Futures Grind Higher After Biden-Xi Summit

Futures Grind Higher After Biden-Xi Summit

US equity futures reversed earlier losses, trading slightly in the green, while bonds were lifted as traders awaited a decision from the White House on who the next Federal Reserve head will be…

Share this:

US equity futures reversed earlier losses, trading slightly in the green, while bonds were lifted as traders awaited a decision from the White House on who the next Federal Reserve head will be amid speculation Fed policy tightening could be slowed down under Elizabeth Warren's favorite progressive, Lael Brainard. At 730am, S&P futures were up 1.75 of 0.04%, Nasdaq futures were up 2.75 or 0.02% and Dow Jones futures traded 58 points higher or 0.161%. 10-year Treasury yield retreats back toward the 1.6% level after climbing for three days in a row; the dollar was flat and bitcoin tumbled, briefly sliding below $60,000 on no news, before reversing modestly.

As a reminder, both current Chair Jerome Powell and Fed Governor Lael Brainard have been interviewed for the top job, and a decision is expected imminently, according to the Senate Banking Chairman. The news earlier this month that Brainard is in the running sent long bond yields tumbling on the assumption that she would be significantly more dovish.

Futures bounced on news Pfizer reached a licensing agreement that will allow generic-drug manufacturers to produce inexpensive versions of its Covid-19 pill for 95 low- and middle-income countries, following a similar move by Merck & Co. In a statement on Tuesday, Pfizer said it has signed an agreement with the United Nations-backed Medicines Patent Pool to license the experimental pill, once it is authorized by regulators, to generic companies that can supply it to countries that account for roughly 53% of the world population.

Sentiment was also molded by the outcome of the 3-hour long virtual summit between Biden and Xi who covered a range of topics including trade, the status of Taiwan and human rights in their first face-to- face summit, which went on longer than expected - after all it was way past Joe's bedtime - even though they announced no major breakthroughs. The virtual summit sent a message that the two sides are open to engaging in more communication -- rather than confrontation -- to avoid escalation in areas of conflict, Bloomberg Intelligence economist Eric Zhu writes in a note. Riskier markets have struck an optimistic tone spurred by headlines around talks between U.S. President Joe Biden and China President Xi Jinping, according to Credit Agricole analysts including Eddie Cheung.

“The key in our view is that both sides continue to engage and are sending messages for potential near-term cooperation which is still supportive at the margin of sentiment” they wrote in a note. “Outside of that, there is a dearth of significant EM data to drive markets today and tomorrow, we expect EM markets to be driven more by events elsewhere. The rise in U.S. yields should once more keep the market on its toes.”

Shares of Walmart rose 1.9% in premarket trading after the country’s largest brick-and-mortar retailer hiked its annual sales and profit forecasts, banking on soaring demand expected during the crucial holiday season. Retailer Home Depot also inched higher after beating quarterly same-store sales estimates, helped by strong demand for tools and materials from builders and handymen working on housing projects.

In the premarket, Tesla Inc. shares fell after Elon Musk exercised options to sell more of his stock. Musk exercised options and sold around another $930m in Tesla shares on Monday, adding to the $6.9b he had already sold last week. Rivian Automotive Inc. added to recent gains, doubling the $78 it sold its shares at when it listed last week. In corporate news, JPMorgan sued Tesla seeking a $162 million payment for warrants that expired above their strike price following Elon Musk’s 2018 tweet about taking the company private. Meanwhile, crypto-exposed stocks are slumping in premarket trading as Bitcoin and other digital currencies see steep declines. Here are some of the biggest U.S. movers today:

- Peloton (PTON) shares plunged as much as 8.1% in premarket trading after the company said it has started an underwritten public offering of $1 billion of its Class A shares.

- Tesla (TSLA US) shares fall as much as 1.7% in U.S. premarket trading after CEO Elon Musk sold more shares in the EV maker. Musk exercised options and sold around another $930m in Tesla shares on Monday, adding to the $6.9b he had already sold last week.

- Cryptocurrency-exposed stocks fell in U.S. premarket trading and in Europe, with Bitcoin and Ether both declining amid a broad selloff in digital assets. Stocks moving include Riot Blockchain (RIOT US) and Marathon Digital (MARA US), the latter after it plunged in the prior session.

- Rivian Automotive (RIVN US) shares rise as much as 5.4% in U.S. premarket trading, continuing the run of gains for the EV maker since its IPO last week. The stock touched slightly more than double its IPO price.

- Creatd (CRTD US) jump as much as 50% in U.S. premarket trading after it reported 3Q earnings, reaffirmed its 2021 revenue view and initiated guidance for 2022.

European stocks turned green after opening in the red, with travel shares hitting session highs on new of the cheap Covid-pill. The Stoxx 600 Travel & Leisure Index hits session high on optimism about increased tourism after Pfizer reaches a licensing agreement allowing generic-drug manufacturers to produce cheap versions of its Covid-19 pill for 95 low- and middle-income countries. SXTP gains as much as 0.9%, +0.5% as of 1:02pm CET.

Earlier in the session, Asian stocks rose for a fourth day, led by gains in Hong Kong, with investors closely watching the U.S.-China summit for fresh cues. The MSCI Asia Pacific Index climbed 0.2%, on track for its longest string of gains since early September. Consumer discretionary and technology sectors gave the biggest boost to the benchmark. Hong Kong’s Hang Seng Index jumped more than 1%: shares of Macau casino operators surged on hopes of better-than-expected outcomes from Macau’s public consultation on a proposed gaming law amendment. The Asian stock benchmark is heading for its highest close in two months, buoyed by optimism over reopening economies that’s helping outweigh worries over inflation. Singapore said Monday that it will open its borders to five more countries as the city-state presses on with plans to live with Covid. Sentiment among Asia ex-Japan and Chinese investors has remained “bullish,” Olivier d’Assier, head of APAC applied research at Qontigo, wrote in a note. “Investors in emerging markets appear less worried about market risk, and focused more on strong consumer demand abroad and low valuations at home.” The first face-to-face virtual summit between U.S. President Joe Biden and Chinese President Xi Jinping got under way, with both sides aiming to stabilize the relationship between the nations while downplaying expectations for major breakthroughs

In rates, treasuries were higher with the curve flatter after unwinding Asia-session losses during European morning. Yields are richer by ~1bp across long-end of the curve, flattening 2s10s and 5s30s spreads by less than 1bp; 10-year is around 1.606% after topping at 1.618%. Spanish and Italian bonds outperform, while bunds and gilts keep pace with Treasuries. Focal points for U.S. session include October retail sales, following last week’s hot CPI print, and two Fed purchase operations. During Asia session, Aussie bonds dropped even after RBA Governor Philip Lowe said it’s “still plausible” the central bank doesn’t hike before 2024. Bunds bull-steepen with 5y yields richer by ~2bps. Gilts and USTs bull-flatten, richer by ~2.5bps across the back end. Peripheral spreads tighten slightly. In FX, Bloomberg dollar index fades Asia’s modest weakness to trade flat

In FX, the Bloomberg Dollar Spot Index was little changed and the greenback traded mixed versus its Group-of-10 peers after U.S. President Joe Biden and Chinese leader Xi Jinping spoke of the need for cooperation in their first face-to-face summit, even though they announced no major breakthroughs. The euro fell to its lowest level since July 2020 as European data lose steam against the U.S., and options bets look for further weakness. The pound rose to a nearly one-week high after data showed the U.K. jobs market strengthened in October, bolstering the case for a Bank of England rate hike. U.K. companies added 160,000 more people to their payrolls, while vacancies surged to a record high. The figures suggest very few of the 1.1 million workers who were on furlough became unemployed when the government’s benefit program for those out of work in the pandemic finished in September. China’s yuan climbed to a five-month high as talks between U.S. President Joe Biden and his Chinese counterpart Xi Jinping fueled hopes of better ties. Australia’s yield curve bear- steepened following the Reserve Bank’s November meeting minutes and after central bank chief Philip Lowe in a speech opened the door to an interest-rate increase before 2024.

China's yuan climbed to a five-month high, approaching its strongest level since May 2018, as traders grew hopeful that a summit between the U.S. and China will ease tensions between the nations. The index for developing-nation stocks rose for a seventh day, heading for its longest winning streak in nine months. The onshore yuan gained as much as 0.3% to 6.3666 per dollar. It’s now within striking distance of a year-to-date high of 6.3565 reached on May 31. A breach of that would take the yuan to its strongest level since 2018, just before the U.S.-China trade war pummeled the currency. USD/CNH slips as much as 0.3% to 6.3616;

In commodities, Natural gas pops higher after Nord Stream 2 certification temporarily suspended in Germany. Crude futures hold in the green but drift off Asia’s best levels. WTI holds above $80, Brent trades near $83.40 after failing to breach $83 overnight

Looking at the day ahead now, and US data releases include retail sales, industrial production and capacity utilisation for October, while in Europe there’s the second estimate of Euro Area GDP in Q3 and UK unemployment for September. Central bank speakers include ECB President Lagarde, and the Fed’s Barkin, Bostic, George and Daly. Finally, earnings releases include Walmart and Home Depot.

Market Snapshot

- S&P 500 futures little changed at 4,674.50

- STOXX Europe 600 up 0.2% to 489.21

- MXAP up 0.2% to 201.28

- MXAPJ up 0.3% to 658.32

- Nikkei up 0.1% to 29,808.12

- Topix up 0.1% to 2,050.83

- Hang Seng Index up 1.3% to 25,713.78

- Shanghai Composite down 0.3% to 3,521.79

- Sensex down 0.4% to 60,445.89

- Australia S&P/ASX 200 down 0.7% to 7,420.44

- Kospi little changed at 2,997.21

- German 10Y yield little changed at -0.23%

- Euro little changed at $1.1363

- Brent Futures up 0.4% to $82.41/bbl

- Brent Futures up 0.4% to $82.41/bbl

- Gold spot up 0.6% to $1,874.23

- U.S. Dollar Index up 0.11% to 95.51

Top Overnight News from Bloomberg

- Senate Banking Chairman Sherrod Brown said he was told by White House officials to expect an “imminent” announcement about President Joe Biden’s pick to chair the Federal Reserve

- A gauge of implied volatility suggests the action in Treasuries is far from over. The ICE BofA MOVE Index, which measures one-month swings in U.S. sovereign debt, climbed to 81.59 on Monday, the highest since April 2020. The U.S. Government Securities Liquidity Index closed at a 20-month peak last week, indicating worsening conditions for trading the securities

- The tightness in global oil markets that propelled prices to a seven-year high is starting to ease as production recovers in the U.S. and elsewhere, the International Energy Agency said

- OPEC+ would face challenges to quickly pump more oil if a decision was taken to do so, according to the head of Nigeria’s state energy company

Asia-Pac stocks traded mixed in a slight improvement on the inconclusive handover from Wall Street where the major indices ended a choppy session flat as yields grinded higher led by inflation breakevens, while focus shifted to the Biden-Xi virtual meeting in which the opening remarks set a friendly tone although the expectations had been lowered beforehand as tariffs were unlikely to be on the agenda and with the meeting not expected to yield further deliverables or dialogues. ASX 200 (-0.7%) and Nikkei 225 (+0.1%) were mixed with the Australian benchmark pressured by broad weakness across most its sectors and with the declines led by the mining and materials industries, while Tokyo stocks were just about kept afloat amid a choppy currency and after the recent draft details of the incoming stimulus plan but with upside capped by resistance on approach to the 30k level. Hang Seng (+1.3%) and Shanghai Comp. (-0.3%) were both initially encouraged after the warm start to the Biden-Xi meeting in which President Biden stated that he hopes the leaders meet face to face next time and that their responsibility as leaders is to ensure ties do not veer into open conflict, while Chinese President Xi said that he was happy to see his 'old friend’ and suggested that they must increase communication and cooperation. The advances in Hong Kong were led by gambling names and tech, although gains were capped for the mainland as the tempered expectations for the meeting came to fruition and with the PBoC draining liquidity, as well as lingering default concerns with Kaisa Group so far failing to make payments to its dollar bond investors due last week, but still has a grace period. Finally, 10yr JGBs declined as Japanese stocks remained afloat and with spillover selling from the bear steepening stateside which was led by inflation breakevens and amid corporate supply in the long-end, while the latest 5yr JGB auction did little to spur prices despite a higher b/c as all other metrics printed relatively inline with the previous.

Top Asian News

- China Party Reiterates Complete Reunification to Be Achieved

- Asia Stocks Advance, Hong Kong Leads Gains With Casino Names

- Singapore Air Bringing 737 Max Back Into Service in Coming Weeks

- Chairman’s Aide Pledges Luxury Homes For Loan: Evergrande Update

Stocks in Europe are predominantly trading with marginal gains (Stoxx 600 +0.2%) as the Stoxx 600, CAC 40 and DAX have all made incremental new ATHs. The handover from the APAC session was a mixed one with focus on the Xi-Biden virtual meeting which struck a conciliatory tone although, expectations were pared back ahead of the event with tariffs not an item on the agenda. Stateside, futures trade with minor losses ahead of US Retail Sales at 13:30GMT/08:30EST with expectations looking for a 1.2% M/M increase for October. The corporate slate has seen earnings from Home Depot (HD) who are firmer by 0.5% in the pre-market after above forecasts earnings, ahead of Walmart's update due at 12:00GMT/07:00EST. In bank commentary, Goldman Sachs forecasts the S&P 500 climbing by 9% to 5,100 at year-end 2022; sees S&P 500 EPS +8% to USD 226 in 2022, and +4% to USD 236 in 2023. Elsewhere, the latest BofA Fund Manager Survey revealed that investors are ending the year "risk-on" with the largest overweight of US stocks since August 2013. Back to Europe, sectors are mostly firmer with Telecoms the best performer as Vodafone (+5.8%) sits at the top of the FTSE 100 after the Co. upgraded FCF guidance for the year following a solid H1. Auto names have been supported by Renault (+1.6%) announcing two new hydrogen-powered vehicles, whilst the CFO of Daimler’s (+0.8%) Truck unit cautioned that there will need to be significant price increases. Elsewhere, Oil & Gas names have been led higher by advances in the crude complex, whilst a broker upgrade for Kering (+2.7%) at HSBC has supported the retail sector. Diageo (+2.4%) lifts the Food & Beverage sector after noting that it anticipates the strong momentum in H1 to continue through the remainder of FY22. To the downside, Imperial Brands (-0.2%) and Bouygues (-1.5%) are both lower post-earnings.

Top European News

- German Covid Deaths Spike as Lockdown for Unvaccinated Nears

- Romania GDP Growth Slows as Virus, Supply Chains Hit Rebound

- Total’s South Africa Gas Discovery Could Fast-Track Output

- Credit Suisse Downgraded Again as JPMorgan Doubts Strategy Shift

In FX, hot on the heels of generally hawkish testimony from members of the BoE’s MPC to a TSC, UK labour data has cemented market expectations for a December hike and boosted Sterling in the process, as Cable probes the semi-psychological 1.3450 mark and the Eur/Gbp cross tests 0.8450 having already fallen through the 50 DMA and 0.8500 yesterday. However, the Turkish Lira continues to slide on prospects of further easing from the CBRT (among other things) this Thursday in stark contrast to the orthodox monetary policy approach when faced with rising inflation pressures. Indeed, Usd/Try has now been as high as circa 10.2240 and is extending a bull run that has seen the Lira plunge to successive daily all time lows for five sessions in the most recent phase, even when the Dollar paused for breath again more generally. Looking at the index as a proxy, 95.500 is now acting as a pivot after Monday’s rebound through the post-US CPI high to set a fresh 2021 peak, at 95.595 and minor subsequent breach to top 95.600 before attention turns to the demand side with retail sales on the agenda ahead of ip and more from the Fed via Barkin, Bostic, George and Daly.

- NZD/CHF/CAD/AUD - All softer vs the Greenback, but the Kiwi also losing further ground closer to home as Aud/Nzd advances towards 1.0450 regardless of the fact that RBA minutes and Governor Lowe remained relatively dovish on the timing of a first rate hike overnight. Nzd/Usd has retreated through 0.7050 and Aud/Usd from above 0.7050 again in advance of NZ ppi and Aussie wages for Q3 that are expected to pick up pace, though still fall short of the 3% level required to boost overall inflation. Elsewhere, the Franc is under 0.9050, but still firmer against the Euro beyond 1.0550 and the Loonie has handed back some of its gains after briefly climbing over 1.2500 in the run up to Canadian housing starts and BoC’s Schembri on uncertainties in the jobs market and monetary policy, irrespective of a bounce in WTI.

- JPY/EUR - The Yen has relinquished 114.00+ status again, but may derive some underlying support from hefty 1.6 bn option expiry interest at the 114.30 strike, while the Euro will be hoping for more dip-buyers into 1.1350 after losing grip of 1.1400 and no real or key technical prop until the next Fib retracement of the major reversal from 1.2349 to 1.0636 that comes in at 1.1290 and represents 61.8% of the move.

- SCANDI/EM - Firmer Brent and perhaps an improvement in Q4 Norwegian consumer sentiment is keeping the Nok’s nose above 9.9000 vs the Eur, but the Sek has not derived sufficient impetus from higher Swedish money market expectations or comments from Riksbank’s Bremen in favour of a higher repo rate path to stay afloat of 10.0000. Conversely, early pleasantries between Chinese and US Presidents are underpinning the Cnh and Cny, while the Pln has taken on board hawkish guidance from NBP’s Gatnar who said two more rate hikes are needed and he will vote for back-to-back 50bp moves at both the December and January policy meetings.

In commodities, WTI and Brent are firmer to the tune of USD 0.45/bbl this morning, with price action steady throughout the European morning in-spite of a number of fresh catalysts/commentary for the complex. Firstly, the IEA OMR rounded off the monthly releases and left their forecasts for 2021 and 2022 demand growth largely unchanged while noting that US oil production will not hit pre-COVID levels until end-2022. Additionally, there has been rhetoric from multiple energy officials with Russia’s Novak remarking that it’s too early to predict the December meeting’s outcome. While the Secretary General of OPEC says an oil surplus is already beginning in December, signalling that OPEC needs to be careful; commentary which strikes a similar tone to that from the UAE yesterday, albeit the timing is more aggressive with the UAE not expecting a surplus until Q1-2022. Elsewhere, nat gas has taken centre stage given the morning’s updates around Nord Stream 2. To surmise, the German energy regulator has halted the certification process for the pipeline until the operating company arranges German company status – updates that prompted notable upside in European gas benchmarks. However, the Nord Stream 2 operator has reportedly established a subsidiary in Germany to meet these requirements, an update that has seemingly tempered the gas upside; though it remains to be seen if this will be seen as sufficient from a German perspective. Moving to metals, spot gold and silver are moderately firmer benefitting from a brief upside-flurry that took place seemingly without a fundamental driver, sending spot gold above yesterday’s best to a high of USD 1874.75/oz. Finally, base metals remain softer in-fitting with APAC performance once it became clear that, as expected, the Biden-Xi summit would not result in any breakthrough(s).

US Event Calendar

- 8:30am: Oct. Retail Sales Ex Auto and Gas, est. 0.7%, prior 0.7%

- 8:30am: Oct. Retail Sales Control Group, est. 0.9%, prior 0.8%

- 8:30am: Oct. Retail Sales Ex Auto MoM, est. 1.0%, prior 0.8%

- 8:30am: Oct. Retail Sales Advance MoM, est. 1.4%, prior 0.7%

- 8:30am: Oct. Import Price Index YoY, est. 10.3%, prior 9.2%

- 8:30am: Oct. Import Price Index ex Petroleu, est. 0.3%, prior 0.1%

- 8:30am: Oct. Import Price Index MoM, est. 1.0%, prior 0.4%

- 8:30am: Oct. Export Price Index YoY, prior 16.3%

- 8:30am: Oct. Export Price Index MoM, est. 0.9%, prior 0.1%

- 9:15am: Oct. Capacity Utilization, est. 75.9%, prior 75.2%

- 9:15am: Oct. Manufacturing (SIC) Production, est. 0.8%, prior -0.7%

- 9:15am: Oct. Industrial Production MoM, est. 0.9%, prior -1.3%

- 10am: Sept. Business Inventories, est. 0.6%, prior 0.6%

- 10am: Nov. NAHB Housing Market Index, est. 80, prior 80

- 4pm: Sept. Net Foreign Security Purchases, prior $79.3b

- 4pm: Sept. Total Net TIC Flows, prior $91b

DB's Jim Reid concludes the overnight wrap

The main event this morning has been the Biden / Xi virtual summit where both the presidents are trying to stabilise the relationship between both US & China. It’s now over with the first press statement from the White House a pretty bland reflection of topics covered at the meeting without suggesting any major announcements are likely. There has been no mentions of tariffs being discussed but we’ll likely hear more detail later on so keep your eyes peeled on the screens for that. At first glance it seems like it was a co-operative meeting but with little of substance likely to have come out of it. We will see.

This follows a familiar start to the week yesterday, with equities hovering around their all-time highs in spite of continued concerns about inflation sparking another selloff in sovereign bond markets. There wasn’t an obvious catalyst behind the moves, though the Treasury selloff began not long after a Washington Post article from former Treasury Secretary Larry Summers was released, in which he critiqued the various claims from those who still believe inflation would prove transitory. That was then followed up by remarks from BoE officials later in the session, which leant hawkish at the margins as Governor Bailey said that he was “very uneasy about the inflation situation”.

Looking at those moves in more depth, it was evident that inflation jitters were showing no sign of abating yesterday, and in fact, the 10yr US breakeven hit its highest closing level since 2005, after rising another +3.7bps to 2.76%. Those moves were echoed over different time horizons, with the 5yr breakeven up +7.5bps to a record high of 3.19%, and even the 30yr breakeven hit a post-2013 high of 2.49%. However, even as breakevens continued to rise, real rates remained relatively subdued, with the 10yr real yield (+2.2bps) hovering close to an all-time low at -1.15%, whilst the 5yr real yield actually fell -4.3bps to -1.95%. All in all, that left the Treasury yield curve steeper, with the 2yr nominal yield (+0.4bps) basically unchanged, whilst the 5yr yield (+3.4bps) hit a post-pandemic high and the 10yr yield rose +6.2bps to 1.63%. 30yr yields managed to rise back just above 2.0%, after increasing +7.7bps on the day. Overnight US yields are back down a couple of basis points.

Over in Europe there was a similar pattern, albeit to a lesser extent, with yields on 10yr bunds (+3.1bps), OATs (+3.0bps) and BTPs (+4.1bps) all moving higher. Interestingly, that meant the gap between 10yr Treasury and bund yields hit their widest level since late-April at 186bps, although that’s still less than the recent peak above 200bps at the start of April, when optimism about a potential US reflation was at its peak, less than a month after Biden had signed the American Rescue Plan Act featuring $1.9tn of stimulus.

For equities it was a much more subdued picture, with the S&P 500 (0.00%) paring back its gains from earlier in the session to end flat on the day. Defensive stocks outperformed, with Utilities (+1.31%) outpacing the rest of the index. There wasn’t a particular driver behind the declines, though Tesla (-1.94%) weighed on sentiment after more Musk induced speculation about selling more of his holdings permeated. It ended the session as the third-worst performer in the S&P 500, and its decline was also evident in the FANG+ index (-0.26%) of megacap tech stocks. European equities outperformed, with the STOXX 600 (+0.35%) reaching another record high, just as others including the CAC 40 (+0.53%) and the DAX (+0.34%) ascended to fresh all-time highs of their own.

Overnight in Asia stocks are trading in the green with the Hang Seng (+1.05%) leading the pack followed by the CSI (+0.53%), Shanghai Composite (+0.29%), the Nikkei (+0.23%) and the KOSPI (+0.01%). Stocks rose for a fourth day with investors closely watching the Biden-Xi summit. Japan’s Finance Minister Shunichi Suzuki said that the size of the economic stimulus package expected to be released over the weekend is yet to be decided. He also said that the overall size will be decided based on the requests from ministries and not the other way around. Also BoJ Governor Haruhiko Kuroda clarified that he does not intend on reducing monetary easing even if inflation were to get near 1% in Japan. Elsewhere futures are indicating a flat start to markets in the US and Europe with S&P 500 futures +0.06% and DAX futures +0.01%.

President Biden signed the bi-partisan infrastructure bill into law, codifying $550 billion of new spending over the next decade. In prepared remarks the President heralded the bill as an important, incremental achievement, “With this law, we focused on getting things done” despite not getting everything people may have wanted. He also made the case that the investments in supply chain resilience should push against inflation in the long term. The President’s social and climate spending bill is due to be scored by the Congressional Budget Office by the end of this week, a precondition some moderate Democrats had for supporting the package. While the Biden administration has asserted the bill would be paid for by revenue offsets, ameliorating any budget or inflation impact, the CBO Director declined to confirm whether or not the agency would score it that way.

On the topic of inflation, oil prices barely managed to eek out a positive day after spending most of the day in the red as speculation continued that President Biden could use the Strategic Petroleum Reserve to ease the rise in gasoline prices seen over recent weeks. Indeed, Energy Secretary Granholm told CNN earlier in the day that Biden was evaluating the SPR. WTI (+0.11%) had fallen beneath $80/bbl intraday but finished at $80.88/bbl. That said, a number of other commodities showed no signs of declining, with European natural gas futures (+5.06%), finishing just shy of €80 per megawatt-hour for the first time in nearly three weeks, whilst wheat futures (+1.69%) rose for a 6th consecutive session to a fresh 8-year high. Reports indicated that spot prices of US coal from Central Appalachia surged to their highest levels since 2009, at just below $90/ton.

Turning to the Fed, markets are still eagerly awaiting to find out who’s going to be chosen as the next Chair, but we did hear from a Wall Street Journal report that President Biden is expected to make a decision “as soon as this week”. After the New York close, Senate Banking Chair Sherrod Brown reportedly said that a pick was imminent. Senator Brown didn’t know who the pick would be but noted he was pretty sure it was one of the two front runners, Powell or Brainard. That said, previous deadlines that have been reported in the press have come and gone, and it’s two weeks’ ago today that Biden himself said we’d get an announcement “fairly quickly”, so we’ll bring it to you as get anything concrete. One potential line of interest in the WSJ story was that Biden’s interview with Governor Brainard, who’s also considered to be in contention, “went better than expected”. News that Roger Ferguson, former TIAA head and Fed Vice Chair, would not be taking the helm of Apollo Global Management, as was previously reported, drove speculation that he was now a contender for one of the Fed vacancies, as well.

Looking at the pandemic, cases are continuing to rise at the global level and a number of countries in Europe are moving to toughen up restrictions in response. In Ireland, the Irish Times reported that the government was set to return to advice to work from home, and in Austria yesterday marked the start of their lockdown for the unvaccinated. Separately, there were moves to extend the rollout of booster jabs as countries look to avoid further restrictions, and the UK extended their programme yesterday to individuals in their 40s. I’ll therefore be doing my bit by booking mine as soon as my 6 months gap between doses is up.

There wasn’t much to report on the data front yesterday, though the New York Fed’s Empire State manufacturing survey saw the headline general business conditions index rise to 30.9 (vs. 22.0 expected). Nevertheless, price pressures continued to remain elevated, with the prices received index up to a record high of 50.8, whilst prices paid rose to 83.0.

To the day ahead now, and US data releases include retail sales, industrial production and capacity utilisation for October, while in Europe there’s the second estimate of Euro Area GDP in Q3 and UK unemployment for September. Central bank speakers include ECB President Lagarde, and the Fed’s Barkin, Bostic, George and Daly. Finally, earnings releases include Walmart and Home Depot.

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

{kind=link}

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

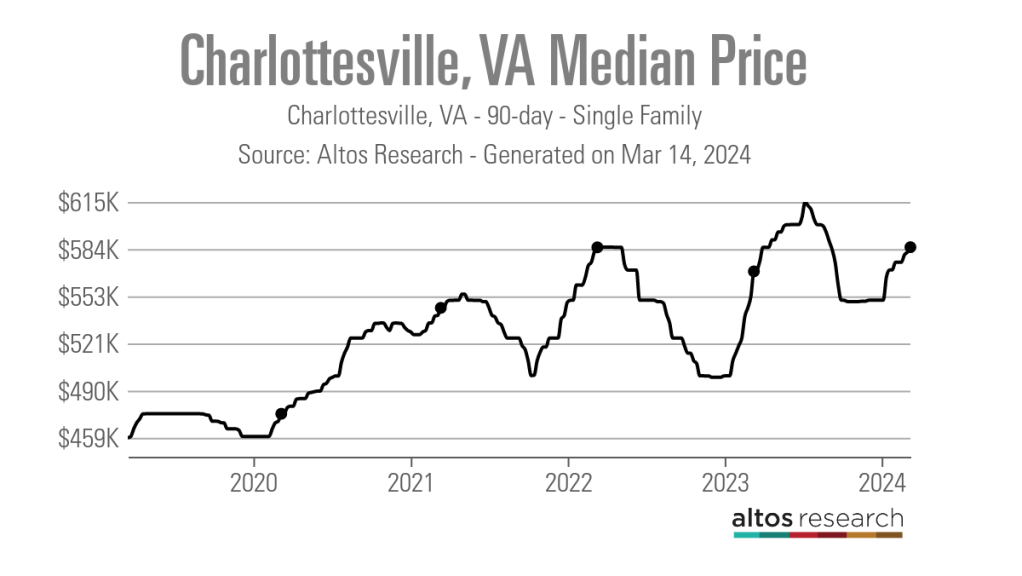

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest rates

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Key shipping company files for Chapter 11 bankruptcy

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges