Futures, Global Stocks Rise As Dollar Rout Accelerates

Futures, Global Stocks Rise As Dollar Rout Accelerates

US equity futures rose for the 3rd day in 4 and world stocks pushed higher on Tuesday while the dollar tumbled to three-month lows as optimism that economic reopening will boost growth..

Futures, Global Stocks Rise As Dollar Rout Accelerates

US equity futures rose for the 3rd day in 4 and world stocks pushed higher on Tuesday while the dollar tumbled to three-month lows as optimism that economic reopening will boost growth outweighed concern about a pick-up in virus cases in parts of Asia even if it leads to higher prices. Oil gained and 10Y yields dropped marginally.

At 7:30 a.m. ET, Dow e-minis were up 77 points, or 0.22%, S&P 500 e-minis were up 9 points, or 0.3%, and Nasdaq 100 e-minis were up 73 points, or 0.55%. Retailers Walmart and Macy’s jumped in premarket trading after raising their full-year guidance, while Home Depot gained as its results beat estimates. Commodity and automotive shares boosted the Stoxx Europe 600 Index, while Asian equities also climbed.

Nasdaq 100 contracts led U.S. futures higher after dovish remarks on Monday from Fed Vice-Chair Richard Clarida, who pointed to the weak April jobs report as proof of slack in the economy, and from other Fed policymakers helped to reassure markets that U.S. monetary policy will remain easy. The comments came ahead of Wednesday’s release of the minutes from the Fed’s policy meeting last month, which will be closely watched for any indications about where monetary policy is headed this year.

“Investors welcomed reassuring words from Fed Vice Chairman Richard Clarida yesterday as he continued to downplay inflation data, highlighting lingering lack of progress on employment numbers,” said Pierre Veyret, an analyst at ActivTrades in London. “The trading stance remains bull-oriented so far and investors are ready to seize any opportunity to buy dips on stocks.”

“In short, the Fed’s music is still the same. It is not yet time for tapering, and will not be for a while,” said Giuseppe Sersale, fund manager at Anthilia in Milan.

Here are some notable premarket movers:

AMC Entertainment jumped 9.5%, adding to recent gains fueled by a social-media frenzy about meme stocks and crypto-currencies

AT&T shares extend Monday’s slide in premarket trading after the communications giant said it will spin off its media operations and merge them with Discovery. Shares fall 4.3%

Baidu reported revenue for the first quarter that beat the average analyst estimate. Shares rise 3.2%

Shares of EV charging equipment makers Chargepoint Holdings and Blink Charging gained 1.7% and 2.6% as President Joe Biden was set to make the case for his $174 billion electric vehicle plan on Tuesday

Eastman Kodak falls 5.4% after Reuters reports that the New York Attorney General’s office is preparing an insider-trading lawsuit against the firm and its executive chairman, Jim Continenza. Reuters cites the company and people familiar with the matter

Home Depot shares rose as much as 2.6% ahead of the bell after the home improvement retailer reported first-quarter results that handily topped analysts’ estimates. Shares of competitor Lowe’s, which reports premarket Wednesday, may also rise

II-VI was downgraded to equal weight from overweight at Barclays, which wrote that the stock offered limited upside given its acquisition of Coherent. Shares fall 0.6%

MGM Resorts International rises as much as 2.5% after JPMorgan analyst Joseph Greff raised his recommendation on the stock to overweight from neutral

Macy’s Inc. soared after posting first-quarter sales that outpaced Wall Street’s expectations -- a sign that shoppers are venturing back to department stores and malls as vaccination rates rise. Shares rise 4.8%

Performance Food has agreed to buy Core-Mark in a cash and stock deal with $2.1 billion equity value, according to Bloomberg data. Shares climb 6.3%

Tencent Music analysts were mostly positive on the China-based online music entertainment company after it reported first- quarter revenue that beat expectations. However, at least two firms trimmed their price targets on account of higher investments. U.S.-listed shares rose 0.7%

Walmart Inc. posted strong quarterly sales growth and boosted its profit outlook, an impressive feat as the retailer was facing a difficult comparison with last year’s pandemic-fueled stockpiling. The shares rose 3.5% in premarket trading.

Market volatility had risen in recent weeks on worries that abundant stimulus and rising inflationary pressure in the United States could force the Federal Reserve to reduce its support in order to prevent the world’s largest economy from overheating. “Taper talk is the new taper,” said Mike Kelly, head of multi-asset at PineBridge Investments. “Structural inflation is still some way off but temporary supply-side bottlenecks will last at least until September. The Fed will try to talk their way through it and markets will get frustrated. But the more temporary inflation overshoots, the harder it will be to avoid taper talk."

Connected with that, tomorrow traders will parse the Fed minutes for policy discussion about inflation and hints of a timeline for reducing stimulus, after Vice Chair Richard Clarida said Monday that the weak U.S. jobs report showed the economy had not yet reached the threshold to warrant scaling back asset purchases.

Clarida's comments spilled over to global markets, and bourses in Europe rose, with the STOXX 600 regional benchmark closing in on its previous record high, up 0.4% led higher by energy and basic resources firms on optimism around easing economic restrictions. Italy’s FTSE MIB outperforms peers. Vodafone fell 6.5% after Chief Executive Officer Nick Read’s strategy showed higher capital expenditure on network investments will hit free cash flow. Here are some notable European movers:

Sonova shares climb as much as 12% to a record high after the company reported better-than-expected 2H results. Analysts were particularly impressed by the company’s guidance, which exceeded expectations.

Ubisoft shares advance as much as 6.8%, its biggest intraday rise since Jan. 13, after Exane upgrades the video game maker to outperform from neutral on outlook for net booking growth acceleration.

Oxford Biomedica shares rise as much as 12% after the company announced an increase to the expected quantity of AstraZeneca vaccine it will be manufacturing this year and raised guidance.

Scor shares jump as much as 5.6%, their biggest intraday increase in more than 4 months, after the French insurer named a new CEO and announced the earlier than expected departure of long-standing CEO Denis Kessler, who stays on as chairman.

Vodafone shares fall as much as 8.3% in their biggest one-day drop since March last year as analysts flag that the telecoms group’s higher spending plans could weigh on its free cash flow.

Earlier in the session, MSCI’s broadest index of Asia-Pacific shares outside Japan rallied 1.6%, rising for a third-straight session, with Taiwan leading the charge Tuesday in a dramatic rebound from a week-long selloff amid concerns over a resurgence of the coronavirus. Taiwan’s benchmark gauge climbed more than 5% in its best day since March 2020 on news the country is in talks with the United States for a share of the vaccine doses Washington plans to send abroad. Gains were driven by tech giants including chipmaker TSMC and iPhone assembler Hon Hai Precision, which also ranked among the biggest boosts to the MSCI Asia Pacific Index. Stocks were also strong in Japan, where investors shrugged off data showing Japan’s economy shrank more than expected in the first quarter as a slow vaccine rollout and new COVID-19 infections hit spending and engaged in dip-buying after recent declines. Among larger names, human-resources firm Recruit and the nation’s largest bank MUFG climbed after encouraging outlooks. South Korean shares gained as local institutional investors added tech and auto names. MSCI’s key regional index has gained over 3% in the past three days of trading after tumbling 4.9% over three days last week. In addition to rising virus infections in places including India, Taiwan and Singapore, global markets have been spooked by fears of accelerating inflation as economies ramp back up, especially in the U.S.

“Despite the optics, underlying growth is still favorable given the conducive external backdrop -- aggressive U.S. stimulus and U.S. economic reopening will lend further impetus to Asia’s export recovery,” Morgan Stanley analysts led by Terence Cheng wrote in a note. “We see recent Covid-19 flare-ups across Asia as a temporary speed bump” and “inflation should still stay benign in Asia.”

China stocks rose slightly, with the CSI 300 Index climbing 0.1% to close at 5,187.60, in its third straight day of gains and led by energy and material companies, as investor caution weighed on market sentiment. China Oilfield Services rose 4.7% to lead gains in the energy sector as Brent oil edges toward $70 a barrel. Meanwhile, vaccine makers were the biggest decliners on the gauge, as investors took profit following gains over the past week. Shanghai Fosun Pharmaceutical and Shenzhen Kangtai Biological Products fell more than 6.5% each. Semiconductor products manufacturer JCET Group was also one of the biggest drags on the index, falling 5% after saying a state chip fund planned to trim its stake in the firm.

Morgan Stanley said it remained cautious on the broader Chinese stock market despite the recent rebound, with lingering uncertainties including limited room for upside earnings revisions as they are already priced in and a reflationary environment putting pressure on company margins. There are also concerns around liquidity tightening and continued regulatory risks for internet and fintech stocks, the Wall Street broker said. Stocks in China and Hong Kong will only see gains of mid -to high-single digits over the next year, “marginally higher” than the broader emerging market universe, analysts including Laura Wang wrote in the note.

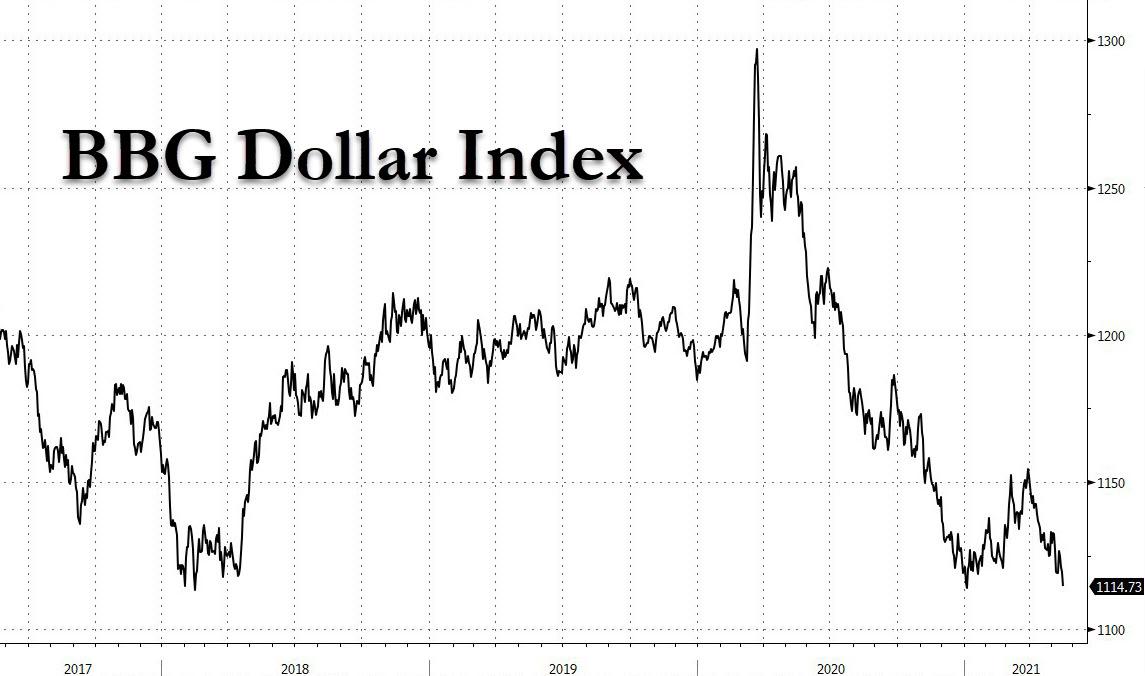

In FX, the dollar fell toward a four-month low, while U.S. 10-year Treasuries were steady as investors awaited key housing data ahead of minutes due Wednesday from the Federal Reserve’s last meeting.

The Bloomberg dollar index fell against all of its Group-of-10 peers while the euro advanced beyond $1.22 for the first time in almost three months. The New Zealand dollar outperformed led by a rally in equity and commodity markets after the Fed’s Richard Clarida played down the risk of policy tightening. The pound climbed to its highest level since February and neared amulti-year high, with the focus turning to Bank of England speeches later Tuesday, and Wednesday’s inflation data. The U.K. labor market strengthened more than expected and added more payrolls in April than any month since early 2015. The Norwegian krone touched a one-week high versus the greenback as Brent crude topped $70 a barrel in London for the first time since mid-March amid signs that recovering consumption has whittled away a glut of oil built up at the height of the Covid-19 pandemic. The yen advanced a fourth consecutive day versus the dollar.

In rates, treasuries were little changed in early U.S. session, off lows despite gains for stock futures; regional support for U.S. debt emerged during Asia session in light trading. 10-year yield near flat around 1.65% with belly of the curve slightly richer, long-end marginally cheaper on the day, steepening 5s30s by ~1bp; bunds and gilts underperform by less than a basis point. Curve slightly steeper although yields remain within a basis point of Monday’s closing levels. U.S. data includes housing starts, while Fed’s Kaplan is expected to speak. IG dollar issuance slate includes World Bank 5Y, CDP Financial $1b 5Y and Cades 3Y; another active session is expected after almost $20b was priced Monday, led by $7b UnitedHealth offering whose order book was said to approach $27b

In commodities, Brent crude topped $70 a barrel for the first time since March, as expectations of demand recovery following reopenings of the European and U.S. economies offset concern over spreading coronavirus cases in Asia. Brent crude was up 0.8% at $70.03 and U.S. West Texas Intermediate crude gained 0.7% at $66.75. Copper rose toward a record as the potential for tighter regulation and higher taxes in Chile fueled concerns about the long-term supply outlook; zinc jumped amid speculation about disruptions to Chinese output. Spot gold rose to its highest in nearly four months as a weaker U.S. dollar and growing inflationary pressure bolstered the metal’s appeal as an inflation hedge. It was last up 0.1% at $1,867.9 per ounce.

Bitcoin rose 4%, paring some of its steep losses since Tesla boss Elon Musk said he would stop taking bitcoin as payment due to environmental concerns. Ether jumped 6.7%.

Looking at the day ahead now, and data releases include US housing starts and building permits for April, UK unemployment data for March, and the second estimate Q1 GDP in the Euro Area. Central bank speakers include BoE Governor Bailey and Deputy Governors Broadbent and Ramsden, the ECB’s Villeroy and the Fed’s Kaplan. Finally, earnings releases include Walmart and Home Depot.

Market Snapshot

S&P 500 futures up 0.4% to 4,172.50

STOXX Europe 600 up 0.33% at 443.8

MXAP up 1.7% to 204.56

MXAPJ up 1.7% to 684.94

Nikkei up 2.1% to 28,406.84

Topix up 1.5% to 1,907.74

Hang Seng Index up 1.4% to 28,593.81

Shanghai Composite up 0.3% to 3,529.01

Sensex up 1.3% to 50,231.13

Australia S&P/ASX 200 up 0.6% to 7,065.98

Kospi up 1.2% to 3,173.05

German 10Y yield rose 0.2 bps at -0.113%

Euro up 0.5% to $1.2215

Brent Futures up 0.8% to $70.01/bbl

Gold spot up 0.1% to $1,869.23

U.S. Dollar Index down 0.41% to 89.79

Top Overnight News from Bloomberg

The surge in commodities prices is failing to trigger some of the traditional responses in bonds and currencies. Unlike recent commodities rallies in 2008 and 2011, yields on Treasuries and currencies of major exporters like Australia have barely budged. Likewise, the Federal Reserve’s favored measure of inflation expectations has disconnected from moves in raw materials

There’s currently no risk of a lasting return of inflation in the euro area even as the outlook for economic growth improves, European Central Bank Governing Council member Francois Villeroy de Galhau says

Germany’s top court rejected bids to enforce its controversial 2020 ruling on the ECB’s PSPP program with more orders against the Bundesbank and the nation’s government

Almost every day for the past week, in the European morning a chunky buyer of Eurodollar futures has shown up. Assuming the trades are new positions, the recent slide in USD Libor has the trades mostly coming good so far

In a world awash with U.S. currency, the premium for lending dollars in funding markets is disappearing as investors turn elsewhere for positive yields

A look at global markets courtesy of Newsquawk

Asian equities traded mostly positive as the region shrugged off the negative lead from Wall Street where sentiment was dragged lower by lingering inflationary concerns and following somewhat mixed NY Fed Manufacturing data, while US equity futures also staged a rebound after-hours. ASX 200 (+0.6%) was underpinned as the mining-related sectors benefitted from the continued strength in underlying commodity prices and amid reports that Australian PM Morrison is pushing states to remove domestic restrictions on vaccinated citizens as part of a plan to boost travel freedom. Nikkei 225 (+2.1%) notched firm gains with the index unfazed by the wider than expected contraction in Japan’s Q1 GDP which printed -1.3% vs exp. -1.2% Q/Q and -5.1% vs exp. -4.6% for the annualized reading. The decline in the world’s 3rd largest economy was widely anticipated due to the state of emergency for nearly a dozen prefectures including Tokyo which lasted for almost the entirety of Q1, although there was also plenty of jawboning from Economic Minister Nishimura who stated the decline was smaller than during last year's state of emergency as spending on durable goods was solid and that the economy still has potential to recover with exports continuing to increase due to the overseas recovery. Furthermore, Nishimura suggested that job and income conditions are improving, consumer spending appetite appears strong and that the government will take flexible action including using reserves set aside to address the virus as required. Hang Seng (+1.4%) and Shanghai Comp. (+0.3%) were varied whereby the mainland lagged despite a lack of direct catalysts, but there were reports that the US Senate voted overwhelmingly to open the debate on the bill that would provide USD 110bln for technology research to address China competition, while the TAIEX (+5.2%) was the outperformer in an aggressive resurgence from yesterday’s COVID-triggered slump. Finally, 10yr JGBs languished amid strength in Japanese stocks and following the recent pullback in T-notes, while the lack of BoJ purchases also contributed to the subdued demand with the central bank only in the market today for treasury discount bills.

Top Asian News

Vodacom, Alibaba Look to Boost South Africa Sales With Super- App

China’s Neusoft Medical Said to Mull $400 Million Hong Kong IPO

Citi Hires 650 Wealth Professionals in Hong Kong, Singapore

India Seeks to Defer Prompt LNG Deliveries as Virus Curbs Demand

Major bourses in Europe have drifted off best levels but still hold onto modest gains (Euro Stoxx 50 +0.4%) amid a distinct lack of catalysts throughout the European morning and as earning seasons simmers down. US equity futures meanwhile hold onto a bulk of overnight gains but have lost momentum as Europe wanes alongside a pickup in the EUR. Bank of America’s May Fund Manager survey suggested the first signs of “peak optimism” on growth, whilst tech stocks overweight is at a three-year low as investors load up on resources and banking names, whilst suggesting that the most prominent tail risks include inflation and a taper tantrum. Back to Europe, major bourses largely see broad-based gains with some mild outperformance in the FTSE MIB (+0.7%) and AEX (+0.7%) with the former lifted by banks and the latter underpinned by its tech exposure. In fitting with this, Tech and Banks reside as top performers, but Oil & Gas and Basic Resources outpace amid price action in those respective complexes (see commodities section). Meanwhile, the Telecoms sector is the marked laggard following its outperformance yesterday as Vodafone (-10%) and Iliad (-9.0%) shares slump after earnings underwhelmed. Healthcare resides at the bottom of the pile, pressured by Novartis (-0.8%) after the US supreme court rebuffed the Co’s appeal over its arthritis drug. Overall, the sectors are portraying a pro-cyclical bias. In terms of individual movers, BT (+1.8%) bucks the telecoms trend amid reports its CEO has purchased another GBP 2mln worth of shares, whilst Vivendi (+1.7%) is also firmer on the back of news that it could offload a further 10% of its Universal Music Group business.

Top European News

German Top Court Rejects Bids to Enforce ECB PSPP Ruling

ECB’s Villeroy: No Inflation Risk, Monetary Policy to Stay Loose

U.K. Ministers Stuck in Talks Over Australia Trade Deal

Watch Food Delivery Stocks on Report DoorDash Plans German Entry

In FX, the Greenback has now given up all and more of its post-US CPI recovery gains amidst almost universal declines and a resumption of the bear trend that was prevalent prior to last Wednesday’s inflation data. Indeed, the DXY has fallen to a new sub-90.000 multi-month low at 89.751 to expose the only remaining trough ahead of 89.500 from late February (89.677 on the 25th of that month) and before Buck bears train crosshairs on the current 2021 trough (89.206 from January 6). The negative narrative for the Dollar remains the same and is compounded by renewed strength in commodities on the ROTW reopening bandwagon, bar recent/latest COVID-19 outbreak hotspots, as vaccine rollouts catch up to the US, while the Fed continues to hold back on tapering and policy normalisation in contrast to other Central Banks that have started the process of removing pandemic levels of accommodation. Ahead, housing data and more from Fed hawks Bostic and Kaplan, but it’s hard to imagine anything that might turn the tide for the index and Greenback in general at present.

CHF/NZD/AUD/EUR/GBP - Not much to pick between the best performing majors, or the ones extracting most from Buck’s downfall to be more precise. However, the Franc and Kiwi are just about edging it relative to fellow G10 currencies and perhaps in quid pro quo fashion following heavier depreciation when the boot was on the other foot, with the former up over 0.8975 and latter back above 0.7250, albeit facing formidable option expiry interest between 0.7260-70 in 1.4 bn before attention switches to NZ PPI later today. Conversely, the Aussie appears to have pulled far enough away from 1.2 bn expiries at the 0.7750 strike to probe 0.7800 irrespective of yet another set of dovish RBA minutes overnight ramming home the no rate hike likely before 2024, at the earliest. Elsewhere, the Euro has breached 1.2200 and Pound has climbed beyond 1.4200, as the single currency and Sterling tussle either side of the 0.8600 handle in cross terms.

CAD/JPY - The major ‘laggards’, though the Loonie continues to set almost daily highs against its US rival and has been close to 1.2000 as the clock ticks down to Canadian CPI tomorrow, while the Yen has rallied through 109.00 even though Japanese Q1 GDP and Capex fell short of expectations and subsequent coronavirus restrictions will take more toll on the economy.

SCANDI/EM - Somewhat conflicting impulses for the Nok as Brent finally overcomes resistance to scale Usd 70/brl, but Norway’s trade surplus narrows to leave the Crown under 10.0000 vs the Eur, while the Try has given up post-Turkish holiday corrective gains in stark contrast to the rest of the community that are reaping rewards of strength in underlying crude, metals and raw material prices plus Usd weakness and relatively buoyant risk sentiment overall. Note also, the Brl could well get an extra fillip from Brazilian Federal tax revenues beating consensus by some distance in March.

In commodities, WTI and Brent July contracts have been choppy but ultimately firmer, with Brent topping USD 70/bbl (vs low 69.44/bbl) alongside the European cash open in what seemed to be a tech-driven move at the time, whilst WTI tested USD 67/bbl to the upside (vs low 66.24/bbl). News flow for the complex has again been on the lighter side, with eyes remaining on the fallout of COVID across the globe, whilst geopolitical risks also remain heightened. Meanwhile, the private inventory data later today will be followed for any hints towards tomorrow’s DoEs, which is expected to be distorted by the Colonial Pipeline outage. As a reminder, a significant draw is expected in PADD1 (East Coast) product stocks alongside builds in crude and products from PADD3 (US Gulf Coast) and a decline in refining activity. Elsewhere, spot gold and silver see sideways trade as upside from softer Dollar is countered by elevated yields. LME copper meanwhile eyes USD 10,500/t to the upside with the aid of risk appetite alongside the weaker Dollar. On this front, BHP sees a rise in average copper production over the next five years of over 300k tonnes per year and predicts that there will be strong demand in steel-making as the world decarbonises. Overnight, Dalian iron ore and Shanghai zinc surged, with traders citing robust domestic demand and expectations for overseas demand to rise significantly.

US Event Calendar

8:30am: April Building Permits MoM, est. 0.6%, prior 2.7%, revised 2.3%

8:30am: April Housing Starts MoM, est. -2.1%, prior 19.4%

8:30am: April Building Permits, est. 1.77m, prior 1.77m, revised 1.76m

8:30am: April Housing Starts, est. 1.7m, prior 1.74m

DB's Jim Reid concludes the overnight wrap

Yesterday I hinted at the need for fresh knee surgery. Well today I’m putting out a public health announcement in the hope that I save others. About 2 months ago I felt tightness and swelling at the back of my knee one morning as I started on my exercise bike. There was no specific catalyst or pain. 2 months later, and with my knee constantly swollen, the scan revealed a hole in my cartilage. There were only two things that could have caused it. Speed swing training for golf or trampolining with the kids. When I cited these two things to my consultant on Friday I fully expected him to blame golf and tell me I had to take it easier at my age. However when I said the word trampolining he looked at me in horror and said if there was one thing he would rip out of every garden that has one it would be a trampoline. He said he’s treated nearly as many of these injuries as he has skiing ones. My kids were devastated over the weekend when I told them that I had to officially retire from bouncing them on the trampoline. This is an extended list that now includes running, tennis, football and cricket. Secretly I was very relieved that golf hadn’t caused it though. So full throttle with that while I decide when to have microfracture surgery for a second time and on a different knee. This will involve 6 weeks on crutches with no weight bearing and then rehab. Sigh. So next time your kid asks you to bounce them give it a second thought.

Markets are bouncing around at the moment without quite working out what to do about the onslaught of important data since payrolls. Net net, 10yr yields are c.8.3bps higher since just before that employment report and the S&P 500 and Nasdaq are down -1.64% and -2.71% respectively. So although there have been some big daily moves in the opposite direction we’ve generally seen small risk off at the same time as higher yields over this period.

Yesterday saw a similar trend alongside a rebound in commodity prices that only served to bolster the existing inflationary pressures argument. In terms of the moves, the S&P 500 (-0.25%) and Europe’s STOXX 600 (-0.05%) both fell back by the close of trade, with technology stocks underperforming in both regions as the NASDAQ fell a larger -0.38%. This coincided with higher volatility, with the VIX index up +0.9pts to 19.7pts, though this was some way beneath the intraday high of 28.93 reached on Thursday of last week. Energy stocks were more buoyant with the S&P energy sector gaining +2.30% and the STOXX 600 Oil and Gas sector up a lesser +0.38%, aided by the fact that WTI oil prices were up +1.38% to just about reach a post-pandemic high of $66.27/bbl.

The market moves came as yesterday’s Fed speakers continued to strike their overall dovish tone, as well as their belief that the inflationary pressures seen will prove temporary. In terms of tapering, Vice Chair Clarida said that the weak jobs report in April demonstrated that “we have not made substantial further progress” that the Fed needs to see in order to begin that process. This message was also reiterated by Atlanta Fed President Bostic, who said that “We are still 8 million jobs short of where we were pre-pandemic. Until we make substantial progress to close that gap, I think we have got to have our policies in a very strongly accommodative situation or stance”.

Against this backdrop, US Treasuries were fairly steady yesterday, with the 10yr yield seeing a modest +2.0bps rise to 1.649%. The rise was driven by inflation expectations with the 10yr breakevens increasing +2.6bps to 2.56% - a new 8 year high. The moves were similar in Europe, where yields climbed to fresh pandemic highs as nervousness over ECB tapering and higher inflation remained in the background. 10yr bunds saw yields rise +1.4bps to -0.12%, which is their highest level in almost 2 years, while French OATs were up +2.7bps to 0.289%, their highest level in over a year themselves. The risk-off tone meant that bunds outperformed their counterparts across the continent, with the Italian (+2.0bps) and Spanish (+1.6bps) spreads over bunds both moving wider. The taper story is gathering some momentum here. Elsewhere the greenback fell -0.17% for its 6th daily loss in its last 8 sessions and is now trading near three month lows.

Asian markets are mostly trading higher this morning with the Nikkei (+2.24%), Hang Seng (+1.25%) and Kospi (+1.07%) all posting gains. Chinese markets are trading a bit more mixed though with the CSI (-0.16%) and Shenzhen Comp (-0.06%) down while the Shanghai Comp (+0.08%) is up. Meanwhile, Taiwan’s TAIEX exchange is up as much as +4.96% as the country’s financial stabilisation fund said it was monitoring stocks after the worst rout in more than a year. Futures on the S&P 500 (+0.23%) are also pointing towards a positive open for nowalongside the Stoxx 50 and Dax futures being up +0.68% and +0.55% respectively. In terms of overnight data, Japan’s preliminary 1Q21 annualised GDP print came in at -5.1% qoq (vs. -4.5% expected) while the previous quarter was revised down to 11.6% qoq from 11.7% qoq. In other news, Variety reported that Amazon is in discussion to buy MGM movie studio for about $9bn. Small change for a company worth $1.65tn.

In other market news, Bitcoin rose +1.63% bouncing as it reached a 3-month low, closing at $44,816. That’s just the second gain in the last week for the cryptocurrency after a variety of tweets from Elon Musk, including a new one yesterday where he clarified in a fresh tweet that “Tesla has not sold any Bitcoin”. Companies exposed to cryptocurrencies struggled yesterday, with Coinbase down -4.07% as it caught up with the moves over the weekend. Tesla was down another -2.34% and is now down -34.7% from its peaks in late-January and -18.3% YTD.

In terms of the pandemic, cases continue to decline at the global level with the number of new cases in India also having now peaked for the time being. But other areas have experienced a renewed surge, particularly in Asia, and fresh restrictions were being imposed yesterday to deal with this. In Singapore, the Ministry of Health said that they’d found a further 21 cases, of which 11 weren’t linked to existing clusters. It comes as the World Economic Forum announced that they were cancelling their annual meeting that had been scheduled to be held in Singapore, saying that it would instead happen in the first half of 2022, at a location to be determined. Given I was planning to attend I’ve recommended the Bahamas. Meanwhile, Hong Kong moved to classify Singapore as a high-risk virus destination, and will now require a 21-day quarantine for arrivals from the city-state. Elsewhere, a flareup in Taiwan saw them ban foreigners from entering for a month from May 19 until June 18. However, there was better news out of the US, where John Hopkins data showed that Sunday saw the lowest number of new cases since March 2020, at the start of the pandemic. President Biden announced that the US will send an additional 20 million vials of vaccine abroad by the end of June. The shots will be a mix of Pfizer, Johnson & Johnson and Moderna vaccines, and will be on top of the 60 million Astrazenca shots that have already been promised.

There wasn’t a great deal of data out yesterday, thoughthe New York Fed’s Empire State manufacturing survey for May fell slightly to 24.3 (vs. 23.9 expected). Notably however, the prices paid index rose to an all-time record of 83.5, as did the prices received index at 37.1, so adding to those signs of building inflationary pressures. Separately, the NAHB’s housing market index for May remained at 83 as expected.

To theday aheadnow, and data releases include US housing starts and building permits for April, UK unemployment data for March, and the second estimate Q1 GDP in the Euro Area. Central bank speakers include BoE Governor Bailey and Deputy Governors Broadbent and Ramsden, the ECB’s Villeroy and the Fed’s Kaplan. Finally, earnings releases includeWalmartandHome Depot.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}