Futures Slide On Growing Stagflation Fears As Treasury Yields Surge

Futures Slide On Growing Stagflation Fears As Treasury Yields Surge

US index futures, European markets and Asian stocks all turned negative during the overnight session, surrendering earlier gains as investors turned increasingly concerned…

Futures Slide On Growing Stagflation Fears As Treasury Yields Surge

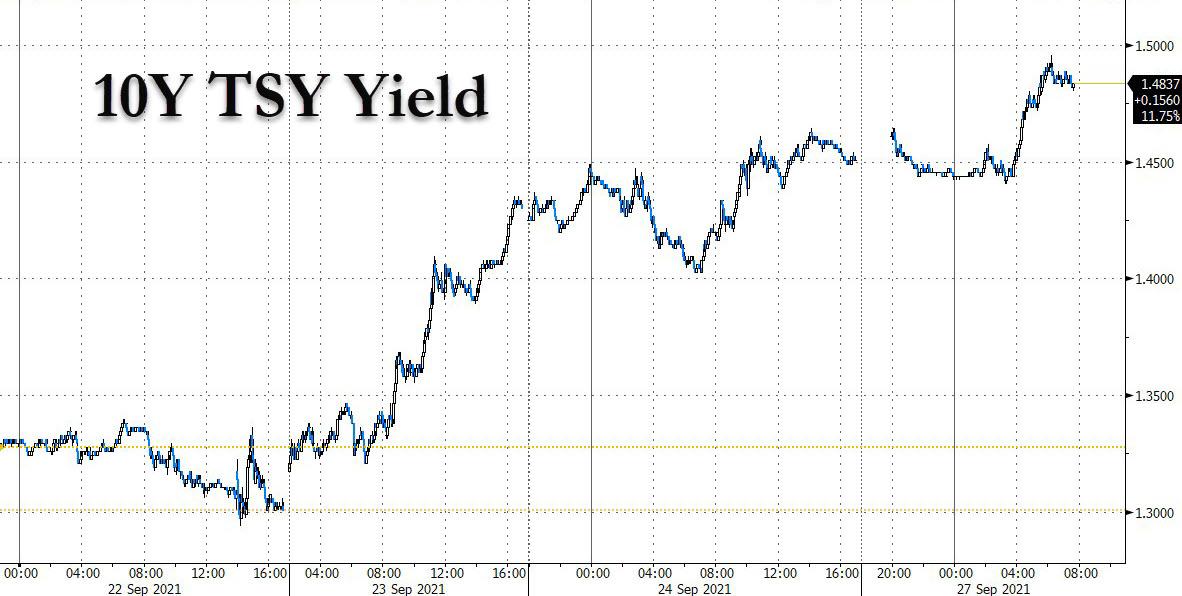

US index futures, European markets and Asian stocks all turned negative during the overnight session, surrendering earlier gains as investors turned increasingly concerned about China's looming slowdown - and outright contraction - amid a global stagflationary energy crunch, which sent 10Y TSY yields just shy of 1.50% this morning following a Goldman upgrade in its Brent price target to $90 late on Sunday. At 745 a.m. ET, S&P 500 e-minis were down 4.75 points, or 0.1% after rising as much as 0.6%, Nasdaq 100 e-minis were down 83 points, or 0.54% and Dow e-minis were up 80 points, or 0.23%. The euro slipped as Germany looked set for months of complex coalition talks.

While the market appears to have moved beyond the Evergrande default, the debt crisis at China's largest developer festers (with Goldman saying it has no idea how it will end), and data due this week will show a manufacturing recovery in the world’s second-largest economy is faltering faster. A developing energy crisis threatens to crimp global growth further at a time markets are preparing for a tapering of Fed stimulus. The week could see volatile moves as traders scrutinize central bankers’ speeches, including Chair Jerome Powell’s meetings with Congressional panels.

“Most bad news comes from China these days,” Ipek Ozkardeskaya, a senior analyst at Swissquote Group Holdings, wrote in a note. “The Evergrande debt crisis, the Chinese energy crackdown on missed targets and the ban on cryptocurrencies have been shaking the markets, along with the Fed’s more hawkish policy stance last week.”

Oil majors Exxon Mobil and Chevron Corp rose 1.5% and 1.2% in premarket trade, respectively, tracking crude prices, while big lenders including JPMorgan, Citigroup, Morgan Stanley and Bank of America Corp gained about 0.8%.Giga-cap FAAMG growth names such as Alphabet, Microsoft, Amazon.com, Facebook and Apple all fell between 0.3% and 0.4%, as 10Y yield surged, continuing their selloff from last week, which saw the 10Y rise as high as 1.4958% and just shy of breaching the psychological 1.50% level.

While growth names were hit, value names rebounded as another market rotation appears to be in place: industrials 3M Co and Caterpillar Inc, which tend to benefit the most from an economic rebound, also inched higher (although one should obviously be shorting CAT here for its China exposure). Market participants have moved into value and cyclical stocks from tech-heavy growth names after the Federal Reserve last week indicated it could begin unwinding its bond-buying program by as soon as November, and may raise interest rates in 2022. Here are some other notable premarket movers:

Gores Guggenheim (GGPI US) shares rise 7.2% in U.S. premarket trading as Polestar agreed to go public with the special purpose acquisition company, in a deal valued at about $20 billion.

Naked Brand (NAKD US), one of the stocks caught up in the first retail trading frenzy earlier this year, rises 11% in U.S. premarket trading, extending Friday’s gains. Among other so-called meme stocks in premarket trading: ReWalk Robotics (RWLK) +6.5%, Vinco Ventures (BBIG) +18%, Camber Energy (CEI) +2.9%

Pfizer (PFE US) and Opko Health (OPK US) in focus after they said on Friday that the FDA extended the review period for the biologics license application for somatrogon. Opko fell 3.5% in post-market trading.

Aspen Group (ASPU) climbed 10% in Friday postmarket trading after board member Douglas Kass buys $172,415 of shares, according to a filing with the U.S. Securities & Exchange Commission.

Seaspine (SPNE US) said spine surgery procedure volumes were curtailed in many areas of the U.S. in 3Q and particularly in August.

Tesla (TSLA US) and other electric- vehicle related stocks globally may be active on Monday after Germany’s election, in which the Greens had their best-ever showing and are likely to be part of any governing coalition.

Europe likewise drifted lower, with the Stoxx Europe 600 Index erasing earlier gains and turning negative as investors weighed the risk to global growth from the China slowdown and the energy crunch. The benchmark was down 0.1% at last check. Subindexes for technology (-0.9%) and consumer (-0.8%) provide the main drags while value outperformed, with energy +2.4%, banks +2% and insurance +1.3%. The DAX outperformed up 0.5%, after German election results avoided the worst-case left-wing favorable outcome. U.S. futures. Rolls-Royce jumped 12% to the highest since March 2020 after the company was selected to provide the powerplant for the B-52 Stratofortress under the Commercial Engine Replacement Program. Here are some of the other biggest European movers today

IWG rises as much as 7.5% after a report CEO Mark Dixon is exploring a multibillion-pound breakup of the flexible office-space provider

AUTO1 gains as much as 6.1% after JPMorgan analyst Marcus Diebel raised the recommendation to overweight from neutral

Cellnex falls as much as 4.3% to a two-month low after the tower firm is cut to sell from neutral at Citi, which says the stock is “priced for perfection in an imperfect industry”

European uranium stocks fall with Yellow Cake shares losing as much as 6% and Nac Kazatomprom shares declining as much as 4.7%. Both follow their U.S. peers down following weeks of strong gains as the price of uranium ballooned

For those who missed it, Sunday's closely-watched German elections concluded with the race much closer than initially expected:

SPD at 25.7%,

CDU/CSU at 24.1%,

Greens at 14.8%,

FDP at 11.5%,

AfD at 10.3%

Left at 4.9%,

the German Federal Returning Officer announced the seat distribution from the preliminary results which were SPD at 206 seats, CDU/CSU at 196. Greens at 118, FDP at 92, AfD at 83, Left at 39 and SSW at 1.

As it stands, three potential coalitions are an option,

1) SPD, Greens and FDP (traffic light),

2) CDU/CSU, Greens and FDP (Jamaica),

3) SPD and CDU/CSU (Grand Coalition but led by the SPD).

Note, option 3 is seen as the least likely outcome given that the CDU/CSU would be unlikely willing to play the role of a junior partner to the SPD. Therefore, given the importance of the FDP and Greens in forming a coalition for either the SPD or CDU/CSU, leaders of the FDP and Greens have suggested that they might hold their own discussions with each other first before holding talks with either of the two larger parties. Given the political calculus involved in trying to form a coalition, the process is expected to play out over several months. From a markets perspective, the tail risk of the Left party being involved in government has now been removed due to their poor performance and as such, Bunds trade on a firmer footing. Elsewhere, EUR is relatively unfazed due to the inconclusive nature of the result. We will have more on this in a subsequent blog post.

Asian stocks fell, reversing an earlier gain, as a drop in the Shanghai Composite spooked investors in the region by stoking concerns about the pace of growth in China’s economy. The MSCI Asia Pacific Index wiped out an advance of as much as 0.7%, on pace to halt a two-day climb. Consumer discretionary names and materials firms were the biggest contributors to the late afternoon drag. Financials outperformed, helping mitigate drops in other sectors. “Seeing Shanghai shares extending declines, investors’ sentiment has turned weak, leading to profit-taking on individual stocks or sectors that have been gaining recently,” said Shoichi Arisawa, an analyst at Iwai Cosmo Securities. “The drop in Chinese equities is reminding investors about a potential slowdown in their economy.” The Shanghai Composite was among the region’s worst performers along with Vietnam’s VN Index. Shares of China’s electricity-intensive businesses tumbled after Beijing curbed power supplies in the country’s manufacturing hubs to cut emissions. The CSI 300 still rose, thanks to gains in heavily weighted Kweichow Moutai and other liquor makers. Asian equities started the day on a positive note as financials jumped, tracking gains in U.S. peers and following a rise in Treasury yields. Resona Holdings was among the top performers after Morgan Stanley raised its view on the stock and Japanese banks. The regional market has been calmer over the past few trading sessions after being whipsawed by concerns over any fallout from China Evergrande Group’s debt troubles. While anxiety lingers, many investors expect China will resolve the distressed property developer’s problems rather than let them spill over into an echo of 2008’s Lehman crisis.

Japanese equities closed lower, erasing an earlier gain, as concerns grew over valuations following recent strength in the local market and turmoil in China. Machinery and electronics makers were the biggest drags on the Topix, which fell 0.1%. Daikin and Bandai Namco were the largest contributors to a dip of less than 0.1% in the Nikkei 225. Both gauges had climbed more 0.5% in morning trading. Meanwhile, the Shanghai Composite Index fell as much as 1.5% as industrials tumbled amid a power crunch. “Seeing Shanghai shares extending declines, investors’ sentiment has turned weak, leading to profit-taking on individual stocks or sectors that have been gaining recently,” said Shoichi Arisawa, an analyst at Iwai Cosmo Securities Co. “The drop in Chinese equities is reminding investors about a potential slowdown in their economy. That’s why marine transportation stocks, which are representative of cyclical sectors, fell sharply.” Shares of shippers, which have outperformed this year, fell as investors turned their attention to reopening plays. Travel and retail stocks gained after reports that the government is making final arrangements to lift all the coronavirus state of emergency order in the nation as scheduled at the end of this month.

Australia's commodity-heavy stocks advanced as energy, banking shares climb. The S&P/ASX 200 index rose 0.6% to close at 7,384.20, led by energy stocks. Banks also posted their biggest one-day gain since Aug. 2. Travel stocks were among the top performers after the prime minister said state premiers must not keep borders closed once agreed Covid-19 vaccination targets are reached. NextDC was the worst performer after the company’s CEO sold 1.6 million shares. In New Zealand, the S&P/NZX 50 index.

In FX, the U.S. dollar was up 0.1%, while the British pound, Australian dollar, and Canadian dollar lead G-10 majors, with the Swedish krona and Swiss franc lagging.

• The Bloomberg Dollar Spot Index was little changed and the greenback traded mixed versus its Group-of-10 peers

o Volatility curves in the major currencies were inverted last week due to a plethora of central bank meetings and risk-off concerns. They have since normalized as stocks stabilize and traders assess the latest forward guidance on monetary policy

• The yield on two-year U.S. Treasuries touched the highest level since April 2020, as tightening expectations continued to put pressure on front-end rates and ahead of debt sales later Monday

• The pound advanced, with analyst focus on supply chain problems as Prime Minister Boris Johnson considers bringing in army drivers to help. Bank of England Governor Andrew Bailey’s speech later will be watched after last week’s hawkish meeting

• Antipodean currencies, as well as the Norwegian krone and the Canadian dollar were among the best Group-of-10 performers amid a rise in commodity prices

• The yen pared losses after falling to its lowest level in six weeks and Japanese stocks paused their rally and amid rising Treasury yields

In rates, treasuries extended their recent drop, led by belly of the curve ahead of this week’s front-loaded auctions, which kick off Monday with 2- and 5-year note sales. Yields were higher by up to 4bp across belly of the curve, cheapening 2s5s30s spread by 3.2bp on the day; 10-year yields sit around 1.49%, cheaper by 3.5bp and underperforming bunds, gilts by 1.5bp and 0.5bpwhile the front-end of the curve continues to sell off as rate-hike premium builds -- 2-year yields subsequently hit 0.284%, the highest level since April 2020. 5-year yields top at 0.988%, highest since Feb. 2020 while 2-year yields reach as high as 0.288%; in long- end, 30-year yields breach 2% for the first time since Aug. 13. Auctions conclude Tuesday with 7-year supply. Host of Fed speakers due this week, including three scheduled for Monday.

In commodities, Brent futures climbed 1.4% to $79 a barrel, while WTI futures hit $75 a barrel for the first time since July, amid an escalating energy crunch across Europe and now China. Base metals are mixed: LME copper rises 0.4%, LME tin and nickel drop over 2%. Spot gold gives back Asia’s gains to trade flat near $1,750/oz

In equities, Stoxx 600 is up 0.6%, led by energy and banks, and FTSE 100 rises 0.4%. Germany’s DAX climbs 1% after German elections showed a narrow victory for social democrats, with the Christian Democrats coming in a close second, according to provisional results. S&P 500 futures climb 0.3%, Dow and Nasdaq contracts hold in the green. In FX, the U.S. dollar is up 0.1%, while the British pound, Australian dollar, and Canadian dollar lead G-10 majors, with the Swedish krona and Swiss franc lagging. Base metals are mixed: LME copper rises 0.4%, LME tin and nickel drop over 2%. Spot gold gives back Asia’s gains to trade flat near $1,750/oz

Investors will now watch for a raft of economic indicators, including durable goods orders and the ISM manufacturing index this week to gauge the pace of the recovery, as well as bipartisan talks over raising the $28.4 trillion debt ceiling. The U.S. Congress faces a Sept. 30 deadline to prevent the second partial government shutdown in three years, while a vote on the $1 trillion bipartisan infrastructure bill is scheduled for Thursday.

On today's calendar we get the latest Euro Area M3 money supply, US preliminary August durable goods orders, core capital goods orders, September Dallas Fed manufacturing activity. We also have a bunch of Fed speakers including Williams, Brainard and Evans.

Market Snapshot

S&P 500 futures down 0.1% to 4,442.50

STOXX Europe 600 up 0.3% to 464.54

MXAP little changed at 200.75

MXAPJ little changed at 642.52

Nikkei little changed at 30,240.06

Topix down 0.1% to 2,087.74

Hang Seng Index little changed at 24,208.78

Shanghai Composite down 0.8% to 3,582.83

Sensex up 0.2% to 60,164.70

Australia S&P/ASX 200 up 0.6% to 7,384.17

Kospi up 0.3% to 3,133.64

German 10Y yield fell 3.1 bps to -0.221%

Euro down 0.3% to $1.1689

Brent Futures up 1.2% to $79.04/bbl

Gold spot little changed at $1,750.88

U.S. Dollar Index up 0.15% to 93.47

Top Overnight News from Bloomberg

House Speaker Nancy Pelosi put the infrastructure bill on the schedule for Monday under pressure from moderates eager to get the bipartisan bill, which has already passed the Senate, enacted. But progressives -- whose votes are likely vital -- are insisting on progress first on the bigger social-spending bill

Olaf Scholz of the center-left Social Democrats defeated Chancellor Angela Merkel’s conservatives in an extremely tight German election, setting in motion what could be months of complex coalition talks to decide who will lead Europe’s biggest economy

China’s central bank pumped liquidity into the financial system after borrowing costs rose, as lingering risks posed by China Evergrande Group’s debt crisis hurt market sentiment toward its peers as well

Global banks are about to get a comprehensive blueprint for how derivatives worth several hundred trillion dollars may be finally disentangled from the London Interbank Offered Rate

Economists warned of lower economic growth in China as electricity shortages worsen in the country, forcing businesses to cut back on production

Governor Haruhiko Kuroda says it’s necessary for the Bank of Japan to continue with large-scale monetary easing to achieve the bank’s 2% inflation target

The quant revolution in fixed income is here at long last, if the latest Invesco Ltd. poll is anything to go by. With the work-from-home era fueling a boom in electronic trading, the majority of investors in a $31 trillion community say they now deploy factor strategies in bond portfolios

A more detailed look at global markets courtesy of Newsquawk

Asian equity markets traded somewhat mixed with the region finding encouragement from reopening headlines but with gains capped heading towards month-end, while German election results remained tight and Evergrande uncertainty continued to linger. ASX 200 (+0.6%) was led higher by outperformance in the mining related sectors including energy as oil prices continued to rally amid supply disruptions and views for a stronger recovery in demand with Goldman Sachs lifting its year-end Brent crude forecast from USD 80/bbl to USD 90/bbl. Furthermore, respectable gains in the largest weighted financial sector and details of the reopening roadmap for New South Wales, which state Premier Berijiklian sees beginning on October 11th, further added to the encouragement. Nikkei 225 (Unch) was kept afloat for most of the session after last week’s beneficial currency flows and amid reports that Japan is planning to lift emergency measures in all areas at month-end, although upside was limited ahead of the upcoming LDP leadership race which reports noted are likely to go to a run-off as neither of the two main candidates are likely to achieve a majority although a recent Kyodo poll has Kono nearly there at 47.4% of support vs. nearest contender Kishida at 22.4%. Hang Seng (+0.1%) and Shanghai Comp. (-0.8%) were varied with the mainland choppy amid several moving parts including back-to-back daily liquidity efforts by the PBoC since Sunday and with the recent release of Huawei’s CFO following a deal with US prosecutors. Conversely, Evergrande concerns persisted as Chinese cities reportedly seized its presales to block the potential misuse of funds and its EV unit suffered another double-digit percentage loss after scrapping plans for its STAR Market listing. There were also notable losses to casino names after Macau tightened COVID-19 restrictions ahead of the Golden Week holidays and crypto stocks were hit after China declared crypto activities illegal which resulted in losses to cryptoexchange Huobi which dropped more than 40% in early trade before nursing some of the losses, while there are also concerns of the impact from an ongoing energy crisis in China which prompted the Guangdong to ask people to turn off lights they don't require and use air conditioning less. Finally, 10yr JGBs were flat but have clawed back some of the after-hour losses on Friday with demand sapped overnight amid the mild gains in stocks and lack of BoJ purchases in the market. Elsewhere, T-note futures mildly rebounded off support at 132.00, while Bund futures outperformed the Treasury space amid mild reprieve from this month’s losses and with uncertainty of the composition for the next German coalition.

Top Asian News

Moody’s Says China to Safeguard Stability Amid Evergrande Issues

China’s Tech Tycoons Pledge Allegiance to Xi’s Vision

China Power Crunch Hits iPhone, Tesla Production, Nikkei Reports

Top Netflix Hit ‘Squid Game’ Sparks Korean Media Stock Surge

Bourses in Europe have trimmed the gains seen at the open, albeit the region remains mostly in positive territory (Euro Stoxx 50 +0.4%; Stoxx 600 +0.2%) in the aftermath of the German election and amid the looming month-end. The week also sees several risk events, including the ECB's Sintra Forum, EZ CPI, US PCE and US ISM Manufacturing – not to mention the vote on the bipartisan US infrastructure bill. The mood in Europe contrasts the mixed handover from APAC, whilst US equity futures have also seen more divergence during European trade – with the yield-sensitive NQ (-0.3%) underperforming the cyclically-influenced RTY (+0.4%). There has been no clear catalyst behind the pullback since the Cash open. Delving deeper into Europe, the DAX 40 (+0.6%) outperforms after the tail risk of the Left party being involved in government has now been removed. The SMI (-0.6%) has dipped into the red as defensive sectors remain weak, with the Healthcare sector towards to bottom of the bunch alongside Personal & Household Goods. On the flip side, the strength in the price-driven Oil & Gas and yield-induced Banks have kept the FTSE 100 (+0.2%) in green, although the upside is capped by losses in AstraZeneca (-0.4%) and heavy-weight miners, with the latter a function of declining base metal prices. The continued retreat in global bonds has also hit the Tech sector – which resides as the laggard at the time of writing. In terms of individual movers, Rolls-Royce (+8.5%) trades at the top of the FTSE 100 after winning a USD 1.9bln deal from the US Air Force. IWG (+6.5%) also extended on earlier gains following reports that founder and CEO Dixon is said to be mulling a multibillion-pound break-up of the Co. that would involve splitting it into several distinct companies. Elsewhere, it is worth being cognizant of the current power situation in China as the energy crisis spreads, with Global Times also noting that multiple semiconductor suppliers for Tesla (Unch), Apple (-0.4% pre-market) and Intel (Unch), which have manufacturing plants in the Chinese mainland, recently announced they would suspend their factories' operations to follow local electricity use policies.

Top European News

U.K. Relaxes Antitrust Rules, May Bring in Army as Pumps Run Dry

Magnitude 5.8 Earthquake Hits Greek Island of Crete

German Stocks Rally as Chances Wane for Left-Wing Coalition

German Landlords Rise as Left’s Weakness Trumps Berlin Poll

In FX, the Aussie is holding up relatively well on a couple of supportive factors, including a recovery in commodity prices overnight and the Premier of NSW setting out a timetable to start lifting COVID lockdown and restrictions from October 11 with an end date to completely re-open on December 1. However, Aud/Usd is off best levels against a generally firm Greenback on weakness and underperformance elsewhere having stalled around 0.7290, while the Loonie has also run out of momentum 10 pips or so from 1.2600 alongside WTI above Usd 75/brl.

DXY/EUR/CHF - Although the risk backdrop is broadly buoyant and not especially supportive, the Buck is gleaning traction and making gains at the expense of others, like the Euro that is gradually weakening in wake of Sunday’s German election that culminated in narrow victory for the SPD Party over the CDU/CSU alliance, but reliant on the Greens and FDP to form a Government. Eur/Usd has lost 1.1700+ status and is holding a fraction above recent lows in the form of a double bottom at 1.1684, but the Eur/Gbp cross is looking even weaker having breached several technical levels like the 100, 21 and 50 DMAs on the way down through 0.8530. Conversely, Eur/Chf remains firm around 1.0850, and largely due to extended declines in the Franc following last week’s dovish SNB policy review rather than clear signs of intervention via the latest weekly Swiss sight deposit balances. Indeed, Usd/Chf is now approaching 0.9300 again and helping to lift the Dollar index back up towards post-FOMC peaks within a 93.494-206 range in advance of US durable goods data, several Fed speakers, the Dallas Fed manufacturing business index and a double dose of T-note supply (Usd 60 bn 2 year and Usd 61 bn 5 year offerings).

GBP/NZD/JPY - As noted above, the Pound is benefiting from Eur/Gbp tailwinds, but also strength in Brent to offset potential upset due to the UK’s energy supply issues, so Cable is also bucking the broad trend and probing 1.3700. However, the Kiwi is clinging to 0.7000 in the face of Aud/Nzd headwinds that are building on a break of 1.0350, while the Yen is striving keep its head afloat of another round number at 111.00 as bond yields rebound and curves resteepen.

SCANDI/EM - The Nok is also knocking on a new big figure, but to the upside vs the Eur at 10.0000 following the hawkish Norges Bank hike, while the Cnh and Cny are holding up well compared to fellow EM currencies with loads of liquidity from the PBoC and some underlying support amidst the ongoing mission to crackdown on speculators in the crypto and commodity space.

In commodities, WTI and Brent front-month futures kicked the week off on a firmer footing, which saw Brent Nov eclipse the USD 79.50/bbl level (vs low 78.21/bbl) whilst its WTI counterpart hovers north of USD 75/bbl (vs low 74.16/bbl). The complex could be feeling some tailwinds from the supply crunch in Britain – which has lead petrol stations to run dry as demand outpaces the supply. Aside from that, the landscape is little changed in the run-up to the OPEC+ meeting next Monday, whereby ministers are expected to continue the planned output hikes of 400k BPD/m. On that note, there have been reports that some African nations are struggling to pump more oil amid delayed maintenance and low investments, with Angola and Nigeria said to average almost 300k BPD below their quota. On the Iranian front, IAEA said Iran permitted it to service monitoring equipment during September 20th-22nd with the exception of the centrifuge component manufacturing workshop at the Tesa Karaj facility, with no real updates present regarding the nuclear deal talks. In terms of bank commentary, Goldman Sachs raised its year-end Brent crude forecast by USD 10 to USD 90/bbl and stated that Hurricane Ida has more than offset the ramp-up in OPEC+ output since July with non-OPEC+, non-shale output continuing to disappoint, while it added that global oil demand-deficit is greater than expected with a faster than anticipated demand recovery from the Delta variant. Conversely, Citi said in the immediate aftermath of skyrocketing prices, it is logical to be bearish on crude oil and nat gas today and forward curves for later in 2022, while it added that near-term global oil inventories are low and expected to continue declining maybe through Q1 next year. Over to metals, spot gold and silver have fallen victim to the firmer Dollar, with spot gold giving up its overnight gains and meandering around USD 1,750/oz (vs high 1760/oz) while spot silver briefly dipped under USD 22.50/oz (vs high 22.73/oz). Turning to base metals, China announced another round of copper, zinc and aluminium sales from state reserves – with amounts matching the prior sales. LME copper remains within a tight range, but LME tin is the outlier as it gave up the USD 35k mark earlier in the session. Finally, the electricity crunch in China has seen thermal coal prices gain impetus amid tight domestic supply, reduced imports and increased demand.

US Event Calendar

8:30am: Aug. Cap Goods Ship Nondef Ex Air, est. 0.5%, prior 0.9%

8:30am: Aug. Cap Goods Orders Nondef Ex Air, est. 0.4%, prior 0.1%

8:30am: Aug. -Less Transportation, est. 0.5%, prior 0.8%

8:30am: Aug. Durable Goods Orders, est. 0.6%, prior -0.1%

10:30am: Sept. Dallas Fed Manf. Activity, est. 11.0, prior 9.0

Central Banks

8am: Fed’s Evans Speaks at Annual NABE Conference

9am: Fed’s Williams Makes Opening Remarks at Conference on...

12pm: Fed’s Williams Discusses the Economic Outlook

12:50pm: Fed’s Brainard Discusses Economic Outlook at NABE Conference

DB's Jim Reid concludes the overnight wrap

Straight to the German elections this morning where unlike the Ryder Cup the race was tight. The centre-left SPD have secured a narrow lead according to provisional results, which give them 25.7% of the vote, ahead of Chancellor Merkel’s CDU/CSU bloc, which are on 24.1%. That’s a bit narrower than the final polls had suggested (Politico’s average put the SPD ahead by 25-22%), but fits with the slight narrowing we’d seen over the final week of the campaign. Behind them, the Greens are in third place, with a record score of 14.8%, which puts them in a key position when it comes to forming a majority in the new Bundestag, and the FDP are in fourth place currently on 11.5%.

Although the SPD appear to be in first place the different parties will now enter coalition negotiations to try to form a governing majority. Both Olaf Scholz and the CDU’s Armin Laschet have said that they will seek to form a government, and to do that they’ll be looking to the Greens and the FDP as potential coalition partners, since those are the most realistic options given mutual policy aims. So the critical question will be whether it’s the SPD or the CDU/CSU that can convince these two to join them in coalition. On the one hand, the Greens have a stronger policy overlap with the SPD, and governed with them under Chancellor Schröder from 1998-2005, but the FDP seems more in line with the Conservatives, and were Chancellor Merkel’s junior coalition partner from 2009-13. So it’s likely that the FDP and the Greens will talk to each other before talking to either of the two biggest parties.

For those wanting more information, our research colleagues in Frankfurt have released a post-election update (link here) on the results and what they mean. An important implication of last night’s result is that (at time of writing) it looks as though a more left-wing coalition featuring the SPD, the Greens and Die Linke would not be able for form a majority in the next Bundestag. So the main options left are for the FDP and the Greens to either join the SPD in a “traffic light” coalition or instead join the CDU/CSU in a “Jamaica” coalition. The existing grand coalition of the SPD and the CDU/CSU would actually have a majority as well, but both parties have signalled that they don't intend to continue this. That said, last time in 2017, a grand coalition wasn’t expected after that result, and there were initially attempts to form a Jamaica coalition. But once those talks proved unsuccessful, discussions on another grand coalition began once again.

In terms of interesting snippets, this election marks the first time the SPD have won the popular vote since 2002, which is a big turnaround given that the party were consistently polling in third place over the first half of this year. However, it’s also the worst ever result for the CDU/CSU, and also marks the lowest combined share of the vote for the two big parties in post-war Germany, which mirrors the erosion of the traditional big parties we’ve seen elsewhere in continental Europe. Interestingly, the more radical Die Linke and AfD parties on the left and the right respectively actually did worse than in 2017, so German voters have remained anchored in the centre, and there’s been no sign of a populist resurgence. This also marks a record result for the Greens, who’ve gained almost 6 percentage points relative to four years ago, but that’s still some way down on where they were polling earlier in the spring (in the mid-20s), having lost ground in the polls throughout the final weeks of the campaign.

Markets in Asia have mostly started the week on a positive note, with the Hang Seng (+0.28%), Nikkei (+0.04%), and the Kospi (+0.25%) all moving higher. That said, the Shanghai Comp is down -1.30%, as materials (-5.91%) and industrials (-4.24%) in the index have significantly underperformed, which comes amidst power curbs in the country. In the US and Europe however, futures are pointing higher, with those on the S&P 500 up +0.37%, and those on the DAX up +0.51%.

Moving onto another big current theme, all the talk at the moment is about supply shocks and it’s not inconceivable that things could get very messy on this front over the weeks and months ahead. However, I think the discussion on supply in isolation misses an important component and that is demand. In short we had a pandemic that effectively closed the global economy and interrupted numerous complicated supply chains. The global authorities massively stimulated demand relative to where it would have been in this environment and in some areas have created more demand than there would have been at this stage without Covid. However the supply side has not come back as rapidly. As such you’re left with demand outstripping supply. So I think it’s wrong to talk about a global supply shock in isolation. It’s not as catchy but this is a “demand is much higher than it should be in a pandemic with lockdowns, but supply hasn't been able to fully respond” world. If the authorities hadn’t responded as aggressively we would have plenty of supply for the demand and a lot of deflation. Remember negative oil prices in the early stages of the pandemic. So for me every time you hear the phrase “supply shock” remember the phenomenal demand there is relative to what the steady state might have been.

This current “demand > supply” at lower levels of activity than we would have had without covid is going to cause central banks a huge headache over the coming months. Should they tighten due to what is likely to be a prolonged period of higher prices than people thought even a couple of months ago or should they look to the potential demand destruction of higher prices? The risk of a policy error is high and the problem with forward guidance is that markets demand to know now what they might do over the next few months and quarters so it leaves them exposed a little in uncertain times. This problem has crept up fast on markets with an epic shift in sentiment in the rates market after the BoE meeting Thursday lunchtime. I would say they were no more hawkish than the Fed the night before but the difference is that the Fed are still seemingly at least a year from raising rates and a lot can happen in that period whereas the BoE could now raise this year (more likely February). That has focused the minds of global investors, especially as Norway became the first central bank among the G-10 currencies to raise rates on the same day. Towards the end of this note we’ll recap the moves in markets last week including a +15bps climb in US 10yr yields in the last 48 hours of last week.

One factor that will greatly influence yields over the week ahead is the ongoing US debt ceiling / government shutdown / infrastructure bill saga that is coming to a head as we hit October on Friday - the day that there could be a partial government shutdown without action by the close on Thursday. It’s a fluid situation. So far the the House of Representatives has passed a measure that would keep the government funded through December 3, but it also includes a debt ceiling suspension, so Republicans are expected to block this in the Senate if it still includes that.

The coming week could also see the House of Representatives vote on the bipartisan infrastructure bill (c.$550bn) that’s already gone through the Senate, since Speaker Pelosi had previously committed to moderate House Democrats that there’d be a vote on the measure by today. She reaffirmed that yesterday although the timing may slip. However, there remain divisions among House Democrats, with some progressives not willing to support it unless the reconciliation bill also passes. In short we’ve no idea how this get resolved but most think some compromise will be reached before Friday. Pelosi yesterday said it “seems self-evident” that the reconciliation bill won’t reach the $3.5 trillion hoped for by the administration which hints at some compromise. Overall the sentiment has seemingly shifted a little more positively on there being some progress over the weekend.

From politics to central banks and following a busy week of policy meetings, there are an array of speakers over the week ahead. One of the biggest highlights will be the ECB’s Forum on Central Banking, which is taking place as an online event on Tuesday and Wednesday, and the final policy panel on Wednesday will include Fed Chair Powell, ECB President Lagarde, BoE Governor Bailey and BoJ Governor Kuroda. Otherwise, Fed Chair Powell will also be testifying before the Senate Banking Committee on Tuesday, alongside Treasury Secretary Yellen, and on Monday, ECB President Lagarde will be appearing before the European Parliament’s Committee on Economic and Monetary Affairs as part of the regular Monetary Dialogue. There are lots of other Fed speakers this week and they can add nuances to the taper and dot plot debates.

Finally on the data front, there’ll be further clues about the state of inflation across the key economies, as the Euro Area flash CPI estimate for September is coming out on Friday. Last month's reading showed that Euro Area inflation rose to +3.0% in August, which was its highest level in nearly a decade. Otherwise, there’s also the manufacturing PMIs from around the world on Friday given it’s the start of the month, along with the ISM reading from the US, and Tuesday will see the release of the Conference Board’s consumer confidence reading for the US as well. For the rest of the week ahead see the day-by-day calendar of events at the end.

Back to last week now and the highlight was the big rise in global yields which quickly overshadowed the ongoing Evergrande story. Bonds more than reversed an early week rally as yields rose for a fifth consecutive week. US 10yr Treasury yields ended the week up +8.9bps to finish at 1.451% - its highest level since the start of July and +15bps off the Asian morning lows on Thursday. The move saw the 2y10y yield curve steepen +4.5bps, with the spread reaching its widest point since July as well. However, at the longer end of the curve the 5y30y spread ended the week largely unchanged after a volatile week. It was much flatter shortly following the FOMC and steeper following the BoE. Bond yields in Europe moved higher as well with the central bank moves again being the major impetus especially in the UK. 10yr gilt yields rose +7.9bps to +0.93% and the short end moved even more with the 2yr yield rising +9.4bps to 0.38% as the BoE’s inflation forecast and rhetoric caused investors to pull forward rate hike expectations. Yields on 10yr bunds rose +5.2bps, whilst those on the OATs (+6.3bps) and BTPs (+5.7bps) increased substantially as well, but not to the same extent as their US and UK counterparts.

While sovereign debt sold off, global equity markets recovered following two consecutive weeks of declines. Although markets entered the week on the back foot following the Evergrande headlines from last weekend, risk sentiment improved at the end of the week, especially toward cyclical industries. The S&P 500 gained +0.51% last week (+0.15% Friday), nearly recouping the prior week’s loss. The equity move was primarily led by cyclicals as higher bond yields helped US banks (+3.43%) outperform, while higher commodity prices saw the energy (+4.46%) sector gain sharply. Those higher bond yields led to a slight rerating of growth stocks as the tech megacap NYFANG index fell back -0.46% on the week and the NASDAQ underperformed, finishing just better than unchanged (+0.02). Nonetheless, with four trading days left in September the S&P 500 is on track for its third losing month this year, following January and June.

European equities rose moderately last week, as the STOXX 600 ended the week +0.31% higher despite Friday’s -0.90% loss. Bourses across the continent outperformed led by particularly strong performances by the IBEX (+1.28%) and CAC 40 (+1.04%).

There was limited data from Friday. The Ifo's business climate indicator in Germany fell slightly from the previous month to 98.8 (99.0 expected) from 99.4 on the back a lower current assessment even though business expectations was higher than expected. In Italy, consumer confidence rose to 119.6 (115.8 expected), up just over 3pts from August and at its highest level on record (since 1995).

Vetted by HousingWire | Our editors independently review the products we recommend. When you buy through our links, we may earn a commission.

Real estate is a vibrant, dynamic and competitive industry. From the thrill of a sale to the pursuit of new leads, it keeps you on your toes. That said, it can also be incredibly isolating, and it can be hard to stay motivated. As a way to deal with this, many agents and brokers seek out professional mentorship as a means to gain insight and level up their performance. Across the country, the best real estate coaches serve as valuable mentors who can help agents and brokers achieve the success they deserve.

“It’s really hard for independent business owners to get unbiased advice from themselves,” says Kyle Scott, President of SERHANT. Ventures. “So they need unbiased experts to work with that will help them grow their business — someone who has been there, who has done it, and who is able to see their business from both the 35,000-foot view and down in the weeds.”

A quick internet search will prove that real estate coaching programs are plentiful. Whether you’re looking to expand your team or client network or figure out how to delegate work so you can focus on the tasks you do best, a real estate coaching program could be a valuable launchpad. But when it comes to choosing the right one for your unique needs, there’s a lot to consider. Here, we highlight some of the best real estate coaches in the industry and their programs.

An unbiased view is worth millions. Often, we turn to our closest friends and family for guidance. Unfortunately, they’re usually not familiar with the ins and outs of the real estate industry and can’t provide you with the relevant feedback you need. As a result, many independent contractors rely on themselves, which generally doesn’t work either.

You can’t advise yourself, you’re too close to it. A coach works best for someone who is actually looking to grow their business, someone who is looking to put in the time and the energy to make a difference in achieving more income this year.

Hire a coach if you want to start taking your business to the next level for any reason — you want to make more money, have more freedom with your time, or stop riding the ins and outs of the commission cycle.President of SERHANT. Ventures

1. Sell It Like Serhant

Key Facts

Grown throughout the pandemic, the Sell It Like Serhant program has been carefully adapted to the current market. It follows a weekly and bi-weekly platform featuring one-on-one virtual coaching from Serhant’s proprietary video platform. After a half-hour or hour-long group meeting every week or every other week, participants follow actionable steps to help them grow their business. Thus far, more than 22,000 enrollees in 128 countries have been through the Sell It Like Serhant program.

What We Love

Serhant offers daily office hours so participants can pop into virtual sessions to ask questions or get expert advice between their regularly scheduled sessions. A community platform also allows participants to pass referrals to each other. Thus far, it seems to have worked: To date, participating agents have closed over $250 million of referral deals.

Pricing

There are different membership tiers, depending on the level of guidance you need. The introductory Real Estate Core Course starts at $497. Prices are higher for a more specific course or one with 1:1 coaching.

Who’s it Best For?

If you’re looking to build a memorable personal brand, SERHANT. is the way to go. “The number one differentiator about our program is we understand that as a real estate agent, you have one job: to generate leads,” says SERHANT. Ventures President Kyle Scott. “Our number one focus is helping you build a clear, compelling, memorable personal brand and put your lead generation on autopilot. So that way, you can do what you do best, which is build relationships and close deals.”

Visit Sell It Like Serhant

2. Tom Ferry International

Key Facts

For good reason, Ferry International refers to itself as the real estate industry’s leading coaching and training company. Focused on Ferry’s “8 Levels of Performance,” the programs are a staple of real estate coaching. Their new group coaching sessions cover various aspects of real estate sales.

Prospecting Bootcamp is a 14-hour program comprised of seven two-hour group coaching sessions, and includes a peer-to-peer collaboration space. It involves independent work pulled from training videos and downloadable resources.

Recruitment Roadmap consists of hour-long sessions each week for ten weeks. Completed over Zoom and through the Tom Ferry video platform, each group coaching program offers a high level of specialization.

Finally, their Fast Track program offers 12 interactive group coaching sessions designed to help new agents build the necessary skills to succeed — like mastering listing presentations and handling objections.

What we love

If you’re looking for the gold standard of real estate coaching, Tom Ferry has the goods to back up the bravado. Because of their many years in the biz, Tom Ferry has a huge base of coaches, which means there are plenty of options to find the program best suited for your specific needs.

Pricing

Tom Ferry’s Prospecting Bootcamp and Fast Track coaching programs cost $999 but can be broken down into three monthly payments. The Recruitment Roadmap group coaching costs $1,499 but can be split into three monthly payments of $500. Consider their free coaching consultation if you want to dip your toes in the water. Check out their customer reviews, where several coaching program alums rave about the program.

Who’s it Best For?

If you thrive in a group setting that allows you to feed off the energy of others, Tom Ferry might be right for you. Their group coaching programs are new and more affordable alternatives to often costly 1:1 coaching fees.

Visit Tom Ferry

3. Tim and Julie Harris

Key Facts

The dynamic duo of real estate coaching, Tim and Julie Harris are a major name in the industry. Under their business, Harris Real Estate Coaching, their programs are divided into three tiers: Premier, Premier Plus, and VIP, all of which rely on a user-friendly online platform.

Pricing

Premier platform costs $197 per month, but a 30-day free trial is available. Premier Plus costs $599 per month, while VIP costs $999 per month. Of course, their wildly successful podcast is a great free resource to tap into, as well as Tim and Julie’s many written contributions to HousingWire.

Who’s it Best For?

If you’re constantly on the go, the ability to access the course from any device is a major asset.

4. Candy Miles-Crocker

Key Facts

Newbies are welcome at Candy Miles Crocker’s program. Known as the “Real Life Realtor,” she’s the brain behind Real Life Real Estate Training. With a variety of courses in her offerings, including a plethora of self-paced online courses, Miles-Crocker gives new agents a leg-up on the rest.

What we love

Miles-Crocker is still an active agent, working with clients to close deals. Her 20+ years of experience practicing in Washington, D.C., Virginia and Maryland have helped her build “systems, strategies and scripts” that she shares with her coaching clients.

Pricing

The CORE Essentials Blueprint program retails for $1,597. Smaller, more specific courses, such as The Buyer Presentation, are priced at $347. While all pricing isn’t listed on her website, Miles-Crocker also offers a free course that includes her 6-point system for growth.

Who’s it Best For?

Miles-Crocker’s courses could be beneficial if you are new to agent life or looking to get your business reorganized. She even has one specifically for your first 30 days as a real estate agent.

5. Ashley Harwood

Key Facts

Boston-based Ashley Harwood inspires introverts with her convincing, heartfelt and high-touch approach to practicing real estate. Her very human, very relatable Move Over Extroverts coaching approach is the perfect antidote for cheerleader-style coaches that urge you to door-knock, chase down divorce leads or become a social media superstar.

What we love

Harwood is a licensed agent coaching agents week-in and week-out at no less than three Keller-Williams offices in the great Boston metro. We love her humanity, inspiring videos, and her latest enterpise — The Quiet Success Club. Inspired by Susan Cain’s New York Times bestseller Quiet, about the power of introverts, Harwood brings together a community of like-minded real estate agents wanting a more client-centric approach to succeeding as an agent.

Pricing

Join The Quiet Success Club for $45 per month (paid monthly) or get two months free when you pay for an annual subscription (for $450). The club is currently offering founding member pricing for $25 per month or $250, but it’s a limited-time offer available only under April 30, 2024. Or get a lifetime membership to Harwood’s suite of courses, called IntrovertU, for a one-time cost of $997.

Who’s it Best For?

Introverts, of course! While you may not count yourself as one, if you read Susan Cain’s book, you may unearth your more introverted traits — like recharging your battery by being alone. Ok, even if you don’t bask in solitude, Harwood promises a calming community where agents can be themselves, be seen, and where they don’t have to be the loudest voice in her mastermind group, purposefully (and quietly) designed to teach successful lead generation and other strategies.

6. Levi Lascsak

If you’re looking to improve your social media game, Levi Lascsak is the YouTube master. The author of Passive Prospecting specializes in helping real estate professionals embrace the video platform, and he does so in jam-packed, 2-day virtual events. Discover how he earned over $4 million in gross commission income as a new agent.

What we love

Lascsak’s social media marketing skills are top-of-the-line. While he may not be part of the traditional world of real estate coaching, Lascak’s ability to relate to younger audiences is an asset that Millennial and Gen Z agents might appreciate.

Pricing

The live, 2-day events are available at a discount for $47. But as you can expect, he’s got endless information available for free on YouTube.

Who’s it best for?

If you’re a digital native looking to pack a bunch of education into a short period, a Lascsak course is particularly beneficial.

7. Jess Lenouvel

Key Facts

Promising to help agents scale from six to seven figures, The Listings Lab founder Jess Lenouvel is the author of More Money, Less Hustle. A strong example of a coach with a significant understanding of social media, Lenouvel hosts vibrant live events that hype up the audience and prepare them to take their career to the next level.

What we Love

Lenouvel emphasizes the significant power of mindset to achieve one’s goals. She understands how quickly the market shifts and emphasizes staying on top of trends to succeed.

Lenouvel’s live events focus on messaging. For those looking to solidify their brand and develop a clear, concise message, her events might be what you need.

8. Buffini & Company

Key Facts

Another giant of the real estate coaching industry, Buffini & Company is one of the largest coaching and training companies in the United States. They have two major coaching programs: The Leadership Coaching program includes three monthly coaching calls, free admission to a 2-day conference, and curriculums and training led by Brian Buffini. There are also bi-monthly coaching sessions and a monthly web series with a live Q&A.

Buffini & Company also performs a REALstrengths profile — an in-depth personality assessment. In the One2One Coaching program, there are two coaching calls per month, a monthly marketing kit, the REALStrengths profile, and as with the SERHANT. program, Buffini features the Buffini Referral Network, allowing participants to send and receive referrals with other agents.

What We Love

Buffini coaches aren’t independent contractors. Instead, they’re full-time employees who go through intense training. Thus far, they’ve conducted 1.7 million coaching calls and more than one million hours of coaching.

Pricing

The Leadership Coaching program costs $1,499 a month. Private coaching, referred to as One2One Coaching, costs $549 per month. Two tiers of Referral Maker courses are available from $45 to $149 each per month.

Who’s it Best For?

Team spirit is the name of the game for Buffini’s Leadership Coaching program. If you’re a team leader looking to improve your coaching skills and assist your team in leveling up, the Leadership Coaching program might be right for you. If you want a more personalized path as a solo agent, the One2One Coaching program may be a better fit.

9. Vanda Martin

Key Facts

A popular name in the real estate coaching industry, Vanda Martin’s VIP Coaching Program follows three components: coaching, content, and community. Martin doesn’t shy away from mistakes – instead, she emphasizes avoiding indecision that puts you behind the pack.

What we love

Positive vibes are plentiful in Martin’s world, and her energy is tangible. Just check out her Instagram videos.

Pricing

Martin’s pricing isn’t listed.

Who’s it best for?

If you’re looking for a female leader who emphasizes loving your job and building habits that will take you to a greater level of success, Martin’s ability to convey those feelings is clear. Just check out the endless testimonials on her website.

9. Tat Londono

Key Facts

Tatiana Londono is the founder and CEO of Londono Realty Group Inc. The author of Real Estate Unfiltered, she offers a variety of programming that ranges from free templates to intensive coaching sessions. The Millionaire Realtor Membership provides weekly input from Londono, while the intensive Millionaire Real Estate Agent Coaching Program focuses on building 12-month objectives using a custom success action plan. It uses live programming and workshops with Londono herself, as well as an exclusive online community and referral network for members.

What we love

Londono’s keen sense of social media and her posts are a masterclass in how to boost your engagement on platforms like TikTok and Instagram. Don’t miss her takes on Taylor Swift’s real estate portfolio.

Londono’s programs specifically target agents who are looking to scale their business. If you’re struggling with lead generation or want to increase the number of views you’re racking up on social media, Londono is a valuable source within the industry.

10. Steve Shull

Key Facts

Steve Shull’s Performance Coaching focuses on using consistent execution to achieve your goals. With options ranging from 1:1 private coaching to small group coaching for 10 to 20 agents, the groups have 30-minute Zoom calls three times a day, but the number of sessions you choose to attend is up to you. Several self-directed courses are also available on the website, focusing on topics ranging from mindset to time blocking.

What we love

If you’re not positive you want to make the investment, Performance Coaching allows a 14-day free trial of daily accountability calls.

Pricing

Small group coaching costs $6,000 a year, and while 1:1 coaching prices aren’t listed online, you should prepare for a hefty price tag.

Who’s it Best For?

If you have a specific area you’re looking to improve upon, Performance Coaching offers coaches with unique areas of expertise, ranging from CRMs to business strategy. Tailoring your program to your greatest areas of weakness can help you become a more well-rounded agent.

11. Aaron Novello

Key Facts

Aaron Novello of Elite Real Estate Coaching has several programs tailor-made for agents looking to hone their craft. A Masterclass in Systems works to teach agents how to scale their real estate business, organize their team, and use programming like Follow Up Boss to manage their business.

The Role Play Mastermind is for agents looking to prepare themselves for tough discussions by working with a role-play partner for 15 to 30 minutes, five days a week. The group coaching option includes a variety of scripts Novello used to close on homes, as well as mindset guides, skill sheets, and expert guidance from experts in the field.

What we love

Novello’s exclusive accountability group allows active members and former coaching clients to share everything from guidance to motivation. If you’re looking to save money, Novello also has a free podcast available on YouTube.

If you struggle with having difficult conversations and are looking for solid templates to guide you, Novello’s Role Play Mastermind is a solid investment. The group coaching option emphasizes taking the educational portion and putting it into practice in the real world rather than just watching videos.

12. Krista Mashore Coaching

Key Facts

Filled with energy and known for popping up in the press, Krista Mashore is the mind behind Unstoppable Agent, her 3-day mastery class. It includes over 15 hours of coaching, group workshops, breakout sessions, and skill-building workshops to provide you with the skills to implement digital marketing successfully into your real estate business.

What we love

A positive attitude counts for a lot, and Mashore’s personality is a key component of the success of her course.

Pricing

Mashore’s accessibility is another one of her program’s best assets. Her 3-day class is currently priced at $47, but pricing occasionally varies.

Who’s it best for?

If you crave energy and enthusiasm, Krista Mashore has the goods. She’s also an expert on working in today’s low-inventory market, which is ideal for someone struggling with the current housing shortage. But she’s also got a good sense of humor, which shines through in her social media presence.

The full picture: The best real estate coaches for 2024

Hiring a top real estate coach goes far beyond just expanding your skills. While growing and educating yourself as you navigate your career is essential, hiring a coach is all about seeking to achieve more. Whether you’re looking to boost lead generation, build a solid personal brand, or make more commission income, having the input of a seasoned expert is a priceless step in the right direction. As you can see through the endless reviews and testimonials on coaches’ websites, agents who want to scale their business and take their profits to a higher level often seek the outside guidance of a coach. While the cost of hiring someone may be significant, the return on investment is equally as monumental.

Real estate coaching programs vary in price significantly. Most cost over $500 per month, with others charging several thousand dollars per month. “Oftentimes, it is the case that you get what you pay for,” said Kyle Scott, President of SERHANT. Ventures.

However, prices can also vary depending on the specific niche of real estate coaching you’re focusing on. The more specificity you’re seeking, the higher the financial investment. Of course, self-led courses are likely to cost much less.

Does your career feel stalled right now? Are you ready to take your career to the next level, but you’re not sure where to start? In a down market, you can channel your time and energy into actively improving your business skills so that you’ll be sufficiently prepared for when the market changes.

“When things pick up again, you’re ready to capture the climbing market,” says Scott. “If that’s the case, then the best time to embrace coaching is now. At the same time, a thriving market presents agents with new challenges, ranging from having to turn away business or being unable to service your existing business in a way you’re proud of,” Scott noted. “In that type of market, a real estate coach can help you determine what kind of junior agent or assistant would serve you best. How do I figure out how to manage my business in a way that I can keep up with the volume?”

Former Secretary of State Mike Pompeo said in a new interview that he’s not ruling out accepting a White House position if former President Donald Trump is reelected in November.

“If I get a chance to serve and think that I can make a difference ... I’m almost certainly going to say yes to that opportunity to try and deliver on behalf of the American people,” he told Fox News, when asked during a interview if he would work for President Trump again.

“I’m confident President Trump will be looking for people who will faithfully execute what it is he asked them to do,” Mr. Pompeo said during the interview, which aired on March 8. “I think as a president, you should always want that from everyone.”

He said that as a former secretary of state, “I certainly wanted my team to do what I was asking them to do and was enormously frustrated when I found that I couldn’t get them to do that.”

Mr. Pompeo, a former U.S. representative from Kansas, served as Central Intelligence Agency (CIA) director in the Trump administration from 2017 to 2018 before he was secretary of state from 2018 to 2021. After he left office, there was speculation that he could mount a Republican presidential bid in 2024, but announced that he wouldn’t be running.

President Trump hasn’t publicly commented about Mr. Pompeo’s remarks.

In 2023, amid speculation that he would make a run for the White House, Mr. Pompeo took a swipe at his former boss, telling Fox News at the time that “the Trump administration spent $6 trillion more than it took in, adding to the deficit.”

“That’s never the right direction for the country,” he said.

In a public appearance last year, Mr. Pompeo also appeared to take a shot at the 45th president by criticizing “celebrity leaders” when urging GOP voters to choose ahead of the 2024 election.

2024 Race

Mr. Pompeo’s interview comes as the former president was named the “presumptive nominee” by the Republican National Committee (RNC) last week after his last major Republican challenger, former South Carolina Gov. Nikki Haley, dropped out of the 2024 race after failing to secure enough delegates. President Trump won 14 out of 15 states on Super Tuesday, with only Vermont—which notably has an open primary—going for Ms. Haley, who served as President Trump’s U.S. ambassador to the United Nations.

On March 8, the RNC held a meeting in Houston during which committee members voted in favor of President Trump’s nomination.

“Congratulations to President Donald J. Trump on his huge primary victory!” the organization said in a statement last week. “I’d also like to congratulate Nikki Haley for running a hard-fought campaign and becoming the first woman to win a Republican presidential contest.”

Earlier this year, the former president criticized the idea of being named the presumptive nominee after reports suggested that the RNC would do so before the Super Tuesday contests and while Ms. Haley was still in the race.

Also on March 8, the RNC voted to name Trump-endorsed officials to head the organization. Michael Whatley, a North Carolina Republican, was elected the party’s new national chairman in a vote in Houston, and Lara Trump, the former president’s daughter-in-law, was voted in as co-chair.

“The RNC is going to be the vanguard of a movement that will work tirelessly every single day to elect our nominee, Donald J. Trump, as the 47th President of the United States,” Mr. Whatley told RNC members in a speech after being elected, replacing former chair Ronna McDaniel. Ms. Trump is expected to focus largely on fundraising and media appearances.

President Trump hasn’t signaled whom he would appoint to various federal agencies if he’s reelected in November. He also hasn’t said who his pick for a running mate would be, but has offered several suggestions in recent interviews.

In various interviews, the former president has mentioned Sen. Tim Scott (R-S.C.), Texas Gov. Greg Abbott, Rep. Elise Stefanik (R-N.Y.), Vivek Ramaswamy, Florida Gov. Ron DeSantis, and South Dakota Gov. Kristi Noem, among others.

Riley Gaines Explains How Women's Sports Are Rigged To Promote The Trans Agenda

Is there a light forming when it comes to the long, dark and bewildering tunnel of social justice cultism? Global events have been so frenetic that many people might not remember, but only a couple years ago Big Tech companies and numerous governments were openly aligned in favor of mass censorship. Not just to prevent the public from investigating the facts surrounding the pandemic farce, but to silence anyone questioning the validity of woke concepts like trans ideology.

From 2020-2022 was the closest the west has come in a long time to a complete erasure of freedom of speech. Even today there are still countries and Europe and places like Canada or Australia that are charging forward with draconian speech laws. The phrase "radical speech" is starting to circulate within pro-censorship circles in reference to any platform where people are allowed to talk critically. What is radical speech? Basically, it's any discussion that runs contrary to the beliefs of the political left.

Open hatred of moderate or conservative ideals is perfectly acceptable, but don't ever shine a negative light on woke activism, or you might be a terrorist.

Riley Gaines has experienced this double standard first hand. She was even assaulted and taken hostage at an event in 2023 at San Francisco State University when leftists protester tried to trap her in a room and demanded she "pay them to let her go." Campus police allegedly witnessed the incident but charges were never filed and surveillance footage from the college was never released.

It's probably the last thing a champion female swimmer ever expects, but her head-on collision with the trans movement and the institutional conspiracy to push it on the public forced her to become a counter-culture voice of reason rather than just an athlete.

For years the independent media argued that no matter how much we expose the insanity of men posing as women to compete and dominate women's sports, nothing will really change until the real female athletes speak up and fight back. Riley Gaines and those like her represent that necessary rebellion and a desperately needed return to common sense and reason.

In a recent interview on the Joe Rogan Podcast, Gaines related some interesting information on the inner workings of the NCAA and the subversive schemes surrounding trans athletes. Not only were women participants essentially strong-armed by colleges and officials into quietly going along with the program, there was also a concerted propaganda effort. Competition ceremonies were rigged as vehicles for promoting trans athletes over everyone else.

The bottom line? The competitions didn't matter. The real women and their achievements didn't matter. The only thing that mattered to officials were the photo ops; dudes pretending to be chicks posing with awards for the gushing corporate media. The agenda took precedence.

Lia Thomas, formerly known as William Thomas, was more than an activist invading female sports, he was also apparently a science project fostered and protected by the athletic establishment. It's important to understand that the political left does not care about female athletes. They do not care about women's sports. They don't care about the integrity of the environments they co-opt. Their only goal is to identify viable platforms with social impact and take control of them. Women's sports are seen as a vehicle for public indoctrination, nothing more.

The reasons why they covet women's sports are varied, but a primary motive is the desire to assert the fallacy that men and women are "the same" psychologically as well as physically. They want the deconstruction of biological sex and identity as nothing more than "social constructs" subject to personal preference. If they can destroy what it means to be a man or a woman, they can destroy the very foundations of relationships, families and even procreation.

For now it seems as though the trans agenda is hitting a wall with much of the public aware of it and less afraid to criticize it. Social media companies might be able to silence some people, but they can't silence everyone. However, there is still a significant threat as the movement continues to target children through the public education system and women's sports are not out of the woods yet.

The ultimate solution is for women athletes around the world to organize and widely refuse to participate in any competitions in which biological men are allowed. The only way to save women's sports is for women to be willing to end them, at least until institutions that put doctrine ahead of logic are made irrelevant.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}

Uncategorized3 weeks ago

Uncategorized3 weeks ago

International5 days ago

International5 days ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

Uncategorized3 weeks ago

Uncategorized3 weeks ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

International5 days ago

International5 days ago

Uncategorized4 weeks ago

Uncategorized4 weeks ago

Uncategorized3 weeks ago

Uncategorized3 weeks ago