Futures Bounce On Evergrande Reprieve With Fed Looming

Futures Bounce On Evergrande Reprieve With Fed Looming

Despite today’s looming hawkish FOMC meeting in which Powell is widely expected to unveil that tapering is set to begin as soon as November and where the Fed’s dot plot may signal one…

Futures Bounce On Evergrande Reprieve With Fed Looming

Despite today's looming hawkish FOMC meeting in which Powell is widely expected to unveil that tapering is set to begin as soon as November and where the Fed's dot plot may signal one rate hike in 2022, futures climbed as investor concerns over China's Evergrande eased after the property developer negotiated a domestic bond payment deal. Commodities rallied while the dollar was steady.

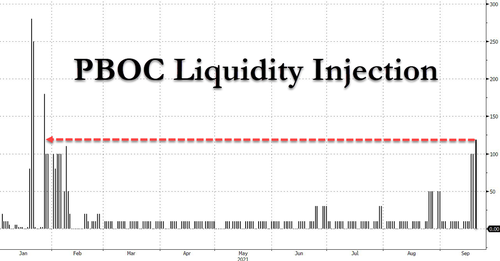

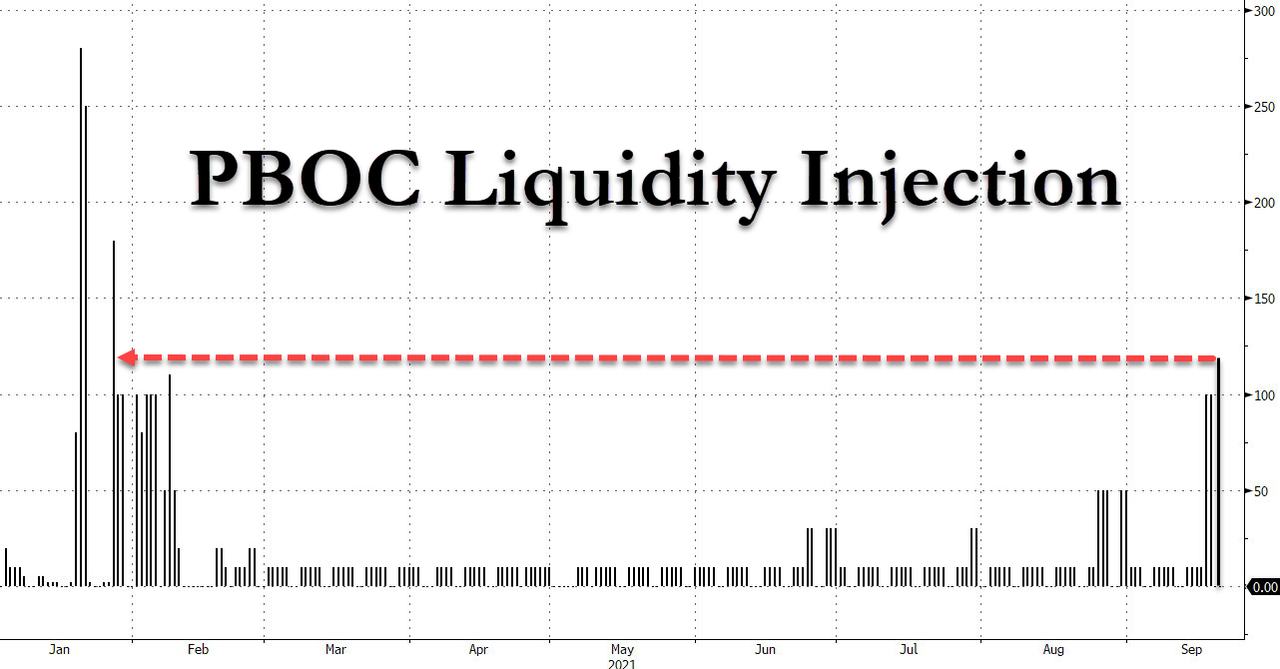

Contracts on the S&P 500 and Nasdaq 100 flipped from losses to gains as China’s central bank boosted liquidity when it injected a gross 120BN in yuan, the most since January...

... and investors mulled a vaguely-worded statement from the troubled developer about an interest payment. S&P 500 E-minis were up 23.0 points, or 0.53%, at 7:30 a.m. ET. Dow E-minis were up 199 points, or 0.60%, and Nasdaq 100 E-minis were up 44.00 points, or 0.29%.

Among individual stocks, Fedex fell 5.8% after the delivery company cut its profit outlook on higher costs and stalled growth in shipments. Morgan Stanley says it sees the company’s 1Q issues getting “tougher from here.” Commodity-linked oil and metal stocks led gains in premarket trade, while a slight rise in Treasury yields supported major banks. However, most sectors were nursing steep losses in recent sessions. Here are some of the biggest U.S. movers:

Adobe (ADBE US) down 3.1% after 3Q update disappointed the high expectations of investors, though the broader picture still looks solid, Morgan Stanley said in a note

Freeport McMoRan (FCX US), Cleveland- Cliffs (CLF US), Alcoa (AA US) and U.S. Steel (X US) up 2%-3% premarket, following the path of global peers as iron ore prices in China rallied

Aethlon Medical (AEMD US) and Exela Technologies (XELAU US) advance along with other retail traders’ favorites in the U.S. premarket session. Aethlon jumps 21%; Exela up 8.3%

Other so-called meme stocks also rise: ContextLogic +1%; Clover Health +0.9%; Naked Brand +0.9%; AMC +0.5%

ReWalk Robotics slumps 18% in U.S. premarket trading, a day after nearly doubling in value

Stitch Fix (SFIX US) rises 15.7% in light volume after the personal styling company’s 4Q profit and sales blew past analysts’ expectations

Hyatt Hotels (H US) seen opening lower after the company launches a seven-million-share stock offering

Summit Therapeutics (SMMT US) shares fell as much as 17% in Tuesday extended trading after it said the FDA doesn’t agree with the change to the primary endpoint that has been implemented in the ongoing Phase III Ri-CoDIFy studies when combining the studies

Marin Software (MRIN US) surged more than 75% Tuesday postmarket after signing a new revenue-sharing agreement with Google to develop its enterprise technology platforms and software products

The S&P 500 had fallen for 10 of the past 12 sessions since hitting a record high, as fears of an Evergrande default exacerbated seasonally weak trends and saw investors pull out of stocks trading at lofty valuations. The Nasdaq fell the least among its peers in recent sessions, as investors pivoted back into big technology names that had proven resilient through the pandemic.

Focus now turns to the Fed's decision, due at 2 p.m. ET where officials are expected to signal a start to scaling down monthly bond purchases (see our preview here). The Fed meeting comes after a period of market volatility stoked by Evergrande’s woes. China’s wider property-sector curbs are also feeding into concerns about a slowdown in the economic recovery from the pandemic.

“Chair Jerome Powell could hint at the tapering approaching shortly,” said Sébastien Barbé, a strategist at Credit Agricole CIB. “However, given the current uncertainty factors (China property market, Covid, pace of global slowdown), the Fed should remain cautious when it comes to withdrawing liquidity support.”

Meanwhile, confirming what Ray Dalio said that the taper will just bring more QE, Governing Council member Madis Muller said the European Central Bank may boost its regular asset purchases once the pandemic-era emergency stimulus comes to an end.

“Dovish signals could unwind some of the greenback’s gains while offering relief to stock markets,” Han Tan, chief market analyst at Exinity Group, wrote in emailed comments. A “hawkish shift would jolt markets, potentially pushing Treasury yields and the dollar past the upper bound of recent ranges, while gold and equities would sell off hunting down the next levels of support.”

China avoided a major selloff as trading resumed following a holiday, after the country’s central bank boosted its injection of short-term cash into the financial system. MSCI’s Asia-Pacific index declined for a third day, dragged lower by Japan.

Stocks were also higher in Europe. Basic resources - which bounced from a seven month low - and energy were among the leading gainers in the Stoxx Europe 600 index as commodity prices steadied after Beijing moved to contain fears of a spiraling debt crisis. Entain Plc rose more than 7%, extending Tuesday’s gain as it confirmed it received a takeover proposal from DraftKings Inc. Peer Flutter Entertainment Plc climbed after settling a legal dispute. Here are some of the biggest European movers today:

Entain shares jump as much as 11% after DraftKings Inc. offered to acquire the U.K. gambling company for about $22.4 billion.

Vivendi rises as much as 3.1% in Paris, after Tuesday’s spinoff of Universal Music Group.

Legrand climbs as much as 2.1% after Exane BNP Paribas upgrades to outperform and raises PT to a Street-high of EU135.

Orpea shares falls as much as 2.9%, after delivering 1H results that Jefferies (buy) says were a “touch” below consensus.

Bechtle slides as much as 5.1% after Metzler downgrades to hold from buy, saying persistent supply chain problems seem to be weighing on growth.

Sopra Steria drops as much as 4.1% after Stifel initiates coverage with a sell, citing caution on company’s M&A strategy

Despite the Evergrande announcement, Asian stocks headed for their longest losing streak in more than a month amid continued China-related concerns, with traders also eying policy decisions from major central banks. The MSCI Asia Pacific Index dropped as much as 0.7% in its third day of declines, with TSMC and Keyence the biggest drags. China’s CSI 300 tumbled as much as 1.9% as the local market reopened following a two-day holiday. However, the gauge came off lows after an Evergrande unit said it will make a bond interest payment and as China’s central bank boosted liquidity. Taiwan’s equity benchmark led losses in Asia on Wednesday, dragged by TSMC after a two-day holiday, while markets in Hong Kong and South Korea were closed. Key stock gauges in Australia, Indonesia and Vietnam rose

“A liquidity injection from the People’s Bank of China accompanied the Evergrande announcement, which only served to bolster sentiment further,” according to DailyFX’s Thomas Westwater and Daniel Dubrovsky. “For now, it appears that market-wide contagion risk linked to a potential Evergrande collapse is off the table.”

Japanese equities fell for a second day amid global concern over China’s real-estate sector, as the Bank of Japan held its key stimulus tools in place while flagging pressures on the economy. Electronics makers were the biggest drag on the Topix, which declined 1%. Daikin and Fanuc were the largest contributors to a 0.7% loss in the Nikkei 225. The BOJ had been expected to maintain its policy levers ahead of next week’s key ruling party election. Traders are keenly awaiting the Federal Reserve’s decision due later for clues on the U.S. central banks plan for tapering stimulus. “Markets for some time have been convinced that the BOJ has reached the end of the line on normalization and will remain in a holding pattern on policy until at least April 2023 when Governor Kuroda is scheduled to leave,” UOB economist Alvin Liew wrote in a note. “Attention for the BOJ will now likely shift to dealing with the long-term climate change issues.”

In the despotic lockdown regime that is Australia, the S&P/ASX 200 index rose 0.3% to close at 7,296.90, reversing an early decline in a rally led by mining and energy stocks. Banks closed lower for the fourth day in a row. Champion Iron was among the top performers after it was upgraded at Citi. IAG was among the worst performers after an earthquake caused damage to buildings in Melbourne. In New Zealand, the S&P/NZX 50 index rose 0.3% to 13,215.80

In FX, commodity currencies rallied as concerns about China Evergrande Group’s debt troubles eased as China’s central bank boosted liquidity and investors reviewed a statement from the troubled developer about an interest payment. Overnight implied volatility on the pound climbed to the highest since March ahead of Bank of England’s meeting on Thursday. The British pound weakened after Business Secretary Kwasi Kwarteng warnedthat people should prepare for longer-term high energy prices amid a natural-gas shortage that sent power costs soaring. Several U.K. power firms have stopped taking in new clients as small energy suppliers struggle to meet their previous commitments to sell supplies at lower prices.

Overnight volatility in the euro rises above 10% for the first time since July ahead of the Federal Reserve’s monetary policy decision announcement. The Aussie jumped as much as 0.5% as iron-ore prices rebounded. Spot surged through option-related selling at 0.7240 before topping out near 0.7265 strikes expiring Wednesday, according to Asia- based FX traders. Elsewhere, the yen weakened and commodity-linked currencies such as the Australian dollar pushed higher.

In rates, the dollar weakened against most of its Group-of-10 peers. Treasury futures were under modest pressure in early U.S. trading, leaving yields cheaper by ~1.5bp from belly to long-end of the curve. The 10-year yield was at ~1.336% steepening the 2s10s curve by ~1bp as the front-end was little changed. Improved risk appetite weighed; with stock futures have recovering much of Tuesday’s losses as Evergrande concerns subside. Focal point for Wednesday’s session is FOMC rate decision at 2pm ET. FOMC is expected to suggest it will start scaling back asset purchases later this year, while its quarterly summary of economic projections reveals policy makers’ expectations for the fed funds target in coming years in the dot-plot update; eurodollar positions have emerged recently that anticipate a hawkish shift

Bitcoin dropped briefly below $40,000 for the first time since August amid rising criticism from regulators, before rallying as the mood in global markets improved.

In commodities, Iron ore halted its collapse and metals steadied. Oil advanced for a second day. Bitcoin slid below $40,000 for the first time since early August before rebounding back above $42,000.

To the day ahead now, and the main highlight will be the aforementioned Federal Reserve decision and Chair Powell’s subsequent press conference. Otherwise on the data side, we’ll get US existing home sales for August, and the European Commission’s advance consumer confidence reading for the Euro Area in September.

Market Snapshot

S&P 500 futures up 0.4% to 4,362.25

STOXX Europe 600 up 0.5% to 461.19

MXAP down 0.7% to 199.29

MXAPJ down 0.4% to 638.39

Nikkei down 0.7% to 29,639.40

Topix down 1.0% to 2,043.55

Hang Seng Index up 0.5% to 24,221.54

Shanghai Composite up 0.4% to 3,628.49

Sensex little changed at 59,046.84

Australia S&P/ASX 200 up 0.3% to 7,296.94

Kospi up 0.3% to 3,140.51

Brent Futures up 1.5% to $75.47/bbl

Gold spot up 0.0% to $1,775.15

U.S. Dollar Index little changed at 93.26

German 10Y yield rose 0.6 bps to -0.319%

Euro little changed at $1.1725

Top Overnight News from Bloomberg

What would it take to knock the U.S. recovery off course and send Federal Reserve policy makers back to the drawing board? Not much — and there are plenty of candidates to deliver the blow

The European Central Bank will discuss boosting its regular asset purchases once the pandemic-era emergency stimulus comes to an end, but any such increase is uncertain, Governing Council member Madis Muller said

Investors seeking hints about how Beijing plans to deal with China Evergrande Group’s debt crisis are training their cross hairs on the central bank’s liquidity management

A quick look at global markets courtesy of Newsquawk

Asian equity markets traded mixed as caution lingered ahead of upcoming risk events including the FOMC, with participants also digesting the latest Evergrande developments and China’s return to the market from the Mid-Autumn Festival. ASX 200 (+0.3%) was positive with the index led higher by the energy sector after a rebound in oil prices and as tech also outperformed, but with gains capped by weakness in the largest-weighted financials sector including Westpac which was forced to scrap the sale of its Pacific businesses after failing to secure regulatory approval. Nikkei 225 (-0.7%) was subdued amid the lack of fireworks from the BoJ announcement to keep policy settings unchanged and ahead of the upcoming holiday closure with the index only briefly supported by favourable currency outflows. Shanghai Comp. (+0.4%) was initially pressured on return from the long-weekend and with Hong Kong markets closed, but pared losses with risk appetite supported by news that Evergrande’s main unit Hengda Real Estate will make coupon payments due tomorrow, although other sources noted this is referring to the onshore bond payments valued around USD 36mln and that there was no mention of the offshore bond payments valued at USD 83.5mln which are also due tomorrow. Meanwhile, the PBoC facilitated liquidity through a CNY 120bln injection and provided no surprises in keeping its 1-year and 5-year Loan Prime Rates unchanged for the 17th consecutive month at 3.85% and 4.65%, respectively. Finally, 10yr JGBs were flat amid the absence of any major surprises from the BoJ policy announcement and following the choppy trade in T-notes which were briefly pressured in a knee-jerk reaction to the news that Evergrande’s unit will satisfy its coupon obligations tomorrow, but then faded most of the losses as cautiousness prevailed.

Top Asian News

Gold Steady as Traders Await Outcome of Fed Policy Meeting

Evergrande Filing on Yuan Bond Interest Leaves Analysts Guessing

Singapore Category E COE Price Rises to Highest Since April 2014

Asian Stocks Fall for Third Day as Focus Turns to Central Banks

European equities (Stoxx 600 +0.5%) trade on a firmer footing in the wake of an encouraging APAC handover. Focus overnight was on the return of Chinese participants from the Mid-Autumn Festival and news that Evergrande’s main unit, Hengda Real Estate will make coupon payments due tomorrow; however, we await indication as to whether they will meet Thursday’s offshore payment deadline as well. Furthermore, the PBoC facilitated liquidity through a CNY 120bln injection whilst keeping its 1-year and 5-year Loan Prime Rates unchanged (as expected). Note, despite gaining yesterday and today, thus far, the Stoxx 600 is still lower to the tune of 0.7% on the week. Stateside, futures are also trading on a firmer footing ahead of today’s FOMC policy announcement, at which, market participants will be eyeing any clues for when the taper will begin and digesting the latest dot plot forecasts. Furthermore, the US House voted to pass the bill to fund the government through to December 3rd and suspend the debt limit to end-2022, although this will likely be blocked by Senate Republicans. Back to Europe, sectors are mostly firmer with outperformance in Basic Resources and Oil & Gas amid upside in the metals and energy complex. Elsewhere, Travel & Leisure is faring well amid further upside in Entain (+6.1%) with the Co. noting it rejected an earlier approach from DraftKings at GBP 25/shr with the new offer standing at GBP 28/shr. Additionally for the sector, Flutter Entertainment (+4.1%) are trading higher after settling the legal dispute between the Co. and Commonwealth of Kentucky. Elsewhere, in terms of deal flow, Iliad announced that it is to acquire UPC Poland for around USD 1.8bln.

Top European News

Energy Cost Spike Gets on EU Ministers’ Green Deal Agenda

Travel Startup HomeToGo Gains in Frankfurt Debut After SPAC Deal

London Stock Exchange to Shut Down CurveGlobal Exchange

EU Banks Expected to Add Capital for Climate Risk, EBA Says

In FX, trade remains volatile as this week’s deluge of global Central Bank policy meetings continues to unfold amidst fluctuations in broad risk sentiment from relatively pronounced aversion at various stages to a measured and cautious pick-up in appetite more recently. Hence, the tide is currently turning in favour of activity, cyclical and commodity currencies, albeit tentatively in the run up to the Fed, with the Kiwi and Aussie trying to regroup on the 0.7000 handle and 0.7350 axis against their US counterpart, and the latter also striving to shrug off negative domestic impulses like a further decline below zero in Westpac’s leading index and an earthquake near Melbourne. Next up for Nzd/Usd and Aud/Usd, beyond the FOMC, trade data and preliminary PMIs respectively.

DXY/CHF/EUR/CAD - Notwithstanding the overall improvement in market tone noted above, or another major change in mood and direction, the Dollar index appears to have found a base just ahead of 93.000 and ceiling a similar distance away from 93.500, as it meanders inside those extremes awaiting US existing home sales that are scheduled for release before the main Fed events (policy statement, SEP and post-meeting press conference from chair Powell). Indeed, the Franc, Euro and Loonie have all recoiled into tighter bands vs the Greenback, between 0.9250-26, 1.1739-17 and 1.2831-1.2770, but with the former still retaining an underlying bid more evident in the Eur/Chf cross that is consolidating under 1.0850 and will undoubtedly be acknowledged by the SNB tomorrow. Meanwhile, Eur/Usd has hardly reacted to latest ECB commentary from Muller underpinning that the APP is likely to be boosted once the PEPP envelope is closed, though Usd/Cad is eyeing a firm rebound in oil prices in conjunction with hefty option expiry interest at the 1.2750 strike (1.8 bn) that may prevent the headline pair from revisiting w-t-d lows not far beneath the half round number.

GBP/JPY - The major laggards, as Sterling slips slightly further beneath 1.3650 against the Buck to a fresh weekly low and Eur/Gbp rebounds from circa 0.8574 to top 0.8600 on FOMC day and T-1 to super BoE Thursday. Elsewhere, the Yen has lost momentum after peaking around 109.12 and still not garnering sufficient impetus to test 109.00 via an unchanged BoJ in terms of all policy settings and guidance, as Governor Kuroda trotted out the no hesitation to loosen the reins if required line for the umpteenth time. However, Usd/Jpy is holding around 109.61 and some distance from 1.1 bn option expiries rolling off between 109.85-110.00 at the NY cut.

SCANDI/EM - Brent’s revival to Usd 75.50+/brl from sub-Usd 73.50 only yesterday has given the Nok another fillip pending confirmation of a Norges Bank hike tomorrow, while the Zar has regained some poise with the aid of firmer than forecast SA headline and core CPI alongside a degree of retracement following Wednesday’s breakdown of talks on a pay deal for engineering workers that prompted the union to call a strike from early October. Similarly, the Cnh and Cny by default have regrouped amidst reports that the CCP is finalising details to restructure Evergrande into 3 separate entities under a plan that will see the Chinese Government take control.

In commodities, WTI and Brent are firmer this morning though once again fresh newsflow for the complex has been relatively slim and largely consisting of gas-related commentary; as such, the benchmarks are taking their cue from the broader risk tone (see equity section). The improvement in sentiment today has brought WTI and Brent back in proximity to being unchanged on the week so far as a whole; however, the complex will be dictated directly by the EIA weekly inventory first and then indirectly, but perhaps more pertinently, by today’s FOMC. On the weekly inventories, last nights private release was a larger than expected draw for the headline and distillate components, though the Cushing draw was beneath expectations; for today, consensus is a headline draw pf 2.44mln. Moving to metals where the return of China has seen a resurgence for base metals with LME copper posting upside of nearly 3.0%, for instance. Albeit there is no fresh newsflow for the complex as such, so it remains to be seen how lasting this resurgence will be. Finally, spot gold and silver are firmer but with the magnitude once again favouring silver over the yellow metal.

US Event Calendar

10am: Aug. Existing Home Sales MoM, est. -1.7%, prior 2.0%

All eyes firmly on China this morning as it reopens following a 2-day holiday. As expected the indices there have opened lower but the scale of the declines are being softened by the PBoC increasing its short term cash injections into the economy. They’ve added a net CNY 90bn into the system. On Evergrande, we’ve also seen some positive headlines as the property developers’ main unit Hengda Real Estate Group has said that it will make coupon payment for an onshore bond tomorrow. However, the exchange filing said that the interest payment “has been resolved via negotiations with bondholders off the clearing house”. This is all a bit vague and doesn’t mention the dollar bond at this stage. Meanwhile, Bloomberg has reported that Chinese authorities have begun to lay the groundwork for a potential restructuring that could be one of the country’s biggest, assembling accounting and legal experts to examine the finances of the group. All this follows news from Bloomberg yesterday that Evergrande missed interest payments that had been due on Monday to at least two banks. In terms of markets the CSI (-1.11%), Shanghai Comp (-0.29%) and Shenzhen Comp (-0.53%) are all lower but have pared back deeper losses from the open.

We did a flash poll in the CoTD yesterday (link here) and after over 700 responses in a couple of hours we found only 8% who we thought Evergrande would still be impacting financial markets significantly in a month’s time. 24% thought it would be slightly impacting. The other 68% thought limited or no impact. So the world is relatively relaxed about contagion risk for now. The bigger risk might be the knock on impact of weaker Chinese growth. So that’s one to watch even if you’re sanguine on the systemic threat. Craig Nicol in my credit team did a good note yesterday (link here) looking at the contagion risk to the broader HY market. I thought he summed it up nicely as to why we all need to care one way or another in saying that “Evergrande is the largest corporate, in the largest sector, of the second largest economy in the world”. For context AT&T is the largest corporate borrower in the US market and VW the largest in Europe.

Turning back to other Asian markets now and the Nikkei (-0.65%) is down but the Hang Seng (+0.51%) and Asx (+0.58%) are up. South Korean markets continue to remain closed for a holiday. Elsewhere, yields on 10y USTs are trading flattish while futures on the S&P 500 are up +0.10% and those on the Stoxx 50 are up +0.21%. Crude oil prices are also up c.+1% this morning. In other news, the Bank of Japan policy announcement overnight was a non-event as the central bank maintained its yield curve target while keeping the policy rate and asset purchases plan unchanged. The central bank also unveiled more details of its green lending program and said that it would immediately start accepting applications and would begin making the loans in December.

The relatively calm Asian session follows a stabilisation in markets yesterday following their rout on Monday as investors looked forward to the outcome of the Fed’s meeting later today. That said, it was hardly a resounding performance, with the S&P 500 unable to hold on to its intraday gains and ending just worse than unchanged after the -1.70% decline the previous day as investors remained vigilant as to the array of risks that continue to pile up on the horizon.

One of these is in US politics and legislators seem no closer to resolving the various issues surrounding a potential government shutdown at the end of the month, along with a potential debt ceiling crisis in October, which is another flashing alert on the dashboard for investors that’s further contributing to weaker sentiment right now.

Looking ahead now, today’s main highlight will be the latest Federal Reserve decision along with Chair Powell’s subsequent press conference, with the policy decision out at 19:00 London time. Markets have been on edge for any clues about when the Fed might begin to taper asset purchases, but concern about tapering actually being announced at this meeting has dissipated over recent weeks, particularly after the most recent nonfarm payrolls in August came in at just +235k, and the monthly CPI print also came in beneath consensus expectations for the first time since November. In terms of what to expect, our US economists write in their preview (link here) that they see the statement adopting Chair Powell’s language that a reduction in the pace of asset purchases is appropriate “this year”, so long as the economy remains on track. They see Powell maintaining optionality about the exact timing of that announcement, but they think that the message will effectively be that the bar to pushing the announcement beyond November is relatively high in the absence of any material downside surprises. This meeting also sees the release of the FOMC’s latest economic projections and the dot plot, where they expect there’ll be an upward drift in the dots that raises the number of rate hikes in 2023 to 3, followed by another 3 increases in 2024.

Back to yesterday, and as mentioned US equity markets fell for a second straight day after being unable to hold on to earlier gains, with the S&P 500 slightly lower (-0.08%). High-growth industries outperformed with biotech (+0.38%) and semiconductors (+0.18%) leading the NASDAQ (+0.22%) slightly higher, however the Dow Jones (-0.15%) also struggled. Europe saw a much stronger performance though as much of the US decline came after Europe had closed. The STOXX 600 gained +1.00% to erase most of Monday’s losses, with almost every sector in the index ending the day in positive territory.

With risk sentiment improving for much of the day yesterday, US Treasuries sold off slightly and by the close of trade yields on 10yr Treasuries were up +1.2bps to 1.3226%, thanks to a +1.8bps increase in real yields. However, sovereign bonds in Europe told a different story as yields on 10yr bunds (-0.3bps), OATs (-0.3bps) and BTPs (-1.9bps) moved lower. Other safe havens including gold (+0.59%) and silver (+1.02%) also benefited, but this wasn’t reflected across commodities more broadly, with Bloomberg’s Commodity Spot Index (-0.30%) losing ground for a 4th consecutive session.

Democratic Party leaders plan to vote on the Senate-approved $500bn bipartisan infrastructure bill next Monday, even with no resolution to the $3.5tr budget reconciliation measure that encompasses the remainder of the Biden Administration’s economic agenda. Democrats continue to work on the reconciliation measure but have turned their attention to the debt ceiling and government funding bills.Congress has fewer than two weeks before the current budget expires – on Oct 1 – to fund the government and raise the debt ceiling. Republicans yesterday noted that the Democrats could raise the ceiling on their own through the reconciliation process, with many saying that they would not be offering their support to any funding bill. Democrats continue to push for a bipartisan bill to raise the debt ceiling, pointing to their votes during the Trump administration. If Democrats are forced to tie the debt ceiling and funding bills to budget reconciliation, it could limit how much of the $3.5 trillion bill survives the last minute negotiations between progressives and moderates. More to come over the next 10 days.

Staying on the US, there was an important announcement in President Biden’s speech at the UN General Assembly, as he said that he would work with Congress to double US funding to poorer nations to deal with climate change. That comes as UK Prime Minister Johnson (with the UK hosting the COP26 summit in less than 6 weeks’ time) has been lobbying other world leaders to find the $100bn per year that developed economies pledged by 2020 to support developing countries as they reduce their emissions and deal with climate change.

In Germany, there are just 4 days to go now until the federal election, and a Forsa poll out yesterday showed a slight narrowing in the race, with the centre-left SPD remaining on 25%, but the CDU/CSU gained a point on last week to 22%, which puts them within the +/- 2.5 point margin of error. That narrowing has been seen in Politico’s Poll of Polls as well, with the race having tightened from a 5-point SPD lead over the CDU/CSU last week to a 3-point one now.

Turning to the pandemic, Johnson & Johnson reported that their booster shot given 8 weeks after the first offered 100% protection against severe disease, 94% protection against symptomatic Covid in the US, and 75% against symptomatic Covid globally. Speaking of boosters, Bloomberg reported that the FDA was expected to decide as soon as today on a recommendation for Pfizer’s booster vaccine. That follows an FDA advisory panel rejecting a booster for all adults last Friday, restricting the recommendation to those over-65 and other high-risk categories. Staying with the US and vaccines, President Biden announced that the US was ordering 500mn doses of the Pfizer vaccine to be exported to the rest of the world.

On the data front, there were some strong US housing releases for August, with housing starts up by an annualised 1.615m (vs. 1.55m expected), and building permits up by 1.728m (vs. 1.6m expected). Separately, the OECD released their Interim Economic Outlook, which saw them upgrade their inflation expectations for the G20 this year to +3.7% (up +0.2ppts from May) and for 2022 to +3.9% (up +0.5ppts from May). Their global growth forecast saw little change at +5.7% in 2021 (down a tenth) and +4.5% for 2022 (up a tenth).

To the day ahead now, and the main highlight will be the aforementioned Federal Reserve decision and Chair Powell’s subsequent press conference. Otherwise on the data side, we’ll get US existing home sales for August, and the European Commission’s advance consumer confidence reading for the Euro Area in September.

It was Jan. 11, 2024 when software giant Microsoft (MSFT) briefly passed Apple (AAPL) as the most valuable company in the world.

Microsoft's stock closed 0.5% higher, giving it a market valuation of $2.859 trillion.

It rose as much as 2% during the session and the company was briefly worth $2.903 trillion. Apple closed 0.3% lower, giving the company a market capitalization of $2.886 trillion.

"It was inevitable that Microsoft would overtake Apple since Microsoft is growing faster and has more to benefit from the generative AI revolution," D.A. Davidson analyst Gil Luria said at the time, according to Reuters.

The two tech titans have jostled for top spot over the years and Microsoft was ahead at last check, with a market cap of $3.085 trillion, compared with Apple's value of $2.684 trillion.

Analysts noted that Apple had been dealing with weakening demand, including for the iPhone, the company’s main source of revenue.

Demand in China, a major market, has slumped as the country's economy makes a slow recovery from the pandemic and competition from Huawei.

Sales in China of Apple's iPhone fell by 24% in the first six weeks of 2024 compared with a year earlier, according to research firm Counterpoint, as the company contended with stiff competition from a resurgent Huawei "while getting squeezed in the middle on aggressive pricing from the likes of OPPO, vivo and Xiaomi," said senior Analyst Mengmeng Zhang.

“Although the iPhone 15 is a great device, it has no significant upgrades from the previous version, so consumers feel fine holding on to the older-generation iPhones for now," he said.

A man scrolling through Netflix on an Apple iPad Pro. Photo by Phil Barker/Future Publishing via Getty Images.

Counterpoint said that the first six weeks of 2023 saw abnormally high numbers with significant unit sales being deferred from December 2022 due to production issues.

Apple is planning to open its eighth store in Shanghai – and its 47th across China – on March 21.

The company also plans to expand its research centre in Shanghai to support all of its product lines and open a new lab in southern tech hub Shenzhen later this year, according to the South China Morning Post.

Meanwhile, over in Europe, Apple announced changes to comply with the European Union's Digital Markets Act (DMA), which went into effect last week, Reuters reported on March 12.

Beginning this spring, software developers operating in Europe will be able to distribute apps to EU customers directly from their own websites instead of through the App Store.

"To reflect the DMA’s changes, users in the EU can install apps from alternative app marketplaces in iOS 17.4 and later," Apple said on its website, referring to the software platform that runs iPhones and iPads.

"Users will be able to download an alternative marketplace app from the marketplace developer’s website," the company said.

Apple has also said it will appeal a $2 billion EU antitrust fine for thwarting competition from Spotify (SPOT) and other music streaming rivals via restrictions on the App Store.

The company's shares have suffered amid all this upheaval, but some analysts still see good things in Apple's future.

Bank of America Securities confirmed its positive stance on Apple, maintaining a buy rating with a steady price target of $225, according to Investing.com.

The firm's analysis highlighted Apple's pricing strategy evolution since the introduction of the first iPhone in 2007, with initial prices set at $499 for the 4GB model and $599 for the 8GB model.

BofA said that Apple has consistently launched new iPhone models, including the Pro/Pro Max versions, to target the premium market.

Analyst says Apple selloff 'overdone'

Concurrently, prices for previous models are typically reduced by about $100 with each new release.

This strategy, coupled with installment plans from Apple and carriers, has contributed to the iPhone's installed base reaching a record 1.2 billion in 2023, the firm said.

Apple has effectively shifted its sales mix toward higher-value units despite experiencing slower unit sales, BofA said.

This trend is expected to persist and could help mitigate potential unit sales weaknesses, particularly in China.

BofA also noted Apple's dominance in the high-end market, maintaining a market share of over 90% in the $1,000 and above price band for the past three years.

The firm also cited the anticipation of a multi-year iPhone cycle propelled by next-generation AI technology, robust services growth, and the potential for margin expansion.

On Monday, Evercore ISI analysts said they believed that the sell-off in the iPhone maker’s shares may be “overdone.”

The firm said that investors' growing preference for AI-focused stocks like Nvidia (NVDA) has led to a reallocation of funds away from Apple.

In addition, Evercore said concerns over weakening demand in China, where Apple may be losing market share in the smartphone segment, have affected investor sentiment.

And then ongoing regulatory issues continue to have an impact on investor confidence in the world's second-biggest company.

“We think the sell-off is rather overdone, while we suspect there is strong valuation support at current levels to down 10%, there are three distinct drivers that could unlock upside on the stock from here – a) Cap allocation, b) AI inferencing, and c) Risk-off/defensive shift," the firm said in a research note.

Major typhoid fever surveillance study in sub-Saharan Africa indicates need for the introduction of typhoid conjugate vaccines in endemic countries

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high…

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

Credit: IVI

There is a high burden of typhoid fever in sub-Saharan African countries, according to a new study published today in The Lancet Global Health. This high burden combined with the threat of typhoid strains resistant to antibiotic treatment calls for stronger prevention strategies, including the use and implementation of typhoid conjugate vaccines (TCVs) in endemic settings along with improvements in access to safe water, sanitation, and hygiene.

The findings from this 4-year study, the Severe Typhoid in Africa (SETA) program, offers new typhoid fever burden estimates from six countries: Burkina Faso, Democratic Republic of the Congo (DRC), Ethiopia, Ghana, Madagascar, and Nigeria, with four countries recording more than 100 cases for every 100,000 person-years of observation, which is considered a high burden. The highest incidence of typhoid was found in DRC with 315 cases per 100,000 people while children between 2-14 years of age were shown to be at highest risk across all 25 study sites.

There are an estimated 12.5 to 16.3 million cases of typhoid every year with 140,000 deaths. However, with generic symptoms such as fever, fatigue, and abdominal pain, and the need for blood culture sampling to make a definitive diagnosis, it is difficult for governments to capture the true burden of typhoid in their countries.

“Our goal through SETA was to address these gaps in typhoid disease burden data,” said lead author Dr. Florian Marks, Deputy Director General of the International Vaccine Institute (IVI). “Our estimates indicate that introduction of TCV in endemic settings would go to lengths in protecting communities, especially school-aged children, against this potentially deadly—but preventable—disease.”

In addition to disease incidence, this study also showed that the emergence of antimicrobial resistance (AMR) in Salmonella Typhi, the bacteria that causes typhoid fever, has led to more reliance beyond the traditional first line of antibiotic treatment. If left untreated, severe cases of the disease can lead to intestinal perforation and even death. This suggests that prevention through vaccination may play a critical role in not only protecting against typhoid fever but reducing the spread of drug-resistant strains of the bacteria.

There are two TCVs prequalified by the World Health Organization (WHO) and available through Gavi, the Vaccine Alliance. In February 2024, IVI and SK bioscience announced that a third TCV, SKYTyphoid™, also achieved WHO PQ, paving the way for public procurement and increasing the global supply.

Alongside the SETA disease burden study, IVI has been working with colleagues in three African countries to show the real-world impact of TCV vaccination. These studies include a cluster-randomized trial in Agogo, Ghana and two effectiveness studies following mass vaccination in Kisantu, DRC and Imerintsiatosika, Madagascar.

Dr. Birkneh Tilahun Tadesse, Associate Director General at IVI and Head of the Real-World Evidence Department, explains, “Through these vaccine effectiveness studies, we aim to show the full public health value of TCV in settings that are directly impacted by a high burden of typhoid fever.” He adds, “Our final objective of course is to eliminate typhoid or to at least reduce the burden to low incidence levels, and that’s what we are attempting in Fiji with an island-wide vaccination campaign.”

As more countries in typhoid endemic countries, namely in sub-Saharan Africa and South Asia, consider TCV in national immunization programs, these data will help inform evidence-based policy decisions around typhoid prevention and control.

###

About the International Vaccine Institute (IVI)

The International Vaccine Institute (IVI) is a non-profit international organization established in 1997 at the initiative of the United Nations Development Programme with a mission to discover, develop, and deliver safe, effective, and affordable vaccines for global health.

IVI’s current portfolio includes vaccines at all stages of pre-clinical and clinical development for infectious diseases that disproportionately affect low- and middle-income countries, such as cholera, typhoid, chikungunya, shigella, salmonella, schistosomiasis, hepatitis E, HPV, COVID-19, and more. IVI developed the world’s first low-cost oral cholera vaccine, pre-qualified by the World Health Organization (WHO) and developed a new-generation typhoid conjugate vaccine that is recently pre-qualified by WHO.

IVI is headquartered in Seoul, Republic of Korea with a Europe Regional Office in Sweden, a Country Office in Austria, and Collaborating Centers in Ghana, Ethiopia, and Madagascar. 39 countries and the WHO are members of IVI, and the governments of the Republic of Korea, Sweden, India, Finland, and Thailand provide state funding. For more information, please visit https://www.ivi.int.

Incidence of typhoid fever in Burkina Faso, Democratic Republic of the Congo, Ethiopia, Ghana, Madagascar, and Nigeria (the Severe Typhoid in Africa programme): a population-based study

We’ve added 60% to national debt since 2018. Germany - a country with major economic woes - added ‘just’ 32%.

Maybe it will never matter. Maybe MMT is real. Maybe we just cancel or inflate it out. Maybe career real estate borrowers or career politicians aren’t the answer.

I have no idea. Only time will tell. But it’s going to be fascinating to watch it play out.

He is right: it will be fascinating, and the latest budget deficit data simply confirmed that the day of reckoning will come very soon, certainly sooner than the two years that One River's Eric Peters predicted this weekend for the coming "US debt sustainability crisis."

According to the US Treasury, in February, the US collected $271 billion in various tax receipts, and spent $567 billion, more than double what it collected.

The two charts below show the divergence in US tax receipts which have flatlined (on a trailing 6M basis) since the covid pandemic in 2020 (with occasional stimmy-driven surges)...

... and spending which is about 50% higher compared to where it was in 2020.

The end result is that in February, the budget deficit rose to $296.3 billion, up 12.9% from a year prior, and the second highest February deficit on record.

And the punchline: on a cumulative basis, the budget deficit in fiscal 2024 which began on October 1, 2023 is now $828 billion, the second largest cumulative deficit through February on record, surpassed only by the peak covid year of 2021.

But wait there's more: because in a world where the US is spending more than twice what it is collecting, the endgame is clear: debt collapse, and while it won't be tomorrow, or the week after, it is coming... and it's also why the US is now selling $1 trillion in debt every 100 days just to keep operating (and absorbing all those millions of illegal immigrants who will keep voting democrat to preserve the socialist system of the US, so beloved by the Soros clan).

... having already surpassed total US defense spending and soon to surpass total health spending and, finally all social security spending, the largest spending category of all, which means that US debt will now rise exponentially higher until the inevitable moment when the US dollar loses its reserve status and it all comes crashing down.

We conclude with another observation by CNBC's Brian Sullivan, who quotes an email by a DC strategist...

.. which lays out the proposed Biden budget as follows:

The budget deficit will growth another $16 TRILLION over next 10 years. Thats *with* the proposed massive tax hikes.

Without them the deficit will grow $19 trillion.

That's why you will hear the "deficit is being reduced by $3 trillion" over the decade.

No family budget or business could exist with this kind of math.

Of course, in the long run, neither can the US... and since neither party will ever cut the spending which everyone by now is so addicted to, the best anyone can do is start planning for the endgame.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}