Why Albert Edwards Is Starting To Panic About Soaring Food Prices

Why Albert Edwards Is Starting To Panic About Soaring Food Prices

Tyler Durden

Thu, 12/17/2020 – 16:41

Is it time to worry about food inflation?

The reason this has suddenly become a hot topic is because while overall inflation remains subdu

Share this:

Is it time to worry about food inflation?

The reason this has suddenly become a hot topic is because while overall inflation remains subdued (we will spare a discussion here of why the CPI is purposefully distorted to stay as low as possible - readers can catch up here, here and here), food inflation has been on a tear in recent months. In fact, it has gotten so high that earlier this week Goldman published a report looking at "The Recent Spike In Food Inflation", in which it noted that "in recent months, inflation has risen and surprised to the upside across a number of major EM economies (e.g. Turkey, South Africa, India, Brazil andRussia)." According to Goldman, one of the main drivers of these increases has been higher food inflation, which has coincided with a sharp increase in the price of some key agricultural commodities (e.g. grains, oils and soybeans)."

Yet despite admitting there is a clear food inflation problem, Goldman is quick to brush it off, making the following arguments:

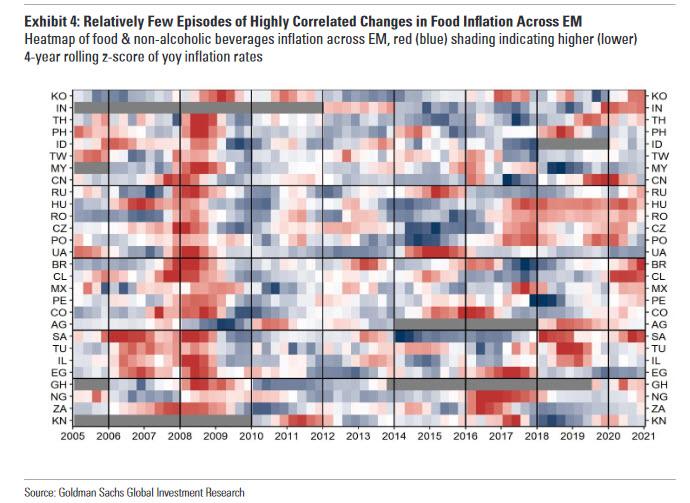

- Outside of major agricultural price shocks, the cross-country correlation in food inflation is generally weak, suggesting that food inflation is more typically driven by local rather than global factors. In addition, inflation in high-yield EMs is typically more sensitive to global agricultural commodity prices than in low-yielders, because food represents are latively large share of CPI baskets in low-income economies.

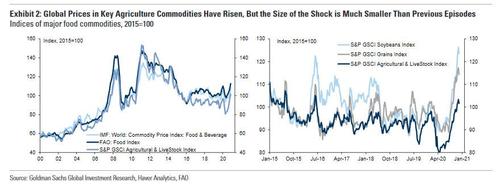

- Although the recent rise in food price inflation has been material in some EM economies, food inflation had previously been on a downward trend this year inmost EMs, and has generally exhibited much less volatility over the past 10 years than was previously the case. Similarly, while the recent rise in global agricultural commodity prices has been significant in percentage terms, the increase has been much more limited than the sharp swings observed between 2006-2012,and it follows a prolonged period in which agricultural prices had been relatively weak.

In short, Goldman dismisses the risk of surging food inflation especially in emerging markets, because "given the limited size of the shock to date, and with other factors (such as spare capacity) weighing on EM inflation, the recent rise in agricultural commodity prices would need to extend quite a bit further for it to have a significant and lasting effect on inflation and monetary policy across the majority of EMs."

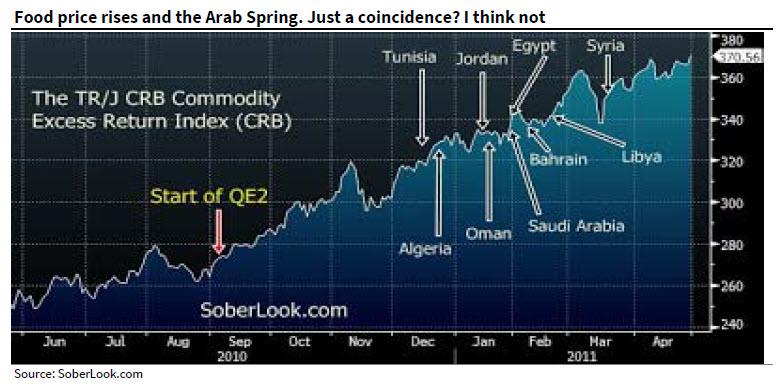

One wonders if Goldman was just as dismissive during the food price surge observed in late 2010 that ultimately culminated in the Arab Spring of early 2011. As the Guardian reminds us:

"A decade ago this week, a young fruit seller called Mohammed Bouazizi set himself alight outside the provincial headquarters of his home town in Tunisia, in protest against local police officials who had seized his cart and produce.”

It is this backdrop that brings us a far more concerning note published this morning from everyone's favorite permabear, SocGen's Albert Edwards, who unlike Goldman is starting to worry about food inflation. A lot.

As Edwards explains, for much of the past decade he - and other Fed skeptics - have railed about the distorting impact of QE on asset prices. And aside from capital markets where the Fed's intervention has spawned a record wealth divide leading to unprecedented political and social polarization, perhaps the most disturbing episode of such distortion was the abovementioned explosion of food prices that began towards the end of 2010. According to Edwards, many economists - this website included - believe the Fed’s QE2 was the primary cause for the 2010-11 bubble in food prices which contributed to the social unrest and ensuing revolutions in many Arab countries.

This is a problem because in a time when central banks are injecting a record $1.4 billion in liquidity every hour, and when most economists’ attention is now focused on the impact of the Fed’s QE on buoyant equity and industrial commodity prices, Albert says that "we should also watch the unfolding surge in food prices very closely indeed – and with trepidation."

The reason for that is again what happened in early 2011 in Tunisia: That event marked the start of a chain reaction of social unrest around the Middle East and elsewhere that toppled governments and became known as the Arab Spring, Edwards writes and adds that "although the narrative of these revolutions had its origins in longstanding grievances and a thirst for democracy, many economists identified rocketing global food prices from the end of 2010 as the trigger. (T’was always so: certainly, higher food prices contributed to both the French and Russian revolutions, and to the 1989 unrest in China.)"

As for whether central banks were responsible for these revolutionary dominoes, Edwards is a bit more nuanced, writing that while they certainly spawned much of the asset reflation observed in late 2010, "the truth is that central banks have no control over which financial bubbles will ultimately emerge as they spray QE into financial markets." It just so happens that food is one of them with alarming periodicity.

Case in point: bitcoin, which is soaring precisely because institutions have finally realized that central banks injecting 0.66% of GDP into capital markets every month will lift everything, even digital tokens with no intrinsic value. It will certainly lift food prices too.

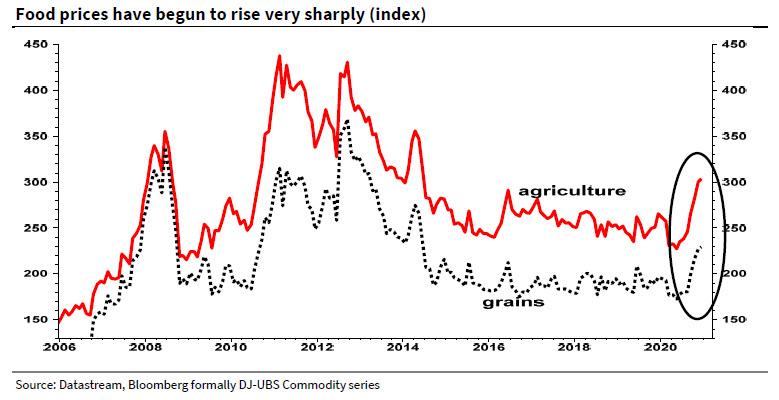

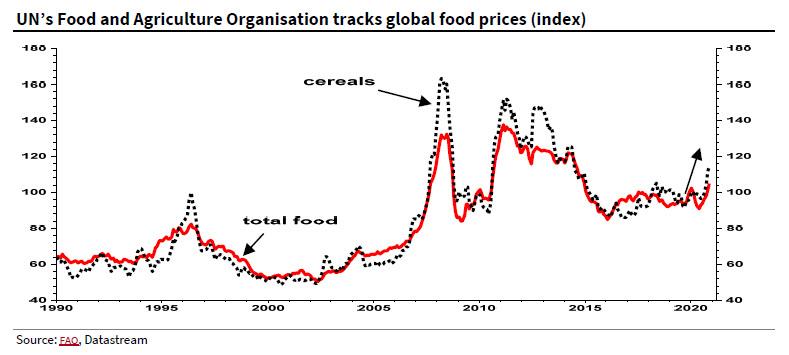

So going back to the facts, Edwards writes that "one thing you may have missed recently is that the UN’s Food and Agriculture Organization’s (FAO) widely followed food price index (the basket measures prices for oilseeds, dairy products, meat and sugar)" which as shown above, has - once again - been surging over the last few months. As noted previously, the FAO food index rose for a sixth month running in November, on pace to hit a six-year high, with Edwards noting that "annual inflation in cereals reached 20%, the highest annual rise since mid-2011 when the Arab Spring was in full flow! (see chart below)."

Edwards then doubles down on his makes his feelings clear on who ultimately was to blame for the global tidal wave in food inflation back in 2011: "Despite Ben Bernanke’s denials that the Fed’s QE policies caused rampant food price inflation in 2011 (link), many economists such as myself believe that was absolutely the case."

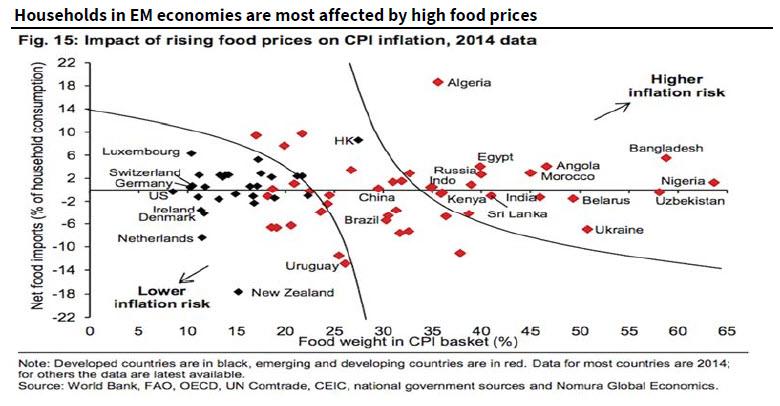

Next, Edwards expands on the superficial Goldman analysis, and points out that the effect of higher food prices tends to be much greater for EM countries that are 1) large net importers of food, and 2) where households spend a greater percentage of their income on food (ie they have a much larger weighting of food in their CPI basket).

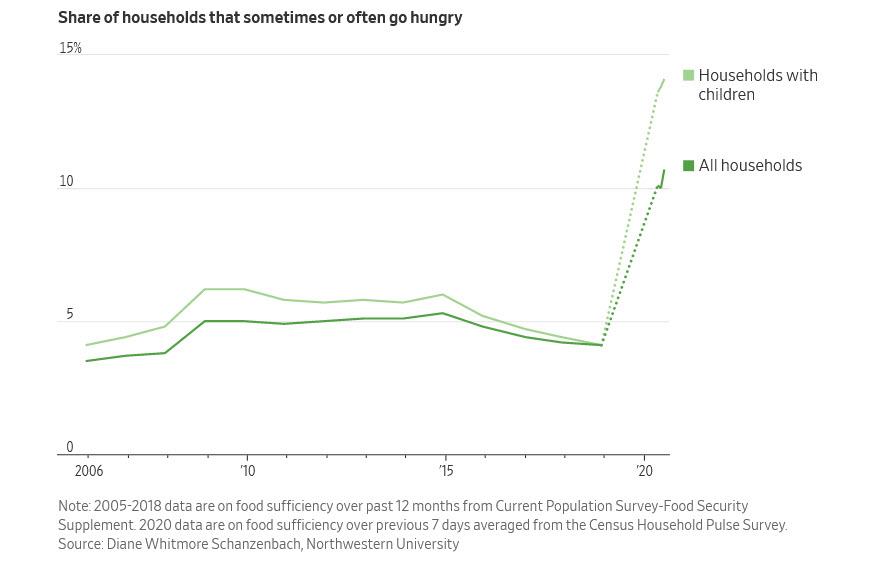

What, however, makes the current episode of surging food prices even worse is that it comes in the aftermath of the global covid shock, which has had a crushing impact on the well-being of hundreds of millions of people around the globe. In fact, as the WSJ reports, surging food prices is not just an EM issue.

Edwards summarizes his concerns best with the following statement: "even in the richest country in the world, food poverty has become a real problem during this pandemic."

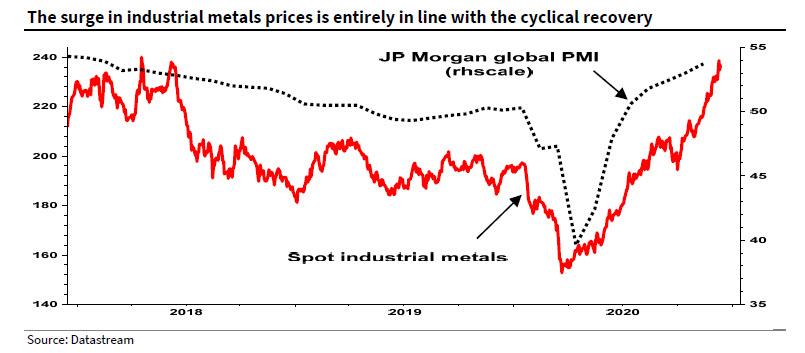

But wait, because the real inflation may be just starting, and it has to do with the "beautiful reflation" trade that everyone is convinced is coming. As Edwards notes, "now that a vaccine has arrived, investors are revelling in the cyclical beneficiaries of policy stimulus such as equity markets overall, value stocks, a steepening yield curve, and industrial metals. Certainly, the latter has risen entirely in line with the recovery in the global PMI."

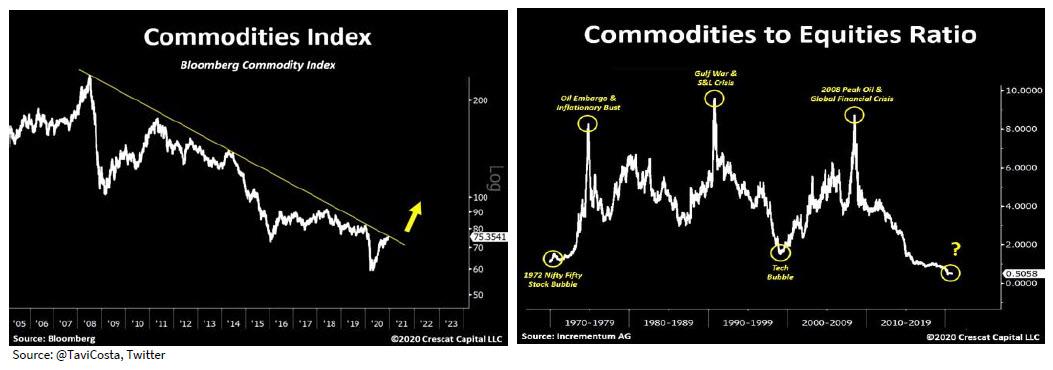

One sector that would certainly benefit from the return of inflation is commodities (such as food). As we showed earlier this week, while commodities have been in a secular bear market for a long while now, the following charts from Crescat Capital suggest that we could be in for a powerful reversal. Edwards agrees, noting that he "and many others believe that the end of the Ice Age and transition to the Great Melt will be extremely beneficial for commodities."

And as industrial commodities break upwards fuelled by the double-whammy of a cyclical recovery and extremely loose monetary policies worldwide, Edwards urges us to "keep a very close eye as to whether we see a repeat of the 2010/11 surge in food prices" because "on the 10th anniversary of the start of the Arab Spring, and with poverty having already been made much worse by the pandemic, another food price bubble could well be the straw to break the very angry camel’s back."

Uncategorized

Homes listed for sale in early June sell for $7,700 more

New Zillow research suggests the spring home shopping season may see a second wave this summer if mortgage rates fall

The post Homes listed for sale in…

Share this:

- A Zillow analysis of 2023 home sales finds homes listed in the first two weeks of June sold for 2.3% more.

- The best time to list a home for sale is a month later than it was in 2019, likely driven by mortgage rates.

- The best time to list can be as early as the second half of February in San Francisco, and as late as the first half of July in New York and Philadelphia.

Spring home sellers looking to maximize their sale price may want to wait it out and list their home for sale in the first half of June. A new Zillow® analysis of 2023 sales found that homes listed in the first two weeks of June sold for 2.3% more, a $7,700 boost on a typical U.S. home.

The best time to list consistently had been early May in the years leading up to the pandemic. The shift to June suggests mortgage rates are strongly influencing demand on top of the usual seasonality that brings buyers to the market in the spring. This home-shopping season is poised to follow a similar pattern as that in 2023, with the potential for a second wave if the Federal Reserve lowers interest rates midyear or later.

The 2.3% sale price premium registered last June followed the first spring in more than 15 years with mortgage rates over 6% on a 30-year fixed-rate loan. The high rates put home buyers on the back foot, and as rates continued upward through May, they were still reassessing and less likely to bid boldly. In June, however, rates pulled back a little from 6.79% to 6.67%, which likely presented an opportunity for determined buyers heading into summer. More buyers understood their market position and could afford to transact, boosting competition and sale prices.

The old logic was that sellers could earn a premium by listing in late spring, when search activity hit its peak. Now, with persistently low inventory, mortgage rate fluctuations make their own seasonality. First-time home buyers who are on the edge of qualifying for a home loan may dip in and out of the market, depending on what’s happening with rates. It is almost certain the Federal Reserve will push back any interest-rate cuts to mid-2024 at the earliest. If mortgage rates follow, that could bring another surge of buyers later this year.

Mortgage rates have been impacting affordability and sale prices since they began rising rapidly two years ago. In 2022, sellers nationwide saw the highest sale premium when they listed their home in late March, right before rates barreled past 5% and continued climbing.

Zillow’s research finds the best time to list can vary widely by metropolitan area. In 2023, it was as early as the second half of February in San Francisco, and as late as the first half of July in New York. Thirty of the top 35 largest metro areas saw for-sale listings command the highest sale prices between May and early July last year.

Zillow also found a wide range in the sale price premiums associated with homes listed during those peak periods. At the hottest time of the year in San Jose, homes sold for 5.5% more, a $88,000 boost on a typical home. Meanwhile, homes in San Antonio sold for 1.9% more during that same time period.

| Metropolitan Area | Best Time to List | Price Premium | Dollar Boost |

| United States | First half of June | 2.3% | $7,700 |

| New York, NY | First half of July | 2.4% | $15,500 |

| Los Angeles, CA | First half of May | 4.1% | $39,300 |

| Chicago, IL | First half of June | 2.8% | $8,800 |

| Dallas, TX | First half of June | 2.5% | $9,200 |

| Houston, TX | Second half of April | 2.0% | $6,200 |

| Washington, DC | Second half of June | 2.2% | $12,700 |

| Philadelphia, PA | First half of July | 2.4% | $8,200 |

| Miami, FL | First half of June | 2.3% | $12,900 |

| Atlanta, GA | Second half of June | 2.3% | $8,700 |

| Boston, MA | Second half of May | 3.5% | $23,600 |

| Phoenix, AZ | First half of June | 3.2% | $14,700 |

| San Francisco, CA | Second half of February | 4.2% | $50,300 |

| Riverside, CA | First half of May | 2.7% | $15,600 |

| Detroit, MI | First half of July | 3.3% | $7,900 |

| Seattle, WA | First half of June | 4.3% | $31,500 |

| Minneapolis, MN | Second half of May | 3.7% | $13,400 |

| San Diego, CA | Second half of April | 3.1% | $29,600 |

| Tampa, FL | Second half of June | 2.1% | $8,000 |

| Denver, CO | Second half of May | 2.9% | $16,900 |

| Baltimore, MD | First half of July | 2.2% | $8,200 |

| St. Louis, MO | First half of June | 2.9% | $7,000 |

| Orlando, FL | First half of June | 2.2% | $8,700 |

| Charlotte, NC | Second half of May | 3.0% | $11,000 |

| San Antonio, TX | First half of June | 1.9% | $5,400 |

| Portland, OR | Second half of April | 2.6% | $14,300 |

| Sacramento, CA | First half of June | 3.2% | $17,900 |

| Pittsburgh, PA | Second half of June | 2.3% | $4,700 |

| Cincinnati, OH | Second half of April | 2.7% | $7,500 |

| Austin, TX | Second half of May | 2.8% | $12,600 |

| Las Vegas, NV | First half of June | 3.4% | $14,600 |

| Kansas City, MO | Second half of May | 2.5% | $7,300 |

| Columbus, OH | Second half of June | 3.3% | $10,400 |

| Indianapolis, IN | First half of July | 3.0% | $8,100 |

| Cleveland, OH | First half of July | 3.4% | $7,400 |

| San Jose, CA | First half of June | 5.5% | $88,400 |

The post Homes listed for sale in early June sell for $7,700 more appeared first on Zillow Research.

federal reserve pandemic home sales mortgage rates interest ratesGovernment

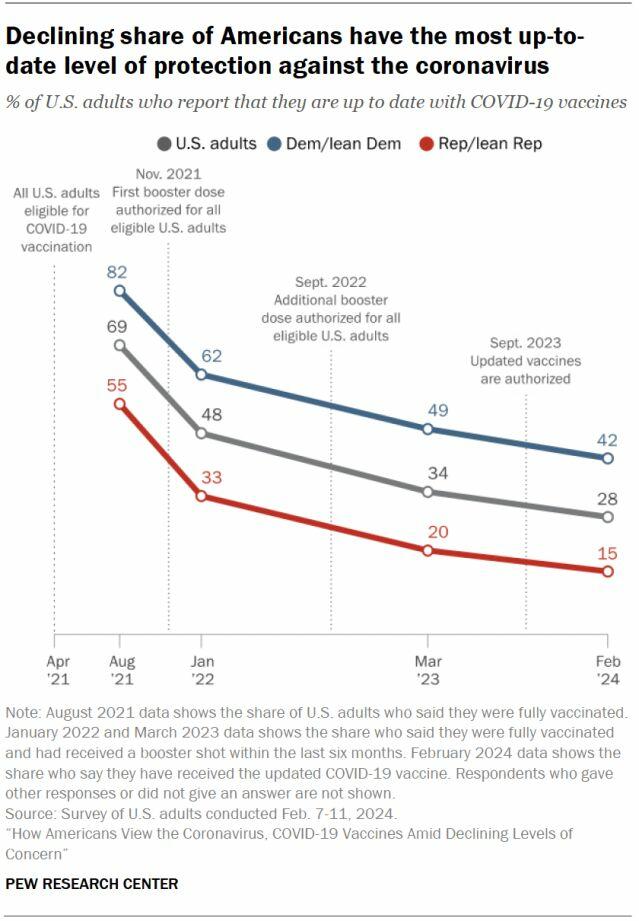

Survey Shows Declining Concerns Among Americans About COVID-19

Survey Shows Declining Concerns Among Americans About COVID-19

A new survey reveals that only 20% of Americans view covid-19 as "a major threat"…

Share this:

A new survey reveals that only 20% of Americans view covid-19 as "a major threat" to the health of the US population - a sharp decline from a high of 67% in July 2020.

What's more, the Pew Research Center survey conducted from Feb. 7 to Feb. 11 showed that just 10% of Americans are concerned that they will catch the disease and require hospitalization.

"This data represents a low ebb of public concern about the virus that reached its height in the summer and fall of 2020, when as many as two-thirds of Americans viewed COVID-19 as a major threat to public health," reads the report, which was published March 7.

According to the survey, half of the participants understand the significance of researchers and healthcare providers in understanding and treating long COVID - however 27% of participants consider this issue less important, while 22% of Americans are unaware of long COVID.

What's more, while Democrats were far more worried than Republicans in the past, that gap has narrowed significantly.

"In the pandemic’s first year, Democrats were routinely about 40 points more likely than Republicans to view the coronavirus as a major threat to the health of the U.S. population. This gap has waned as overall levels of concern have fallen," reads the report.

More via the Epoch Times;

The survey found that three in ten Democrats under 50 have received an updated COVID-19 vaccine, compared with 66 percent of Democrats ages 65 and older.

Moreover, 66 percent of Democrats ages 65 and older have received the updated COVID-19 vaccine, while only 24 percent of Republicans ages 65 and older have done so.

“This 42-point partisan gap is much wider now than at other points since the start of the outbreak. For instance, in August 2021, 93 percent of older Democrats and 78 percent of older Republicans said they had received all the shots needed to be fully vaccinated (a 15-point gap),” it noted.

COVID-19 No Longer an Emergency

The U.S. Centers for Disease Control and Prevention (CDC) recently issued its updated recommendations for the virus, which no longer require people to stay home for five days after testing positive for COVID-19.

The updated guidance recommends that people who contracted a respiratory virus stay home, and they can resume normal activities when their symptoms improve overall and their fever subsides for 24 hours without medication.

“We still must use the commonsense solutions we know work to protect ourselves and others from serious illness from respiratory viruses, this includes vaccination, treatment, and staying home when we get sick,” CDC director Dr. Mandy Cohen said in a statement.

The CDC said that while the virus remains a threat, it is now less likely to cause severe illness because of widespread immunity and improved tools to prevent and treat the disease.

“Importantly, states and countries that have already adjusted recommended isolation times have not seen increased hospitalizations or deaths related to COVID-19,” it stated.

The federal government suspended its free at-home COVID-19 test program on March 8, according to a website set up by the government, following a decrease in COVID-19-related hospitalizations.

According to the CDC, hospitalization rates for COVID-19 and influenza diseases remain “elevated” but are decreasing in some parts of the United States.

Government

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Rand Paul Teases Senate GOP Leader Run – Musk Says "I Would Support"

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump…

Share this:

{kind=link}

Republican Kentucky Senator Rand Paul on Friday hinted that he may jump into the race to become the next Senate GOP leader, and Elon Musk was quick to support the idea. Republicans must find a successor for periodically malfunctioning Mitch McConnell, who recently announced he'll step down in November, though intending to keep his Senate seat until his term ends in January 2027, when he'd be within weeks of turning 86.

So far, the announced field consists of two quintessential establishment types: John Cornyn of Texas and John Thune of South Dakota. While John Barrasso's name had been thrown around as one of "The Three Johns" considered top contenders, the Wyoming senator on Tuesday said he'll instead seek the number two slot as party whip.

Paul used X to tease his potential bid for the position which -- if the GOP takes back the upper chamber in November -- could graduate from Minority Leader to Majority Leader. He started by telling his 5.1 million followers he'd had lots of people asking him about his interest in running...

Thousands of people have been asking if I'd run for Senate leadership...

— Rand Paul (@RandPaul) March 8, 2024

...then followed up with a poll in which he predictably annihilated Cornyn and Thune, taking a 96% share as of Friday night, with the other two below 2% each.

????????️VOTE NOW ????️ ???? Who would you like to be the next Senate leader?

— Rand Paul (@RandPaul) March 8, 2024

Elon Musk was quick to back the idea of Paul as GOP leader, while daring Cornyn and Thune to follow Paul's lead by throwing their names out for consideration by the Twitter-verse X-verse.

I would support Rand Paul and suspect that other candidates will not actually run polls out of concern for the results, but let’s see if they will!

— Elon Musk (@elonmusk) March 8, 2024

Paul has been a stalwart opponent of security-state mass surveillance, foreign interventionism -- to include shoveling billions of dollars into the proxy war in Ukraine -- and out-of-control spending in general. He demonstrated the latter passion on the Senate floor this week as he ridiculed the latest kick-the-can spending package:

This bill is an insult to the American people. The earmarks are all the wasteful spending that you could ever hope to see, and it should be defeated. Read more: https://t.co/Jt8K5iucA4 pic.twitter.com/I5okd4QgDg

— Senator Rand Paul (@SenRandPaul) March 8, 2024

In February, Paul used Senate rules to force his colleagues into a grueling Super Bowl weekend of votes, as he worked to derail a $95 billion foreign aid bill. "I think we should stay here as long as it takes,” said Paul. “If it takes a week or a month, I’ll force them to stay here to discuss why they think the border of Ukraine is more important than the US border.”

Don't expect a Majority Leader Paul to ditch the filibuster -- he's been a hardy user of the legislative delay tactic. In 2013, he spoke for 13 hours to fight the nomination of John Brennan as CIA director. In 2015, he orated for 10-and-a-half-hours to oppose extension of the Patriot Act.

{kind=link}

Among the general public, Paul is probably best known as Capitol Hill's chief tormentor of Dr. Anthony Fauci, who was director of the National Institute of Allergy and Infectious Disease during the Covid-19 pandemic. Paul says the evidence indicates the virus emerged from China's Wuhan Institute of Virology. He's accused Fauci and other members of the US government public health apparatus of evading questions about their funding of the Chinese lab's "gain of function" research, which takes natural viruses and morphs them into something more dangerous. Paul has pointedly said that Fauci committed perjury in congressional hearings and that he belongs in jail "without question."

Musk is neither the only nor the first noteworthy figure to back Paul for party leader. Just hours after McConnell announced his upcoming step-down from leadership, independent 2024 presidential candidate Robert F. Kennedy, Jr voiced his support:

Mitch McConnell, who has served in the Senate for almost 40 years, announced he'll step down this November.

— Robert F. Kennedy Jr (@RobertKennedyJr) February 28, 2024

Part of public service is about knowing when to usher in a new generation. It’s time to promote leaders in Washington, DC who won’t kowtow to the military contractors or…

In a testament to the extent to which the establishment recoils at the libertarian-minded Paul, mainstream media outlets -- which have been quick to report on other developments in the majority leader race -- pretended not to notice that Paul had signaled his interest in the job. More than 24 hours after Paul's test-the-waters tweet-fest began, not a single major outlet had brought it to the attention of their audience.

That may be his strongest endorsement yet.

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

The Coming Of The Police State In America

‘I couldn’t stand the pain’: the Turkish holiday resort that’s become an emergency dental centre for Britons who can’t get treated at home

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

February Employment Situation

Low Iron Levels In Blood Could Trigger Long COVID: Study

Rand Paul Teases Senate GOP Leader Run – Musk Says “I Would Support”

Walmart has really good news for shoppers (and Joe Biden)

Another beloved brewery files Chapter 11 bankruptcy

Walmart joins Costco in sharing key pricing news

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International3 days ago

International3 days agoWalmart launches clever answer to Target’s new membership program

-

International3 days ago

International3 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex