Futures Jump On Profit Optimism As Oil Tops $85; Bitcoin Nears $60,000

Futures Jump On Profit Optimism As Oil Tops $85; Bitcoin Nears $60,000

One day after the S&P posted its biggest one-day surge since March, index futures extended this week’s gains, helped by a stellar bank earnings, while the latest…

Futures Jump On Profit Optimism As Oil Tops $85; Bitcoin Nears $60,000

One day after the S&P posted its biggest one-day surge since March, index futures extended this week’s gains, helped by a stellar bank earnings, while the latest labor market data and inflation eased stagflation fears for the time being. . The 10-year Treasury yield rose and the dollar was steady. Goldman Sachs reports on Friday. At 715 a.m. ET, Dow e-minis were up 147 points, or 0.42%, S&P 500 e-minis were up 16.5 points, or 0.37%, and Nasdaq 100 e-minis were up 42.75 points, or 0.28%.

Oil futures topped $85/bbl, jumping to their highest in three years amid an energy crunch that’s stoking inflationary pressures and prices for raw materials. A gauge of six industrial metals hit a record high on the London Metal Exchange. Energy firms including Chevron and Exxon gained about half a percent each, tracking Brent crude prices that scaled the 3 year high.

Solid earnings in the reporting season are tempering fears that rising costs and supply-chain snarls will hit corporate balance sheets and growth. At the same time, the wider debate about whether a stagflation-like backdrop looms remains unresolved.

“We don’t sign up to the stagflation narrative that is doing the rounds,” said Hugh Gimber, global strategist at the perpetually optimistic J.P. Morgan Asset Management. “The economy is being supported by robust consumer balance sheets, rebounding business investment and a healthy labor market.”

“After a choppy start to the week, equity markets appear to be leaning towards a narrative that companies can continue to grow profits, despite the combined pressures of higher energy prices and supply chain disruptions,” said Michael Hewson, chief market analyst at CMC Markets in London.

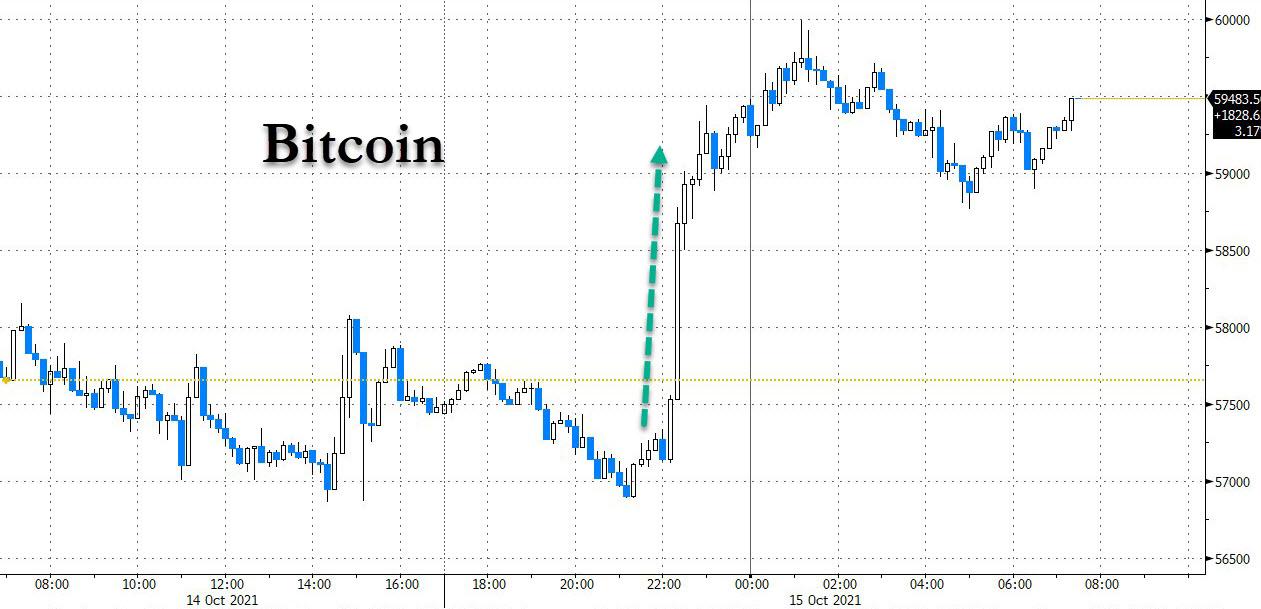

Bitcoin and the crypto sector jumped after Bloomberg reported late on Thursday that the Securities and Exchange Commission is poised to allow the first U.S. Bitcoin futures exchange-traded fund to begin trading in a watershed moment for the cryptocurrency industry. Bitcoin traded off session highs having tested $60k during Asian hours, but will likely rise to new all time highs shortly.

Also overnight, Joe Biden signed a bill providing a short-term increase in the debt limit, averting the imminent threat of a financial calamity. But it only allows the Treasury Department to meets its financial obligations until roughly Dec. 3, so the can has been kicked for less than two months - brace for more bitter partisan battles in the coming weeks.

This week’s move into rate-sensitive FAAMG growth names looked set to continue, with their shares inching up. Moderna rose 3.0% after a U.S. FDA panel voted to recommend booster shots of its COVID-19 vaccine for Americans aged 65 and older and high-risk people. Western Digital slipped 2.5% as Goldman Sachs downgraded the storage hardware maker’s stock to “neutral” from “buy”. Here are some of the key premarket movers on Friday morning:

Virgin Galactic (SPCE US) shares slump as much as 23% in U.S. premarket trading as the firm is pushing the start of commercial flights further into next year after rescheduling a test flight, disappointing investors with the unexpected delay to its space tourism business plans

Cryptocurrency-exposed stocks rise in U.S. premarket trading after a report that the Securities and Exchange Commission is poised to allow the first U.S. Bitcoin futures exchange-traded fund to begin trading. Bit Digital (BTBT US) +6.7%, Riot Blockchain (RIOT US) +4.6%, Marathon Digital (MARA US) +3.6%

Alcoa (AA US) shares jump 5.6% in thin volumes after co. reported profits that beat the average analyst estimate and said it will be paying a dividend to its shareholders

Moderna (MRNA US) extends Thursday’s gains; Piper Sandler recommendation on Moderna Inc. to overweight from neutral, a day after co.’s Covid-19 booster got FDA nod for use in older, high-risk people

Duck Creek Technologies (DCT US) shares fell 12% in Thursday postmarket trading after the software company projected 2022 revenue that fell short of the average analyst estimate

23andMe Holdings (ME US) soared 14% in Thursday postmarket trading after EMJ Capital founder Eric Jackson called the genetics testing company “the next Roku” on CNBC

Corsair Gaming (CRSR US) shares fell 3.7% in post-market trading after it cut its net revenue forecast for the full year

Early on Friday, China's PBOC broke its silence on Evergrande, saying risks to the financial system are controllable and unlikely to spread. Authorities and local governments are resolving the situation, central bank official Zou Lan said. The bank has asked lenders to keep credit to the real estate sector stable and orderly.

In Europe, gains for banks, travel companies and carmakers outweighed losses for utilities and telecommunications industries, pushing the Stoxx Europe 600 Index up 0.3%. Telefonica fell 3.3%, the most in more than four months, after Barclays cut the Spanish company to underweight. Temenos and Pearson both slumped more than 10% after their business updates disappointed investors. Here are some of the biggest European movers today:

Devoteam shares rise as much as 25% after its controlling shareholder, Castillon, increased its stake in the IT consulting group to 85% and launched an offer for the remaining capital.

QinetiQ rises as much as 5.4% following a plunge in the defense tech company’s stock on Thursday. Investec upgraded its recommendation to buy and Berenberg said the shares now look oversold.

Hugo Boss climbs as much as 4.4% to the highest level since September 2019 after the German apparel maker reported 3Q results that exceeded expectations. Jefferies (hold) noted the FY guidance hike also was bigger than expected.

Mediclinic rises as much as 7.7% to highest since May 26 after 1H results, which Morgan Stanley says showed strong underlying operating performance with “solid metrics.”

Temenos sinks as much as 14% after the company delivered a “mixed bag” with its 3Q results, according to Baader (sell). Weakness in Europe raises questions about the firm’s outlook for a recovery in the region, the broker said.

Pearson declines as much as 12%, with analysts flagging weaker trading in its U.S. higher education courseware business in its in-line results.

Earlier in the session, Asian stocks headed for their best week in more than a month amid a list of positive factors including robust U.S. earnings, strong results at Taiwan Semiconductor Manufacturing Co. and easing home-loan restrictions in China. The MSCI Asia Pacific Index gained as much as 1.3%, pushing its advance this week to more than 1.5%, the most since the period ended Sept. 3. Technology shares provided much of the boost after chip giant TSMC announced fourth-quarter guidance that beat analysts’ expectations and said it will build a fabrication facility for specialty chips in Japan.

Shares in China rose as people familiar with the matter said the nation loosened restrictions on home loans at some of its largest banks. Conditions are good for tech and growth shares now long-term U.S. yields have fallen following inflation data this week, Shogo Maekawa, a strategist at JPMorgan Asset Management in Tokyo. “If data going forward are able to provide an impression that demand is strong too -- on top of a sense of relief from easing supply chain worries -- it’ll be a reason for share prices to take another leap higher.” Asia’s benchmark equity gauge is still 10% below its record-high set in February, as analysts stay on the lookout for higher bond yields and the impact of supply-chain issues on profit margins.

Japanese stocks rose, with the Topix halting a three-week losing streak, after Wall Street rallied on robust corporate earnings. The Topix rose 1.9% to close at 2,023.93, while the Nikkei 225 advanced 1.8% to 29,068.63. Keyence Corp. contributed the most to the Topix’s gain, increasing 3.7%. Out of 2,180 shares in the index, 1,986 rose and 155 fell, while 39 were unchanged. For the week, the Topix climbed 3.2% and the Nikkei added 3.6%. Semiconductor equipment and material makers rose after TSMC said it will build a fabrication facility for specialty chips in Japan and plans to begin production there in late 2024. U.S. index futures held gains during Asia trading hours. The contracts climbed overnight after a report showed applications for state unemployment benefits fell last week to the lowest since March 2020. “U.S. initial jobless claims fell sharply, and have returned to levels seen before the spread of the coronavirus,” said Nobuhiko Kuramochi, a market strategist at Mizuho Securities in Tokyo. “The fact that more people are returning to their jobs will help ease supply chain problems caused by the lack of workers.”

Australian stocks also advanced, posting a second week of gains. The S&P/ASX 200 index rose 0.7% to close at 7,362.00, with most sectors ending higher. The benchmark added 0.6% since Monday, climbing for a second week. Miners capped their best week since July 16 with a 3% advance. Hub24 jumped on Friday after Evans & Partners upgraded the stock to positive from neutral. Pendal Group tumbled after it reported net outflows for the fourth quarter of A$2.3 billion. In New Zealand, the S&P/NZX 50 index fell 0.3% to 13,012.19

In rates, the U.S. 10-year Treasury yield rose over 3bps to 1.54%. Treasuries traded heavy across long-end of the curve into early U.S. session amid earning-driven gains for U.S. stock futures. Yields are higher by more than 3bp across long-end of the curve, 10- year by 2.8bp at about 1.54%, paring its first weekly decline since August; weekly move has been led by gilts and euro-zone bonds, also under pressure Friday, with U.K. 10-year yields higher by 3.3bp. Today's bear-steepening move pares the weekly bull-flattening trend. U.S. session features a packed economic data slate and speeches by Fed’s Bullard and Williams.

In FX, the Bloomberg Dollar Spot Index was little changed even as the greenback weakened against most of its Group-of-10 peers; the euro hovered around $1.16 while European and U.S. yields rose, led by the long end. Norway’s krone led G-10 gains as oil jumped to $85 a barrel for the first time since late 2018 amid the global energy crunch; the currency rallied by as much as 0.6% to 8.4015 per dollar, the strongest level since June. New Zealand’s dollar advanced to a three-week high as bets on RBNZ’s tightening momentum build ahead of Monday’s inflation data; the currency is outperforming all G-10 peers this week. The yen dropped to a three-year low as rising equities in Asia damped demand for low-yielding haven assets. China’s offshore yuan advanced to its highest in four months while short-term borrowing costs eased after the central bank added enough medium-term funds into the financial system to maintain liquidity at existing levels.

In commodities, crude futures trade off best levels. WTI slips back below $82, Brent fades after testing $85. Spot gold slips back through Thursday’s lows near $1,786/oz. Base metals extend the week’s rally with LME nickel and zinc gaining over 2%.

Today's retail sales report, due at 08:30 a.m. ET, is expected to show retail sales fell in September amid continued shortages of motor vehicles and other goods. The data will come against the backdrop of climbing oil prices, labor shortages and supply chain disruptions, factors that have rattled investors and have led to recent choppiness in the market.

Looking at the day ahead now, and US data releases include September retail sales, the University of Michigan’s preliminary consumer sentiment index for October, and the Empire State manufacturing survey for October. Central bank speakers include the Fed’s Bullard and Williams, and earnings releases include Charles Schwab and Goldman Sachs.

Market Snapshot

S&P 500 futures up 0.3% to 4,443.75

STOXX Europe 600 up 0.4% to 467.66

German 10Y yield up 2.4 bps to -0.166%

Euro little changed at $1.1608

MXAP up 1.3% to 198.33

MXAPJ up 1.2% to 650.02

Nikkei up 1.8% to 29,068.63

Topix up 1.9% to 2,023.93

Hang Seng Index up 1.5% to 25,330.96

Shanghai Composite up 0.4% to 3,572.37

Sensex up 0.9% to 61,305.95

Australia S&P/ASX 200 up 0.7% to 7,361.98

Kospi up 0.9% to 3,015.06

Brent Futures up 1.0% to $84.83/bbl

Gold spot down 0.5% to $1,787.54

U.S. Dollar Index little changed at 93.92

Top Overnight News from Bloomberg

China’s central bank broke its silence on the crisis at China Evergrande Group, saying risks to the financial system stemming from the developer’s struggles are “controllable” and unlikely to spread

The ECB has a good track record when it comes to flexibly deploying its monetary instruments and will continue that approach even after the pandemic crisis, according to policy maker Pierre Wunsch

Italian Ministry of Economy and Finance says fourth issuance of BTP Futura to start on Nov. 8 until Nov. 12, according to a statement

The world’s largest digital currency rose about 3% to more than $59,000 on Friday -- taking this month’s rally to over 35% -- after Bloomberg News reported the U.S. Securities and Exchange Commission looks poised to allow the country’s first futures-based cryptocurrency ETF

Copper inventories available on the London Metal Exchange hit the lowest level since 1974, in a dramatic escalation of a squeeze on global supplies that’s sent spreads spiking and helped drive prices back above $10,000 a ton

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks traded higher amid tailwinds from the upbeat mood across global peers including the best day for the S&P 500 since March after strong US bank earnings, encouraging data and a decline in yields spurred risk appetite. The ASX 200 (+0.7%) was positive as the tech and mining sectors continued to spearhead the advances in the index in which the former took impetus from Wall St where the softer yield environment was conducive to the outperformance in tech, although mining giant Rio Tinto was among the laggards following weaker quarterly production results. The Nikkei 225 (+1.8%) was buoyed as exporters benefitted from the JPY-risk dynamic but with Fast Retailing failing to join in on the spoils despite an 88% jump in full-year net as its profit guidance underwhelmed with just 3% growth seen for the year ahead, while Taiwan's TAIEX (+2.2%) surged with the spotlight on TSMC earnings which reached a record high amid the chip crunch and with the Co. to also build a factory in Japan that could receive JPY 500bln of support from the Japanese government. The Hang Seng (+1.5%) and Shanghai Comp. (+0.4%) were initially indecisive amid the overhang from lingering developer default concerns although found some mild support from reports that China is to relax banks' mortgage limits through the rest of 2021. Focus was also on the PBoC which announced a CNY 500bln MLF operation, although this just matched the amount maturing this month and there are mixed views regarding prospects of a looming RRR cut with ANZ Bank's senior China strategist recently suggesting the potential for a 50bps cut in RRR or targeted MLF as early as today, although a recent poll showed analysts had pushed back their calls for a RRR cut from Q4 2021 to Q1 2022. Finally, 10yr JGBs marginally pulled back from this week’s advances after hitting resistance at the 151.50 level, with demand hampered amid the firm gains in Japanese stocks and the lack of BoJ purchases in the market today.

Top Asian News

Hong Kong Probes Going Concern Reporting of Evergrande

U.S. Futures Hold Gains as Oil Hits 3-Year High: Markets Wrap

Toyota Cuts November Outlook by 15% on Parts Shortage, Covid

Yango Group Wires Repayment Fund for Onshore Bond Due Oct. 22

Bourses in Europe have held onto the modest gains seen at the cash open (Euro Stoxx 50 +0.4%; Stoxx 600 +0.3%), but the region is off its best levels with the upside momentum somewhat faded heading into the US open, and amidst a lack of fresh newsflow. US equity futures have remained in positive territory, although the latest leg lower in bonds has further capped the tech-laden NQ (+0.2%), which underperforms vs the ES (+0.3%), YM (+0.3%) and RTY (+0.7%), with traders on the lookout for another set of earnings, headlined by Goldman Sachs at 12:25BST/07:25EDT. Back to Europe, bourses see broad-based gains, whilst sectors are mostly in the green with clear underperformance experienced in defensives, with Telecoms, Utilities, Healthcare and Staples at the foot of the bunch. On the flipside, Banks reap rewards from the uptick in yields, closely followed by Travel & Leisure, Autos & Parts and Retail. Renault (+4%) drives the gains in Autos after unveiling a prototype version of the Renault Master van that will go on sale next year. Travel & Leisure is bolstered by the ongoing reopening trade with potential tailwinds heading into the Christmas period. Retail meanwhile is boosted by Hugo Boss (+1.8%) topping forecasts and upgrading its guidance.

Top European News

Autumn Heat May Curb European Gas Demand, Prices Next Week

Bollore Looking for Buyers for Africa Logistics Ops: Le Monde

U.K. Offers Foreign Butchers Visas After 6,000 Pigs Culled

Europe’s Car-Sales Crash Points to Worse Year Than Poor 2020

In FX, the Greenback was already losing momentum after a relatively tame bounce on the back of Thursday’s upbeat US initial claims data, and the index failed to sustain its recovery to retest intraday highs or remain above 94.000 on a closing basis. However, the Buck did reclaim some significant and psychological levels against G10, EM currencies and Gold that was relishing the benign yield environment and the last DXY price was marginally better than the 21 DMA from an encouraging technical standpoint. Nevertheless, the Dollar remains weaker vs most majors and in need of further impetus that may come via retail sales, NY Fed manufacturing and/or preliminary Michigan Sentiment before the spotlight switches to today’s Fed speakers featuring arch hawk Bullard and the more neutral Williams.

GBP/NZD/NOK - Sterling has refuelled and recharged regardless of the ongoing UK-EU rift over NI Protocol, though perhaps in part due to the fact that concessions from Brussels are believed to have been greeted with welcome surprise by some UK Ministers. Cable has reclaimed 1.3700+ status, breached the 50 DMA (at 1.3716 today) and yesterday’s best to set a marginal new w-t-d peak around 1.3739, while Eur/Gbp is edging closer to 0.8450 having clearly overcome resistance at 1.1800 in the reciprocal cross. Similarly, the Kiwi continues to derive impetus from the softer Greenback and Aud/Nzd flows as Nzd/Usd extends beyond 0.7050 and the Antipodean cross inches nearer 1.0500 from 1.0600+ highs. Elsewhere, the Norwegian Crown is aiming to add 9.7500 to its list of achievements relative to the Euro with a boost from Brent topping Usd 85/brl at one stage and a wider trade surplus.

CAD - The Loonie is also profiting from oil as WTI crude rebounds through Usd 82 and pulling further away from 1.5 bn option expiry interest between 1.2415-00 in the process, with Usd/Cad towards the base of 1.2337-82 parameters.

EUR/AUD/CHF/SEK - All narrowly mixed and rangy vs the Greenback, or Euro in the case of the latter, as Eur/Usd continues to straddle 1.1600, Aud/Usd churn on the 0.7400 handle, the Franc meander from 0.9219 to 0.9246 and Eur/Sek skirt 10.0000 having dipped below the round number briefly on Thursday.

In commodities, WTI and Brent front month futures remain on a firmer footing, aided up the overall constructive risk appetite coupled with some bullish technical developments, as WTI Nov surpassed USD 82/bbl (vs 81.39/bbl low) and Brent Dec briefly topped USD 85/bbl (vs 84.16/bbl low). There has been little in terms of fresh fundamental catalysts to drive the price action, although Russia's Gazprom Neft CEO hit the wires earlier and suggested that reserve production capacity could meet the increase in oil demand, whilst a seasonal decline in oil consumption is possible and the oil market will stabilise in the nearest future. On the Iranian JCPOA front, Iran said it is finalising steps to completing its negotiating team but they are absolutely decided to go back to Vienna discussions and conclude the negotiations, WSJ's Norman. The crude complex seems to have (for now) overlooked reports that the White House is engaged in diplomacy" with OPEC+ members regarding output. UK nat gas prices were higher as European players entered the fray, but prices have since waned off best levels after Russian Deputy PM Novak suggested that gas production in Russia is running at maximum capacity. Elsewhere, spot gold has been trundling amid yield-play despite lower despite the Buck being on the softer side of today’s range. Spot gold failed to hold onto USD 1,800/oz status yesterday and has subsequently retreated below its 200 DMA (1,794/oz) and makes its way towards the 50 DMA (1,776/oz). LME copper prices are on a firmer footing with prices back above USD 10,000/t – supported by technicals and the overall risk tone, although participants are cognizant of potential Chinese state reserves releases. Conversely, Dalian iron ore futures fell for a third straight session, with Rio Tinto also cutting its 2021 iron ore shipment forecasts due to dampened Chinese demand.

US Event Calendar

8:30am: Sept. Retail Sales Advance MoM, est. -0.2%, prior 0.7%

8:30am: Sept. Retail Sales Ex Auto MoM, est. 0.5%, prior 1.8%

8:30am: Sept. Retail Sales Control Group, est. 0.5%, prior 2.5%

8:30am: Sept. Retail Sales Ex Auto and Gas, est. 0.3%, prior 2.0%

8:30am: Oct. Empire Manufacturing, est. 25.0, prior 34.3

8:30am: Sept. Import Price Index MoM, est. 0.6%, prior -0.3%; YoY, est. 9.4%, prior 9.0%

8:30am: Sept. Export Price Index MoM, est. 0.7%, prior 0.4%; YoY, prior 16.8%

10am: Aug. Business Inventories, est. 0.6%, prior 0.5%

10am: Oct. U. of Mich. 1 Yr Inflation, est. 4.7%, prior 4.6%; 5-10 Yr Inflation, prior 3.0%

10am: Oct. U. of Mich. Sentiment, est. 73.1, prior 72.8

10am: Oct. U. of Mich. Current Conditions, est. 81.2, prior 80.1

10am: Oct. U. of Mich. Expectations, est. 69.1, prior 68.1

DB's Jim Ried concludes the overnight wrap

A few people asked me what I thought of James Bond. I can’t say without spoilers so if anyone wants my two sentence review I will cut and paste it to all who care and reply! At my age I was just impressed I sat for over three hours (including trailers) without needing a comfort break. By the time you email I will have also listened to the new Adele single which dropped at midnight so happy to include that review as well for free.

While we’re on the subject of music, risk assets feel a bit like the most famous Chumbawamba song at the moment. They get knocked down and they get up again. Come to think about it that’s like James Bond too. Yesterday was a strong day with the S&P 500 (+1.71%) moving back to within 2.2% of its all-time closing high from last month. If they can survive all that has been thrown at them of late then one wonders where they’d have been without any of it.

The strong session came about thanks to decent corporate earnings releases, a mini-collapse in real yields, positive data on US jobless claims, as well as a further fall in global Covid-19 cases that leaves them on track for an 8th consecutive weekly decline. However, inflation remained very much on investors’ radars, with a range of key commodities taking another leg higher, even as US data on producer prices was weaker than expected.

Starting with the good news, the equity strength was across the board with the S&P 500 experiencing its best daily performance since March, whilst Europe’s STOXX 600 (+1.20%) also put in solid gains. It was an incredibly broad-based move higher, with every sector group in both indices rising on the day, with a remarkable 479 gainers in the S&P 500, which is the second-highest number we’ve seen over the last 18 months. Every one of the 24 S&P 500 industry groups rose, led by cyclicals such as semiconductors (+3.12%), transportation (+2.51%) and materials (+2.43%). A positive start to the Q3 earnings season buoyed sentiment, as a number of US banks (+1.45%) reported yesterday, all of whom beat analyst estimates. In fact, of the nine S&P 500 firms to report yesterday, eight outperformed analyst expectations. Weighing in on recent macro themes, Bank of America Chief, Brian Moynihan, noted that the current bout of inflation is “clearly not temporary”, but also that he expects consumer demand to remain robust and that supply chains will have to adjust. I’m sure we’ll hear more from executives as earnings season continues today.

Alongside those earnings releases, yesterday saw much better than expected data on the US labour market, which makes a change from last week’s underwhelming jobs report that showed the slowest growth in nonfarm payrolls so far this year. In terms of the details, the weekly initial jobless claims for the week through October 9, which is one of the most timely indicators we get, fell to a post-pandemic low of 293k (vs. 320k expected). That also saw the 4-week moving average hit a post-pandemic low of 334.25k, just as the continuing claims number for the week through October 2 hit a post-pandemic low of 2.593m (vs. 2.670m expected). We should get some more data on the state of the US recovery today, including September retail sales, alongside the University of Michigan’s consumer sentiment index for October.

That optimism has fed through into Asian markets overnight, with the Nikkei (+1.43%), the Hang Seng (+0.86%), the Shanghai Comp (+0.29%) and the KOSPI (+0.93%) all moving higher. That came as Bloomberg reported that China would loosen restrictions on home loans amidst the concerns about Evergrande. And we also got formal confirmation that President Biden had signed the debt-limit increase that the House had passed on Tuesday, which extends the ceiling until around December 3. Equity futures are pointing to further advances in the US and Europe later on, with those on the S&P 500 (+0.30%) and the STOXX 50 (+0.35%) both moving higher.

Even with the brighter news, inflation concerns are still very much with us however, and yesterday in fact saw Bloomberg’s Commodity Spot Index (+1.16%) advance to yet another record high, exceeding the previous peak from early last week. That was partly down to the continued rise in oil prices, with WTI (+1.08%) closing at $81.31/bbl, its highest level since 2014, just as Brent Crude (+0.99%) hit a post-2018 high of $84.00/bbl. Both have posted further gains this morning of +0.58% and +0.61% respectively. Those moves went alongside further rises in natural gas prices, which rose for a 3rd consecutive session, albeit they’re still beneath their peak from earlier in the month, as futures in Europe (+9.14%), the US (+1.74%) and the UK (+9.26%) all moved higher. And that rise in Chinese coal futures we’ve been mentioning also continued, with their rise today currently standing at +13.86%, which brings their gains over the week as a whole to +39.02% so far.

As well as energy, industrial metals were another segment where the recent rally showed no sign of abating yesterday. On the London metal exchange, a number of multi-year milestones were achieved, with aluminum prices (+1.60%) up to their highest levels since 2008, just as zinc prices (+3.73%) closed at their highest level since 2018. Separately, copper prices (+2.56%) hit a 4-month high, and other winners yesterday included iron ore futures in Singapore (+1.16%), as well as nickel (+1.99%) and lead (+2.43%) prices in London.

With all this momentum behind commodities, inflation expectations posted further advances yesterday. Indeed, the 10yr US Breakeven closed +1.0bps higher at 2.536%, which is just 3bps shy of its closing peak back in May that marked its highest level since 2013. And those moves came in spite of US producer price data that came in weaker than expected, with the monthly increase in September at +0.5% (vs. +0.6% expected). That was the smallest rise so far this year, though that still sent the year-on-year number up to +8.6% (vs. +8.7% expected). That rise in inflation expectations was echoed in Europe too, with the 10yr UK breakeven (+5.6bps) closing at its highest level since 2008, whilst its German counterpart also posted a modest +0.7bps rise.

In spite of the rise in inflation expectations, sovereign bonds posted gains across the board as the moves were outweighed by the impact of lower real rates. By the end of yesterday’s session, yields on 10yr Treasuries were down -2.6bps to 1.527%, which came as the 10yr real yield moved back beneath -1% for the first time in almost a month. Likewise in Europe, yields pushed lower throughout the session, with those on 10yr bunds (-6.3bps), OATs (-6.2bps) and BTPs (-7.1bps) all moving aggressively lower.

To the day ahead now, and US data releases include September retail sales, the University of Michigan’s preliminary consumer sentiment index for October, and the Empire State manufacturing survey for October. Central bank speakers include the Fed’s Bullard and Williams, and earnings releases include Charles Schwab and Goldman Sachs.

Bougie Broke The Financial Reality Behind The Facade

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive…

Social media users claiming to be Bougie Broke share pictures of their fancy cars, high-fashion clothing, and selfies in exotic locations and expensive restaurants. Yet they complain about living paycheck to paycheck and lacking the means to support their lifestyle.

Bougie broke is like “keeping up with the Joneses,” spending beyond one’s means to impress others.

Bougie Broke gives us a glimpse into the financial condition of a growing number of consumers. Since personal consumption represents about two-thirds of economic activity, it’s worth diving into the Bougie Broke fad to appreciate if a large subset of the population can continue to consume at current rates.

The Wealth Divide Disclaimer

Forecasting personal consumption is always tricky, but it has become even more challenging in the post-pandemic era. To appreciate why we share a joke told by Mike Green.

Bill Gates and I walk into the bar…

Bartender: “Wow… a couple of billionaires on average!”

Bill Gates, Jeff Bezos, Elon Musk, Mark Zuckerberg, and other billionaires make us all much richer, on average. Unfortunately, we can’t use the average to pay our bills.

According to Wikipedia, Bill Gates is one of 756 billionaires living in the United States. Many of these billionaires became much wealthier due to the pandemic as their investment fortunes proliferated.

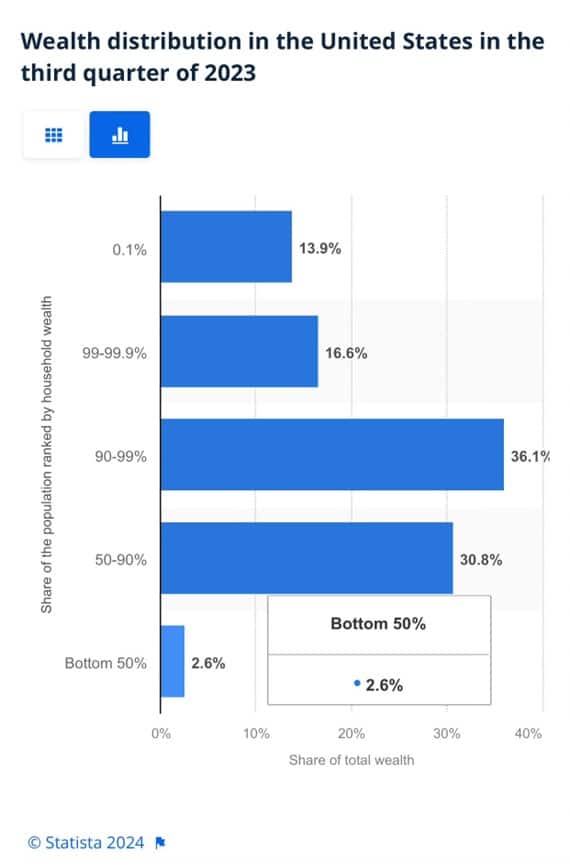

To appreciate the wealth divide, consider the graph below courtesy of Statista. 1% of the U.S. population holds 30% of the wealth. The wealthiest 10% of households have two-thirds of the wealth. The bottomhalf of the population accounts for less than 3% of the wealth.

The uber-wealthy grossly distorts consumption and savings data. And, with the sharp increase in their wealth over the past few years, the consumption and savings data are more distorted.

Furthermore, and critical to appreciate, the spending by the wealthy doesn’t fluctuate with the economy. Therefore, the spending of the lower wealth classes drives marginal changes in consumption. As such, the condition of the not-so-wealthy is most important for forecasting changes in consumption.

Revenge Spending

Deciphering personal data has also become more difficult because our spending habits have changed due to the pandemic.

A great example is revenge spending. Per the New York Times:

Ola Majekodunmi, the founder of All Things Money, a finance site for young adults, explained revenge spending as expenditures meant to make up for “lost time” after an event like the pandemic.

So, between the growing wealth divide and irregular spending habits, let’s quantify personal savings, debt usage, and real wages to appreciate better if Bougie Broke is a mass movement or a silly meme.

The Means To Consume

Savings, debt, and wages are the three primary sources that give consumers the ability to consume.

Savings

The graph below shows the rollercoaster on which personal savings have been since the pandemic. The savings rate is hovering at the lowest rate since those seen before the 2008 recession. The total amount of personal savings is back to 2017 levels. But, on an inflation-adjusted basis, it’s at 10-year lows. On average, most consumers are drawing down their savings or less. Given that wages are increasing and unemployment is historically low, they must be consuming more.

Now, strip out the savings of the uber-wealthy, and it’s probable that the amount of personal savings for much of the population is negligible. A survey by Payroll.org estimates that 78% of Americans live paycheck to paycheck.

More on Insufficient Savings

The Fed’s latest, albeit old, Report on the Economic Well-Being of U.S. Households from June 2023 claims that over a third of households do not have enough savings to cover an unexpected $400 expense. We venture to guess that number has grown since then. To wit, the number of households with essentially no savings rose 5% from their prior report a year earlier.

Relatively small, unexpected expenses, such as a car repair or a modest medical bill, can be a hardship for many families. When faced with a hypothetical expense of $400, 63 percent of all adults in 2022 said they would have covered it exclusively using cash, savings, or a credit card paid off at the next statement (referred to, altogether, as “cash or its equivalent”). The remainder said they would have paid by borrowing or selling something or said they would not have been able to cover the expense.

Debt

After periods where consumers drained their existing savings and/or devoted less of their paychecks to savings, they either slowed their consumption patterns or borrowed to keep them up. Currently, it seems like many are choosing the latter option. Consumer borrowing is accelerating at a quicker pace than it was before the pandemic.

The first graph below shows outstanding credit card debt fell during the pandemic as the economy cratered. However, after multiple stimulus checks and broad-based economic recovery, consumer confidence rose, and with it, credit card balances surged.

The current trend is steeper than the pre-pandemic trend. Some may be a catch-up, but the current rate is unsustainable. Consequently, borrowing will likely slow down to its pre-pandemic trend or even below it as consumers deal with higher credit card balances and 20+% interest rates on the debt.

The second graph shows that since 2022, credit card balances have grown faster than our incomes. Like the first graph, the credit usage versus income trend is unsustainable, especially with current interest rates.

With many consumers maxing out their credit cards, is it any wonder buy-now-pay-later loans (BNPL) are increasing rapidly?

Insider Intelligence believes that 79 million Americans, or a quarter of those over 18 years old, use BNPL. Lending Tree claims that “nearly 1 in 3 consumers (31%) say they’re at least considering using a buy now, pay later (BNPL) loan this month.”More telling, according to their survey, only 52% of those asked are confident they can pay off their BNPL loan without missing a payment!

Wage Growth

Wages have been growing above trend since the pandemic. Since 2022, the average annual growth in compensation has been 6.28%. Higher incomes support more consumption, but higher prices reduce the amount of goods or services one can buy. Over the same period, real compensation has grown by less than half a percent annually. The average real compensation growth was 2.30% during the three years before the pandemic.

In other words, compensation is just keeping up with inflation instead of outpacing it and providing consumers with the ability to consume, save, or pay down debt.

It’s All About Employment

The unemployment rate is 3.9%, up slightly from recent lows but still among the lowest rates in the last seventy-five years.

The uptick in credit card usage, decline in savings, and the savings rate argue that consumers are slowly running out of room to keep consuming at their current pace.

However, the most significant means by which we consume is income. If the unemployment rate stays low, consumption may moderate. But, if the recent uptick in unemployment continues, a recession is extremely likely, as we have seen every time it turned higher.

It’s not just those losing jobs that consume less. Of greater impact is a loss of confidence by those employed when they see friends or neighbors being laid off.

Accordingly, the labor market is probably the most important leading indicator of consumption and of the ability of the Bougie Broke to continue to be Bougie instead of flat-out broke!

Summary

There are always consumers living above their means. This is often harmless until their means decline or disappear. The Bougie Broke meme and the ability social media gives consumers to flaunt their “wealth” is a new medium for an age-old message.

Diving into the data, it argues that consumption will likely slow in the coming months. Such would allow some consumers to save and whittle down their debt. That situation would be healthy and unlikely to cause a recession.

The potential for the unemployment rate to continue higher is of much greater concern. The combination of a higher unemployment rate and strapped consumers could accentuate a recession.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}