The Tax Cuts and Jobs Act of 2017 was the result of a political process constrained by anticipated effects on the long-run fiscal condition of the federal government. In order to bring the projected cost of the overall package down to politically acceptable levels, many of the tax cuts have an expiration date at the end of 2025. If Congress does not act, an array of taxes will automatically increase in 2026.

Perhaps it is a sign of the relative power of various constituencies, but the steep cut in the corporate tax rate is one of the few that do not expire in 2025. The corporate tax rate was cut from 35% to 21% and this was advertised as a “permanent” change. If Congress is gridlocked in 2025, the corporate tax will remain at 21%.

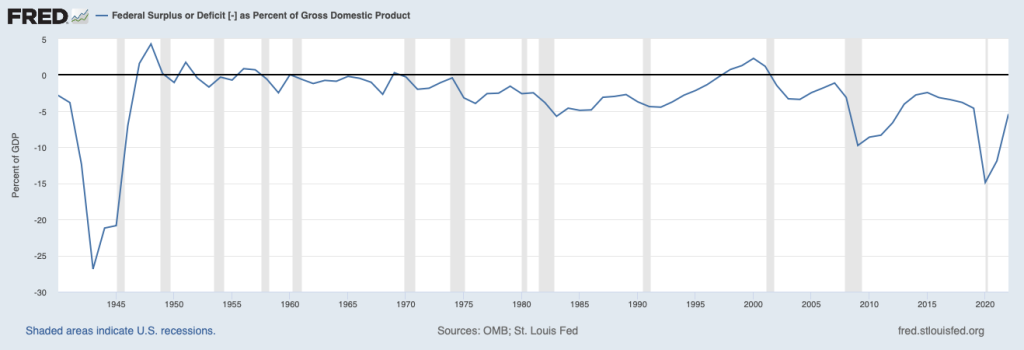

When it comes to tax policy, it is dangerous to consider anything to be “permanent” when the fiscal condition of the United States is in disarray. The pandemic brought about massive deficit spending and debt as a percentage of GDP has skyrocketed, as we can see from the charts below. The first chart shows the federal budget deficit as a percentage of GDP since 1940. The second chart shows total public debt as a percentage of GDP since 1966, the first year in the data series.

The Congressional Budget Office (CBO) projections for deficits and debt in the years to come are extremely disturbing, even with optimistic assumptions regarding the interest rates paid on the national debt. There is a massive gap between projected revenues and spending as far as the eye can see. The pandemic spending spree does not appear to be transitory; instead, it established a new and much higher baseline.

I should emphasize that the CBO is assuming that the “temporary” tax cuts will expire on schedule in 2025. If Congress wishes to extend any of those cuts, the outlook will be even worse than the chart indicates. One can observe that we have a spending problem, not a revenue problem, given that revenues are on trend while outlays have risen far above trend, but few politicians seem willing to even propose serious cuts.

I do not regard the “permanent” status of the corporate tax rate to be of much comfort because it will be politically difficult to maintain a 21% rate if the other provisions of the 2017 legislation are allowed to expire in 2025. Most investors seem oblivious to this potential headwind that could start blowing with a vengeance in the near future. Markets are forward looking and if it looks like the corporate tax rate might rise in 2026, markets will reflect this well ahead of time, perhaps starting next year.

Many companies experienced a strong tailwind when the corporate tax cut went into effect in 2018. For example, look at the effective tax rate of Dollar General, the subject of an article I wrote earlier this week:

Source: Dollar General 10-Q and 10-K Reports

It is obvious that Dollar General benefited from the 14% cut in the federal tax rate and would be harmed by a tax increase. It is unlikely that the corporate tax rate will return to 35% but we should note that President Biden’s fiscal 2024 budget called for the rate to rise to 28%. Obviously, this will not happen with the current composition of Congress, but it indicates that there could be upward pressure in the future.

The political landscape is constantly evolving. One unmistakable shift in recent years is that the Republican Party has moved in a “populist” direction, a major change from the party’s traditional “pro business” philosophy. From a political perspective, the GOP could very well be amenable to an increase in the corporate tax rate in exchange for retaining tax cuts that have more populist appeal. Therefore, I think that the corporate tax rate is not just a function of which party is in power.

Investors have mostly shrugged off the strong headwinds of rising interest rates over the past year which seems odd given that it is now possible to purchase a ten year treasury note yielding 4.3% or a ten year TIPS yielding 2% + CPI. As Warren Buffett has said on more than one occasion, interest rates act like “financial gravity” when it comes to the valuation of all assets. If Uncle Sam, our “silent partner” as investors, decides that he will claim an additional 7% of corporate profits in a few years, that will represent yet another headwind that investors must account for.

The stereotype of value investors is that we are not supposed to consider the macroeconomy. It’s one thing to avoid making investments based on projections of the CPI in September or GDP in the third quarter. But we should be aware of longer term trends related to taxes and interest rates, particularly when it comes to our central expectation for the returns of stocks over the next decade.

Articles

Warren Buffett’s Green Cash Washes Over Coal Country by Scott Patterson, September 5, 2023. The “Inflation Reduction Act” included major incentives for clean energy projects. Berkshire Hathaway Energy has a long history of responding to tax incentives. This article reports on a project in West Virginia involving BHE as well as Precision Castparts, another Berkshire subsidiary. These projects apparently came together without Warren Buffett’s direct involvement. “I’m glad it worked out,” Buffett told The Wall Street Journal. “I can claim no personal credit.”(WSJ)

The Real Story of Elon Musk’s Twitter Takeover by Walter Isaacson, September 2, 2023. In an excerpt from his biography of Elon Musk to be released next week, Walter Isaacson provides some behind-the-scenes reporting on the Twitter acquisition. “The way that Musk blustered into buying Twitter and renaming it X was a harbinger of the way he now runs it: impulsively and irreverently. It is an addictive playground for him. It has many of the attributes of a school yard, including taunting and bullying. But in the case of Twitter, the clever kids win followers; they don’t get pushed down the steps and beaten, like Musk was as a kid. Owning it would allow him to become king of the school yard.”(WSJ)

The Rise and Fall of ESPN’s Leverage by Ben Thompson, September 5, 2023. Disney’s stock has been beaten down severely in recent months. One of the difficulties in analyzing the company has to do with the long term future of ESPN, a crown jewel that has seen its moat slowly erode in recent years. I found this article’s discussion of ESPN’s history and current competitive position very useful. (Stratechery)

Initial estimates point to Hurricane Idalia insured loss of below $10 billion by Saumya Jain, August 31, 2023. “The Big Bend area of the Florida coast where Idalia made landfall is far less densely populated than the region devastated by Hurricane Ian last year. In contrast to Hurricane Idalia, there were approximately 1 million people within 30 miles of landfall for Ian, while there were about 38,000 people within that distance for Idalia, according to an AccuWeather report.”(Reinsurance News)

These 38 Reading Rules Changed My Life by Ryan Holiday, September 6, 2023. I agree with almost everything in this article, especially the benefits of reading older books, taking notes, and turning to books rather than the mainstream media to better understand current events. I continue to have trouble abandoning “bad” books before I finish them. Hope springs eternal, I suppose. (RyanHoliday.net)

Never Look Down the Road Not Taken by Nick Maggiulli, September 5, 2023. Attempting to replay history is an exercise fraught with peril. This article reminds me of the article I wrote about selling Apple stock in 2001. (Of Dollars and Data)

Respect and Admiration by Morgan Housel, September 6, 2023. This is a good reminder that buying expensive things to impress people is pointless vanity. Respect is not driven by showy displays but by innate qualities. (Collaborative Fund)

Podcasts

Nvidia: The Dawn of the AI Era, September 5, 2023. 2 hours, 54 minutes. This is an interesting overview of the development of AI over the past decade. “Over the past 18 months Nvidia has weathered one of the steepest stock crashes in history ($500B+ market cap wiped away peak-to-trough!). And, it has of course also experienced an even more fantastical rise — becoming the platform that’s powering the emergence of perhaps a new form of intelligence itself… and in the process becoming a trillion-dollar company.” (Acquired)

Where Does Your Return Come From: Yield, Growth, and Multiple Expansion, September 4, 2023, 32 minutes. This discussion breaks down the sources of returns on an investment. It’s important to understand where you expect your returns to come from when considering a new investment as well as where your returns have actually come from when evaluating current and past investments. (Focused Compounding)

Good vs. bad science: how to read and understand scientific studies, September 4, 2023. 1 hour, 50 minutes. Mainstream media articles covering scientific studies cannot possibly discuss all of the complexities that one needs to understand in order to separate signal from noise. In this long and detailed podcast, Peter Attia explains his process for reading scientific papers, focusing on how studies and clinical trials work. He delves into topics including differentiating relative risk from absolute risk and how to determine the statistical significance of study results. (The Drive)

Berkshire’s Beginnings w/Jacob McDonough, August 31, 2023. 1 hour, 25 minutes. “In 1962, Warren Buffett began purchasing shares in Berkshire Hathaway, a struggling textile maker in the midst of a decline. Ironically, in hindsight, Buffett has said that purchasing Berkshire Hathaway in the first place was one of his worst decisions ever. In this episode, you’ll learn how Buffett was able to turn the business around and make its way to eventually becoming worth nearly $800 billion in 2023.”(We Study Billionaires)

Why Doomberg left Twitter (okay, X) to go all in on Substack, September 4, 2023. “If the new owner of Twitter had not specifically and proactively throttled all Substack authors, we would almost certainly still be on the platform. It’s his private property. He can run his property in any way that he sees fit… but the primary driver and the motivation to leave the platform was because of the impact on all of our friends.”(On Substack)

The Lifecycle of Greed and Fear, August 31, 2012. 12 minutes. “All greed starts with an innocent idea: that you are right, deserve to be right, and are owed something for the efforts you put into establishing your beliefs and opinions. It’s a reasonable feeling. But it sets off a chain reaction that leads to an inevitable boom-and-bust cycle. This episode explores one of the most important topics in investing: the lifecycle of greed and fear, and why it cannot, and will not, ever go away.”(The Morgan Housel Podcast)

Jimmy Buffett

No matter the weather outside, you can always get a virtual ticket to the tropics. Jimmy Buffett, who died on September 1, invented his own tropical sound that transcended country and rock and earned the loyalty of generations of fans.

Jimmy Buffett and Warren Buffett were not related but they were friends who referred to each other as “Cousin Warren” and “Cousin Jimmy”. Jimmy Buffett was a Berkshire Hathaway shareholder for many decades and was known to appear at annual meetings and hold impromptu performances for shareholders.

I don’t think that Fruitcakes is one of Jimmy Buffett’s best known hits but I’ve always liked it because it says something about our flawed human condition. RIP.

Evolution Valley, Kings Canyon National Park, September 7, 2013

Copyright, Disclosures, and Privacy Information

Nothing in this article constitutes investment advice and all content is subject to the copyright and disclaimer policy of The Rational Walk LLC. The Rational Walk is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com.

Mandating COVID-19 vaccination was a mistake due to ethical and other concerns, a top government doctor warned Dr. Anthony Fauci after Dr. Fauci promoted mass vaccination.

“Coercing or forcing people to take a vaccine can have negative consequences from a biological, sociological, psychological, economical, and ethical standpoint and is not worth the cost even if the vaccine is 100% safe,” Dr. Matthew Memoli, director of the Laboratory of Infectious Diseases clinical studies unit at the U.S. National Institute of Allergy and Infectious Diseases (NIAID), told Dr. Fauci in an email.

“A more prudent approach that considers these issues would be to focus our efforts on those at high risk of severe disease and death, such as the elderly and obese, and do not push vaccination on the young and healthy any further.”

Employing that strategy would help prevent loss of public trust and political capital, Dr. Memoli said.

The email was sent on July 30, 2021, after Dr. Fauci, director of the NIAID, claimed that communities would be safer if more people received one of the COVID-19 vaccines and that mass vaccination would lead to the end of the COVID-19 pandemic.

“We’re on a really good track now to really crush this outbreak, and the more people we get vaccinated, the more assuredness that we’re going to have that we’re going to be able to do that,” Dr. Fauci said on CNN the month prior.

Dr. Memoli, who has studied influenza vaccination for years, disagreed, telling Dr. Fauci that research in the field has indicated yearly shots sometimes drive the evolution of influenza.

Vaccinating people who have not been infected with COVID-19, he said, could potentially impact the evolution of the virus that causes COVID-19 in unexpected ways.

“At best what we are doing with mandated mass vaccination does nothing and the variants emerge evading immunity anyway as they would have without the vaccine,” Dr. Memoli wrote. “At worst it drives evolution of the virus in a way that is different from nature and possibly detrimental, prolonging the pandemic or causing more morbidity and mortality than it should.”

The vaccination strategy was flawed because it relied on a single antigen, introducing immunity that only lasted for a certain period of time, Dr. Memoli said. When the immunity weakened, the virus was given an opportunity to evolve.

Some other experts, including virologist Geert Vanden Bossche, have offered similar views. Others in the scientific community, such as U.S. Centers for Disease Control and Prevention scientists, say vaccination prevents virus evolution, though the agency has acknowledged it doesn’t have records supporting its position.

Other Messages

Dr. Memoli sent the email to Dr. Fauci and two other top NIAID officials, Drs. Hugh Auchincloss and Clifford Lane. The message was first reported by the Wall Street Journal, though the publication did not publish the message. The Epoch Times obtained the email and 199 other pages of Dr. Memoli’s emails through a Freedom of Information Act request. There were no indications that Dr. Fauci ever responded to Dr. Memoli.

Later in 2021, the NIAID’s parent agency, the U.S. National Institutes of Health (NIH), and all other federal government agencies began requiring COVID-19 vaccination, under direction from President Joe Biden.

In other messages, Dr. Memoli said the mandates were unethical and that he was hopeful legal cases brought against the mandates would ultimately let people “make their own healthcare decisions.”

“I am certainly doing everything in my power to influence that,” he wrote on Nov. 2, 2021, to an unknown recipient. Dr. Memoli also disclosed that both he and his wife had applied for exemptions from the mandates imposed by the NIH and his wife’s employer. While her request had been granted, his had not as of yet, Dr. Memoli said. It’s not clear if it ever was.

According to Dr. Memoli, officials had not gone over the bioethics of the mandates. He wrote to the NIH’s Department of Bioethics, pointing out that the protection from the vaccines waned over time, that the shots can cause serious health issues such as myocarditis, or heart inflammation, and that vaccinated people were just as likely to spread COVID-19 as unvaccinated people.

He cited multiple studies in his emails, including one that found a resurgence of COVID-19 cases in a California health care system despite a high rate of vaccination and another that showed transmission rates were similar among the vaccinated and unvaccinated.

Dr. Memoli said he was “particularly interested in the bioethics of a mandate when the vaccine doesn’t have the ability to stop spread of the disease, which is the purpose of the mandate.”

The message led to Dr. Memoli speaking during an NIH event in December 2021, several weeks after he went public with his concerns about mandating vaccines.

“Vaccine mandates should be rare and considered only with a strong justification,” Dr. Memoli said in the debate. He suggested that the justification was not there for COVID-19 vaccines, given their fleeting effectiveness.

Julie Ledgerwood, another NIAID official who also spoke at the event, said that the vaccines were highly effective and that the side effects that had been detected were not significant. She did acknowledge that vaccinated people needed boosters after a period of time.

The NIH, and many other government agencies, removed their mandates in 2023 with the end of the COVID-19 public health emergency.

A request for comment from Dr. Fauci was not returned. Dr. Memoli told The Epoch Times in an email he was “happy to answer any questions you have” but that he needed clearance from the NIAID’s media office. That office then refused to give clearance.

Dr. Jay Bhattacharya, a professor of health policy at Stanford University, said that Dr. Memoli showed bravery when he warned Dr. Fauci against mandates.

“Those mandates have done more to demolish public trust in public health than any single action by public health officials in my professional career, including diminishing public trust in all vaccines.” Dr. Bhattacharya, a frequent critic of the U.S. response to COVID-19, told The Epoch Times via email. “It was risky for Dr. Memoli to speak publicly since he works at the NIH, and the culture of the NIH punishes those who cross powerful scientific bureaucrats like Dr. Fauci or his former boss, Dr. Francis Collins.”

President Joe Biden claimed that COVID vaccines are now helping cancer patients during his State of the Union address on March 7, but it was a response on Truth Social from former President Donald Trump that drew the ire of independent presidential candidate Robert F. Kennedy Jr.

During the address, President Biden said: “The pandemic no longer controls our lives. The vaccines that saved us from COVID are now being used to help beat cancer, turning setback into comeback. That’s what America does.”

President Trump wrote: “The Pandemic no longer controls our lives. The VACCINES that saved us from COVID are now being used to help beat cancer—turning setback into comeback. YOU’RE WELCOME JOE. NINE-MONTH APPROVAL TIME VS. 12 YEARS THAT IT WOULD HAVE TAKEN YOU.”

An outspoken critic of President Trump’s COVID response, and the Operation Warp Speed program that escalated the availability of COVID vaccines, Mr. Kennedy said on X, formerly known as Twitter, that “Donald Trump clearly hasn’t learned from his COVID-era mistakes.”

“He fails to recognize how ineffective his warp speed vaccine is as the ninth shot is being recommended to seniors. Even more troubling is the documented harm being caused by the shot to so many innocent children and adults who are suffering myocarditis, pericarditis, and brain inflammation,” Mr. Kennedy remarked.

“This has been confirmed by a CDC-funded study of 99 million people. Instead of bragging about its speedy approval, we should be honestly and transparently debating the abundant evidence that this vaccine may have caused more harm than good.

“I look forward to debating both Trump and Biden on Sept. 16 in San Marcos, Texas.”

Mr. Kennedy announced in April 2023 that he would challenge President Biden for the 2024 Democratic Party presidential nomination before declaring his run as an independent last October, claiming that the Democrat National Committee was “rigging the primary.”

Since the early stages of his campaign, Mr. Kennedy has generated more support than pundits expected from conservatives, moderates, and independents resulting in speculation that he could take votes away from President Trump.

Many Republicans continue to seek a reckoning over the government-imposed pandemic lockdowns and vaccine mandates.

President Trump’s defense of Operation Warp Speed, the program he rolled out in May 2020 to spur the development and distribution of COVID-19 vaccines amid the pandemic, remains a sticking point for some of his supporters.

Operation Warp Speed featured a partnership between the government, the military, and the private sector, with the government paying for millions of vaccine doses to be produced.

President Trump released a statement in March 2021 saying: “I hope everyone remembers when they’re getting the COVID-19 Vaccine, that if I wasn’t President, you wouldn’t be getting that beautiful ‘shot’ for 5 years, at best, and probably wouldn’t be getting it at all. I hope everyone remembers!”

President Trump said about the COVID-19 vaccine in an interview on Fox News in March 2021: “It works incredibly well. Ninety-five percent, maybe even more than that. I would recommend it, and I would recommend it to a lot of people that don’t want to get it and a lot of those people voted for me, frankly.

“But again, we have our freedoms and we have to live by that and I agree with that also. But it’s a great vaccine, it’s a safe vaccine, and it’s something that works.”

On many occasions, President Trump has said that he is not in favor of vaccine mandates.

An environmental attorney, Mr. Kennedy founded Children’s Health Defense, a nonprofit that aims to end childhood health epidemics by promoting vaccine safeguards, among other initiatives.

Last year, Mr. Kennedy told podcaster Joe Rogan that ivermectin was suppressed by the FDA so that the COVID-19 vaccines could be granted emergency use authorization.

He has criticized Big Pharma, vaccine safety, and government mandates for years.

Since launching his presidential campaign, Mr. Kennedy has made his stances on the COVID-19 vaccines, and vaccines in general, a frequent talking point.

“I would argue that the science is very clear right now that they [vaccines] caused a lot more problems than they averted,” Mr. Kennedy said on Piers Morgan Uncensored last April.

“And if you look at the countries that did not vaccinate, they had the lowest death rates, they had the lowest COVID and infection rates.”

Additional data show a “direct correlation” between excess deaths and high vaccination rates in developed countries, he said.

President Trump and Mr. Kennedy have similar views on topics like protecting the U.S.-Mexico border and ending the Russia-Ukraine war.

COVID-19 is the topic where Mr. Kennedy and President Trump seem to differ the most.

Former President Donald Trump intended to “drain the swamp” when he took office in 2017, but he was “intimidated by bureaucrats” at federal agencies and did not accomplish that objective, Mr. Kennedy said on Feb. 5.

Speaking at a voter rally in Tucson, where he collected signatures to get on the Arizona ballot, the independent presidential candidate said President Trump was “earnest” when he vowed to “drain the swamp,” but it was “business as usual” during his term.

John Bolton, who President Trump appointed as a national security adviser, is “the template for a swamp creature,” Mr. Kennedy said.

Scott Gottlieb, who President Trump named to run the FDA, “was Pfizer’s business partner” and eventually returned to Pfizer, Mr. Kennedy said.

Mr. Kennedy said that President Trump had more lobbyists running federal agencies than any president in U.S. history.

“You can’t reform them when you’ve got the swamp creatures running them, and I’m not going to do that. I’m going to do something different,” Mr. Kennedy said.

During the COVID-19 pandemic, President Trump “did not ask the questions that he should have,” he believes.

President Trump “knew that lockdowns were wrong” and then “agreed to lockdowns,” Mr. Kennedy said.

He also “knew that hydroxychloroquine worked, he said it,” Mr. Kennedy explained, adding that he was eventually “rolled over” by Dr. Anthony Fauci and his advisers.

MaryJo Perry, a longtime advocate for vaccine choice and a Trump supporter, thinks votes will be at a premium come Election Day, particularly because the independent and third-party field is becoming more competitive.

Ms. Perry, president of Mississippi Parents for Vaccine Rights, believes advocates for medical freedom could determine who is ultimately president.

She believes that Mr. Kennedy is “pulling votes from Trump” because of the former president’s stance on the vaccines.

“People care about medical freedom. It’s an important issue here in Mississippi, and across the country,” Ms. Perry told The Epoch Times.

“Trump should admit he was wrong about Operation Warp Speed and that COVID vaccines have been dangerous. That would make a difference among people he has offended.”

President Trump won’t lose enough votes to Mr. Kennedy about Operation Warp Speed and COVID vaccines to have a significant impact on the election, Ohio Republican strategist Wes Farno told The Epoch Times.

President Trump won in Ohio by eight percentage points in both 2016 and 2020. The Ohio Republican Party endorsed President Trump for the nomination in 2024.

“The positives of a Trump presidency far outweigh the negatives,” Mr. Farno said. “People are more concerned about their wallet and the economy.

“They are asking themselves if they were better off during President Trump’s term compared to since President Biden took office. The answer to that question is obvious because many Americans are struggling to afford groceries, gas, mortgages, and rent payments.

“America needs President Trump.”

Multiple national polls back Mr. Farno’s view.

As of March 6, the RealClearPolitics average of polls indicates that President Trump has 41.8 percent support in a five-way race that includes President Biden (38.4 percent), Mr. Kennedy (12.7 percent), independent Cornel West (2.6 percent), and Green Party nominee Jill Stein (1.7 percent).

A Pew Research Center study conducted among 10,133 U.S. adults from Feb. 7 to Feb. 11 showed that Democrats and Democrat-leaning independents (42 percent) are more likely than Republicans and GOP-leaning independents (15 percent) to say they have received an updated COVID vaccine.

The poll also reported that just 28 percent of adults say they have received the updated COVID inoculation.

The peer-reviewed multinational study of more than 99 million vaccinated people that Mr. Kennedy referenced in his X post on March 7 was published in the Vaccine journal on Feb. 12.

It aimed to evaluate the risk of 13 adverse events of special interest (AESI) following COVID-19 vaccination. The AESIs spanned three categories—neurological, hematologic (blood), and cardiovascular.

The study reviewed data collected from more than 99 million vaccinated people from eight nations—Argentina, Australia, Canada, Denmark, Finland, France, New Zealand, and Scotland—looking at risks up to 42 days after getting the shots.

Three vaccines—Pfizer and Moderna’s mRNA vaccines as well as AstraZeneca’s viral vector jab—were examined in the study.

Researchers found higher-than-expected cases that they deemed met the threshold to be potential safety signals for multiple AESIs, including for Guillain-Barre syndrome (GBS), cerebral venous sinus thrombosis (CVST), myocarditis, and pericarditis.

A safety signal refers to information that could suggest a potential risk or harm that may be associated with a medical product.

The study identified higher incidences of neurological, cardiovascular, and blood disorder complications than what the researchers expected.

President Trump’s role in Operation Warp Speed, and his continued praise of the COVID vaccine, remains a concern for some voters, including those who still support him.

Krista Cobb is a 40-year-old mother in western Ohio. She voted for President Trump in 2020 and said she would cast her vote for him this November, but she was stunned when she saw his response to President Biden about the COVID-19 vaccine during the State of the Union address.

“I love President Trump and support his policies, but at this point, he has to know they [advisers and health officials] lied about the shot,” Ms. Cobb told The Epoch Times.

“If he continues to promote it, especially after all of the hearings they’ve had about it in Congress, the side effects, and cover-ups on Capitol Hill, at what point does he become the same as the people who have lied?” Ms. Cobb added.

“I think he should distance himself from talk about Operation Warp Speed and even admit that he was wrong—that the vaccines have not had the impact he was told they would have. If he did that, people would respect him even more.”

Mathematicians use AI to identify emerging COVID-19 variants

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants…

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

Scientists at The Universities of Manchester and Oxford have developed an AI framework that can identify and track new and concerning COVID-19 variants and could help with other infections in the future.

The framework combines dimension reduction techniques and a new explainable clustering algorithm called CLASSIX, developed by mathematicians at The University of Manchester. This enables the quick identification of groups of viral genomes that might present a risk in the future from huge volumes of data.

The study, presented this week in the journal PNAS, could support traditional methods of tracking viral evolution, such as phylogenetic analysis, which currently require extensive manual curation.

Roberto Cahuantzi, a researcher at The University of Manchester and first and corresponding author of the paper, said: “Since the emergence of COVID-19, we have seen multiple waves of new variants, heightened transmissibility, evasion of immune responses, and increased severity of illness.

“Scientists are now intensifying efforts to pinpoint these worrying new variants, such as alpha, delta and omicron, at the earliest stages of their emergence. If we can find a way to do this quickly and efficiently, it will enable us to be more proactive in our response, such as tailored vaccine development and may even enable us to eliminate the variants before they become established.”

Like many other RNA viruses, COVID-19 has a high mutation rate and short time between generations meaning it evolves extremely rapidly. This means identifying new strains that are likely to be problematic in the future requires considerable effort.

Currently, there are almost 16 million sequences available on the GISAID database (the Global Initiative on Sharing All Influenza Data), which provides access to genomic data of influenza viruses.

Mapping the evolution and history of all COVID-19 genomes from this data is currently done using extremely large amounts of computer and human time.

The described method allows automation of such tasks. The researchers processed 5.7 million high-coverage sequences in only one to two days on a standard modern laptop; this would not be possible for existing methods, putting identification of concerning pathogen strains in the hands of more researchers due to reduced resource needs.

Thomas House, Professor of Mathematical Sciences at The University of Manchester, said: “The unprecedented amount of genetic data generated during the pandemic demands improvements to our methods to analyse it thoroughly. The data is continuing to grow rapidly but without showing a benefit to curating this data, there is a risk that it will be removed or deleted.

“We know that human expert time is limited, so our approach should not replace the work of humans all together but work alongside them to enable the job to be done much quicker and free our experts for other vital developments.”

The proposed method works by breaking down genetic sequences of the COVID-19 virus into smaller “words” (called 3-mers) represented as numbers by counting them. Then, it groups similar sequences together based on their word patterns using machine learning techniques.

Stefan Güttel, Professor of Applied Mathematics at the University of Manchester, said: “The clustering algorithm CLASSIX we developed is much less computationally demanding than traditional methods and is fully explainable, meaning that it provides textual and visual explanations of the computed clusters.”

Roberto Cahuantzi added: “Our analysis serves as a proof of concept, demonstrating the potential use of machine learning methods as an alert tool for the early discovery of emerging major variants without relying on the need to generate phylogenies.

“Whilst phylogenetics remains the ‘gold standard’ for understanding the viral ancestry, these machine learning methods can accommodate several orders of magnitude more sequences than the current phylogenetic methods and at a low computational cost.”

Journal

Proceedings of the National Academy of Sciences

DOI

10.1073/pnas.2317284121

Article Title

Unsupervised identification of significant lineages of SARS-CoV-2 through scalable machine learning methods

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}