Futures Fly To All-Time High On Quad Witching Day

Futures Fly To All-Time High On Quad Witching Day

Tyler Durden

Fri, 12/18/2020 – 08:01

Normally, "quad-witching" option expiration days tend to be volatile affairs resulting in bursts of volatility and occasionally aggravated downside for…

Share this:

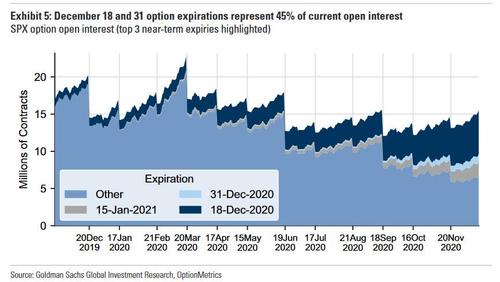

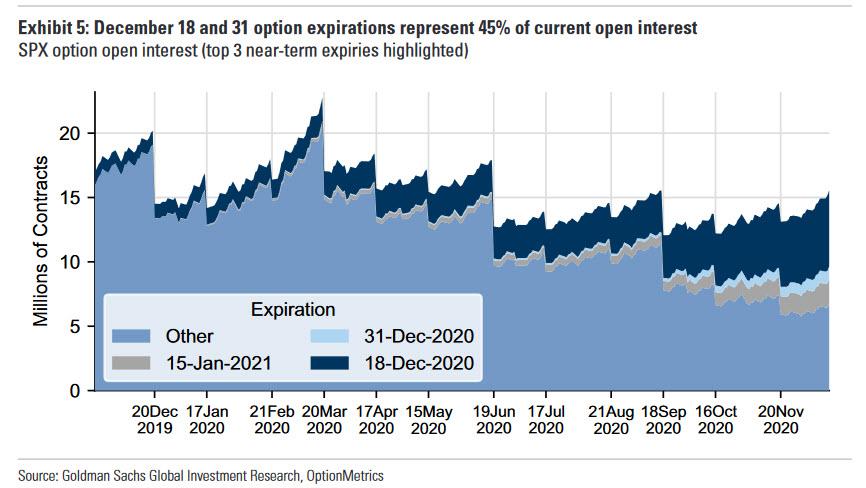

Normally, "quad-witching" option expiration days tend to be volatile affairs resulting in bursts of volatility and occasionally aggravated downside for risk assets. Today's quad-witch, however, will not be one of those days because while some 45% of outstanding SPX option open interest - totaling more than $2.5tln of notional - expires, the concentration of strikes is below the current spot level and will thus have limited potential gamma impact, as we noted yesterday.

And since what won't go down must come up in these bizarro markets, Emini futures hit a new all time overnight, up 5.00 points, or 0.18%, to 3,718 despite fresh US-China tensions following a Reuters report that the US is preparing to blacklist Semiconductor Manufacturing International Corp. and dozens of other Chinese companies, while little progress was made on a federal spending deal in Washington; ironically, the latest dismal retail sales data and unemployment claims were seen as good news as they bolstered the case for further stimulus. The dollar rose for the first day in five.

Wall Street indexes were set to end the week sharply higher, with the Nasdaq set to outperform its peers with a 3.1% gain on sustained buying into technology stocks. Notable premarket movers included Microsoft, which dropped 0.5% after the company said it found malicious software in its systems related to a massive hacking campaign disclosed by U.S. officials this week. FedEx fell 2.8% after the package delivery company again declined to give an earnings forecast for 2021, even as its quarterly profit almost doubled. Shares of rival UPS also declined 0.9%. Centene Corp dropped 1.3% after the health insurer forecast 2021 adjusted profit below Wall Street estimates, as it said enrollment in its Obamacare plans was not coming in as expected. Meanwhile, retail stocks including Kohl’s, Walmart and Macy’s rose between 0.5% and 2.6% after the National Retail Federation said over 150 million American shoppers could buy holiday gifts in stores or online this year on the last Saturday before Christmas, or “Super Saturday,” up by more than 2 million from last year.

With just days left to renew pandemic aid, leaders in Washington are pressured to resolve their differences after months of deadlock amid signs of a faltering economic recovery. A bipartisan U.S. stimulus deal “appears to be close at hand,” Senate Majority Leader Mitch McConnell said, but will probably require work over the weekend to get through Congress, Bloomberg reported. The stimulus package “ought to be a sufficient bridge,” Steven Wieting, global investment strategist at Citigroup Private Bank, said on Bloomberg TV. “That along with at this stage a preparedness for this Covid emergency and the fact that vaccines are ahead by mid-year, would certainly be sufficient to get us through this period of weakness.”

European shares faded early gains amid doubts over a post-Brexit trade deal. The pan-European STOXX 600 index rose 0.1%, hitting a fresh 10-month high with Spain's IBEX lagging, down 0.6%. Losses in UK’s exporter-heavy index were limited by a slide in the pound after Britain and European Union negotiators warned that they remained far apart on a number of issues and that it was becoming more likely they would fail to reach an agreement. Travel & leisure stocks were the biggest decliners in early European trading, with British Airways-owner IAG slipping 1.0% after a media report that it had agreed to buy Spanish carrier Air Europa for 500 million euros. European shares were mixed even as Germany's IFO beat handily on both current conditions (91.3, exp.89.0) and expectations (92.8, exp. 92.0).

Earlier in the session, Asian stocks traded lower to close the week as shares in Australia and New Zealand slumped. Even so, the regional stock gauge was headed for a seventh straight weekly advance, the longest run since January. A cluster of Covid-19 infections in Sydney’s northern beaches stoked investor caution, causing Australia’s benchmark gauge to slip 1.2%. Qantas Airways fell 3.5% as travel names dropped. New Zealand’s benchmark was dragged lower by A2 Milk, which plunged after cutting its revenue guidance due to reduced sales to Chinese tourists and students. Japan’s Nikkei 225 fell 0.2% as the central bank left policy unchanged. Data showed the country’s key consumer prices slid at the fastest pace in 10 years in November. Meanwhile, the Shanghai Composite fell 0.3% even as some companies affected by a U.S. executive order rallied on an FT report that the Treasury is seeking to water down the investment ban. The MSCI Asia Pacific Index fell 0.5% as investors took profit ahead of the weekend on continued political wrangling in Washington

In rates, Treasuries were little changed as US trading begins, and off session highs. Small gains during Asia session were erased in London trading amid gains for European stocks and US futures that pushed S&P 500 E-minis to new highs. The 10-year yield was at ~0.935%, near the high end of 0.88%-0.95% weekly range and more than 3bp higher on the week during which S&P 500 rose to record highs; bunds lag by ~0.5bp while gilts outperform by more than 2bp. Gilts outperformed after U.K.’s chief Brexit negotiator said progress on a trade deal is blocked and time running out. Bunds bear flatten, 10y yields ~1.2bps higher and roughly a half basis point cheaper to treasuries. Peripheral spreads widen: 10y BTP/Bund spread widens 2.2bps near 113bps. Semi-core trades marginally tighter.

In FX, the Bloomberg dollar index remained in the green but faded all of Asia’s gains. Sterling fell against all G-10 peers and neared $1.35, after Britain’s chief Brexit negotiator, David Frost, warned progress in the talks has been “blocked and time is running out”; euro slipped 0.2% after Germany reported its biggest-ever jump in coronavirus infections. Be it a hard Brexit deadline on Sunday or not, options pricing suggests the pound is in for a volatile session on Monday, with forward implied overnight volatility standing above 20%, according to Bloomberg data. The Australian dollar declined as Sydney scrambled to contain an outbreak of Covid-19.

In commodities, Crude futures trade a narrow range. WTI 0.3% lower near $48.20, Brent off 0.4% near $51.30. Spot gold drifts around Asia’s worst levels. Base metals post small gains, with LME copper outperforming. Copper topped $8,000 a ton for the first time in more than seven years on rising demand and supply bottlenecks.

Looking at the day ahead, we get the November leading index from the US. We’ll also get a monetary policy decision from the Central Bank of Russia.

Market Snapshot

- S&P 500 futures up 0.09% to 3,724.50

- STOXX Europe 600 up 0.1% to 397.80

- MXAP down 0.5% to 196.43

- MXAPJ down 0.5% to 648.77

- Nikkei down 0.2% to 26,763.39

- Topix up 0.04% to 1,793.24

- Hang Seng Index down 0.7% to 26,498.60

- Shanghai Composite down 0.3% to 3,394.90

- Sensex up 0.1% to 46,937.81

- Australia S&P/ASX 200 down 1.2% to 6,675.47

- Kospi up 0.06% to 2,772.18

- Brent Futures down 0.2% to $51.39/bbl

- Gold spot down 0.3% to $1,879.89

- U.S. Dollar Index up 0.2% to 89.98

- German 10Y yield rose 1.5 bps to -0.555%

- Euro down 0.1% to $1.2253

- Brent Futures down 0.2% to $51.39/bbl

- Italian 10Y yield rose 0.3 bps to 0.429%

- Spanish 10Y yield rose 2.9 bps to 0.058%

Top Overnight News from Bloomberg

- German businesses are hopeful that Europe’s largest economy will pick up in the first half of next year

- China said talks with the European Union on a bilateral investment deal are in the final stages

- The U.S. is preparing to blacklist Semiconductor Manufacturing International Corp. and dozens of other Chinese companies, Reuters reported

- The Bank of Japan unexpectedly pledged to review the sustainability of its stimulus without totally overhauling its main policy framework, hours after data showed consumer prices falling at the fastest pace in a decade

- Copper topped $8,000 a ton for the first time in more than seven years, pointing to the start of a new commodities super- cycle as supply-side investment falls short of an expected surge in demand

A quick look at global markets courtesy of NewSquawk

Asian equity markets traded cautiously as momentum from the fresh record levels on Wall Street where sentiment was underpinned by stimulus hopes, failed to resonate in the region heading into the weekend and amid unresolved US stimulus and Brexit talks. ASX 200 (-1.2%) was pressured as tech and financials led the descent and with a cluster of infections in Sydney prompting states to impose border curbs, while investor appetite was also bruised by heavy losses in Mesoblast which slumped 35% after poor results in its Remestemcel-L trial for the treatment of acute respiratory distress syndrome related to COVID-19 and with QBE Insurance suffering after it flagged an FY loss of around AUD 1.5bln. Nikkei 225 (-0.2%) was also lacklustre but with downside stemmed by a mixed currency and tentativeness amid the BoJ policy decision in which the central bank maintained its main policy settings and but extended corporate funding measures for COVID-stricken firms as expected. Hang Seng (-0.7%) and Shanghai Comp. (-0.3%) were uninspired after another tepid PBoC operation and mixed newsflow with EU said to have agreed in principle for an investment treaty with China, although there were also reports the US issued a new ban to prohibit electric utilities that supply critical defense facilities, from importing certain power system items from China and that the Trump administration is set to add dozens of Chinese companies including SMIC (981 HK) to the Commerce Department's entity list today. Finally, 10yr JGBs were lacklustre with prices remaining near support at the psychological 152.00 level and after the BoJ provided very few surprises.

Top Asian News

- U.S. to Blacklist Dozens of Chinese Firms, Incl. SMIC: Reuters

- Tencent Group Buys Further 10% of Vivendi’s Universal Music

- BOJ Calls for Review to Tweak Policy as Price Falls Deepen

- Sony Pulls Cyberpunk From PlayStation Store After Outcry

European equities (Eurostoxx 50 +0.3%) trade with modest gains after opening on a softer footing, in what has been a session void of incremental macro newsflow. Many of the same themes remain at the forefront of investor sentiment as markets await updates on Brexit, the passage of COVID relief in the US and the progress of vaccination efforts. It’s worth highlighting that today is quadruple witching day (full schedule available on the newsquawk calendar/headline feed) and as such this could stoke some volatility throughout the session. Additionally, today marks the last trading day before Tesla is added into the S&P 500 on December 21st and as such, funds that track the S&P 500 will need to purchase the stock at today’s closing price in order to track the index. In an interview with CNBC, Bleakley Advisory Group’s Boockvar stated “it’s probably going to be one of the biggest market on close buy orders of all time”. Back to Europe, most sectors trade firmer, albeit modestly so with telecoms and chemicals leading, whilst travel & leisure, retail & banks lag in what has been a morning lacking in noteworthy stock-specific updates. Looking further ahead to 2021, Deutsche Bank strategists expect that European equities will catch up to US peers and have set an end-2021 target of 450 which would imply upside of 14%, compared to its 7% gain pencilled in for the S&P 500.

Top European News

- Wienerberger Boosts U.S. Business With $250 Million Deal

- Barnier Gives Johnson Fishing Ultimatum as Brexit Reaches Climax

- Philips Buys BioTelemetry for $2.8 Billion in Cardio Push

- PPG to Buy Tikkurila in $1.4 Billion Deal to Tap Nordics

In FX, no obvious reaction to the BoJ that was bang in line with expectations on all counts, but the Yen has treated further from pre-policy meeting peaks vs the Dollar and other G10 peers perhaps taking some note of Governor Kuroda’s reminder that currency moves are being closely observed rather than his contention that Jpy strength is not having a serious (adverse) effect on the Japanese economy. However, the sharp turnaround in Usd/Jpy to circa 103.60 from around 102.88 only yesterday also looks technical as tend-line support held at 102.75 on some charts. Meanwhile, Sterling has suffered a similar if not worse fall from grace as Brexit vibes turn decidedly more downbeat with the clock ticking down fast to the next EU deadline to strike a trade deal and big gaps still apparent on fishing rights mainly, but not solely. Hence, Cable has recoiled from 1.3600+ to probe bids/support at 1.3500 and Thursday’s base near 1.3490, while Eur/Gbp is almost 100 pips higher and eyeing 0.9100.

- NZD/AUD/CAD/DXY - The Kiwi is paring advances on the 0.7100 handle vs its US counterpart with no additional independent impetus via NZ trade data or lasting momentum from improvements in ANZ business sentiment and activity outlook, while the Aussie has lost 0.7600+ status amidst renewed coronavirus jitters after reports of a cluster of cases in Sydney, NSW. Elsewhere, the Loonie looks drawn to hefty option expiries at 1.2750 (1.1 bn) awaiting Canadian retail sales having reversed from yet another foray above 1.2700, and contributing to the broader Greenback recovery that has nudged the index back up to 90.000, albeit marginally and tentatively between 90.033-89.822 parameters.

- CHF/EUR - Holding up somewhat better than their major rivals, with the Franc clawing back some post-SNB losses across the board as Usd/Chf straddles and Eur/Chf slips back below 1.0850 even though the Euro remains elevated elsewhere in wake of a decent Ifo survey, though again mitigated by the timing of responses not to mention the fact that the COVID-19 situation in Germany appears increasingly bleak. Nevertheless, Eur/Usd is relatively resilient either side of 1.2250 where mega expiry interest lies (2.2 bn) after another approach towards 1.2275.

- SCANDI/EM - The Nok has not gleaned more traction from a lower than forecast Norwegian jobless rate and is back under 10.5000 vs the Eur after relatively hawkish Norges Bank rate projections pushed the cross down to almost 10.4900 yesterday, while the Rub has resumed its downward trajectory after no change in rates from the CBR and Mxn is also weaker after Banxico stood pat, both as expected. Conversely, the Try continues to recover on the back of CBRT reassurance about getting inflation back on track and ahead of December’s year end CPI survey estimate (12.47% previously).

In commodities, throughout the European morning, WTI and Brent have experienced some modest choppy price action given the movements associated with the approach to month/quarter/year end. Thus far, the session has been devoid of macro newsflow either generally or pertinent explicitly to the complex; as such, the benchmarks are currently in proximity to the unchanged mark on the session; posting ranges of around USD 0.40/bbl thus far. For the session ahead the only crude highlight is the weekly Baker Hughes rig count but more pertinently markets will be focused on the US fiscal narrative ahead of tonight’s shutdown narrative and as the near-term COVID-19 narrative remains downbeat going into the Christmas period. Turning away from oil and to metals where spot gold isn’t too differed on the session but has lost some allure as the DXY has marginally reclaimed 90.00, with the precious metal capped at USD 1886.84/oz at present; but, well within yesterday’s range of USD 1895/oz and USD 1861/oz.

US Event Calendar

- 8:30am: Current Account Balance, est. $187.0b deficit, prior $170.5b deficit

- 10am: Leading Index, est. 0.5%, prior 0.7%

DB's Jim Reid concludes the overnight wrap

I’m technically on holiday today but I don’t have much better to do at the moment so I’ll be doing a bit of admin on and off today before my 2 week break. So this will be the last EMR until early January. Peppa Pig World beckons on Monday!! Happy holidays from all of us on the team. Many many thanks for all your interactions, feedback and for reading in what has been a year like no other. Have as good a holiday season as you can. It’s fair to say there has been a big disconnect between life, the economy and asset markets in 2020. The authorities have done a remarkable job to ensure that. Only time will tell what the real cost of that achievement will be. Anyway as per normal before I step away I have listed, in order, my favourite TV programs of the year at the end today. One hour of TV a night can get you a long way.

Back to 2020 and one asset that won’t want to see the back of this year is Bitcoin. We’ve had a remarkable 48 hours in a remarkable year. It’s traded in a 22.1% range since 9am GMT on Wednesday and is 17.8% higher than that level as we go to print. It’s now up 221.2% on the year. We did a quick flash poll yesterday in CoTD as to where you think Bitcoin will end 2021. We’ll publish the results in addition to today’s CoTD. Please vote here . Thanks for all the responses so far.

Onto more mundane markets and equities hit more all-time/ post pandemic highs yesterday as optimism on a US stimulus deal, Brexit negotiations and Covid vaccinations proved strongly supportive for risk assets. In fact by the close, the S&P 500 (+0.58%), the NASDAQ (+0.84%) and the Dow Jones (+0.49%) had all climbed to record levels, while in Europe both the STOXX 600 (+0.30%) and the DAX (+0.75%) had also reached their highest points since the pandemic began. Other risk assets were similarly buoyant, with Brent Crude (+0.82%) and WTI (+1.13%) ascending to post-pandemic highs as well, while the reflation trade showed further signs of gathering pace as 10yr US breakevens rose to 1.95%, their highest level since April 2019. US 10yr Treasury yields themselves rose +1.7bps to 0.933%.

As we are about to go to print, Reuters is reporting that the US is set to blacklist 80 companies, nearly all from China, including SMIC. Asian markets had already given back some of yesterday’s global gains before the news but they are dipping further now with the Nikkei (-0.23%), Hang Seng (-0.96%), Shanghai Comp (-0.51%), Asx (-1.20%) and India’s Nifty (-0.27%) all down while the Kospi (+0.15%) is up. S&P 500 futures are down -0.30% too. In keeping with the slight risk off, the US dollar index is up +0.22% and yields on 10yr USTs are back down -1.7bps to 0.917%.

Before this slight reversal, one thing that likely helped the reflation trade yesterday was the positive developments in the US stimulus talks. While it is not likely the agreement will be done today, Senate Majority Leader McConnell and a White House spokesman separately said that Congressional leaders are close to a final deal. If there is no deal today, the US government would technically “shutdown”, having run out of funding at midnight tonight, but the Senate may pass yet another continuing resolution to get through the weekend and the vote on the stimulus bill.

According to Bloomberg reports, the current bill framework is around $900bn with $600 of direct payments for individuals, $300-per-week in supplemental unemployment insurance payments and separate aid for small businesses, as well as about $17 billion for airlines. The bill does not include aid to state and local governments or lawsuit liability protection, both of which have held up talks for weeks.

Recent data has focused minds a bit. Indeed yesterday the weekly initial jobless claims came in worse than expected for a 2nd week running, up to a 3-month high of 885k in the week through December 12. In a sign that many on both sides seem to agree that a bill will get passed in short order, Democrats and Republicans already started talking about the chances for more stimulus in the early days of the Biden Administration. GOP Senator Thune acknowledged that the chances that the Biden White House seeks more stimulus, “probably depends on what happens in Georgia.” That race is on Jan.5, which means the EMR will be back just in time to cover it.

Overnight, the BoJ has kept its monetary policy settings unchanged while extending its special COVID programs by 6-months. However to conclude, the BoJ did announce a policy sustainability review and said that "The Bank will conduct an assessment for further effective and sustainable monetary easing, with a view to supporting the economy and thereby achieving the price stability target of 2%." Further, the central bank said that it saw no need to change its yield-curve-control policy framework with quantitative easing as part of the review and added that it would likely announce the findings in March. The review came as the November CPI came in at -0.9% yoy (vs. -0.8% yoy expected) indicating that the prices are falling at the fastest pace since August 2010.

In other overnight news, the SCMP has reported that China and the EU have reached an ‘in principle’ agreement on a bilateral investment deal, the Comprehensive Agreement on Investment.

Back to markets and although the dollar has rallied a bit overnight, yesterday saw the dollar index fall to a fresh 2-year low, after experiencing another -0.69% slide in its 4th consecutive move lower. For context, the greenback now stands less than -1.37% away from its lows in early 2018, and if it broke through that point that would take us back to levels not seen since 2014. In turn, the dollar’s weakness helped other currencies breach recent records, with sterling climbing above $1.36 in trading for the first time since May 2018.

On Brexit, UK Prime Minister Johnson indicated talks with the EU are in a “serious situation” last night, warning that a deal will be impossible without the bloc softening their stances on fisheries. EC President von der Leyen tweeted she saw “substantial progress on many issues”, but that “big differences” remain between the two sides as negotiations are set to continue today. Fisheries surely can’t scupper a deal when everything else is slowly falling into place though. Stranger things have happened I suppose and overnight, Britain’s chief Brexit negotiator, David Frost, has warned via a tweet that progress in the talks has been “blocked and time is running out”. Sterling is trading down -0.44% at -$1.3525 but it seems as much on the back of a stronger dollar overnight.

Last-minute agreements have been a pattern of EU negotiations throughout recent years, as plenty of readers will remember with the sovereign debt crisis. The main news yesterday came from the European Parliament’s Conference of Presidents, who said in a statement yesterday that they were prepared to organise an extraordinary session towards the end of December, but so long as an agreement were reached by midnight on Sunday. In a tweet, Manfred Weber, who chairs the centre-right EPP group, said that after Sunday “we cannot reasonably scrutinize the deal before the end of the year. The agreement is too important to rush through Parliament.” This was followed by Cabinet Office Minister Gove telling the House of Lords that the ever-moving deadline for a deal will be the days following Christmas, with Parliament possibly being called in early to vote. If a deal were reached late in the day Sunday or afterwards, it is technically possible for it to be implemented provisionally pending full ratification without a vote in the European parliament, so long as the member states in the Council of the EU agreed.

Staying on the UK, yesterday saw the Bank of England leave its policy settings unchanged, in line with expectations. They said that the recent restrictions on activity had been tighter than they’d assumed in November, and were expected to weigh on Q1 growth, but also noted that the positive vaccine news and recent fiscal measures should support the economic rebound. The other main UK economic news came with the announcement that the furlough scheme would be extended an extra month until the end of April.

On the coronavirus, the main news was that French President Macron tested positive and has begun a 7-day isolation. More broadly however, a number of world leaders have also been sent into self-isolation by the news after meeting Macron in recent days, including Spanish PM Sanchez and European Council president Michel. There was some good vaccine news with Moderna’s vaccine candidate winning the backing of the US FDA advisers with a vote of 20-0 with 1 abstention, it is now expected that the agency will approve the vaccine in short order. Nevertheless, the case numbers have continued to deteriorate throughout the world and it seems the darkest days will still be coming before the vaccine dawn bursts through.

Finally, there weren’t a great deal of other data releases yesterday, though housing data from the US for November was somewhat better than expected, with housing starts rising to an annualised rate of 1.547m (vs. 1.535m expected), and building permits also coming in at an annualised 1.639m (vs. 1.560m).

To the day ahead now, data releases will include UK retail sales for November, the Ifo business climate indicator from Germany for December, and the November leading index from the US. We’ll also get a monetary policy decision from the Central Bank of Russia.

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

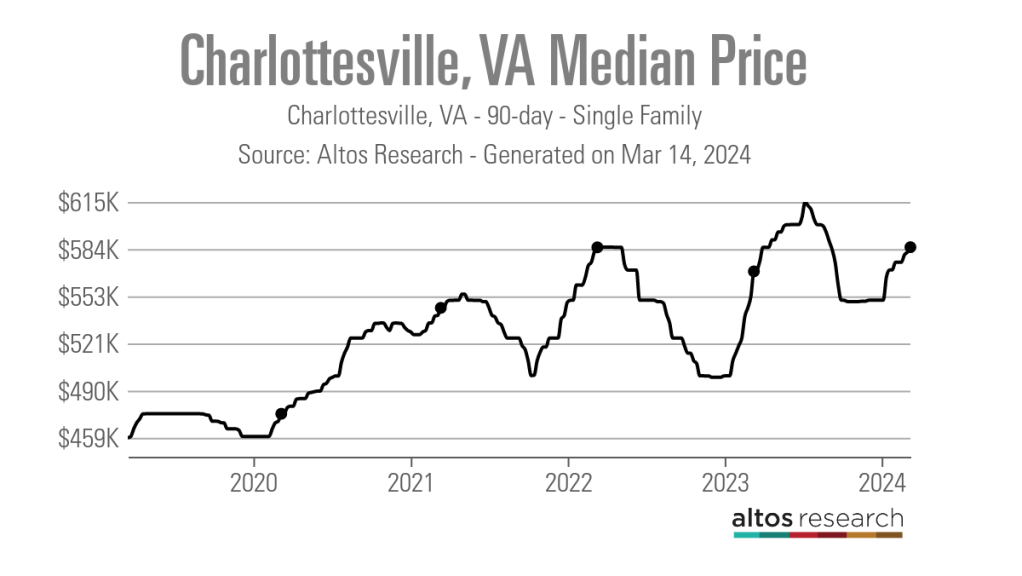

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest rates

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Key shipping company files for Chapter 11 bankruptcy

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

Part 1: Current State of the Housing Market; Overview for mid-March 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges