Euphoria Goes To 11: Futures, Global Markets, Bitcoin Soar As Dollar Collapse Continues

Euphoria Goes To 11: Futures, Global Markets, Bitcoin Soar As Dollar Collapse Continues

Tyler Durden

Thu, 12/17/2020 – 08:12

Global stocks scaled new record highs, bitcoin exploded to never before seen levels and oil also marched higher on…

Share this:

Global stocks scaled new record highs, bitcoin exploded to never before seen levels and oil also marched higher on Thursday as investors waved in anything that isn't nailed down, on hopes of a U.S. fiscal stimulus and the Federal Reserve’s pledge to keep pumping cash into markets and extending FX swap lines, which naturally kept pressure on the dollar. At 7:15am, S&P 500 E-minis were up 18 points, or 0.49%, trading off openinghighs. Dow E-minis were up 100 points, or 0.35%, while Nasdaq 100 E-minis were up 59.75 points, or 0.41%.

Big banks such as JPMorgan, Wells Fargo, Morgan Stanley, Citigroup, Bank of America and Goldman Sachs Group rose between 0.3% and 0.8% in premarket trade after Wells Fargo bank analyst Mike Mayo raised his price target for top-pick Goldman Sachs by 20% to $310 on the heels of recent winning deals like DoorDash and Snowflake. He also lifted PTs across large banks, with outperformance since what he referred to as “Pfizer Monday” when news of vaccine efficacy hit on Nov. 9, likely to continue amid strong capital markets, better-than-expected credit and declining costs. 4Q’s capital markets momentum in mergers, acquisition financing, IPOs and trading will keep going more than investors expect, he said, due to “cheap money, high stocks, and heightened client activity.”

Already euphoric sentiment was lifted by the Federal Reserve which kept interest rates at near-zero levels on Wednesday and vowed to keep funneling cash into financial market furnaces over the long term. Equity markets have been among the main beneficiaries of accommodative policy through the virus outbreak. The Nasdaq ended Wednesday at a second consecutive record high, and this trend was set to continue on Thursday. Bitcoin hit another all-time high, briefly topping $23,000 after first shattering the $20,000 level on Wednesday.

Adding to the optimism, U.S. congressional negotiators were “closing in on” a $900 billion COVID-19 aid bill expected to include $600-$700 stimulus checks to individuals, lawmakers said on Wednesday. Speaking to Reuters, a trader in London pointed to chances of a new retail-led boost to stock markets, referring to the stimulus checks issued during the Spring which led to money pouring into stock markets and bitcoin from punters, helping stocks recover quickly from the COVID-19 blow.

“We should be careful as to how much we extrapolate U.S. consumer spending – after all, this stimulus package would simply replace expiring stimulus programmes, to a large extent,” said Edmund Shing, chief investment officer at BNP Paribas Wealth Management. “So it is not just additional stimulus, but rather maintenance of existing stimulus."

That nuance was lost on markets where the general risk-on mood sent the dollar to 2-1/2-year lows against major peers, while the MSCI world stock index reached a new high of 639.33. The index has climbed 16% since the end of October. Since then, multiple COVID-19 vaccine breakthroughs have been announced.

European stocks and the euro rallied for the fourth straight session as investors built up positions in riskier assets, anticipating a sharp economic recovery in 2021 backed by wider vaccine rollouts and ultra-easy monetary policy. Europe's Stoxx 50 rose 0.6%, with Germany's DAX outperforming while the FTSE 100 traded flat after the BOE kept policy unchanged. Miners, media and retailers are the best performers in Europe with telecoms the only sector in the red. V2X briefly trades a 19-handle.

Earlier in the session, Asian stocks also advanced with MSCI’s index of Asia-Pacific shares ex-Japan rising 0.6% to a record high. Japan’s Nikkei rose 0.2% - just shy of a 29-year peak. Hong Kong shares ended the day up 0.8%, bolstered by a more than 2% gain for both Tencent and Alibaba. Chinese drugmakers also jumped as investors bet the latest round of negotiations for firms to enter the national reimbursement drug list will result in milder price cuts than previous rounds. Australia’s ASX 200 climbed 1.2% as employers added more than twice the number of jobs forecast, helped by a hiring surge in Victoria. The country’s mid-year budget update showed the government’s books in better shape than two months ago. Korean shares saw modest losses, with concerns rising over the possibility of the government raising its social distancing alert to the highest level. Some cryptocurrency-linked stocks jumped in Korea and elsewhere in Asia after Bitcoin surpassed $22,000 for the first time. Central banks in Indonesia, the Philippines and Taiwan kept interest rates unchanged. All three markets closed in the red. Overall, the MSCI Asia Pacific Index rose 0.7%, helped by gains in Chinese stocks.

In rates, Treasuries traded a narrow range, slightly cheaper across the curve in early U.S. trading as S&P 500 futures attain new highs and European stocks rally. Yields remained within a basis point of Wednesday’s closing levels, 10-year around 0.92%, close to where it stood just before FOMC rate decision, which sparked a temporary selloff as bond-buying program was left unchanged. European bonds are relatively quiet with bund futures either side of 177.50, German curve marginally richer and steeper. Gilts weakened slightly after Bank of England policy decision. Peripheral and semi-core spreads tighten marginally to Germany.

In FX, the Bloomberg Dollar Spot Index fell a fourth consecutive day as the greenback was lower versus all of its Group-of-10 peers; the euro rose a fourth day to a high of $1.2244. “While we expect stocks to benefit further from positive news on vaccine rollouts and U.S. fiscal support, the same cannot be said for the US dollar,” said Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.“We see further (dollar) weakness ahead."

Norway’s krone led gains, rising to a more-than-three month high against the euro after the central bank lifted its rate path more than expected, signaling a first rate hike in early 2022. The pound climbed to a two-and-a-half-year high against the dollar, largely unchanged after the BoE announcement. The New Zealand dollar reached highest since April 2018 after Finance Minister Grant Robertson says there is no discomfort with level of the kiwi; the Australian dollar also climbed amid weak greenback and strong jobs print. Bitcoin breached $23,000 for the first time as more Wall Street names crowd into the the world’s largest digital currency up 220% this year.

The Swiss National Bank also kept its ultra-expansive monetary policy on hold, keeping the world’s lowest interest rates and staying ready to launch currency interventions despite being labelled a currency manipulator by the United States. The Bank of England followed suit, also leaving policy unchanged without a mention of negative rates.

In commodities, crude futures fade Asia’s rally; WTI falls back to $48 having traded highs of $48.59 earlier in Europe; Brent falls back below $51.50. Gold advanced to $1,883/oz before fading half the move after the Federal Reserve strengthened its commitment to brrrr. Base metals are in the green amid the broad risk-positive environment, with LME zinc outperforming.

Looking at the day ahead, data releases from the US include November’s housing starts, building permits, December’s Philadelphia Fed Business Outlook and Kansas City Fed manufacturing activity, along with the weekly initial jobless claims. Finally, the FDA will be meeting to discuss an Emergency Use Authorization for the Moderna vaccine.

Market Snapshot

- S&P 500 futures up 0.6% to 3,721.25

- STOXX Europe 600 up 0.5% to 397.95

- MXAP up 0.6% to 197.14

- MXAPJ up 0.6% to 651.20

- Nikkei up 0.2% to 26,806.67

- Topix up 0.3% to 1,792.58

- Hang Seng Index up 0.8% to 26,678.38

- Shanghai Composite up 1.1% to 3,404.87

- Sensex up 0.6% to 46,921.79

- Australia S&P/ASX 200 up 1.2% to 6,756.67

- Kospi down 0.05% to 2,770.43

- Brent futures up 0.5% to $51.35/bbl

- Gold spot up 0.7% to $1,877.74

- U.S. Dollar Index down 0.5% to 89.97

- German 10Y yield fell 1.3 bps to -0.58%

- Euro up 0.2% to $1.2228

- Italian 10Y yield rose 1.7 bps to 0.426%

- Spanish 10Y yield fell 0.7 bps to 0.016%

Top Overnight News from Bloomberg

- European authorities are pushing for a compressed approval timeline for the Covid-19 vaccine from Pfizer Inc. and BioNTech SE, according to people familiar with the plan, which could enable a rollout on the continent before Christmas

- Germany will sell a record amount of federal debt in 2021 to help prop up the economy in the second year of the coronavirus crisis. Europe’s benchmark issuer plans to sell as much as 471 billion euros ($576 billion) in bonds and bills, easily exceeding a previous high of 407 billion euros sold this year, according to the Federal Finance Agency’s provisional calendar published Thursday

- The Swiss National Bank renewed its pledge to use currency interventions to counter upward pressure on the franc just a day after being censured by the U.S. for the practice

- French President Emmanuel Macron tested positive for Covid-19, his office said in statement Thursday

A quick look at global markets courtesy of NewSquawk

Asian equity markets gradually shrugged off the early indecision following a mixed lead from Wall Street as markets digested the FOMC meeting where the Fed kept rates unchanged, enhanced its guidance and refrained from extending the weighted average maturity of purchases. As a potential adjustment to the WAM was seen to be a coinflip, this resulted in some unwinding of dovish bets before Fed Chair Powell reaffirmed a firm dovish stance at the presser, while participants also continue to await any breakthrough in government spending and COVID-19 relief discussions with negotiators reportedly closing in on a USD 900bln COVID-19 aid bill. ASX 200 (+1.2%) was higher with gains led by strength in tech which found inspiration from the outperformance of the sector stateside, while miners and financials also notched respectable gains, with the overall mood further underpinned by strong jobs data. Nikkei 225 (+0.2%) was indecisive as exporters contended with the recent fluctuations of the domestic currency and the KOSPI (-0.1%) lagged as record daily new COVID-19 infections added to the drag on the index which pulled back from near all-time highs. Hang Seng (+0.8%) and Shanghai Comp. (+1.1%) eventually conformed to the mostly constructive tone although price action was initially choppy after a neutral PBoC liquidity operation and with the latest headlines continuing to underscore tensions surrounding China as USTR Lighthizer suggested that President-elect Biden should insist China stick to the Phase 1 trade deal and US SEC announced that Chinese coffee company Luckin Coffee agreed a USD 180mln fine to settle accounting fraud charges. Finally, 10yr JGBs were rangebound and languished near support at 152.00 with price action hampered by indecision in Japanese stocks and as the BoJ kick starts its 2-day policy meeting.

Top Asian News

- Japan Post Insurer Plans $2.9 Billion Buyback From Parent

- Robertson Signals Unease With RBNZ’s Requested Housing Tool

- Scandal-Hit Finablr Sold for $1 to Israeli-UAE Consortium

- Indonesia, Philippines Hold Rates as Virus Recovery Continues

European equities trade higher across the board (Eurostoxx 50 +0.6%) after extending on initial upside at the cash open throughout the morning. Price action for Europe comes in the wake of an initially indecisive Asia-Pac session after a mixed lead from Wall St. post-FOMC whereby policymakers kept rates unchanged, enhanced guidance and refrained from extending the weighted average maturity of purchases, before Fed Chair Powell reaffirmed a dovish stance at the press conference and hammered home the point that markets will remain highly accommodative. Sentiment was also underpinned yesterday by reports that negotiators on Capitol Hill were nearing an agreement on a USD 900bn COVID relief package. The deal is yet to be formally signed off, however, given the mood music yesterday amongst officials and reporters, markets are now assuming that the package will get the green light shortly. Sectors in Europe trade firmer (ex-telecoms) with outperformance in retail, media and basic resources names. For basic resources, sentiment has largely been underpinned by price action in the metals complex, whilst for Rio Tinto (+1.7%) specifically, CFO Stausholm has been appointed as CEO from January 1st. Media names have been aided by gains in FTSE 100 outperformer WPP (+4.4%) after the Co. announced it expects sales to return to pre-pandemic levels by a year 2022, which was a year earlier than expected. Elsewhere, Talk Talk (+3.0%) are firmer on the session after the Co. recommended to shareholders the acquisition by Toscafund for GBP 0.97/shr, whilst Zalando (+3.4%) are a notable gainer in the Stoxx 600 after being upgraded to buy from neutral at UBS.

Top European News

- EU Is Said to Expedite Covid Vaccine for Pre-Christmas Rollout

- TalkTalk Agrees to $1.5 Billion Toscafund Take-Private Bid

- SNB Reacts to Climate Calls, Cuts Coal Firms From Investments

- EBay $9.2 Billion Unit Sale to Adevinta Faces U.K. Probe

In FX, not much bang for the Buck via the FOMC as a knee-jerk rebound on initial hawkish market perceptions quickly faded and reversed in wake of Fed chair Powell’s more dovish/cautious press conference reiterating high uncertainty over the near term economic outlook and repeating that accommodative policy will remain in place until substantial progress towards inflation and employment goals is seen. In short, no rate normalisation for some time even though a couple of dot plots pencil in hikes in 2023, while QE may yet be expanded/extended, and any tapering will be flagged well in advance to avoid another tantrum. Hence, plenty to counter disappointment over no shift in the WAM towards the longer end of the curve and the Greenback has subsequently fallen further, with the index struggling to keep sight of the 90.000 handle between 90.282-89.879 parameters amidst all round losses ahead of a raft of US data.

- NOK/CHF - In stark contrast to the above, hawkish vibes from the Norges Bank in terms of a steeper repo rate path have compounded gains and outperformance in the Norwegian Krona that has now scaled 10.5000 against the Euro, while the Franc has also rallied in wake of the SNB’s quarterly policy review as the key 3 month benchmark was held and highly valued currency assessment maintained. However, Usd/Chf is holding above 0.8800 and Eur/Chf appears reluctant to stray far from 1.0800, partly due to ongoing Euro appreciation vs the Dollar, but mainly in acknowledgment of the fact that the Swiss Central Bank reaffirmed its commitment to continue intervening to stop the Franc strengthening too much regardless of the currency manipulation assignation by the US.

- AUD/NZD/GBP - After labouring somewhat around 0.7550 in the run up to jobs data, the Aussie has made pretty light work of hurdling 0.7600 and approaching 0.7650 following another hefty and well above consensus rise in payrolls and lower than forecast unemployment rate to back up the Treasurer’s view that the economy is rebounding strongly. Similarly, the Kiwi has overcome qualms around 0.7100 to breach 0.7150 on the back of a firmer than anticipated rebound in NZ Q3 GDP and an apparent green light from Finance Minister Robertson who is not that uncomfortable with the Nzd’s level given the stronger than predicted economic recovery. Next up for the Kiwi, trade data and the export side of the equation may not be quite as dismissive. Elsewhere, the Pound looks primed to take on another round number just shy of 1.3600 and is eyeing 0.9000 again in Eur/Gbp cross terms as chief EU Brexit negotiator Barnier reports more progress towards a trade accord with the UK, as talks enter the final stage, albeit with stumbling blocks still obscuring the tunnel exit. More immediately, the spotlight falls on Threadneedle Street, though the bar is set high for any further BoE policy tweaks after November’s APF action – see the Newsquawk Research for our in depth preview of the MPC meeting.

- JPY/CAD/EUR/SEK - Also taking advantage of their US counterpart’s demise, with the Yen on the cusp of 103.00 just a day before the BoJ, Loonie revisiting 1.2700 with some assistance from firm oil prices, Euro extending upwards from 1.2200 to loftier y-t-d highs not far from 1.2250 and Swedish Crown trying to keep pace with its Scandinavian peer after considerably firmer than expected labour data, but lagging behind around 10.1600 in percentage terms.

- EM - Broad gains at the expense of the Usd, but the Czk and Mxn will be looking for independent direction and guidance from the CNB and Banxico, with the latter also eyed for further reaction to recent moves by the Government to revise its mandate.

In commodities, WTI and Brent are moving very much in lockstep with the broader risk narrative this morning and as such exhibit gains of around 0.3% or USD ~0.20/bbl as things stand. Newsflow explicitly for the complex has been sparse for much of the session as have updates on broader macro themes, aside from rate decisions, as we approach month/quarter/year end. Explicitly, the Saudi Energy Minister stated the current OPEC+ agreement which is intended for a two-year period could be extended further if deemed necessary and that the bloc will continue its management of the oil market. Price action throughout the morning has seen WTI and Brent wain off earlier highs somewhat, very much in-fitting with equity performance throughout the morning and similarly precious metals have continued to make gains on the back of the depressed USD with the DXY below 90.00 and spot gold elevated to a USD 1883.30/oz peak for the session thus far. Sticking with gold, RBC believed the precious metal will lose some of its allure in 2021 and into 2022 as well; lowering their 2021 forecast to USD 1875/oz vs prev. USD 1942/oz and the 2021 forecast to USD 1810/oz vs prev. USD 1893/oz.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 815,000, prior 853,000; Continuing Claims, est. 5.7m, prior 5.76m

- 8:30am: Housing Starts, est. 1.54m, prior 1.53m; Building Permits, est. 1.56m, prior 1.55m

- 8:30am: Philadelphia Fed Business Outlook, est. 20, prior 26.3

- 11am: Kansas City Fed Manf. Activity, actual 14, est. 9, prior 11

DB's Jim Reid concludes the overnight wrap

We sent the kids to “Christmas Camp” yesterday at their nursery/school and we had our first outing during the day alone since having kids. We did a 10-mile walk and had a big Xmas lunch in a very quiet country pub near where we live. We didn’t run out of things to chat about until at least mile 4!! Notwithstanding that it was absolutely wonderful to have a day off that didn’t involve looking after children. I then spent the afternoon surreptitiously trying to record a song I’ve written about the twins for my wife’s Xmas present which I will create a photo based video to go alongside it. It’s certainly cheaper than jewellery. Anyway the most expensive Xmas present I’ve ever bought her wasn’t a success so I’m trying the cheap option. It was a huge oil painting I commissioned based on one of our wedding photos. I thought it was wonderful but as someone who went to art college she was a bit shocked when I unveiled it at Xmas 2013. She immediately thought it was a bit tacky and couldn’t hide that she didn’t like it!! However 7 years on it hangs in our hallway, is almost life size, and is the first thing you see as you come in our house. I wore her down.

The Fed last night didn’t provide any new Xmas gifts for financial markets but Mr Powell did everything he could to convince investors that they had no intention of taking any of the many previous presents away from them anytime soon. The committee noted that they would maintain the current pace of QE until achieving "substantial further progress" towards their dual mandate goals.

There was no movement on WAM (as expected) and when asked specifically about it, Powell said that the new language surrounding the forward guidance was “powerful”, while also choosing not to provide a level that either inflation or unemployment would need to hit in order to change the pace of asset purchases. He added that WAM, was “not something high on our list in terms of possibilities". The Fed also published its refreshed ‘dot plot’, with one more dot showing a hike in 2023, but this was also relatively expected. One wrinkle was the inflation outlook into 2023, namely four officials moved from the 1.9-2% to the 2.1-2.2% bucket, thereby shifting the central tendency to 2.1% - a small overshoot of the target. See our economists’ review of the meeting here.

In terms of the market reaction the S&P 500 dropped -0.2% shortly after the written statement before rebounding over half a per cent during the Powell press conference before dipping slightly to settle up +0.18% on the day. There was not that much movement under the surface either, as 21 of 24 industry groups moved less than 1.0% on the day. 10yr breakevens rose to 1.93%, their highest since April 2019. The US 10yr itself rose +0.8bps to 0.916%. The Dollar index fell to fresh 2-year low, with the euro climbing above $1.22 in trading for first time since April 2018, while the US Dollar index fell -0.03% - the third daily retreat for the index, which is now also at its lowest level since April 2018. The index is down a further -0.45% this morning. With the lower dollar, metals rose with Gold up +0.60% and Silver +3.40%. Another major move was Bitcoin (+9.17%), which climbed above $20,000 early in the day, powered through $21,000 later, and then has now poked its head above $22,000 this morning in Asia. It is now up +210.7% on the year and up +16.8% from 2017 highs. As someone who has long believed there will be a search for alternative currencies due to constant fiat money debasement it does feel that Bitcoin will continue to be in high demand.

There was further stimulus talk as well with Congressional leaders continuing to try and get legislation done by the end of the week. House Majority Leader Hoyer said the deal could come together quickly enough to get a House vote later on today, however a Friday vote would mean that the Senate likely has to vote over the weekend. Any spillage into the weekend would require another continuing resolution as the government is set to run out of funding at midnight on Friday. New deal specifics from yesterday include direct payments of $600 to $700 for individuals and $300-per-week in enhanced unemployment benefits according to GOP Senator Thune. While the deal won’t have the $160 billion specifically for state-and-local aid, it could include other avenues give states funding. There have been talks for $100 billion for schools and universities along with additional funds for vaccine distribution.

Earlier in Europe, risk assets put in a strong performance ahead of the Fed meeting, with the STOXX 600 (+0.82%) and the DAX (+1.52%) indices both climbing to their highest levels since the pandemic began. The moves were supported by positive upward surprises in the December flash PMIs, which painted a stronger picture of economic performance in Europe than had been expected. The composite PMI for the Euro Area came in at 49.8 (vs. 45.7 expected), with both the German (52.5) and French (49.6) composite readings coming in above expectations. Elsewhere, sovereign bonds sold off as investors rotated out of safer assets, with yields on ten-year bunds up 4.4bps, and in another milestone, the spread of 10yr Italian yields over bunds fell -2.7bps to a 4-year low of just 1.10%.

The aforementioned stimulus discussions in the US looked ever more needed after economic data from the country was rather less rosy however, with retail sales in November contracting by -1.1% month-on-month (vs. -0.3% expected), while the October reading was revised down four-tenths as well to show a -0.1% contraction.

Overnight Asian markets are largely trading up outside of the Kospi (-0.36%) which is down. The Nikkei (+0.16%), Hang Seng (+0.18%), Shanghai Comp (+0.63%), and Asx (+1.16%) are all up. Futures on the S&P 500 are also up +0.23% this morning.

Onto Brexit, and further optimism on the chances that the UK and the EU would agree a trade deal meant that sterling was among the strongest-performing G10 currency for the 3rd day running, as it climbed +0.36% against the dollar to a 2-year high of $1.35. Helping matters were remarks from European Commission President von der Leyen, who said that “I can tell you that there is a path to an agreement now. The path may be very narrow but it is there and it is therefore our responsibility to continue trying.” As a reminder, there are now just 2 weeks until the transition period ends, and any agreement would need to be ratified, so if there is any deal it’s going to have to be passed in astonishingly quick time. And though it’s been confirmed that the House of Commons will go into recess tomorrow, in reality it could be recalled in the event that a Brexit deal were reached.

Staying on the UK, one of the highlights today will be the Bank of England’s final monetary policy decision this year, which is coming out later today. It comes as data yesterday showed UK inflation fell back to just +0.3% in November (vs. +0.6% expected), and a reasonable way below the BoE’s 2% target. In their preview (link here), our UK economists write that their base case is for no chance in the BoE’s policy settings, but the focus will be on the pace of QE announced following the £150bn package they announced at their meeting last month.

On the coronavirus, today sees the FDA in the US meet to discuss an Emergency Use Authorization for the Moderna vaccine, which follows the approval of the Pfizer/BioNTech vaccine that has already started to be rolled out. In our monthly survey, vaccine concerns were among the largest worries next year (see link here ), and yesterday saw the first slight hiccup in the US as Pfizer announced that they would ship about 900,000 fewer doses next week than were shipped this week. Meanwhile, in a bid to build public confidence in the vaccine, the US VP Mike Pence will publicly receive the vaccine tomorrow while President-elect Joe Biden is expected to get vaccinated as soon as next week. Sticking with vaccines, the European Commission is planning to sign-off the Pfizer/ BioNtech vaccine on Monday should the vaccine receive the backing from a key drugs oversight committee on the same day (originally planned for December 29 but brought forward due to much criticism about falling behind the U.K. and the US.). This would enable shipping the first shots to vaccine centers as early as Wednesday.

In the meantime however, US Secretary of State Mike Pompeo went into quarantine yesterday after contact with someone who tested positive. This comes as California continues to see daily case counts break pandemic records (over 53,000 in the last 24 hours), even with the majority of the state currently under stay-at-home orders. In the UK, Prime Minister Johnson urged people to minimise the numbers they meet over the Christmas period, when the government are easing restrictions over a 5-day period. Spain granted regional administrations power to further restrict movement of their residents in order to limit the size of Christmas gatherings – no more than 10 people should gather and these should be limited to family members. Across the other side of world, the Tokyo Metropolitan Government raised its warning on the city’s medical system to “under strain,” the highest of four levels on rising number of hospitalised patients.

To the day ahead now, and the highlights will include the aforementioned Bank of England decision, as well as remarks from the ECB’s de Guindos and Schnabel. Data releases from the US include November’s housing starts, building permits, December’s Philadelphia Fed Business Outlook and Kansas City Fed manufacturing activity, along with the weekly initial jobless claims. Finally, the FDA will be meeting to discuss an Emergency Use Authorization for the Moderna vaccine.

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Key shipping company files Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocksUncategorized

Tight inventory and frustrated buyers challenge agents in Virginia

With inventory a little more than half of what it was pre-pandemic, agents are struggling to find homes for clients in Virginia.

Share this:

No matter where you are in the state, real estate agents in Virginia are facing low inventory conditions that are creating frustrating scenarios for their buyers.

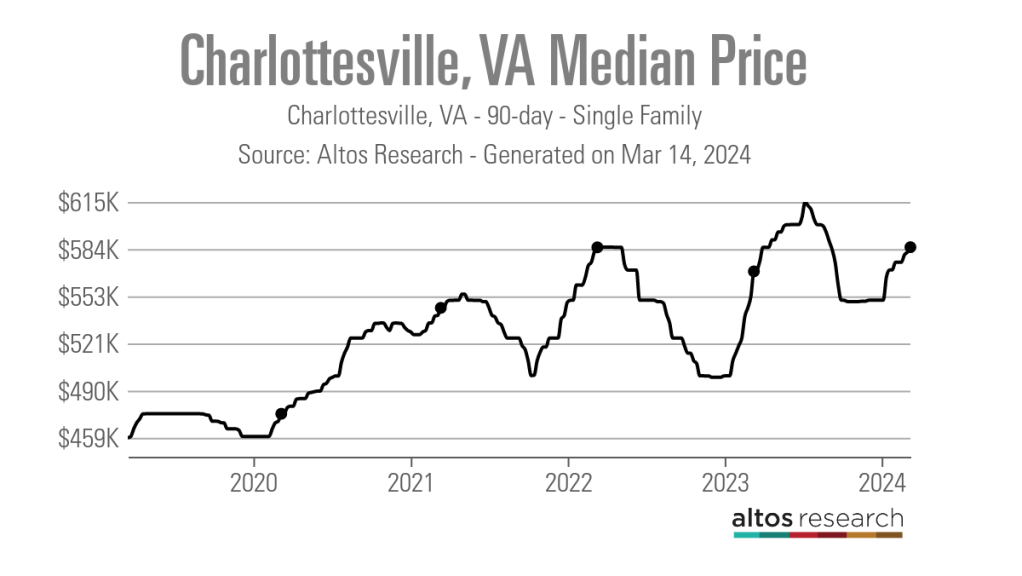

“I think people are getting used to the interest rates where they are now, but there is just a huge lack of inventory,” said Chelsea Newcomb, a RE/MAX Realty Specialists agent based in Charlottesville. “I have buyers that are looking, but to find a house that you love enough to pay a high price for — and to be at over a 6.5% interest rate — it’s just a little bit harder to find something.”

Newcomb said that interest rates and higher prices, which have risen by more than $100,000 since March 2020, according to data from Altos Research, have caused her clients to be pickier when selecting a home.

“When rates and prices were lower, people were more willing to compromise,” Newcomb said.

Out in Wise, Virginia, near the westernmost tip of the state, RE/MAX Cavaliers agent Brett Tiller and his clients are also struggling to find suitable properties.

“The thing that really stands out, especially compared to two years ago, is the lack of quality listings,” Tiller said. “The slightly more upscale single-family listings for move-up buyers with children looking for their forever home just aren’t coming on the market right now, and demand is still very high.”

Statewide, Virginia had a 90-day average of 8,068 active single-family listings as of March 8, 2024, down from 14,471 single-family listings in early March 2020 at the onset of the COVID-19 pandemic, according to Altos Research. That represents a decrease of 44%.

In Newcomb’s base metro area of Charlottesville, there were an average of only 277 active single-family listings during the same recent 90-day period, compared to 892 at the onset of the pandemic. In Wise County, there were only 56 listings.

Due to the demand from move-up buyers in Tiller’s area, the average days on market for homes with a median price of roughly $190,000 was just 17 days as of early March 2024.

“For the right home, which is rare to find right now, we are still seeing multiple offers,” Tiller said. “The demand is the same right now as it was during the heart of the pandemic.”

According to Tiller, the tight inventory has caused homebuyers to spend up to six months searching for their new property, roughly double the time it took prior to the pandemic.

For Matt Salway in the Virginia Beach metro area, the tight inventory conditions are creating a rather hot market.

“Depending on where you are in the area, your listing could have 15 offers in two days,” the agent for Iron Valley Real Estate Hampton Roads | Virginia Beach said. “It has been crazy competition for most of Virginia Beach, and Norfolk is pretty hot too, especially for anything under $400,000.”

According to Altos Research, the Virginia Beach-Norfolk-Newport News housing market had a seven-day average Market Action Index score of 52.44 as of March 14, making it the seventh hottest housing market in the country. Altos considers any Market Action Index score above 30 to be indicative of a seller’s market.

Further up the coastline on the vacation destination of Chincoteague Island, Long & Foster agent Meghan O. Clarkson is also seeing a decent amount of competition despite higher prices and interest rates.

“People are taking their time to actually come see things now instead of buying site unseen, and occasionally we see some seller concessions, but the traffic and the demand is still there; you might just work a little longer with people because we don’t have anything for sale,” Clarkson said.

“I’m busy and constantly have appointments, but the underlying frenzy from the height of the pandemic has gone away, but I think it is because we have just gotten used to it.”

While much of the demand that Clarkson’s market faces is for vacation homes and from retirees looking for a scenic spot to retire, a large portion of the demand in Salway’s market comes from military personnel and civilians working under government contracts.

“We have over a dozen military bases here, plus a bunch of shipyards, so the closer you get to all of those bases, the easier it is to sell a home and the faster the sale happens,” Salway said.

Due to this, Salway said that existing-home inventory typically does not come on the market unless an employment contract ends or the owner is reassigned to a different base, which is currently contributing to the tight inventory situation in his market.

Things are a bit different for Tiller and Newcomb, who are seeing a decent number of buyers from other, more expensive parts of the state.

“One of the crazy things about Louisa and Goochland, which are kind of like suburbs on the western side of Richmond, is that they are growing like crazy,” Newcomb said. “A lot of people are coming in from Northern Virginia because they can work remotely now.”

With a Market Action Index score of 50, it is easy to see why people are leaving the Washington-Arlington-Alexandria market for the Charlottesville market, which has an index score of 41.

In addition, the 90-day average median list price in Charlottesville is $585,000 compared to $729,900 in the D.C. area, which Newcomb said is also luring many Virginia homebuyers to move further south.

“They are very accustomed to higher prices, so they are super impressed with the prices we offer here in the central Virginia area,” Newcomb said.

For local buyers, Newcomb said this means they are frequently being outbid or outpriced.

“A couple who is local to the area and has been here their whole life, they are just now starting to get their mind wrapped around the fact that you can’t get a house for $200,000 anymore,” Newcomb said.

As the year heads closer to spring, triggering the start of the prime homebuying season, agents in Virginia feel optimistic about the market.

“We are seeing seasonal trends like we did up through 2019,” Clarkson said. “The market kind of soft launched around President’s Day and it is still building, but I expect it to pick right back up and be in full swing by Easter like it always used to.”

But while they are confident in demand, questions still remain about whether there will be enough inventory to support even more homebuyers entering the market.

“I have a lot of buyers starting to come off the sidelines, but in my office, I also have a lot of people who are going to list their house in the next two to three weeks now that the weather is starting to break,” Newcomb said. “I think we are going to have a good spring and summer.”

real estate housing market pandemic covid-19 interest rates

IFM’s Hat Trick and Reflections On Option-To-Buy M&A

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges