Futures Drop As Yields Push Higher, Hawkish ECB Looms

Futures Drop As Yields Push Higher, Hawkish ECB Looms

After yesterday’s bizarro rally, US futures and European bourses dipped ending two days…

Share this:

After yesterday's bizarro rally, US futures and European bourses dipped ending two days of gains, as yields reversed Tuesday's slide and climbed ahead of highly anticipated CPI data on Friday and a hawkish ECB meeting tomorrow, as traders try to predict the Federal Reserve’s policy path. Nasdaq 100 futures were flat at 7:30 a.m. in New York, with contracts on the S&P 500 and Dow Jones also modestly lower. European markets also dipped, with Credit Suisse shares tumbling after the Swiss bank announced that it expects a loss in the 2Q and is weighing a fresh round of job cuts. Meanwhile, Asian stocks rose as Beijing’s move to approve a slew of new video games bolstered bets that the outlook is improving for the Chinese technology sector. The yield on the 10-year US Treasury resumed its advance, climbing to 3%, while the dollar rose as the yen cratered to fresh 20 year lows, flat and bitcoin traded around $30K again.

Among notable premarket movers, energy companies’ extended their Tuesday gains with Imperial Petroleum rising 8.3% and Energy Focus adding 20%. Western Digital shares climbed 4.1% in US premarket trading after the chipmaker said that it’ll consider splitting its main units as part of a review of “strategic alternatives” following talks with activist investor Elliott. US-listed Chinese stocks jump in premarket trading, on track for a third day of gains, after China approved a second batch of video games this year, providing a signal of policy support to the the country’s internet sector; Alibaba (BABA US) gained 5.8%, JD.com (JD US) +4.4%, Pinduoduo (PDD US) +5.9%, Baidu (BIDU US) +2.7%. Other notable premarket movers:

- Intel (INTC US) shares fell 1.9% in premarket trading as Citi lowered its estimates on the chipmaker after the company’s management mentioned at a conference that circumstances are worse than expected during the quarter.

- Altria Group (MO US) stock slid 2.4% in premarket trading as Morgan Stanley downgraded it to underweight, citing increasing macro pressures and competitive risks.

- Western Digital (WDC US) shares rise 4.1% in premarket trading, after the chipmaker said that it will consider splitting its main units as part of a review of “strategic alternatives”.

- Smartsheet (SMAR US) stock fell about 7% in premarket trading as analysts said the software company delivered a mixed set of results with billings growth decelerating to top estimates by a slimmer margin than in previous quarters.

- Novavax (NVAX US) shares jump as much as 22% in US premarket trading after the company’s coronavirus vaccine won support from an FDA advisory panel.

- DBV Technologies ADRs (DBVT US) gain as much as 22% in US premarket trading after a trial for the biotech firm’s peanut allergy treatment met its primary endpoint.

Sentiment remains fragile on concerns rising rates will spark a recession as corporate earnings are set to slide. Thursday the ECB is set to wind down trillions of euros of asset purchases in a prelude to a rate hike expected in July that will mark the end of eight years of negative interest rates. "Higher yields will inevitably resume the pressure on valuations,” said Roger Lee, head of UK equity strategy at Investec Bank.

Inflation now exceeds 8% in the euro area, and is expected to stay above that level in the US when May data comes out on Friday, increasing pressure on central banks to stick to aggressive rate hikes. “Recent bouts of optimism can only be short-lived for now, as they were based on the wrong assumptions, that lower growth would push central bankers to ease their aggressive path,” Olivier Marciot, a portfolio manager at Unigestion SA, wrote in a report. Yet some argue that central banks will be forced back into dovish mode, among them hedge fund founder Ray Dalio. The billionaire said central banks across the globe will be required to cut interest rates in 2024 after a period of stagflation.

On Friday, focus will turn to the US CPI reading for hints on the Fed's tightening path following the central bank’s outsized hike on May 4. The data is expected to show inflation picked up from a month ago, but slightly slowed from a year earlier. Complicating the task of policy makers trying to arrest runaway inflation without choking off growth, the war in Ukraine shows no signs of ending. That’s ignited higher food and energy prices across the world, despite the best efforts of central banks to use higher rates to cool economies.

In Europe, the Stoxx 600 Index was down 0.4%, with shares of basic resources companies and financial sector stocks leading the drop, while the region’s bonds fell as traders braced for a crucial European Central Bank meeting. Credit Suisse shares tumbled as much as 7.6% after the Swiss bank announced that it expects a loss in the 2Q. In addition, people familiar with the matter said that the lender is weighing a fresh round of job cuts. European mining stocks also underperformed the Stoxx 600 benchmark as copper declines, while iron ore fluctuates with investors weighing signs of demand recovery against caution that China may seek to stabilize commodity prices. The Stoxx Europe 600 Basic Resources sub-index slid 1.1% as of 9:45 a.m. in London after rising to the highest since April on Tuesday. Here are the most notable European movers:

- Prosus’s shares jump as much as 8.6% in Amsterdam trading after China approved its second batch of video games this year, with a total of 60 titles.

- Naspers, which holds a 29% stake in Tencent through Prosus, up as much as 9.8%.

- Inditex shares gain as much as 5.3% after the Zara owner reported 1Q results. Analysts were impressed by the sales beat, with Bryan Garnier calling the company a “safe-haven choice” in the retail sector.

- UK and European retail stocks rise after Inditex’s results helped boost sentiment, with the retail segment the biggest gainer in the Stoxx 600 Index. Asos gained as much as +3.9%, Boohoo +3.1%, JD Sports +2.5%.

- Voestalpine shares rise as much as 4.5% after the company reported strong results for the business year, even as its guidance for FY23 points at a lack of visibility for fiscal 2H, according to analysts.

- Haldex shares rise as much as 45% after SAF-Holland offers SEK66 in cash per share for the Swedish brake and air suspension products maker, representing a 46.5% premium to its closing price on Tuesday.

- Wizz Air shares fall as much as 8.6% after the company reported results that were in line with expectations but flagged an operating loss for the 1Q of fiscal year 2023.

- European mining stocks underperform the Stoxx 600 benchmark as copper declines, while iron ore fluctuates. Anglo American shares fell as much as 1.7%, Rio Tinto -1.8%, Glencore -1.7%, Antofagasta -3.3%.

- Orpea shares declined as much as 5.9% as the company said that French police investigators began an evidence-gathering raid on Wednesday at its headquarters.

Asian stocks rose as Beijing’s move to approve a slew of new video games bolstered bets that the outlook is improving for the Chinese technology sector. The MSCI Asia Pacific Index advanced as much as 1.1%, with Alibaba and Tencent providing the biggest boosts. Benchmarks in Hong Kong outperformed on the approvals news, while Japanese equities climbed as the yen continued to weaken. Stocks in India fell after the country’s central bank raised interest rates as expected while Thai shares inched up after the Bank of Thailand kept its benchmark rate unchanged. China approved more games in a step toward normalization after a months-long freeze amid the government’s crackdowns on the tech sector. The news follows a report earlier this week that regulators are preparing to conclude an investigation of ride-hailing giant Didi.

“We think the significant dangers have passed” in Chinese equities markets, said Eric Schiffer, chief executive officer at California-based private equity firm Patriarch Organization, which holds positions in Alibaba and JD. “The approval on the game titles signals that policymakers are following through on their intention to back off tech regulation and reverse the pain that caused investors to leave the sector." Optimism toward a less-harsh regulatory environment and China’s post-Covid economic reopening has helped Hong Kong’s tech stocks outperform US peers recently. The Hang Seng Tech Index is up more than 17% the past month compared with little change in the Nasdaq 100. The rebound in Chinese equities also helped the MSCI Asia Pacific Index stage a bigger recovery than the S&P 500 in the same period.

Japanese equities advanced for a fourth straight day, as the yen’s weakness provided support for the nation’s exporters. The Topix rose 1.2% to 1,969.98 as of market close, while the Nikkei advanced 1% to 28,234.29. Toyota Motor Corp. contributed the most to the Topix gain, increasing 1.8%. Out of 2,170 shares in the index, 1,646 rose and 435 fell, while 89 were unchanged.

Stocks in India declined as the Reserve Bank of India said it would withdraw pandemic-era accommodation to quell inflation after raising borrowing costs for a second straight month. The S&P BSE Sensex dropped 0.4% to 54,893.84, as of 2:46 p.m. in Mumbai, while the NSE Nifty 50 Index fell 0.6%. Both gauges erased gains of as much as 0.8% reached during the central bank’s briefing and are heading for a fourth day of declines. Of 30 shares in the Sensex, 13 rose and 17 fell. Sustained high prices could unhinge inflationary expectations and trigger second-round effects, central bank Governor Shaktikanta Das said in an online briefing, emphasizing that preserving price stability is key to ensuring lasting economic growth. Reliance Industries was the biggest drag on the Sensex, while State Bank of India gave the biggest boost. All except two of BSE’s 19 sector sub-gauges declined, with telecom and energy groups the worst performers as realty and metals gained

In FX, Yen weakness extends in European trade, with JPY hitting the weakest level since 2002 at 133.77/USD after BOJ’s Kuroda reiterated easing stance. The dollar strengthened against all its group-of-10 peers with the yen and Australian and New Zealand dollars as the worst performers. The euro fluctuated around the $1.07 handle while bunds and Italian bonds fell alongside Treasuries, paring some of Tuesday’s gains. Australian and New Zealand dollars both weakened amid greenback strength and falling US stock futures. Aussie further was weighed by local yields giving up Tuesday’s RBA-driven gains.

In rates, Treasuries drifted lower, giving back a portion of Tuesday’s gains and following bigger losses for bunds, which underperformed ahead of Thursday’s ECB policy meeting. Yields are cheaper by 2bp-3bp across the curve with front-end marginally outperforming, steepening 2s10s spread by ~1.5bp and building curve concession for the auction; bunds underperform by 1.5bp in 10-year sector. Focal points of US session include 10-year auction, following soft results for Tuesday’s 3-year. $33b 10-year reopening at 1pm ET is second of this week’s three auctions; $19b 30-year reopening is ahead Thursday. WI 10-year yield ~3.015% is above auction stops since 2011 and ~7bp cheaper than May’s, which tailed by 1.4bp. JGBs little changed, with benchmark 10-year bonds trading again after no transactions on Tuesday. Peripheral spreads widen to Germany; Italy lags, widening ~3bps to core at the 10y points ahead of the ECB on Thursday.

In commodities, WTI drifts 0.6% higher to trade at around $120. Most base metals are in the green; LME tin rises 2.8%, outperforming peers. Spot gold falls roughly $5 to trade at $1,848/oz.

Looking at To the day ahead now, and it’s a fairly quiet one on the calendar, but data releases include German industrial production and Italian retail sales for April, as well as the UK construction PMI for May and the final reading of US wholesale inventories for April.

Market Snapshot

- S&P 500 futures down 0.4% to 4,144.00

- STOXX Europe 600 down 0.3% to 441.39

- MXAP up 0.8% to 169.14

- MXAPJ up 1.1% to 559.98

- Nikkei up 1.0% to 28,234.29

- Topix up 1.2% to 1,969.98

- Hang Seng Index up 2.2% to 22,014.59

- Shanghai Composite up 0.7% to 3,263.79

- Sensex down 0.4% to 54,907.55

- Australia S&P/ASX 200 up 0.4% to 7,121.10

- Kospi little changed at 2,626.15

- Brent Futures up 0.3% to $120.92/bbl

- Gold spot down 0.3% to $1,847.71

- U.S. Dollar Index up 0.34% to 102.67

- German 10Y yield little changed at 1.33%

- Euro down 0.2% to $1.0686

Top Overnight News from Bloomberg

- Boris Johnson plans to press ahead with legislation giving him the power to override parts of the Brexit deal, three people familiar with the matter said, a move likely to anger some of his MPs and the EU

- The yen’s historic weakness is spreading from the dollar into other currency crosses as the Bank of Japan’s policy isolation grows. Bloomberg’s Correlation-Weighted Currency Index for the yen -- a gauge of its relative strength against a broad basket of Group-of-10 peers -- slumped to a seven-year low Wednesday

- Japanese investors sold US Treasuries for the sixth consecutive month in April, underscoring waning appetite for the securities as the Federal Reserve sticks to its aggressive monetary tightening path

- Inflation in Hungary exceeded 10% for the first time in more than 20 years, putting pressure on the central bank to tighten monetary policy further and prop up the forint

- Australian inflation is likely to breach 6% and potentially could go “well above” that level and remain there for the rest of the year, Secretary to the Treasury Steven Kennedy said Wednesday

- Economists and investors criticized Australia’s central bank for confusing communications after it raised interest rates by twice as much as expected, having previously signaled a preference for quarter-point moves

- The RBI delivered a 50 basis-point rate hike as predicted by 17 of 41 economists in a Bloomberg survey

- A slew of China video game approvals is giving stock bulls renewed hope that a nascent rebound in tech shares could become a sustainable rally. The Hang Seng Tech Index jumped more than 4% Wednesday after the government approved 60 licenses

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly higher following the gains on Wall St and optimism of China easing its tech crackdown. ASX 200 recovered from the prior day’s RBA-induced selling with nearly all sectors in the green, although financials underperformed. Nikkei 225 extended further above the 28k level on currency weakness and with Q1 GDP data revised upwards to a narrower contraction. Hang Seng and Shanghai Comp. traded mixed with tech fuelling the gains in Hong Kong after China’s NPPA approved the publishing licences for 60 games this month, while sentiment in the mainland gradually soured despite support efforts as an official also warned that China's foreign trade stabilisation faces uncertainties and large pressure.

Top Asian News

- China Vice Commerce Minister Wang said China's foreign trade stabilisation faces uncertainties and a large pressure from domestic and external factors. Furthermore, he sees global demand growth as low, while he added that China will accelerate export tax rebates and MOFCOM will assist foreign trade companies in securing orders, according to Reuters.

- Chinese Retail Passenger Car Sales (May) +30% M/M, according to PCA's Prelim data cited by Bloomberg.

- Japan's CDP has, as expected, submitted a no-confidence motion against the governing administration within the Lower House, motion will be put to a vote on June 9th, via Asahi; Asahi adds that the move is not expected to go anywhere

European bourses have trimmed initial upside, Euro Stoxx 50 -0.2%, with macro newsflow limited and the initial strength primarily a continuation of APAC/Wall St. leads. In specifics, Credit Suisse (-5%) issued a Q2 profit warning for the group and its Investment Bank division while noted Retail name Inditex (+4%) provided a positive update. Stateside, futures are modestly pressured overall but well within overnight ranges ahead of a slim docket; ES -0.4%. DiDi (DIDI) is in advanced discussions to own a one-third stake of Sinomach Zhijun, a China state-backed EV maker, according to Reuters sources.

Top European News

- Euro-Zone Economy Grew More Than Estimated at Start of Year

- Even the ECB’s Most Dire Forecast May Have Been Too Optimistic

- Euro Options Point to Most-Pivotal ECB Meeting Since 2019

- Ireland Accuses Johnson of Acting in ‘Bad Faith’ on Brexit Deal

- Saudi Wealth Fund Makes Second $1 Billion Bet on Swedish Gaming

Central banks

- RBI hiked the Repurchase Rate by 50bps to 4.90% (exp. 40bps hike) via unanimous decision and dropped mention of "staying accommodative", while RBI Governor Das noted that inflation has increased above upper tolerance levels and they remain focused on bringing down inflation. Das added they will control inflation without losing sight of growth and that further monetary policy measures are necessary to anchor inflation, as well as noted that upside risk to inflation had intensified and materialised sooner than expected.

- RBI Governor says they dropped the word "accommodative" from their stance, but they remain accommodative; liquidity withdrawal going forward will be calibrated and gradual.

- BoJ's Kuroda says rapid weakening of JPY as seen recently is undesirable; various macroeconomic models show that a weak JPY is positive. I It is important for FX to move stably, reflecting fundamentals.

- BoJ is expected to maintain its view that the domestic economy is picking up as a trend and will likely continue improving, according to Reuters sources.

- PBoC international department official Zhou said the PBoC will keep guiding financing costs lower, while the PBoC also announced that China will extend the trading hours of the interbank FX market, according to Reuters.

FX

- Buck bounces as Yen rout continues after soft verbal intervention from BoJ Governor and Japanese Economy Minister; DXY back around 102.500 axis, USD.JPY climbs to circa 133.86 at one stage.

- More Lira depreciation on multiple negative factors including unconventional easing policy stance aimed at returning inflation to target, USD/TRY touches 17.1500.

- Aussie and Kiwi undermined by Greenback rebound and fade in general risk sentiment; AUD/USD loses 0.7200+ status again, NZD/USD sub-0.6450.

- Franc and Pound down, but Euro and Loonie resilient as former awaits ECB and latter leans on strong crude prices; USD/CHF just shy of 0.9790, Cable under 1.2550, EUR/USD probing 1.0700 and USD/CAD pivoting 1.2550.

- Forint and Zloty underpinned post-strong Hungarian CPI metrics and pre-NBP that is expected to hike 75bp; EUR/HUF & EUR/PLN around 389.60 and 4.5700 respectively.

Fixed Income

- Bunds and Gilts pare some losses after testing round and half round number levels at 149.00 and 114.50 respectively, with added incentive after solid demand for 10 year German and UK supply.

- US Treasuries await 2032 issuance with caution given a lukewarm reception at 3 year auction.

- 10 year note just off base of 118-03/13 overnight range.

Commodities

- WTI and Brent have been moving in-line with broader risk; however, following the UAE Minister the benchmarks have extended to the upside and post gains in excess of USD 1.50/bbl.

- US Energy Inventory Data (bbls): Crude +1.8mln (exp. -1.9mln), Cushing -1.8mln, Gasoline +1.8mln (exp. +1.1mln), Distillates +3.4mln (exp. +1.1mln)

- Brazilian government is considering measures to monitor fuel prices at distributors, according to Reuters sources.

- UAE Energy Minister says situation is not encouraging when it comes to the amounts of crude OPEC+ can bring to the market, via Reuters; Notes conformity with the OPEC+ deal is more than 200%, are risks when China is back, in talks with Germany and other nations to see if they are interested in UAE natgas.

- Spot gold is essentially unchanged, and continues to pivot its 10-DMA, while base metals are primarily tracking broader risk sentiment.

US Event Calendar

- 07:00: June MBA Mortgage Applications -6.5%, prior -2.3%

- 10:00: April Wholesale Trade Sales MoM, prior 1.7%

- 10:00: April Wholesale Inventories MoM, est. 2.1%, prior 2.1%

DB's Henry Allen concludes the overnight wrap

A reminder that Jim’s annual default study was released yesterday. His view is that while nothing much will change for the remainder of 2022, we might be coming to the end of the ultra-low default world discussed in previous editions. First, there’ll likely be a cyclical US recession to address in 2023, and after that, a risk that various trends reverse that have made the last 20 years so subdued for defaults. See the report here for more details.

It’s been another topsy-turvy session for markets over the last 24 hours as investors look forward to the big macro events later in the week, namely the ECB tomorrow and then the US CPI print the day after. Initially it had looked like we were set for another day of higher rates, not least after the hawkish surprise from the RBA we mentioned in yesterday’s edition as they hiked by a larger-than-expected 50bps. But more negative developments subsequently dampened the mood, including an unexpected contraction in German factory orders, and then an announcement by Target (-2.31%) that they were cutting their profit outlook for the second time in three weeks. But then sentiment turned once again later in the US session, with equities seeing a late rally that put the major indices back in positive territory for the day.

Against that backdrop, equities swung between gains and losses, but the S&P 500 rallied to a broad-based gain after the European close, finishing the day +0.95% higher after being as much as -1% lower following the open, with only the consumer discretionary (-0.37%) sector finishing in the red after Target updated their guidance again to now expect Q2’s operating margin to be around 2% amid price reductions to reduce inventory. For the index as a whole, it was also the first back-to-back positive start the week since in a month, that’s also seen it recover all of last week’s declines. Energy (+3.14%) was the biggest outperformer in the S&P amidst a further rise in oil prices, with Brent Crude (+0.89%) moving back above the $120/bbl mark. However, Europe’s STOXX 600 (-0.28%) missed the late rally and eventually settled in negative territory.

Whilst equities had a mixed session, sovereign bonds put in a more consistent performance ahead of tomorrow’s ECB decision, with decent gains posted on both sides of the Atlantic. Yields on 10yr Treasuries were down -6.6bps to 2.97%, moving back beneath 3% again, although this morning’s +2.8bps rise has taken them just back above that point to 3.001% at time of writing. Yesterday’s moves lower in yields were more pronounced at the long end of the curve, with the 2yr yield essentially flat as investors’ expectations of the near-term path of Fed rate hikes remained fairly steady. Indeed, the futures-implied rate by the December meeting was also down just -1.5bps to 2.84%.

It was much the same story in Europe too of lower yields and flatter curves, as the amount of ECB tightening priced in for the rest of the year fell a modest -1.4bps from its high of 125bps the previous day. Yields on 10yr bunds (-2.9bps), OATs (-3.6bps) and gilts (-3.3bps) all fell back, and there was a noticeable decline in peripheral spreads thanks to even larger reductions in the Italian (-12.1bps) and Spanish (-7.4bps) 10yr yields. Interestingly, another trend over recent days that continued was the fall in European natural gas prices (-3.57%), which fell for a 5th consecutive session to hit its lowest level since Russia’s invasion of Ukraine, at €79.61/MWh.

Those late gains for US equities have carried over into Asia overnight, with the Hang Seng (+1.70%) the Nikkei (+0.85%) both advancing strongly. The main exception to that has been in mainland China however, where the CSI 300 (-0.41%) and the Shanghai Composite (-0.70%) have just taken a tumble this morning. We’ve also seen that in US equity futures too, with those on the S&P 500 down -0.335 this morning.

On the data side, the final estimate of Japan’s GDP for Q1 showed a smaller contraction than initially thought, with GDP only falling by an annualised -0.5%, which is half the -1% decline initially thought. However, the Japanese Yen has continued to weaken overnight, and is currently trading at a fresh 20-year low against the US Dollar of 133.13 per dollar. It’s also at a 7-year low against the Euro of 142.19 per euro.

Here in the UK, Brexit could be back in the headlines shortly as it’s been reported by multiple outlets including Bloomberg that legislation will be introduced that would enable the UK government to override the Northern Ireland Protocol. That’s the part of the Brexit deal that avoids the need for a hard border between Northern Ireland and the Republic of Ireland, but has been a persistent source of tension between the two sides since the deal was signed, since it creates an economic border between Northern Ireland and Great Britain that Northern Irish unionists are opposed to. Irish PM Martin said yesterday that Europe would respond in a “calm and firm” way, and Bloomberg’s report suggested the draft bill could be presented to the House of Commons tomorrow.

Looking at yesterday’s data releases, German factory orders for April unexpectedly saw a -2.7% contraction (vs. +0.4% expansion expected). That was the third consecutive monthly decline, and was driven by a -4.0% decline in foreign orders. On the other hand, the final PMIs from the UK for May were revised up relative to the flash readings, with the composite PMI at 53.1 (vs. flash 51.8), helping sterling to strengthen +0.48% against the US Dollar. Finally, the World Bank yesterday became the latest body to downgrade their global growth forecast, now projecting a +2.9% rise in GDP for 2022 compared to their 4.1% estimate put out in January, and openly warned about the risk of stagflation.

To the day ahead now, and it’s a fairly quiet one on the calendar, but data releases include German industrial production and Italian retail sales for April, as well as the UK construction PMI for May and the final reading of US wholesale inventories for April.

Uncategorized

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-March 2024

A brief excerpt: This 2-part overview for mid-March provides a snapshot of the current housing market.

I always like to star…

Share this:

A brief excerpt:

This 2-part overview for mid-March provides a snapshot of the current housing market.There is much more in the article.

I always like to start with inventory, since inventory usually tells the tale!

...

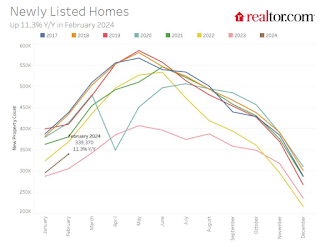

Here is a graph of new listing from Realtor.com’s February 2024 Monthly Housing Market Trends Report showing new listings were up 11.3% year-over-year in February. This is still well below pre-pandemic levels. From Realtor.com:

However, providing a boost to overall inventory, sellers turned out in higher numbers this February as newly listed homes were 11.3% above last year’s levels. This marked the fourth month of increasing listing activity after a 17-month streak of decline.Note the seasonality for new listings. December and January are seasonally the weakest months of the year for new listings, followed by February and November. New listings will be up year-over-year in 2024, but we will have to wait for the March and April data to see how close new listings are to normal levels.

There are always people that need to sell due to the so-called 3 D’s: Death, Divorce, and Disease. Also, in certain times, some homeowners will need to sell due to unemployment or excessive debt (neither is much of an issue right now).

And there are homeowners who want to sell for a number of reasons: upsizing (more babies), downsizing, moving for a new job, or moving to a nicer home or location (move-up buyers). It is some of the “want to sell” group that has been locked in with the golden handcuffs over the last couple of years, since it is financially difficult to move when your current mortgage rate is around 3%, and your new mortgage rate will be in the 6 1/2% to 7% range.

But time is a factor for this “want to sell” group, and eventually some of them will take the plunge. That is probably why we are seeing more new listings now.

Government

RFK Jr. Reveals Vice President Contenders

RFK Jr. Reveals Vice President Contenders

Authored by Jeff Louderback via The Epoch Times,

New York Jets quarterback Aaron Rodgers and former…

Share this:

Authored by Jeff Louderback via The Epoch Times,

New York Jets quarterback Aaron Rodgers and former Minnesota governor and professional wrestler Jesse Ventura are among the potential running mates for independent presidential candidate Robert F. Kennedy Jr., the New York Times reported on March 12.

Citing “two people familiar with the discussions,” the New York Times wrote that Mr. Kennedy “recently approached” Mr. Rodgers and Mr. Ventura about the vice president’s role, “and both have welcomed the overtures.”

Mr. Kennedy has talked to Mr. Rodgers “pretty continuously” over the last month, according to the story. The candidate has kept in touch with Mr. Ventura since the former governor introduced him at a February voter rally in Tucson, Arizona.

Stefanie Spear, who is the campaign press secretary, told The Epoch Times on March 12 that “Mr. Kennedy did share with the New York Times that he’s considering Aaron Rodgers and Jesse Ventura as running mates along with others on a short list.”

Ms. Spear added that Mr. Kennedy will name his running mate in the upcoming weeks.

Former Democrat presidential candidates Andrew Yang and Tulsi Gabbard declined the opportunity to join Mr. Kennedy’s ticket, according to the New York Times.

Mr. Kennedy has also reportedly talked to Sen. Rand Paul (R-Ky.) about becoming his running mate.

Last week, Mr. Kennedy endorsed Mr. Paul to replace Sen. Mitch McConnell (R-Ky.) as the Senate Minority Leader after Mr. McConnell announced he would step down from the post at the end of the year.

CNN reported early on March 13 that Mr. Kennedy’s shortlist also includes motivational speaker Tony Robbins, Discovery Channel Host Mike Rowe, and civil rights attorney Tricia Lindsay. The Washington Post included the aforementioned names plus former Republican Massachusetts senator and U.S. Ambassador to New Zealand and Samoa, Scott Brown.

In April 2023, Mr. Kennedy entered the Democrat presidential primary to challenge President Joe Biden for the party’s 2024 nomination. Claiming that the Democrat National Committee was “rigging the primary” to stop candidates from opposing President Biden, Mr. Kennedy said last October that he would run as an independent.

This year, Mr. Kennedy’s campaign has shifted its focus to ballot access. He currently has qualified for the ballot as an independent in New Hampshire, Utah, and Nevada.

Mr. Kennedy also qualified for the ballot in Hawaii under the “We the People” party.

In January, Mr. Kennedy’s campaign said it had filed paperwork in six states to create a political party. The move was made to get his name on the ballots with fewer voter signatures than those states require for candidates not affiliated with a party.

The “We the People” party was established in five states: California, Delaware, Hawaii, Mississippi, and North Carolina. The “Texas Independent Party” was also formed.

A statement by Mr. Kennedy’s campaign reported that filing for political party status in the six states reduced the number of signatures required for him to gain ballot access by about 330,000.

Ballot access guidelines have created a sense of urgency to name a running mate. More than 20 states require independent and third-party candidates to have a vice presidential pick before collecting and submitting signatures.

Like Mr. Kennedy, Mr. Ventura is an outspoken critic of COVID-19 vaccine mandates and safety.

Mr. Ventura, 72, gained acclaim in the 1970s and 1980s as a professional wrestler known as Jesse “the Body” Ventura. He appeared in movies and television shows before entering the Minnesota gubernatorial race as a Reform Party headliner. He was a longshot candidate but prevailed and served one term.

Former pro wrestler Jesse Ventura in Washington on Oct. 4, 2013. (Brendan Smialowski/AFP via Getty Images)

In an interview on a YouTube podcast last December, Mr. Ventura was asked if he would accept an offer to run on Mr. Kennedy’s ticket.

“I would give it serious consideration. I won’t tell you yes or no. It will depend on my personal life. Would I want to commit myself at 72 for one year of hell (campaigning) and then four years (in office)?” Mr. Ventura said with a grin.

Mr. Rodgers, who spent his entire career as a quarterback for the Green Bay Packers before joining the New York Jets last season, remains under contract with the Jets. He has not publicly commented about joining Mr. Kennedy’s ticket, but the four-time NFL MVP endorsed him earlier this year and has stumped for him on podcasts.

The 40-year-old Rodgers is still under contract with the Jets after tearing his Achilles tendon in the 2023 season opener and being sidelined the rest of the year. The Jets are owned by Woody Johnson, a prominent donor to former President Donald Trump who served as U.S. Ambassador to Britain under President Trump.

Since the COVID-19 vaccine was introduced, Mr. Rodgers has been outspoken about health issues that can result from taking the shot. He told podcaster Joe Rogan that he has lost friends and sponsorship deals because of his decision not to get vaccinated.

Quarterback Aaron Rodgers of the New York Jets talks to reporters after training camp at Atlantic Health Jets Training Center in Florham Park, N.J., on July 26, 2023. (Rich Schultz/Getty Images)

Earlier this year, Mr. Rodgers challenged Kansas City Chiefs tight end Travis Kelce and Dr. Anthony Fauci to a debate.

Mr. Rodgers referred to Mr. Kelce, who signed an endorsement deal with vaccine manufacturer Pfizer, as “Mr. Pfizer.”

Dr. Fauci served as director of the National Institute of Allergy and Infectious Diseases from 1984 to 2022 and was chief medical adviser to the president from 2021 to 2022.

When Mr. Kennedy announces his running mate, it will mark another challenge met to help gain ballot access.

“In some states, the signature gathering window is not open. New York is one of those and is one of the most difficult with ballot access requirements,” Ms. Spear told The Epoch Times.

“We need our VP pick and our electors, and we have to gather 45,000 valid signatures. That means we will collect 72,000 since we have a 60 percent buffer in every state,” she added.

The window for gathering signatures in New York opens on April 16 and closes on May 28, Ms. Spear noted.

“Mississippi, North Carolina, and Oklahoma are the next three states we will most likely check off our list,” Ms. Spear added. “We are confident that Mr. Kennedy will be on the ballot in all 50 states and the District of Columbia. We have a strategist, petitioners, attorneys, and the overall momentum of the campaign.”

Uncategorized

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45%…

Share this:

{kind=link}

{kind=link}

{kind=link}

The pharma industry is hanging on to reputation gains notched during the Covid-19 pandemic. Positive perception of the pharma industry is steady at 45% of US respondents in 2023, according to the latest Harris Poll data. That’s exactly the same as the previous year.

Pharma’s highest point was in February 2021 — as Covid vaccines began to roll out — with a 62% positive US perception, and helping the industry land at an average 55% positive sentiment at the end of the year in Harris’ 2021 annual assessment of industries. The pharma industry’s reputation hit its most recent low at 32% in 2019, but it had hovered around 30% for more than a decade prior.

“Pharma has sustained a lot of the gains, now basically one and half times higher than pre-Covid,” said Harris Poll managing director Rob Jekielek. “There is a question mark around how sustained it will be, but right now it feels like a new normal.”

The Harris survey spans 11 global markets and covers 13 industries. Pharma perception is even better abroad, with an average 58% of respondents notching favorable sentiments in 2023, just a slight slip from 60% in each of the two previous years.

Pharma’s solid global reputation puts it in the middle of the pack among international industries, ranking higher than government at 37% positive, insurance at 48%, financial services at 51% and health insurance at 52%. Pharma ranks just behind automotive (62%), manufacturing (63%) and consumer products (63%), although it lags behind leading industries like tech at 75% positive in the first spot, followed by grocery at 67%.

The bright spotlight on the pharma industry during Covid vaccine and drug development boosted its reputation, but Jekielek said there’s maybe an argument to be made that pharma is continuing to develop innovative drugs outside that spotlight.

“When you look at pharma reputation during Covid, you have clear sense of a very dynamic industry working very quickly and getting therapies and products to market. If you’re looking at things happening now, you could argue that pharma still probably doesn’t get enough credit for its advances, for example, in oncology treatments,” he said.

vaccine pandemic covid-19

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Four Years Ago This Week, Freedom Was Torched

Red Candle In The Wind

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Digital Currency And Gold As Speculative Warnings

Analyst reviews Apple stock price target amid challenges

The SNF Institute for Global Infectious Disease Research announces new advisory board

CDC Warns Thousands Of Children Sent To ER After Taking Common Sleep Aid

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International5 days ago

International5 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International5 days ago

International5 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges