Uncategorized

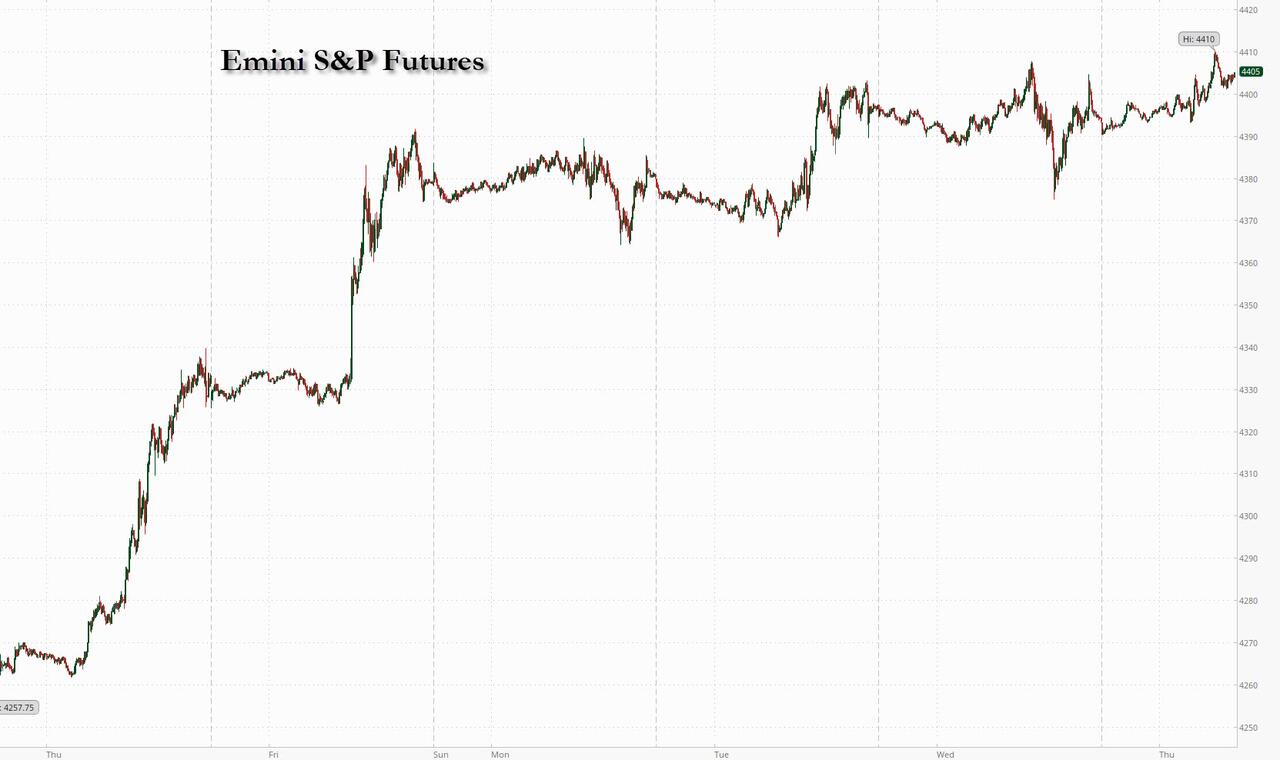

S&P Futures Rise, Set For Longest Winning Streak Since 2004

S&P Futures Rise, Set For Longest Winning Streak Since 2004

S&P 500 futures edged higher on Thursday after notching an eight-day streak…

Share this:

S&P 500 futures edged higher on Thursday after notching an eight-day streak of gains, and setting up the benchmark index for its longest winning streak since 2004, as investors monitored bond yields, corporate earnings and the price of oil. Treasuries fell and the dollar rose ahead of more speeches by central bank officials including more remarks by Fed chair Powell. After a listless overnight session, as of 7:45am S&P futures were up 0.1% and Nasdaq was down by a similar amount. Elsewhere, Europe’s Stoxx 600 index rose 0.6%, Asian stocks closed green, oil hovered near a three-month low after plunging almost 7% over the previous two sessions, yields on 10-year Treasuries held below 4.5%, the dollar gained and bitcoin was set to rise above $37,000, an 18 month high.

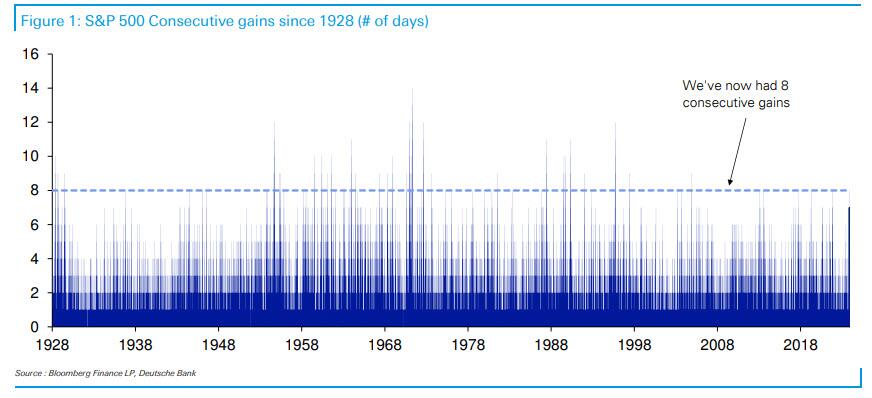

While the rapid momentum has fizzled out, the S&P 500 has inched higher every day this week and if the index closes up for another day, it would be the 9th day in a row stocks have risen (alternatively the VIX is now also down for 9 straight days). As DB's Jim Reid notes this morning, although a 9-day run has happened 31 times in the last 95 years it actually hasn’t happened since 2004. And If we end the week with 2 more up days, the 10-day run will be the first since 1995, even though they’ve happened every 6.3 years on average over the last 95 years.

In summary, in the last 95 years:

- An 8-day winning streak has happened 63 times (average c. every 1.5 years)

- A 9-day streak has happened 31 times (average c. every 3.1 years)

- A 10-day streak has happened 15 times (average c. every 6.3 years)

- An 11-day streak has happened 8 times (average c. every 11.9 years)

- A 12-day streak has happened 5 times (average c. every 19 years)

- A 13-day streak has happened 1 time (average c. every 95 years)

- A 14-day streak has happened 1 time (average c. every 95 years)

In premarket trading, Walt Disney gained 4% after profit beat estimates. Arm Holdings Plc sank 4.7% after the chip designer issued a disappointing sales forecast as the company is pressured by a weak smartphone market and uncertainties surrounding new licensing deals. Cryptocurrency-linked stocks rose as Bitcoin extends gains for a fourth consecutive session to touch its highest level since May 2022. The recent rally is led by expectations of an approval for exchange traded funds to invest in the largest crypto token. Coinbase +4.2%, Riot Platforms +6.3%, Marathon Digital +10%, Hut 8 Mining +8.9%. Disney shares gained 3.8% after the media company reported better-than-expected 4Q adjusted earnings and a strong read on subscribers for its streaming-video service. The company also said it plans to resume paying a dividend for the first time since the pandemic. Here are the other notable premarket movers:

- Affirm Holdings shares rally 14% after the buy-now-pay-later (BNPL) company posted first-quarter revenue that was ahead of consensus. The firm forecast revenue for the second quarter of $495 million to $520 million, compared to analyst estimates for $505.9 million.

- Bill Holdings shares tumble 8.8% as Bloomberg News reports that the company, which provides financial-automation software to small and mid-size businesses, is in advanced talks to acquire the digital payment tools provider Melio Payments.

- Cardlytics shares sink 35% after the digital advertising company gave a fourth-quarter outlook that fell short of consensus and reported revenue for the third quarter that missed the average analyst estimate.

- Lyft shares fall 1.7% after the ride-hailing company gave a lackluster revenue outlook for the holiday period, overshadowing the company’s third-quarter revenue beat.

- Tesla shares fall 1.7% as HSBC initiated coverage on the electric-vehicle maker’s stock with a recommendation of reduce, citing the timing of delivery as its primary concern.

In global equity markets, the recent upswing is down to conviction that the Federal Reserve and other policy makers are done hiking interest rates, even as officials caution that they won’t be quick to cut. European Central Bank Vice President Luis de Guindos told Slovenia’s Finance newspaper that any talk of lowering borrowing costs in the coming months is too early. Fed Chair Jerome Powell will speak at the IMF’s annual research conference and ECB President Christine Lagarde is also scheduled to deliver remarks later today.

“Markets are listening to central bankers, but they’re also taking on board recent data and are becoming more confident that further hikes are off the table,” said James Rossiter, head of global macro strategy at TD Securities.

It's not just stocks: rates traders are also betting that the steepest global tightening cycle in a generation is over. Swaps signal the average cash rate for developed economies will be steady over the coming six months, the first time in two years that they’re not pricing in a hike over that time frame, according to data compiled by Bloomberg. The Bank of England Chief Economist Huw Pill reinforced that view on Thursday, saying the BOE doesn’t need to raise rates further because policy is already restrictive enough. UK markets are pricing in three quarter-point rate cuts, starting in August next year.

European markets extended gains, with the Stoxx 600 adding 0.6% with chemical, industrial and real estate shares leading gains. Sentiment was boosted by a 32% surge in shares of Adyen NV, a Dutch payments processor that competes with PayPal Holdings Inc. The company unveiled growth targets and a pathway to achieving them, a key sign that it’s intent on winning back investor confidence. Here are the most notable European movers:

- Adyen shares soar as much as 37% in Amsterdam, the biggest gain since June 2018. The payment firm’s 3Q sales were much better than expected and its new medium-term goals appear more realistic and credible, according to analysts

- AstraZeneca shares rise as much as 4.2%, after the pharmaceuticals company reported better-than-expected earnings in the third quarter, raised its profit outlook for the year and clinched a deal to develop a drug targeting patients with diabetes and obesity

- Deutsche Telekom shares gain as much as 1.6% to the highest level since May, after the telecom operator reported estimate-beating results in Europe. Operational metrics in home market of Germany were seen as strong by analysts as pricing pressure eases

- Auto Trader shares gains as much as 7.7%, the most since March 2022, with analysts flagging a revenue beat at the automotive marketplace operator’s first-half results

- Henkel shares gain as much as 4% in Frankfurt after the German consumer-products group reported third-quarter organic sales growth that was higher than consensus expectations

- Nexi shares soar as much as 11% and are the best performers in the Stoxx Europe 600 Index after the Italian payments specialist reported broadly in-line third-quarter results and reaffirmed its full-year guidance

- Airbus shares fall as much as 3.1% after it reported third-quarter results below expectations due to a charge related to satellite development programs, but analysts say they do see some signs of positives for the planemaker

- Coloplast falls as much as 6.4%, the most since Aug. 17, after the Danish ostomy and continence care firm’s 2024 guidance fell short of expectations, with Bernstein flagging continued struggles with profitability as a key negative

- KBC shares fell as much as 5.8%, to the lowest in year, after the Belgian bank cut its net interest income forecast for the full year, a move which analysts said would hurt its valuation moving forward

- Flutter shares dive as much as 12%, the steepest one-day drop since March 2022, after the gambling firm reported 3Q earnings that failed to impress. Though analysts made note of a soft quarter, the stock remains a highlight among gambling firms at Goodbody and Morgan Stanley

- ArcelorMittal falls as much as 2% after the world’s top steelmaker outside China reported a drop in third-quarter profit as steel prices declined in key markets due to weaker demand

- B&M European Value Retail shares drop as much as 7.3%, after the discount retailer reported third-quarter adjusted Ebitda that missed estimates. RBC Capital Markets said the guidance was a “touch below” consensus and noted a slow start to the third quarter

Asia’s stocks also closed higher Thursday following a two-day decline, with Japan helping to lead gains. The MSCI Asia Pacific Index rose as much as 0.4%, with Toyota, Samsung and Nintendo among the biggest boosts. Shares in Vietnam, Singapore, Australia and South Korea also advanced. Key gauges in Hong Kong declined after data showed that Chinese consumer prices fell more than expected in October — mainland benchmarks were little changed.

- Hang Seng and Shanghai Comp were mixed with Mainland China flat/firmer whilst the latest Chinese inflation metrics painted a picture of a fragile economy as the nation fell back into deflation. Hong Kong underperformed as the Property sector dragged the index lower.

- Japan's Nikkei 225 was firmer from the start as the recent JPY weakness lent exporters a hand and the index eventually topped 32,500.

- Australia's ASX 200 saw its upside supported by Health and Financials, with the latter as NAB rose post-earnings, although the IT and Energy sectors lagged.

- India stocks fell amid weakness in technology and consumer staple companies. Reliance Industries declines most in two weeks. The S&P BSE Sensex fell 0.2% to 64,832.20 in Mumbai, while the NSE Nifty 50 Index declined 0.3% to 19,395.30.

In FX, the Bloomberg Dollar Spot Index rises for a fourth day, adding 0.1%. The euro and the Swiss franc are the weakest of the G-10 currencies. The Kiwi is the strongest.

In rates, treasuries dropped, led by the long-end and partially unwinding the effect on 2s10s and 5s30s of Wednesday’s curve-flattening rally ahead of the Treasury’s 30-year bond auction later on Thursday. US 10-year yields rise 4bps to 4.54%. Traders are also watching for comments from Fed Chair Powell at an IMF event. Bunds and gilts are on the back foot as well. UK bonds were weighed down by comments from Bank of England chief economist Pill who seemed to recalibrate his dovish language from earlier in the week.

In commodities, oil prices finally advanced, with WTI rising 0.9% to trade near $76. Spot gold falls 0.2%.

Bitcoin rose sharply again, rising as high as $37,000. Among other news, the SEC has reportedly opened talks with Grayscale Investments on the details of the company's application to convert its trust product GBTC to a spot Bitcoin (BTC) ETF, according to CoinDesk citing sources.

To the day ahead now, there is an array of central bank speakers, including Bostic (9:30am), Barkin (11am), Paese (12pm) and Powell (2pm), who participates in a panel discussion on monetary policy challenges in a global economy at the IMF’s annual research conference (text and Q&A expected). US economic data scheduled for the session includes initial jobless claims at 8:30am New York time.

Market Snapshot

- S&P 500 futures little changed at 4,402.00

- MXAP up 0.4% to 157.17

- MXAPJ little changed at 491.91

- Nikkei up 1.5% to 32,646.46

- Topix up 1.3% to 2,335.12

- Hang Seng Index down 0.3% to 17,511.29

- Shanghai Composite little changed at 3,053.28

- Sensex down 0.2% to 64,813.78

- Australia S&P/ASX 200 up 0.3% to 7,014.90

- Kospi up 0.2% to 2,427.08

- STOXX Europe 600 up 0.3% to 445.46

- German 10Y yield little changed at 2.64%

- Euro little changed at $1.0702

- Brent Futures up 1.0% to $80.33/bbl

- Gold spot down 0.2% to $1,946.91

- U.S. Dollar Index little changed at 105.55

Top Overnight News

- China’s CPI fell back into deflation territory in Oct (-0.2% vs. the Street -0.1% and vs. 0.0% in Sept) while PPI deflation deepened to -2.6% (vs. -2.6% in Sept and vs. the Street -2.7%). FT

- Cloud Software Group, which owns enterprise-software brand Citrix, is ceasing business transactions in China, becoming the latest U.S. company to pull back from China. In an email to clients and partners on Monday seen by The Wall Street Journal, Cloud Software Group said it has made the decision to cease all new commercial transactions in China, including Hong Kong, on Dec. 3. It cited rising costs in the market. WSJ

- White House hopes to announce a new commitment from China to stem the flow of fentanyl into the US along w/a resumption of military communication following the Biden-Xi summit. NBC News

- BOJ’s Ueda says the central bank will be careful when raising rates to avoid creating volatility (he added that while some progress is happening toward achieving the desired level of inflation, “there’s still some distance to cover”). FT

- Mario Draghi has delivered a downbeat view of EU economic growth, forecasting a recession by the end of this year, as he warned that the European project’s long-term survival depends on urgent political integration. FT

- US strikes Iranian weapons facility in Syria in retaliation for attacks against American forces in the region by Tehran-backed proxies. WaPo

- America’s long streak of population growth is expected to come to an end. Census Bureau projections released Thursday show that, under the most likely scenario, the U.S. will stop growing by 2080 and shrink slightly by 2100. Slowing growth would produce a peak U.S. population of almost 370 million before an ebb to 366 million in the final years of the century, according to the bureau. WSJ

- Hollywood actors and studios reached a tentative deal to end a 118-day strike. The contract — worth over $1 billion — includes unprecedented restrictions on the use of AI and the first-ever performance-based bonuses, the actors’ union said. BBG

- Apple risks having to pay a €13 billion ($14 billion) tax bill to Ireland after an adviser to the European Union’s top court said the iPhone maker’s victory in an earlier challenge should be thrown out. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly firmer following a similar lead from Wall Street with most major APAC markets in the green although Chinese markets saw more of a muted performance. ASX 200 saw its upside supported by Health and Financials, with the latter as NAB rose post-earnings, although the IT and Energy sectors lagged. Nikkei 225 was firmer from the start as the recent JPY weakness lent exporters a hand and the index eventually topped 32,500. Hang Seng and Shanghai Comp were mixed with Mainland China flat/firmer whilst the latest Chinese inflation metrics painted a picture of a fragile economy as the nation fell back into deflation. Hong Kong underperformed as the Property sector dragged the index lower.

Top Asian News

- Japan's Government will seek JPY 2tln (USD 13.2bln) in budget funding to support chip production and advances in generative AI technology, including more aid for Taiwan Semiconductor Manufacturing Co. (TSM), according to Nikkei.

- BoJ Oct Summary of Opinions: one member said must patiently maintain monetary easing; One member said that given extremely high uncertainty and must take steps to make YCC operation more flexible. Click here for the detailed headline.

- BoJ Governor Ueda reiterates that firms becoming more active in raising prices and wages than before, according to Reuters.

- Ex-BoJ executive Maeda said the BoJ may end the negative interest rate policy in January and keep raising short-term rates in stages, according to Reuters.

- PBoC injected CNY 202bln via 7-day reverse repos with the rate at 1.80% for a CNY 8bln net daily injection.

- RBI Governor Das said India's current account deficit remains eminently manageable, and they have bolstered FX reserves to deal with potential eventualities.

- BoJ's Ueda cautions that unwinding ultra-loose policy is a serious challenge, adding that the BoJ will move carefully on raising interest rates, via FT. On commitment to quantitative/qualitative easing until inflation target is attained says: “We are making progress towards achieving this same goal, but there’s still some distance to cover before we can scrap the forward guidance,”. In the scenario of an overshoot in inflation, believe we will be able to deal with it by lifting rates. Rate of growth of wages, around 2%, will need to continue and at a slightly higher rate. Yet to decide what order they would terminate the measures which are in place.

- Japan lobby head urges BoJ to normalise policy to live with interest rates; the leader said the BoJ should unwind its easing programmes to live with interest rates although it may take a year to exit monetary stimulus.

European bourses are in the green with newsflow relatively limited and the tone gradually improving throughout the session, Euro Stoxx 50 +0.8%. Action which follows a more mixed APAC handover, where China and Hong Kong underperformed on inflation data and the property sector respectively. Sectors are primarily in the green, with Industrials outperforming after Schneider Electric though Airbus' update has capped gains. At the other end of the spectrum, Travel & Leisure is in the red after Flutter Entertainment's report. Stateside, futures are making their way into the green as we near the commencement of US cash trade, ES +0.2%; with action for much of the session near-unchanged and tentative/rangebound. EU court advisor has backed the EU's USD 14bln tax order to Apple (AAPL); advisor agrees with the Commission's view that the General Court erred when the case against Apple was thrown out, proposes the case is referred back for a new decision. Nvidia (NVDA) is reportedly planning to unveil three new chips for China, via Star Market Daily citing sources; to be announced as soon as November 16th

Top European News

- BoE's Pill assumes rates are to stay restrictive for an extensive period. Inflation remains much too high. No grounds for complacency when it comes to inflation. Do not need to raise rates to bear down on inflation. Need a persistent level of restrictive monetary policy for an extended period. If the economic situation changes, will need to change policy. BoE does not make promises when it comes to interest rates. Slowing growth does not appear to be lowering inflation or firms pricing power.

- The German Government reached an agreement on electricity price support for the industry, via Handelsblatt citing sources; agreement for five years, relief will amount to over EUR 10bln in the coming year alone.

FX

- Buck back on recovery track after midweek time out as Treasury yields rebound and curve re-steepens, DXY towards top end of 105.67-46 band.

- Yen losing ground sub-151.00 vs Dollar as BoJ Governor Ueda continues to bang the dovish drum.

- Euro capped by heavy 1.0700+ option expiry interest against the Greenback, and Franc underpinned by expiries above 0.9000.

- Pound propped around 1.2300 and 0.8700 vs Euro after BoE's Pill pushes the case for a prolonged period of restrictive policy.

- Kiwi elevated ahead of NZ manufacturing PMI, as NZD/USD grips 0.5900 handle and AUD/NZD slips under 1.0800.

- PBoC set USD/CNY mid-point at 7.1772 vs exp. 7.2723 (prev. 7.1773)

Fixed Income

- Debt futures regress after upside extension and curves flip a bit from bull-flattening.

- Bunds fade closer to 131.00 within a 130.93-39 range, Gilts retreat from 96.14 to 95.35.

- T-note towards the base of 108-04/17 band as 10 year yield fails to hold below 4.5% ahead of US jobless claims, long bond auction and more Fed speak.

Commodities

- Crude benchmarks are firmer on the session though the magnitude of the move pales in comparison to the downside seen WTD and since the middle of October when the Israel-Hamas geopolitical premium peaked, so far at least.

- As it stands, WTI Dec’23 and Brent Jan’24 are posting upside of just under USD 1/bbl on the session; but, have only been able to recover to around the mid-point of Wednesday’s USD 74.91-77.53/bbl parameters in WTI at best.

- Metals are modestly softer but with action relatively contained as the USD inches higher and the overall risk tone remains firmer in Europe but much more tentative thus far stateside.

- Chinese importers bought at least five more US soybean cargoes on Wednesday for Dec-Mar shipment, according to Reuters citing traders.

- China Commerce Ministry said China is to re-investigate anti-dumping duties case on stainless steel billets and stainless steel hot-rolled sheets and coils imported from the EU, Japan, South Korea, and Indonesia, according to Reuters.

- China Vice Premier Ding will increase coal, natural gas production and actively expand imports of resources to ensure stable energy supply this winter.

Geopolitics

- US military forces confirm it conducted a self-defence strike on a facility in eastern Syria, according to the Pentagon; the strike is a response to attacks against US personnel in Iraq and Syria by IRGC-Quds Force affiliates.

- Two marches attack on the Silk base in Iraq and sirens sound at the US embassy [in Iraq]", according to Sky News Arabia.

- Hamas is reportedly discussing the possible release of a few hostages in exchange for a brief pause in fighting, officials said via NYT.

- Vice chairman of China's Central Military Commission, in a meeting with Russian President Putin, said "China is ready to work with Russia to jointly safeguard the two countries' interests and safeguard global and regional prosperity and stability", according to Global Times.

- Germany will send four fighter jets to Romania to support NATO's air policing mission from the end of November, according to Reuters sources.

US Event Calendar

- 08:30: Oct. Continuing Claims, est. 1.82m, prior 1.82m

- 08:30: Nov. Initial Jobless Claims, est. 218,000, prior 217,000

Central Bank Speakers

- 09:30: Fed’s Bostic and Barkin Speak on Survey Data

- 11:00: Fed’s Barkin Discusses Fed Policy, US Economy outlook

- 12:00: Fed’s Paese Speaks About the Economy and Monetary Policy

- 14:00: Fed’s Powell Speaks on Panel at IMF Conference

DB's Jim Reid concludes the overnight wrap

The bond rally continued over the last 24 hours, with long-end yields falling to their lowest level in weeks as investors grew more confident that inflation was set to fall back and that central banks were now finished with their rate hikes. In part, that was driven by another round of oil price declines, with Brent crude closing beneath $80/bbl for the first time since July, whilst WTI closed beneath $76/bbl. And even though risk assets lost some of their recent momentum given the concerns about economic demand, the S&P 500 (+0.10%) still managed to post an 8th consecutive gain for the first time since late-2021. In fact, if we manage to get a 9th consecutive advance today, that would make it the longest run of gains since 2004, although futures for the S&P 500 are slightly negative overnight, with a -0.03% decline .

For Treasuries, there was a sizeable rally at the long-end of the curve, with yields falling to their lowest levels in some time. Most notably, the 10yr yield fell back -7.4bps to a 6-week low of 4.49%, marking the first time it’s closed below 4.5% since the Friday after the September FOMC meeting. That rally had been underway early in the session, but there was a further advance thanks to a mixed $40bn 10yr auction, with a positive reaction to the market’s ability to digest increased issuance volumes. The 30yr yield was down by a larger -11.1bps to 4.61% ahead of the 30yr auction today. That’s a sizeable decline from their recent levels, as it was only on Tuesday of last week that the 30yr yield closed at 5.09%.

Those moves come as there are already signs that this decline is filtering through to the real economy, with data from the Mortgage Bankers Association showing that the average 30yr fixed mortgage rate was down -25bps to 7.61% over the week ending November 3. That’s the biggest weekly decline since July 2022, as well as the third-biggest weekly decline since the GFC. And in turn, it helped the index of mortgage applications for home purchase rise from its lowest level since 1995 the previous week.

Over in Europe it was much the same story, with yields on 10yr bunds (-4.3bps), OATs (-5.0bps) and BTPs (-6.7bps) all moving lower. Inflation expectations drove the decline, with the 10yr German breakeven down -2.6bps to 2.12%, which is its lowest closing level since January. And that was evident across the wider Euro Area too, with the 5y5y forward inflation swap (-1.0bps) falling to its lowest in nearly six months, at 2.43% .

The main catalyst for that decline in inflation expectations was the sharp move lower in commodity prices. In particular, energy prices fell across the board, with Brent crude oil (-2.54%) down to $79.54/bbl, and WTI (-2.64%) down to $75.33/bbl. That’s come as investors have become increasingly concerned about economic demand, not least after several weaker-than-expected data releases since the start of the month. And the moves were evident across several different commodities, with European natural gas down -1.93%, copper down -1.11% and gold down -0.52% .

Central bankers themselves provided little direction for yesterday’s moves. We did hear from Fed Chair Powell, although he didn’t discuss the outlook for Fed policy, so attention will now turn to his appearance later today, where he’s speaking on a panel at an IMF conference. When it came to the ECB, we did hear from Bundesbank President Nagel, who said that “I don’t like this discussion going on about when will be the point you lower interest rates”. That was echoed by the Central Bank of Ireland’s Governor Makhlouf, who said that it was “far too early in my view to start talking about when we’ll start reducing or cutting rates”. Furthermore, despite the moves lower in market-based inflation expectations, the ECB’s latest Consumer Expectations Survey found that in September, median inflation expectations at the 1yr horizon were up half a point to 4.0%, which is their highest level since April. Looking further out at the 3yr horizon, they were unchanged at 2.5%.

Equities lost momentum but still managed to continue their recent advance, with the S&P 500 (+0.10%) extending its run to 8 consecutive gains, the longest since November 2021. Furthermore, the VIX index of volatility was down for an 8th consecutive session as well (-0.4pts to 14.5), which was its longest run of declines since 2015. However, this equity advance was a narrow one as 55% of S&P stocks actually fell on the day, with energy stocks and other defensive sectors among the worst performers. Indeed, other indices struggled including the Dow Jones (-0.12%) and the Russell 2000 (-1.10%), with the latter falling back for a 3rd consecutive day, bringing its decline for the week so far to -2.65%. On the other hand, megacap tech stocks outperformed with the FANG+ Index up +0.47%. Over in Europe, there was also a relatively stronger performance, with the STOXX 600 (+0.28%) bouncing back from its losses on Monday and Tuesday, whilst the DAX was also up +0.51% .

Overnight in Asia , we’ve seen a mixed performance for the major equity indices. Some have seen decent advances, with the Nikkei up +1.52%, and the KOSPI up +0.53%. However, the Shanghai Comp (+0.03%) and the CSI 300 (-0.01%) have seen little movement, and the Hang Seng (-0.25%) has lost ground. That comes as data from China showed that consumer prices were down -0.2% year-on-year in October (vs. -0.1% expected), whilst producer prices were down -2.6% (vs. -2.7% expected) .

To the day ahead now, and there’s several central bank speakers to hear from, including Fed Chair Powell, the Fed’s Bostic, Barkin and Paese, ECB President Lagarde, the ECB’s Villeroy and Lane, as well as the BoE’s Pill. In addition, the ECB will publish their Economic Bulletin, and on the data side, we’ve got the US weekly jobless claims coming out. Otherwise, there’s a 30yr US Treasury auction taking place.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

{kind=link}

{kind=link}

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex