International

“This Is For You, Dad”: Interview With An Anonymous GameStop Investor

"This Is For You, Dad": Interview With An Anonymous GameStop Investor

Authored by Matt Taibbi via TK News,

Thursday, January 21st was a critical day in the story of the video game chain GameStop (ticker name: GME). Retail investors, includin

Share this:

Authored by Matt Taibbi via TK News,

Thursday, January 21st was a critical day in the story of the video game chain GameStop (ticker name: GME). Retail investors, including many subscribers to a Reddit forum called wallstreetbets, pushed the company’s stock from $6 to $43.03, but experts said playtime was over. It was time for the big shots to clean up.

According to Citron Research, one of many funds that had bet on the brick-and-mortar store to fail, those investing in GME were “the suckers at this poker game,” and would soon be sorry when the stock went “back to $20 fast.”

They were wrong. Instead of amateurs being shoved aside by hedge funds, it was the pros who had their backs broken, as GME soared to $65.05, beginning a steep ascent that would become an international news phenomenon.

It was the “We’re gonna need a bigger boat” moment for Wall Street. The pros had been sloppy. By late 2020, shares in GameStop were well over 100% short. A sudden rise in value would force shorts to pay exorbitant prices just to get out of the trade. By the afternoon of the 21st, all the “suckers” on Reddit had to do to beat them was nothing, and they did just that, behind the rallying cry “diamond hands,” signifying a determination to hold at all costs.

Why hold? One of the millions of subscribers to wallstreetbets posted a note, explaining what the trade meant to him:

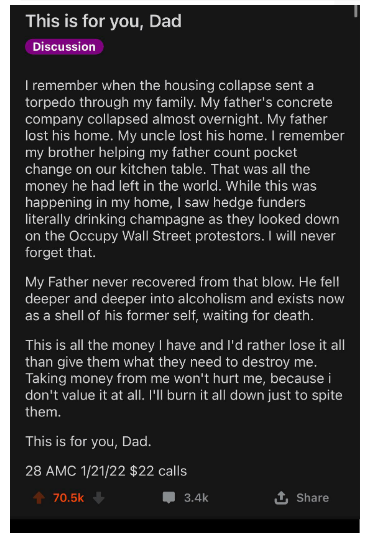

This is for you, Dad

I remember when the housing collapse sent a torpedo through my family. My father’s concrete company collapsed almost overnight. My father lost his home. My uncle lost his home. I remember my brother helping my father count pocket change on our kitchen table. That was all the money he had left in the world. While this was happening in my home, I saw hedge funders literally drinking champagne as they looked down on the Occupy Wall Street protesters. I will never forget that.

My father never recovered from that blow. He fell deeper and deeper into alcoholism and exists now as a shell of his former self, waiting for death.

This is all the money I have and I’d rather lose it all than give them what they need to destroy me. Taking money from me won’t hurt me, because I don’t value it at all. I’ll burn it down just to spite them.

This is for you, Dad.

The post went viral, scoring over 70,000 upvotes the first day and ending up on the front page of Reddit. The author, who had gone to lengths to keep his identity private, saw his Reddit handle “Space-peanut” inundated with press requests, from podcasts all the way up to the New York Times. Stuart Varney of Fox Business News read his post out loud on live television.

Meanwhile, on wallstreetbets, Redditor after Redditor responded with similar tales.

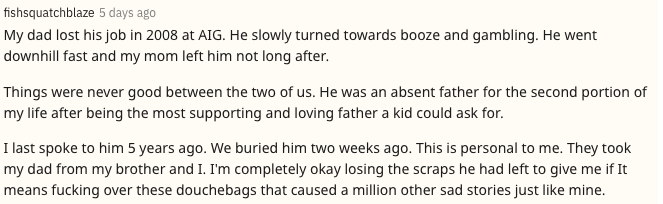

“My mother lost her house that spent 20 years saving for in 2008 while raising me and my sister,” wrote one. “I remember sitting on the curb, trying to keep it together myself at 16 while watching her break down uncontrollably…”

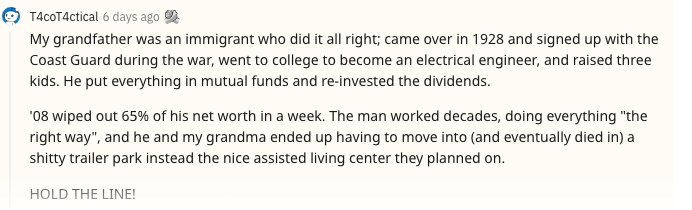

“My dad is a carpenter and thirty years of work, retirement, and savings was nearly wiped out,” wrote another, adding: “This is for you, Dad.”

A third letter described a man who, having lost his dairy business after the crash, attempted suicide by shooting himself in the face in the woods. He survived, leaving his son to “carry his blown-apart body to the house,” only to finish the job by throwing himself in front of a train soon after.

“Space-peanut” watched in awe as stories piled up. The thread soon read like the untold history of America after the 2008 financial crisis:

The original poster, whom I’ll call SP, was unaccustomed to attention. A one-time military man and father of two, he had no other social media presence and joined Reddit exclusively to comment about stock on wallstreetbets. He was overwhelmed by what he calls “just an endless Rolodex of sad stories,” nearly all referencing the same period after the crash.

“I think that's why my post, however terse, hit such a nerve,” he says. “So many people were saying, ‘I have deep pain from this point in time, too.’”

An acquaintance of a long-ago source of mine, the man reached out this week. Across several conversations, he explained what GameStop meant to him, and why. For a variety of reasons, mainly having to do with his professional situation, he asked to remain anonymous.

SP is cautious, articulate, and well-read. In our first call, one of the first things he told me was that even growing up, he’d “always wanted to work on a trading desk.” I asked why. The answer was a three-decade story that ran all the way to GameStop. It’s reproduced below, in Q&A form.

Since 2008, the tendency among mainstream commentators has been to shrug off reverberations from the crash that force their way into news, usually on the grounds that the millions who lost homes, careers, marriages, lifetimes of savings, health, and in thousands of cases, their lives, are not truly poor or “working class,” or are only “relatively low-wealth,” as New York magazine recently put it. In the case of GameStop, there’s been a parade of stories describing investors as dupes, dummies, financial Trumpists, irresponsible gamblers, even crooks, their trade pegged as almost everything but what on some level it surely was and is, an echo of a suppressed national disaster.

Was GameStop “recreational” investing gone haywire, or a climax to a story building for a generation? Here’s one person’s answer:

SP: I grew up watching my parents struggle with money. Money was discussed all the time. They fought all the time. The older I got, the more I felt I had to do anything to keep my own kids from going through the same thing.

My parents worried in different ways. With my mother, I regularly knew how much money was in her checking account because she would stress-yell the amount whenever I asked for anything. It was really difficult for her.

My dad was the opposite. He wanted you to think he had money, but you were looking around and thinking, "I'm pretty sure we don't." Because I don't have a bed, and my brother is sleeping on a couch. So if you've got it, maybe we should use it, I don't know. So they were different in that regard.

From the time I was eight and nine, I was spending summers working. When I was with my father he thought it was important for us to do the hardest manual labor possible.

TK: Was that supposed to be about character-building?

SP: So my dad thought it was a good idea, but at the same time, I think he needed to go to work. And that was the best place for us to be, because I don't think he could leave us alone all day. So he was like, "I know what we'll do. I'll bring you to work. You can work and then we'll be together." (Laughs) That was character-building, yes. I built a lot of character out there. I'd say that much. I had way too much character.

To this day I know I can outwork people in physical labor simply because my threshold for what is considered difficult is much higher, because I spent summers as a child doing that. I'm not sure where that squares with labor laws, but it happened.

TK: What kind of work?

SP: At that time, we were doing field work out where we were from. So you're doing a lot of leaching, which just is basically watching a big field fill up with water to prepare it for planting. One summer, we were doing that. And then we tore down houses. We were working with other guys who were grown men and didn't speak English.

Those guys would do anything to get here and take that job, especially the day laborers. They wake up super early, go to a spot where they know a contractor is going to drive by, and try to pick some of them up for the day. I mean, not an easy existence. So it's difficult to hear people lambast a specific group of migrant workers. I feel like saying, "Hey, I know I've done work with migrant workers and I'll tell you what, that would be difficult to say, ‘This is what I'm going to do my whole life.’ I'll tell you that right now.

TK: What did your mother do?

SP: After the divorce was over, she moved to a new state, and she spent years starting up a new business, a dining guide in a big city. Put her own money in it. There was a lot of driving, over an hour every morning to get to the city, then appointments all day. She was a single mom at the time, so she had to get back, get the kids, take care of us. But she was doing well. She had advertising contracts lined up and after years of work, was just about ready to launch, when the dot-com bubble burst and she lost it all.

Almost overnight, the only thing really left of the business was a fax machine in our apartment. Before, companies would be faxing her signed agreements, letters of intent, and so on. All the marketing calls would come back to that number hanging on the fax machine. So basically, anything connected with her company was coming back there.

For a long time, she would just lay on the couch, locked in depression. The fax would go off from time to time and she wouldn’t react, she would lie there in a daze. Looking back on it, it must have been painful every time that fricking thing rang, a reminder of the thing you failed at. Just imagine, you're so close to making it, and then an exogenous shock prevents you from achieving the dream you’d set out for yourself.

She could've just let that beat her down forever. But she eventually got her shit together and was like, "Hey, I need to retool myself." She went back to school, got a master's degree, started teaching. My dad, on the other hand, didn't do that. He never got over what happened.

TK: This was the concrete company?

SP: Right. In the 2000s, he was a superintendent at a concrete company that was very successful for a time, employed hundreds of people. I worked there, too, when I was 19. Again, there were a lot of migrant laborers doing this work too, guys who were supporting families back in Mexico. And 2008 hit, another financial collapse.

There was such explosive growth, and all of the sudden, it was gone. My father lost his job, his house, and he just got worse and worse and worse. He’s got heart problems now, he’s on a bunch of medication. I just expect to get the call any day that he's going to be dead. He's just circling the drain. He's been in and out of the hospital. He doesn't take care of himself.

One of the people who answered my post on Reddit talked about how he felt the crash basically robbed his father from him. That's how it was. We used to talk five times a day, man. Talking to my dad was the most reliable thing that I could do. I talked to him and my brother four or five times a day for fifteen, twenty years. And then over the past probably four or five years, it was less and less. I think I went a full year without talking to him. He didn't know I got married. He hasn’t seen my second daughter.

I’ll tell you, when you look in the eyes of a grown man who has no options to support his kids, that’s devastating. I decided when I first saw that in him, I would sweat blood to make sure that never happened to my family.

I put myself through school, going for the cheapest state tuition, and did the same for the MBA program. I was able to take out a loan and I was able to start the program a semester early, while I was still finishing undergrad, so I could economize the cost. And then I went straight through both summers and got it done really quickly, overloading my class schedule because I didn't want to take out more loans. So I got it done for $25,000, and I was working full-time too, while I was there. Later, I was able to save up enough to get it completely discharged, though in order to do that, I had to have five roommates for four years.

TK: Why business school, why finance?

SP: By the time I was getting ready to go to college, my brother had already been in the Marine Corps for a few years and had already done two tours in Iraq, and it was the worst time to be there. He saw a lot of carnage. And he was saying, "You know, if you still want to be in the military, it's a much better route if you go to college first, from what I've seen." And every single person I'd ever done manual labor jobs with had said, if they could do one thing differently, they would have gone to college. They’d be on the job and put a hand on my shoulder and say, "You don't want to have to do this when you're 50." Like I'm 50, I'm hanging drywall. It's my company, but it would be nice to not have to do it.

Anyway, I got into being a Wall Street trader when I was an undergrad. I liked the high energy. I also knew a bunch of people from my home city that grew up to be traders. (Laughs). Some of them were really dumb and some of them didn't even finish high school, but they knew a guy who was on the floor like (mimics a Chicago accent) "And my boy Tony, he hooked me up with a jawb on the exchange…”

But they made a lot of money. I thought, "This is ridiculous. I'm more intelligent than that guy." He could barely do math, but he’s trading options. Still, I liked hanging out with those people. Some of them were not real class acts, but… I liked the idea that it was challenging. I just wanted to study everything I could. I knew I was going to be competing with people that had way better educational pedigrees than I did, and I needed every single edge that I could get just to get myself in the door.

I got really interested in the question, "what were the things you look for when a company starts going into financial dire straits?" That led me down the path of finding good books that had been written in the past about major bankruptcies and collapses, books like When Genius Failed, Predator’s Ball, and A Colossal Failure of Common Sense. I was studying companies like Long Term Capital Management, which got bailed out in the late nineties.

At the time, it was just interesting to see how, when people did their homework and took a big risk on some distressed debt, they could make a gigantic payday in one day. And I was like, man, that would be exhilarating. I even saw the original movie Wall Street and I was like, "That's badass. Even though these guys are criminals, just the idea of being on a trading floor seems really cool."

Now I look back at that and think, if I’d become that person, I’d be sitting in the place of some of these hedge funds who do this all day. They go out and find companies that are going to be struggling at a specific date and time, and that's when they start buying massive put spreads, shorting the piss out of the stock, putting it in the dirt, ensuring it will fail. I look back on it now, and it's like, “Goddamn, that would have really sucked.” They're two very different paths I was going down. I'm glad I chose this one.

TK: What was the other path?

SP: Look, I originally did all that reading because I was looking for insights on how to make money. But studying firms like Drexel Burnham Lambert, Long Term Capital Management, Lehman Brothers, I learned two other things.

One is that these guys get bailed out. The second is that they never go to jail, even when they’re dead to rights. I think the two people that got prosecuted first after the financial crisis were the two Bear Stearns hedge fund managers. The implosion of those two hedge funds was the canary in the coal mine, because that was the death knell for the coming crash.

These two guys had emails back and forth, talking about how fraudulent their products were. Talking about how they're totally screwing over clients, in writing! And not one of them went to jail. And who did they go after at that time? Bernie Madoff. He was the one person who went to jail. Why did he get prosecuted? Because he stole from the rich!

TK: They even made a movie about it, starring Robert DeNiro…

SP: Exactly! How come they didn't make any movies about these other horrible people that profited off of the destruction of the economy? The people who ran Countrywide, or the people who were working at the ratings agencies, who knew the things they were rating were fraudulent? Even just down at the mortgage origination level. They made tons of money, and not one of those people went to jail.

Anyway, I didn’t go that route. After I got my MBA, I joined the military.

TK: Why?

SP: My brother at the time had already been out of the Marines for a while. He was working for a hedge fund out in California. And his boss was very, very old, in his nineties. I thought, "Man, you can literally die at your desk at 100 years old in finance, but there's only a short window that you can serve the nation, and once that, once that door closes, it never opens again." So I joined, went to Officer Candidate School, got in, went to other countries, saw a lot of very, very poor places, which gave me some perspective. Long story short, I ended up working as a software engineer.

TK: How did you get into online investing?

SP: I was still keeping up with all my financial periodicals, because I knew one day I was going to step back into that world. I was able to start making stock picks for myself. The first real investment I made was in Netflix when it was still double digits. I made a brokerage account with my bank and threw some money in there and started going at it.

The industry was really changing. Robinhood's slogan is “Democratizing Finance,” but really it’s the computer science industry democratizing finance, because all those tools that used to be proprietary are free now, included in your trading app.

If you make a TD Ameritrade account, you can run, think or swim. It’s like a mini Bloomberg terminal. You're not going to get the same richness of data, but you're going to get a significant amount that you normally wouldn't ten years ago. And in places like wallstreetbets, I was meeting people who clearly used to or still did work on Wall Street, who would teach you, for free, how to do things like recognize distressed companies, research their debt covenants, look up public data about who was invested in what, and so on.

There’s one guy, he goes by the name fuzzy blankeet — it’s surreal on wallstreetbets, you discuss such serious topics with such ridiculously named people — who was teaching us how to be distressed debt buyers. These are really intelligent people, just giving away knowledge.

A lot of the tools we have now, it used to be only people working at the top hedge funds on Wall Street had access to that information. So a lot of the barriers had collapsed. But the system is still skewed, which I started to see more clearly when the pandemic hit.

TK: How so?

I remember last March, just as the pandemic was taking hold, I was watching CNBC, and Bill Ackman, the big hedge fund guy, basically saying it’s the end of the American economy. He’s saying, “Shutdown is inevitable,” and calling for everything to be closed except essential services:

At the time, I was wrapped up in the doom, on the side of, "I don't think we're prepared for what's coming." Because I was watching the videos coming out of China and thinking, "There are people just passing out. That's not normal. I think that's bad." I saw a video of somebody being welded into his apartment, and I again, I thought, that seems bad. Seeing Ackman on TV, I was like, "I think he's right."

As time went on, though, that moment bothered me. I thought, “That fuck, he’s causing the panic.”

I guarantee a lot of people were like, "Bill Ackman's a smart dude. He's a lot more successful investor than I am, and he says shit's about to hit the fan. I better start buying some protection. I don't know, short really volatile, high flying stocks, and maybe buy a lot of put spreads." But then we all know what happened after that.

TK: That broadcast was March 18th, so the $2 trillion bailout was announced a week after. The market had been plummeting straight down, but it bounced right back up and kept going.

SP: It’s the COVID-19 sell-off and pump. It’s what these guys do. It really does feel as though CNBC is a participant in market manipulation for the rich. These hedge fund guys go on air and it’s like they’re trying to spook the herd in the direction of their trades. They tell everyone to get out when they’re short, and once all the meat is all off the bone, they go long, just in time for the recovery. They get to call the top and the bottom of the market. It’s totally fucked.

The bailout and the pandemic just exposed how there are different sets of rules, not just for different types of investors, but different types of businesses. Your favorite sandwich shop? Closed. If you've got 200 of those sandwich shops? Open.

If you had sufficient capital to lobby whatever your government is, you could get an exemption, but if you were a small-time business owner, you were out of luck, and that just made no sense to me. I was like, “We're just making this up on the fly.”

TK: When did you first pay attention to GameStop?

SP: I remember people posting about the GameStop potential short squeeze last summer. I definitely didn't catch any of the attention earlier than that, but I didn't get the trade. I'll be honest with you. I saw the potential there. I really did, but I was like, there's just so much going against you on that. And at the same time, the business needs to make money and they're in debt and they're not making money.

But at some point, once this all started, I started to think about it. We’re in a pandemic, and there are all these people who couldn’t work all year. Or they’re small businesses that don’t have the political impact. They’re going to take the loss. And in the middle of all this misery, you have a group of the most cancerous rent-seekers on earth, aligning to destroy this company GameStop, because they decided it shouldn’t exist anymore.

And it was GameStop! It’s such a visceral symbol for people in my generation. Even for me, in all those bad times growing up, it was always a nice memory just to go to a strip mall, go in the store, check out a game or two. I like GameStop. Everyone remembers going to GameStop. It’s part of what made it such an obvious rallying cry.

That was it for me. I found myself thinking, I didn’t care if I lost every last dollar doing it, I was going to put it on GameStop, just to see them panic for once. Even if for just one moment they have to think about how they’re going to make their payments for their Manhattan apartments, that’s worth it. They’re playing these games while there are people out there who can’t afford Christmas presents for their kids, can’t afford food. What are these families supposed to do?

Meanwhile those guys at the hedge funds, they’re not sharing that fear. Why should they? They’re going to get bailed out anyway.

TK: One criticism of the GME traders is that while there are billion-dollar shorts losing on the other side, there are also big money managers on the long side, essentially using what some call “recreational” day-traders as camouflage. What do you say to that?

There are definitely some high net worth individuals in wallstreetbets, and they were probably making good money early on, incidentally getting some good research done for free and getting in on some trades early. But there are a lot of small-time investors in there, too. The forum is so big, there's probably a healthy bell curve of every demographic in there now. To say that the forum is made up of people who are just sitting in the basement, and don't really have anything to lose, that’s not right. A lot of people may not care about the money not because they have too much, but too little. It may be their stimulus check, and they’re saying, "Well, I don't have anything anyway. This was my only way to maybe make something, but I’d rather send a message with it."

TK: What’s Robinhood’s role?

SP: Imagine that Wall Street is a big building, Robinhood is basically letting you into the lobby. The barrier to entry to buying and trading and stocks and options with apps like Robinhood really is very low. What we've discovered in the last ten days, though, is that the pen they built for us does not scale well. Big shocker!

It's ironic, for a brokerage that's primarily run by software engineers, that they seem never to have thought about the edge case of millions of people transferring in thousands of dollars in one day, and all buying the same security. I don't think that they really thought about, "Hey, what if this happens?"

TK: GameStop crested last Thursday, January 28th, when Robinhood and other platforms began restricting trades in GME and other stocks. Robinhood obviously makes its money selling its “order flow” to a major high-frequency trader, Citadel, which was likely also the firm that made capital calls on Robinhood during the GME frenzy.

A lot of Reddit investors believe Citadel and its billionaire CEO Ken Griffin used those collateral calls to pressure Robinhood into restricting trading in GME. Some press analysts think that explanation is conspiratorial. What’s your take?

SP: Whether or not they were pressured to kill the rally doesn't matter. The effect was the same. Robinhood’s restriction killed the rally, a hundred percent. That was the only thing that gave all the firms that had short interests a chance to try to recover. Now, the thing that is really insidious is some retail brokerages that locked out their retail traders, if you had an account with a certain minimum amount of money in it, you could call the customer service line that was reserved for your level of account and they would turn trading back on.

So two people using the same trading app could have different market access. It’s just like we were talking about before. When the GameStop thing started, the shorts were like, “Hey, let's just kill this business because it's a pandemic, they're going to close anyway, let's just destroy it.” And then, once we started kicking it in the balls, they changed the game and killed the trade. It was like, "Okay, of course, of course."

As for the conspiracy charge, it makes me laugh. JP Morgan Chase last fall settled for $920 million or whatever in a case involving spoofing in the metals markets. Before that, they would have said, there’s no such thing as spoofing! Same with manipulation of LIBOR. Once upon a time, if you accused the banks of manipulating LIBOR, they’d say, “That’s a conspiracy theory.” Then there were settlements and now everyone knows it happened. With these people, it's always a conspiracy until it isn't. Once they’re found out, it's like, "Oh, you caught us. You're right. It wasn't a conspiracy. But this other thing, that's a conspiracy. That's not happening."

TK: What was your reaction to the press coverage of GameStop?

SP: The majority of the media that I've seen on WallStreetBets is just incorrect. The stuff that came out really early was trying to label it as a far right-ish type movement, and they got smacked down really hard on that because that’s the opposite of what happens in there. The forum is not political at all. If you post any political bullshit, that is the fastest way to get banned. There’s literally a rule, “No political bullshit.” Nobody wants to hear it. It’s strictly to talk about trades.

TK: What’s the future of wallstreetbets?

SP: I'm fearful of what could happen. The forum is big now. It’s never going to be ignored again. There are two opposing forces. You have big businesses that are going to try to channel this movement to benefit themselves. But at the same time, you've got a lot of long-time people who've been on there who can sniff out a fraud pretty quickly.

It’s going to be a cat and mouse game. We already see it happening. The biggest one was in silver. Silver is often used as a way for large owners of silver, like in the SLVETF, to cover losses elsewhere. Last week I saw zero advertisements to buy Gamestop stock. Over the weekend, I saw countless news articles and advertisements all over to buy physical bullion. They’re saying, “Silver is going to get pumped. The Reddit crowd is turning to silver.”

TK: Yahoo! had “Silver Squeeze: How to join the Reddit Bandwagon.” CNBC had, “Is Silver the Next GameStop?” It was like wallstreetbets went Hollywood.

SP: I'm like, "I’ve got to call bullshit on this." Now, if a large institutional owner of an asset was to, I don't know, take out a bunch of ads and hire some people to post on wallstreetbets and maybe hire some botnets through a cut-out, would that be legal? Sounds like a pump and dump to me, but it also sounds difficult to prove. I'm not saying it's happened. I'm saying it's odd, and it's very possible.

There's going to be a constant battle to direct the Sauron-like gaze of this board now. It’s going to be very difficult to get ahead of that, just like it's difficult to know what the number one meme is for next month.

TK: Was a message sent in the GameStop story, and if so, what was it?

You had a leaderless group rise up and use whatever market power they had, whether it was buying a hundred thousand shares, or one. Some very established traders who trade for themselves frequent those boards. And then you had people who saw the message, they saw the Batman symbol and they rallied to that. You know how many messages I saw in the thread, of people just lining up? It meant something to them. They got to buy a fractional share of the hero's journey.

But the trade was destroyed. Whether or not that was intentional is not for me to say. All I can say is what happened. Retail brokerages all of a sudden stopped allowing their clients to trade, unless they were of a certain net worth. Banks could do it. Hedge funds could keep doing it. They could still be in the trade. But you and I could not. We could only sell. We could only do the one thing that they would need us to do, to get themselves out of the quagmire. And it wasn't about price at that point. It was about control of physical shares that would allow you to cover.

So yeah, a message got sent. But one was also received. They basically said, “We understand the message you're sending. And here's the message we're sending back.”

But it was worth it.

International

Fuel poverty in England is probably 2.5 times higher than government statistics show

The top 40% most energy efficient homes aren’t counted as being in fuel poverty, no matter what their bills or income are.

Share this:

The cap set on how much UK energy suppliers can charge for domestic gas and electricity is set to fall by 15% from April 1 2024. Despite this, prices remain shockingly high. The average household energy bill in 2023 was £2,592 a year, dwarfing the pre-pandemic average of £1,308 in 2019.

The term “fuel poverty” refers to a household’s ability to afford the energy required to maintain adequate warmth and the use of other essential appliances. Quite how it is measured varies from country to country. In England, the government uses what is known as the low income low energy efficiency (Lilee) indicator.

Since energy costs started rising sharply in 2021, UK households’ spending powers have plummeted. It would be reasonable to assume that these increasingly hostile economic conditions have caused fuel poverty rates to rise.

However, according to the Lilee fuel poverty metric, in England there have only been modest changes in fuel poverty incidence year on year. In fact, government statistics show a slight decrease in the nationwide rate, from 13.2% in 2020 to 13.0% in 2023.

Our recent study suggests that these figures are incorrect. We estimate the rate of fuel poverty in England to be around 2.5 times higher than what the government’s statistics show, because the criteria underpinning the Lilee estimation process leaves out a large number of financially vulnerable households which, in reality, are unable to afford and maintain adequate warmth.

Energy security

In 2022, we undertook an in-depth analysis of Lilee fuel poverty in Greater London. First, we combined fuel poverty, housing and employment data to provide an estimate of vulnerable homes which are omitted from Lilee statistics.

We also surveyed 2,886 residents of Greater London about their experiences of fuel poverty during the winter of 2022. We wanted to gauge energy security, which refers to a type of self-reported fuel poverty. Both parts of the study aimed to demonstrate the potential flaws of the Lilee definition.

Introduced in 2019, the Lilee metric considers a household to be “fuel poor” if it meets two criteria. First, after accounting for energy expenses, its income must fall below the poverty line (which is 60% of median income).

Second, the property must have an energy performance certificate (EPC) rating of D–G (the lowest four ratings). The government’s apparent logic for the Lilee metric is to quicken the net-zero transition of the housing sector.

In Sustainable Warmth, the policy paper that defined the Lilee approach, the government says that EPC A–C-rated homes “will not significantly benefit from energy-efficiency measures”. Hence, the focus on fuel poverty in D–G-rated properties.

Generally speaking, EPC A–C-rated homes (those with the highest three ratings) are considered energy efficient, while D–G-rated homes are deemed inefficient. The problem with how Lilee fuel poverty is measured is that the process assumes that EPC A–C-rated homes are too “energy efficient” to be considered fuel poor: the main focus of the fuel poverty assessment is a characteristic of the property, not the occupant’s financial situation.

In other words, by this metric, anyone living in an energy-efficient home cannot be considered to be in fuel poverty, no matter their financial situation. There is an obvious flaw here.

Around 40% of homes in England have an EPC rating of A–C. According to the Lilee definition, none of these homes can or ever will be classed as fuel poor. Even though energy prices are going through the roof, a single-parent household with dependent children whose only income is universal credit (or some other form of benefits) will still not be considered to be living in fuel poverty if their home is rated A-C.

The lack of protection afforded to these households against an extremely volatile energy market is highly concerning.

In our study, we estimate that 4.4% of London’s homes are rated A-C and also financially vulnerable. That is around 171,091 households, which are currently omitted by the Lilee metric but remain highly likely to be unable to afford adequate energy.

In most other European nations, what is known as the 10% indicator is used to gauge fuel poverty. This metric, which was also used in England from the 1990s until the mid 2010s, considers a home to be fuel poor if more than 10% of income is spent on energy. Here, the main focus of the fuel poverty assessment is the occupant’s financial situation, not the property.

Were such alternative fuel poverty metrics to be employed, a significant portion of those 171,091 households in London would almost certainly qualify as fuel poor.

This is confirmed by the findings of our survey. Our data shows that 28.2% of the 2,886 people who responded were “energy insecure”. This includes being unable to afford energy, making involuntary spending trade-offs between food and energy, and falling behind on energy payments.

Worryingly, we found that the rate of energy insecurity in the survey sample is around 2.5 times higher than the official rate of fuel poverty in London (11.5%), as assessed according to the Lilee metric.

It is likely that this figure can be extrapolated for the rest of England. If anything, energy insecurity may be even higher in other regions, given that Londoners tend to have higher-than-average household income.

The UK government is wrongly omitting hundreds of thousands of English households from fuel poverty statistics. Without a more accurate measure, vulnerable households will continue to be overlooked and not get the assistance they desperately need to stay warm.

Torran Semple receives funding from Engineering and Physical Sciences Research Council (EPSRC) grant EP/S023305/1.

John Harvey does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

european uk pandemicInternational

Looking Back At COVID’s Authoritarian Regimes

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked,…

Share this:

After having moved from Canada to the United States, partly to be wealthier and partly to be freer (those two are connected, by the way), I was shocked, in March 2020, when President Trump and most US governors imposed heavy restrictions on people’s freedom. The purpose, said Trump and his COVID-19 advisers, was to “flatten the curve”: shut down people’s mobility for two weeks so that hospitals could catch up with the expected demand from COVID patients. In her book Silent Invasion, Dr. Deborah Birx, the coordinator of the White House Coronavirus Task Force, admitted that she was scrambling during those two weeks to come up with a reason to extend the lockdowns for much longer. As she put it, “I didn’t have the numbers in front of me yet to make the case for extending it longer, but I had two weeks to get them.” In short, she chose the goal and then tried to find the data to justify the goal. This, by the way, was from someone who, along with her task force colleague Dr. Anthony Fauci, kept talking about the importance of the scientific method. By the end of April 2020, the term “flatten the curve” had all but disappeared from public discussion.

Now that we are four years past that awful time, it makes sense to look back and see whether those heavy restrictions on the lives of people of all ages made sense. I’ll save you the suspense. They didn’t. The damage to the economy was huge. Remember that “the economy” is not a term used to describe a big machine; it’s a shorthand for the trillions of interactions among hundreds of millions of people. The lockdowns and the subsequent federal spending ballooned the budget deficit and consequent federal debt. The effect on children’s learning, not just in school but outside of school, was huge. These effects will be with us for a long time. It’s not as if there wasn’t another way to go. The people who came up with the idea of lockdowns did so on the basis of abstract models that had not been tested. They ignored a model of human behavior, which I’ll call Hayekian, that is tested every day.

These are the opening two paragraphs of my latest Defining Ideas article, “Looking Back at COVID’s Authoritarian Regimes,” Defining Ideas, March 14, 2024.

Another excerpt:

That wasn’t the only uncertainty. My daughter Karen lived in San Francisco and made her living teaching Pilates. San Francisco mayor London Breed shut down all the gyms, and so there went my daughter’s business. (The good news was that she quickly got online and shifted many of her clients to virtual Pilates. But that’s another story.) We tried to see her every six weeks or so, whether that meant our driving up to San Fran or her driving down to Monterey. But were we allowed to drive to see her? In that first month and a half, we simply didn’t know.

Read the whole thing, which is longer than usual.

(0 COMMENTS) budget deficit coronavirus covid-19 white house fauci trump canadaInternational

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

Authored by Zachary Stieber via The Epoch Times (emphasis…

Share this:

{kind=link}

Authored by Zachary Stieber via The Epoch Times (emphasis ours),

People who recovered from COVID-19 and received a COVID-19 shot were more likely to suffer adverse reactions, researchers in Europe are reporting.

{kind=link}

Participants in the study were more likely to experience an adverse reaction after vaccination regardless of the type of shot, with one exception, the researchers found.

Across all vaccine brands, people with prior COVID-19 were 2.6 times as likely after dose one to suffer an adverse reaction, according to the new study. Such people are commonly known as having a type of protection known as natural immunity after recovery.

People with previous COVID-19 were also 1.25 times as likely after dose 2 to experience an adverse reaction.

The findings held true across all vaccine types following dose one.

Of the female participants who received the Pfizer-BioNTech vaccine, for instance, 82 percent who had COVID-19 previously experienced an adverse reaction after their first dose, compared to 59 percent of females who did not have prior COVID-19.

The only exception to the trend was among males who received a second AstraZeneca dose. The percentage of males who suffered an adverse reaction was higher, 33 percent to 24 percent, among those without a COVID-19 history.

“Participants who had a prior SARS-CoV-2 infection (confirmed with a positive test) experienced at least one adverse reaction more often after the 1st dose compared to participants who did not have prior COVID-19. This pattern was observed in both men and women and across vaccine brands,” Florence van Hunsel, an epidemiologist with the Netherlands Pharmacovigilance Centre Lareb, and her co-authors wrote.

There were only slightly higher odds of the naturally immune suffering an adverse reaction following receipt of a Pfizer or Moderna booster, the researchers also found.

The researchers performed what’s known as a cohort event monitoring study, following 29,387 participants as they received at least one dose of a COVID-19 vaccine. The participants live in a European country such as Belgium, France, or Slovakia.

Overall, three-quarters of the participants reported at least one adverse reaction, although some were minor such as injection site pain.

Adverse reactions described as serious were reported by 0.24 percent of people who received a first or second dose and 0.26 percent for people who received a booster. Different examples of serious reactions were not listed in the study.

Participants were only specifically asked to record a range of minor adverse reactions (ADRs). They could provide details of other reactions in free text form.

“The unsolicited events were manually assessed and coded, and the seriousness was classified based on international criteria,” researchers said.

The free text answers were not provided by researchers in the paper.

“The authors note, ‘In this manuscript, the focus was not on serious ADRs and adverse events of special interest.’” Yet, in their highlights section they state, “The percentage of serious ADRs in the study is low for 1st and 2nd vaccination and booster.”

Dr. Joel Wallskog, co-chair of the group React19, which advocates for people who were injured by vaccines, told The Epoch Times: “It is intellectually dishonest to set out to study minor adverse events after COVID-19 vaccination then make conclusions about the frequency of serious adverse events. They also fail to provide the free text data.” He added that the paper showed “yet another study that is in my opinion, deficient by design.”

Ms. Hunsel did not respond to a request for comment.

She and other researchers listed limitations in the paper, including how they did not provide data broken down by country.

The paper was published by the journal Vaccine on March 6.

The study was funded by the European Medicines Agency and the Dutch government.

No authors declared conflicts of interest.

Some previous papers have also found that people with prior COVID-19 infection had more adverse events following COVID-19 vaccination, including a 2021 paper from French researchers. A U.S. study identified prior COVID-19 as a predictor of the severity of side effects.

Some other studies have determined COVID-19 vaccines confer little or no benefit to people with a history of infection, including those who had received a primary series.

The U.S. Centers for Disease Control and Prevention still recommends people who recovered from COVID-19 receive a COVID-19 vaccine, although a number of other health authorities have stopped recommending the shot for people who have prior COVID-19.

Another New Study

In another new paper, South Korean researchers outlined how they found people were more likely to report certain adverse reactions after COVID-19 vaccination than after receipt of another vaccine.

The reporting of myocarditis, a form of heart inflammation, or pericarditis, a related condition, was nearly 20 times as high among children as the reporting odds following receipt of all other vaccines, the researchers found.

The reporting odds were also much higher for multisystem inflammatory syndrome or Kawasaki disease among adolescent COVID-19 recipients.

Researchers analyzed reports made to VigiBase, which is run by the World Health Organization.

“Based on our results, close monitoring for these rare but serious inflammatory reactions after COVID-19 vaccination among adolescents until definitive causal relationship can be established,” the researchers wrote.

The study was published by the Journal of Korean Medical Science in its March edition.

Limitations include VigiBase receiving reports of problems, with some reports going unconfirmed.

Funding came from the South Korean government. One author reported receiving grants from pharmaceutical companies, including Pfizer.

Net Zero, The Digital Panopticon, & The Future Of Food

Problems After COVID-19 Vaccination More Prevalent Among Naturally Immune: Study

For-profit nursing homes are cutting corners on safety and draining resources with financial shenanigans − especially at midsize chains that dodge public scrutiny

Trump nearly derailed democracy once − here’s what to watch out for in reelection campaign

‘Excess Mortality Skyrocketed’: Tucker Carlson and Dr. Pierre Kory Unpack ‘Criminal’ COVID Response

Looking Back At COVID’s Authoritarian Regimes

MIPIM 2024 Reflects Mixed Feelings on CRE Recovery

Riley Gaines Explains How Women’s Sports Are Rigged To Promote The Trans Agenda

Health Officials: Man Dies From Bubonic Plague In New Mexico

Five Aerospace Investments to Buy as Wars Worsen Copy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex