRz Credit: Alex Kachkaev and Jo Wood, City, University of London

Data visualization for the Museum of London by Alex Kachkaev (a PhD student) with supervisor Joseph Wood, illustrating where people in London congregate in both inside and outside spaces, showing how a creative use of data can be used to build a picture of human behaviour.

Collaborating labs

Collaborators on the international exchange programme comprise the world’s leading visualization research labs, including the Visualization Group at Massachusetts Institute of Technology (MIT), USA, the Embodied Visualisation Group, Monash University, Australia; Georgia Tech, USA; AVIZ, France; the DataXExperience Lab, University of Calgary, Canada, and the ixLab, Simon Fraser University, Canada.

About the funder

The Engineering and Physical Sciences Research Council (EPSRC) is the main funding body for engineering and physical sciences research in the UK. Our portfolio covers a vast range of fields from digital technologies to clean energy, manufacturing to mathematics, advanced materials to chemistry.

EPSRC invests in world-leading research and skills, advancing knowledge and delivering a sustainable, resilient and prosperous UK. We support new ideas and transformative technologies which are the foundations of innovation, improving our economy, environment and society. Working in partnership and co-investing with industry, we deliver against national and global priorities.

About City, University of London

City, University of London is the University of business, practice and the professions.

City attracts around 20,000 students (over 40 per cent at postgraduate level) from more than 150 countries and staff from over 75 countries. In recent years City has made significant investments in its academic staff, its infrastructure, and its estate.

City’s academic range is broadly-based with world-leading strengths in business; law; health sciences; mathematics; computer science; engineering; social sciences; and the arts including journalism, dance and music.

Our research is impactful, engaged and at the frontier of practice. In the last REF (2021) 86 per cent of City research was rated as world leading 4* (40%) and internationally excellent 3* (46%).

We are committed to our students and to supporting them to get good jobs. City was one of the biggest improvers in the top half of the table in the Complete University Guide (CUG) 2023 and is 15th in UK for ‘graduate prospects on track’.

Over 150,000 former students in 170 countries are members of the City Alumni Network.

Under the leadership of our new President, Professor Sir Anthony Finkelstein, we have developed an ambitious new strategy that will direct the next phase of our development.

By a show of hands, I.CON West keynote speaker Christine Cooper, Ph.D., managing director and chief U.S. economist with CoStar Group, polled attendees…

By a show of hands, I.CON West keynote speaker Christine Cooper, Ph.D.,managing director and chief U.S. economist with CoStar Group, polled attendees on their economic outlook – was it bright or bleak? The group responded largely positively, with most indicating they felt the economy was doing better than not.

Four years ago, the World Health Organization declared COVID-19 a global pandemic, seemingly halting life as we knew it. And although those early days of the pandemic seem like a long time ago, we’re still in recovery from two of its major consequences: 1) the $4 trillion in economic stimulus that the U.S. government showered on consumers; and 2) the aggressive monetary policies that have created ripple effects on the industrial markets.

Cooper began with an overview of the economic environment, which she called “the good news.” The nation’s GDP is strong, and the economy gained momentum in the second half of 2023 – we saw economic growth of 4.9% and 3.2% in Q3 and Q4 respectively — much higher than expected. “The reason is consumers,” Cooper said. “When things get tough, we go shopping. This generates sales and economic activity. But how long can it last?”

Consumer sentiment continues to be healthy, and employment is good, although a shortage of workers could impact that moving forward. The U.S. added 275,000 jobs in January, far exceeding expectations. “The Fed raising interest rates hasn’t done what it normally does – slow job growth and the economy,” said Cooper. In addition, the $4 trillion given to keep households afloat during the pandemic has simply padded checking accounts, she said, as consumers couldn’t immediately spend the money because everyone was staying home, and the supply chain was clogged. The money was banked, and there’s still a lot of it to be spent.

Cooper addressed economic risks and the weak points that industrial real estate professionals should be mindful of right now, including mortgage rates that remain at 20-year highs, stalling the housing market, particularly for new home buyers. Mid-pandemic years of 2020-2021 had strong home sales, driven by people moving out of the city or roommates dividing into two properties for more space and protection against the virus. Homeowners who refinanced in the early stages of the pandemic were fortunate and aren’t willing to list their houses for sale quite yet.

“The housing market is a big driver of industrial demand – think furniture, appliances and all the durable goods that go into a home. This equates to warehouse space demand,” said Cooper.

Interest rates on consumer credit are spiking and leading economic indexes are still signaling a recession ahead. Financial markets are indicating the same, with a current probability of 61.5% that we will be in a recession by 2025. However, Cooper said, while all signs point to a recession, economists everywhere say the same thing as the economy seemingly continues to surprise us: “This time is different.”

Consumers are still holding the economy up with solid job and wage gains, yet higher borrowing costs are weighing on business activity and the housing market. Inflation has eased meaningfully but remains a bit too high for comfort. We’ve so far avoided the recession that everyone predicted, and the Federal Reserve appears ready to cut rates this year.

For the industrial markets, the good news is that retailer corporate profits are beginning to bounce back after slowing in 2021 and 2022, with retail sales accelerating.

A slowdown in industrial space absorption was reflected in all the key markets – Atlanta, Chicago, Columbus, Dallas-Fort Worth, Houston, the Inland Empire, Los Angeles, New Jersey and Phoenix – but was worst in the southern California markets, which have since been rebounding.

“Supply responded to strong demand,” Cooper said. “In 2021, 307 million square feet were delivered, followed by 395 million in 2022. In 2023, we saw 534 million square feet delivered – that’s almost 33% higher than the year before.”

The top 20 markets for 2023 deliveries measured by square feet are the expected hot spots: Dallas-Fort Worth (71 million square feet) leads the pack by almost double its follower of Chicago (37 million), then Houston (35 million), Phoenix (30 million) and Atlanta (29 million). Measured by share of inventory, emerging markets like Spartanburg, Pennsylvania, topped the list at 15 million square feet, followed by Austin (10 million), Phoenix and Dallas-Fort Worth (7 million), and Columbus (6 million).

“Developers are more focused on big box distribution projects, and 90% of what’s being delivered is 100,000 square feet or more,” Cooper said. Around 400 million square feet of space currently under construction is unleased, in addition to the around 400,000 square feet that remained unleased in 2023. “Putting supply and demand together, industrial vacancy rate is rising and could peak at 6-7% in 2024,” she said.

In conclusion, Cooper said that industrial real estate is rebalancing from its boom-and-bust years. Pandemic-related demands and accelerated e-commerce growth created a surge in 2021 and 2022, and the strong supply response that began in 2022 will continue to unfold through 2024. With rising interest rates putting a damper on demand in 2023, vacancies began to move higher and will continue to rise this year.

“Consumers are spending and will continue to do so, and interest rates are likely to fall this year,” said Cooper. “We can hope for a recovery from the full effects of the pandemic in 2025.”

This post is brought to you by JLL, the social media and conference blog sponsor of NAIOP’s I.CON West 2024. Learn more about JLL at www.us.jll.com or www.jll.ca.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.