Brace For Astronomical Shipping Costs As China Goes Into Lockdown Mode

Brace For Astronomical Shipping Costs As China Goes Into Lockdown Mode

With the latest weekly update of container shipping rates showing that prices – already at all time high – simply refuse to back down, as rates from China to the US surpas

Brace For Astronomical Shipping Costs As China Goes Into Lockdown Mode

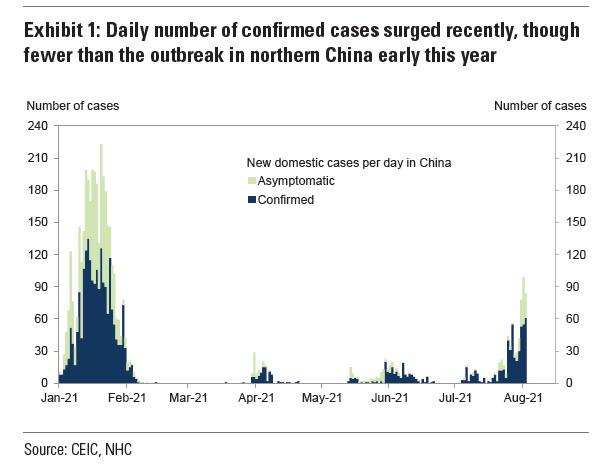

With the latest weekly update of container shipping rates showing that prices - already at all time high - simply refuse to back down, as rates from China to the US surpassing a record $20,000, a new threat looms which could send already sky high prices into orbit. As the delta variant spreads on the mainland, most Chinese ports are now requiring a Covid test for all crew, with vessels forced to remain at anchor until negative results are confirmed, and requiring ships to quarantine for 14-28 days if they previously berthed in India or changed crew within 14 days of arriving.

That spells further delays, further price increases and, according to Splash, shipping will need to start to make contingency plans should China - the world’s most important nation for shipping movements - emerge as another pandemic epicenter.

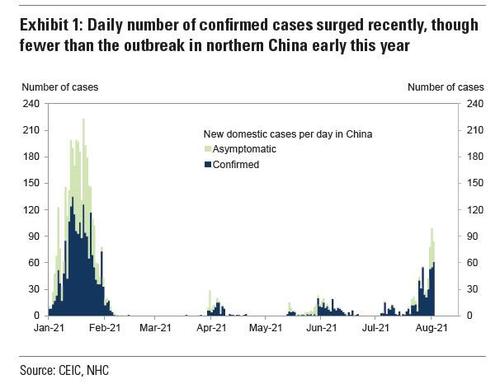

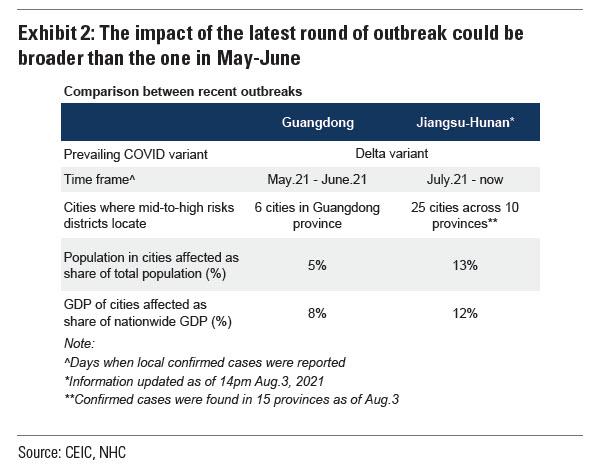

The delta variant has broken through the country’s virus defences, which are some of the strictest in the world, and reached nearly half of China’s 32 provinces in just two weeks. While the overall number of infections — more than 360 so far — is still lower than Covid resurgences elsewhere, the wide spread indicates that the variant is moving quickly with many millions of Chinese now in lockdown.

“For freight markets, the implications include delays at ports as authorities screen crews of incoming vessels and a hit to China’s oil demand if widespread lockdowns are imposed,” a report from Braemar ACM pointed out this week.

When a Covid-19 outbreak was detected at Yantian Port in late May, operations at the key southern Chinese export hub were slashed by 70% for most of June. Similar disruptions are in the cards in the coming weeks, while shipyards are also likely to see their delivery schedules come under pressure if any wider lockdown measures are taken.

“As long as lockdowns remain confined to China, the impact on freight markets is likely to be muted, especially in the case of wet and dry freight. The container market seems most vulnerable if we see more severe disruptions to manufactured products supply chains,” commented Plamen Natzkoff, senior trade expert at VesselsValue. On the potential tanker ramifications, Natzkoff said: “An immediate impact of a lockdown in China is reduced population mobility which would have a direct impact on demand for transportation fuels, potentially impacting negatively the tanker market.”

On the possible consequences for the container sector, Alan Murphy, CEO of Danish consultancy Sea-Intelligence, reminded readers of what happened in February 2020 when China first went into lockdown. Carriers responded with a wave of blank sailings.

“Assuming that a strict China lockdown would lead to a scenario as in February 2020, we would expect a drop in production of 15-20% for about a month,” Murphy suggested.

While that at first might not sound too detrimental, after all that is in rough numbers what happens every normal Chinese New Year, 2021 is not a normal year.

“Cargo owners, already stressed beyond sanity from devastatingly high freight rates and absurd surcharges, and with no way to secure neither equipment nor space, would suddenly see their procurement costs sky-rocket in addition to their back-breaking logistics costs,” Murphy predicted, adding that the one possible silver lining for shippers could be that as the production decreases start to wave out to the Chinese ports, pressure would start to ease off on the ocean bottleneck, which could start to bring down freight rates.

The added concern Murphy has is if Chinese ports were not able to run at full capacity, like Yantian earlier this summer.

"For container shipping, which is more than red-hot at the moment, even a brief halt in Chinese exports is likely to ease the crunch a bit logistically so long as a lockdown only closes manufacturing sectors and not ports and terminals," commented Peter Sand, chief shipping analyst at BIMCO.

Nick Ristic, a dry bulk analyst at Braemar ACM, said the sector would not be as badly affected as it was at the start of the pandemic last year.

“Based on the experience in other countries with prolonged lockdowns, it seems the world has learnt how to keep things running with restrictions in place,” Ristic pointed out. Of greater concern for Ristic is the state of consumer demand and the underlying economy in China, which is starting to slow down.

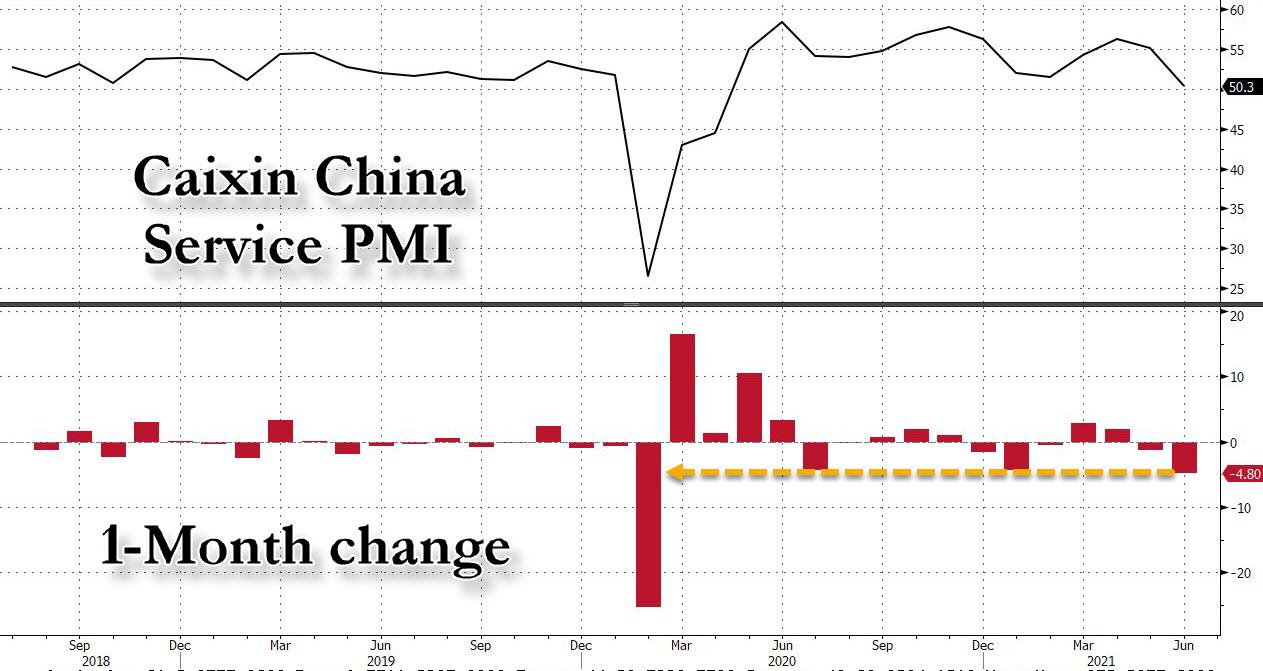

“This could take some real steam out of the Chinese economy and manufacturing base. PMIs are already weakening too,” Ristic said.

Factory activity expanded at the slowest pace in 15 months in China last month as new orders dropped. The Caixin/Markit manufacturing PMI fell to 50.3 in July from 51.3 in June, the lowest since the covid pandemic started.

Bulk carrier congestion in China hit a five-year high of 50.5m dwt over the weekend, rising by 24% year-on-year as new restrictions were put in place in ports across the country. Current queues are 76% above the five-year average according to data from Braemar ACM as Covid-19-related protocols affect all sectors of the dry bulk market, worsening the crew change crisis in the process.

Newly reported positive Covid-19 cases in China have recently forced the country to re-introduce restrictions to curb the spread of the virus. Most ports in the country are now requiring a nucleic acid test for all crew, with vessels forced to remain at anchor until negative results are confirmed.

Many ports in the country are also requiring vessels to quarantine for 14-28 days if they previously berthed in India or performed a crew change within 14 days of arriving in China. “While it is unclear how long these measures will be in place for, they will likely tighten the dry market in the near-term,” Braemar ACM suggested in a note to clients yesterday.

Ralph Leszczynski, global head of research at Banchero Costa, like most analysts contacted by Splash, was adamant that China would not press ahead with a national lockdown. “Larger scale lockdowns would be unsustainable economically, so can happen at local level – in a single neighborhood or city, but not for whole provinces, not to mention nationwide,” Leszczynski said.

China has managed to carry out one of the largest vaccination campaigns this year, with over 60% of the population already reportedly vaccinated, and an 80% vaccination threshold likely to be reached by September or October.

“China will certainly try now to contain and eliminate the current outbreak, but if they don’t manage to do that, and it spreads uncontrollably nationwide, I think they are more likely to shift towards more of a living with Covid strategy thanks to vaccination in the autumn, similar to what Singapore has announced recently, rather than shutting down the whole country, which would be unsustainable economically and create discontent,” Leszczynski said.

Mark Williams, who heads up British consultancy Shipping Strategy, concurred with Leszczynski, telling Splash: “More likely than a national lockdown is a series of targeted lockdowns by province or county. If those lockdowns include coastal regions, key ports and logistics centres, then globalised supply chains will become chaotic.”

Commenting on the latest developments in the increasingly whacky world of hyperinflating shipping rates, Rabobank's Michael Every made the following observations:

Before this surge in shipping costs, most economists thought logistics were invisible, efficient, and of no interest. Like plumbing, you need it, but don’t let it dictate your plans for the day;

Those logistics assumptions were only possible because since 1945 the US Navy has kept global sea lanes open and safe for all maritime traffic. Pirates and hijacking get attention today because they are *rare* – but they did not used to be. Indeed, global sea lanes used to be carved up by empires for their preferred shipping and production, not open to all;

That paradigm starting to fray along with the rest of the post-WW2 global architecture;

Current price surges are due to massive supply-demand imbalances that are not going to go away any time soon;

But imagine shipping costs, and the broader implications, if we get maritime chaos in the Straits of Hormuz, around Suez, or in the South China Sea;

Building new maritime capacity from ship to port to warehouse to rail to truck to store to home to address our supply-demand imbalances is tied to the post-Covid economic geography: is it still a post-1945 open economy?; if not, where will things be made? We still don’t know, but we BRI vs. B3W is an example of how things are trending;

In short, Every concludes, the ship of apolitical logistics has sailed: "Just as ‘a conservative is a liberal who has been mugged’, so a ‘mercantilist is a free trader with squeezed supply chains’."

Pharma and biotech’s top R&D spenders in 2023: a $153B total with M&A as a focus

At a time when biotech is still counting its losses as a thaw gradually sets in after the long market winter, pharma has been on a tear. M&A took off…

At a time when biotech is still counting its losses as a thaw gradually sets in after the long market winter, pharma has been on a tear. M&A took off in Q4 as the industry’s biggest R&D spenders either rolled the dice on the back of their blockbuster bonanzas, were forced to address gaping holes in the pipeline in the face of looming patent expirations, or simply had no choice in the face of repeated setbacks.

Bioregnum Opinion Column by John Carroll

For some, it was all of the above.

As a result, Merck flipped into the lead position generally occupied by Roche with an M&A-inflated expense line for research. The companies joined a hunt for new drugs frequently focused on Phase III; premiums are in — heavy preclinical risks are out of favor. The majors followed some well-worn paths into immunology and oncology. And 2024 kicked off with a new round of buyouts and licensing deals.

The sudden end of Covid as a vaccine, drug and diagnostic market left the likes of Pfizer scrambling to convince investors that they had an exciting new plan. (It’s not working so far.) Eli Lilly has become one of the most valuable companies on the planet as obesity drugs go mainstream. Leaders like Takeda kept upping the ante on the R&D budget as the numbers frayed, with all but Pfizer and Bristol Myers Squibb — two of the most deeply off-balance biopharmas — spending more in 2023. Across the board, we saw $153 billion accounted for in R&D budget lines for last year — which would have registered as a record even without the sudden bolus of spending at Merck.

New, promising drugs at biotechs aren’t getting cheaper. And some of the blockbusters pharma has to cover as the patent cliff approaches will demand multiple replacement franchises.

The Big 15 have the money, desire and need to do much, much more in R&D. And all signs indicate that we’ll see more through 2024.

Merck

Roche

J&J

Novartis

AstraZeneca

Pfizer

Eli Lilly

Bristol Myers Squibb

GSK

AbbVie

Sanofi

Gilead

Takeda

Amgen

Novo Nordisk

1. Merck: The BD team is remaking the pipeline, and they are moving fast

The big picture: Merck moved up to the top of the list this year by bundling a mother lode of M&A and drug licensing deals into the R&D expense line. Otherwise, the top slot would have gone to Roche, the traditional top title holder in the R&D 15.

Merck has been parlaying its unchallenged position as number one in the PD-1 game with Keytruda — a drug that earned $25 billion last year but will face a loss of exclusivity as patents start to expire in 2028 — into a host of big deals in 2023. Keytruda, meanwhile, has cruised to 39 approvals, leaving Bristol Myers’ Opdivo in its wake.

Too much commercial success, though, doesn’t translate into unending praise. Analysts had been grumbling for some time that Merck wasn’t doing enough to diversify its pipeline bets. But that’s been changing.

Merck tallied $5.5 billion upfront for its Daiichi Sankyo deal — picking up rights to three ADCs in the move — along with the across-the-slate hikes in costs for clinical programs, bigger payrolls and benefits. There was another charge for the $11.4 billion that went to buying Prometheus and Imago. Prometheus accounted for $10.8 billion of that — one of the biggest deals that followed the $11.5 billion Acceleron buyout in 2021. With $690 million in cash for a group of partners that includes Moderna, Orna and Orion.

Merck kicked off the new year with a $680 million buyout of Harpoon Therapeutics, underscoring its enduring interest in the oncology market. And it’s leaving no popular stone unturned, capturing attention with its expressed interest in GLP-1 combos as the next generation of weight loss drugs takes shape.

Merck CEO Rob Davis also recently made it clear that the pharma giant can afford more $1 billion-to-$15 billion deals, making it a top candidate for more deals in 2024.

Merck’s firepower on the deals side, though, is needed after some deep wrinkles marred the pipeline plan, like the FDA’s back-to-back CRLs for chronic cough drug gefapixant. The data, however, never matched up to Merck’s rhetoric. Failures in Alzheimer’s and depression underscored Merck’s traditional ill fortunes in neuro.

Merck has a few years to plan for its next big thing. They show every sign of remaining focused on the big prize ahead.

2. Roche: 2023 was a tough year. Will 2024 be any better on the R&D side?

The big picture: It’s not easy being Roche. The behemoth has long had a near-omnivorous approach to R&D, buying up and down the pipeline at all stages with a big appetite for oncology ahead of neuro, ophthalmology and immunology. This year, it’s had to contend with the elimination of its Covid revenue, once a big player on the diagnostics side as testing soared during the pandemic. They’ve had to lower investors’ expectations of 2024 sales to an embarrassingly modest level and saw their stock price slide.

It’s surprising they have any growth, given the corresponding knockoff competition building for Lucentis and Esbriet, but you can’t play with market expectations. They’ll kill you every time you’re off.

Roche found some silver linings in the Vabysmo franchise and they’ve been a significant player on the M&A side, scoring the Carmot buyout for $3 billion after bagging Telavant for $7.1 billion back in October, paying a price for something Pfizer all but gave away to Roivant. James Sabry and the BD team, meanwhile, have kept up their globetrotting ways, uncorking a slate of deals for JP Morgan.

Sabry moved to global BD chief at Roche after winning his spurs at Genentech, and he’s been in the game for quite a long time. His résumé includes a stint as a biotech CEO. He’s the doyen of dealmakers and isn’t sitting on the sidelines. Hope grows eternal at Roche, and to keep it growing, Sabry has to stay busy.

“We have in total 12 NMEs that could potentially transition into a Phase III during this year,” CEO Thomas Schinecker told analysts hopefully during their Q4 call.

On this scale, Roche tends to do things on a wholesale basis. So when execs recently unveiled a pipeline review, they mapped 146 programs covering 82 new molecular entities. That can be hard to keep up with. If raw numbers like that were a good indicator of future success, though, Roche wouldn’t have these troubles.

It’s less difficult to follow the culls. That includes a slate of neurology drugs, with several axed from the oncology area. The write-offs include the longtime disappointment crenezumab, which had been partnered with AC Immune in Alzheimer’s. Roche recently handed back crenezumab as well as semorinemab after working with AC Immune for close to an R&D generation. Some analysts gave up long ago.

We’ve also been hearing complaints about a lack of upcoming pivotal clinical data to arouse enthusiasm. But Roche has two big R&D groups at work trying to counter those impressions, with gRED (Genentech) and pRED (the traditional Roche research group) at bat. They now have a straight-up GLP-1/GIP drug in the clinic for obesity, with oral therapies in the works alongside many others. It may be late to the obesity game with the Carmot buyout, but Roche still sees opportunities worth paying for.

Execs are promising to play a better R&D game, prioritizing their best assets and piling on resources. But Roche has always been willing to invest heavily in R&D. Now the company needs to see some clinical cards fall its way. This has not been a patient market.

3. J&J: Under new management, J&J doubles down on the innovative side of R&D. Can they still surprise us?

The big picture: J&J typically has weighed in heavy on R&D, particularly if you add its medtech work to the total. Even after splitting that out, though, it’s still in the top five, hoovering up large numbers of early-stage licensing deals while occasionally nabbing something major in the $1 billion-plus category.

Last year the pharma giant punted its consumer division, following the footsteps of many major industry outfits, and shut down its work in infectious diseases and vaccines. RSV, a highly competitive field now, went out the window with a host of smaller programs and alliances. Its major fields of interest zero in on oncology, immunology, cardio and retinal disorders. And they chipped in close to $2 billion to join the ADC hunt in January with its acquisition of Ambrx.

J&J earned a rep for out-of-the-box thinking in oncology under former oncology R&D chief Peter Lebowitz, striking a deal with China’s Legend that delivered an approved drug — Carvykti — and following up with a $245 million pact to gain worldwide rights to another CAR-T from CBMG, a low-profile Chinese biotech that erupted into mainstream view with its Big Pharma deal.

Now the big questions about J&J focus on its new leadership after Joaquin Duato moved into the CEO’s role in 2022 and John Reed — leaping into his third Big Pharma R&D posting in 10 years, following Roche and Sanofi — takes command of the global R&D side of the company.

They have plenty of motivation to hustle up major new approvals. Stelara — raking in more than $10 billion a year — will see its patent protection erode in the US in 2025, with Europe moving first this year. That will take a few big wins to cover.

But J&J has been making big promises for years. Just a few months ago, it touted 20 drugs in the pipeline that could fuel 5% to 7% growth through 2030. One of the prime candidates is a drug they picked up from Protagonist: JNJ-2113, an IL-23 they believe can bring in blockbuster revenue in immunology. J&J, though, is likely far from done when it comes to new deals. Oncology R&D has been changing rapidly in the wake of the Inflation Reduction Act, with researchers moving up OS as a primary initial focus in Phase III. And it’s going to take a behemoth effort to deliver on these numbers, with likely failures and shortfalls along the way.

Don’t look for J&J to cut R&D anytime soon. They have a big agenda.

4. Novartis: Another streamlining move is wrapping up as Novartis vows to get back to basics in R&D — again

The big picture: Novartis CEO Vas Narasimhan has been crystal clear about the Big Pharma’s M&A strategy. He’s sticking with the industry sweet spot now in favor: picking up late-stage assets below the $5 billion range. A few weeks ago, that led Novartis to MorphoSys, where they have been partnered for years while distancing themselves from rumors of a pricey Cytokinetics play.

And it springs right off another $3 billion acquisition — for Chinook — that went straight to positive Phase III data for the kidney drug atrasentan, which likely wasn’t much of a surprise inside Novartis.

These days, Narasimhan and Novartis are all about focus. They want to make a deeper impact where they emphasize their priorities — cardio, immunology, neuroscience and oncology. And they also want to be leaders where they are centered, slashing oncology while emphasizing at every opportunity that they jumped out front in radioligands, now a hot commodity in R&D.

Lest anyone forget, Novartis was a pioneer in autologous CAR-T and has held on as it slowly works through all the challenges a cutting-edge technology can inspire.

Narasimhan had been five years before the mast as CEO, after being promoted from development chief, and he’s revising a pipeline strategy away from something he describes now as akin to everything everywhere all at once. Downsizing in 2023 was the big focus, dropping programs, reassigning scientists and promising a swifter pace — a never-ending problem in Big Pharma land. Narasimhan has also been pushing “seamlessness,” projecting a new era of cooperation among scientists and sales.

There’s nothing new about streamlining at Novartis, though. Narasimhan had a billion dollars of cuts in mind back in the spring of 2022. And periodically, the company has been well-known for going in and ironing out budgets. Changes have included an exit for development chief John Tsai, now a biotech CEO, who was replaced by Shreeram Aradhye. Fiona Marshall took the helm at NIBR in the fall of 2022, taking the place of Jay Bradner, who left and later wound up running R&D at Amgen.

The recent cleanup at Novartis included the end of the deal for BeiGene’s PD-1, an area that proved enormously frustrating to Novartis. Their TIGIT pact ended last summer. Phase II for GT005, a gene therapy it picked up in the $800 million Gyroscope buyout, didn’t end well. That program got the axe. And their anti-TGFß antibody, picked up in a small deal with Xoma nine years ago, failed after execs once billed it as a high-risk, high-reward play. Other setbacks include Adakveo, which faced global regulatory challenges following the failure of the Phase III confirmatory study. At the beginning of this year, there was a snafu in Phase III for ligelizumab, once billed as a top asset for peanut allergies.

Warning clouds have also formed around their top-selling drug Entresto, as Novartis fights a battle against the IRA and price negotiations.

The CEO, though, has been able to transition while the stock price was headed up, with a few big drugs driving revenue growth as a struggling Sandoz finally got the heave-ho in a spinout. Their franchise drug Kisqali, for example, is now billed as a $4 billion earner at the peak. As a result, their story has played well on Wall Street. Investors want to see the money and the trajectory. R&D follows sales in priority when it comes to the majors.

5. AstraZeneca: Pascal Soriot never takes defeat lying down. And that stubborn attitude has delivered big dividends as another big R&D test takes shape

The big picture: Back in 2018, AstraZeneca reported R&D expenses just under $6 billion. In the past five years, that big line item has grown 85%, and investors have seen the stock price grow 56%.

The R&D leaders at AstraZeneca have changed, but CEO Pascal Soriot has become a longtime fixture at the company. During his stint he took the weakest pipeline in biopharma and turned it into one of the strongest, building a slate of blockbuster oncology franchises while building a research machine based in Cambridge, UK, that consumes about $1 out of every $4 in revenue. He bet the ranch on Enhertu and won, with some analysts bullishly projecting peak sales that will break $10 billion. And he’s kept many of the promises he had to fire out to investors to keep an unwanted Pfizer takeover at bay in the way back when.

So what’s next?

That’s a question that’s vexing quite a few analysts. AstraZeneca is a restless player and the company takes a lot of chances — which means it racks up a lot of setbacks.

A major initiative aimed at protecting its revenue involves its legal fight against the IRA, which AstraZeneca has so far lost. Its next big ADC with Daiichi Sankyo, Dato-DXd, has sparked a running debate on its potential approval and some analysts have doubted if it can live up to the hype following weak PFS results for the TROP2 ADC. Last summer an early-stage GLP-1 went down in flames, unable to take the heat in a kitchen currently controlled by the commercial chefs at Novo Nordisk and Eli Lilly. Lokelma, picked up in a 2015 buyout, got hit when R&D decided to quash two Phase III studies, denting once-big hopes for blockbuster status. And Soriot has recently been forced to finally give up on one old failure when he finally punted roxadustat’s US rights.

Soriot, though, is a weathered player when it comes to setbacks. Every loss is an opportunity to do better the next time, and no one can be more stubborn. You could see that play out over Covid when its vaccine came in for some undue criticism that blighted its impact in the face of the mRNA stars. That spurred some angry responses as execs dug in. But there was an unexpected upside. The giant didn’t have to readjust as the Covid market went pfffffft.

Their next step: A couple of months ago AstraZeneca touted its new vaccine platform, buying Icosavax for $838 million in cash while contributing an RSV vaccine to the pipeline — a field where GSK has made major headway — and a virus-like particle platform that the company intends to build on.

Volrustomig, a PD-1/CTLA-4 bispecific antibody, has been accelerated into Phase III, with Soriot claiming a leadership spot in bispecifics: “Our portfolio of bispecifics has the potential to replace the first-generation checkpoint inhibitors across a range of cancers.”

And that GLP-1 fail? Last November AstraZeneca paid $185 million to gain a Phase I GLP-1 drug out of China’s Eccogene. And now they’re mapping combo studies with some of their other drugs in a play at creating the next wave of obesity therapies with an edge.

Word in biopharma is that Soriot has been devoting a considerable amount of face time to China, where he committed the company years ago. That’s another one of those market promises that has seen plenty of ups and downs. But Soriot tends to win the big gambles more than he loses, and in this industry, seeing it through can be a major long-term advantage.

6. Pfizer: What the hell happened to the Covid king?

↑

R&D spending 2023: $10.57 billion

R&D spending 2022: $11.4 billion

Change: -7.3%

Revenue: $58.5 billion (down 42% from $100.3 billion)

The big picture: There was one brief, shining moment — or two — when Pfizer could seemingly do no wrong. It had taken a leading role in breaking through scientific barriers to create a new Covid vaccine in record time, harvested a bumper crop of cash and CEO Albert Bourla was the darling of the world’s favored pharma industry.

That was then.

Now, Bourla and his team are having a tough time convincing Wall Street that the company can do even simple things right. They paid $43 billion to bag Seagen and mount a major new campaign on the cancer front, but its stock has been blighted and the focus turned to cost-cutting as revenue plunged. There was fresh humiliation when Roivant flipped a drug it had grabbed from Pfizer for lunch money and sold it to Roche for $7.1 billion a year later. And Pfizer has lost the narrative in convincing investors it can get back to growth.

That somewhat hapless rep was burnished considerably when Pfizer reported that its first try at an oral GLP-1 obesity drug had flopped. It’s still working to move the dial in the hottest new field in pharma, but so is a long list of rivals. Instead of spurring renewed faith in Pfizer, the obesity play turned into another example of getting it wrong, and the focus at Pfizer shifted squarely to downsizing and cost-cutting in acknowledgment of the new reality that set in.

Bourla, though, is committed to pushing the story that a new period of growth lies ahead. And it’s not proving easy.

At the end of February, Pfizer made its best pitch for oncology, underscoring plans to seize the leadership role in genitourinary and breast cancer while making promises for eight-plus possible blockbusters in the next six years. R&D promises, though, are easy to make and hard to keep. Right now, the clarion call in pharma is “show me the money.”

With Covid and the mRNA revolution forgotten like last season’s hit show, there’s an enormous gap now that will be devilishly hard to bridge. But don’t expect anyone at Pfizer to stop trying anytime soon.

7. Eli Lilly: Built for the long term, Lilly’s day has arrived — and they don’t want to let go

The big picture: Historically, Eli Lilly has been known as a ponderously slow pharma outfit that often slowly cruised its way into Phase III squalls. But that view is so 2017. In 2024, Lilly has rebranded itself as the Big Pharma engine that could, and did, blow out expectations. And if it’s still not quite as nimble as some analysts might like, its ability to deliver in massively expensive late-stage studies for drugs aimed at big populations has made it a darling of quite the investor crowd.

Lilly, for example, was thwarted at getting an accelerated approval for its Alzheimer’s med, but that didn’t really cut expectations, with blockbuster peak sales projections — even as Biogen/Eisai’s Leqembi suffers from dimming prospects as their high hopes are lowered by the reality of limited sales in the face of limited efficacy.

That pales, though, in comparison to the bright rainbow that’s emerged in obesity. Lilly continues to work up manufacturing capacity to meet demand for its new obesity version of tirzepatide, the GLP-1/GIP drug building up the diabetes franchise, where neither of the two leaders has been able to meet a seemingly limitless demand.

Lilly attracted considerable attention for its vow to build out manufacturing capacity ahead of Phase III data for its next-gen oral version, orforglipron, while clearly so unhappy about Novo’s decision to muscle in and snap up Catalent that CEO Dave Ricks is grousing about the antitrust implications of their rival’s move. Lilly, though, has bragging rights to solid pivotal data in a market that is nowhere close to saturation point.

Like a lot of the big spenders on the list, Eli Lilly has been hunting new immunology drugs and plunked down $2.4 billion for Dice last summer. That was part of a full slate of acquisitions, including a pair of small ADC companies. Following yet another hot trend, there was a $1.4 billion deal for Point, which put them into radiopharmaceuticals.

Lilly nabbed two new drug approvals last year as it waited on the 2 big franchises in obesity and Alzheimer’s. That’s a testament to the progress that Dan Skovronsky spurred after the global player made him R&D chief 6 years ago. Eli Lilly execs still may not always be first, in an industry where first can be tremendously important to commercialization. But they’ve been right where it counts big in drug development, and it will take a therapeutic earthquake to alter that perception anytime in the near term.

8. Bristol Myers Squibb: A rough year spurs a cut in R&D spending and some major late-stage R&D deals

The big picture: This is a terrible time to try and explain why your Big Pharma company has structural issues that flattened or eroded sales revenue. Pfizer understands that and Bristol Myers got a bad taste of it as its shares slid 18% in the last year.

In both cases, the CEOs stepped up with a transition plan. The companies did some deals, but the late-stage stuff wasn’t cheap. And in Bristol Myers’ case, a new CEO was able to draw a line between its aging franchises and the new arrivals on the market, which saw some growth. The company line now: Just wait for the big pipeline hits to come and give us some time to weather the decline of these legacy drugs and you’ll love what you see.

Investors may not be cheering, but Bristol Myers’ stock did get some traction out of it in the last few weeks.

It was clear well before 2023 arrived that Bristol Myers understood it was facing some of those dreaded headwinds. That 2% drop in R&D spending highlighted the tight rein on spending for what remains a top 10 player in the pharma R&D world. Major figures in R&D, headed by Rupert Vessey, exited the company — in Vessey’s case, later making the flip to biotech at Flagship. And there was an unusual spat with Dragonfly after the pharma giant walked away from its $650 million investment.

New CEO Chris Boerner spotlighted the immediate strategy at hand: M&A. Mirati and KRAS came their way for $5.8 billion. RayzeBio happily landed a premium on top of the premium they had just scored in an IPO, as Bristol Myers followed rivals into radiopharmaceuticals. The $14 billion Karuna buyout put them into a late-stage race on Alzheimer’s, another R&D category that’s been enjoying a renaissance some years after pharma fled the scene.

Boerner’s bottom line in the Q4 review is that the company will steer more into bolt-on plays — rather than big buyouts — and licensing deals like the SystImmune alliance. That sets the stage for a “transition” period that will last until 2028, four long years ahead, when it’s promising “top-tier” results. It will also be looking at lower-priced competition for Opdivo.

Even before 2028, though, BMS will start losing patent protection on Eliquis. They’ve already begun price negotiations with Medicare. And Eliquis earned $12.2 billion in 2022, making it their number-one franchise. That’s left Bristol Myers and Pfizer, both under huge pressure to perform and do more late-stage deals, backing a full-court press in the courts to keep generics at bay.

Bristol Myers has had an active dealmaking arm for years, including in the wake of its big $74 billion buyout of Celgene, which also delivered Vessey to the pharma giant. That was just five years ago after Celgene had fallen on some troubled times. Celgene had been a standout in the licensing field, known for sampling a wide variety of drug plays in the industry pipeline. One of Bristol’s big failures, though, was ceding the high ground in PD-1 to Merck’s Keytruda, which has been buoying its rival for years. Bristol needs major drug franchises to make a difference in this world, and any future setbacks on the leading drugs it’s been buying now will not be welcome by investors.

There is a path forward for Bristol, of course, even as it vows to pay down debt. But it’s fairly narrow, and this field is known for some treacherous results.

9. GSK: After picking up some badly-needed revenue steam, what’s next for R&D?

The big picture: Tony Wood is still shy of his second anniversary as the CSO at GSK, but with an RSV vaccine riding high as a new blockbuster franchise and Shingrix looking every bit the long-distance franchise player GSK needs, he has a reassuring revenue foundation to work with. ViiV’s steady work in HIV — where GSK is a majority owner — also offers a confidence-building revenue stream. And the departure of the consumer unit is well into the rearview mirror now.

Its stock has done well, too, up 28% in the past year.

That’s quite a changed picture from the early days of his predecessor, Hal Barron, who came in with deep oncology experience and a big need to demonstrate a broad-based pipeline reorganization to overcome a well-earned rep for underperformance. Wood’s first moves in R&D were largely defensive, giving up some major alliances — such as a partnership with Adaptimmune — that looked shaky.

GSK has made a lot of early bets, and the risks involved naturally portend that many of its deals won’t survive. You can see that in play right through its recent decision to dump a pair of Vir partnerships in infectious diseases.

In their place, GSK has been inking major new development deals with the likes of China’s Hansoh, for ADCs. Oncology, though, is still only a small performer overall. And it’s been a focus for a while.

GSK spent a billion dollars upfront to bag a mid-stage asthma drug at Aiolos in a rare M&A deal. There was also the $2 billion Bellus buyout last fall, with an eye to creating a new franchise for chronic cough. But there’s been a notable absence of any splashy deals at GSK, with a reorg in research that offers GSK’s latest take on improving efficiency.

We’ll see how that goes.

In the meantime, GSK is doing what it can to stir up some excitement for late-stage drugs like depemokimab (again in asthma), camlipixant (from Bellus) as well as the antibiotic gepotidacin for UTIs/gonorrhea. It’s an uphill fight, though, without much megablockbuster razzmatazz built in. But GSK is a careful player.

After getting stuck with the rep for having one of the worst pipelines in pharma, though, reliable and steady progress with a high-profile launch in RSV will suit just fine. At least for now. It’s likely that investors will keep pressing for something big in Phase III, and that could cost CEO Emma Walmsley a considerable amount of BD money.

10. AbbVie: The slow-motion collapse of Humira keeps them focused on the bottom line while growing R&D spending

The big picture: As Rick Gonzalez finishes his final run as CEO, he’s able to look back on a year that saw AbbVie complete its revamp period as the long-awaited — long, long-awaited — arrival of generic Humira bites into its old cash cow.

The great split at Abbott that created AbbVie set up a scenario where the company would pull out every stop to milk Humira for every conceivable dollar possible, delivering mega-returns while Gonzalez became the poster child of patent reform. The bottom line for AbbVie’s team: What’s repeated waves of congressional criticism with the stock price on the line?

Now AbbVie is able to boost expected revenue on the two big drugs developed on Gonzalez’s watch — Skyrizi and Rinvoq — with two new acquisitions to feed future sales projections. The buyout of Botox created a new, highly reliable franchise for AbbVie’s commercial team to lean on.

AbbVie is skilled at acquiring and building revenue. It had its eyes set on the ADC drug Elahere when it acquired ImmunoGen for $10 billion. Initially approved in 2022 for ovarian cancer, the drug is now being positioned for earlier lines of therapy.

Less than a week after the ImmunoGen deal was announced, AbbVie was back for a late-stage acquisition with the $8.7 billion for Cerevel’s neuro play. The deal will bring in clinical-stage assets for schizophrenia, Parkinson’s and dementia, as CNS moves back into a warmer phase in Wall Street circles. Both buyouts underscore Big Pharma’s considerable appetite for new products, with premiums in play for de-risked drug programs.

Gonzalez’s departure barely caused a murmur on the markets, which is a testament to his success in delivering for shareholders a secure, long-term rebuild. His legacy is a company with a ruthless rep for shepherding drug revenue while building a big interest in curtailing patents for pharma. But looking only at the numbers, he proved the winner at the company as the game was played during his tenure.

11. Sanofi: Paul Hudson is still out to make a great first impression in R&D

The big picture: When Paul Hudson showed up in San Francisco for JP Morgan in January, ready to talk up plans for the road ahead, he noted: “It feels like a lot longer than four years that we’ve been on this journey.”

But Hudson has always been more comfortable sounding like a newly-coined CEO, plotting a turnaround. And in the last few months, he’s played every card in that deck. The announcement late last year that Sanofi is bumping its R&D budget is central to that theme, though the news of its impact on profitability led to a rout of the stock price. And he delights in spotlighting late-stage assets, even though a slate of his early bets failed or have yet to prove themselves.

In what is now standard in pharma, Hudson made what he could out of the news he was spinning out the consumer division. Again, though, investors were less than thrilled by the gambit.

This time around the PR track, Hudson has boasting rights to the recently approved RSV drug Beyfortus, which comes with some big peak sales projections from Jefferies and much, much less from others. We’ll know soon enough if this is a winner or the latest disappointment at Sanofi. And, as always, there’s the Sanofi touchstone: Its megablockbuster Dupixent, which the pharma giant was able to partner on with Regeneron years ago — keeping the franchise fresh and expanding. Dupixent is the cash cow that gives Sanofi the financial strength needed to move ahead.

And that means there’s capacity for more dealmaking.

Not long after the San Francisco appearance, Hudson followed up on his M&A assurances with a $1.7 billion drug buyout, carving out a Phase II drug for a rare disease called alpha-1 antitrypsin deficiency, or AATD. It fits right into the zone for 2024, where pharma can only get positive attention for something within sight of an approval.

Like others on this list, Sanofi’s R&D rep will ultimately rest on its ability to deliver on the 12 would-be blockbusters the company is betting on. That includes three “products in a pipeline“: amlitelimab, frexalimab and SAR441566 (oral TNFR1si). They’re followed by tolebrutinib, lunsekimig, rilzabrutinib, an anti-TL1A in IBD, an IRAK4 degrader and itepekimab for COPD.

Behind it all, Hudson has also been promising to make Sanofi a leader in AI-assisted pharma operations. Sanofi, though, has been promising a makeover in innovation for well over a decade and has done nothing to prove it’s worked beyond staying on track with the megablockbuster it got from Regeneron. One breakout franchise delivered on Hudson’s watch would change that in a heartbeat.

We’re waiting.

12. Gilead: The CEO gambled on big innovation — and often lost. But the wagers keep coming

The big picture: Daniel O’Day jumped into the CEO job at Gilead five years ago and hit the ground running. He hasn’t stopped, even though some of his biggest bets have run into brick walls.

That was apparent weeks ago with the news that Gilead would ice its work on blood cancer involving magrolimab, the CD47 drug picked up in a $5 billion buyout back in 2020. Their mid-stage work on solid tumors ground to a halt shortly after.

Rehashing and refocusing their deal with Arcus, putting in significantly more money while axing one of the Phase IIIs, didn’t help.

Gilead’s rep was built around HIV, where it has remained dominant, though more than a bit taken for granted. The old regime’s follow-up — after a cloudburst of cash for curing hep C that quickly dried up — was to buy out Kite and take a pioneering position in CAR-T, which hasn’t lived up to the financial hype that attended its arrival, despite the clear scientific innovation it brought to the field.

The stock was hammered hard in January after Trodelvy — acquired in the 2020 Immunomedics buyout, which achieved blockbuster status last year — failed a Phase III in second-line lung cancer.

But when you raise doubts and see your stock sinking, counter with a late-stage buyout. That’s clearly what O’Day had in mind when he plunked down more than $4 billion to buy CymaBay after the biotech unveiled late-stage data on seladelpar. Gilead bought a would-be blockbuster with a PDUFA date. And that’s a sign of some desperation at a company that badly needs a breakout.

13. Takeda: Moving up another notch on the top 15, as profitability wobbles, Takeda execs are still reaching for the golden ring in R&D

The big picture: Takeda has been aggressively taking chances in R&D right from the time CEO Christophe Weber and R&D chief Andy Plump teamed up to remake the aging Japanese pharma company into a global drug player back in 2015. That meant steadily upping the ante in R&D — now up another slot in this year’s rankings — and investing in deals like the Shire buyout, which gave Plump his base in the Cambridge/Boston hub, along with a big stake in rare diseases.

For Takeda, that mission meant a broad effort to develop a major pipeline, from collaborations through Phase III. More recently, it’s been about concentrating their new work around a pair of key deals, particularly the $4 billion acquisition of Nimbus’ TYK2. It likely wasn’t much of a surprise, but their drug — which also has a $2 billion rider for milestones — cleared a Phase IIb hurdle in psoriatic arthritis.

For Takeda, it’s a clear indication of just how popular it is these days for pharma players to zero in on late-stage therapies in search of relatively near-term approvals.

Want more evidence of that?

Takeda bet $400 million in cash and more than a billion dollars in milestones to gain rights to Hutchmed’s fruquintinib and then was rewarded with an approval for treatment-naive cases of colorectal cancer in the fall. And they demonstrated its continued appetite in the rare disease space with the recent $300 million deal for Protagonist’s late-stage drug rusfertide, designed to treat a rare blood disease called polycythemia vera (PV).

The risks it’s taken on have been readily apparent to Takeda’s leaders, with its decision to drop Exkivity after flunking the Phase III NSCLC confirmatory trial, a Phase II fail for its key metachromatic leukodystrophy program, as well as a decision to drop Theravance as a partner after a seven-year alliance. The late-stage setbacks cost Takeda a $770 million write-down. Add in a loss of exclusivity for Vyvanse in 2023 — a $3 billion blockbuster in fiscal 2022 — and you have the outlines of unsteady performance for the pharma player, with Weber promising to do better in the near term.

Takeda is unusual in the Big Pharma world for winding up its fiscal year at the end of March. In order to do an apples-to-apples comparison, they prepared a summary of their R&D expenses and revenue for all of 2023 for Endpoints News.

14. Amgen: Capitalizing on a history of striking high-profile deals, Amgen stays in the spotlight

The big picture: Amgen is a considerable distance from spending on research like the top 10 players in our R&D 15, but it frequently finds ways to box competitively in the biggest heavyweight category. It had done that with KRAS, taking a legit scientific advance that couldn’t quickly move the dial in a major way on the commercial side. That happens a lot in oncology. And now it’s in the spotlight with an obesity drug — branded as MariTide now — with hopes to take on the likes of Eli Lilly and Novo Nordisk.

The chutzpah originates with longtime CEO Bob Bradway, who has parlayed his Wall Street cred as a former banker at Morgan Stanley into major league status with a savvy understanding of the numbers and investors. He skillfully navigated the $28 billion Horizon buyout last year, bagging a lineup of commercial therapies as the company looks for the approaching patent cliff on Enbrel, a reliable blockbuster that has kept the revenue flowing in.

Amgen may not do a lot in M&A or Phase III, but what it does do, it does with style.

To complete the Horizon deal, Bradway had to orchestrate a deal with the FTC to skirt its objections to price bundling, which essentially leaves the pharma company on commercial probation with regular reporting to the federal agency. That took skill and boldness while maintaining the CEO’s rep for delivering on the bottom line. Its stock is up 18% over the past year.

Analysts will be watching carefully to see how Jay Bradner does in the top R&D post after the Harvard prof-and-former-NIBR chief assumes the seat of David Reese, now chief technology officer. Reese seems truly energized in his new role heading up tech, and Bradner is a die-hard research enthusiast who loves nothing better than jumping into conversations about the details of target degeneration.

Amgen is all about message.

15. Novo Nordisk: The longtime diabetes franchise player has a breakout run going in obesity — with vows to stay in front

The big picture: R&D spending as a percentage of sales has edged up a bit in the last few years, but the key driver here is GLP-1, where Novo has capitalized on its first-in-class leadership position in obesity. After decades spent in the shadow of chronic R&D failure, safety issues and a recent swarm of largely ineffective drugs, the obesity field is crushing it. That has swelled sales revenue as semaglutide glowed, so Novo’s research spending has boomed at a fast pace.

Now that the good times are rolling, and Novo already has a well-earned rep as a realistic and committed player in diabetes, which didn’t come cheap or easy, the new player on the R&D 15 is promising to stay out front — no easy task with Eli Lilly gunning for it. Novo has been snapping up new obesity tech at a furious pace, determined to stay out front.

Its one limiting factor here has been manufacturing capacity. Novo can’t satisfy the demand for a drug that is now a staple of public conversation, as the field gets a boost from a wide range of celebrities, including Oprah Winfrey. That’s marketing you could buy, but don’t have to. It’s coming for free.

With uncharacteristic bravado, Novo doubled down by striking a deal to acquire the global CDMO giant Catalent for $16.5 billion, and Lilly has been fuming about the antitrust aspects as CEO Dave Ricks complains that worldwide manufacturing capacity has either been maxed out or is not easily converted from its existing uses.

Novo’s commitment to growing R&D has international implications that far exceed the limits of its home country of Denmark, extending to hubs in Oxford, Seattle and Beijing. Most recently, Novo has committed to boosting its Boston-area research hub. And it’s likely to remain a key player in its dominant fields — unless some other tech can topple the megablockbuster that is remaking this company.

Novo may be at the end of this list in terms of R&D spending, but it has overachieved with its success for semaglutide. It has the capacity to do more and should continue to climb for several years to come as it makes a case for continued growth.

Postscript: Regeneron, with $4.44 billion in research spending — up 23% over $3.6 billion in 2022 — deserves an honorable mention in the competitive 16th spot. This year, Regeneron expects R&D spending to top up at or close to $5 billion. The company’s value has swollen on the success of its high-profile founders, Len Schleifer and George Yancopoulos, who continue to build the company — hitting a market cap in excess of $100 billion with the stock up 29% over the past year. Regeneron will likely find its way into the top 15 at some point, and we’ll be watching for it.

Chronic stress and inflammation linked to societal and environmental impacts in new study

From anxiety about the state of the world to ongoing waves of Covid-19, the stresses we face can seem relentless and even overwhelming. Worse, these stressors…

From anxiety about the state of the world to ongoing waves of Covid-19, the stresses we face can seem relentless and even overwhelming. Worse, these stressors can cause chronic inflammation in our bodies. Chronic inflammation is linked to serious conditions such as cardiovascular disease and cancer – and may also affect our thinking and behavior.

Credit: Image: Vodovotz et al/Frontiers

From anxiety about the state of the world to ongoing waves of Covid-19, the stresses we face can seem relentless and even overwhelming. Worse, these stressors can cause chronic inflammation in our bodies. Chronic inflammation is linked to serious conditions such as cardiovascular disease and cancer – and may also affect our thinking and behavior.

A new hypothesis published in Frontiers in Science suggests the negative impacts may extend far further.

“We propose that stress, inflammation, and consequently impaired cognition in individuals can scale up to communities and populations,” explained lead author Prof Yoram Vodovotz of the University of Pittsburgh, USA.

“This could affect the decision-making and behavior of entire societies, impair our cognitive ability to address complex issues like climate change, social unrest, and infectious disease – and ultimately lead to a self-sustaining cycle of societal dysfunction and environmental degradation,” he added.

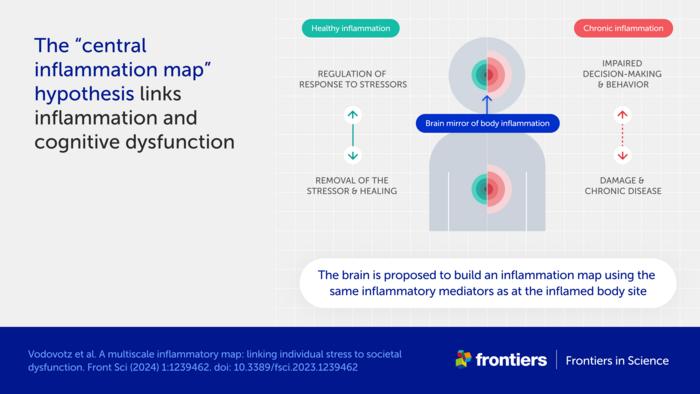

Bodily inflammation ‘mapped’ in the brain

One central premise to the hypothesis is an association between chronic inflammation and cognitive dysfunction.

“The cause of this well-known phenomenon is not currently known,” said Vodovotz. “We propose a mechanism, which we call the ‘central inflammation map’.”

The authors’ novel idea is that the brain creates its own copy of bodily inflammation. Normally, this inflammation map allows the brain to manage the inflammatory response and promote healing.

When inflammation is high or chronic, however, the response goes awry and can damage healthy tissues and organs. The authors suggest the inflammation map could similarly harm the brain and impair cognition, emotion, and behavior.

Accelerated spread of stress and inflammation online

A second premise is the spread of chronic inflammation from individuals to populations.

“While inflammation is not contagious per se, it could still spread via the transmission of stress among people,” explained Vodovotz.

The authors further suggest that stress is being transmitted faster than ever before, through social media and other digital communications.

“People are constantly bombarded with high levels of distressing information, be it the news, negative online comments, or a feeling of inadequacy when viewing social media feeds,” said Vodovotz. “We hypothesize that this new dimension of human experience, from which it is difficult to escape, is driving stress, chronic inflammation, and cognitive impairment across global societies.”

Inflammation as a driver of social and planetary disruption

These ideas shift our view of inflammation as a biological process restricted to an individual. Instead, the authors see it as a multiscale process linking molecular, cellular, and physiological interactions in each of us to altered decision-making and behavior in populations – and ultimately to large-scale societal and environmental impacts.

“Stress-impaired judgment could explain the chaotic and counter-intuitive responses of large parts of the global population to stressful events such as climate change and the Covid-19 pandemic,” explained Vodovotz.

“An inability to address these and other stressors may propagate a self-fulfilling sense of pervasive danger, causing further stress, inflammation, and impaired cognition in a runaway, positive feedback loop,” he added.

The fact that current levels of global stress have not led to widespread societal disorder could indicate an equally strong stabilizing effect from “controllers” such as trust in laws, science, and multinational organizations like the United Nations.

“However, societal norms and institutions are increasingly being questioned, at times rightly so as relics of a foregone era,” said Prof Paul Verschure of Radboud University, the Netherlands, and a co-author of the article. “The challenge today is how we can ward off a new adversarial era of instability due to global stress caused by a multi-scale combination of geopolitical fragmentation, conflicts, and ecological collapse amplified by existential angst, cognitive overload, and runaway disinformation.”

Reducing social media exposure as part of the solution

The authors developed a mathematical model to test their ideas and explore ways to reduce stress and build resilience.

“Preliminary results highlight the need for interventions at multiple levels and scales,” commented co-author Prof Julia Arciero of Indiana University, USA.

“While anti-inflammatory drugs are sometimes used to treat medical conditions associated with inflammation, we do not believe these are the whole answer for individuals,” said Dr David Katz, co-author and a specialist in preventive and lifestyle medicine based in the US. “Lifestyle changes such as healthy nutrition, exercise, and reducing exposure to stressful online content could also be important.”

“The dawning new era of precision and personalized therapeutics could also offer enormous potential,” he added.

At the societal level, the authors suggest creating calm public spaces and providing education on the norms and institutions that keep our societies stable and functioning.

“While our ‘inflammation map’ hypothesis and corresponding mathematical model are a start, a coordinated and interdisciplinary research effort is needed to define interventions that would improve the lives of individuals and the resilience of communities to stress. We hope our article stimulates scientists around the world to take up this challenge,” Vodovotz concluded.

The article is part of the Frontiers in Science multimedia article hub ‘A multiscale map of inflammatory stress’. The hub features a video, an explainer, a version of the article written for kids, and an editorial, viewpoints, and policy outlook from other eminent experts: Prof David Almeida (Penn State University, USA), Prof Pietro Ghezzi (University of Urbino Carlo Bo, Italy), and Dr Ioannis P Androulakis (Rutgers, The State University of New Jersey, USA).

Journal

Frontiers in Science

DOI

10.3389/1239462

Method of Research

Computational simulation/modeling

Subject of Research

Not applicable

Article Title

A multiscale inflammatory map: linking individual stress to societal dysfunction

Article Publication Date

12-Mar-2024

COI Statement

YV is a cofounder of, and stakeholder in, Immunetrics, Inc. and a consultant to Anuna AI. PFMJV is the founder of, and stakeholder in, Eodyne Systems s.l. and Sapiens5 Holding BV. DLK was employed by Tangelo – Intend, Inc. Neither these companies nor the funders mentioned above were involved in the study design, data collection, analysis, interpretation of data, the writing of this article, or the decision to submit it for publication. The companies mentioned above also did not provide funding for the study. The remaining author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest. The authors YV and PV declared that they are editorial board members of Frontiers, at the time of submission. This had no impact on the peer review process and the final decision.

Acadia’s Nuplazid fails PhIII study due to higher-than-expected placebo effect

After years of trying to expand the market territory for Nuplazid, Acadia Pharmaceuticals might have hit a dead end, with a Phase III fail in schizophrenia…

After years of trying to expand the market territory for Nuplazid, Acadia Pharmaceuticals might have hit a dead end, with a Phase III fail in schizophrenia due to the placebo arm performing better than expected.

Steve Davis

“We will continue to analyze these data with our scientific advisors, but we do not intend to conduct any further clinical trials with pimavanserin,” CEO Steve Davis said in a Monday press release. Acadia’s stock $ACAD dropped by 17.41% before the market opened Tuesday.

Pimavanserin, a serotonin inverse agonist and also a 5-HT2A receptor antagonist, is already in the market with the brand name Nuplazid for Parkinson’s disease psychosis. Efforts to expand into other indications such as Alzheimer’s-related psychosis and major depression have been unsuccessful, and previous trials in schizophrenia have yielded mixed data at best. Its February presentation does not list other pimavanserin studies in progress.

The Phase III ADVANCE-2 trial investigated 34 mg pimavanserin versus placebo in 454 patients who have negative symptoms of schizophrenia. The study used the negative symptom assessment-16 (NSA-16) total score as a primary endpoint and followed participants up to week 26. Study participants have control of positive symptoms due to antipsychotic therapies.

The company said that the change from baseline in this measure for the treatment arm was similar between the Phase II ADVANCE-1 study and ADVANCE-2 at -11.6 and -11.8, respectively. However, the placebo was higher in ADVANCE-2 at -11.1, when this was -8.5 in ADVANCE-1. The p-value in ADVANCE-2 was 0.4825.

In July last year, another Phase III schizophrenia trial — by Sumitomo and Otsuka — also reported negative results due to what the company noted as Covid-19 induced placebo effect.

According to Mizuho Securities analysts, ADVANCE-2 data were disappointing considering the company applied what it learned from ADVANCE-1, such as recruiting patients outside the US to alleviate a high placebo effect. The Phase III recruited participants in Argentina and Europe.

Analysts at Cowen added that the placebo effect has been a “notorious headwind” in US-based trials, which appears to “now extend” to ex-US studies. But they also noted ADVANCE-1 reported a “modest effect” from the drug anyway.

Nonetheless, pimavanserin’s safety profile in the late-stage study “was consistent with previous clinical trials,” with the drug having an adverse event rate of 30.4% versus 40.3% with placebo, the company said. Back in 2018, even with the FDA approval for Parkinson’s psychosis, there was an intense spotlight on Nuplazid’s safety profile.

Acadia previously aimed to get Nuplazid approved for Alzheimer’s-related psychosis but had many hurdles. The drug faced an adcomm in June 2022 that voted 9-3 noting that the drug is unlikely to be effective in this setting, culminating in a CRL a few months later.

As for the company’s next R&D milestones, Mizuho analysts said it won’t be anytime soon: There is the Phase III study for ACP-101 in Prader-Willi syndrome with data expected late next year and a Phase II trial for ACP-204 in Alzheimer’s disease psychosis with results anticipated in 2026.

Acadia collected $549.2 million in full-year 2023 revenues for Nuplazid, with $143.9 million in the fourth quarter.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}