International

Emerging Market Vulnerability Heatmap: Are EMs Threatened By Increasing Inflation Expectations

Emerging Market Vulnerability Heatmap: Are EMs Threatened By Increasing Inflation Expectations

By Wouter van Eijkelenburg, economist at Rabobank

Emerging Market Vulnerability Heatmap

Summary

There are divergent paths to economic recovery..

Share this:

By Wouter van Eijkelenburg, economist at Rabobank

Emerging Market Vulnerability Heatmap

Summary

- There are divergent paths to economic recovery in advanced economies and emerging markets, due in part to differences in Covid-19 infections and vaccination rates

- Inflation expectations are increasing in advanced economies, raising questions on central bank policies going forward

- Tapering of QE or even policy interest rates hikes by central banks in advanced economies, particularly by the Fed, pose downside risks to the economies of emerging markets

- Our vulnerability Heatmap provides an overview of economic indicators that signal potential vulnerabilities for certain emerging markets

- Factors like a country’s (foreign currency denominated) debt, international trade position and interest rate risks are important determinants for EM vulnerability

- We examine these factors in detail for certain emerging markets by diving into debt metrics, current accounts and interest rates

Back to business?

In 2020, the Covid-19 pandemic triggered the largest crisis since WW2. Across the world countries went into lockdown to mitigate the spread of the corona virus. While they succeeded in containing the virus, the lockdowns had severe economic implications. Governments and central banks have stepped in by providing enormous amounts of fiscal and monetary stimulus in order to counter the negative economic consequences of the imposed lockdowns. A recent publication showed that economic contractions could have been much worse if there had been no additional fiscal stimulus by governments.

Halfway through 2021, we are seeing restrictions being loosened in many parts of the world due to increased vaccination rates. Although the virus is far from beaten, as new variants continue to emerge, economies are opening up globally and the economic outlook for most, if not all, countries is improving. A better economic outlook might require other policies by central banks and governments as inflationary pressure intensifies. However, economies are not all recovering at the same pace, and every economy has its own individual characteristics and autonomous regime. In this publication we will explore some of the implications of divergent economic growth paths between advanced economies (AEs) and emerging markets (EMs) with a special focus on the vulnerability of emerging markets to potential tighter monetary policy by AEs.

Different speeds of recovery

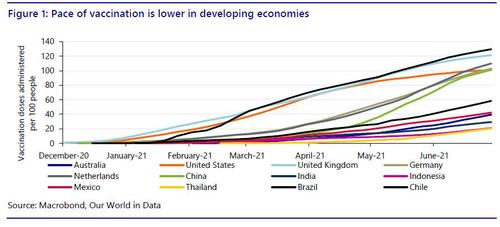

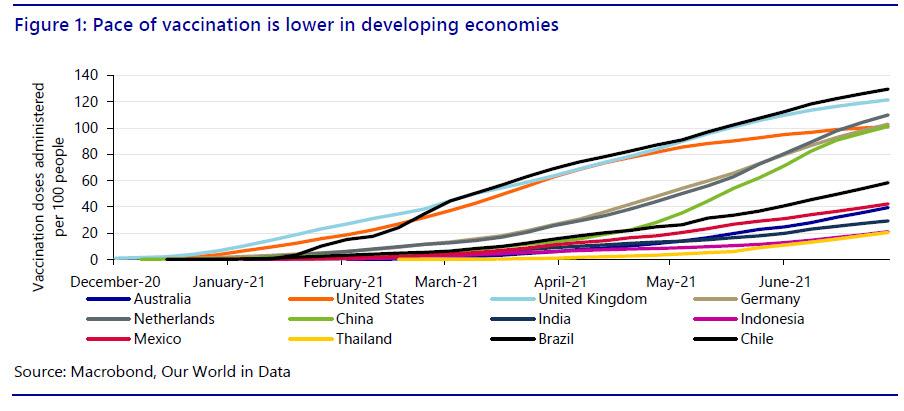

Globally, all of us have felt the impacts of the pandemic. But the intensity, limitations and consequences vary per country and probably even per person. Diverse policy actions have led to differences between countries in terms of virus penetration, containment success and economic consequences. Furthermore, we have seen that AEs have a greater vaccine availability and better logistical networks to start vaccinating quickly and effectively while most EMs are lagging behind. Figure 1 shows the varied pace of vaccination rates, which tends to be lower for most EMs (notwithstanding some exceptions, like Chile). It’s generally thought that higher vaccination rates allow economies to open up with a reduced risk of infections rising and therefore a lower risk of new waves of the virus hitting the country and economy.

While many Europeans are planning or enjoying summer holidays at home abroad, countries like Indonesia, Thailand and Vietnam are close to or at the highest number of infections since the start of the pandemic. At the same time, India is still licking its wounds after a devastating 2nd wave, while other countries like Brazil, Argentina, and Colombia still need to up their games and improve their current pace of vaccination. These differences translate into the path to economic recovery and the economic outlook going forward. Figure 2 shows GDP growth per country compared to what it would have been in the absence of the Covid-19 pandemic based on average GDP growth in the period 2011-2019. Figure 2 illustrates that not only did AEs (solid lines) generally suffer less than EMs (dashed lines) in terms of “lost” growth in 2020, they are also better able to regain lost ground in 2021 through to 2022. The US is expected to have regained almost all lost ground by the end of 2022. In contrast by the end of 2022 especially Asian EMs like Thailand, India and Indonesia will still face a loss of almost 10% in economic output due to the crisis.

Structural impact on the economy

Manufacturing in general bounced back relatively quickly in 2021 (especially compared to the aftermath of the Global Financial Crisis), due to pent-up demand, government support to households in advanced countries and more spending in durables instead of services. The car industry has been the largest driver of the manufacturing recovery, accounting for about 35 percent of the global rebound in the second half of 2020, while electrical equipment accounted for almost 5 percent of the rebound.

However, the economic recovery is mainly driven by large, while small and medium-sized enterprises (SMEs) were hit very hard by the pandemic, due to lower capital levels, lower capacity to adjust to remote working, and lower access to government funds. Moreover, the penetration of online retailers increased substantially during the lockdowns, which reduced the market share of traditional SMEs. In most emerging markets, the line between the SMEs and the informal sector is quite blurred, making it particularly difficult for these companies to receive government support. Support for SMEs was an important part of government packages in many countries: the Brazilian government dedicated 58.0% of their BRL1.27trn package to support workers and firms, the Indian government extended guarantees for SME loans, created a fund for equity infusion and loosened the regulations; Turkey offered an extended lending scheme for SMEs ; Thailand approved close to USD 20bn in soft loans to SMEs (both through private banks and directly from the government), to name but a few. It is likely that in the coming years non-payment of these loans or guarantees might materialize as liabilities for the sovereigns states.

Rising inflation (expectations)

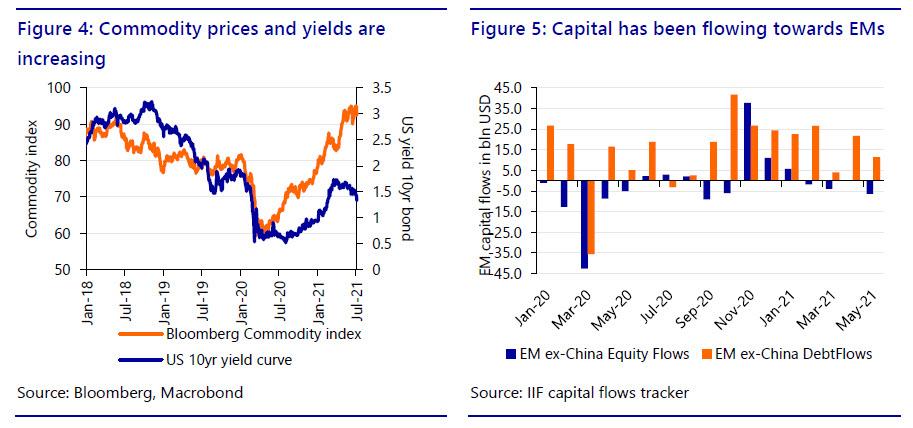

The recovering economic growth and optimistic growth outlook in AEs increase pressure on prices in a number of ways, potentially leading to higher inflation. This extensive report dives deeper into drivers for inflation and potential scenarios. Here we give only a brief description of some main drivers of current inflation expectations: Firstly, the restrictions of the pandemic are fading, leading to higher private consumption and consumer confidence which increases demand and puts pressure on prices. Secondly, global commodities prices are surging (Figure 4) which increases input costs for manufacturers and potentially pushes costs down the supply chain, leading to higher prices. Thirdly, most central banks have an ultra-accommodative stance: this means low interest rates and low borrowing costs, leading to increased investments and potentially an increase in prices (for example, housing prices). Finally, fiscal stimulus by governments is very large (as explained in this publication), which also has the potential to increase inflation.

Reaction of central banks

All of these factors push up inflation expectations. Recently, we have already seen the first examples in the US and UK, where inflation figures were higher than expected. Many central banks explain the rise in inflation as “transitory”, but the voices questioning the length of the period of higher inflation are getting louder. These developments cause us to wonder: what are central banks going to do? The question is particularly relevant for the Fed, as any material policy decisions related to inflation, which accelerated again in June, and a more hawkish stance by the Fed will potentially have direct consequences for the financial stability of EMs.

The last time the Fed started tapering had dramatic consequences for many EMs, known as the “taper tantrum” back in 2013. One of the main reasons for the sudden collapse of EM currencies was that the tapering came somewhat unexpectedly. Therefore the Fed tries to be as predictable as possible in order to prevent such shocks going forward. For this reason, Fed chair Powell speaks about an advanced notice, which will signal any changes in policy before announcing a decision on a change in asset purchases. So how far away are we from an advanced notice?

As we explain in our comments on the FOMC, the minutes from June highlight that the rise in inflation was higher than anticipated and a substantial majority of the participants think inflation risk is towards the upside. Furthermore, various participants expect the conditions to start reducing the pace of asset purchases (tapering) somewhat earlier than they expected previously. The median FOMC participant now expects two rate hikes of 25bps in 2023 instead of zero last March. Meanwhile, the discussion on tapering has started and Powell’s advance notice could come as soon as the Jackson Hole symposium in late August or the FOMC meeting in September.

How vulnerable are EMs to any tightening of monetary policy at this time? Especially taking into account the asymmetry in the pandemic and divergence in economic recovery as described above.

Risks for emerging markets

Explosive cocktail in the making

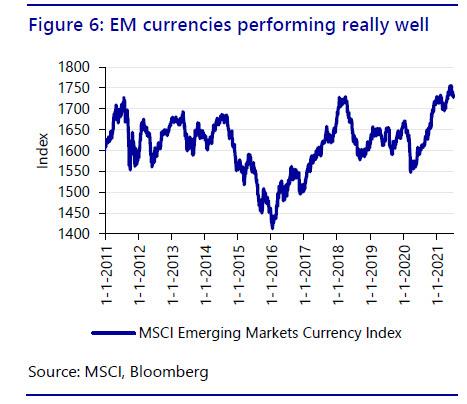

Tightening monetary policy in the US generally pushes up US yields and may also strengthen the USD verses EM currencies. This can potentially reverse some of the international capital flows which have been flowing towards EMs in the past year as a spill-over effect of the ultra-loose fiscal and monetary policy by advanced economies (Figure 5). These spill-over effects strengthened emerging market currencies over the last year, pushing them close to the highest level in a decade (Figure 6). The strength of the EM currencies, as a result of the capital inflows, helped EM governments in providing affordable financing to battle the consequences of the pandemic. However, there may be an explosive cocktail in store for vulnerable EMs due to the combination of weakening of domestic currencies vs. USD as a result of FED policy action, increased foreign currency debt levels as a result of Covid-19, high commodity prices (including oil), and faltering domestic recovery as a result of new waves of Covid-19.

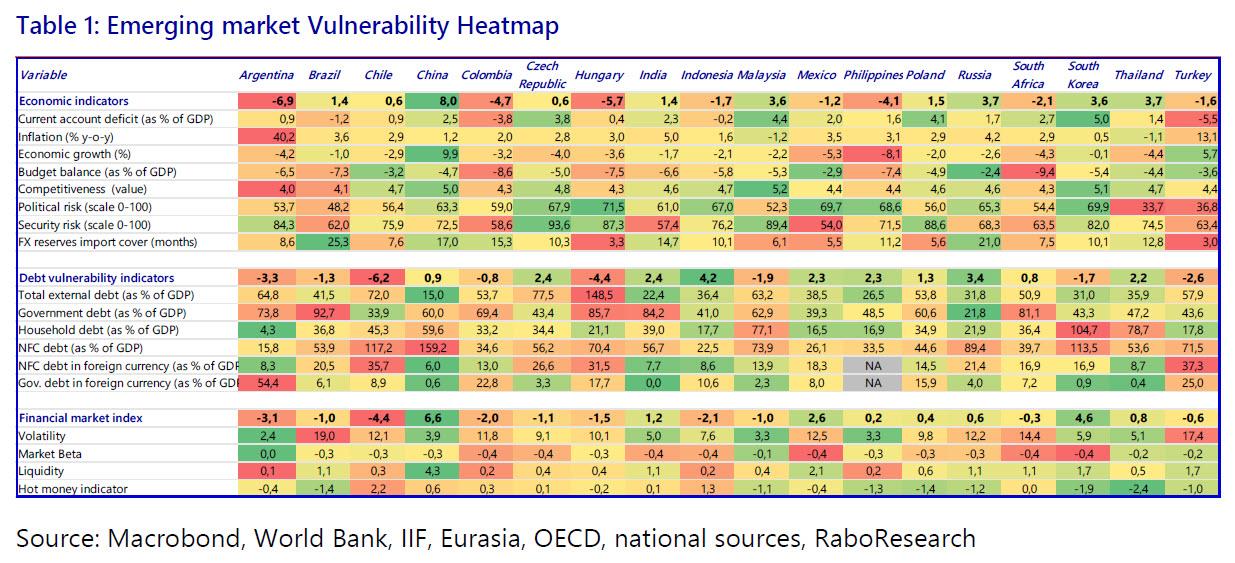

The ‘EM Vulnerability Heatmap’ as presented in Table 1 provides an overview of many economic indicators which allow us to asses and compare the relative vulnerability of EMs. In the next section we dive deeper into five indicators that could be valuable in order to assess a country’s vulnerability.

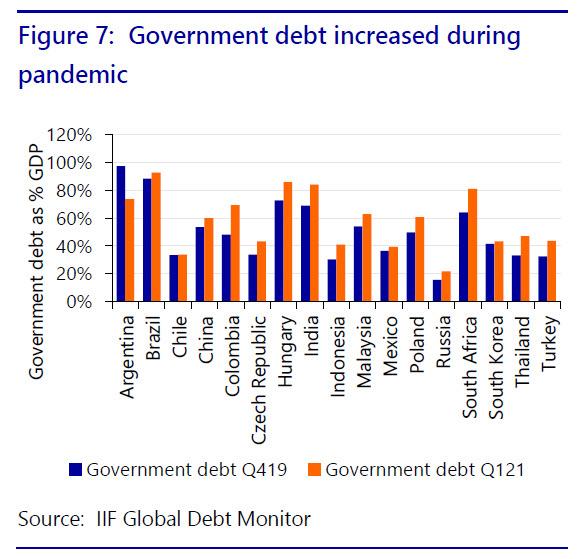

Public debt levels have increased across the board

Governments have increased expenditures as a reaction to the negative economic consequences of the pandemic, resulting in higher debt levels (as a % of GDP) in many countries (Figure 7). Especially Colombia, India and South Africa show large increases in public debt over the past year.

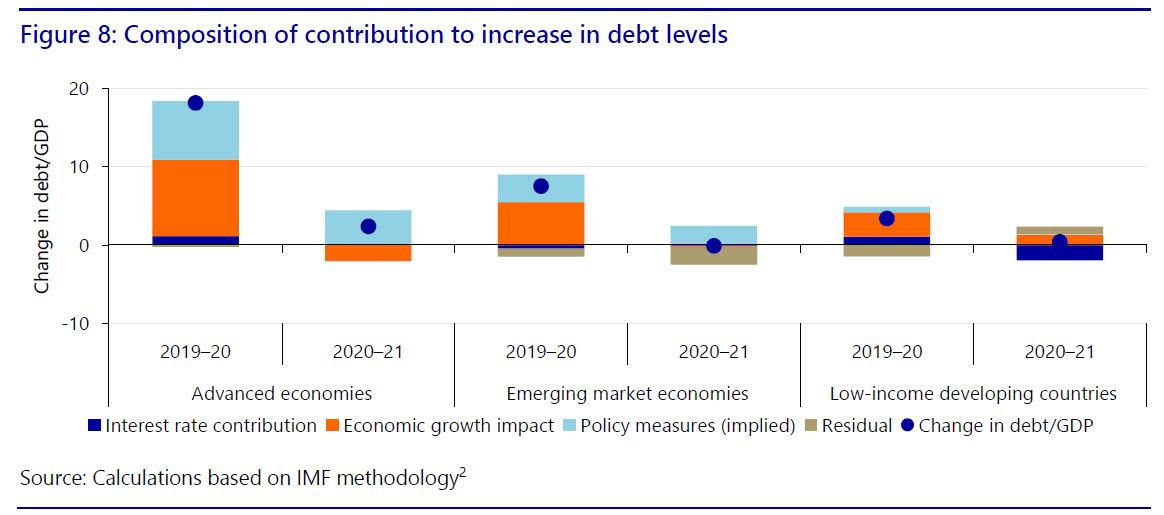

However, by using a methodology developed by Mauro and Zilinsky (Figure 8) we are able to nuance the growth in public debt to GDP ratio. Interestingly, despite falling interest rates, the interest expenses of advanced economies have slightly increased due to massive increases in the gross debt level. Simultaneously, we observe that the interest expense in emerging economies is only a marginal effect of the increase in public debt, while the loss in economic growth accounts for a much more significant part of the increase in public debt to GDP ratio. What is even more striking is that economic growth had a greater impact on the increase in debt to GDP ratio than fiscal policy measures in EMs. Figure 8 demonstrates that economic growth plays a much bigger role in emerging markets and low-income developing economies. In other words, economic growth rates are very important with regard to managing sustainable public debt levels. As already mentioned above, this is precisely what might work against EMs in 2021 as long as vaccination programs are slow to develop and the spread of the virus continues to drag on the economy.

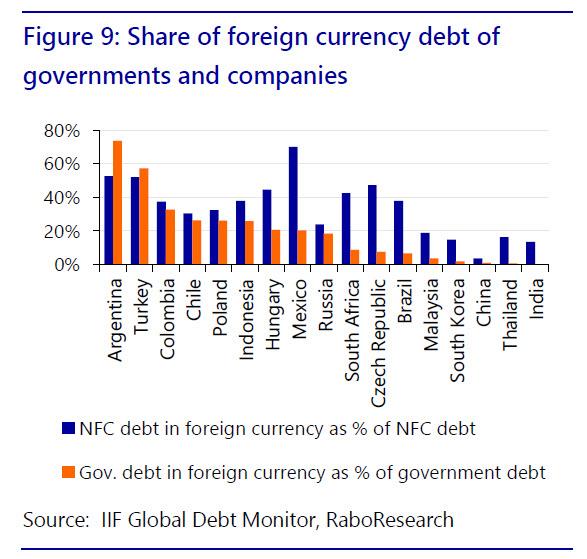

Nonetheless, while total public debt levels provide valuable information on the fiscal state of a country, there are other metrics which are well suited to explain EMs’ vulnerability. Debt levels are not always directly affected by any of the exogenous factors we discussed above (like increasing US interest rates). Therefore, a better indicator to gauge vulnerability would be the part of the total debt which is denominated in a foreign currency. : If the USD (or other foreign currency) were to strengthen versus the domestic currency this could have severe implications for the sustainability of EM debt levels Why? As the domestic currency depreciates this essentially increases the debt level in domestic currency. This implies that the higher your foreign currency denominated debt level is, the more vulnerable your fiscal position with regard to a depreciating currency.

Moreover, a country can only service its foreign currency debt by reducing its currency reserves and/or earning enough currency in foreign trade. So apart from holding external FX reserves and international assets, a positive current account balance is crucial for these countries. On the other hand, a deficit here increases their financial troubles. We will look at the current account in more detail in the next section. Figure 9 shows that the governments of countries on the left-hand side like Argentina, Turkey and Colombia are relatively vulnerable in terms of foreign currency debt. China, Thailand and India have less foreign currency debt , making them less vulnerable to exogenous shocks that affect the price of the domestic currency.

Trade positions have shifted due to the pandemic

The pandemic hit countries in an asymmetric fashion as a result of diverse characteristics of domestic economies. This has also undoubtedly been the case with regard to trade. There have been swings in the current account of many emerging countries, in a positive sense for some and negative for others. A few developments that were aa direct consequence of the pandemic impacted the current account over the course of last year. Firstly, increased demand for medical goods meant that exporters of health-related products or inputs saw a dramatic rise in demand for their products. Secondly, at the same time, due to lockdowns in advanced economies people were unable to spend their money on services and therefore private expenditures shifted partly towards purchasing goods. This higher demand for goods from AE’s increased exports of products for emerging markets that produce these goods. Thirdly, over the course of the year commodity prices started to increase (Figure 4): this was due to a more positive economic growth outlook that increased demand and benefitted commodity exporters but negatively impacted commodity importers. Finally, domestic import of products and services collapsed in many EMs as a result of lower domestic consumption during the crisis, thereby increasing the current account. Figure 10 illustrates and compares the differences in current accounts of EMs from Q2 2020 to Q2 2021.

The recent developments pose certain risks to the current account going forward. Firstly, as the coronavirus slowly fades, consumers in AEs might substitute the expenditures on goods back to services, which decreases the exports of EMs over time, shifting back to pre-corona levels. The second is that the de-globalisation trend will continue going forward and re-shoring will move some export products from EMs towards AEs. As explained earlier, a current account surplus makes it easier for countries to service their foreign currency debt. However, if one of the above scenarios materializes this might negatively impact the current account, leaving some EMs with current account deficits. In such a scenario the export cover is a factor that could limit the domestic FX currency risks. In Figure 11 we show how many months of imports can be covered by the FX reserves of the country. We observe that countries on the left-hand side, like Brazil, Russia and China, have many FX reserves, mitigating the risks of a depreciating currency. In contrast countries like Mexico, Hungary and Turkey are more vulnerable to FX shocks.

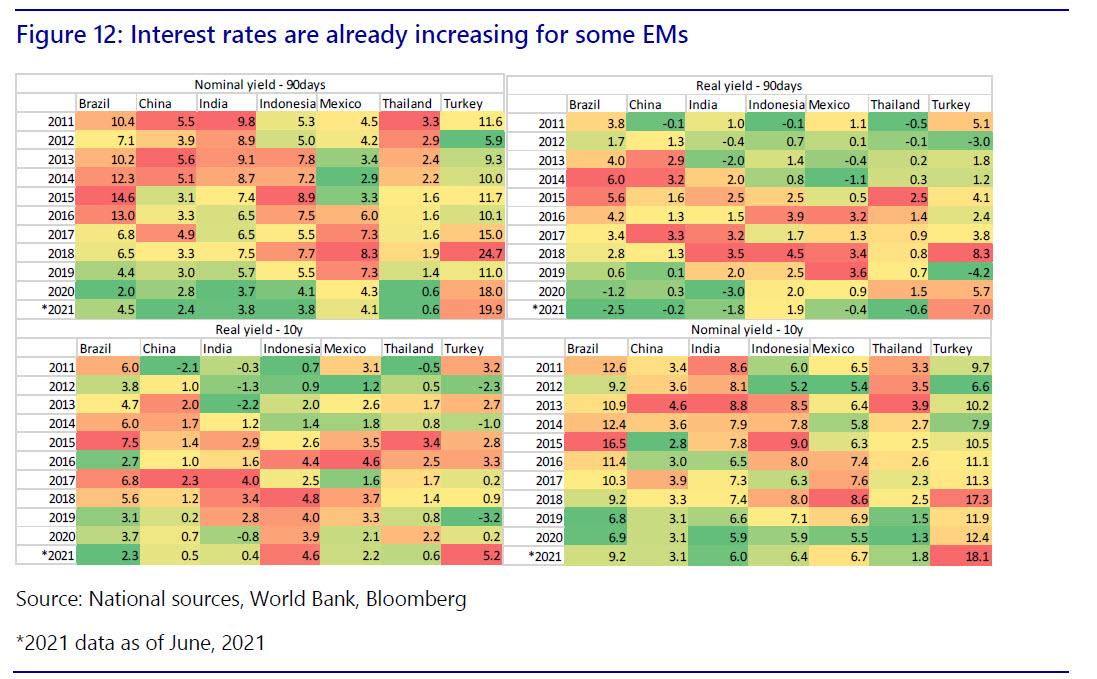

Interest rate costs

Nominal and real rates of EMs have steadily decreased over the past year partly as a result of the pandemic. But it is likely that 2021/22 will see a rise in interest rates across the emerging markets. This can be clearly seen with Brazil which is poised to hike its Selic rate by year-end to levels seen before the pandemic, but it has also been the case for other EMs like Russia and Chile. Anticipation of a US normalization of monetary policy might add pressures for central banks to hike sooner across the board.

To give a more nuanced picture we have captured the real short-term interest rates (ex-post) in Figure 12. These are negative for five out of the seven countries in consideration (nominal rate adjusted for inflation) in 2021. Countries are using this as an opportunity to increase short-term borrowing instead of longer-term borrowing. This has been observed across both AEs and EMs. The strategy is to roll over short-term debts in the current “higher” inflation environment and wait for the market uncertainty to settle before converting it to long-term debt. Some countries like China and Mexico are relying on recovering revenues to pay back this debt, while others, like India, are also looking at privatization of public sector entities for the required cash.

However, emerging markets will probably not be benefitting from negative real interest rates forever. Figure 12 already illustrates that nominal and real interest rates have started to climb in some countries over the course of 2021. So while the public debt figures kept climbing, the pandemic (or rather the related fiscal and monetary measures) temporarily reduced the cost of financing for most countries. Nevertheless, there is an increasing likelihood of higher interest rates on the back of inflation expectations and subsequent rate hikes by central banks. Higher interest rates will probably lead to higher interest rate costs for EMs, posing a threat to debt sustainability going forward.

Having discussed some important indicators to monitor with regard to emerging market vulnerability, the question is: how do all of these factors add up?

The final ranking

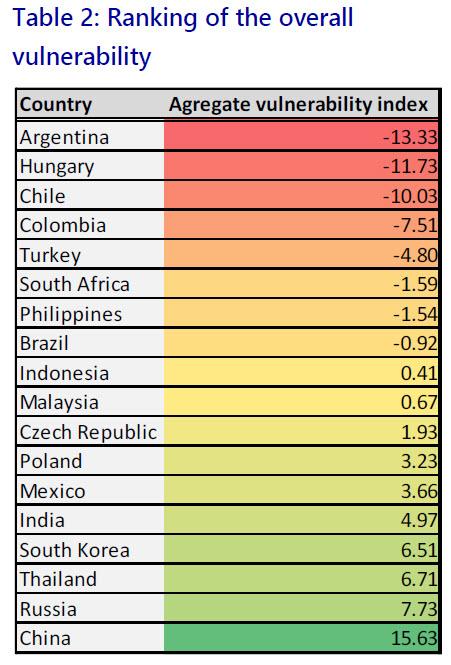

Table 1 summarizes the main factors determining EM vulnerability according to the indicators included in our Heatmap. In Table 2 we have added them up to get a general sense of which countries can be deemed more vulnerable with regard to the indicators included. In general we see that LatAm countries are relatively vulnerable compared to their peers. Asian countries are relatively less vulnerable, although the Philippines, Malaysia and Indonesia are increasingly vulnerable and rank lower compared to six months ago. The same holds for South Korea, although it is still close to the top of the chart. European countries are now better ranked than 6 months ago although their individual scores did not improve so much.

In conclusion, we hope that the use of the Heatmap and accompanying economic indicators has helped to sketch a clear picture of potential risks and vulnerabilities of EMs. Naturally, they help to indicate risks and compare the relative vulnerabilities of EMs. However, keep in mind that these are based on current economic indicators and are therefore an illustration of the current situation and vulnerability. They do not include any forecasts or have the intention to rank future economic performance of the countries included.

International

Four Years Ago This Week, Freedom Was Torched

Four Years Ago This Week, Freedom Was Torched

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare…

Share this:

Authored by Jeffrey Tucker via The Brownstone Institute,

"Beware the Ides of March,” Shakespeare quotes the soothsayer’s warning Julius Caesar about what turned out to be an impending assassination on March 15. The death of American liberty happened around the same time four years ago, when the orders went out from all levels of government to close all indoor and outdoor venues where people gather.

It was not quite a law and it was never voted on by anyone. Seemingly out of nowhere, people who the public had largely ignored, the public health bureaucrats, all united to tell the executives in charge – mayors, governors, and the president – that the only way to deal with a respiratory virus was to scrap freedom and the Bill of Rights.

And they did, not only in the US but all over the world.

The forced closures in the US began on March 6 when the mayor of Austin, Texas, announced the shutdown of the technology and arts festival South by Southwest. Hundreds of thousands of contracts, of attendees and vendors, were instantly scrapped. The mayor said he was acting on the advice of his health experts and they in turn pointed to the CDC, which in turn pointed to the World Health Organization, which in turn pointed to member states and so on.

There was no record of Covid in Austin, Texas, that day but they were sure they were doing their part to stop the spread. It was the first deployment of the “Zero Covid” strategy that became, for a time, official US policy, just as in China.

It was never clear precisely who to blame or who would take responsibility, legal or otherwise.

This Friday evening press conference in Austin was just the beginning. By the next Thursday evening, the lockdown mania reached a full crescendo. Donald Trump went on nationwide television to announce that everything was under control but that he was stopping all travel in and out of US borders, from Europe, the UK, Australia, and New Zealand. American citizens would need to return by Monday or be stuck.

Americans abroad panicked while spending on tickets home and crowded into international airports with waits up to 8 hours standing shoulder to shoulder. It was the first clear sign: there would be no consistency in the deployment of these edicts.

There is no historical record of any American president ever issuing global travel restrictions like this without a declaration of war. Until then, and since the age of travel began, every American had taken it for granted that he could buy a ticket and board a plane. That was no longer possible. Very quickly it became even difficult to travel state to state, as most states eventually implemented a two-week quarantine rule.

The next day, Friday March 13, Broadway closed and New York City began to empty out as any residents who could went to summer homes or out of state.

On that day, the Trump administration declared the national emergency by invoking the Stafford Act which triggers new powers and resources to the Federal Emergency Management Administration.

In addition, the Department of Health and Human Services issued a classified document, only to be released to the public months later. The document initiated the lockdowns. It still does not exist on any government website.

The White House Coronavirus Response Task Force, led by the Vice President, will coordinate a whole-of-government approach, including governors, state and local officials, and members of Congress, to develop the best options for the safety, well-being, and health of the American people. HHS is the LFA [Lead Federal Agency] for coordinating the federal response to COVID-19.

Closures were guaranteed:

Recommend significantly limiting public gatherings and cancellation of almost all sporting events, performances, and public and private meetings that cannot be convened by phone. Consider school closures. Issue widespread ‘stay at home’ directives for public and private organizations, with nearly 100% telework for some, although critical public services and infrastructure may need to retain skeleton crews. Law enforcement could shift to focus more on crime prevention, as routine monitoring of storefronts could be important.

In this vision of turnkey totalitarian control of society, the vaccine was pre-approved: “Partner with pharmaceutical industry to produce anti-virals and vaccine.”

The National Security Council was put in charge of policy making. The CDC was just the marketing operation. That’s why it felt like martial law. Without using those words, that’s what was being declared. It even urged information management, with censorship strongly implied.

The timing here is fascinating. This document came out on a Friday. But according to every autobiographical account – from Mike Pence and Scott Gottlieb to Deborah Birx and Jared Kushner – the gathered team did not meet with Trump himself until the weekend of the 14th and 15th, Saturday and Sunday.

According to their account, this was his first real encounter with the urge that he lock down the whole country. He reluctantly agreed to 15 days to flatten the curve. He announced this on Monday the 16th with the famous line: “All public and private venues where people gather should be closed.”

This makes no sense. The decision had already been made and all enabling documents were already in circulation.

There are only two possibilities.

One: the Department of Homeland Security issued this March 13 HHS document without Trump’s knowledge or authority. That seems unlikely.

Two: Kushner, Birx, Pence, and Gottlieb are lying. They decided on a story and they are sticking to it.

Trump himself has never explained the timeline or precisely when he decided to greenlight the lockdowns. To this day, he avoids the issue beyond his constant claim that he doesn’t get enough credit for his handling of the pandemic.

With Nixon, the famous question was always what did he know and when did he know it? When it comes to Trump and insofar as concerns Covid lockdowns – unlike the fake allegations of collusion with Russia – we have no investigations. To this day, no one in the corporate media seems even slightly interested in why, how, or when human rights got abolished by bureaucratic edict.

As part of the lockdowns, the Cybersecurity and Infrastructure Security Agency, which was and is part of the Department of Homeland Security, as set up in 2018, broke the entire American labor force into essential and nonessential.

They also set up and enforced censorship protocols, which is why it seemed like so few objected. In addition, CISA was tasked with overseeing mail-in ballots.

Only 8 days into the 15, Trump announced that he wanted to open the country by Easter, which was on April 12. His announcement on March 24 was treated as outrageous and irresponsible by the national press but keep in mind: Easter would already take us beyond the initial two-week lockdown. What seemed to be an opening was an extension of closing.

This announcement by Trump encouraged Birx and Fauci to ask for an additional 30 days of lockdown, which Trump granted. Even on April 23, Trump told Georgia and Florida, which had made noises about reopening, that “It’s too soon.” He publicly fought with the governor of Georgia, who was first to open his state.

Before the 15 days was over, Congress passed and the president signed the 880-page CARES Act, which authorized the distribution of $2 trillion to states, businesses, and individuals, thus guaranteeing that lockdowns would continue for the duration.

There was never a stated exit plan beyond Birx’s public statements that she wanted zero cases of Covid in the country. That was never going to happen. It is very likely that the virus had already been circulating in the US and Canada from October 2019. A famous seroprevalence study by Jay Bhattacharya came out in May 2020 discerning that infections and immunity were already widespread in the California county they examined.

What that implied was two crucial points: there was zero hope for the Zero Covid mission and this pandemic would end as they all did, through endemicity via exposure, not from a vaccine as such. That was certainly not the message that was being broadcast from Washington. The growing sense at the time was that we all had to sit tight and just wait for the inoculation on which pharmaceutical companies were working.

By summer 2020, you recall what happened. A restless generation of kids fed up with this stay-at-home nonsense seized on the opportunity to protest racial injustice in the killing of George Floyd. Public health officials approved of these gatherings – unlike protests against lockdowns – on grounds that racism was a virus even more serious than Covid. Some of these protests got out of hand and became violent and destructive.

Meanwhile, substance abuse rage – the liquor and weed stores never closed – and immune systems were being degraded by lack of normal exposure, exactly as the Bakersfield doctors had predicted. Millions of small businesses had closed. The learning losses from school closures were mounting, as it turned out that Zoom school was near worthless.

It was about this time that Trump seemed to figure out – thanks to the wise council of Dr. Scott Atlas – that he had been played and started urging states to reopen. But it was strange: he seemed to be less in the position of being a president in charge and more of a public pundit, Tweeting out his wishes until his account was banned. He was unable to put the worms back in the can that he had approved opening.

By that time, and by all accounts, Trump was convinced that the whole effort was a mistake, that he had been trolled into wrecking the country he promised to make great. It was too late. Mail-in ballots had been widely approved, the country was in shambles, the media and public health bureaucrats were ruling the airwaves, and his final months of the campaign failed even to come to grips with the reality on the ground.

At the time, many people had predicted that once Biden took office and the vaccine was released, Covid would be declared to have been beaten. But that didn’t happen and mainly for one reason: resistance to the vaccine was more intense than anyone had predicted. The Biden administration attempted to impose mandates on the entire US workforce. Thanks to a Supreme Court ruling, that effort was thwarted but not before HR departments around the country had already implemented them.

As the months rolled on – and four major cities closed all public accommodations to the unvaccinated, who were being demonized for prolonging the pandemic – it became clear that the vaccine could not and would not stop infection or transmission, which means that this shot could not be classified as a public health benefit. Even as a private benefit, the evidence was mixed. Any protection it provided was short-lived and reports of vaccine injury began to mount. Even now, we cannot gain full clarity on the scale of the problem because essential data and documentation remains classified.

After four years, we find ourselves in a strange position. We still do not know precisely what unfolded in mid-March 2020: who made what decisions, when, and why. There has been no serious attempt at any high level to provide a clear accounting much less assign blame.

Not even Tucker Carlson, who reportedly played a crucial role in getting Trump to panic over the virus, will tell us the source of his own information or what his source told him. There have been a series of valuable hearings in the House and Senate but they have received little to no press attention, and none have focus on the lockdown orders themselves.

The prevailing attitude in public life is just to forget the whole thing. And yet we live now in a country very different from the one we inhabited five years ago. Our media is captured. Social media is widely censored in violation of the First Amendment, a problem being taken up by the Supreme Court this month with no certainty of the outcome. The administrative state that seized control has not given up power. Crime has been normalized. Art and music institutions are on the rocks. Public trust in all official institutions is at rock bottom. We don’t even know if we can trust the elections anymore.

In the early days of lockdown, Henry Kissinger warned that if the mitigation plan does not go well, the world will find itself set “on fire.” He died in 2023. Meanwhile, the world is indeed on fire. The essential struggle in every country on earth today concerns the battle between the authority and power of permanent administration apparatus of the state – the very one that took total control in lockdowns – and the enlightenment ideal of a government that is responsible to the will of the people and the moral demand for freedom and rights.

How this struggle turns out is the essential story of our times.

CODA: I’m embedding a copy of PanCAP Adapted, as annotated by Debbie Lerman. You might need to download the whole thing to see the annotations. If you can help with research, please do.

* * *

Jeffrey Tucker is the author of the excellent new book 'Life After Lock-Down'

International

Red Candle In The Wind

Red Candle In The Wind

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by…

Share this:

By Benjamin PIcton of Rabobank

February non-farm payrolls superficially exceeded market expectations on Friday by printing at 275,000 against a consensus call of 200,000. We say superficially, because the downward revisions to prior months totalled 167,000 for December and January, taking the total change in employed persons well below the implied forecast, and helping the unemployment rate to pop two-ticks to 3.9%. The U6 underemployment rate also rose from 7.2% to 7.3%, while average hourly earnings growth fell to 0.2% m-o-m and average weekly hours worked languished at 34.3, equalling pre-pandemic lows.

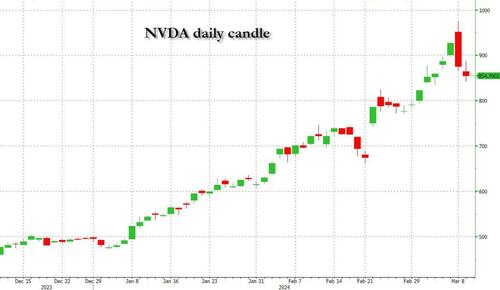

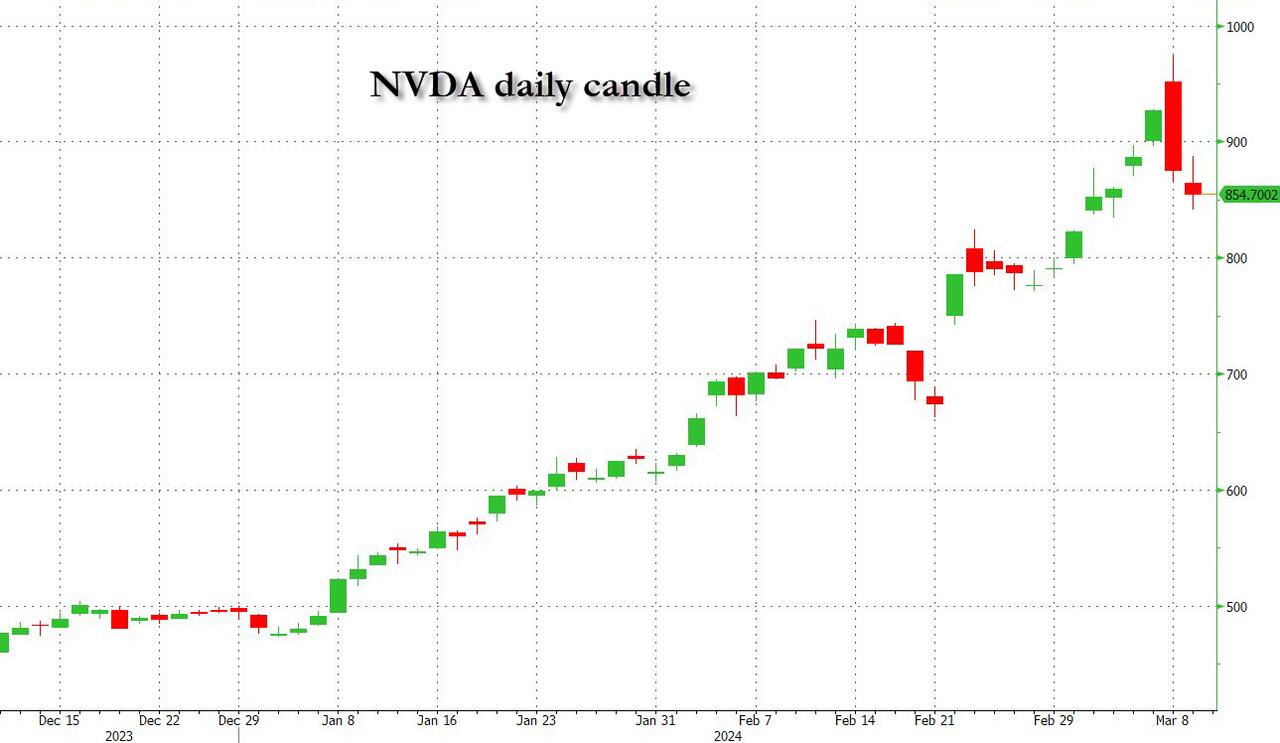

Undeterred by the devil in the detail, the algos sprang into action once exchanges opened. Market darling NVIDIA hit a new intraday high of $974 before (presumably) the humans took over and sold the stock down more than 10% to close at $875.28. If our suspicions are correct that it was the AIs buying before the humans started selling (no doubt triggering trailing stops on the way down), the irony is not lost on us.

The 1-day chart for NVIDIA now makes for interesting viewing, because the red candle posted on Friday presents quite a strong bearish engulfing signal. Volume traded on the day was almost double the 15-day simple moving average, and similar price action is observable on the 1-day charts for both Intel and AMD. Regular readers will be aware that we have expressed incredulity in the past about the durability the AI thematic melt-up, so it will be interesting to see whether Friday’s sell off is just a profit-taking blip, or a genuine trend reversal.

AI equities aside, this week ought to be important for markets because the BTFP program expires today. That means that the Fed will no longer be loaning cash to the banking system in exchange for collateral pledged at-par. The KBW Regional Banking index has so far taken this in its stride and is trading 30% above the lows established during the mini banking crisis of this time last year, but the Fed’s liquidity facility was effectively an exercise in can-kicking that makes regional banks a sector of the market worth paying attention to in the weeks ahead. Even here in Sydney, regulators are warning of external risks posed to the banking sector from scheduled refinancing of commercial real estate loans following sharp falls in valuations.

Markets are sending signals in other sectors, too. Gold closed at a new record-high of $2178/oz on Friday after trading above $2200/oz briefly. Gold has been going ballistic since the Friday before last, posting gains even on days where 2-year Treasury yields have risen. Gold bugs are buying as real yields fall from the October highs and inflation breakevens creep higher. This is particularly interesting as gold ETFs have been recording net outflows; suggesting that price gains aren’t being driven by a retail pile-in. Are gold buyers now betting on a stagflationary outcome where the Fed cuts without inflation being anchored at the 2% target? The price action around the US CPI release tomorrow ought to be illuminating.

Leaving the day-to-day movements to one side, we are also seeing further signs of structural change at the macro level. The UK budget last week included a provision for the creation of a British ISA. That is, an Individual Savings Account that provides tax breaks to savers who invest their money in the stock of British companies. This follows moves last year to encourage pension funds to head up the risk curve by allocating 5% of their capital to unlisted investments.

As a Hail Mary option for a government cruising toward an electoral drubbing it’s a curious choice, but it’s worth highlighting as cash-strapped governments increasingly see private savings pools as a funding solution for their spending priorities.

Of course, the UK is not alone in making creeping moves towards financial repression. In contrast to announcements today of increased trade liberalisation, Australian Treasurer Jim Chalmers has in the recent past flagged his interest in tapping private pension savings to fund state spending priorities, including defence, public housing and renewable energy projects. Both the UK and Australia appear intent on finding ways to open up the lungs of their economies, but government wants more say in directing private capital flows for state goals.

So, how far is the blurring of the lines between free markets and state planning likely to go? Given the immense and varied budgetary (and security) pressures that governments are facing, could we see a re-up of WWII-era Victory bonds, where private investors are encouraged to do their patriotic duty by directly financing government at negative real rates?

That would really light a fire under the gold market.

Government

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

Trump "Clearly Hasn’t Learned From His COVID-Era Mistakes", RFK Jr. Says

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President…

Share this:

{kind=link}

{kind=link}

{kind=link}

Authored by Jeff Louderback via The Epoch Times (emphasis ours),

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

{kind=link}

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Red Candle In The Wind

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Is the National Guard a solution to school violence?

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Trump “Clearly Hasn’t Learned From His COVID-Era Mistakes”, RFK Jr. Says

The next pandemic? It’s already here for Earth’s wildlife

Fauci Deputy Warned Him Against Vaccine Mandates: Email

Vaccine-skeptical mothers say bad health care experiences made them distrust the medical system

Survey Shows Declining Concerns Among Americans About COVID-19

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

International4 days ago

International4 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International4 days ago

International4 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoGOP Efforts To Shore Up Election Security In Swing States Face Challenges