Eschler Recovery Fund 2020 Year End Commentary

Eschler Recovery Fund commentary for the year ended December 31, 2020. Q4 2020 hedge fund letters, conferences and more Dear Partners, Eschler Recovery Fund Performance In 2020 Eschler Recovery Fund rose over 50% on an asset-weighted basis, net of fees…

Share this:

Eschler Recovery Fund commentary for the year ended December 31, 2020.

Get The Full Series in PDF

Get the entire 10-part series on Charlie Munger in PDF. Save it to your desktop, read it on your tablet, or email to your colleagues.

Q4 2020 hedge fund letters, conferences and more

Dear Partners,

Eschler Recovery Fund Performance

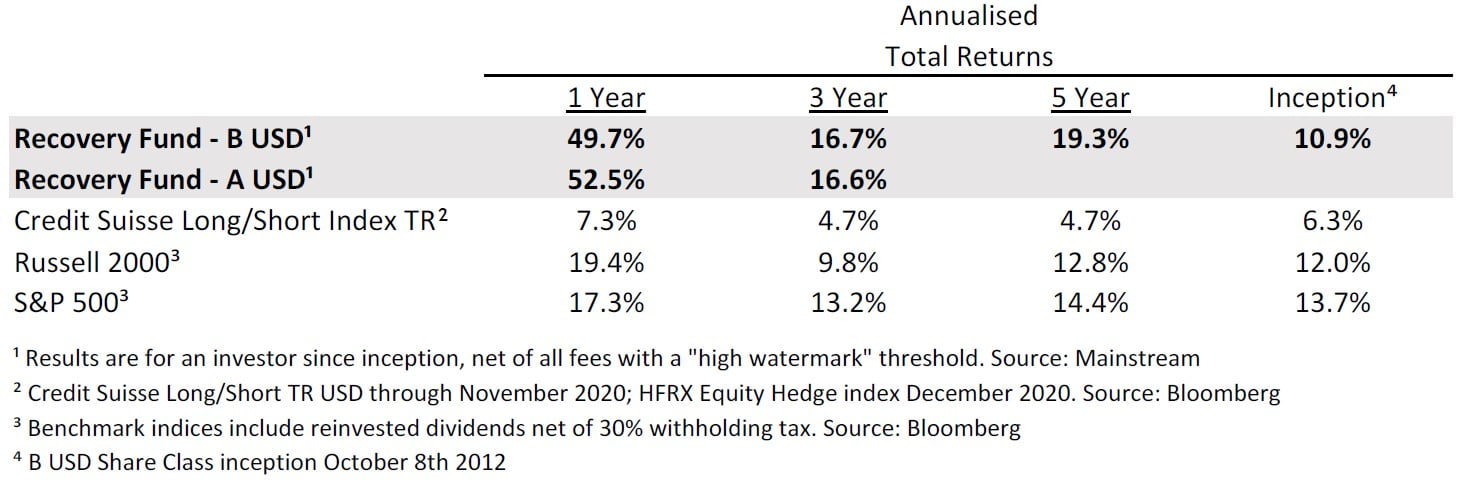

In 2020 Eschler Recovery Fund rose over 50% on an asset-weighted basis, net of fees and expenses. This was the best annual tally since inception. This strong result belies a sometimes uneven flight path over the past eight years (and I have the grey sideburns to prove it!). The 37 year-old who set up Eschler in 2010 may have had second thoughts had he enjoyed perfect foresight. Markets exist to destroy one’s ego and it didn’t take long for mine to be cut down to size. Before launching Recovery Fund I received valuable early experience running third-party capital for 18 months which helped to inform and hone my investing approach. Armed with these lessons learned, surely great things were in store? Not so fast. Despite the best laid plans, Recovery Fund was less than breakeven after three years! With no income from the business (Eschler’s day one investors paid no management fees) and a 6% compounding hurdle, quitting would have been easy. Instead, I left the warm bosom of employment and doubled down on Eschler. The past five years, most of it running the fund full-time, have now begun to justify this decision.

What is the moral of this expose? The challenge for stewards of perpetual endowments is to identify investment managers, with whom they can deploy capital over very long periods of time, thereby minimizing the risk of interrupted compounding and maximizing the benefits of longterm partnership. Such managers must necessarily be driven not solely by financial rewards but also by a genuine interest in the craft, learning from setbacks, building enterprise resilience and seeing a project through. To finish first, as they say, you must first finish. I am certainly humbled by the endurance of my investing partners who provided me with encouragement at the low points and truly embody partnership. They deserve much of any credit due for results to date. I would like nothing more than to manage this fund for decades. If collective decisions in the first eight years are anything to go by, we may have a shot at it.

............................................

If one needed any proof that the stock market is not the economy, 2020 provided it in spades. The source of this dichotomy, in my view, was pervasive government meddling in private enterprise. Blanket lockdowns brought exceedingly tough economic conditions on many citizens who could afford it least, while protecting the wealthy. Fiscal and monetary largesse was then indiscriminately showered on those who, in many instances, needed it least. These policies have accelerated inequality and spawned social unrest and a breakdown in trust. Is it any wonder that gold returned 25% last year? I have not been investing in precious metals in recent years out of some obsession with what is a tough business over a full cycle. Rather, I have invested out of necessity, believing the asset class to be a refuge from government policy gone mad. For better or worse, the investment case appears as strong as ever.

Review

The following elements combined to produce what was a standout year: A large cash position prior to the pandemic onset (peaking at ~33% in late January) allowed us to stay on the front foot through March and April and act on our conviction that the lows were in (see the Q1 2020 letter). Our core exposure to precious metals equities in the first half of the year provided more rapid momentum uplift off the lows than did exposure to many cyclical industries whose fundamentals stayed deeply impaired (see the Q2 2020 letter). An incremental shift toward more economically sensitive value stocks in the second half of the year (pre-U.S. election) paid off in November and December. Minimal short exposure throughout the year ensured the portfolio felt the full benefit of the recovery off the lows.

Last but not least, stock picking last year was extremely successful. For example, our largest royalty holding EMX Royalty rose 104%, over 3x the industry average. Our largest uranium holding Paladin Energy rose 152%, over twice the industry average. Our largest silver holding Fortuna Silver Mines rose 102%, over twice the industry average. Our largest energy holding Antero Resources rose 91% in a negative energy market. Our largest financial holding Affiliated Managers rose 20% against a negative sector return. Losing investments were modest in comparison. Tailored Brands, a formal wear retailer hurt by the pandemic, was our largest single stock detractor shaving 1.3% off the portfolio return. We also lost smaller amounts primarily in energy holdings. Shorts detracted 1.4%, with losses arising primarily from two holdings (Tesla and Plug Power) both of which we immediately stopped out of. The macro hedge, primarily long index puts and straddles, detracted 3% but helped us to stay invested during the initial recovery.

............................................

Parallels with '99-'00

2020 saw the return of the silly season in financial markets. Bubbly conditions in 2020 set records in IPOs, SPACs, high yield bond issuance, negative yielding sovereign debt, ETF flows, retail call buying, margin debt, short-squeezes and more. For those of us who had a front row seat during the internet bubble, drawing parallels with ‘99/’00 is tempting.

After raising $396 million from VCs, online grocery delivery business, Webvan, came public in November 1999 raising another $375 million. The shares doubled on the first day of trading. At its stabilised $5bn market cap the shares traded at 28x 2000 revenues. As we distributed these coveted IPO shares to lucky institutions on the US shares desk at Goldman Sachs, it was no secret that this deeply loss-making, unseasoned, capital intensive enterprise was destined to stumble. Shares fell 95% in 2000 and bankruptcy followed in March 2001. In my view, Webvan was one of the more egregious poster children for internet bubble excess.

Is the recent batch of freshly minted IPOs by new entrants in the same risk category? I would say no. They tend to be seasoned businesses with sales traction which are investing heavily to satisfy customer demand spawned by a genuine value proposition. For example, Airbnb is one of the most disruptive businesses ever in my view, with tremendous long-term opportunities to grow. Where the internet bubble framework does provide a roadmap, though, is in the price investors are paying for future growth and the shameless analyst cheerleading. At a $45bn market cap, investors in loss-making Doordash are paying 53x 2026 estimated earnings per share. Leave aside the improbable growth in earnings that multiple implies. Even if the company is successful, ultimately meets this earnings target and trades at 50x earnings in five years, investors will lose money paying today’s price. This encapsulates the risk in today’s growth investing market. I’m keen to observe how it all plays out—from the sidelines.

Risk Management

Commodity cyclicals, a segment of the market in which we have been active, also showed some signs of life last year, though the complex lagged in aggregate. But I am under no illusion that a pervasive speculative impulse contributed mightily to the Fund’s 60% gross return last year (despite cash holdings averaging 14% of fund equity). It is foolish to believe that telltale signs of excess will not have predictably bad consequences for the entire market at some point and our holdings would not be immune. Hence I have been focused on maintaining a small balance sheet (holding more cash), greater position liquidity (generally >$1m daily trading volume for each of our top 10 holdings) and greater than normal position diversification (4-6% position sizing for our top 10 holdings). The short book has been mostly dormant for the past couple years but the ability to activate it at any time is a big advantage in today’s environment. I foresee once again deploying a small short book while adhering (ruthlessly!) to a hard stop-loss rule which has served me very well recently.

Outlook

I continue to believe the Fund’s precious metals holdings offer excellent risk-reward. The whole sector is in rude health while capital spending and M&A remain restrained. Yet the gold stock indices barely matched gold’s return last year despite rapid fundamental improvement. Forward growth rates in earnings are the best in the stock market while forward P/E ratios are amongst the lowest. Normally, low P/E ratios in a cyclical industry would have me concerned. For now, though, I await further enthusiasm from mainstream investors leading to a robust investment and M&A cycle and a revaluation of the smaller businesses we tend to own.

My best guess is that the performance of the gold mining industry in the past couple years is a leading indicator for the broader commodities complex. This would be consistent with steep global GDP recovery and a wave of fiscal spending coming up against supply constraints across most natural resource subsectors. If this hypothesis is correct, energy, uranium and base metal prices should see upward pressure soon and the fund has geared exposure to this via common stock investments.

Business Update

I’m pleased to say Eschler is now a full-scope AIFM and has submitted an application to register with the SEC. We have also on-boarded an experienced investment advisor with a wellestablished fund onto our platform. These initiatives will facilitate both internal growth and growth of our investment advisors, as well as provide financial and operational ballast. In November, we also hosted our inaugural Emerging Manager Symposium. Lastly, I’m excited to announce that we will be launching Eschler Partnership SP on April 1st 2021, a feeder fund counterpart to Recovery Fund for US taxable investors.

Against an unpredictable backdrop, a lot of good things happened at Eschler last year, only made possible by the support of our clients, service providers and friends. Heartfelt thanks to all of you for your enduring support.

Theron de Ris

Portfolio Manager

The post Eschler Recovery Fund 2020 Year End Commentary appeared first on ValueWalk.

bankruptcy pandemic equities stocks etf gdp recovery commodities goldSpread & Containment

Separating Information From Disinformation: Threats From The AI Revolution

Separating Information From Disinformation: Threats From The AI Revolution

Authored by Per Bylund via The Mises Institute,

Artificial intelligence…

Share this:

Authored by Per Bylund via The Mises Institute,

Artificial intelligence (AI) cannot distinguish fact from fiction. It also isn’t creative or can create novel content but repeats, repackages, and reformulates what has already been said (but perhaps in new ways).

I am sure someone will disagree with the latter, perhaps pointing to the fact that AI can clearly generate, for example, new songs and lyrics. I agree with this, but it misses the point. AI produces a “new” song lyric only by drawing from the data of previous song lyrics and then uses that information (the inductively uncovered patterns in it) to generate what to us appears to be a new song (and may very well be one). However, there is no artistry in it, no creativity. It’s only a structural rehashing of what exists.

Of course, we can debate to what extent humans can think truly novel thoughts and whether human learning may be based solely or primarily on mimicry. However, even if we would—for the sake of argument—agree that all we know and do is mere reproduction, humans have limited capacity to remember exactly and will make errors. We also fill in gaps with what subjectively (not objectively) makes sense to us (Rorschach test, anyone?). Even in this very limited scenario, which I disagree with, humans generate novelty beyond what AI is able to do.

Both the inability to distinguish fact from fiction and the inductive tether to existent data patterns are problems that can be alleviated programmatically—but are open for manipulation.

Manipulation and Propaganda

When Google launched its Gemini AI in February, it immediately became clear that the AI had a woke agenda. Among other things, the AI pushed woke diversity ideals into every conceivable response and, among other things, refused to show images of white people (including when asked to produce images of the Founding Fathers).

Tech guru and Silicon Valley investor Marc Andreessen summarized it on X (formerly Twitter): “I know it’s hard to believe, but Big Tech AI generates the output it does because it is precisely executing the specific ideological, radical, biased agenda of its creators. The apparently bizarre output is 100% intended. It is working as designed.”

There is indeed a design to these AIs beyond the basic categorization and generation engines. The responses are not perfectly inductive or generative. In part, this is necessary in order to make the AI useful: filters and rules are applied to make sure that the responses that the AI generates are appropriate, fit with user expectations, and are accurate and respectful. Given the legal situation, creators of AI must also make sure that the AI does not, for example, violate intellectual property laws or engage in hate speech. AI is also designed (directed) so that it does not go haywire or offend its users (remember Tay?).

However, because such filters are applied and the “behavior” of the AI is already directed, it is easy to take it a little further. After all, when is a response too offensive versus offensive but within the limits of allowable discourse? It is a fine and difficult line that must be specified programmatically.

It also opens the possibility for steering the generated responses beyond mere quality assurance. With filters already in place, it is easy to make the AI make statements of a specific type or that nudges the user in a certain direction (in terms of selected facts, interpretations, and worldviews). It can also be used to give the AI an agenda, as Andreessen suggests, such as making it relentlessly woke.

Thus, AI can be used as an effective propaganda tool, which both the corporations creating them and the governments and agencies regulating them have recognized.

Misinformation and Error

States have long refused to admit that they benefit from and use propaganda to steer and control their subjects. This is in part because they want to maintain a veneer of legitimacy as democratic governments that govern based on (rather than shape) people’s opinions. Propaganda has a bad ring to it; it’s a means of control.

However, the state’s enemies—both domestic and foreign—are said to understand the power of propaganda and do not hesitate to use it to cause chaos in our otherwise untainted democratic society. The government must save us from such manipulation, they claim. Of course, rarely does it stop at mere defense. We saw this clearly during the covid pandemic, in which the government together with social media companies in effect outlawed expressing opinions that were not the official line (see Murthy v. Missouri).

AI is just as easy to manipulate for propaganda purposes as social media algorithms but with the added bonus that it isn’t only people’s opinions and that users tend to trust that what the AI reports is true. As we saw in the previous article on the AI revolution, this is not a valid assumption, but it is nevertheless a widely held view.

If the AI then can be instructed to not comment on certain things that the creators (or regulators) do not want people to see or learn, then it is effectively “memory holed.” This type of “unwanted” information will not spread as people will not be exposed to it—such as showing only diverse representations of the Founding Fathers (as Google’s Gemini) or presenting, for example, only Keynesian macroeconomic truths to make it appear like there is no other perspective. People don’t know what they don’t know.

Of course, nothing is to say that what is presented to the user is true. In fact, the AI itself cannot distinguish fact from truth but only generates responses according to direction and only based on whatever the AI has been fed. This leaves plenty of scope for the misrepresentation of the truth and can make the world believe outright lies. AI, therefore, can easily be used to impose control, whether it is upon a state, the subjects under its rule, or even a foreign power.

The Real Threat of AI

What, then, is the real threat of AI? As we saw in the first article, large language models will not (cannot) evolve into artificial general intelligence as there is nothing about inductive sifting through large troves of (humanly) created information that will give rise to consciousness. To be frank, we haven’t even figured out what consciousness is, so to think that we will create it (or that it will somehow emerge from algorithms discovering statistical language correlations in existing texts) is quite hyperbolic. Artificial general intelligence is still hypothetical.

As we saw in the second article, there is also no economic threat from AI. It will not make humans economically superfluous and cause mass unemployment. AI is productive capital, which therefore has value to the extent that it serves consumers by contributing to the satisfaction of their wants. Misused AI is as valuable as a misused factory—it will tend to its scrap value. However, this doesn’t mean that AI will have no impact on the economy. It will, and already has, but it is not as big in the short-term as some fear, and it is likely bigger in the long-term than we expect.

No, the real threat is AI’s impact on information. This is in part because induction is an inappropriate source of knowledge—truth and fact are not a matter of frequency or statistical probabilities. The evidence and theories of Nicolaus Copernicus and Galileo Galilei would get weeded out as improbable (false) by an AI trained on all the (best and brightest) writings on geocentrism at the time. There is no progress and no learning of new truths if we trust only historical theories and presentations of fact.

However, this problem can probably be overcome by clever programming (meaning implementing rules—and fact-based limitations—to the induction problem), at least to some extent. The greater problem is the corruption of what AI presents: the misinformation, disinformation, and malinformation that its creators and administrators, as well as governments and pressure groups, direct it to create as a means of controlling or steering public opinion or knowledge.

This is the real danger that the now-famous open letter, signed by Elon Musk, Steve Wozniak, and others, pointed to:

“Should we let machines flood our information channels with propaganda and untruth? Should we automate away all the jobs, including the fulfilling ones? Should we develop nonhuman minds that might eventually outnumber, outsmart, obsolete and replace us? Should we risk loss of control of our civilization?”

Other than the economically illiterate reference to “automat[ing] away all the jobs,” the warning is well-taken. AI will not Terminator-like start to hate us and attempt to exterminate mankind. It will not make us all into biological batteries, as in The Matrix. However, it will—especially when corrupted—misinform and mislead us, create chaos, and potentially make our lives “solitary, poor, nasty, brutish and short.”

Government

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Authored by Zachary Stieber via The Epoch Times (emphasis…

Share this:

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

People who recovered from COVID-19 and received a COVID-19 shot were more likely to suffer adverse reactions, researchers in Europe are reporting.

Participants in the study were more likely to experience an adverse reaction after vaccination regardless of the type of shot, with one exception, the researchers found.

Across all vaccine brands, people with prior COVID-19 were 2.6 times as likely after dose one to suffer an adverse reaction, according to the new study. Such people are commonly known as having a type of protection known as natural immunity after recovery.

People with previous COVID-19 were also 1.25 times as likely after dose 2 to experience an adverse reaction.

The findings held true across all vaccine types following dose one.

Of the female participants who received the Pfizer-BioNTech vaccine, for instance, 82 percent who had COVID-19 previously experienced an adverse reaction after their first dose, compared to 59 percent of females who did not have prior COVID-19.

The only exception to the trend was among males who received a second AstraZeneca dose. The percentage of males who suffered an adverse reaction was higher, 33 percent to 24 percent, among those without a COVID-19 history.

“Participants who had a prior SARS-CoV-2 infection (confirmed with a positive test) experienced at least one adverse reaction more often after the 1st dose compared to participants who did not have prior COVID-19. This pattern was observed in both men and women and across vaccine brands,” Florence van Hunsel, an epidemiologist with the Netherlands Pharmacovigilance Centre Lareb, and her co-authors wrote.

There were only slightly higher odds of the naturally immune suffering an adverse reaction following receipt of a Pfizer or Moderna booster, the researchers also found.

The researchers performed what’s known as a cohort event monitoring study, following 29,387 participants as they received at least one dose of a COVID-19 vaccine. The participants live in a European country such as Belgium, France, or Slovakia.

Overall, three-quarters of the participants reported at least one adverse reaction, although some were minor such as injection site pain.

Adverse reactions described as serious were reported by 0.24 percent of people who received a first or second dose and 0.26 percent for people who received a booster. Different examples of serious reactions were not listed in the study.

Participants were only specifically asked to record a range of minor adverse reactions (ADRs). They could provide details of other reactions in free text form.

“The unsolicited events were manually assessed and coded, and the seriousness was classified based on international criteria,” researchers said.

The free text answers were not provided by researchers in the paper.

“The authors note, ‘In this manuscript, the focus was not on serious ADRs and adverse events of special interest.’” Yet, in their highlights section they state, “The percentage of serious ADRs in the study is low for 1st and 2nd vaccination and booster.”

Dr. Joel Wallskog, co-chair of the group React19, which advocates for people who were injured by vaccines, told The Epoch Times: “It is intellectually dishonest to set out to study minor adverse events after COVID-19 vaccination then make conclusions about the frequency of serious adverse events. They also fail to provide the free text data.” He added that the paper showed “yet another study that is in my opinion, deficient by design.”

Ms. Hunsel did not respond to a request for comment.

She and other researchers listed limitations in the paper, including how they did not provide data broken down by country.

The paper was published by the journal Vaccine on March 6.

The study was funded by the European Medicines Agency and the Dutch government.

No authors declared conflicts of interest.

Some previous papers have also found that people with prior COVID-19 infection had more adverse events following COVID-19 vaccination, including a 2021 paper from French researchers. A U.S. study identified prior COVID-19 as a predictor of the severity of side effects.

Some other studies have determined COVID-19 vaccines confer little or no benefit to people with a history of infection, including those who had received a primary series.

The U.S. Centers for Disease Control and Prevention still recommends people who recovered from COVID-19 receive a COVID-19 vaccine, although a number of other health authorities have stopped recommending the shot for people who have prior COVID-19.

Another New Study

In another new paper, South Korean researchers outlined how they found people were more likely to report certain adverse reactions after COVID-19 vaccination than after receipt of another vaccine.

The reporting of myocarditis, a form of heart inflammation, or pericarditis, a related condition, was nearly 20 times as high among children as the reporting odds following receipt of all other vaccines, the researchers found.

The reporting odds were also much higher for multisystem inflammatory syndrome or Kawasaki disease among adolescent COVID-19 recipients.

Researchers analyzed reports made to VigiBase, which is run by the World Health Organization.

“Based on our results, close monitoring for these rare but serious inflammatory reactions after COVID-19 vaccination among adolescents until definitive causal relationship can be established,” the researchers wrote.

The study was published by the Journal of Korean Medical Science in its March edition.

Limitations include VigiBase receiving reports of problems, with some reports going unconfirmed.

Funding came from the South Korean government. One author reported receiving grants from pharmaceutical companies, including Pfizer.

Uncategorized

Key shipping company files for Chapter 11 bankruptcy

The Illinois-based general freight trucking company filed for Chapter 11 bankruptcy to reorganize.

Share this:

{kind=link}

{kind=link}

{kind=link}

The U.S. trucking industry has had a difficult beginning of the year for 2024 with several logistics companies filing for bankruptcy to seek either a Chapter 7 liquidation or Chapter 11 reorganization.

The Covid-19 pandemic caused a lot of supply chain issues for logistics companies and also created a shortage of truck drivers as many left the business for other occupations. Shipping companies, in the meantime, have had extreme difficulty recruiting new drivers for thousands of unfilled jobs.

Related: Tesla rival’s filing reveals Chapter 11 bankruptcy is possible

Freight forwarder company Boateng Logistics joined a growing list of shipping companies that permanently shuttered their businesses as the firm on Feb. 22 filed for Chapter 7 bankruptcy with plans to liquidate.

The Carlsbad, Calif., logistics company filed its petition in the U.S. Bankruptcy Court for the Southern District of California listing assets up to $50,000 and and $1 million to $10 million in liabilities. Court papers said it owed millions of dollars in liabilities to trucking, logistics and factoring companies. The company filed bankruptcy before any creditors could take legal action.

Lawsuits force companies to liquidate in bankruptcy

Lawsuits, however, can force companies to file bankruptcy, which was the case for J.J. & Sons Logistics of Clint, Texas, which on Jan. 22 filed for Chapter 7 liquidation in the U.S. Bankruptcy Court for the Western District of Texas. The company filed bankruptcy four days before the scheduled start of a trial for a wrongful death lawsuit filed by the family of a former company truck driver who had died from drowning in 2016.

California-based logistics company Wise Choice Trans Corp. shut down operations and filed for Chapter 7 liquidation on Jan. 4 in the U.S. Bankruptcy Court for the Northern District of California, listing $1 million to $10 million in assets and liabilities.

The Hayward, Calif., third-party logistics company, founded in 2009, provided final mile, less-than-truckload and full truckload services, as well as warehouse and fulfillment services in the San Francisco Bay Area.

The Chapter 7 filing also implemented an automatic stay against all legal proceedings, as the company listed its involvement in four legal actions that were ongoing or concluded. Court papers reportedly did not list amounts for damages.

In some cases, debtors don't have to take a drastic action, such as a liquidation, and can instead file a Chapter 11 reorganization.

Shutterstock

Nationwide Cargo seeks to reorganize its business

Nationwide Cargo Inc., a general freight trucking company that also hauls fresh produce and meat, filed for Chapter 11 bankruptcy protection in the U.S. Bankruptcy Court for the Northern District of Illinois with plans to reorganize its business.

The East Dundee, Ill., shipping company listed $1 million to $10 million in assets and $10 million to $50 million in liabilities in its petition and said funds will not be available to pay unsecured creditors. The company operates with 183 trucks and 171 drivers, FreightWaves reported.

Nationwide Cargo's three largest secured creditors in the petition were Equify Financial LLC (owed about $3.5 million,) Commercial Credit Group (owed about $1.8 million) and Continental Bank NA (owed about $676,000.)

The shipping company reported gross revenue of about $34 million in 2022 and about $40 million in 2023. From Jan. 1 until its petition date, the company generated $9.3 million in gross revenue.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic covid-19 stocks

Key shipping company files for Chapter 11 bankruptcy

Q4 Update: Delinquencies, Foreclosures and REO

Net Zero, The Digital Panopticon, & The Future Of Food

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International7 days ago

International7 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A