Uncategorized

Four Generations of Workers Are Preparing for Retirement Amid an Uncertain Future

Four Generations of Workers Are Preparing for Retirement Amid an Uncertain Future

PR Newswire

LOS ANGELES, Oct. 12, 2022

New research examines the retirement prospects of Baby Boomers, Generation X, Millennials, Generation Z

LOS ANGELES, Oct. 12, 2…

Share this:

Four Generations of Workers Are Preparing for Retirement Amid an Uncertain Future

PR Newswire

LOS ANGELES, Oct. 12, 2022

New research examines the retirement prospects of Baby Boomers, Generation X, Millennials, Generation Z

LOS ANGELES, Oct. 12, 2022 /PRNewswire/ -- Seventy-six percent of workers say their life priorities changed as a result of the pandemic, and 56 percent cite saving for retirement as a financial priority, according to Emerging From the COVID-19 Pandemic: Four Generations Prepare for Retirement, a survey report released today by nonprofit Transamerica Center for Retirement Studies® (TCRS) in collaboration with Transamerica Institute®.

"Today's workers are emerging from a pandemic and navigating megatrends such as population aging, increases in longevity, workforce disruptors, and concerns about Social Security," said Catherine Collinson, CEO and president of Transamerica Institute and TCRS. "Despite an unclear future, workers of all ages are envisioning and saving for an active and purposeful retirement – but are they adequately preparing?"

As part of TCRS' 22nd Annual Retirement Survey, one of the largest and longest-running surveys of its kind, the study delves into the retirement outlook of U.S. workers aged 18 and older and employed by for-profit companies. Comparing Baby Boomers, Generation X, Millennials, and Generation Z, the study illustrates how workers' expectations and preparations differ and how the retirement landscape has evolved.

Baby Boomers (Born 1946 to 1964)

"Baby Boomers have re-written societal rules at every stage of their lives, including retirement. With aspirations of working into older age and a flexible transition to retirement, they are upending the notion that work and retirement are mutually exclusive. As a result, they are paving the way for future generations," said Collinson.

Many Baby Boomers were already mid-career when the retirement landscape began shifting from traditional defined benefit pension plans toward 401(k) or similar plans. They started saving at an older age than younger generations and have not enjoyed the same long-term time horizon to grow their investments. Emerging from the pandemic, Baby Boomers have been susceptible to employment risks, volatility in the financial markets, and increasing inflation – all of which could disrupt their retirement plans.

Forty percent of Baby Boomer workers expect Social Security to be their primary source of retirement income. Eighty-three percent are saving for retirement in an employer-sponsored 401(k) or similar plan and/or outside the workplace. They began saving at age 35 (median). Those participating in a 401(k) or similar plan contribute 10 percent (median) of their annual pay. Baby Boomer workers have saved $162,000 (estimated median) in total household retirement accounts but only $15,000 (median) in emergency savings.

Almost half of Baby Boomer workers (49 percent) expect to or already are working past age 70 or do not plan to retire. Their reasons for doing so are almost as likely to be healthy aging-related (78 percent) as financial-related (82 percent). However, their success depends on support from employers. Just 59 percent say their employers are age-friendly (for example, by offering opportunities, work arrangements, training and tools needed for employees of all ages to be successful).

"Baby Boomers are extending their working lives, which can help bridge savings shortfalls. However, it's important for them to have backup plans because life's unforeseen circumstances could derail their best intentions," said Collinson.

Generation X (Born 1965 to 1980)

Generation X began entering the workforce in the 1980s and 1990s when 401(k) plans were brand new and traditional defined benefit plans were starting to vanish from the retirement landscape. They were early adopters of 401(k) plans and the first generation who could potentially have access to them for the majority of their careers. However, back in the 1980s and 1990s, 401(k)s were relatively primitive, with few investment options, limited investment education and guidance, and printed quarterly statements sent via U.S. mail.

Only 22 percent of Generation X workers are "very" confident they will be able to fully retire with a comfortable lifestyle and just 28 percent "strongly agree" they are building a large enough retirement nest egg. Seventy-eight percent are concerned that Social Security will not be there for them when they are ready to retire.

Eighty-one percent are saving for retirement in an employer-sponsored 401(k) or similar plan and/or outside the workplace. Generation X began saving at age 30 (median). Those participating in a 401(k) or similar plan contribute 10 percent (median) of their annual pay. They have saved $87,000 (estimated median) in total household retirement accounts but only $5,000 (median) in emergency savings.

Generation X workers seek to extend their working years with more time to save. Thirty-eight percent expect to retire at age 70 or older or do not plan to retire, and 55 percent plan to work in retirement. They have an opportunity to set forth goals: Only 27 percent have a financial strategy for retirement in a written plan.

"Most Generation X workers are saving for retirement, but many may fall short. The oldest Generation Xers are now in their late 50s and the youngest are in their early 40s, so there is no time like the present to build their savings and create long-term financial plans," said Collinson.

Millennials (Born 1981 to 1996)

Millennials entered the workforce around the Great Recession, which began in late 2007. They experienced a turbulent economy in their early working years. They started their careers with higher levels of student debt than previous generations. Millennials have waited to buy homes, get married, and start families – but with the increasingly widespread availability of 401(k) plans, they made a solid and early start in saving for retirement.

Most Millennial workers (84 percent) say their life priorities have changed as a result of the pandemic and 68 percent are concerned about their mental health. Thirty-four percent were unemployed at some point during the pandemic for various reasons. Six in 10 cite paying off debt as a financial priority (60 percent).

Three in four Millennial workers (76 percent) are saving for retirement in a 401(k) or similar plan and/or outside the workplace. They began saving at age 25 (median). Those participating in a 401(k) or similar plan contribute 15 percent (median) of their annual pay. Millennial workers have saved $50,000 (estimated median) in total household retirement accounts but just $3,000 (median) in emergency savings.

Fifty-two percent expect their primary source of retirement income to be self-funded savings, including 401(k)s, 403(b)s, and IRAs (40 percent) or other savings and investments (12 percent). Seventy-three percent are concerned that Social Security will not be there for them when they are ready to retire.

"Many Millennials will be called upon as caregivers for aging parents or loved ones. But, unfortunately, this invaluable labor of love could be at the expense of their employment and ability to save for retirement," said Collinson. Forty-two percent of Millennial workers are currently serving and/or have served as a caregiver for a relative or friend during their working career.

Generation Z (Born 1997 to 2012)

"Generation Z workers are young and have decades to grow their retirement savings. In addition, they will change employers many times throughout their careers, and likely spend time in self-employment, so they must be diligent in managing their retirement savings, especially during transitions," said Collinson.

Generation Z entered the workforce shortly before COVID-19 when unemployment rates were at historic lows, then skyrocketed at the onset of the pandemic, and have since returned to lows as workers have been reluctant to return to the workforce. Despite this tumultuous start to their careers, Generation Z will have even greater access to 401(k)s and workplace retirement plans than their predecessors.

The pandemic has been especially difficult for Generation Z workers. Fifty-nine percent often feel anxious and depressed. Fifty-two percent experienced one or more negative impacts on their employment, ranging from layoffs and furloughs to reductions in hours and pay. Fifty-one percent have trouble making ends meet. Yet, they have not given up on retirement.

Sixty-seven percent of Generation Z workers are saving through employer-sponsored 401(k)s or similar retirement plans and/or outside the workplace – and they started saving at the unprecedented young age of 19 (median). Those participating in a 401(k) or similar plan contribute 20 percent (median) of their annual pay. Generation Z workers have saved $33,000 (estimated median) in total household retirement accounts but only $2,000 (median) in emergency savings.

"As we look toward the future, a future in which all Americans can retire with dignity, policymakers must take center stage in orchestrating ways to strengthen the retirement system for current and future generations. Likewise, employers must continue to play a vital societal role by providing jobs, income, and benefits to help workers protect their health and finances and facilitate saving and investing for retirement. And the private sector must continue innovating products, services, and solutions that can help people live, work, save, and retire better. We're all in this together," said Collinson.

Emerging From the COVID-19 Pandemic: Four Generations Prepare for Retirement provides detailed survey findings about Baby Boomers, Generation X, Millennials, and Generation Z. It also provides recommendations for workers, employers, and policymakers. To download the report, visit www.transamericainstitute.org. Follow on Twitter @TCRStudies.

About Transamerica Center for Retirement Studies

Transamerica Center for Retirement Studies® (TCRS) is an operating division of Transamerica Institute®, a nonprofit, private foundation. Transamerica Institute is funded by contributions from Transamerica Life Insurance Company and its affiliates. TCRS and its representative cannot give ERISA, tax, investment, or legal advice. This material is provided for informational purposes only and should not be construed as ERISA, tax, investment, or legal advice. Interested parties must consult and rely solely upon their independent advisors regarding their situation and the concepts presented here. For more information about TCRS, please refer to www.transamericainstitute.org and follow TCRS on Twitter at @TCRStudies.

About the 22nd Annual Transamerica Retirement Survey

The 28-minute online survey was conducted within the U.S. by The Harris Poll on behalf of Transamerica Institute and TCRS between October 28 and December 10, 2021 among a nationally representative sample of 5,493 workers in a for-profit company employing one or more employees, including 398 Generation Z, 2,326 Millennials, 1,631 Generation X, 1,100 Baby Boomers, and 38 workers born before 1946. Results were weighted where necessary to align with the population of U.S. residents, referencing Census data for education, age, gender, race/ethnicity, region, household income, education, employment, marital status, and size of household. Weighting also adjusts for attitudinal and behavioral differences between those who are online versus those who are not, those who join online panels versus those who do not, and those who respond to surveys versus those who do not.

Transamerica Center for Retirement Studies®

Los Angeles, Calif.

Media Contact: Morgan Karbowski

mkarbowski@webershandwick.com

425-753-5719

View original content to download multimedia:https://www.prnewswire.com/news-releases/four-generations-of-workers-are-preparing-for-retirement-amid-an-uncertain-future-301646874.html

SOURCE Transamerica Center for Retirement Studies

Uncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

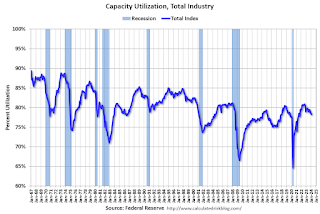

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

{kind=link}

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Futures Rise To New Record High Ahead Of Data Deluge

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex