Government

US Futures Stabilize After Rollercoaster Session As Yuan, Chinese Stocks Crater

US Futures Stabilize After Rollercoaster Session As Yuan, Chinese Stocks Crater

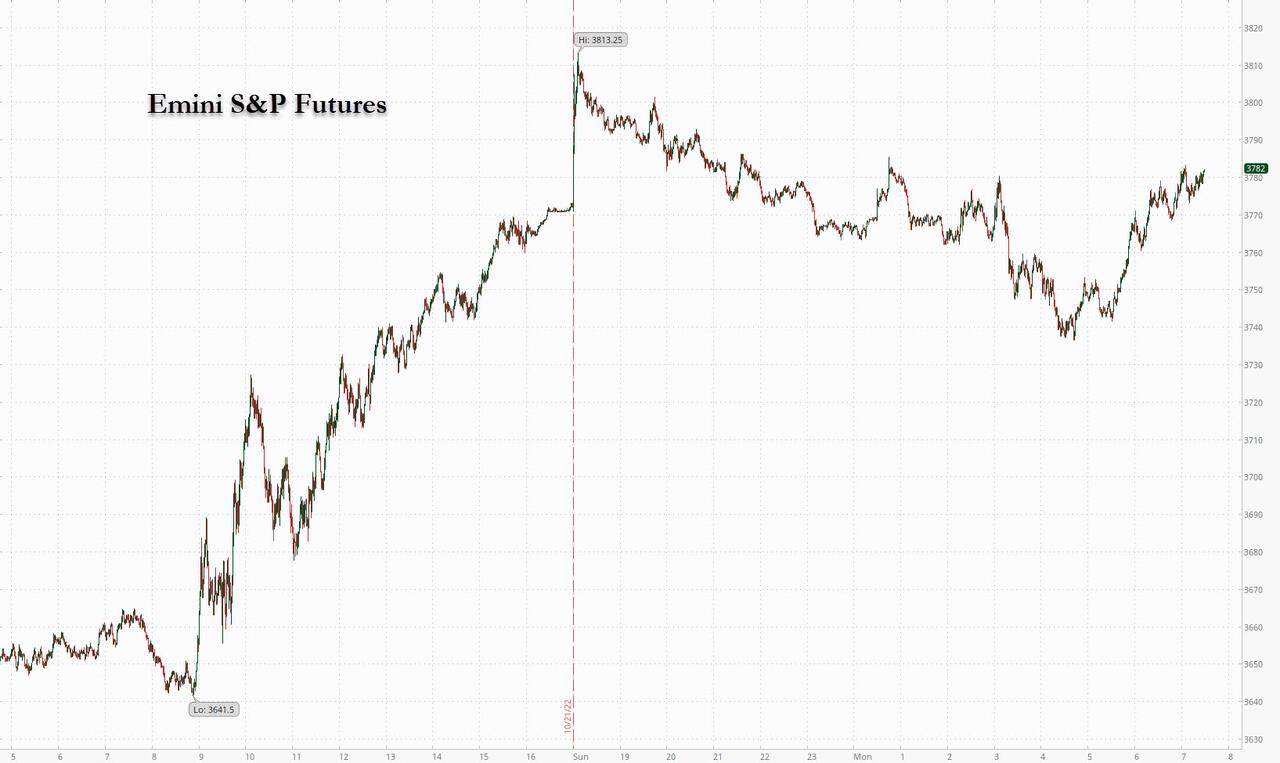

US stock futures steadied following a rollercoaster move earlier…

Share this:

US stock futures steadied following a rollercoaster move earlier in the session and after Friday’s sharp rally as traders assessed moves by Chinese President Xi Jinping to tighten his grip on the nation’s leadership while keeping an eye on macro data now that the Fed is in a chatterbox blackout. Contracts on the S&P 500 edged 0.7% higher at 7:30a.m. in New York after earlier rising as much as 1.3% and dropping 0.7%, while the yield on the 10-year Treasury slipped for a second session. Nasdaq 100 futures were up 0.4% after bouncing between gains and losses earlier. Both underlying gauges are coming off their best week since June, and are entering the busiest week of the earnings season with 46% of the S&P 500’s market cap due to announce third-quarter results.

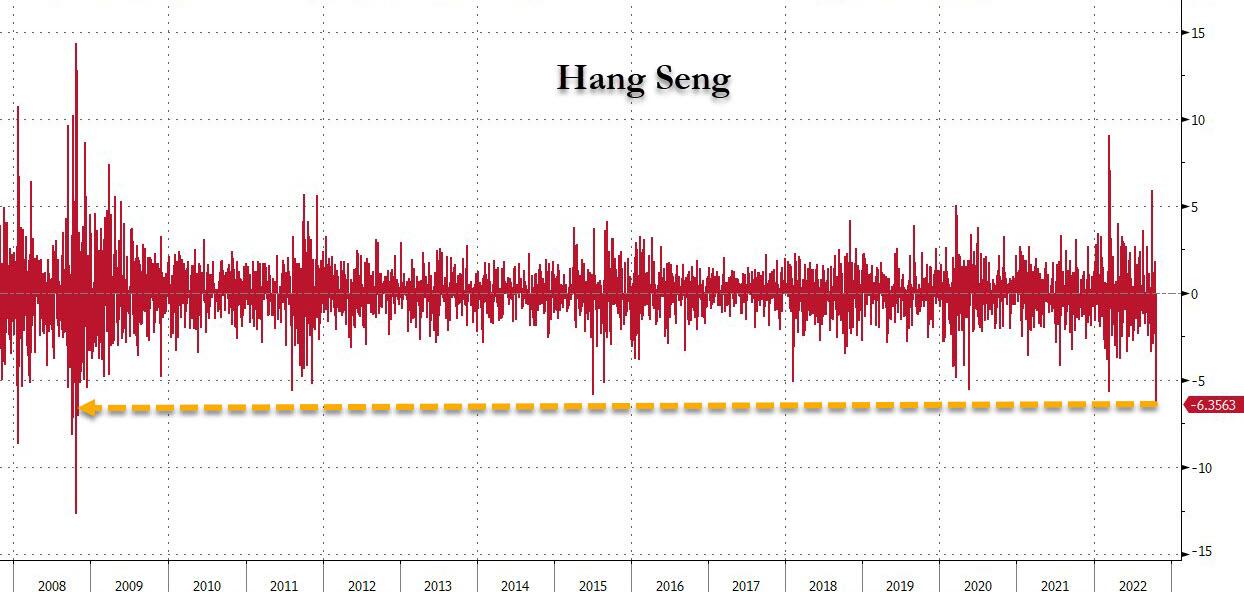

A gauge of the dollar’s strength rose sharply unwinding some of Friday's losses, supported by a risk-off mood sparked by a rout across Chinese markets which saw the Hang Seng plunge 6.4%, the biggest one day drop since 2008!

The offshore yen resumed its decline, tumbling by 1.3% - the biggest one-day slide since August 20019, to a record of 7.31, while the pound outperformed on bets for fiscal caution from the next UK prime minister.

“Market sentiment could remain cautious near-term on China, on concerns of a shift of focus toward more state control versus a market-driven approach under the new leadership team,” said Xiaojia Zhi, the chief China economist at Credit Agricole CIB. “The exit path from zero-Covid is not yet clear.”

Chinese economic data that was delayed last week and published Monday showed a mixed recovery, with unemployment rising and retail sales weakening despite a pickup in growth. Yet Xi’s Covid-zero campaign looks likely to continue to drag on the economy and there has been speculation that his “common prosperity” goal may even lead to property and inheritance taxes.

“It’s clear demand is slowing but so far we’ve seen pockets of tech like software, cloud computing still being quite resilient,” said Laura Cooper, a senior investment strategist at BlackRock International Ltd., on Bloomberg TV. “We will be watching for any signs of cracks coming through that could put a dent to some of these earnings expectations.”

In premarket trading, US-listed Chinese stocks tumbled, dragged lower by major internet and EV names including Alibaba, Baidu and Li Auto, which closed down more than 11%; search company Baidu was 12% lower while food delivery firm Meituan tanked more than 14%. The moves come after Chinese President Xi Jinping paved the way for an unprecedented third term as leader and packed the Politburo standing committee with loyalists. Tesla shares dropped after the company cut prices in China, reversing hikes imposed earlier this year.US stock futures steadied after Friday’s rally as traders assessed moves by Chinese President Xi Jinping to tighten his grip on the nation’s leadership. Other notable premarket movers:

- US-listed Macau casino stocks are also down, declining along with Chinese ADRs. Las Vegas Sands (LVS US) -7.9%, Wynn Resorts (WYNN US) -6.8%, Melco Resorts (MLCO US) -8.6%

- FedEx (FDX US) declines 1.9% in premarket trading after it was cut to equal-weight from overweight at Wells Fargo on concern that the revenue implications are not yet “fully captured” as the company pivots from growth and toward efficiency.

- Keep an eye on Williams-Sonoma (WSM US) stock as it was downgraded to underperform from hold at Jefferies, with broker saying it sees the home furnishing store operator underperforming ahead of a softer macroeconomic environment.

- Watch NXP Semiconductors (NXPI US) and Analog Devices (ADI US) shares as they were downgraded at Barclays, with the brokerage saying it expects cuts in the analog chip sector in the coming year and recommended “rotating out of the sub-sector sooner rather than later.”

US investors have begun looking beyond the Federal Reserve’s ongoing tightening to a stage when it may begin to slow rate hikes. St. Louis Fed President James Bullard and his San Francisco counterpart Mary Daly made it clear they expect discussion at the November meeting to include debate on how high to raise rates and when to ease the pace.

At the same time, Morgan Stanley’s Michael Wilson expects stocks to grind higher as markets transition to expectations of falling inflation and lower interest rates. The strategist, who correctly predicted this year’s slump, sees the S&P 500 Index bouncing as much as 15% if it breaches its 200-week moving average of 3,605 points, about 4% below Friday’s close. A similar view is held by Stifel Nicolaus & Co. strategists, who said in a separate note they see the benchmark rallying to 4,300 points in the next 6 months.

"With the back end of the bond market offering real value for the first time since early 2021, rates are poised to come in," Wilson in a note on Monday. “Such a move could provide the necessary fuel for the next leg of the tactical rally in stocks until we get full capitulation on 2023 earnings estimates, something we think may take a few more months.”

By contrast, Goldman Sachs Inc. strategists led by David Kostin are more cautious, seeing rising rates and slowing US growth hurting cyclicals and tech stocks. They recommend being overweight defensive sectors, as well as energy.

In Europe, the Stoxx Europe 600 Index held an advance of about 1.3%. Media, utilities and travel are the strongest-performing sectors in Europe while miners and energy lag. IBEX outperforms peers, adding 0.9%, FTSE 100 lags, dropping 0.4% after Boris Johnson pulled out of the race to lead the UK’s ruling Conservative Party, placing Rishi Sunak closer to becoming the next prime minister. A 12% slump in Prosus NV shares amid the China concerns pushed the technology sector into the red, while basic resources and energy stocks weighed on the benchmark amid lower commodity prices. Michelin shares rose as much as 3.7% in Paris trading and are the day’s top performers on the Stoxx 600 Automobiles & Parts Index, with the French tiremaker set to give a quarterly sales update on Tuesday. Here are the biggest European movers:

- Pearson shares jump as much as 7.8%, reaching the highest since January 2019, after the publishing and education company reported a 7% increase in underlying revenue in the first nine months of the year.

- Indivior gains as much as 7.6%, the most since February, after Morgan Stanley upgrades to overweight from equal-weight, describing the stock as a “value, growth and margin expansion story.”

- Auto Trader rises as much as 4.3% after announcing the disposal of Webzone Ltd. Peel Hunt upgrades to buy from hold, saying the sale shows the company’s “dedication to its key market.”

- Temenos climbs as much as 8.2%, the most intraday since mid-June, after Dealreporter reported that Goldman Sachs and Citi are sounding out interest in the buyout of the Swiss banking software developer.

- Prosus falls as much as 14% in Amsterdam and parent Naspers sinks as much as 14% in Johannesburg, with both declines the sharpest since March. Naspers holds a 28% stake in Tencent, which plunged in Hong Kong trading following President Xi Jinping’s move to stack his leadership ranks with loyalists.

- Galp drops as much as 6.1% after reporting third-quarter profit that missed the average analyst estimate.

- Philips falls as much as 4.5% to the lowest since 2011 after saying it would cut 4,000 jobs as part of a EU300 million cost-saving package, which analysts say may imply liquidity problems for the Dutch medical technology firm.

Asian stocks fell, dragged by Chinese shares as President Xi Jinping’s move to tighten his leadership deepened investor worries, offsetting advances in Australia, South Korea and Japan. The MSCI Asia Pacific Index erased an earlier gain to drop as much as 1.2%, with Internet giants Tencent and Alibaba the biggest drags. A selloff in Chinese stocks deepened in afternoon trading, as the Hang Seng plunged by more than 6%, its biggest drop since Lehman while the Hang Seng Tech Index crashed 9.7% to the lowest since February 2016, after Xi filled China’s most powerful bodies with close allies while securing a precedent-breaking third term. He installed six trusted associates alongside him on the Politburo’s supreme Standing Committee and put his former chief of staff Li Qiang in line for the premiership.

Investors remained jittery as a leadership reshuffle highlighted Xi’s unquestioned grip over the ruling party, with allies set to take up key economic posts. An early loosening of Covid restrictions seemed less likely, while a set of long-delayed economic data showed a mixed recovery, further damping market sentiment.

“The latest rally underlines our view that markets will remain volatile, and investors should prepare for large moves in both directions,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “Incremental improvements in inflation or labor market data, indications of economic resilience, any softening of language from the Fed, has the potential to drive a market bounce, as we have seen in recent days.”

“Markets may be hoping now that the leadership transition is finalized, the focus will turn to the economy and mending the property sector,” said Marvin Chen, a strategist at Bloomberg Intelligence, adding that property investment is still a weak spot for the economy. “Still, these may take time. We may not see much change to Covid policies in the near term.” The declines in Chinese shares contrasted with the upbeat mood elsewhere in Asia, buoyed by declines in US Treasury yields and Federal Reserve officials’ indications of a potential slowing of rate hikes. Markets were closed for holidays in Singapore, India, Malaysia, Thailand and New Zealand

In FX, the Bloomberg Dollar Spot Index rose, paring some of Friday’s losses and the greenback was steady or higher against all of its Group-of-10 peers.

- The pound jumped and gilts led Treasuries and European bonds higher as investors bet that Rishi Sunak would bring more stability to the country’s financial markets. Initial moves were however tempered, and the pound inched lower, sliding back under 1.13 after earlier rallying by as much as 0.9% to $1.1409.

- China’s offshore yuan led the decline in most emerging Asian currencies as traders assessed the impact of President Xi Jinping’s consolidation of power. Indonesia’s rupiah outperformed peers, supported by higher nickel prices. China’s onshore yuan weakened to a 14-year low while stocks headed for their biggest daily plunge in Hong Kong since the 2008 global financial crisis. Market setbacks following the reshuffle highlighted President Xi Jinping’s unquestioned grip over the ruling party and showed deep disappointment over a likely continuation of policies staked on Covid Zero and state- driven companies.

- The euro retreated after earlier rising to more than a two-week high of $0.9899. Eurozone composite PMI fell to 47.1 in October; economists had expected 47.6

- The yen fell by more than 1%, to trade above 149 per dollar, after earlier surging to as much as 145.56 after suspected interventions by Japanese authorities

- Australian dollar declined against all of its G-10 peers after the Reserve Bank said it isn’t yet worried about the risk of imported inflation from a falling currency. Reports of fresh Covid restrictions in Guangzhou helped fuel a drop in China stocks and the yuan, pushing the Aussie even lower

In rates, Treasuries trade off best levels of the session, although intermediate and long-end yields remain richer by 5bp-6bp. Gilts lead a global bond market rally, with front-end yields down nearly 40bp after Rishi Sunak emerged as the frontrunner to become new UK Prime Minister. 10-year TSY yields trade around 4.15%, richer by ~7bp on the day, trailing gilts by 18bp, bunds by 4bp in the sector; US 2s10s is ~5bp flatter on the day while gilt curve steepens. Treasuries extended their late-Friday rally during Monday’s Asia session, adding to a move sparked by comments from Fed’s Daly, who said policy makers should start planning for a reduction in the size of interest-rate increases, and a WSJ article predicting they will debate the size of future hikes in November. According to Bloomberg, dollar issuance slate includes OKB $1b 3Y and Cades 3Y; $20b of new bond sales are expected this week as companies emerge from earnings blackout periods; banks including JPMorgan Chase & Co., Citigroup Inc., Goldman Sachs Group Inc. and Bank of America Corp. could all come to market soon.

Commodities were clipped as the USD rebounded and recessionary concerns mount (again); crude benchmarks are hampered on such factors, though similarly to US equity futures have recently eased off lows. Specifically, WTI and Brent benchmarks post downside of circa. USD 1.00/bbl compared to losses just shy of USD 2.00/bbl at worst. Both precious and base metals are broadly speaking under pressure; currently, Gold is impaired by circa. USD 10/oz and has been pushed back below the 10-DMA at USD 1650/oz. QatarEnergy head said the Co. is open to discussing working with Shell (SHEL LN) in all energy sectors, via Reuters.

Looking at today's calendar, we get the US October PMIs, and September Chicago Fed national activity index, we also get PMI updates from Japan, UK, Germany, France and the Eurozone.

Market Snapshot

- S&P 500 futures up 0.7% to 3,792

- STOXX Europe 600 up 0.5% to 398.32

- MXAP down 1.1% to 134.36

- MXAPJ down 2.0% to 431.12

- Nikkei up 0.3% to 26,974.90

- Topix up 0.3% to 1,887.19

- Hang Seng Index down 6.4% to 15,180.69

- Shanghai Composite down 2.0% to 2,977.56

- Sensex up 0.2% to 59,307.15

- Australia S&P/ASX 200 up 1.5% to 6,779.36

- Kospi up 1.0% to 2,236.16

- German 10Y yield down 0.2% at 2.41%

- Euro down 0.3% to $0.9831

- Brent Futures down 1.8% to $91.86/bbl

- Gold spot down 0.6% to $1,647.67

- U.S. Dollar Index up 0.25% to 112.29

Top Overnight News from Bloomberg

- A sense of exasperation swept across Chinese markets as President Xi Jinping moved to stack his leadership ranks with loyalists, with stocks capping their worst day in Hong Kong since the 2008 global financial crisis and the yuan weakening to a 14-year low

- The ECB is priming another hefty hike in interest rates this week as the attention increasingly switches to how high it will eventually push

- Japan’s government will set out its expectation that the central bank watches the impact of moves in financial markets while emphasizing the two sides’ cooperation on policy, according to a draft of an upcoming stimulus plan obtained by Bloomberg

- Most of Japan’s currency intervention, confirmed and suspected, took place outside of regular trading hours, with the exception of probable action Monday -- unlike moves in 2010 and 2011 to weaken the yen. In contrast to that period, the government has only stated it intervened once, with the reluctance to do so seen as an additional tool to deter speculators

- Much of continental Europe is poised for an unusually warm end to the month, with Paris seeing temperatures more common on a summer day than well into the heating season

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacififc stocks traded mixed after the initial optimism from Wall Street on Friday began to fade. ASX 200 was boosted by its commodities sector as the rise in underlying metals supported mining names in the region. Nikkei 225 was also firmer but lagged behind peers (ex-China) following the touted FX intervention on Friday and again on Monday. KOSPI was led by gains in its IT names, but the region felt some jitters following an exchange of fire between North and South Korea after a North Korean boat crossed the South Korean maritime border. Shanghai Comp. initially traded flat after Chinese President Xi secured an unprecedented third term as the party leader, as expected. Chinese President Xi also suggested China's economy has high resilience and sufficient potential. The index also saw some brief upside after China released a myriad of delayed economic data, with Q3 GDP Y/Y topping forecasts and Trade Balance printing a larger surplus than expected, whilst exports also increased more than forecast, although these gains pared back. Hang Seng buckled as Xi’s leadership overhaul could prove to result in prolonged oversight and less autonomy for Hong Kong, with the Hang Seng Tech Index slumping over 5% and Alibaba, Tencent, JD.com, Baidu and Meituan shedding as much as 7-10%.

Asia Data Recap

- Chinese GDP (Q3) Y/Y 3.9% (Exp. 3.3%, Prev. 0.4%); Q/Q 3.9% (Exp. 3.5%, Prev. -2.6%)

- Chinese Trade Balance (Sep) (USD) Y/Y 84.7bln (Exp. 80.3bln, Prev. 79.39B); Exports +5.7% (Exp. +4.0%, Prev. 7.1%), Imports +0.3% (Exp. 1.0%, Prev. 0.3%)

- Chinese Retail Sales (Sep) Y/Y 2.5% (Exp. 3.0%, Prev. 5.4%); YTD Y/Y 0.7% (Exp. 0.9%, Prev. 0.5%)

- Chinese Industrial Output (Sep) Y/Y 6.3% (Exp. 4.8%, Prev. 4.2%); YTD Y/Y 3.9% (Exp. 3.7%, Prev. 3.6%)

- Chinese Fixed Investments (Jan-Sep) 5.9% (Exp. 6.0%)

- Australian Composite PMI (Oct) 49.6 (Prev. 50.9); Services PMI (Oct) 49.0 (Prev. 50.6); Manufacturing PMI (Oct) 52.8 (Prev. 53.5)

- Japanese Jibun Manufacturing PMI (Oct) 50.7 (Prev. 50.8); Services PMI (Oct) 53.0 (Prev. 52.2); Composite PMI (Oct) 51.7 (Prev. 51.0)

Top Asian News

- China suspended in-person schooling and dining-in at restaurants in a district in Guangzhou, "stoking concerns about the potential for disruption in the southern Chinese manufacturing hub that’s home to about 19mln people", Bloomberg reported.

- PBoC injected CNY 10bln via 7-day reverse repos at a maintained rate 2.00% for a daily injection of CNY 8bln.

- Japan's Top Currency Diplomat Kanda will not comment on whether they intervened in FX markets and said there is no change in stance that "we are ready to take action 24/7" and will continue to take appropriate action, via Reuters. Japan's Top Currency Diplomat Kanda offered no comments on intervention on Monday morning.

- Japanese Finance Minister Suzuki said no comment on FX intervention; currently trying to confront speculators; monitoring FX with a high sense of urgency.

- USD/JPY drop on Monday likely due to intervention, according to market participants cited by Reuters.

- Japanese government urges the BoJ to remain vigilant to the impact of sharp market moves, according to a draft document cited by Reuters.

- The Japanese government and the BoJ decided to intervene in FX on Friday by buying the Yen and selling the Dollar, according to Nikkei sources citing sources.

- Japan's FX intervention on October 21st is estimated at JPY 5.4-5.5tln, according to market sources and calculations cited by Reuters.

- BoJ Governor Kuroda said CPI growth beyond next FY likely to fall below 2%, will continue to put all effort into achieving price target along with rise in wages.

- Japanese gov't expects the BoJ to watch the impact of market moves, via Bloomberg citing a document; to collaborate closely with the BoJ on the policy mix; Finance Minister will not comment on FX intervention.

- Japan is to ease rules in relation to brokerages offering investment advice, according to reports citing Nikkei.

- Japanese Economy Minister Yamagiwa is planning to step down, according to NHK.

- South Korea is to expand its corporate-bond buying program, according to the finance minister cited by Reuters.

- RBA's Kent reiterated the Board expects to increase interest rates further in the period ahead; size and timing of rate increases in Australia will depend on incoming data.

European bourses are mixed, though are well off lows, as initial strength faded following the open amid renewed USD strength and as PMIs flash ongoing recessionary/inflationary concerns. Sectors are a touch mixed amid the above action, Energy remains the standout laggard amid the complex's broader price action. US futures have managed to make their way back to being essentially unchanged on the session, as the initial bout of underperformance eases as US participants enter the fray pre-PMIs.

Top European News

- UK's Boris Johnson has pulled out of the Conservative Party leadership contest, according to The Times' Swinford. UK's Boris Johnson and Rishi Sunak failed to strike a deal in talks on Saturday, according to the Times.

- UK leadership candidate Rishi Sunak so far received support from 147 MPs vs 24 for Penny Mordaunt. The deadline to reach the 100 threshold is at 14:00BST/09:00EDT on Monday.

- UK leadership candidate Penny Mordaunt will stay in the race as she reportedly sees a route to 100 nominations now Boris Johnson is out, according to sources cited by Bloomberg's Wickham.

- UK Chancellor Hunt backs Rishi Sunak for PM, via The Telegraph.

- UK Chancellor Hunt is said to be mulling up to GBP 20bln of tax rises in the October 31st budget, according to The Telegraph. The October 31st fiscal statement could be delayed after PM Truss' resignation, according to the FT.

- UK Chancellor Hunt is expected to extend the current freeze in income tax and allowances into the next parliament, according to FT citing sources.

- BoE's Mann said bond purchases for financial stability were targeted and temporary, and the start of bond selling on Nov 1st shows the BoE does not feel like its hands are tied. Mann said it is the BoE's job to address financial stability risks.

- Moody's affirmed UK's rating at Aa3; revised outlook to "Negative" from "Stable.

FX

- Dollar regroups after Friday's reversal on less hawkish Fed dynamic and reports of Japanese intervention, DXY above 112.500 at best vs 111.760 low.

- Sterling underpinned ahead of deadline in race to be next UK PM with Sunak hot favourite to succeed, Cable holding within 1.1400-1.1300 range.

- Yen reverses from peaks as official buying momentum wanes, USD/JPY up to 149.70 from sub-145.50 at one stage.

- Aussie underperforms ahead of Budget that is expected to see growth forecast downgraded, AUD/USD under 0.6300 and Kiwi down in sympathy on NZ Labour Day as NZD/USD declines through 0.5700.

- Offshore Yuan below 7.3000 vs Buck as China tightens COVID restrictions in key southern manufacturing hub.

- Euro fades from a fraction below 0.9900 towards 0.9800 after broadly weak PMIs and amidst heavy option expiry interest.

- PBoC set USD/CNY mid-point at 7.1230 vs exp. 7.1173 (prev. 7.1186); weakest fix since June 1st 2020.

Commodities

- Commodities clipped as the USD regains poise and recessionary concerns mount; crude benchmarks are hampered on such factors, though similarly to US equity futures have recently eased off lows.

- Specifically, WTI and Brent benchmarks post downside of circa. USD 1.00/bbl compared to losses just shy of USD 2.00/bbl at worst.

- Both precious and base metals are broadly speaking under pressure; currently, Gold is impaired by circa. USD 10/oz and has been pushed back below the 10-DMA at USD 1650/oz.

- QatarEnergy head said the Co. is open to discussing working with Shell (SHEL LN) in all energy sectors, via Reuters.

- China sold 100% of wheat offered at auction of state reserves on Oct 19th, according to Reuters citing the traded centre; sold at an average price of CNY 2,829/t.

CCP National Congress

- Chinese President Xi secured an unprecedented third term as Chinese Communist Party (CCP) leader, as expected.

- The CCP amended its constitution to include "two establishes" and "two safeguards" to "cement" Xi Jinping's status as the core of the party, according to Reuters.

- Chinese President Xi is to head the communist party's central commission for discipline inspection, according to state media.

- The new CCP Politburo Standing Committee includes Li Qang, Li Xi, Ding Xuexiang, Cai Qi, Zhao Leji, Wang Huning, according to state media. The new Central Committee (comprising of 171 alternate members) does not include Liu He, Han Zheng, Sun Chunlan, Yi Gang, Guo Shuoing,

- Chinese President Xi said China's economy has high resilience, sufficient potential and has room for manoeuvre. Xi said China will open its doors even wider. Xi said China must ensure the CCP continues to be the backbone people can lean on, according to state media.

Geopolitics

- Russian Defence Minister held phone calls with the US Pentagon Chief, UK Defence Minister, and the French Armed Forces Minister, according to Interfax and Reuters.

- French Armed Forces Minister has confirmed Russian Defence Minister told him Russia fears that Ukraine may use a "dirty bomb" on Russian territory. Russia's Shoigu warns of 'uncontrolled escalation' in Ukraine conflict, via Reuters.

- Ukraine's Foreign Minister spoke with US Defence Secretary Blinken and said they both agreed the Russian rhetoric on "dirty bombs" is aimed at creating a pretext for a false flag operation. They also discussed further practical steps to boost Ukraine’s air defense.

- Russian forces continued to target Ukraine's energy and military infrastructure over the weekend, according to the Russia Defence Ministry cited by Interfax.

- Russian authorities said two pilots died in a military plane crash into a residential building in Irkutsk, Russia, according to Interfax.

- Russian Deputy Foreign Minister said Russia completely reject any demilitarized zones in the vicinity of the Zaporozhye station, Via Al Jazeera.

- Russia continues to use Iranian uncrewed aerial vehicles (UAVs) against targets throughout Ukraine, according to the UK Ministry of Defence.

US Event Calendar

- 08:30: Sept. Chicago Fed Nat Activity Index, est. -0.10, prior 0

- 09:45: Oct. S&P Global US Manufacturing PM, est. 51.0, prior 52.0

- 09:45: Oct. S&P Global US Composite PMI, est. 49.2, prior 49.5

- 09:45: Oct. S&P Global US Services PMI, est. 49.5, prior 49.3

DB's Jim Reid concludes the overnight wrap

Morning from the middle of a forest in Center Parcs. We’ve had a biblical amount of rain, flash flooding in the resort and a weekend of over excitable children. We’re off to a safari park today where monkeys jump on your car. Only 24 hours before I can escape on a plane to New York.

As we start a new week where we’re now in the Fed blackout period ahead of next week’s FOMC, we’re perhaps starting the 6th attempt this year at the Fed pivot trade. This only started on Friday as well-connected Nick Timiraos (WSJ) suggested that while a 75bps hike at the Fed’s next meeting was set to go ahead, officials were also likely to discuss “whether and how to signal plans to approve a smaller increase in December.” Whether this gets any further than the previous failed attempts to reprice markets only time will tell but with markets pricing in a terminal rate of over 5% prior to this, at least this is the first one that starts from anything vaguely resembling a realistic starting point given where inflation is. San Fran Fed President Daly also said on Friday that the Fed should start planning for a shift down in the pace of hikes but added that they are not there yet.

The news helped price -8.0bps less Fed tightening by year-end on Friday, whilst also triggering a significant one-day decline in the 2yr Treasury yield of -13.8bps (-16bps post Timiraos). In turn the S&P 500 completed its strongest weekly performance since June, advancing +4.74% (+2.37% Friday). Futures are +0.3% this morning. The longer end rallied 12bps off the highs but was only -1.2bps on Friday as the same article discussed how the Fed could also signal a higher dot plot for 2023. Net net this left the biggest curve steepening since the pandemic (-12.2bps) which given that its not a huge move shows how massively flatter the curve has been since then. This morning in Asia 2 and 10yr yields are -4.3bps and -6.7bps lower respectively and this continuing the momentum from Friday.

In the cold light of day (and it’s cold and dark in the forests of Center Parcs this morning), these more dovish stories are all plausible but between next week’s FOMC and the December equivalent we have CPI and NFP twice. So plenty of cold or hot water to flow under the bridge before then. On balance there are few signs at the moment that core inflation is about to see a rapid about turn and the Fed will be data dependent so it'll be impossible to have high conviction on what they do next without a strong view on the data.

Before we examine the week ahead we should note that overall the 10yr yield ended last week up by +19.8bps (-1.2bps Friday), which marked its 12th consecutive weekly rise, and is also its longest run since 1984 when Paul Volcker was Fed Chair. So we need to put things into some perspective.

In light of all this maybe the most interesting data this week comes on Friday with the Q3 employment cost index (DB at +1.1% vs. +1.3% last month) and the September personal income (+0.1% vs. +0.3%) and consumption (+0.3% vs. +0.4%) report, including the core PCE deflator (+0.58% vs. +0.56%). With respect to core PCE, our economists expect the Fed's preferred measure of inflation to rise by 40bps to 5.3%. Our economists highlight that as the median forecast for 2022 core PCE inflation in the Fed's Summary of Economic Projections from the September 21st meeting was 4.5%, it’s going to be tough to signal a downshift in December.

Elsewhere this week the main highlights are the ECB (Thursday) and the BoJ (Friday) decisions and a huge round of earnings with big Tech the highlight. We’ll also have a new UK Prime Minister by Friday with a possibility we may have one after today’s ultra compressed rounds of Parliamentary votes. After Boris Johnson pulled out late last night it is possible that only tactical voting will stop ex-Chancellor Sunak being declared PM tonight. We’ll also see US Q3 GDP (Thursday) and flash PMIs in the US and Europe (today) and October CPIs and GDP for many European countries (Friday). There are other data which are in the day by day guide at the end as usual for a Monday but let’s take a brief look at the highlights outside the already discussed PCE. The ECB's decision on Thursday will be a big event with our European economists expecting another +75bps hike (72.3bp priced in), followed by +75bps in December (c.62bps priced in), +50bps in February (c.38bps priced), and +25bps in March, reaching a terminal rate of 3%. The press conference as ever will be a focal point and there’ll be lots of attention on technical things surrounding TLTROs and excess reserves. For more on the options here see our fixed income strategists blog from Friday here.

Staying with central banks, over in Japan, the BoJ announces its decision on Friday amidst continued downward pressure on the yen, which hit a 32-year low against the dollar of 151.95 on Friday before surging again to end the week at 147.65 - c.3.5% swing while the Japanese slept after Nikkei reported fresh intervention from the Japanese authorities. The Yen has again seen a wild session in Asia. After falling again to 149.67 it surged to 145.65 and now trades at 148.88 as we go to press with no clarity on if and what intervention has been done.

For US Q3 GDP this week, our US economists expect real growth to rebound to +3.0% from Q2's -0.6%. Q3 GDP figures will also be out for European countries on Friday, including for Germany and France with the former likely to be slightly negative and the latter slightly positive. Overall it’s likely to be the start of growth grinding towards or below zero and then staying negative for a few quarters. On European CPI on Friday remember September readings saw Germany's CPI reaching 10% for the first time since 1950.

Earnings will come thick and fast this week, featuring the big tech, oil majors and key automakers and staples. In tech alone we have Microsoft, Alphabet (tomorrow), Meta (Wednesday) and Apple and Amazon (Thursday). A huge slug (20% by market cap) of the S&P 500 in 48 hours. Other notable tech firms reporting results will include Intel, Twitter, SAP and Samsung. The other main reporters are in the day by day week ahead at the end.

Asian markets are higher outside of China/HK this morning with the Nikkei (+0.62%) and the KOSPI (+0.87%) up but with the Hang Seng (-4.99%) and the Shanghai composite (-0.89%) lower as markets worry about the policy direction of travel after the ending of the 20th Party Congress. We've also finally seen the monthly data dump out of China and despite a beat on Q3 GDP (+3.9% vs +3.3% expected) and industrial production (+6.3% vs 4.8%), we saw weaker retail sales (+2.5% vs +3.0%) and jobless rate (5.5% vs 5.2%).

Looking back to last week, we've already discussed the US rates and equities pricing at the top. Over in Europe, gilts outperformed other sovereign bonds over the week as a whole thanks to the government’s Monday U-turn on the mini-budget. However, they became a major underperformer again on Friday as investors contemplated the likelihood that former Prime Minister Johnson could return to office. All-in-all that left 10yr yields down -28.2bps over the week (+14.1bps Friday), and after the close we heard that Moody’s had affirmed the UK’s credit rating but cut the outlook to negative. Elsewhere in Europe though there was a similar pattern to Treasuries, with 10yr bund yields also rising for a 12th week in a row with a +7.0bps gain over the week (+1.4bps Friday). At the same time, the STOXX 600 put in its best week since July, with a +1.27% advance (-0.62% Friday).

Finally last week, European natural gas futures fell -20.02% (-10.67% Friday) to €114 per megawatt-hour after EU leaders endorsed a plan to cap gas prices.

International

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

The struggling chain has given up the fight and will close hundreds of stores around the world.

Share this:

It has been a brutal period for several popular retailers. The fallout from the covid pandemic and a challenging economic environment have pushed numerous chains into bankruptcy with Tuesday Morning, Christmas Tree Shops, and Bed Bath & Beyond all moving from Chapter 11 to Chapter 7 bankruptcy liquidation.

In all three of those cases, the companies faced clear financial pressures that led to inventory problems and vendors demanding faster, or even upfront payment. That creates a sort of inevitability.

Related: Beloved retailer finds life after bankruptcy, new famous owner

When a retailer faces financial pressure it sets off a cycle where vendors become wary of selling them items. That leads to barren shelves and no ability for the chain to sell its way out of its financial problems.

Once that happens bankruptcy generally becomes the only option. Sometimes that means a Chapter 11 filing which gives the company a chance to negotiate with its creditors. In some cases, deals can be worked out where vendors extend longer terms or even forgive some debts, and banks offer an extension of loan terms.

In other cases, new funding can be secured which assuages vendor concerns or the company might be taken over by its vendors. Sometimes, as was the case with David's Bridal, a new owner steps in, adds new money, and makes deals with creditors in order to give the company a new lease on life.

It's rare that a retailer moves directly into Chapter 7 bankruptcy and decides to liquidate without trying to find a new source of funding.

Image source: Getty Images

The Body Shop has bad news for customers

The Body Shop has been in a very public fight for survival. Fears began when the company closed half of its locations in the United Kingdom. That was followed by a bankruptcy-style filing in Canada and an abrupt closure of its U.S. stores on March 4.

"The Canadian subsidiary of the global beauty and cosmetics brand announced it has started restructuring proceedings by filing a Notice of Intention (NOI) to Make a Proposal pursuant to the Bankruptcy and Insolvency Act (Canada). In the same release, the company said that, as of March 1, 2024, The Body Shop US Limited has ceased operations," Chain Store Age reported.

A message on the company's U.S. website shared a simple message that does not appear to be the entire story.

"We're currently undergoing planned maintenance, but don't worry we're due to be back online soon."

That same message is still on the company's website, but a new filing makes it clear that the site is not down for maintenance, it's down for good.

The Body Shop files for Chapter 7 bankruptcy

While the future appeared bleak for The Body Shop, fans of the brand held out hope that a savior would step in. That's not going to be the case.

The Body Shop filed for Chapter 7 bankruptcy in the United States.

"The US arm of the ethical cosmetics group has ceased trading at its 50 outlets. On Saturday (March 9), it filed for Chapter 7 insolvency, under which assets are sold off to clear debts, putting about 400 jobs at risk including those in a distribution center that still holds millions of dollars worth of stock," The Guardian reported.

After its closure in the United States, the survival of the brand remains very much in doubt. About half of the chain's stores in the United Kingdom remain open along with its Australian stores.

The future of those stores remains very much in doubt and the chain has shared that it needs new funding in order for them to continue operating.

The Body Shop did not respond to a request for comment from TheStreet.

bankruptcy pandemic canadaGovernment

Are Voters Recoiling Against Disorder?

Are Voters Recoiling Against Disorder?

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super…

Share this:

Authored by Michael Barone via The Epoch Times (emphasis ours),

The headlines coming out of the Super Tuesday primaries have got it right. Barring cataclysmic changes, Donald Trump and Joe Biden will be the Republican and Democratic nominees for president in 2024.

With Nikki Haley’s withdrawal, there will be no more significantly contested primaries or caucuses—the earliest both parties’ races have been over since something like the current primary-dominated system was put in place in 1972.

The primary results have spotlighted some of both nominees’ weaknesses.

Donald Trump lost high-income, high-educated constituencies, including the entire metro area—aka the Swamp. Many but by no means all Haley votes there were cast by Biden Democrats. Mr. Trump can’t afford to lose too many of the others in target states like Pennsylvania and Michigan.

Majorities and large minorities of voters in overwhelmingly Latino counties in Texas’s Rio Grande Valley and some in Houston voted against Joe Biden, and even more against Senate nominee Rep. Colin Allred (D-Texas).

Returns from Hispanic precincts in New Hampshire and Massachusetts show the same thing. Mr. Biden can’t afford to lose too many Latino votes in target states like Arizona and Georgia.

When Mr. Trump rode down that escalator in 2015, commentators assumed he’d repel Latinos. Instead, Latino voters nationally, and especially the closest eyewitnesses of Biden’s open-border policy, have been trending heavily Republican.

High-income liberal Democrats may sport lawn signs proclaiming, “In this house, we believe ... no human is illegal.” The logical consequence of that belief is an open border. But modest-income folks in border counties know that flows of illegal immigrants result in disorder, disease, and crime.

There is plenty of impatience with increased disorder in election returns below the presidential level. Consider Los Angeles County, America’s largest county, with nearly 10 million people, more people than 40 of the 50 states. It voted 71 percent for Mr. Biden in 2020.

Current returns show county District Attorney George Gascon winning only 21 percent of the vote in the nonpartisan primary. He’ll apparently face Republican Nathan Hochman, a critic of his liberal policies, in November.

Gascon, elected after the May 2020 death of counterfeit-passing suspect George Floyd in Minneapolis, is one of many county prosecutors supported by billionaire George Soros. His policies include not charging juveniles as adults, not seeking higher penalties for gang membership or use of firearms, and bringing fewer misdemeanor cases.

The predictable result has been increased car thefts, burglaries, and personal robberies. Some 120 assistant district attorneys have left the office, and there’s a backlog of 10,000 unprosecuted cases.

More than a dozen other Soros-backed and similarly liberal prosecutors have faced strong opposition or have left office.

St. Louis prosecutor Kim Gardner resigned last May amid lawsuits seeking her removal, Milwaukee’s John Chisholm retired in January, and Baltimore’s Marilyn Mosby was defeated in July 2022 and convicted of perjury in September 2023. Last November, Loudoun County, Virginia, voters (62 percent Biden) ousted liberal Buta Biberaj, who declined to prosecute a transgender student for assault, and in June 2022 voters in San Francisco (85 percent Biden) recalled famed radical Chesa Boudin.

Similarly, this Tuesday, voters in San Francisco passed ballot measures strengthening police powers and requiring treatment of drug-addicted welfare recipients.

In retrospect, it appears the Floyd video, appearing after three months of COVID-19 confinement, sparked a frenzied, even crazed reaction, especially among the highly educated and articulate. One fatal incident was seen as proof that America’s “systemic racism” was worse than ever and that police forces should be defunded and perhaps abolished.

2020 was “the year America went crazy,” I wrote in January 2021, a year in which police funding was actually cut by Democrats in New York, Los Angeles, San Francisco, Seattle, and Denver. A year in which young New York Times (NYT) staffers claimed they were endangered by the publication of Sen. Tom Cotton’s (R-Ark.) opinion article advocating calling in military forces if necessary to stop rioting, as had been done in Detroit in 1967 and Los Angeles in 1992. A craven NYT publisher even fired the editorial page editor for running the article.

Evidence of visible and tangible discontent with increasing violence and its consequences—barren and locked shelves in Manhattan chain drugstores, skyrocketing carjackings in Washington, D.C.—is as unmistakable in polls and election results as it is in daily life in large metropolitan areas. Maybe 2024 will turn out to be the year even liberal America stopped acting crazy.

Chaos and disorder work against incumbents, as they did in 1968 when Democrats saw their party’s popular vote fall from 61 percent to 43 percent.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Government

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The…

Share this:

{kind=link}

{kind=link}

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

The U.S. Department of Veterans Affairs (VA) reviewed no data when deciding in 2023 to keep its COVID-19 vaccine mandate in place.

{kind=link}

VA Secretary Denis McDonough said on May 1, 2023, that the end of many other federal mandates “will not impact current policies at the Department of Veterans Affairs.”

He said the mandate was remaining for VA health care personnel “to ensure the safety of veterans and our colleagues.”

Mr. McDonough did not cite any studies or other data. A VA spokesperson declined to provide any data that was reviewed when deciding not to rescind the mandate. The Epoch Times submitted a Freedom of Information Act for “all documents outlining which data was relied upon when establishing the mandate when deciding to keep the mandate in place.”

The agency searched for such data and did not find any.

“The VA does not even attempt to justify its policies with science, because it can’t,” Leslie Manookian, president and founder of the Health Freedom Defense Fund, told The Epoch Times.

“The VA just trusts that the process and cost of challenging its unfounded policies is so onerous, most people are dissuaded from even trying,” she added.

The VA’s mandate remains in place to this day.

The VA’s website claims that vaccines “help protect you from getting severe illness” and “offer good protection against most COVID-19 variants,” pointing in part to observational data from the U.S. Centers for Disease Control and Prevention (CDC) that estimate the vaccines provide poor protection against symptomatic infection and transient shielding against hospitalization.

There have also been increasing concerns among outside scientists about confirmed side effects like heart inflammation—the VA hid a safety signal it detected for the inflammation—and possible side effects such as tinnitus, which shift the benefit-risk calculus.

President Joe Biden imposed a slate of COVID-19 vaccine mandates in 2021. The VA was the first federal agency to implement a mandate.

President Biden rescinded the mandates in May 2023, citing a drop in COVID-19 cases and hospitalizations. His administration maintains the choice to require vaccines was the right one and saved lives.

“Our administration’s vaccination requirements helped ensure the safety of workers in critical workforces including those in the healthcare and education sectors, protecting themselves and the populations they serve, and strengthening their ability to provide services without disruptions to operations,” the White House said.

Some experts said requiring vaccination meant many younger people were forced to get a vaccine despite the risks potentially outweighing the benefits, leaving fewer doses for older adults.

“By mandating the vaccines to younger people and those with natural immunity from having had COVID, older people in the U.S. and other countries did not have access to them, and many people might have died because of that,” Martin Kulldorff, a professor of medicine on leave from Harvard Medical School, told The Epoch Times previously.

The VA was one of just a handful of agencies to keep its mandate in place following the removal of many federal mandates.

“At this time, the vaccine requirement will remain in effect for VA health care personnel, including VA psychologists, pharmacists, social workers, nursing assistants, physical therapists, respiratory therapists, peer specialists, medical support assistants, engineers, housekeepers, and other clinical, administrative, and infrastructure support employees,” Mr. McDonough wrote to VA employees at the time.

“This also includes VA volunteers and contractors. Effectively, this means that any Veterans Health Administration (VHA) employee, volunteer, or contractor who works in VHA facilities, visits VHA facilities, or provides direct care to those we serve will still be subject to the vaccine requirement at this time,” he said. “We continue to monitor and discuss this requirement, and we will provide more information about the vaccination requirements for VA health care employees soon. As always, we will process requests for vaccination exceptions in accordance with applicable laws, regulations, and policies.”

The version of the shots cleared in the fall of 2022, and available through the fall of 2023, did not have any clinical trial data supporting them.

A new version was approved in the fall of 2023 because there were indications that the shots not only offered temporary protection but also that the level of protection was lower than what was observed during earlier stages of the pandemic.

Ms. Manookian, whose group has challenged several of the federal mandates, said that the mandate “illustrates the dangers of the administrative state and how these federal agencies have become a law unto themselves.”

Veterans Affairs Kept COVID-19 Vaccine Mandate In Place Without Evidence

When Military Rule Supplants Democracy

Low Iron Levels In Blood Could Trigger Long COVID: Study

Walmart has really good news for shoppers (and Joe Biden)

Angry Shouting Aside, Here’s What Biden Is Running On

Jack Smith Says Trump Retention Of Documents “Starkly Different” From Biden

Walmart joins Costco in sharing key pricing news

Beloved mall retailer files Chapter 7 bankruptcy, will liquidate

Are Voters Recoiling Against Disorder?

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex