Futures Flat, Global Stocks Mixed In Thin Thanksgiving Trade Tyler DurdenThu, 11/26/2020 - 08:12

Global stocks held near record highs on Thursday, with US equity futures flat due to the Thanksgiving holiday while the rally in European stocks paused, as recent vaccine progress and hopes for further stimulus - whether monetary or fiscal - kept markets bullish.

While US cash equities are closed for the Thanksgiving holiday, S&P futures were flat after fading modest overnight gains, however Nasdaq futures were well in the green, as cyclical companies including banks and energy firms which have benefited the most from the post-vaccine surge retreated while more defensive tech shares gained.

Markets also took a boost from minutes from the latest Fed minutes which showed that officials discussed how the central bank’s asset purchases could be adjusted to provide additional support to the economy. The minutes said policymakers may give new guidance about its bond-buying “fairly soon”.

“2021 is going to be a year of economic catch-up,” said Samy Chaar, chief economist at Lombard Odier. “When you keep the pandemic contained and under control, economic activity catches up very quick.”

Recovery sentiment turned cautious Thursday, however, as the virus toll continued to rise in Europe and the U.S., leading German Chancellor Angela Merkel to call on Europe’s ski resorts to close this winter. The task of a global vaccination comes with logistical problems, all while the virus gains ground and economic recoveries wobble.

"Question marks still surround the speed of a global roll-out and the proportion of populations willing to be vaccinated," Geir Lode, head of global equities at the international business of Federated Hermes, wrote in a note to clients. “These factors, combined with a second consecutive week of rising jobless claims in the U.S,, appear to have brought the rotation into value and back-to-work stocks grinding to a halt for now."

"The market’s very much looking forward to 2021 and the time when vaccines will be rolled out and economic activity can get back to normal,” said Kiran Ganesh, a multi-asset strategist at UBS, adding that the equities rally is "particularly driven by the rotation trade away from large caps and towards small caps, away from the U.S. and towards Europe, and away from technology and towards some of the cyclicals."

The MSCI world equity index rose to a record high on Wednesday and held close to it on Thursday, up 0.1% on the day as markets shrugged off the latest rise in U.S. jobless claims. Global stocks are having their best month on record in November, boosted by a slew of positive vaccine announcements and hopes that Biden’s administration will deliver more economic stimulus and political stability.

Europe’s STOXX 600, which is also having its best month on record, up 14.4% in November, was down 0.1% on the day. European equities traded a narrow range in a quiet morning, with a few central bank speakers and minutes from the ECB’s October meeting the only scheduled events of interest. Gains in tech, travel and healthcare stocks were offset by losses in banks, oil & gas and autos. The UK's FTSE 100 and Spain's IBEX laged European peers. In France and Germany, consumer confidence plunged in November under new lockdown restrictions, challenging the idea of a quick return to normal in the euro zone’s two biggest economies. German Chancellor Angela Merkel told parliament that lockdown measures will be in place until at least the end of December and possibly longer.

Earlier in the session, Asian stocks gained, led by the communications and IT sectors, after falling in the last session. Most markets in the region were up, with Indonesia's Jakarta Composite advancing 1.4% and Thailand's SET rising 0.9%, while Australia's S&P/ASX 200 slid 0.7%. The Topix added 0.6%, with SoftBank and Nintendo contributing the most to the move. The Shanghai Composite Index rose 0.2%, driven by Ping An Insurance and Yangtze Power.

Emerging-market stocks resumed gains after a one-day drop, suggesting the remains intact even as trading slows due to the U.S. Thanksgiving holiday. The MSCI Inc. measure of developing-nation equities moved to within 50 points of its 2018 high, a level that was only surpassed before the global financial crisis. Foreign-exchange markets were mixed, with Asian currencies and the Turkish lira rising, while eastern European currencies and the South African rand fell

In rates, Treasury futures edged higher with the cash market closed, with traders off for Thanksgiving holiday in the U.S. A deluge of data on Wednesday brought the first back-to-back rise in weekly U.S. jobless claims since July and a widening trade deficit. In Europe, bunds and gilts bull-flattened gently while peripheral and semi-core spreads widened slightly to core, with Italy underperforming.

In FX, Bloomberg dollar index drifts higher, back into the green. NOK and SEK are the worst G-10 performers. EUR/USD fades an early push up to 1.1941, cable trades at the lows.

In crypto, Bitcoin plunged over 10% on the session amid a sudden bout of overnight selling.

In commodities, crude futures slumped with WTI dropping ~1.5% having failed to breach $46 overnight, Brent drops back on a $47-handle after running into resistance near $49 during Asian trade. Spot gold grinds higher near $1,814/oz. Base metals trade well, with LME copper outperforming

There is nothing on today's calendar with the US closed for holiday.

Top Overnight News from Bloomberg

Sweden’s central bank surprised markets with a bigger-than- expected expansion of its asset purchase program, amid signs the Covid crisis will do more damage to the largest Nordic economy than previously feared

Trillions of euros in spare cash sloshing through the euro zone have made it cheaper for investors to access funding for one week as opposed to one day for the first time

The U.K. Debt Management Office will continue selling inflation-linked debt tied to the flawed Retail Price Index even after plans were announced to move away from the benchmark, according to Chief Executive Officer Robert Stheeman

The European Central Bank should consider wiping out or holding forever the government debt it buys during the current crisis to help nations recover and restructure, a top Italian government official said

Chancellor Angela Merkel urged Germans to do more to rein in the coronavirus to avoid the “worst-case scenario” of an overburdened health care system

China’s imports of U.S. goods under the phase-one trade deal slowed last month after hitting a high in September, leaving the full-year target well out of reach

China will maintain normal monetary policy for as long as possible and keep macro leverage ratio basically stable, PBOC says in its quarterly policy implementation report

A more detailed look at Global Markets courtesy of NewsSquawk

Major European bourses see a mixed session thus far (Euro Stoxx 50 Unch) as the non-committal tone and holiday-thinned trade from Asia-Pac reverberates into Europe on US Thanksgiving. Sectoral performance have more of a defensive bias, with Healthcare, Utilities and Staples among the top gainer, whilst cyclicals reside at the bottom of the pile but IT bucks the trend. The oil and gas sector is the laggard as the crude complex pulls back following its recent rally ahead of next week's key energy meetings, whilst Financial names also sees losses on account of lower yields. Thus, UK's FTSE 100 (-0.6%) narrowly underperforms regional peers with its heavy-weight banking and energy names hampering performance. Travel & Leisure names continues to be underpinned on vaccine hopes, with easyJet (+2%) and Air France-KLM (+1.4%) trading firmer. In terms of individual movers, Volkswagen (-1.8%) sees more pronounced losses than some peers amid reports that the Co. and Audi are to face prosecution in India under charges of cheating & conspiracy.

A non-committal tone was evident for most of Asia-Pac trade following the indecisive lead from the US where stocks were rangebound heading into the Thanksgiving holiday and after a deluge of mixed data releases. ASX 200 (-0.7%) was led lower by an unwinding of yesterday’s outperformance in cyclicals and with sentiment clouded by frictions with Australia’s largest trading partner after China alleged there were environmental quality issues concerning Australian coal in which AUD 700mln worth is stuck on ships being delayed from entering and unloading at Chinese ports. Nikkei 225 (+0.9%) shook off the initial caution to outperform its regional peers on supportive measures with the Japanese government to extend its employment subsidy program until end-February and the virus loan application period to end-March, while KOSPI (+0.6%) was kept afloat after the BoK maintained its Base Rate at 0.50% as expected and upgraded its GDP growth forecasts for 2020 and 2021 as it anticipates an export-driven recovery. Hang Seng (+0.1%) and Shanghai Comp. (+0.2%) lacked firm direction with the mainland tentative amid ongoing trade uncertainty after the Trump administration granted ByteDance a new 7-day extension of the divestiture order directing it to sell to TikTok by December 4th, while the Peterson Institute for International Economics also noted that China total purchases of US goods during the first 10 months of the year, were less than half of the annual commitment under the Phase 1 deal.

In FX, hot on the heels of dovish FOMC minutes and ahead of the ECB account that is tipped to follow a similar path, the Riksbank has exceeded or confounded expectations by expanding and extending its QE remit by Sek 200 bn for an extra 6 months through the end of 2021. Two Board members entered reservations, but the accompanying statement and updated (downgraded) economic forecasts supported the policy action – see 8.30GMT post on the headline feed for full details and our snap analysis. Predictably, Eur/Sek rebounded in response from a low around 10.1200 to circa 10.1770 before paring back, albeit no more so in percentage terms than Eur/Nok between 10.5130-5740 parameters, as the Norwegian Krona tracks a retreat in crude prices.

DXY - The Dollar remains on the back foot in wake of, if not directly due to the aforementioned Fed release, as the Committee committed to provide further guidance on bond buying and could enhance stimulus via increasing the pace, moving down the curve or maintaining the size and current maturity profile, but continue purchases for a longer period. However, the index has survived another attempt to test y-t-d lows (91.740 from September 1st) and is trying to regain a foothold above the 92.000 handle within a 92.091-91.844 range in thin US Thanksgiving holiday trade.

JPY - Contrary to month end rebalancing models signalling a strong Greenback sell vs G10 counterparts, bar the Yen, Usd/Jpy is capped below 104.50 and a key Fib retracement level at 104.67, but the headline pair faces even bigger option expiry interest at the 104.00 strike (1.7 bn) ahead of the NY cut and more Japanese inflation data in the form of Tokyo CPI.

AUD/EUR/CAD/NZD/GBP/CHF - All narrowly mixed against the Buck and holding in fairly familiar ranges, with the Aussie reclaiming 0.7350+ status following mixed Capex data and Euro consolidating above 1.1900 having reached another new November pinnacle, but not able to breach 1.1950 in advance of the latest ECB minutes and remarks from chief economist Lane before Schnabel. Elsewhere, the Loonie pivoting 1.3000 without further impetus from oil awaiting rather stale Canadian average weekly earnings and the Kiwi is straddling 0.7000 after in line NZ trade data and reflecting on potential changes to the RBNZ mandate to incorporate house prices that are running hot. Meanwhile, Sterling is still eagerly and anxiously looking for Brexit updates, as Cable continues to hit a brick wall into 1.3400 where latest heavy offers are said to have been layered from 1.3390 through 1.3385 to 1.3380, and the Franc is hovering above 0.9100.

In commodities, WTI and Brent front month futures see a session of losses in what seems to be a retracement from the recent rally, which was fueled by optimism OPEC+ will extend current cuts despite the recent vaccine news lifting the outlook for the complex. News flow for the complex has remained light throughout early European hours, but source reports later on in the day cannot be dismissed given the preparatory OPEC meetings in the run-up to the main even at month-end. Market expectations (as things stand) are widely skewed towards the second tranche (7.7mln BPD cuts) being extended through Q1 2021, a view also backed by Goldman Sachs, ING and UBS, despite positive vaccine noise and amid rising production in Libya. Recent sources also noted OPEC+ are still leaning towards a rollover of the current tranche notwithstanding the recent oil price rally, with Russia likely to agree to this if necessary, however, enthusiasm for cuts is not universal. WTI briefly dipped below USD 45/bbl (vs. high 46.09/bbl), whilst Brent Feb hovers around USD 48/bbl after hitting resistance at USD 49/bbl. Elsewhere, spot gold and silver saw a bout of upside, albeit modest, heading into the European cash open amid thinned conditions and a distinct lack of newsflow. The precious metals have since waned off best levels with spot gold ~1815/oz (vs. low 1806/oz) whilst spot silver hit highs just shy of USD 23.50/oz (vs. low 23.19/oz)

DB's Jim Reid concludes the overnight wrap

Happy Thanksgiving to our US readers. Let’s hope you have better things to do than read this though. Ahead of the holiday, US equities fell back from their record highs on Tuesday as a deteriorating situation on the coronavirus and weak economic data served as a reality check to the surge in risk assets we’ve seen in recent days. By the close, the S&P 500 had fallen -0.16% and the Dow Jones was down a larger -0.58%, as the latest data showed weekly initial jobless claims in the US rose more than expected for a second week running, up to 778k for the week through November 21. Furthermore, data on personal income for October showed an unexpectedly large -0.7% fall (vs. -0.1% expected), which will add to fears that the US economy is losing momentum as the number of Covid-19 cases continues to rise throughout the country heading into the winter. Even as the equity rally took a pause, the VIX volatility index fell -0.4 pts to its lowest closing levels (21.3) since February 21. That was the initial Friday sell-off before the S&P 500 fell a further -33% over the next 21 trading sessions.

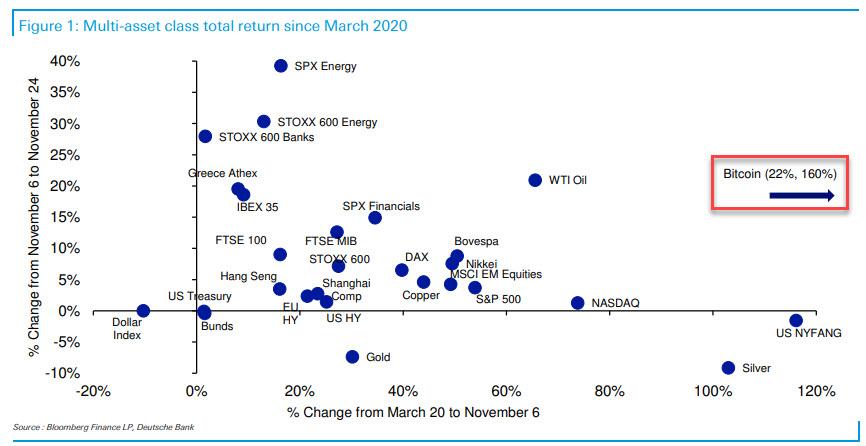

With the economic picture showing signs of weakness, big tech got a renewed bid again with the NASDAQ Composite +0.48% to reach its highest-ever closing level thanks to decent performances from Amazon (+2.15%), Apple (+0.75%) and Tesla (+3.35%). Even as tech outperformed yesterday, they still have massively lagged cyclicals over the past 2.5 weeks as our CoTD yesterday (link here) shows. The chart looks at a scatter of asset class and sector returns from after the Pfizer/BioNTech vaccine news against their returns from March 20th to November 6th. Energy and bank stocks of the top level sectors have led the charge post the vaccine news, even as they paused for breath yesterday.

Other safe havens showed signs of strength too, with core sovereign bonds in Europe rising as yields on bunds (-0.5bps) and gilts (-1.2bps) fell back, whereas their counterparts in southern Europe such as 10yr Italian (+0.3bps) and Greek (+1.7bps) debt rose. In equities, however, southern Europe outperformed the rest of the continent, with Italy’s FTSE MIB (+0.72%) and Spain’s IBEX 35 (+0.26%) both outperforming the STOXX 600 (-0.08%). On the other hand, yields on 10yr Treasuries (+0.2bps) rose slightly to 0.882%.

Asian markets are trading mostly higher this morning with a few indices at multi-year highs. The Nikkei (+0.88%), Hang Seng (+0.23%) and Kospi (+0.70%) are up while the Shanghai Comp (-0.01%) is flat and the ASX (-0.70%) is down. Futures on the S&P 500 are up +0.19% ahead of the holiday. Meanwhile, the BoK at its monetary policy decision today kept the interest rates unchanged while revising GDP forecasts upwards by 0.2pp for both this year and next. Elsewhere, Bitcoin is down -5.38% this morning following its spectacular run so far this year.

The minutes from the Federal Open Market Committee’s November 4-5th meeting were released last night. The committee viewed current asset valuations as “moderate” when taking low interest rates into account. The participants noted that “immediate adjustments to the pace and composition of asset purchases were not necessary” but, “they recognized that circumstances could shift to warrant such adjustments.” There was a more pertinent discussion of updating forward guidance on their bond-buying strategy “fairly soon”, ensuring that any additions in the Central Banks’ securities holdings would taper and end before the federal funds rate was raised. There was some discussion on the facilities that the Treasury department has since shut with officials at the meeting “emphasizing the important roles” the lending programs played “in restoring financial market confidence and supporting financial stability”. With these programs closed, the central bank could act more aggressively if financial conditions do worsen going forward.

In terms of the latest on the virus, it feels a little like summer again with case count news easing in Europe and worsening in the US. Yesterday, France’s 7-day running tally of infections fell to its lowest levels since October 9, while general hospitalisations and ICU usage continue to fall. Geneva and other Swiss cities are said to be reopening restaurants from December 10 onwards, while non-essential shops will reopen from this weekend. On the other hand, Germany has decided to extend its partial lockdown for at least 3 weeks to December 20 and has tightened restrictions on private gatherings. The German government has also indicated that they expect wide-ranging restrictions to stay in place until early January, particularly for restaurants and hotels. Meanwhile, New York saw its daily case numbers rise above 6,000 for the first time since April and California reported over 18,000 new cases, well over the 15,400 daily record from this past weekend. While mass gatherings have been largely discouraged by local governments, there still seems to be quite a bit of mobility ahead of today’s holiday and we will learn the impact of this in the first couple of weeks of December, just ahead of Christmas travel. Across the other side of world, South Korea reported 583 infections in the past 24 hours, the highest since March.

Here in the UK, the main headlines yesterday surrounded the government’s latest spending review, where the OBR forecast that the budget deficit in 2020-21 would climb to a peacetime record of 19% of GDP, while public sector net debt would reach 105.2% of GDP. Though the government was eager to advertise the funds being spent on infrastructure and tackling Covid-19, one of the key takeaways was the likely fiscal consolidation in the years ahead, with the announcements including a public sector pay freeze in 2021-22 and major cuts to the overseas aid budget. The UK is seemingly looking to fiscally consolidate, which is brave at this point but with no election for 4 years one can understand the political motivation. On Brexit, the OBR’s forecasts assumed that there would be a trade deal reached with a smooth transition to the new arrangements, but if there were a no-deal outcome, that could reduce real GDP next year by an extra 2% relative to their central forecast.

Speaking of Brexit, with just 5 weeks today until the transition period comes to an end, there’s still no sign of progress on the key issues in the trade negotiations. In a speech to the European Parliament yesterday, Commission President Ursula von der Leyen said that “I cannot tell you today, if in the end there will be a deal”, and although she said that there’d been “genuine progress” on a number of issues, the three usual stumbling blocks of the level-playing field, fisheries and governance remained. It’s still not obvious from where or from whom the compromises will come, and the BBC’s Europe Editor Katya Adler tweeted yesterday that EU sources had said that the talks weren’t going well. There is a story on Bloomberg this morning where the French foreign minister is accusing the UK of dragging its feet with Barnier apparently also suggesting there is little point in him coming to London unless the UK is prepared to give ground. So tension are mounting.

Wrapping up with yesterday’s other data, the second estimate of US GDP growth in Q3 was maintained at an annualised growth rate of +33.1%. Meanwhile, the preliminary October reading for durable goods orders showed a stronger-than-expected +1.3% rise (vs. +0.8% expected). US home sales rose to an annualised rate of 999k in October, which was actually slightly lower than the upwardly revised 1002k the previous month. And the University of Michigan’s final consumer sentiment index for November fell a tenth from the preliminary reading to 76.9, having been 81.8 the previous month.

To the day ahead now, and it’ll likely be a quieter one because of the Thanksgiving holiday in the US. Otherwise, we’ll get the minutes of the ECB’s October meeting, remarks from the ECB’s Lane and Schnabel, as well as the Euro Area’s M3 money supply data for October. There’ll also be a decision on interest rates from the Riksbank.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}