Futures At All Time High As Target Reports Record QuarterTyler DurdenWed, 08/19/2020 - 07:58

S&P futures edged higher, alongside European stocks, flirting with record highs and just shy of 3,400 following blockbuster earnings from retailers Target and Lowe’s, a day after the S&P 500 completed its fastest recovery from a bear market in history. The dollar headed for a sixth daily drop while Treasuries rose again, the 10Y yield sliding to 0.6477%.

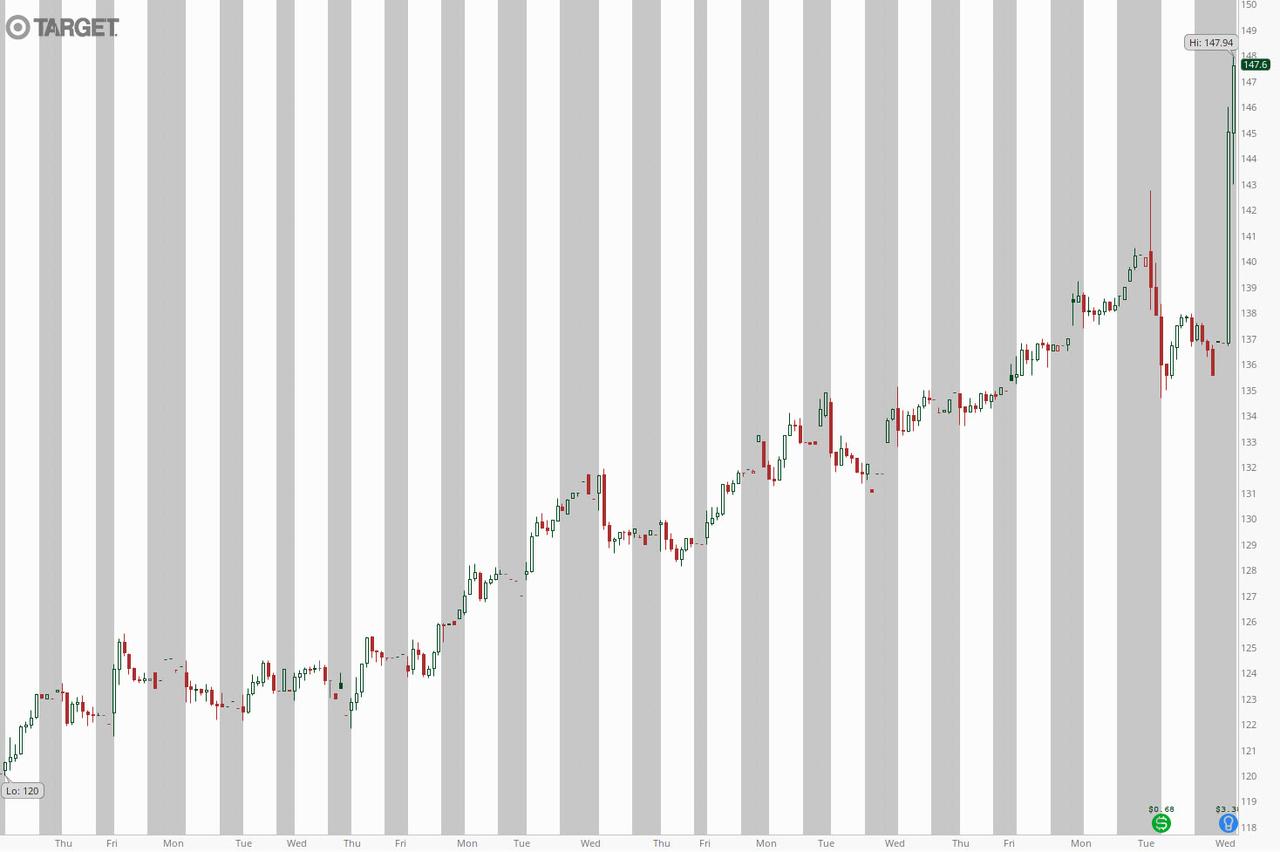

Target Corp soared in premarket trade to a record high of $150 after posting its best quarterly comparable sales growth on record and online revenues that nearly tripled. The supermarket operator reported second-quarter sales that smashed analysts’ expectations, brushing off concerns that demand would ebb after consumers spent their relief checks. Comparable sales rose a record 24% in the three months through Aug. 1, Target said Wednesday - the fastest pace in the retailer’s 58-year history, and almost three times higher than the average estimate of 8.6%. Adjusted earnings per share also touched an all-time high at $3,38, more than double the 1.58 expected, while revenue hit $22.98 billion, beating estimates of $19.82 billion. Additionally, the average Q2 transaction amount rose +18.8% vs. +0.90% y/y, while digital sales as share of total sales rose 17.2% in Q2 vs. 7.30% y/y.

Target CEO Brian Cornell said the retailer attracted consumers’ dollars because they couldn’t go on vacation or spend money on typical summer activities during the pandemic. "We’re not on planes. We’re not spending dollars on lodging, so many of those dollars have been redirected into retail," he said in an interview with CNBC.

Home improvement chain Lowe’s Companies also jumped 2.7% after beating estimates for quarterly same-store sales as it benefited from a surge in demand for its products from consumers stuck indoors. Its larger rival Home Depot and retail behemoth Walmart reported similar results on Tuesday, although they reversed gains after warning that the Q2 selling frenzy was fading as stimulus payments were cut.

On Tuesday, the S&P 500 closed at a new record high, completing a stunning 50% recovery from a dramatic pandemic-led sell-off. The Nasdaq, the first of the three main indexes to confirm a bull market in June, also closed at an all-time high. Only the Dow remains some 6% below February’s record closing high. Yet while trillions of dollars in fiscal and monetary support and a preference for tech-related stocks have helped the benchmark surge about 55% from its March lows, the battered economy is still far from the pre-pandemic levels.

"We have a Federal Reserve that is all in, keeping rates low probably across the curve for as far as the eye can see," Katie Nixon, chief investment officer at Northern Trust Wealth Management, said on Bloomberg TV. "That is supportive of higher valuations."

In a positive signal for equities, Nancy Pelosi suggested that Democrats might be willing to make more cuts to their stimulus proposal to seal a deal with Republicans and speed Covid-19 relief. "The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story," strategists including Craig Nicol at Deutsche Bank AG wrote in a note.

In Europe, the Stoxx 600 reversed early losses, gaining as health-care firms including AstraZeneca and Roche Holding led the index higher.

Earlier in the session, Asia stocks were mixed: sentiment was dampened after President Donald Trump said he called off last weekend’s trade talks. The State Department is also asking colleges and universities to divest from Chinese holdings in their endowments. Australia's S&P/ASX 200 and South Korea's Kospi Index rose; Japan's Topix also gained 0.2% with Softbrain and TEMONA rising the most. Meanwhile, the Shanghai Composite Index retreated 1.2% pausing after recent gains, with Haiqi Transportation and Yijiahe Tech posting the biggest slides.

In FX, the Bloomberg Dollar index fell for a sixth consecutive day, but failed to breach its lowest level in over two years reached Tuesday as profit taking on short exposure was quickly offset by momentum and hedge funds looking to sell even the shortest of rallies. The pound edged higher amid firmer-than-expected U.K. inflation in July and managed to erase this year’s drop versus the greenback. U.S. corporate names and institutional accounts were among the main sellers of the euro around $1.1950 and the pound at $1.3260 on a take-profit basis.

The Aussie climbed, supported by higher iron ore prices, though rising tensions between Australia and China likely limited gains; the Kiwi led gains among Group-of-10 peers as short positions versus the Aussie were unwound. Japan’s yen halted a three-day gain to trade little changed after earlier strengthening toward 105 per dollar as offshore banks earlier sent the Japanese yen to day highs around 105.10, according to three traders in Europe.

The Yuan enjoyed a firm session as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In rates, Treasuries are higher across the curve led by the long end, while bunds gained amid record demand for 30-year German bond sale. Yields are lower by as much as 2.8bp at long end, 10-year by 2.1bp at 0.648%, with front-end yields little changed, flattening 2s10s and 5s30s by ~1.5bp; S&P 500 futures are little changed after cash index closed at a record high Tuesday. 10-year and 30-year yields, which climbed into last week’s record-size auctions of those tenors, are lower for a third straight day, both at lower yields (higher prices) than buyers in the auction obtained. On deck today, bond market prepares to digest a $25BN 20-year bond auction at 1pm ET.

An hour later, at 2pm the Fed is slated to release minutes of July 29 FOMC meeting, which will offer clues into the policymaker’s view of the economy and its actions in September, where Average Inflation Targeting is expected to be unveiled. The market’s focus will also shift to U.S. presidential elections, which is about 11 weeks away. Democrats on Tuesday formally nominated Joe Biden for president. The Republican National Convention is slated for next week.

Also on today's calendar, Analog Devices, TJX and Nvidia are among companies reporting earnings.

Market Snapshot

S&P 500 futures up 0.1% to 3,391.25

STOXX Europe 600 up 0.1% to 367.64

MXAP down 0.04% to 172.34

MXAPJ down 0.2% to 568.35

Nikkei up 0.3% to 23,110.61

Topix up 0.2% to 1,613.73

Hang Seng Index down 0.7% to 25,178.91

Shanghai Composite down 1.2% to 3,408.13

Sensex up 0.6% to 38,759.63

Australia S&P/ASX 200 up 0.7% to 6,167.64

Kospi up 0.5% to 2,360.54

Brent futures down 1% to $45.01/bbl

Gold spot down 0.6% to $1,989.88

U.S. Dollar Index down 0.1% to 92.18

German 10Y yield fell 1.9 bps to -0.482%

Euro up 0.1% to $1.1943

Italian 10Y yield fell 0.4 bps to 0.801%

Spanish 10Y yield fell 0.6 bps to 0.304%

Top Overnight News from Bloomberg

U.K. inflation accelerated to the fastest in four months in July, an unexpected jump that’s unlikely to last or persuade the Bank of England to ease off the stimulus pedal

An auction of 30- year German debt saw the highest demand in the record books, which date back to 1997

The Trump administration sees a possibility for Republicans and Democrats to agree on a smaller round of pandemic relief totaling $500 billion that would omit the biggest areas of disagreement, according to a senior U.S. official

The $20 trillion U.S. Treasury market is giving the Federal Reserve a thumbs-up for its efforts to revive inflation after the coronavirus pandemic threatened to inflict a damaging bout of deflation on the U.S. economy

Japanese exports continued to drop steeply in July even as a recovery in shipments to China helped cushion declines to Europe and other key markets where the coronavirus is spreading rapidly

A quick rundown of global markets courtesy of NewsSquawk.

Asian equity markets sustained the mixed lead from their counterparts on Wall St where the S&P 500 and Nasdaq notched fresh record intraday highs shortly after the open, although the tone briefly soured before picking back up again with participants somewhat tentative and volumes thinner due to the lack of data and risk events ahead. Nonetheless, ASX 200 (+0.7%) was positive with the best performing stocks in the index driven by earnings, while Nikkei 225 (+0.3%) was rangebound as participants digested mixed releases including disappointing Machinery Orders and although trade data printed better than expected, there were still substantial contractions to both Exports and Imports. Elsewhere, Shanghai Comp. (-1.2%) weakened alongside the closure of morning trade in Hong Kong due to a typhoon signal, ultimately, Hang Seng (-0.7%); as well as the continued antagonism between US-China as President Trump noted that he postponed talks with China and does not want to talk with China right now, while he responded “we'll see“ when questioned if he will pull out of the trade agreement. Finally, 10yr JGBs were choppy with mild pressure seen as Japanese stocks just about remained afloat, but with downside also stemmed amid the BoJ presence in the market for JPY 770bln of JGBs with 3yr-10yr maturities.

Top Asian News

Japan Exports Drop Steeply Again as Virus Continues Spread

Bank Indonesia Holds Rates Steady to Safeguard Weak Currency

China Stocks Post Biggest Loss in Three Weeks on U.S. Tensions

European equities trade with little in the way of firm direction (Eurostoxx 50 +0.3%) with ongoing pessimism surrounding US-China relations and stimulus talks in Washington unable to impose any meaningful sway on summer-thinned European markets. Price action thus far has been more of a case of treading water ahead of the US entrance to market, although Europe has seen a modest pick-up in recent trade as indices across the Atlantic continue to eye record highs. From a sectoral standpoint in Europe, energy names are a laggard in-fitting with price action in with some of the modest losses seen in the complex, albeit downside is relatively small in terms of magnitude. Elsewhere, some of the travel & leisure names such as IAG (+2.9%), easyJet (+0.5%) and Ryanair (+0.9%) began the session on a slightly firmer footing amid reports in UK press that Heathrow could expand its testing capabilities in an attempt to replace the imposition of blanket quarantines. Utility names are seen lower in Europe amid losses in RWE (-4.0%) with the DAX-constituent having completed a USD 2bln share issue to support its expansion into renewable energy. Of note for the DAX, investors are awaiting the release of the updated composition of the index at 21:00BST today with reports suggesting that Wirecard could be replaced by Delivery Hero (+0.8%). Maersk (+4.7%) have been a standout outperformer thus far following its Q2 earnings release, in which the Co. beat on estimates for profits and subsequently reinstated guidance at a higher level than indicated previously.

Top European News

Billionaire Greensill’s German Bank Draws Regulatory Scrutiny

Galapagos Suffers Biggest Fall Ever as FDA Fails to Approve Drug

The Best Days May Be Over for Europe’s Stock Rally This Year

U.K. Is Working on Covid Tests at Airports to Ease Quarantine

In FX, The broader Dollar and index are losing steam as the APAC consolidatory strength, which reverberated into early European hours, fades ahead of the FOMC Minutes (Full preview available in the Research Suite). DXY found an overnight base at 92.150 ahead of the YTD low at 92.124, with the index now residing closer to the middle of the current 92.150-92.388 intraday band.

NZD, AUD, CAD - The non-US Dollars posted various degrees of resilience vs. the Buck in overnight trade and have since extended on gains as the Dollar wanes. NZD/USD outperforms in the G10 FX space after finding support at the 0.6600 mark before topping its 21 DMA at 0.6621. AUD/USD gains in tandem after breaching mild resistance around 0.7237-43, but market participants eye a sustained break above the 200 WMA at 0.7255 ahead of the Feb 2019 weekly high at 0.7295. Meanwhile, the Loonie ekes mild gains despite losses in the crude complex with potential technical factors at play - USD/CAD drifted below its 200 DMA (1.3169) overnight before dipping under 1.3150 as it eyes the release of Canadian CPI later today.

GBP, EUR - Both marginally firmer against the USD, although the former saw some fleeting strength on the back of UK CPI metrics notably topping forecasts across the board, mainly due to a less significant decline in clothing prices alongside the easing of lockdown restrictions. Cable meanders around mid-range after printing a post-CPI high of 1.3267 (low 1.3230) ahead of the Dec 31st 2019 high of 1.3283. EUR/USD meanwhile remains within recent ranges and moves in tandem with the USD, having had shrugged off Final CPI figures heading into the European summit on Belarusian sanctions, albeit EU diplomats noted that these are unlikely to be agreed on until the end of this week at the earliest. Note: EUR/USD sees a hefty EUR 1.7bln in options expiring at strike 1.1900 at the NY cut.

CHF, JPY - Mixed trade between the CHF and the JPY, with the former compliant to USD-action and the latter flat after a choppy APAC session amid mixed data and an absence of clear sentiment. USD/CHF inched closer towards 0.9000 to the downside, with yesterday’s low residing at 0.9008. USD/JPY remains sub-105.50 after rebounding from an overnight base at 105.11, with the pair seeing USD 762mln in options rolling off at 105.00 and USD 800mln scattered between 105.25-30. For the technicians, if 105.00 fails to hold then focus will turn on 104.86 which marks the 76.4% Fib of the Jul-Aug rise.

Yuan - A firm session for the Yuan as the recent Dollar weakness prompted the PBoC to set the CNY mid-point at a 7-month high, with today’s USD/CNY setting at 6.9168 vs. yesterday’s 6.9325. USD/CNH was driven lower during the APAC session and briefly traded sub-6.9000 for the first time since January.

In commodities, WTI and Brent October futures have been edging lower in early European trade as participants eye the fallout of the JMMC meeting poised to commence from 15:00BST. Although no fireworks are expected from the meeting, market chatter yesterday noted of a possible recommendation of an early taper of the output cut deal, speculations that were dismissed by Russian Energy Minister Novak last week. Focus will likely fall on the laggards’ compliance levels amid pledges to over-comply to make up for their earlier shortfalls, whilst commentary on the JMMC’s outlook will also garner attention given resurging COVID-19 cases. Alongside the meeting, the weekly EIA inventories will be released, with headline crude forecast to have fallen 2.670mln barrels in the past week after private inventories printed a larger than expected draw of 4mln barrels vs. Exp. -2.7mln – with prices shrugging off the release. Elsewhere, Eastern Libyan authorities are to allow limited and temporary exports from the blockaded oil ports in a bid to free up storage to allow fuel production for fire stations. The blockades have resulted in a build-up in condensates and the reduction of gas production used for power stations. In terms of precious metals, spot gold and silver largely move in tandem with the Dollar amidst a lack of fresh catalysts, with the former meandering just under USD 2,000/oz and the latter just north of USD 27.50/oz. UBS remains constructive on gold over the next 6-month, with its base case is at USD 2,000/oz and an upside case of USD 2,200-2,300/oz, whilst UBS’ silver upside case resides around USD 30-40/oz. Over to base metals, Dalian iron ore continued to rise amid firm demand from China as steel mill outputs remain near record levels. However, analysts at ING note that as uncertainties over Brazilian supply subsides, the bank expects prices to ease. Meanwhile, copper prices gain as mining giant Rio Tinto lowered its copper guidance to 135k-175k tons from 165k-205k tons.

US Event Calendar

7am: MBA Mortgage Applications, prior 6.8%

2pm: FOMC Meeting Minutes

DB's Craig Nicol concludes the overnight wrap

Much of the focus in markets over the last 24 hours has been on yet another leg lower for the dollar. Indeed the dollar index fell -0.62% yesterday - good for a fifth consecutive daily decline – and to the lowest level since April 2018 with the move fairly broad across most major currency pairs with the euro in particular above $1.19 for the first time since May 2018. The lack of fiscal progress has been a big driver of late and has taken the baton from what was initially a more virus-led story. Mnuchin’s comment yesterday about not knowing why a deal seems so far off didn’t do much to help, as did comments from Walmart’s CFO about potential earnings pressure ahead with the end of stimulus checks.

There was one glimmer of good news on the fiscal front late in the US session though, when House Speaker Pelosi indicated that Democrats could pullback their stimulus demands to cut a deal with Republicans now before introducing additional bills after the November elections. With all that in mind it’ll be interesting to see if the FOMC minutes today change the narrative at all with monetary policymakers recently reiterating the need for further fiscal support.

A reminder that at the meeting, Powell noted that the Committee aims to wrap up the policy review in the “near future”, which would be consistent with our economists’ expectation that the results of this review will be released at the September meeting. The minutes should give a sense as to what kind of issues were discussed at the July meeting and how close the Committee is to announcing any changes to how they conduct monetary policy. So, worth keeping an eye on.

Ahead of that the S&P 500 finally closed at an all-time high last night, finishing up +0.23%. The NASDAQ also hit a fresh record high of its own, following a further +0.73% advance. While the weaker dollar certainly helped, the US housing data for July also played a part. Indeed the number of housing starts rose to an annualised 1.496m (vs. 1.245m expected), while building permits also rose to 1.495m (vs. 1.326m expected), in a move that puts them basically back at their pre-Covid levels. It was a somewhat tentative rally again though, with roughly 67% of the S&P down on the day and the majority of the move was driven by retail and communications stocks.

Of course it wouldn’t be a recap without another round of US-China trade headlines. Late last night, President Trump said that he cancelled last weekend’s talks with China, saying “I don’t want to talk to China right now”. He also said “we’ll see what happens” when addressing whether the US would pull out of the phase one trade deal. Prior to this the US administration said that it wants university endowments to divest Chinese holdings, saying it would be “prudent” to get ahead of potentially more onerous measures on holding the shares including a wholesale de-listing of PRC firms from U.S. exchanges. The State Department letter also warned universities of China’s growing influence on campuses and said the US is accelerating investigations of what it called “illicit PRC funding of research, intellectual property theft and the recruitment of talent”.

The Shanghai Comp -0.30%, Shenzhen Comp -0.86% and CSI -0.54% are all lower in response overnight. In contrast, the Nikkei (+0.37%), Kospi (+0.89%) and ASX (+1.10%) are up while the Hang Seng is yet to reopen as we go to print after scrapping the morning session following a typhoon alert. Futures on the S&P 500 are also up with +0.17% gain while spot gold is back below $2000/oz, and bond markets are a touch stronger.

Back to yesterday, where along with the weaker dollar, treasuries continue to unwind some of last week’s selloff. Indeed 10y yields fell by -2.0bps and measures of the curve including 2s10s and 5s30s have now retraced -3.9bps and -3.4bps of the +12.9bps and +15.0bps respective steepening last week. It was a stronger day for bonds in Europe too where 10y bunds closed -1.2bps lower however equity markets closed at their lows for the session – the STOXX 600 down -0.56% - not helped by the stronger euro and also deteriorating virus news including German Chancellor Merkel warning that the recent increase in cases meant that it wouldn’t be possible to ease restrictions further. German cases doubled in the last 3 weeks and are now seeing the highest daily increases in infections in nearly four months. Elsewhere, Amsterdam has increased scrutiny of bars and restaurants to ensure they adhere to guidelines as the number of new cases is on the rise. In Asia, South Korea reported 297 additional cases in the past 24 hours, marking the biggest daily increase since March.

In other virus news, trackthrecovery.com’s updated small business stats in the US showed a continued downward trend through August 7. Small businesses open are now roughly 20% below pre-virus levels and are near the lowest since mid-May. Job postings, while very volatile, fell to near a low for the recession period being down -36%. These stats lines up well with the NY Fed survey that came out yesterday, which could point to lower ISM service index numbers this month. Cases overall in the US rose 0.8% yesterday, in-line with the 0.9% 7-day average.

To the day ahead now, and the data highlights include the UK’s CPI reading for July, the Euro Area’s current account for June, along with Canada’s CPI for July. From central banks, the Fed will be releasing the minutes from their latest meeting and we’ll hear from Richmond Fed President Barkin. Finally, the Democratic vice presidential nominee Kamala Harris will be speaking at the party’s convention.

Mandating COVID-19 vaccination was a mistake due to ethical and other concerns, a top government doctor warned Dr. Anthony Fauci after Dr. Fauci promoted mass vaccination.

“Coercing or forcing people to take a vaccine can have negative consequences from a biological, sociological, psychological, economical, and ethical standpoint and is not worth the cost even if the vaccine is 100% safe,” Dr. Matthew Memoli, director of the Laboratory of Infectious Diseases clinical studies unit at the U.S. National Institute of Allergy and Infectious Diseases (NIAID), told Dr. Fauci in an email.

“A more prudent approach that considers these issues would be to focus our efforts on those at high risk of severe disease and death, such as the elderly and obese, and do not push vaccination on the young and healthy any further.”

Employing that strategy would help prevent loss of public trust and political capital, Dr. Memoli said.

The email was sent on July 30, 2021, after Dr. Fauci, director of the NIAID, claimed that communities would be safer if more people received one of the COVID-19 vaccines and that mass vaccination would lead to the end of the COVID-19 pandemic.

“We’re on a really good track now to really crush this outbreak, and the more people we get vaccinated, the more assuredness that we’re going to have that we’re going to be able to do that,” Dr. Fauci said on CNN the month prior.

Dr. Memoli, who has studied influenza vaccination for years, disagreed, telling Dr. Fauci that research in the field has indicated yearly shots sometimes drive the evolution of influenza.

Vaccinating people who have not been infected with COVID-19, he said, could potentially impact the evolution of the virus that causes COVID-19 in unexpected ways.

“At best what we are doing with mandated mass vaccination does nothing and the variants emerge evading immunity anyway as they would have without the vaccine,” Dr. Memoli wrote. “At worst it drives evolution of the virus in a way that is different from nature and possibly detrimental, prolonging the pandemic or causing more morbidity and mortality than it should.”

The vaccination strategy was flawed because it relied on a single antigen, introducing immunity that only lasted for a certain period of time, Dr. Memoli said. When the immunity weakened, the virus was given an opportunity to evolve.

Some other experts, including virologist Geert Vanden Bossche, have offered similar views. Others in the scientific community, such as U.S. Centers for Disease Control and Prevention scientists, say vaccination prevents virus evolution, though the agency has acknowledged it doesn’t have records supporting its position.

Other Messages

Dr. Memoli sent the email to Dr. Fauci and two other top NIAID officials, Drs. Hugh Auchincloss and Clifford Lane. The message was first reported by the Wall Street Journal, though the publication did not publish the message. The Epoch Times obtained the email and 199 other pages of Dr. Memoli’s emails through a Freedom of Information Act request. There were no indications that Dr. Fauci ever responded to Dr. Memoli.

Later in 2021, the NIAID’s parent agency, the U.S. National Institutes of Health (NIH), and all other federal government agencies began requiring COVID-19 vaccination, under direction from President Joe Biden.

In other messages, Dr. Memoli said the mandates were unethical and that he was hopeful legal cases brought against the mandates would ultimately let people “make their own healthcare decisions.”

“I am certainly doing everything in my power to influence that,” he wrote on Nov. 2, 2021, to an unknown recipient. Dr. Memoli also disclosed that both he and his wife had applied for exemptions from the mandates imposed by the NIH and his wife’s employer. While her request had been granted, his had not as of yet, Dr. Memoli said. It’s not clear if it ever was.

According to Dr. Memoli, officials had not gone over the bioethics of the mandates. He wrote to the NIH’s Department of Bioethics, pointing out that the protection from the vaccines waned over time, that the shots can cause serious health issues such as myocarditis, or heart inflammation, and that vaccinated people were just as likely to spread COVID-19 as unvaccinated people.

He cited multiple studies in his emails, including one that found a resurgence of COVID-19 cases in a California health care system despite a high rate of vaccination and another that showed transmission rates were similar among the vaccinated and unvaccinated.

Dr. Memoli said he was “particularly interested in the bioethics of a mandate when the vaccine doesn’t have the ability to stop spread of the disease, which is the purpose of the mandate.”

The message led to Dr. Memoli speaking during an NIH event in December 2021, several weeks after he went public with his concerns about mandating vaccines.

“Vaccine mandates should be rare and considered only with a strong justification,” Dr. Memoli said in the debate. He suggested that the justification was not there for COVID-19 vaccines, given their fleeting effectiveness.

Julie Ledgerwood, another NIAID official who also spoke at the event, said that the vaccines were highly effective and that the side effects that had been detected were not significant. She did acknowledge that vaccinated people needed boosters after a period of time.

The NIH, and many other government agencies, removed their mandates in 2023 with the end of the COVID-19 public health emergency.

A request for comment from Dr. Fauci was not returned. Dr. Memoli told The Epoch Times in an email he was “happy to answer any questions you have” but that he needed clearance from the NIAID’s media office. That office then refused to give clearance.

Dr. Jay Bhattacharya, a professor of health policy at Stanford University, said that Dr. Memoli showed bravery when he warned Dr. Fauci against mandates.

“Those mandates have done more to demolish public trust in public health than any single action by public health officials in my professional career, including diminishing public trust in all vaccines.” Dr. Bhattacharya, a frequent critic of the U.S. response to COVID-19, told The Epoch Times via email. “It was risky for Dr. Memoli to speak publicly since he works at the NIH, and the culture of the NIH punishes those who cross powerful scientific bureaucrats like Dr. Fauci or his former boss, Dr. Francis Collins.”

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

Mathematicians use AI to identify emerging COVID-19 variants

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants…

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

The framework combines dimension reduction techniques and a new explainable clustering algorithm called CLASSIX, developed by mathematicians at The University of Manchester. This enables the quick identification of groups of viral genomes that might present a risk in the future from huge volumes of data.

The study, presented this week in the journal PNAS, could support traditional methods of tracking viral evolution, such as phylogenetic analysis, which currently require extensive manual curation.

Roberto Cahuantzi, a researcher at The University of Manchester and first and corresponding author of the paper, said: “Since the emergence of COVID-19, we have seen multiple waves of new variants, heightened transmissibility, evasion of immune responses, and increased severity of illness.

“Scientists are now intensifying efforts to pinpoint these worrying new variants, such as alpha, delta and omicron, at the earliest stages of their emergence. If we can find a way to do this quickly and efficiently, it will enable us to be more proactive in our response, such as tailored vaccine development and may even enable us to eliminate the variants before they become established.”

Like many other RNA viruses, COVID-19 has a high mutation rate and short time between generations meaning it evolves extremely rapidly. This means identifying new strains that are likely to be problematic in the future requires considerable effort.

Currently, there are almost 16 million sequences available on the GISAID database (the Global Initiative on Sharing All Influenza Data), which provides access to genomic data of influenza viruses.

Mapping the evolution and history of all COVID-19 genomes from this data is currently done using extremely large amounts of computer and human time.

The described method allows automation of such tasks. The researchers processed 5.7 million high-coverage sequences in only one to two days on a standard modern laptop; this would not be possible for existing methods, putting identification of concerning pathogen strains in the hands of more researchers due to reduced resource needs.

Thomas House, Professor of Mathematical Sciences at The University of Manchester, said: “The unprecedented amount of genetic data generated during the pandemic demands improvements to our methods to analyse it thoroughly. The data is continuing to grow rapidly but without showing a benefit to curating this data, there is a risk that it will be removed or deleted.

“We know that human expert time is limited, so our approach should not replace the work of humans all together but work alongside them to enable the job to be done much quicker and free our experts for other vital developments.”

The proposed method works by breaking down genetic sequences of the COVID-19 virus into smaller “words” (called 3-mers) represented as numbers by counting them. Then, it groups similar sequences together based on their word patterns using machine learning techniques.

Stefan Güttel, Professor of Applied Mathematics at the University of Manchester, said: “The clustering algorithm CLASSIX we developed is much less computationally demanding than traditional methods and is fully explainable, meaning that it provides textual and visual explanations of the computed clusters.”

Roberto Cahuantzi added: “Our analysis serves as a proof of concept, demonstrating the potential use of machine learning methods as an alert tool for the early discovery of emerging major variants without relying on the need to generate phylogenies.

“Whilst phylogenetics remains the ‘gold standard’ for understanding the viral ancestry, these machine learning methods can accommodate several orders of magnitude more sequences than the current phylogenetic methods and at a low computational cost.”

Journal

Proceedings of the National Academy of Sciences

DOI

10.1073/pnas.2317284121

Article Title

Unsupervised identification of significant lineages of SARS-CoV-2 through scalable machine learning methods

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}