Uncategorized

Futures Slide As 10Y Yields Spike Back Over 4.80%

Futures Slide As 10Y Yields Spike Back Over 4.80%

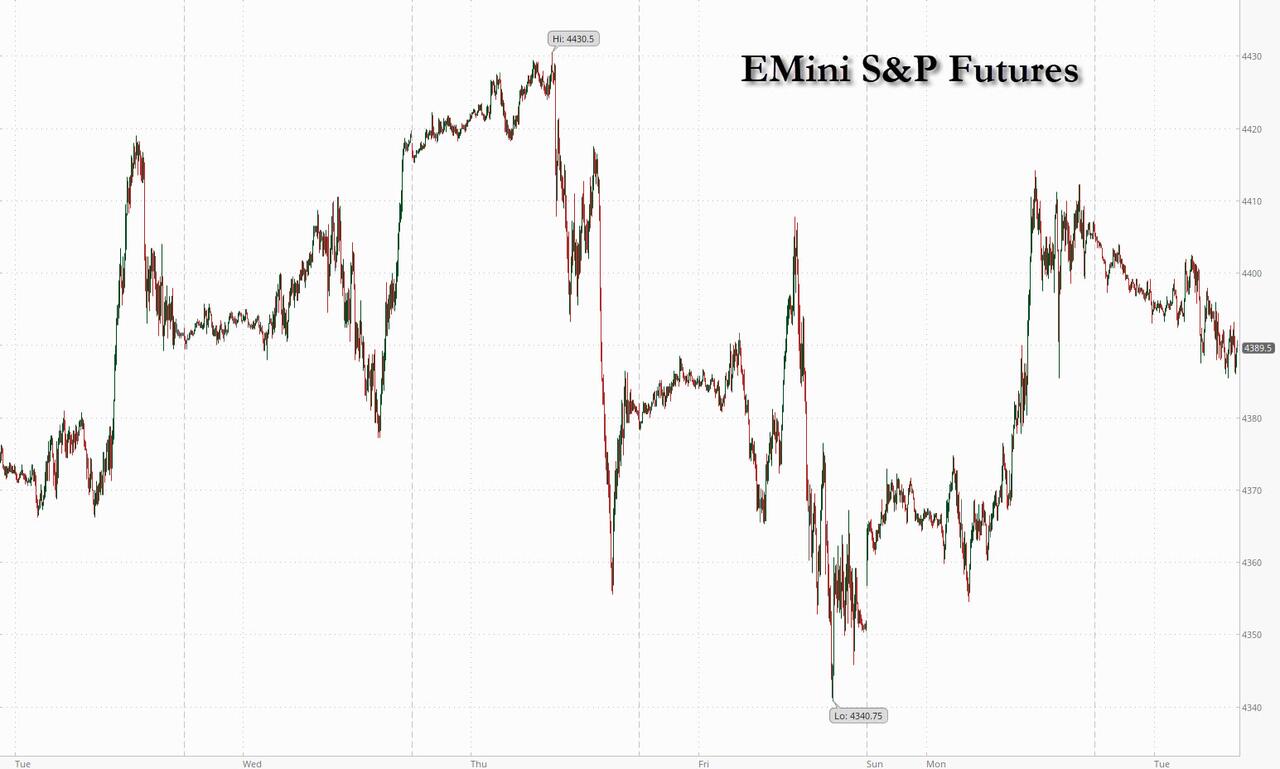

US index futures slid and global markets dropped as yields rose to session highs as complacent…

Share this:

US index futures slid and global markets dropped as yields rose to session highs as complacent investors once again pressed hopes that the Israel-Hamas war could be resolved diplomatically, after Joe Biden said he will travel to Israel to "show his support", which in turn shifted attention back to the untenable US fiscal situation which meant the blowout in yields would continue. At 8:15am S&P futures dropped 0.3% as traders assessed a flurry of major earnings. 10Y TSY yields rose to a high of 4.76%, spiking 20bps in the past two days and undoing much of the "flight to safety" after the Israel war. The dollar steadied, while the pound fell after cooling UK wage growth reduced pressure on the Bank of England to raise interest rates further. Israel’s shekel gained after weakening past 4 against the greenback on Monday. Brent crude oil traded near $90 a barrel.

Today we get the September retail sales and industrial production data before markets open, as well as reports on business inventories and cross-border investment. We also get a slew of Fed speakers including New York Fed President John Williams, Richmond Fed President Tom Barkin, Fed Governor Michelle Bowman and Minneapolis Fed President Neel Kashkari.

In premarket trading, Bank of America gained after its net interest income beat estimates even as its HTM losses soared by $26 billion to a record $132 billion. Goldman Sachs Group Inc. fluctuated as its results showed a beat in trading revenue and a drop in profit. Here are some other premarket movers:

- Johnson & Johnson jumped 1.6% after reporting sales for the third quarter that beat the average analyst estimate.

- Dollar Tree rises 2.6% as Goldman Sachs raises its recommendation on the retailer to buy from neutral, based on its strong earnings growth potential.

- Mondelez International shares rise 0.8%. The company’s lower exposure to the US market is probably a positive, BNP Paribas Exane writes in a note upgrading its rating on the packaged-food company to outperform.

- Viasat rose 5.54% as JPMorgan raised its recommendation to overweight from neutral. The broker said investors should be encouraged by the satellite company’s increased cost discipline.

- NetScout fell 23% as the cybersecurity company cut its adjusted earnings per share guidance for the full year. The guidance also missed the average analyst estimate.

The market mood was largely set by news that JOe Biden is set to travel to Israel Wednesday, aiming to show solidarity with the US’s closest ally in the Middle East and prevent the conflict from engulfing the wider region. He’ll then be in Jordan for talks with King Abdullah II and Egyptian and Palestinian Authority leaders.

“Markets fear a ground offensive by Israel that could ignite a larger and more complicated regional conflict that risks regional supply chains, energy output, economic growth and financial stability,” said Kyle Rodda, senior market analyst at Capital.com. “The presence of President Biden in the region potentially lowers the odds of such an offensive in the coming days, providing markets with some breathing room, if only for a small window.”

Meanwhile, investors are closely assessing the health of this batch of corporate results, after Wall Street strategists warned that the outlook for earnings is weakening. An update is also due Tuesday from United Airlines Holdings Inc. before Netflix Inc. and Tesla Inc. kick off tech-related earnings on Wednesday.

On top of geopolitics and earnings, Bloomberg notes that traders are tracking comments from a slew of Federal Reserve speakers this week before a blackout period in the lead-up to the central bank’s November rate-setting meeting. Philadelphia Fed President Patrick Harker on Monday repeated comments he made last week asserting the central bank can hold its benchmark rate steady as long as there is not a sharp turn in the economic data.

Pessimism around the economic outlook is driving investors to cash, according to BofA’s global fund manager survey. The broadest measure of sentiment — based on cash positions, equity allocation and economic predictions — fell in the October poll after showing an improvement in the summer months, BofA strategists led by Michael Hartnett wrote in a note. Cash levels as a percentage of assets under management have climbed above 5%.

A net 50% of investors in the BofA survey expect a weaker global economy over the next 12 months, with more concerned about a hard landing than previously. At the same time, the soft landing of a “Goldilocks” scenario remains the base case. Most surveyed remain convinced the Fed has finished its rate-hiking cycle.

European stocks opened higher but then traded lower as markets awaited President Biden’s arrival in Israel. The Stoxx 600 is down 0.4% after fluctuating during the trading session. Ericsson AB plunged more than 9% after the Swedish 5G-equipment maker warned of persisting weak demand. Rolls Royce Holdings Plc rose after the jet engine maker announced plans to cut jobs and streamline its business. Poland’s stocks and currency extended gains following Sunday’s elections, which gave pro-European Union parties a majority in parliament. Here are some of the most notable European movers:

- Rolls-Royce rises as much as 2.4%, extending this year’s continent-beating rally, as the British engineer announces plans to cut as many as 2,500 jobs

- Umicore jumps as much as 16%, the most in more than a year, after the governments of Canada and its largest province, Ontario, said they would provide the company subsidies to build a large plant

- St James’s Place shares rally, recovering from an initial drop after the UK wealth manager said it sees a hit to underlying cash from its revised charging structure

- Chemring rises as much as 6%, the steepest advance since Aug. 1, after the UK defense company received most of the necessary approvals from the US Department of Defense on certain countermeasure deliveries

- XPS Pensions rises as much as 11%, hitting a record high, after saying it expects to deliver results ahead of previous expectations. Canaccord lifts its EPS estimates and price target following Tuesday’s update

- Unieuro rises as much as 7.2%, the most intraday since June 2022, after the Italian consumer electronics chain agreed to buy Covercare

- EQT falls as much as 7.9% after the Swedish private equity firm reported third-quarter sales and revenues. The group said fundraising is taking longer than before, which Citi flags as a key negative

- Ericsson shares fall as much as 9.5% on Tuesday to the lowest level since 2017, after the telecom equipment maker gave a tepid profitability outlook for the fourth quarter and scrapped its 2024 Ebita margin target

- Lonza Group shares slump as much as 12%, after the Swiss supplier for pharmaceutical and nutrition companies warned on a hit to 2024 earnings

- Munters drops as much as 6.5%, hitting the lowest in three months, as Nordea downgrades its rating on the Swedish industrial ventilation and climate systems group to hold

- Bellway shares fall as much as 4.2% after the housebuilder lowered guidance for housing completions in fiscal 2024, missing estimates

Earlier in the session, Asian stocks advanced, halting a two-day selloff, as technology stocks rallied amid easing concerns over a wider conflict in the Middle East. The MSCI Asia Pacific Index climbed as much as 0.8%, with chipmakers Taiwan Semiconductor and Samsung the biggest boosts. Benchmarks in South Korea, and the Philippines were among the largest gainers amid broad regional gains.

- Stocks climbed in Hong Kong while a key measure of mainland-listed stocks edged higher after China said it would tighten curbs on short-selling activities. Investors await GDP data Wednesday that is expected to show continued weakness in the economy.

- Japan's Nikkei 225 was boosted at the open and briefly climbed above 32,000 although has since pulled back from intraday highs and proceeded to oscillate around the key aforementioned level.

- Australia's ASX 200 was led by outperformance in tech and telecoms, while mining names also benefitted following Rio Tinto’s quarterly update which showed an increase in iron ore shipments despite a decline in output.

- Indian stock rose, snapping a three-day losing streak, after the nation’s largest private lender posted net income that topped estimates. The S&P BSE Sensex closed 0.4% higher to 66,428.09 in Mumbai, while the NSE Nifty 50 Index rose by a similar magnitude. Local shares tracked gains in Asian equities as technology stocks rallied amid easing concerns over a wider conflict in the Middle East.

In FX, the Bloomberg Dollar Spot Index rose 0.3% as markets weighed ongoing diplomatic efforts to contain an escalation in the Israel-Hamas war; the dollar gained against all Group-of-10 peers bar the Australian dollar

- The yen briefly spiked after a report that the Bank of Japan is likely to discuss raising its inflation projections for 2023 and 2024 fiscal years at its policy meeting later this month.

- AUD/USD rose as much as 0.4% to 0.6367 after RBA minutes indicated the central bank considered hiking rates again

- GBP/USD fell as much as 0.6% to 1.2150 after cooling UK wage growth data bolstered the case for the Bank of England to keep rates on hold next month

- NZD/USD slumped as much as 0.6%, leading Group-of-10 declines against the dollar, after New Zealand’s inflation level slowed more than expected in the third quarter

In Rates, treasuries resumed their selloff on Tuesday, with futures near session lows as US trading day begins after sliding during Asia session and London morning. Weakness continues to be led by long-end and intermediates, steepening the curve. US yields are cheaper by more than 6bp at long end, steepening 2s10s, 5s30s curves by ~4bp and ~2bp on the day; 10-year around 4.80% is cheaper by ~10bp vs Monday close with bunds and gilts outperforming by 1bp and 4bp in the sector. Gilts outperform their German counterparts after UK wage growth eased in August. UK two-year yields are down 2bps.

In commodities, Brent futures rise 0.5% to trade near $90.10 and spot gold adds 0.2% to around $1,923.

Bitcoin traded just above $28,000; Israel ordered a freeze on some crypto accounts in a bid to block funding for Hamas with about 100 accounts on Binance closed after appeals for donations appeared on social media, according to FT.

To the day ahead, and today’s data releases include US retail sales, industrial production and capacity utilisation for September, along with the NAHB’s housing market index for October. Elsewhere, we’ll get Canada’s CPI for September and the German ZEW survey for October. From central banks, we’ll hear from the Fed’s Williams, Bowman, Barkin and Kashkari, ECB Vice President de Guindos, the ECB’s Knot, Centeno, Holzmann and Nagel, and the BoE’s Dhingra. Finally, today’s earnings releases include Bank of America, Goldman Sachs, United Airlines, and Johnson & Johnson.

Market Snapshot

- S&P 500 futures little changed at 4,396.75

- MXAP up 0.7% to 156.62

- MXAPJ up 0.5% to 491.64

- Nikkei up 1.2% to 32,040.29

- Topix up 0.8% to 2,292.08

- Hang Seng Index up 0.8% to 17,773.34

- Shanghai Composite up 0.3% to 3,083.50

- Sensex up 0.4% to 66,410.45

- Australia S&P/ASX 200 up 0.4% to 7,056.09

- Kospi up 1.0% to 2,460.17

- STOXX Europe 600 little changed at 450.37

- German 10Y yield little changed at 2.79%

- Euro down 0.2% to $1.0539

- Brent Futures little changed at $89.63/bbl

- Gold spot down 0.0% to $1,919.52

- U.S. Dollar Index up 0.18% to 106.43

Top Overnight News

- The weak outcome of Japan’s 20-year bond auction is pointing to a lack of demand from domestic banks and life insurers. The ¥1.2 trillion ($8 billion) sale of sovereign debt Tuesday indicated poor investor appetite by three major measures, including the bid-cover ratio, amid expectations of higher yields at home and abroad. Japanese major banks and regional lenders have dumped super-long Japanese government bonds for nine straight months through August. BBG

- China has told state-owned banks to roll over existing local government debt with longer-term loans at lower interest rates, two sources with knowledge of the matter said, as part of Beijing's efforts to reduce debt risks in a faltering economy. RTRS

- Chinese civil servants and employees of state-linked enterprises are facing tighter constraints on private travel abroad and scrutiny of their foreign connections, according to official notices and more than a dozen people familiar with the matter, as Beijing wages a campaign against foreign influence. RTRS

- The clock is ticking for Country Garden to avoid its first-ever public dollar-bond default. The Chinese builder missed the original deadline for the $15.4 million coupon on the note last month, and the grace period ends Oct. 17-18. BBG

- Vladimir Putin arrived in Beijing as China kicks off its Belt and Road Forum. Xi Jinping is set to meet Putin tomorrow just as the US presses China to help it reduce tensions in the Middle East. The ties between the two leaders face heightened scrutiny. BBG

- President Biden is expected to visit Israel on Wednesday as pressure mounted to provide safety and aid to hundreds of thousands of Palestinians in Gaza who have fled their homes before a likely Israeli invasion. Officials have warned a humanitarian crisis there will worsen without immediate help. NYT

- US retail sales probably rose 0.3% in September, half of August’s advance. There’s limited scope for an upside surprise, Bloomberg Economics said. Looking ahead, holiday season spending is expected to grow 14% this year, a Deloitte survey showed, with middle-income consumers impacted by college debt and low wage growth. BBG

- Jim Jordan closed in on the votes he needs to be the next House speaker, but a band of Republican holdouts continues to threaten his bid. The hardline conservative from Ohio plans to proceed with a vote as early as noon today and is prepared for multiple ballots if necessary, a person familiar said. BBG

- The boom in private credit, a fast-growing $1.5 trillion corner of Wall Street born during an era of ultralow interest rates, is starting to show cracks. High borrowing costs, an economic slowdown and contractions in credit markets are testing private credit as never before. Many borrowers paying floating rates that fluctuate with benchmark interest rates are having a difficult time keeping up with rising debt payments, resulting in defaulting loans and, in some cases, bankruptcies. WSJ

- The push by employers to get American workers back into the office appears to be working. Fewer than 26% of US households still have someone working remotely at least one day a week, a sharp decline from the early-2021 peak of 37%, according to the two latest Census Bureau Household Pulse Surveys. Only seven states plus Washington, DC, have a remote-work rate above 33%, the data shows, down from 31 states and DC mid-pandemic. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive following the gains across global counterparts which unwound the recent geopolitical hedging and with President Biden to travel to the Middle East on Wednesday, although the upside was capped as risks of a widening conflict in the Middle East conflict lingered amid threats from Iran. ASX 200 was led by outperformance in tech and telecoms, while mining names also benefitted following Rio Tinto’s uarterly update which showed an increase in iron ore shipments despite a decline in output. Nikkei 225 was boosted at the open and briefly climbed above 32,000 although has since pulled back from intraday highs and proceeded to oscillate around the key aforementioned level. Hang Seng and Shanghai Comp. were both positive although the mainland lagged amid developer debt concerns with Country Garden on the cusp of a default as the grace period for a USD 15mln coupon payment expires today and with an Evergrande unit to seek creditor approval to extend yuan-denominated bonds.

Top Asian News

- RBA Minutes from the October meeting stated the board considered raising rates by 25bps or holding steady and agreed the case for holding steady was the stronger one, while members noted data on inflation, jobs and updated forecasts would be available at the November meeting. RBA Minutes stated members acknowledged upside risks to inflation were a significant concern and said progress in lowering service sector inflation was slow, while the Board had a low tolerance for a slower return of inflation to the target and it stated that further tightening may be required if inflation is more persistent than expected.

- Japan's Rengo (labour organisation) intends to ask for more than a 5% wage hike in the spring 2024 wage discussions, via NHK; is planning to ask for a "more than 3%" base wage hike in Spring 2024 wage discussions.

- PBoC has instructed state banks are to roll over local govt loans with longer term and lower rates; PBoC is to set up an emergency liquidity tool with banks; loans made via tool should be repaid in two years, according to Reuters sources. New interest rates should not be lower than China's Treasury bonds, with terms no longer than 10 years.

- BoJ reportedly mulls raising its FY23 price view closer to 3%; mulls raising FY24 price view to 2% or above; inflation outlook is said to keep FY25 around 1.6%, according to Bloomberg sources.

European bourses are near the unchanged mark with performance mixed as some regions manage to eke out mild gains while others reside slightly in the red as geopolitical tensions continue to dominate newsflow, Euro Stoxx 50 -0.3%. After the cash open, a bout of pressure occurred in proximity to remarks from the Iranian Supreme Leader Khamenei, commentary which aired just prior to the ZEW release which sparked a recovery from the rhetoric-driven session lows in European equity benchmarks. Sectors are mixed with defensively inclined components such as Real Estate, Health Care and Utilities outperforming while Basic Resources is the laggard alongside underlying benchmarks and after Rio Tinto's update.

Top European News

- Poland Election Final Results: PiS 35.38%, Civic Coalition (KO) 30.7%, Third Way 14.4%, New Left 8.6%, far-right Confederation 7.16%. As a reminder, the first exit poll had PiS with 40.36%, Civic Coalition with 26.4%, Third Way 13.6%, Left 8.3% & far-right Confederation 7.4%.

- BoE's Dhingra says average weekly earnings data appear to give a more inflated picture of the wage outlook vs other measures; she expects some letting-up of wage growth. Says the labour market is really loosening and does not see further wage growth momentum. Should see some relenting of domestic inflation pressures.

FX

- Hawkish RBA minutes underpin Aussie as AUD/USD pivots 0.6350 and AUD/NZD approaches 1.0800 from just shy of 1.0700, Kiwi undermined by softer than forecast NZ Q3 CPI metrics, with NZD/USD under 0.5900.

- Pound soft in line with headline UK average earnings vs consensus and BoE's Dhingra chiming with others that the weekly numbers inflate the real picture, Cable tests 1.2150 to the downside from 1.2200+ at one stage.

- Euro supported by 1.0500 expiries and better than expected ZEW survey, Yen initially reliant on 150.00 expiry interest as DXY forms base on 106.000 handle within 106.200-490 range.

- Most recently, USD/JPY has been hit by a BoJ sources piece around the inflation outlook which pushed it down to a brief 148.75 trough, a move which has since partially retraced and as such USD/JPY is currently around 149.40.

- Loonie sits between 1.3650-00 band awaiting Canadian inflation data.

- PBoC set USD/CNY mid-point at 7.1796 vs exp. 7.3038 (prev. 7.1798).

Fixed Income

- Gilts bolstered between 93.91-41 parameters by benign UK wage data, dovish comments from BoE's Dhingra and IFS predicting PSBR undershoot.

- Bunds lag within 128.71-129.14 range after better than forecast German ZEW survey and irrespective of solid Schatz sale.

- T-notes rooted towards base of 106-29/107-08 band ahead of US retail sales, ip and quartet of Fed orators.

Commodities

- Crude benchmarks are modestly firmer on the session but price action has been choppy within relatively tight ranges thus far with geopolitical updates driving action thus far.

- WTI & Brent Dec futures currently post gains of circa. 0.5% on the session, at the top-end of respective USD ~1.00/bbl parameters.

- Spot gold is essentially flat, holding just above the USD 1920/oz figure and as such well within Monday's USD 1908-32 boundaries.

- Base metals are pressured given the cautious mood and as the USD benefits from this, LME Copper towards USD 7.9k/T, pressure perhaps also emanating from the latest Rio Tinto update.

- Commerzbank now sees gold price around USD 1,900/oz at the end of December (prev. USD 2,000/oz); 2024 forecast remains unchanged at USD 2,100/oz.

- Chevron (CVX) Australia spokesperson said they are continuing work to conclude the drafting of proposed enterprise agreements for Gorgon and Wheatstone facilities based on clarification provided by the Fair Work Commission, according to Reuters.

- US State Department said it welcomes the announcement by Maduro representatives and the unitary platform to resume negotiations, while it added the US will continue efforts to unite the international community to support the Venezuelan-led negotiation process.

Geopolitics

- Israeli PM Netanyahu spoke With Russian President Putin and made it clear that Israel will not stop the Gaza operations until Hamas is destroyed, according to Reuters. It was separately reported that Russian President Putin told Israeli PM Netanyahu that Russia is ready to help end the confrontation in the region and resolve it peacefully, according to TASS

- US Secretary of State Blinken confirmed US President Biden will travel to Israel on Wednesday and will reaffirm US solidarity with Israel, while he added that Biden will make it clear that Israel has the right to defend itself and will underscore their message to any actor trying to take advantage of the crisis to attack Israel. Furthermore, Blinken said US and Israel agreed to develop a plan that will allow aid to reach Gaza civilians and noted it is critical that aid begin to flow into Gaza as soon as possible.

- White House's Kirby said US President Biden expects to hear from Israeli officials about what they need, while he added that President Biden will then travel to Amman to meet with Jordan's King Abdullah, Egyptian President El-Sisi and Palestinian Authority President Abbas.

- US Central Command head General Kurilla flew to Israel for talks with military leaders with the visit aiming to ensure Israel has what it needs to defend itself and is focused on avoiding expansion of the conflict.

- Russia's draft UN Security Council resolution on Israel and Gaza failed to receive the minimum nine votes needed, while the Russian UN envoy said the UN Security Council is hostage to Western countries and the UN vote shows who is in favour of a truce in Gaza and delivery of humanitarian aid. Furthermore, the US envoy to the UN accused Russia of giving cover to a terrorist group that brutalises civilians by not condemning Hamas in a draft resolution, according to Reuters.

- US Defense Secretary Austin has put in "be ready to deploy" orders for a select number of American troops should Israel need them, while a separate report stated that about 2,000 troops were told to prepare for deployment.

- The delay in the Israeli ground attack on Gaza is reportedly due to a growing concern that Hezbollah is waiting for the moment that most IDF forces are committed to Gaza to open a full front with the IDF in the north, according to Jerusalem Post sources.

- Russian President Putin said China's proposal for peace talks with Ukraine could become a realistic basis for a peace agreement, according to an interview with Chinese television. However, he also accused Ukraine of not allowing peace negotiations, according to DPA.

- AJA Breaking reports, citing Israeli Radio, that the "Israeli army is intensively bombing many targets in southern Lebanon after bombing the town of Metulla" & "Israeli bombing targets the road between the towns of Kafr Kila and Al-Adisa in the eastern sector of southern Lebanon"

- Iranian Supreme Leader Khamenei says if Israel's crimes continue then no one can stop "Muslims around the world and resistance forces". Gaza bombardments must stop immediately.

- Lebanese Foreign Minister says Israeli attack in south Lebanon pours "oil on fire" and threaten to ignite a front.

- Iran Guard's Deputy Chief says "another shockwave" is on the way if Israel does not end atrocities in Gaza, according to Fars News.

Central Bank speakers

- 08:00: Fed’s Williams Moderates Discussion at Economic Club of NY

- 09:20: Fed’s Bowman Speaks on Innovation in Payments

- 10:45: Fed’s Barkin Speaks on the Economic Outlook

- 17:00: Fed’s Kashkari Participates in a Moderated Discussion

US Event Calendar

- 08:30: Sept. Retail Sales Advance 0.7% MoM, est. 0.3%, prior 0.6%

- 08:30: Sept. Retail Sales Ex Auto 0.6%, est. 0.2%, prior 0.6%

- 08:30: Sept. Retail Sales Ex Auto and Gas 0.6%, est. 0.1%, prior 0.2%

- 08:30: Sept. Retail Sales Control Group 0.6%, est. 0.1%, prior 0.1%

- 09:15: Sept. Industrial Production MoM, est. 0%, prior 0.4%

- 10:00: Aug. Business Inventories, est. 0.3%, prior 0%

- 10:00: Oct. NAHB Housing Market Index, est. 44, prior 45

- 16:00: Aug. Total Net TIC Flows, prior $140.6b

DB's Jim Reid concludes the overnight wrap

Markets seems to be taking the geopolitical risk session by session at the moment, rather than having any strategic sense of where things are heading. It feels like we're in a very dangerous and delicate holding pattern for now, but with no major developments since the Israeli evacuation notice to Gaza residents on Friday, markets have taken off their weekend hedges over the last 24 hours or so.

Headlining this was the +1.06% advance in the S&P 500, which represents the best start to a week since February. Meanwhile the whipsaw in bonds continued with 10yr Treasury yields up +9.4bps on the day to 4.71%, with another +3.8bps move overnight to 4.74%. This time yesterday we highlighted reports that US President Biden was considering a trip to Israel, which was generally taken as a positive sign that the US is working to prevent an escalation, or that one won't happen while he's in the region. But that visit from Biden has since been confirmed by US Secretary of State Blinken overnight, and is set to take place tomorrow. Yesterday’s market moves showed that assets most sensitive to an escalation were reacting in a positive direction. For instance, Brent crude oil prices were down -1.36% to $89.65/bbl, Israel’s TA-35 equity index was up +2.46%, and the US Dollar index weakened by -0.38% as investors took out some of the recent geopolitical risk premium. The exception was Israel’s shekel, which weakened to an 8-year low against the dollar (-0.90%).

The bond sell-off was matched by growing anticipation that the Fed might deliver another rate hike in 2023 after all, with pricing for a hike by December up from 32% at the close last week, to 37% yesterday. In turn, yields on 2yr Treasuries were up +4.3bps to 5.10%, whilst the 30yr yield was up +9.7bps to 4.85%. The long-end sell off was shared across real yields and breakevens, with the 10yr real yield up +4.5bps to 2.32%, and the 30yr real yield was up +5.3bps to 2.42%. US retail sales and industrial production today will be a chance for the macro to compete with the geopolitics again for bonds.

It was much the same story in Europe, with yields rising across most of the continent. Those on UK gilts saw the biggest increase, with the 10yr yield up +9.5bps to 4.48%, which followed comments from BoE Chief economist Pill that there was still “some work to do” for the Monetary Policy Committee to achieve their inflation target. Elsewhere in Europe, yields on 10yr bunds (+4.7bps) and OATs (+3.8bps) also moved higher, but BTPs (-1.0bps) were the exception in spite of a government announcement of a new €24bn budget law that includes tax cuts and public sector wage rises. So risk-on offset the fiscal implications.

Whilst bonds were selling off, equities saw a much better performance with all 24 industry groups in the S&P 500 (+1.06%) rising on the day. Small-cap stocks were one of the strongest performers as the Russell 2000 rose +1.59%. Meanwhile in Europe, the STOXX 600 (+0.23%) also recovered from Friday’s losses, and Polish equities saw a major outperformance following the election on Sunday which will likely yield a pro-EU government under the leadership of former Polish PM and European Council President Donald Tusk. That rally included the WIG20 index (+5.31%), which had its best day since February 2022, whilst the Polish Zloty (+1.82%) had its best day against the Euro since March 2022.

In other news, the sharp run-up in European natural gas prices subsided yesterday, with a -12.2% decline to €48.6/MWh. That’s been h elped by the absence of an escalation in the Middle East, as well as the prospect of milder weather after the present colder period passes. European gas storage is now some way above its levels at the same point in recent years, with storage facilities 97.95% full as of Sunday. There was also a decent move lower in US natural gas futures (-3.92%) as well yesterday, which saw their biggest decline in nearly a month.

Overnight in Asia, those gains for equities have continued against the backdrop of ongoing diplomatic efforts. All the major indices have advanced, including the KOSPI (+1.16%), the Nikkei (+1.08%), the Hang Seng (+0.70%), the CSI 300 (+0.46%) and the Shanghai Comp (+0.26%). Overnight, we’ve also seen a selloff among Australian government bonds following the release of the RBA’s minutes from the October meeting. That said they considered raising rates this month, and also that “the board has a low tolerance for a slower return of inflation to target than currently expected.” In light of that, yields on 10yr Australian government bonds are up +9.2bps, and the Australian Dollar is the best-performing G10 currency overnight. Looking forward, US equity futures are slightly lower this morning, with those on the S&P 500 down -0.12% ahead of several earnings releases this week.

There wasn’t much in the way of data releases yesterday, although we did get the Empire State manufacturing survey for October in the US. That fell back into negative territory at -4.6 (vs. -6.0 expected), and the measure of unfilled orders (-19.1) fell to its lowest level since May 2020 during the initial wave of the pandemic. There were also some more positive signals on the inflation side, with the 6-months ahead prices received indicator down to a 3-year low of 16.0.

Looking forward, we could get some more developments on the election of a new Speaker of the US House of Representatives today. The Republicans have nominated Rep. Jim Jordan, and yesterday he appeared to receive the backing of some key Republicans that had been opposed to his nomination. CNN reported yesterday that Jordan said he would force a floor vote at noon today for the speaker election, so that’s one to look out for. Should Jordan be confirmed as Speaker, investors will be watching what this means for fiscal bargaining in Congress ahead of the next government shutdown deadline in mid-November .

To the day ahead, and today’s data releases include US retail sales, industrial production and capacity utilisation for September, along with the NAHB’s housing market index for October. Elsewhere, we’ll get Canada’s CPI for September and the German ZEW survey for October. From central banks, we’ll hear from the Fed’s Williams, Bowman, Barkin and Kashkari, ECB Vice President de Guindos, the ECB’s Knot, Centeno, Holzmann and Nagel, and the BoE’s Dhingra. Finally, today’s earnings releases include Bank of America, Goldman Sachs, United Airlines, and Johnson & Johnson.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire