Uncategorized

The Greenback is in Narrow Ranges to Start the Week

Overview: The foreign exchange market is quiet. The

Lunar New Year holiday shut most Asian markets. That, coupled with the light

news in Europe, have…

Share this:

Overview: The foreign exchange market is quiet. The Lunar New Year holiday shut most Asian markets. That, coupled with the light news in Europe, have served to keep the dollar in narrow ranges against the G10 currencies. The Swedish krona, Norwegian krone, and Japanese yen are posting minor gains against the greenback. The New Zealand dollar, which was strongest major currency last week (1.4%) is off by almost 0.5% today, making it the weakest today. RBNZ Governor Orr underscored the recent message that inflation is still too high (~4.7%). Emerging market currencies are narrowly mixed (+/-0.2%). Of note, India reports December industrial production and January CPI shortly.

The few equity markets in the Asia Pacific region that were not on holiday today, including Australia, India, and New Zealand slipped. Political uncertainty in Pakistan saw its stock market tagged for 3%. On the other hand, Europe's Stoxx 600 is trying to snap a three-day fall (less than 0.4%). Of note, real estate is the strongest sector today, rising by more than 1%. US index futures are trading firmly after new record-highs before the weekend. Benchmark 10-year bond yields are 3-6 bp lower in Europe. The 10-year US Treasury yield is off a basis point to around 4.16%. Gold is trading with a softer bias near $2020. Last week's low was around $2015. April WTI set this month's high before the weekend near $77.15. It is approaching the pre-weekend lows slightly below $76. Support is seen closer to $75.

Asia Pacific

The top two BOJ officials played down speculation that the central bank’s from negative interest rates will signal the start of a tightening cycle, and for good reason. First, inflation is already well off its peak and could easily fall below the 2% target before the April BOJ meeting that is widely expected to adjust policy. Second, despite a shortage of workers, (Japan's working age population peaked nearly 30 years ago) and the gradual opening to foreign workers, wage growth continues to lag inflation. Third, and related, domestic demand is soft. Toward the end of the week, Japan will publish its initial estimate of Q4 GDP. Consumption is likely to have recovered weakly from the contraction in Q2 and Q3 23. In the five years (20 quarters) before the pandemic, Japan's private consumption component in its GDP contracted by an average of 0.2% a quarter. Also, note that although the BOJ set the overnight target rate at minus 0.10%, the effective rate at the end of last week was 0.005%. Governor Ueda is determined to exit the negative interest rate policy for technical and strategic reasons. Arguably, there was windows of opportunity previously, where the macroeconomic setting was conducive to exiting the negative policy rate.

Most Asian markets were closed today, and China's mainland markets are closed all week for the Lunar New Year holiday. We expect that after the holiday, more efforts to support the economy and fight deflation will be forthcoming. Despite the stimulus in H2 23, the economy does not seem responsive. The assumption that the state-owned banks are just arms of the government is challenged by the same banks not fully passing on the PBOC's lower rates. The one- and five-year loan prime rates will be set on Feb 20. The same state-owned banks have also been reluctant to lend to the property market and enact the support measures Beijing unveiled in 2022. Lastly, consider the offshore yuan. It does not have to but with few exceptions respects the onshore band (2% for the dollar around the reference rate). Why? While the PBOC could intervene there, but when it does it is fairly clear. The last reference rate creates a band of ~CNH6.9640-CNH7.2485. Is it too much to suggest that the same mechanism that keeps the offshore yuan within the onshore band explains a great deal of how the PBOC manages the exchange rate? To paraphrase an old Chinese saying, "kill an occasional chicken to scare the monkeys."

The dollar edged a little closer to the JPY150 level ahead of the weekend (~JPY149.60) before settling virtually unchanged near JPY149.30. There are around $1.4 bln in options at JPY150 that expire tomorrow. During the six-week decline in the yen, speculators in the futures market have grown their net short yen position by more than 50% to 84k contracts (~$7 bln). The greenback is a narrow range of about a third of a yen above JPY149. The price action looks like a bullish pennant or flag, The Australian dollar's range last week, roughly $0.6470-$0.6540, is the key to the near-term direction. We favor an upside break and watching the possible bullish divergence with some of the momentum indicators but recognize the $0.6555-75 area to be an important hurdle. The Aussie eked out a small gain last week (~0.20%), the first of the year. Speculators in the futures markets added to their net short Australian dollar position for the fourth week in a row. It now stands at about 71.8k contracts (~$7.2 bln), up from 32.3k before the streak began. The Aussie is trading in about a fifth of a cent range above $0.6510.

Europe

The European economic calendar is light this week, and what there is, may be a sad reminder of the Europe's sad state. Eurostat will publish the details of Q4 23 GDP. The initial estimate had the regional economy stagnating after a 0.1% contraction in Q3. The dramatic 1.6% drop in Germany December industrial output (-3.0% year-over-year) underscores the lack of growth impulses to start the new year, and the weakness of what had been the European engine. At the same time, leadership is weak. Among the large members, Italy's Meloni, right-government seems among the strongest, and incidentally, the economy is doing better (but still not well). In 2022, Germany grew by 1.8%. Italy grew twice as fast. Last year, the German economy contracted by 0.3%, while Italy expanded by 0.7%. On the other hand, Italy's budget deficit was about 5.4% of GDP last year, while Germany's was less than 2.5%. Italy's 10-year premium over German narrowed to about 140 bp at the end of January, almost a two-year low, after rising to a nine-month peak last October over 200 bp. It is snapping back this month is near 155 bp. Italy's two-year premium peaked near 95 bp in the middle of last October and fell to almost 45 bp late last month. Last year's low was below 30 bp. It has jumped to about 65 bp now, the most since last November.

The Swiss franc was the strongest G10 currency in Q4 23 as dollar fell across the board. It rose 8.8% and so far, this year, the franc has fallen by about 3.9%. The dollar approached the (50%) retracement objective (~CHF0.8790). Above there is the 200-day moving average (~CHF0.8845) and the (61.8%) retracement near CHF0.8900. The euro is recovering from multiyear lows set against the franc in Q4 23 (~CHF0.9255). It traded up to almost CHF0.9475 last month but pulled back to support near CHF0.9300 earlier this month. There may be potential toward CHF0.9500-CHF0.9550. Switzerland reports January CPI tomorrow. The EU harmonized measure is expected to slip to 2.0% from 2.1%. Its own measure is seen easing to 1.6% (from 1.7%) and the core rate to 1.4% (from 1.5%).

The euro reached a six-day high late in thin Asia Pacific turnover near $1.0805. It was quickly sold to almost $1.0765 before finding a bid in early European turnover. It is the fourth session of higher highs. The pre-weekend low was almost $1.0760, and a break of the $1.0755 area would weaken the fragile technical tone. There are options for about $755 mln euros at $1.08 that expire today. There are large (1.4-1.5 bln euros) at $1.07 that expire tomorrow and Wednesday. Stiff resistance is seen in the $1.0830-40 area. Sterling recovered after breaking down at the start of last week (~$1.2520) but settled back into the $1.26-$1.28 trading range in the past three sessions. The $1.2640 area had capped but, like the euro, set a new six-day high before Europe opened and took sterling down to almost $1.2615. Before the weekend, sterling briefly frayed the $1.26 level. It is an important week for UK data, including the labor market report tomorrow and the January CPI on Wednesday. Soft data may encourage bringing forward the first rate cut to June from August.

America

Interest rates and expectations are a key force driving exchange rates. The market has gradually reduced the odds May rate cut to about 73% from 90% chance after the strong January jobs growth. It also scaled back the magnitude of Fed cuts by about 50 bp (to ~112 bp) in the past month. Tomorrow's CPI, more than last week's historic revisions, is a key input into the Fed's reaction function. Fed Chair Powell recently indicated the central bank was looking for more confirmation that inflation was on a sustained path back to its target. The January figures will give the Fed that. Ahead of it, the results of the NY Fed's inflation survey are of little consequence.

Canada reported a loss of full-time jobs in January for the second consecutive month. Wage growth slowed. The decline in the unemployment rate to 5.7% (from 5.8%) can be explained by the decline in the participation rate (65.3% vs. 65.4%). The takeaway is that the market boosted the chances of a June rate cut (to ~77% vs. ~67%). Despite the risk-on mood, which lifted the S&P 500 to a new record high, the Canadian dollar found no traction. It fell slightly for the first time in three sessions. The US dollar made session highs near midday in NY ahead of the weekend near CAD1.3480. The greenback is in a narrow 20-tick range above CAD1.3450 so fat today. Nearby resistance is seen in the CAD1.3500 area but the greenback has been turned back from the CAD1.3540 area three times. There are options for about $630 mln at CAD1.35 that expire tomorrow. The Mexican peso weakened after the central bank seemed to prepare the market for a rate cut as early as next month. However, it recovered and returned to pre-central bank levels near MXN17.08. It has edged low today to MXN17.0640. MXN17.00 was tested early last week. Around $580 mln of options expire there on Thursday. The US dollar reached BRL5.0175 at the start of last week. On the pullback, it found support near BRL4.95. It settled last week just above there. There is a band of technical support between BRL4.91 and BRL4.93.

gdp interest rates unemployment stimulus rate cut fed stimulus us treasury pandemic

Uncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

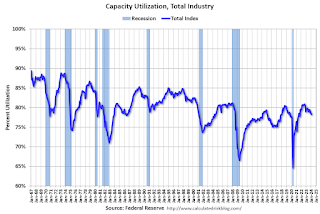

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Uncategorized

Southwest and United Airlines have bad news for passengers

Both airlines are facing the same problem, one that could lead to higher airfares and fewer flight options.

Share this:

{kind=link}

{kind=link}

Airlines operate in a market that's dictated by supply and demand: If more people want to fly a specific route than there are available seats, then tickets on those flights cost more.

That makes scheduling and predicting demand a huge part of maximizing revenue for airlines. There are, however, numerous factors that go into how airlines decide which flights to put on the schedule.

Related: Major airline faces Chapter 11 bankruptcy concerns

Every airport has only a certain number of gates, flight slots and runway capacity, limiting carriers' flexibility. That's why during times of high demand — like flights to Las Vegas during Super Bowl week — do not usually translate to airlines sending more planes to and from that destination.

Airlines generally do try to add capacity every year. That's become challenging as Boeing has struggled to keep up with demand for new airplanes. If you can't add airplanes, you can't grow your business. That's caused problems for the entire industry.

Every airline retires planes each year. In general, those get replaced by newer, better models that offer more efficiency and, in most cases, better passenger amenities.

If an airline can't get the planes it had hoped to add to its fleet in a given year, it can face capacity problems. And it's a problem that both Southwest Airlines (LUV) and United Airlines have addressed in a way that's inevitable but bad for passengers.

Image source: Kevin Dietsch/Getty Images

Southwest slows down its pilot hiring

In 2023, Southwest made a huge push to hire pilots. The airline lost thousands of pilots to retirement during the covid pandemic and it needed to replace them in order to build back to its 2019 capacity.

The airline successfully did that but will not continue that trend in 2024.

"Southwest plans to hire approximately 350 pilots this year, and no new-hire classes are scheduled after this month," Travel Weekly reported. "Last year, Southwest hired 1,916 pilots, according to pilot recruitment advisory firm Future & Active Pilot Advisors. The airline hired 1,140 pilots in 2022."

The slowdown in hiring directly relates to the airline expecting to grow capacity only in the low-single-digits percent in 2024.

"Moving into 2024, there is continued uncertainty around the timing of expected Boeing deliveries and the certification of the Max 7 aircraft. Our fleet plans remain nimble and currently differs from our contractual order book with Boeing," Southwest Airlines Chief Financial Officer Tammy Romo said during the airline's fourth-quarter-earnings call.

"We are planning for 79 aircraft deliveries this year and expect to retire roughly 45 700 and 4 800, resulting in a net expected increase of 30 aircraft this year."

That's very modest growth, which should not be enough of an increase in capacity to lower prices in any significant way.

United Airlines pauses pilot hiring

Boeing's (BA) struggles have had wide impact across the industry. United Airlines has also said it was going to pause hiring new pilots through the end of May.

United (UAL) Fight Operations Vice President Marc Champion explained the situation in a memo to the airline's staff.

"As you know, United has hundreds of new planes on order, and while we remain on path to be the fastest-growing airline in the industry, we just won't grow as fast as we thought we would in 2024 due to continued delays at Boeing," he said.

"For example, we had contractual deliveries for 80 Max 10s this year alone, but those aircraft aren't even certified yet, and it's impossible to know when they will arrive."

That's another blow to consumers hoping that multiple major carriers would grow capacity, putting pressure on fares. Until Boeing can get back on track, it's unlikely that competition between the large airlines will lead to lower fares.

In fact, it's possible that consumer demand will grow more than airline capacity which could push prices higher.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic stocks

Key shipping company files for Chapter 11 bankruptcy

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Part 1: Current State of the Housing Market; Overview for mid-March 2024

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International7 days ago

International7 days agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex