Uncategorized

Futures, Global Markets Rise As Yields Drop Ahead Of PCE Data

Futures, Global Markets Rise As Yields Drop Ahead Of PCE Data

US stock futures, European bourses and Asian markets all rose, while the 10-year…

Share this:

US stock futures, European bourses and Asian markets all rose, while the 10-year Treasury yield traded near a three-week low and the USD eeked out its first gain of the week as traders reacted to a modest improvement in China's mfg PMI and looked ahead to Thursday's PCE data and Friday’s jobs report. At 7:45am ET, S&P futures rose 0.25% to 4,535 while Nasdaq 100 futures reversed earlier losses. Europe’s Stoxx 600 benchmark stayed in the green, buoyed by record profits at UBS as a result of its emergency takeover of Credit Suisse. Commodities are stronger led by oil and metals with natgas and wheat the biggest laggards. Today’s macro data focus includes jobless claims, income/spending and the PCE Deflator. Chicago PMI, expected to rise to 44.2, may point to a stabilization in mfg. Tomorrow we cap off the week with NFP.

In premarket trading, the retail rout continued with Dollar General plunging more than 13% after the company cut its 2024 net sales and profit forecast; Chewy also fell 5.3% as analysts say the pet products company’s customer growth disappointed in the second quarter amid macro uncertainties. Evercore ISI downgraded its rating. Okta jumped 11% after it reported second-quarter results that beat expectations and raised full-year forecast. Analysts highlight improvement in margins and the company’s sales strategy. Here are some other notable premarket movers:

- Arista Networks gains 2.3% after Citi upgraded the communications-equipment company to buy from neutral, citing an expected 400G cloud spend recovery into next year.

- CrowdStrike climbed 1.4% as it again delivered strong results with consistent execution and outperformance across metrics, analyst Matthew Hedberg says he likes the continued momentum and the opportunity to consolidate security spend, seeing this as a building tailwind.

- Palantir declines 4% after Morgan Stanley cut its rating, saying that near-term optimism about the AI product cycle and valuation premium make for an “unfavorable risk-reward.”

- Salesforce rises 5.6% after the software firm reported second-quarter results that beat expectations and gave an outlook that is seen as strong.

- Shopify’s US shares rise 5.6% after Amazon announced an app integration to allow merchants to offer Buy with Prime on Shopify stores.

- UGI jumps 7.3% after the natural gas and electric power distribution company said its board is reviewing strategic alternatives to unlock shareholder value.

- Victoria’s Secret falls 5.3% after the lingerie retailer’s second-quarter results fell shy of estimates and it forecast a sales decline ahead.

Sentiment was modestly boosted after China’s NBS PMIs showed that Manufacturing came in at 49.7 (up from 49.3 in Jul and ahead of the Street’s 49.2 forecast) and Manufacturing new orders back in expansion mode for the first time in 5 months; on the other hand, Non-Manufacturing ticked down to 51 (down from 51.5 in Jul and below the Street’s 51.2 forecast).

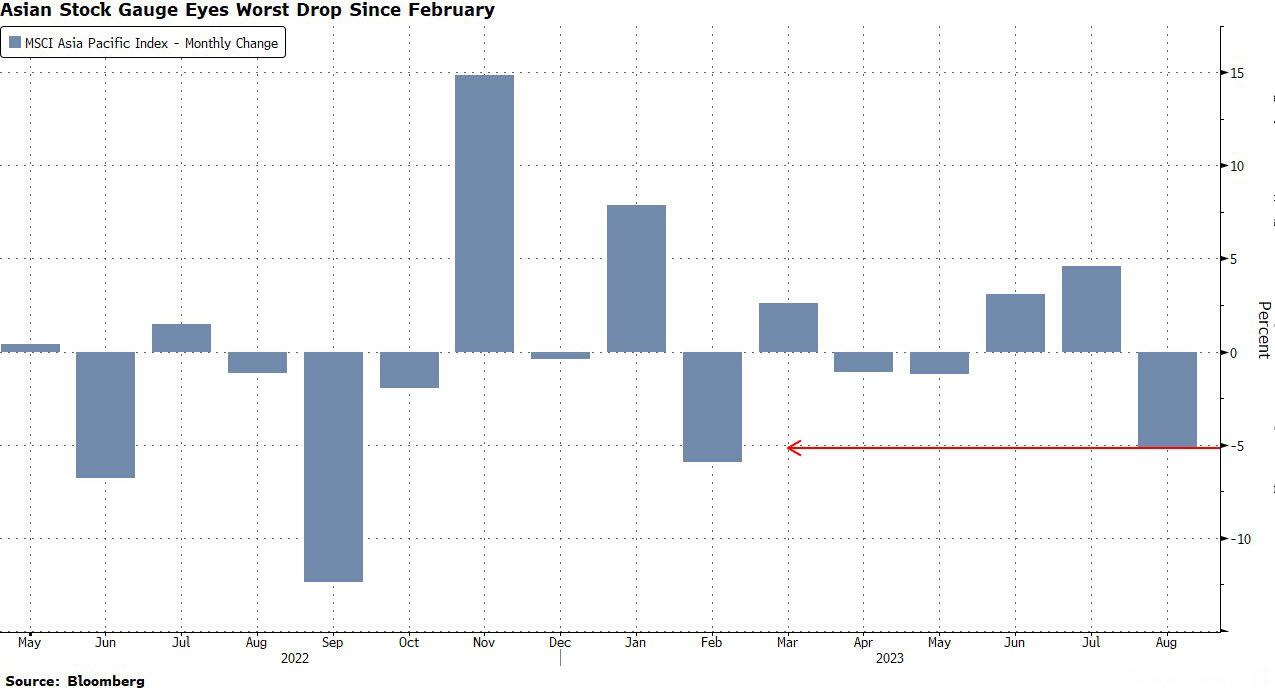

The S&P 500 was headed for the worst month since February, while the Nasdaq 100 is set for the largest decline this year. Asian and global stocks are also on pace for the biggest monthly losses since February.

Traders are closing out the month with economic data and China’s bruised markets center stage. Thursday’s mixed moves come after stocks and bonds pared their August losses in the past week. US jobless numbers picked up slightly to 235,000 according to economists polled by Bloomberg ahead of initial claims data due Thursday. Friday’s non-farm payrolls are seen at 170,000 in August versus 187,000 in July, while hourly wage growth is predicted to slow slightly. Weaker-than-expected economic numbers supported predictions for the Fed to ease back on interest-rate hikes on Wednesday.

“The big market catalyst we’re looking for in September is the Fed meeting,” Hugh Gimber, global market strategist at JPMorgan Asset Management, said by phone. “Tomorrow’s payrolls data will be hugely relevant for that meeting. Without a slowdown in wages, a soft landing is impossible.”

European stocks were higher with the Stoxx 600 rising 0.4%. The financial services, retail and real estate sectors are leading gains. The euro dropped 0.5% versus the dollar as euro-zone inflation stopped slowing in August, according to data on Thursday. That presents European Central Bank officials with a quandary as they weigh the possibility of tighter policy against signs of flagging growth. Here are the biggest European movers:

- UBS shares climb as much as 7.2% to their highest level since October 2008 after the bank posts 2Q net income of $29 billion, bolstered by negative goodwill from Credit Suisse acquisition

- Rockwool rises as much as 6.5%, making it the biggest gainer on Europe’s Stoxx 600 index, after the Danish insulation firm increased its guidance for the second time in two months

- Dormakaba shares soar as much as 13%, most since April 2015, after the Swiss access and security company reported Ebitda for the full year that beat average estimates

- Grafton shares rise as much as 3.5% as analysts highlight optionality from the UK construction and materials company’s strong balance sheet, as evidenced by a new share buyback

- Pernod Ricard falls as much as 5.3%, the most in more than a year, after the maker of Absolut Vodka reported results that were hit by negative FX effects and said it expected a “soft” quarter ahead

- Eiffage drops as much as 2.6% after the construction and concessions company delivered 1H results which Jefferies describes as “soft,” highlighting an increase in net debt and a miss on profit

- Adevinta shares fall as much as 2.7%. The Norwegian classifieds company said on an earnings call its German vehicle marketplace may merely see “more normal” growth rates going forward

- Recticel shares slumped as much as 15% after the Belgian company’s first-half earnings missed estimates due to challenging conditions in the European construction markets

- Ion Beam Applications plunged 15%, the most since March 2020, after the Belgian medical technology company reported first-half earnings that analysts say were below expectations

Earlier in the session, Asian stocks were mixed, heading for their worst monthly drop since February, as the rally in Chinese equities faltered amid worries about growth and the property crisis in Asia’s largest economy.

The MSCI Asia Pacific Index erased earlier gains of as much as 0.4% to trade little changed. Benchmarks in Japan and Singapore rose, while those in South Korea, Taiwan and Australia were lower. Equities in mainland China were set to extended their losses for another session after factory output contracted again, with the onshore stock benchmark poised for its biggest monthly decline since October. Gauges in Hong Kong fluctuated.

After suffering most of August on China’s growth concerns, the main Asian stock benchmark was on course for about a 5% drop this month, even after the recent recovery in Chinese stock markets helped narrow the loss. Equities rebounded earlier this week on the mainland following Beijing’s latest steps to shore up investor confidence in capital markets on Sunday but the rally lost steam after mid-week.

- Japan's Nikkei 225 saw mild gains although the machinery sectors were in the red following the dire Japanese industrial output data, with a Japanese government official highlighting a decline in demand both domestically and abroad, with output falling in several areas including production machinery.

- Australia's ASX 200 was flat on either side of 7,300 as the gains in the Telecoms and Financial sectors were offset by losses in Energy and Consumer Staples.

- Stocks in India posted their biggest decline this week, weighed by a regional selloff. Investors will look forward to release of quarterly GDP data due after close of markets. The S&P BSE Sensex fell 0.4% to 64,831.41 in Mumbai, while the NSE Nifty 50 Index declined 0.5%, their biggest single-day declines since Aug. 25. For the month, the gauges fell more than 2.5% each, their first retreat since February. The selloff in India has come on the back of rising worries over inflation and insufficient rains in many regions.

Asian stocks have been driven by “a combination of what’s happening in the US macro cycle and what’s happening in the Chinese macro cycle,” as well as the “ongoing AI bubble,” Mixo Das, Asia equity strategist at JPMorgan Securities, said in an interview with Bloomberg TV.

In FX, the Bloomberg Dollar Spot Index rose to session highs and after falling as much as 0.2% earlier. The yen rose the most among the Group-of-10 currencies. The greenback is likely to be “somewhat” volatile over the data release as PCE is the Fed’s preferred inflation measure, said Richard Grace, a senior currency analyst at InTouch Capital Markets Pte. “The market appears to still trying to work out the recent pattern of stronger-than-expected US economic data for a number of weeks, and now a pattern of weaker-than-expected US economic data for a number of days”

The euro fell as traders bet the ECB will hold off on raising rates next month, even as recent data shows inflation is still running above target. The repricing in ECB rates comes after policymaker Isabel Schnabel highlighted the mounting risks to growth and said she can’t say how long rates will remain in restrictive territory. “If the weakness we have seen so far is not enough to bring inflation down, the economy needs to weaken even more,” said Athanasios Vamvakidis, head of G-10 FX strategy at Bank of America. “That’s the main concern for the euro.” AUD/USD rose 0.2% to 0.6488, paring an earlier rise of as much as 0.5%.

In rates, treasuries held small gains in early US trading, paced by UK and euro-zone bond markets, with yields mostly inside Wednesday’s ranges. TSY yields are lower across the curve by 1bp-3bp; Wednesday’s ranges included lowest levels in more than two weeks for all benchmarks except the 30-year. Month-end index rebalancing at 4pm will extend its duration by an estimated 0.12 year as Treasuries issued during the month are added. Bunds are higher while the euro has extended declines as traders seem to focus on the slowdown in euro-area core inflation rather than the headline rate which held steady. Market pricing now suggests a less than 30% chance the ECB raises rates in September, down from ~40% before the data. German 10-year yields are down 5bps at 2.49% while two-year yields drops 9bps. The US economic calendar includes weekly jobless claims and July personal income and spending at 8:30am New York time and August MNI Chicago PMI at 9:45am. Focal points of US session include personal income and spending data that includes PCE deflator, Fed’s preferred inflation gauge, and month-end index rebalancing.

In commodities, Brent crude oil advanced for a third day with WTI rising 0.5% to trade around $82. Spot gold rises 0.1%.

Bitcoin was under modest pressure holding around the USD 27k mark within fairly narrow ranges above the figure. Pressure which eminates from the firmer USD in European trade.

Looking to the day ahead now, and data releases include the Euro Area flash CPI print for August, as well as the unemployment rate for July. In the US we’ve got the weekly initial jobless claims, PCE inflation for July, and the MNI Chicago PMI for August. From central banks, we’ll hear from the Fed’s Bostic and Collins, ECB Vice President de Guindos and the ECB’s Schnabel, and the BoE’S Pill. We’ll also get the ECB’s accounts of their June meeting. Finally, earnings releases include Lululemon, Dollar General and Broadcom.

Market Snapshot

- S&P 500 futures up 0.1% to 4,529.00

- MXAP little changed at 161.98

- MXAPJ down 0.4% to 507.25

- Nikkei up 0.9% to 32,619.34

- Topix up 0.8% to 2,332.00

- Hang Seng Index down 0.5% to 18,382.06

- Shanghai Composite down 0.6% to 3,119.88

- Sensex down 0.2% to 64,966.59

- Australia S&P/ASX 200 up 0.1% to 7,305.27

- Kospi down 0.2% to 2,556.27

- STOXX Europe 600 up 0.3% to 460.38

- German 10Y yield little changed at 2.52%

- Euro down 0.3% to $1.0886

- Brent Futures up 0.2% to $85.99/bbl

- Gold spot up 0.2% to $1,945.26

- US Dollar Index up 0.23% to 103.39

Top Overnight News

- China’s NBS PMIs are mixed for Aug, with Manufacturing coming in at 49.7 (up from 49.3 in Jul and ahead of the Street’s 49.2 forecast) and Manufacturing new orders back in expansion mode for the first time in 5 months, but Non-Manufacturing ticked down to 51 (down from 51.5 in Jul and below the Street’s 51.2 forecast). RTRS

- Chinese president Xi Jinping is not planning to attend the G20 leaders’ summit in New Delhi next weekend and is expected to be replaced by the country’s premier, according to western officials briefed on the situation. FT

- Toyota Motor seeks to shatter its production record this year, aiming to manufacture 10.2 million vehicles globally, the Nikkei has learned, and cross the eight-figure milestone for the first time. Nikkei

- Europe’s CPI in Aug szx mixed, with headline running hot at +5.3% Y/Y (unchanged vs. Jul and above the Street’s +5.1% forecast) while core was +5.3% (down from +5.5% in Jul and inline w/the Street). BBG

- UBS soared to the highest since 2008 after it posted the biggest-ever quarterly profit for a bank and CEO Sergio Ermotti said inflows are climbing across the board. The bank sees positive underlying pretax profit in the second half and will cut about 3,000 jobs as it targets cost savings of $10 billion by end-2026 from its takeover of Credit Suisse. BBG

- The EU’s agriculture chief has proposed that the EU subsidize the cost of transiting Ukrainian grain through the bloc after Russia pulled out of an initiative to allow exports via the Black Sea. FT

- Fed’s Bostic warns that US monetary policy should avoid overtightening (“I think we should be cautious and patient and let the restrictive policy continue to influence the economy, lest we risk tightening too much and inflicting unnecessary economic pain”). BBG

- Facing the prospect of a politically damaging government shutdown within weeks, House Speaker Kevin McCarthy is offering a new argument to conservatives reluctant to vote to keep funding flowing: A shutdown would make it more difficult for Republicans to pursue an impeachment inquiry against President Biden, or to push forward with investigations of him and his family that could yield evidence for one. NYT

- Visa and Mastercard are planning to increase credit-card fees. The changes could result in merchants paying an additional $502 million annually in fees, according to a consulting company. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mostly negatively following a marginally positive handover from Wall Street, which saw an equity bid underpinned by dovish US economic data. ASX 200 was flat on either side of 7,300 as the gains in the Telecoms and Financial sectors were offset by losses in Energy and Consumer Staples. Nikkei 225 saw mild gains although the machinery sectors were in the red following the dire Japanese industrial output data, with a Japanese government official highlighting a decline in demand both domestically and abroad, with output falling in several areas including production machinery. Hang Seng and Shanghai Comp varied at the open but later succumbed to losses, whilst Baidu soared 4.6% after winning Chinese approval for its AI model. The Mainland was more cautious from the start following mixed PMI data which saw Manufacturing topping expectations but remaining in contraction.

Top Asian News

- Baidu (BIDU/9888 HK) is reportedly among the first firms to win China approval for AI models, according to Bloomberg. Baidu rolled out its Chat GPT-rival AI app to the public, according to a statement cited by AFP

- PBoC said it will continue to step up loans to private firms and will use stocks and bonds to deal with risks of private property developers in a prudent way, according to Reuters. PBoC added it will encourage and guide institutional investors to buy bonds of private firms and will support IPO and refinancing of private firms.

- PBoC injected CNY 209bln via 7-day reverse repos with the rate at 1.80% for a CNY

- The Japanese government cut its assessment of industrial production and noted industrial output is seesawing, according to Reuters.

- Japanese government official on industrial output said demand fell both domestically and abroad in July, and noted that output fell in many areas including production machinery. The official said the decrease in chip manufacturing machinery is due to weak demand abroad, the outlook appears to be severe; chip shortage is easing in autos, which is on a steady recovery, according to Reuters.

- Japanese government official said the electronics device market in China is in a severe state; Domestic material industries are partially affected by China's real estate concerns, according to Reuters.

- BoJ Board Member Nakamura said the BoJ must patiently maintain easy policy for the time being, and need more time to shift to monetary tightening; Japan's economy is no longer in deflation; tweaks to policy must be cautious. Was not against making YCC flexible, opposition was re. timing. July decision was not part of any exit from ultra-loose policy. BoJ will closely watch impact on Yen moves on economy and prices. FX is not driven by interest rate differentials alone.

- Japanese PM Kishida said to be considering lifting the minimum wage to JPY 1500/hr by mid 2030s, via NHK.

- Japan's major five banks are to increase housing loan interest rates by 0.1% to 0.2%, according to Jiji News.

- Fitch affirms China at A+, outlook stable; revises lower 2023 China GDP Growth forecast to 4.8% (prev. 5.6%).

European bourses are modestly firmer, Euro Stoxx 50 +0.1%, having trimmed initial upside throughout a session of significant Central Bank updates. Downside which has occurred despite a dovish-shift to pricing for the ECB post-HICP & Schnabel; within Europe, Real Estate leads the sectors while Banking names lag as both areas of the economy take impetus from yield action. Though, the Banking pressure is offset somewhat by marked upside in UBS +4.5% post-earnings; SAP modestly firmer after CRM earnings, CRM +5.5% in pre-market. Stateside, futures are mixed around the unchanged mark with some slight underperformance in the NQ -0.1% ahead of key data and despite the broader European-driven yield action.

Top European News

- ECB's Schnabel says outlook for the Euro Area remains highly uncertain, activity has moderated visibly, and forward-looking indicators signal weakness ahead. Cannot predict where the peak rate is going to be, or for how long rates will have to be held at restrictive levels, cannot commit to future actions. Within the remarks, Schnabel is very balanced and holds open the door for a hike or a skip at the September gathering. For reference, the remarks were published pre-HICP

- ECB's Holzmann says August inflation data is a conundrum for the ECB; we are not yet at the highest level for rates, another hike or two is possible. ECB should consider needing PEPP reinvestments before the end of next year. Based on current data, would not exclude a rate hike in September but hasn't made mind up yet. Much closer to terminal rate but likely not there yet. Remarks published after the HICP data

- BoE's Pill says the UK faces second-round inflation effects and inflation is too high, cases for caution on inflation despite the declines in the headline. There is a lot of policy in the pipeline to come through. There is the possibility of doing too much when it comes to the fight against inflation. Policy needs to be sufficiently restrictive for long enough.. Adds, one option for policy is to hold rates steady for longer; tends to favour that approach.

- UK PM Sunak is expected to announce a new Defence Secretary to replace Ben Wallace on Thursday, according to government officials cited by the FT. Grant Shapps is a surprise frontrunner for the role, according to insiders.

FX

- DXY rebounds firmly from 103.000 to 103.550, while Euro reels from 1.0939 to 1.0865 vs the Buck after mixed EZ data and less hawkish remarks from ECB's Schnabel.

- Yen relishes softer yields as it continues consolidation against Greenback either side of 146.00 irrespective of mixed Japanese macro releases.

- Sterling buffeted as BoE's Pill warns against complacency on inflation given second round effects, but backs a steady for longer strategy rather than overtightening.

- Cable wanes around 1.2700 pivot, EUR/GBP eases from 0.8598 towards 0.8560.

- PBoC sets USD/CNY mid-point at 7.1811 vs exp. 7.2765 (prev. 7.1816)

- China's major state-owned banks seen selling USD in onshore spot foreign exchange market; Banks spotted swapping CNY for USD in onshore forwards market, via Reuters citing sources.

- Brazil's 2024 Budget Law revenue measures will reportedly reach BRL 168bln, according to Estadao sources. The revenue package will consider ending the deductibility of Interest on Equity for all sectors.

Fixed Income

- Bonds approaching month end on the up, but not before overcoming several wobbles.

- Bunds towards top of 132.87-131.83 range and perhaps latching on to soft EZ core inflation and less hawkish vibes from ECB's Schnabel.

- Gilts also bid between 95.28-94.66 parameters as BoE's Pill states preference for a longer period of steady rates rather than overtightening.

- T-note more restrained within 111-00/110-24+ confines awaiting PCE, IJC, Fed's Collins and Chicago PMI.

- Following the European data and ECB speakers, pricing for a 25bp hike at the September meeting has dropped to a 30% probability from over 60% in recent sessions.

- UK DMO intends to hold 15 Gilt auctions between October-December, and a syndicated sale of a new long-dated conventional in November.

Commodities

- Crude benchmarks are a touch firmer on the session with specific details light as we await an update from the BSEE on how much, if any, production has been lost due to Hurricane Idalia.

- Gas markets are bid but off highs while spot gold is little changed and torn between the softer risk tone and stronger USD.

- For Ags., Reuters citing Turkish sources reported that President Erdogan is to meet Russia President Putin in Sochi on September 4th to discuss Ukraine and the grain deal. As a reminder, earlier in the week reports indicated that the nation's Foreign Ministers are to speak in today’s session as Turkey looks to bring Russia back to the Black Sea grain deal.

Geopolitics

- US approves first arms to Taiwan under foreign aid program, according to AFP citing an official.

- US reportedly restricts the export of some AMD (AMD) chips to Middle Eastern countries, according to Reuters sources.

- North Korea conducted full-force command training in response to the SK-US joint exercise, according to Yonhap.

- Japanese PM Kishida has requested top LDP lawmaker Nikai to visit China to resolve the Fukushima water issue, according to local press.

- Australia and EU to resume free-trade deal talks on Thursday via teleconference, a month after the sides failed to reach a deal, according to Reuters.

US Event Calendar

- 07:30: Aug. Challenger Job Cuts 266.9%; YoY, prior -8.2%

- 08:30: Aug. Initial Jobless Claims, est. 235,000, prior 230,000

- Continuing Claims, est. 1.71m, prior 1.7m

- 08:30: July Personal Income, est. 0.3%, prior 0.3%

- Personal Spending, est. 0.7%, prior 0.5%

- Real Personal Spending, est. 0.5%, prior 0.4%

- 08:30: July PCE Deflator MoM, est. 0.2%, prior 0.2%

- PCE Deflator YoY, est. 3.3%, prior 3.0%

- PCE Core Deflator MoM, est. 0.2%, prior 0.2%

- PCE Core Deflator YoY, est. 4.2%, prior 4.1%

- 09:45: Aug. MNI Chicago PMI, est. 44.2, prior 42.8

DB's Jim Reid concludes the overnight wrap

Markets had plenty to chew on yesterday, as the latest round of data offered support to both sides of the hard vs soft landing debate. We again had some underwhelming US releases which suggested that growth and inflation were slowing further which could be used to support either side of the debate. However for yesterday the soft landing argument continued to win out with yields on 10yr Treasuries (-0.7bps) inching down to a 3-week low of 4.11% and the S&P 500 (+0.38%) hitting a 3-week high. But in Europe, markets saw a clear underperformance thanks to resilient inflation numbers from Germany and Spain, which added to speculation that the ECB might deliver a 10th consecutive rate hike next month.

With the conflicting releases, all eyes are now on tomorrow’s US jobs report to see if that can shift the narrative one way or the other. Our US economists are expecting nonfarm payrolls to slow down further to 150k, and yesterday we had some further evidence of a softening labour market from the ADP’s report of private payrolls. That showed growth of +177k in August (vs. +195k expected), which is the smallest gain since March. On top of that, there was a continued slowdown in pay growth, with the rate among job-changers down to +9.5% year-on-year, which is the slowest since June 2021, whilst the rate among job-stayers fell to the slowest since September 2021, at +5.9%.

That ADP report came just before the second estimate of Q2 GDP growth, which indicated that the economy was a bit weaker than previously thought. For instance, overall growth came in at an annualised rate of +2.1%, which was down from the initial estimate of +2.4%. And more promisingly for the Fed, both PCE and core PCE for Q2 were each revised down a tenth, with the latest estimate putting them at +2.5% and +3.7% respectively.

These indications of a slowing economy led to a fresh rally among US markets. The main reason for that is because expectations of another rate hike from the Fed have continued to come down, and now stand beneath 50% for the first time since last week. So bad news on the economy is still being treated as good news (for now), since optimism about fewer rate hikes is outweighing the prospects of slower growth. In turn, that led to a rally among US Treasuries, although one that lost steam during the day with yields on 2yr Treasuries (-1.0bps) and 10yr Treasuries (-0.7bps) down only a little by the close. The 2yr yield had traded as much as -6bps lower shortly after the US data in the morning. As discussed, equities put in another decent performance as well, with the S&P 500 (+0.38%), advancing for a 4th consecutive session. On a sectoral basis, it was tech stocks that led the advance once again, and the NASDAQ (+0.54%) hit a 4-week high.

Over in Europe it was a rather different story, since the latest data suggested that inflation was proving more resilient than expected. In particular, the German flash CPI print for August only fell back to +6.4% on the EU-harmonised measure (vs. +6.3% expected). At the same time, Spanish inflation ticked up three-tenths to +2.4%, whilst Irish inflation was also up three-tenths to +4.9%. That sets the stage for the Euro-Area wide print this morning, which is out at 10am London time. Following yesterday’s prints, our European economists see both the headline and core inflation prints coming in at between +5.3% and +5.4%. This would represent a near stable headline reading (+5.3% prev.) and a slight easing in core (+5.5% prev.).

Those CPI numbers led to growing expectations that the ECB might proceed with another hike at their next decision in two weeks’ time. Indeed, market pricing is now suggesting a 55% chance of a 25bp hike at the September meeting, so back up to its level prior to the underwhelming flash PMI data last week. It also led to a significant underperformance among European sovereign bonds, with yields on 10yr bunds (+3.4bps), OATs (+3.7bps) and BTPs (+4.4bps) all moving higher on the day, whilst the STOXX 600 fell -0.15%. The big concern now is that the European outlook is looking increasingly stagflationary, with inflation remaining stubborn whilst there’s few signs of growth either. On the topic of European inflation, our economists yesterday published the results of their latest dbDIG consumer survey, which has shown an uptick in inflation expectations during July and August. See their note here.

Overnight in Asia, several equity markets have lost ground this morning, which follows the release of the official PMIs from China. They showed that manufacturing contracted for a fifth consecutive month, with a 49.7 reading but it was higher than the 49.2 reading expected by the consensus, and above the 49.3 reading in June. However, the non-manufacturing PMI fell a bit more than expected to 51.0 (vs. 51.2 expected).

Against that backdrop, most of the major indices have struggled this morning, with declines for the CSI 300 (-0.54%), the Shanghai Comp (-0.53%), the KOSPI (-0.36%) and the Hang Seng (-0.26%). The main exception is in Japan, where the Nikkei (+0.80%) and other indices including the TOPIX (+0.79%) have seen a decent advance this morning. That comes amidst better-than-expected retail sales data overnight, which grew by +2.1% in July (vs. +0.8% expected). That said, industrial production fell by -2.0% (vs. -1.4% expected).

Looking at yesterday’s other data, there were further signs of resilience in the US housing market, as pending home sales unexpectedly grew by +0.9% in July (vs. -1.0% expected). That said, the July data was before the most recent rise in mortgage rates into August, and separate data from the MBA yesterday showed that the 30yr average fixed rate remained at 7.31% in the week ending August 25.

To the day ahead now, and data releases include the Euro Area flash CPI print for August, as well as the unemployment rate for July. In the US we’ve got the weekly initial jobless claims, PCE inflation for July, and the MNI Chicago PMI for August. From central banks, we’ll hear from the Fed’s Bostic and Collins, ECB Vice President de Guindos and the ECB’s Schnabel, and the BoE’S Pill. We’ll also get the ECB’s accounts of their June meeting. Finally, earnings releases include Lululemon, Dollar General and Broadcom.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Stock indexes are breaking records and crossing milestones – making many investors feel wealthier

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire