Stimulus money in the US, but Equity markets responded with a bear market rally

Stimulus money in the US, but Equity markets responded with a bear market rally

Share this:

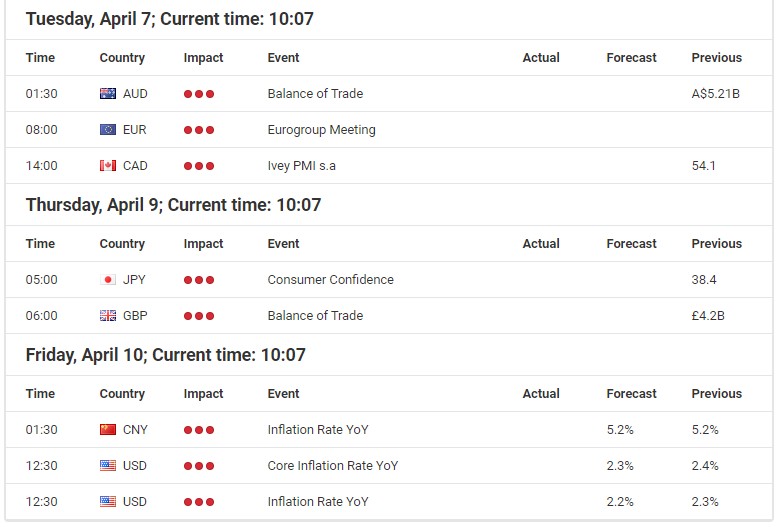

Source: Economic Events Calendar April 6 – 10, 2020 - Admiral Markets' Forex Calendar

DAX30 CFD

While the DAX30 CFD was stable over the course of the last week of trading, the German index failed to recapture the important level of 10,000 points.

As we wrote in our last weekly market outlook, chances seem high that the recent correction was nothing more than a bear market rally, and DAX bulls should be extremely cautious in regards to Long engagements.

In fact, the main driver for the run higher in Equities (especially US Equities) at the end of March (and thus the end of the first quarter) could be a necessary rebalancing of the portfolios of money managers with the need to step up their Equity exposure, and the selling of bonds in order to maintain their allocation targets.

Now, the problem: once this "rebalancing" demand diminishes and with the failure to recapture the mark of 10,000 points, bears are still in control of the price action, and the advantage remains clearly on their side.

That said, a re-test of the region around 8,000 points, and probably a drop even lower, stays a serious option, especially if the situation around the Coronavirus in the US darkens again, with no hints of a lift of the current shutdown with unforeseeable negative consequences for the US and the global economy materializes again.

This is especially true if the DAX30 CFD drops sustainably back below 9,150/200 points again.

Above that level, another attempt to sustainably recapture and rise even more significantly above 10,000 points stays on the table:

Source: Admiral Markets MT5 with MT5-SE Add-on DAX30 CFD Daily chart (between December 17, 2018, to April 3, 2020). Accessed: April 3, 2020, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the DAX30 CFD increased by 9.56%, in 2016, it increased by 6.87%, in 2017, it increased by 12.51%, in 2018, it fell by 18.26%, in 2019, it increased by 26.44% meaning that after five years, it was up by 34.2%.

Check out Admiral Markets' most competitive conditions on the DAX30 CFD and start trading on the DAX30 CFD with a low 0.8 point spread offering during the main Xetra trading hours!

US Dollar

Over the last week of trading, the US dollar Index Future was stable, finding support against the region of 99.00 points.

While this might surprise at first glance, especially when considering the significant drop below 1% in 10-year-US-Treasury yields and the massive monetary stimulus delivered from the US central bank Fed with pumping up their balance sheet to over 5.8 trillion USD, but it seems to underpin the risk of a new wave of de-leveraging hitting global financial markets which will naturally result in high demand for the US dollar given the global USD shortage.

That in mind, the re-test of the region of around 99.00 points can certainly be interpreted as a long-trigger for another stint higher, around 105.00 points.

Mid- to long-term, the massive government spending and given the massive monetary stimulus from the Fed, leaves us with massive USD-scepticism and short-engagements in the Greenback should be attractive from a risk-reward perspective.

Source: Barchart - U.S Dollar Index - Weekly Nearest OHLC Chart (between January 2017 to April 2020). Accessed: April 3, 2020, at 10:00 PM GMT

Don't forget to register for the weekly "Trading Spotlight" webinar with presenters including Jens Klatt, every Monday, Wednesday and Friday at 2pm London time! It's your opportunity to follow Jens and others as they explore the weekly market outlook in detail, so don't miss out!

Euro

Given the recent price action in the Euro and here especially the EUR/USD, volatility stays high, but the overall picture hasn't substantially changed over the last week of trading.

After the EUR/USD pushed back above 1.1100, the currency pair couldn't stabilise there, instead, it dropped clearly back below 1.1000 and we'd stay very cautious in regards to "buying the dip".

We still consider the short-term picture in the EUR/USD bearish, see a serious chance of a re-test, probably even a drop below the current yearly lows around 1.0600/30.

As pointed out in the USD paragraph above, this expectation mainly results out of the ongoing shortage of USD liquidity in European markets.

That said, and if the ECB starts to use the reinstated swap lines from the Fed again, given a next wave of "panic liquidation", a stronger US dollar should be imagined could result in a nee wave of stronger selling pressure in the EUR/USD.

And despite the massive stimulus from the Fed in addition to the massive government spending, our Euro outlook with further bullish potential would only be given if EU governments deliver clear signs towards any kind of unity and sending a clear signal in regards to supportive packages of the European economy (e.g. like a EU coronavirus rescue fund, Euro bonds, Coronabonds, etc.)

Technically, a break below 1.0600/30 makes a further drop in the EUR/USD as low as 1.0500 and probably even lower a serious option.

A next wave of bullish momentum could drive the EUR/USD probably as high as 1.1200/30, but should be carefully reviewed in terms of sustainability:

Source: Admiral Markets MT5 with MT5-SE Add-on EURUSD Daily chart (between February 4, 2019, to April 3, 2020). Accessed: April 3, 2020, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of the EUR/USD fell by 10.2%, in 2016, it fell by 3.2%, in 2017, it increased by 13.92%, 2018, it fell by 4.4%, 2019, it fell by 2.2%, meaning that after five years, it was down by 7.3%.

JPY

The USD/JPY continued to trade lower after its sharp bearish stint on March 26-27, resulting in a sustainable drop below 108.50/109.00.

Driver for the continuation on the downside was potentially the drop in 10-year-US Treasury yields.

And as we expect a new risk-off wave to hit global financial markets which might, under "normal" circumstances, drive the USD/JPY even lower, letting the currency pair eye the region around 105.00. But such a risk-off wave has the potential to result in a sharp USD/JPY reversal.

As pointed out in our USD section above, we consider such a risk-off wave going hand in hand with an increasing demand for the US dollar given the global USD shortage where the usage of the re-installed swap lines of the Fed from the BoJ could result in an ongoing squeeze higher.

While we certainly need to wait if such a wave of risk-off really hits the markets and will really result in a strong USD demand, a test, probably even break of the region around 112.00/30 would be an option.

As already pointed out, further bearish momentum brings a test of the region around 105.00 into play:

Source: Admiral Markets MT5 with MT5-SE Add-on USD/JPY Daily chart (between February 11, 2019, to April 3, 2020). Accessed: April 3, 2020, at 10:00pm GMT

In 2015, the value of the USD/JPY increased by 0.5%, in 2016, it fell by 2.8%, in 2017, it fell by 3.6%, in 2018, it fell by 2.7%, in 2019, it fell by 0.85%, meaning that after five years, it was down by 9.2%.

Gold

The technical picture in Gold stays tense: after finding a (short-term) bottom around 1,440/450 USD and the push back above 1,600 USD given the massive monetary stimulus from the Fed on March 23, and the precious metal dropped back below 1,600 USD over the course of the last week of trading.

As pointed out in our USD paragraph above, we consider chances at least elevated, that a new wave of de-leveraging hitting global financial markets stays a serious option and will naturally not only result in high demand for the US dollar given the global USD shortage, but potentially also in a new wave of aggressive selling the precious metal.

This can also be seen in the still wider than usual spread between physical and paper Gold out of the massive short-supply in regards to physical Gold, resulting out of feared (Coronavirus) shutdowns of precious metal refineries.

That disruption in mind and given the massive steps from the Fed in addition to the massive deficit spending from the US government, to be Long Gold mid- to long-term stays an interesting bet from a risk-reward perspective, but short-term a sharper drop in Gold could happen at any time in our opinion.

Technically the key-support can still be found around 1,440/450, above that level another push up to 1,700 USD stays realistic.

Nevertheless, another "liquidation wave" could bring a short-term drop below 1,440/450 USD into play which would technically darken the picture, activating 1,250/260 USD as a first target:

Source: Admiral Markets MT5 with MT5-SE Add-on Gold Daily chart (between January 4, 2019, to April 3, 2020). Accessed: April 3, 2020, at 10:00pm GMT - Please note: Past performance is not a reliable indicator of future results, or future performance.

In 2015, the value of Gold fell by 10.4%, in 2016, it increased by 8.1%, in 2017, it increased by 13.1%, in 2018, it fell by 1.6%, in 2019, it increased by 18.9%, meaning that after five years, it was up by 28%.

Discover the world's #1 multi-asset platform

Admiral Markets offers professional traders the ability to trade with a custom, upgraded version of MetaTrader 5, allowing you to experience trading at a significantly higher, more rewarding level. Experience benefits such as the addition of the Market Heat Map, so you can compare various currency pairs to see which ones might be lucrative investments, access real-time trading data, and so much more. Click the banner below to start your FREE download of MT5 Supreme Edition!

Disclaimer: The given data provides additional information regarding all analysis, estimates, prognosis, forecasts or other similar assessments or information (hereinafter "Analysis") published on the website of Admiral Markets. Before making any investment decisions please pay close attention to the following:

- This is a marketing communication. The analysis is published for informative purposes only and are in no way to be construed as investment advice or recommendation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research, and that it is not subject to any prohibition on dealing ahead of the dissemination of investment research.

- Any investment decision is made by each client alone whereas Admiral Markets shall not be responsible for any loss or damage arising from any such decision, whether or not based on the Analysis.

- Each of the Analysis is prepared by an independent analyst (Jens Klatt, Professional Trader and Analyst, hereinafter "Author") based on the Author's personal estimations.

- To ensure that the interests of the clients would be protected and objectivity of the Analysis would not be damaged Admiral Markets has established relevant internal procedures for prevention and management of conflicts of interest.

- Whilst every reasonable effort is taken to ensure that all sources of the Analysis are reliable and that all information is presented, as much as possible, in an understandable, timely, precise and complete manner, Admiral Markets does not guarantee the accuracy or completeness of any information contained within the Analysis. The presented figures refer that refer to any past performance is not a reliable indicator of future results.

- The contents of the Analysis should not be construed as an express or implied promise, guarantee or implication by Admiral Markets that the client shall profit from the strategies therein or that losses in connection therewith may or shall be limited.

- Any kind of previous or modeled performance of financial instruments indicated within the Publication should not be construed as an express or implied promise, guarantee or implication by Admiral Markets for any future performance. The value of the financial instrument may both increase and decrease and the preservation of the asset value is not guaranteed.

- The projections included in the Analysis may be subject to additional fees, taxes or other charges, depending on the subject of the Publication. The price list applicable to the services provided by Admiral Markets is publicly available from the website of Admiral Markets.

- Leveraged products (including contracts for difference) are speculative in nature and may result in losses or profit. Before you start trading, you should make sure that you understand all the risks.

Government

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Authored by Matthew Vadum via The Epoch Times (emphasis…

Share this:

Authored by Matthew Vadum via The Epoch Times (emphasis ours),

Public officials may block people on social media in certain situations, the Supreme Court ruled unanimously on March 15.

At the same time, the court held that public officials who post about topics pertaining to their work on their personal social media accounts are acting on behalf of the government. But such officials can be found liable for violating the First Amendment only when they have been properly authorized by the government to communicate on its behalf.

The case is important because nowadays public officials routinely reach out to voters through social media on the same pages where they discuss personal matters unrelated to government business.

“When a government official posts about job-related topics on social media, it can be difficult to tell whether the speech is official or private,” Justice Amy Coney Barrett wrote for the nation’s highest court.

The case is separate from but brings to mind a lawsuit that several individuals previously filed against former President Donald Trump after he blocked them from accessing his social media account on Twitter, which was later renamed X. The Supreme Court dismissed that case, Biden v. Knight First Amendment Institute, in April 2021 as moot because President Trump had already left office.

At the time of the ruling, the then-Twitter had banned President Trump. When Elon Musk took over the company he reversed that policy.

The new decision in Lindke v. Freed was written by Justice Amy Coney Barrett.

Respondent James Freed, the city manager of Port Huron, Michigan, used a public Facebook account to communicate with his constituents. Petitioner Kevin Lindke, a resident of Port Huron, criticized the municipality’s response to the COVID-19 pandemic, including accusations of hypocrisy by local officials.

Mr. Freed blocked Mr. Lindke and others and removed their comments, according to Mr. Lindke’s petition.

The U.S. Court of Appeals for the 6th Circuit ruled for Mr. Freed, finding that he was acting only in a personal capacity and that his activities did not constitute governmental action.

Mr. Freed’s attorney, Victoria Ferres, said during oral arguments before the Supreme Court on Oct. 31, 2023, that her client didn’t give up his rights when using social media.

“This country’s 21 million government employees should have the right to talk publicly about their jobs on personal social media accounts like their private-sector counterparts.”

The position advocated by the other side would unfairly punish government officials, and “will result in uncertainty and self-censorship for this country’s government employees despite this Court repeatedly finding that government employees do not lose their rights merely by virtue of public employment,” she said.

In Lindke v. Freed, the Supreme Court found that a public official who prevents a person from comments on the official’s social media pages engages in governmental action under Section 1983 only if the official had “actual authority” to speak on the government’s behalf on a specific matter and if the official claimed to exercise that authority when speaking in the relevant social media posts.

Section 1983 refers to Title 42, U.S. Code, Section 1983, which allows people to sue government actors for deprivation of civil rights.

Justice Barrett wrote that according to the so-called state action doctrine, the test for “actual authority” must be “rooted in written law or longstanding custom to speak for the State.”

“That authority must extend to speech of the sort that caused the alleged rights deprivation. If the plaintiff cannot make this threshold showing of authority, he cannot establish state action.”

“For social-media activity to constitute state action, an official must not only have state authority—he must also purport to use it,” the justice continued.

“State officials have a choice about the capacity in which they choose to speak.”

Citing previous precedent, Justice Barrett wrote that generally a public employee claiming to speak on behalf of the government acts with state authority when he speaks “in his official capacity or” when he uses his speech to carry out “his responsibilities pursuant to state law.”

“If the public employee does not use his speech in furtherance of his official responsibilities, he is speaking in his own voice.”

The Supreme Court remanded the case to the 6th Circuit with instructions to vacate its judgment and ordered it to conduct “further proceedings consistent with this opinion.”

Also on March 15, the Supreme Court ruled on O’Connor-Ratcliff v. Garnier, a related case. The court’s sparse, unanimous opinion was unsigned.

Petitioners Michelle O’Connor-Ratcliff and T.J. Zane were two elected members of the Poway Unified School District Board of Trustees in California who used their personal Facebook and Twitter accounts to communicate with the public.

Respondents Christopher Garnier and Kimberly Garnier, parents of local students, “spammed Petitioners’ posts and tweets with repetitive comments and replies” so the school board members blocked the respondents from the accounts, according to the petition filed by Ms. O’Connor-Ratcliff and Mr. Zane.

But the Garniers said they were acting in good faith.

“The Garniers left comments exposing financial mismanagement by the former superintendent as well as incidents of racism,” the couple said in a brief.

The U.S. Court of Appeals for the 9th Circuit found in favor of the Garniers, holding that elected officials using social media accounts were participating in a public forum.

The Supreme Court ruled in a three-page opinion that because the 9th Circuit deviated from the standard the high court articulated in Lindke v. Freed, the 9th Circuit’s decision must be vacated.

The case was remanded to the 9th Circuit “for further proceedings consistent with our opinion” in the Lindke case, the Supreme Court stated.

International

Home buyers must now navigate higher mortgage rates and prices

Rates under 4% came and went during the Covid pandemic, but home prices soared. Here’s what buyers and sellers face as the housing season ramps up.

Share this:

Springtime is spreading across the country. You can see it as daffodil, camellia, tulip and other blossoms start to emerge.

You can also see it in the increasing number of for sale signs popping up in front of homes, along with the painting, gardening and general sprucing up as buyers get ready to sell.

Which leads to two questions:

- How is the real estate market this spring?

- Where are mortgage rates?

What buyers and sellers face

The housing market is bedeviled with supply shortages, high prices and slow sales.

Mortgage rates are still high and may limit what a buyer can offer and a seller can expect.

Related: Analyst warns that a TikTok ban could lead to major trouble for Apple, Big Tech

And there's a factor not expected that may affect the sales process. Fixed commission rates on home sales are going away in July.

Reports this week and in a week will make the situation clearer for buyers and sellers.

The reports are:

- Housing starts from the U.S. Commerce Department due Tuesday. The consensus estimate is for a seasonally adjusted rate of about 1.4 million homes. These would include apartments, both rentals and condominiums.

- Existing home sales, due Thursday from the National Association of Realtors. The consensus estimate is for a seasonally adjusted sales rate of about 4 million homes. In 2023, some 4.1 million homes were sold, the worst sales rate since 1995.

- New-home sales and prices, due Monday from the Commerce Department. Analysts are expecting a sales rate of 661,000 homes (including condos), up 1.5% from a year ago.

Here is what buyers and sellers need to know about the situation.

Mortgage rates will stay above 5%

That's what most analysts believe. Right now, the rate on a 30-year mortgage is between 6.7% and 7%.

Rates peaked at 8% in October after the Federal Reserve signaled it was done raising interest rates.

The Freddie Mac Primary Mortgage Market Survey of March 14 was at 6.74%.

Freddie Mac buys mortgages from lenders and sells securities to investors. The effect is to replenish lenders' cash levels to make more loans.

A hotter-than-expected Producer Price Index released that day has pushed quotes to 7% or higher, according to data from Mortgage News Daily, which tracks mortgage markets.

TheStreet

On a median-priced home (price: $380,000) and a 20% down payment, that means a principal and interest rate payment of $2,022. The payment does not include taxes and insurance.

Last fall when the 30-year rate hit 8%, the payment would have been $2,230.

In 2021, the average rate was 2.96%, which translated into a payment of $1,275.

Short of a depression, that's a rate that won't happen in most of our lifetimes.

Most economists believe current rates will fall to around 6.3% by the end of the year, maybe lower, depending on how many times the Federal Reserve cuts rates this year.

If 6%, the payment on our median-priced home is $1,823.

But under 5%, absent a nasty recession, fuhgettaboutit.

Supply will be tight, keeping prices up

Two factors are affecting the supply of homes for sale in just about every market.

First: Homeowners who had been able to land a mortgage at 2.96% are very reluctant to sell because they would then have to find a home they could afford with, probably, a higher-cost mortgage.

More economic news:

- Fed members just hat-tipped what's next for interest rates

- Retail sales tumble clouds impact of inflation data

- Jobs report shocker: 353,000 hires crush forecasts, stokes inflation fears

Second, the combination of high prices and high mortgage rates are freezing out thousands of potential buyers, especially those looking for homes in lower price ranges.

Indeed, The Wall Street Journal noted that online brokerage Redfin said only about 20% of homes for sale in February were affordable for the typical household.

And here mortgage rates can play one last nasty trick. If rates fall, that means a buyer can afford to pay more. Sellers and their real-estate agents know this too, and may ask for a higher price.

Covid's last laugh: An inflation surge

Mortgage rates jumped to 8% or higher because since 2022 the Federal Reserve has been fighting to knock inflation down to 2% a year. Raising interest rates was the ammunition to battle rising prices.

In June 2022, the consumer price index was 9.1% higher than a year earlier.

The causes of the worst inflation since the 1970s were:

- Covid-19 pandemic, which caused the global economy to shut down in 2020. When Covid ebbed and people got back to living their lives, getting global supply chains back to normal operation proved difficult.

- Oil prices jumped to record levels because of the recovery from the pandemic recovery and Russia's invasion of Ukraine.

What the changes in commissions means

The long-standing practice of paying real-estate agents will be retired this summer, after the National Association of Realtors settled a long and bitter legal fight.

No longer will the seller necessarily pay 6% of the sale price to split between buyer and seller agents.

Both sellers and buyers will have to negotiate separately the services agents have charged for 100 years or more. These include pre-screening properties, writing sales contracts, and the like. The change will continue a trend of adding costs and complications to the process of buying or selling a home.

Already, interest rates are a complication. In addition, homeowners insurance has become very pricey, especially in communities vulnerable to hurricanes, tornadoes, and forest fires. Florida homeowners have seen premiums jump more than 102% in the last three years. A policy now costs three times more than the national average.

Related: Veteran fund manager picks favorite stocks for 2024

recession depression pandemic covid-19 stocks fed federal reserve home sales mortgage rates real estate mortgages housing market recovery interest rates oil russia ukraine

Uncategorized

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Westbrook Partners, which acquired the San…

Share this:

{kind=link}

Westbrook Partners, which acquired the San Francisco Four Seasons luxury hotel building, has been served a notice of default, as the developer has failed to make its monthly loan payment since December, and is currently behind by more than $3 million, the San Francisco Business Times reports.

{kind=link}

Westbrook, which acquired the property at 345 California Center in 2019, has 90 days to bring their account current with its lender or face foreclosure.

Related

- Fed Fears "Notable" Financial System Vulnerability As Renowned CRE Investor Tells Team 'Stop All NYC Underwriting'

- The State Of Commercial Real Estate, In Charts

- "Who Could Be Next": Top Canadian Pension Fund Sells Manhattan Office Tower For $1, Sparking Firesale Panic

- "Heightened Risks": Goldman Points To Leading CRE Indicator That Shows Pain Train Not Over

As SF Gate notes, downtown San Francisco hotel investors have had a terrible few years - with interest rates higher than their pre-pandemic levels, and local tourism continuing to suffer thanks to the city's legendary mismanagement that has resulted in overlapping drug, crime, and homelessness crises (which SF Gate characterizes as "a negative media narrative).

Last summer, the owner of San Francisco’s Hilton Union Square and Parc 55 hotels abandoned its loan in the first major default. Industry insiders speculate that loan defaults like this may become more common given the difficult period for investors.

At a visitor impact summit in August, a senior director of hospitality analytics for the CoStar Group reported that there are 22 active commercial mortgage-backed securities loans for hotels in San Francisco maturing in the next two years. Of these hotel loans, 17 are on CoStar’s “watchlist,” as they are at a higher risk of default, the analyst said. -SF Gate

The 155-room Four Seasons San Francisco at Embarcadero currenly occupies the top 11 floors of the iconic skyscrper. After slow renovations, the hotel officially reopened in the summer of 2021.

"Regarding the landscape of the hotel community in San Francisco, the short term is a challenging situation due to high interest rates, fewer guests compared to pre-pandemic and the relatively high costs attached with doing business here," Alex Bastian, President and CEO of the Hotel Council of San Francisco, told SFGATE.

Heightened Risks

In January, the owner of the Hilton Financial District at 750 Kearny St. - Portsmouth Square's affiliate Justice Operating Company - defaulted on the property, which had a $97 million loan on the 544-room hotel taken out in 2013. The company says it proposed a loan modification agreement which was under review by the servicer, LNR Partners.

Meanwhile last year Park Hotels & Resorts gave up ownership of two properties, Parc 55 and Hilton Union Square - which were transferred to a receiver that assumed management.

In the third quarter of 2023, the most recent data available, the Hilton Financial District reported $11.1 million in revenue, down from $12.3 million from the third quarter of 2022. The hotel had a net operating loss of $1.56 million in the most recent third quarter.

Occupancy fell to 88% with an average daily rate of $218 in the third quarter compared with 94% and $230 in the same period of 2022. -SF Chronicle

According to the Chronicle, San Francisco's 2024 convention calendar is lighter than it was last year - in part due to key events leaving the city for cheaper, less crime-ridden places like Las Vegas.

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Gen Z, The Most Pessimistic Generation In History, May Decide The Election

“Extreme Events”: US Cancer Deaths Spiked In 2021 And 2022 In “Large Excess Over Trend”

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

Correcting the Washington Post’s 11 Charts That Are Supposed to Tell Us How the Economy Changed Since Covid

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex