Uncategorized

S&P Futures Approach All Time High As Tech Meltup Goes Full-Tilt

S&P Futures Approach All Time High As Tech Meltup Goes Full-Tilt

After starting off the week with whimper, renewed hopes for a soft Goldilocks…

Share this:

After starting off the week with whimper, renewed hopes for a soft Goldilocks landing as well as two consecutive upgrades of Apple have not only reversed the bitter taste from the preceding two downgrades (today the company was added to Evercore ISI’s tactical outperform, following yesterday's BofA upgrade which fueled the best day for Apple since May), but have also sparked "banging" trader sentiment which pushed US futures higher in premarket trading while lifting the Nasdaq 100 to a recorder high. As of 7:40am, contracts on the Nasdaq 100 climbed about 0.7% after hitting an all time high on Thursday, while S&P 500 futures were up 0.4%, and with the S&P just 16 handles away from all time highs, we may have a new record today (at which point we assume Marko will finally turn bullish and we can once again short). Treasury yields were flat at 4.14% and the dollar dropped after frenetic repricing of the policy outlook earlier in the week. Investors will pay close attention to UMich inflation expectations and Fed speakers today for further cues on the timing and extent of rate cuts. Traders now see the prospect of easing in March at little more than a coin toss, down from almost 80% at the end of last week.

In premarket trading, semiconductor sector names like Nvidia and Broadcom were among the biggest benefactors from the Nasdaq rally, as a brighter outlook from Taiwanese chipmaking behemoth TSMC two days ago lingered on (and on) and helped lift the mood as well as hopes for a broader recovery in the tech sector in 2024 (even as a similar warning by TSMC a quarter ago was very much ignored). Chip companies such as Advanced Micro Devices climbed 2% while Intel rose 1.2%. Texas Instruments rose more than 2% after maintaining its quarterly dividend. Here are some of the other notable premarket movers:

- Coherus BioSciences shares jump 5.8% after the commercial-stage biopharmaceutical company posted data from the lead-in portion of the Phase 2 clinical trial on a treatment for liver cancer.

- Coinbase shares rise 0.8% as Citi hikes its price target on the cryptocurrency exchange operator, following an increase in crypto prices and volumes quarter-on-quarter.

- Endeavor shares climb 7.5% after Bloomberg reported that Silver Lake plans to sell parts of the entertainment company after taking it private.

- iRobot shares slide 37% following reports that the European Union’s antitrust watchdog is planning to block Amazon’s planned acquisition of the Roomba vacuum maker.

- Roku shares rise 2.3% after Seaport Global raised the maker of TV streaming boxes and software to neutral due to to incremental data points that suggest there could be upside to the asset manager’s estimates.

- Super Micro Computer shares rise 12% after the computer hardware maker’s preliminary financial results beat expectations, with the company saying it expects to exceed its previous guidance. Barclays analysts said that it was a positive pre-announcement for the firm.

- AT&T rises 1.5% in premarket trading after Oppenheimer raised the wireless telecommunications company to outperform from perform, citing several tailwinds including improvements to network capacity and coverage, helping boost average revenue per user growth.

- IBM advances 2.5% in premarket trading after Evercore ISI raised the IT services company to outperform from inline, calling it an “overlooked beneficiary” of the increasing adoption of artificial intelligence.

- Apple Inc.’s long-awaited Vision Pro mixed-reality headset will finally be available for preorders on Friday, giving the company its first real taste of consumer demand for the $3,499 device. Apple Inc. vowed to open up its coveted tap-to-pay technology on iPhones to rivals in a bid to sidestep potentially massive European Union antitrust fines.

“Markets have been unnerved by the reluctance of major central banks to cut rates quickly in response to slowing inflation and weak growth,” said Lee Hardman, a currency strategist at MUFG Bank Ltd. “It is difficult to see today’s rebound in risk assets proving sustainable until central banks give the green light for rate cuts.”

In Fed speak, Atlanta Fed President Raphael Bostic urged policymakers to proceed cautiously given the potential impacts of unpredictable events from elections to global conflicts. His Philadelphia counterpart Patrick Harker said he expects inflation to keep ebbing toward the target. Chicago Fed President Austan Goolsbee and the San Franscisco Fed’s Mary Daly are scheduled to speak today.

And speaking of market expectations, BlackRock expects the Fed to start cutting rates in June, senior investment strategist Laura Cooper said in an interview with Bloomberg TV. She sees 75 to 100 basis points of reductions by year-end. “We’re leaning more towards a June rate cut and then a recalibration,” Cooper said. Markets have become “very exuberant” in their bets on policy easing, she said, adding that “there is a degree of repricing that still needs to come through that adds to our view that there’s going to be a bit of volatility ahead.”

On the outlook for US equities, Bank of America strategists said the stocks that led the rally in 2023 are again traders’ top picks amid elevated Treasury yields.Investors are reverting to owning growth, technology, the AI bubble and the so-called Magnificent Seven group of stocks including Apple as the 10-year Treasury yield settles in a range of 3.75% to 4.25%, a BofA team led by Michael Hartnett wrote in a note.

This same group of equities led the Nasdaq 100’s 54% rally last year amid expectations of rate cuts, a solid economy and optimism about artificial intelligence developments. So far in January, Nvidia Corp., Microsoft Corp. and Meta Platforms Inc. — all among those seven dominant stocks — are the top gainers on the tech-heavy gauge.

European stocks rose for a second day, albeit slightly, with the Stoxx 600 up 0.1% and trimming its loss this week to 1.2%. The technology sub-sector advanced further as Taiwan Semi’s outlook fueled hopes for a global recovery in chip sales. Swiss electrical-equipment maker ABB dragged industrials lower after saying US lawmakers are reviewing its operations in China. Here are the biggest European movers on Friday:

- Teleperformance jumps as much as 6.3% after Stifel raised its rating and its target price for the shares of the French call center operator which, the broker believes, has the potential to double in the next three years

- BASF rises as much as 2% after reporting preliminary results. UBS says the 4Q numbers represent a trough, though overall Warburg says the figures fall short of the company’s guidance as well as consensus estimates

- Avanza rises as much as 8% after the Swedish bank’s quarterly earnings beat estimates. Citi says the update should prompt an upgrade to earnings consensus

- Persimmon rises as much as 3.5% and is leading gains among UK housebuilders following double upgrade to overweight from Morgan Stanley. Analysts flag hopes that demand is improving as we approach the key Spring selling season, even as the outlook remains uncertain

- Temenos shares rise as much as 7.6%, the most since April, after the Swiss financial software firm reported preliminary 4Q results that were well above expectations and exceeded guidance, according to Vontobel

- Marel shares jump as much as 8%, to its highest intraday level in Amsterdam as John Bean Technologies raised its offer to buy the company to €3.60/share

- 4imprint Group shares rise as much as 15%, the most since August after the promotional merchandise maker said annual pretax profit for 2023 will be above the upper end of analysts’ consensus range

- Wincanton gains as much as 48% the biggest jump on record to 439p, slightly below the offer price of 450p/share proposed by CEVA Logistics, a subsidiary of French shipping and logistics company CMA CGM

- Corbion plunges as much as 8.5% after ING cut its recommendation on the Dutch ingredients maker to sell from hold. The broker say it’s “quite shocking” that over nearly a decade the company has spent the equivalent of its market value in capital expenditure

Earlier in the session, stocks in Asia mostly rose, as gains in semiconductor stocks drove MSCI’s Asia Pacific gauge higher for a second day, and higher as much as 1.1%, set for its biggest gain in at least six sessions and paring this week’s loss to 2.3%. A sub-gauge of tech shares gained more than 3%, on track for its biggest gain in a year. Taiwan’s benchmark Taiex led gains around the region as TSMC climbed 6% after saying it expects a return to solid growth this quarter. Shares in Japan and South Korea also advanced as the Taiwanese chipmaker’s outlook for capital spending and revenue lifted hopes of a broad tech recovery in 2024.

- Hang Seng and Shanghai Comp were subdued amid the lingering concerns surrounding an uneven recovery in the Chinese economy, while a restriction on short sales by China's largest brokerage did little to spur a recovery.

- Nikkei 225 was underpinned and briefly climbed above 36,000 after Japanese CPI data continued to soften and a source report noted there was no pressure for the BoJ to rush towards the exit.

- ASX 200 climbed back above 7,400 with the advances led by tech after similar outperformance stateside.

- Indian stocks advanced, on track for their first gain in four days, tracking regional peers boosted by a rally in chip shares. The S&P BSE Sensex rose 0.9% to 71,844.37 as of 09:30 a.m. in Mumbai, while the NSE Nifty 50 Index advanced 0.9% to 21,655.75.

“When TSMC reports a strong outlook, you know there will be other winners in the space — market focus is likely to return to other chip stocks and AI plays,” said Charu Chanana, a market strategist at Saxo Capital Markets. “The recovery comes in somewhat faster-than-expected.”

In FX, the Bloomberg Dollar Spot Index dropped 0.1%, its second consecutive day of decline, yet the gauge remains on track for its third straight week of gains as expectations of a Federal Reserve rate cut recede; USDJPY rose 0.4% before paring gains to trade flat at 148.08; Japan’s finance minister Shunichi Suzuki said the government is closely watching FX movements. GBPUSD fell as much as 0.3% to 1.2666, reversing two sessions of gains; after UK retail sales slumped at their fastest pace since January 2021.

In rates, Treasuries trade little changed across the curve. Gilts rallied on the increasing prospect of recession after UK retail sales fell at their fastest pace since Covid-19 lockdowns three years ago. UK 10-year yields drop 3bps to 3.90%.

In commodities, oil was steady after closing at a three-week high on escalating tensions in the Middle East. WTI rose 0.8% to trade near $74.70. Spot gold added 0.3% but was headed for a weekly loss on the recalibration of Fed rate-cut bets.

Bitcoin rose +0.7%, amid attempts to pare back some of the prior day's hefty losses, though still remains below $41.5K.

To the day ahead now, and data releases include German PPI and UK retail sales, and US existing home sales for December. Otherwise in the US, there’s also the University of Michigan’s preliminary consumer sentiment index for January. From central banks, we’ll hear from ECB President Lagarde, along with the Fed’s Daly and Barr.

Market Snapshot

- S&P 500 futures up 0.3% to 4,827.25

- STOXX Europe 600 up 0.3% to 471.69

- MXAP up 1.1% to 163.86

- MXAPJ up 1.2% to 498.73

- Nikkei up 1.4% to 35,963.27

- Topix up 0.7% to 2,510.03

- Hang Seng Index down 0.5% to 15,308.69

- Shanghai Composite down 0.5% to 2,832.28

- Sensex up 0.6% to 71,625.04

- Australia S&P/ASX 200 up 1.0% to 7,421.24

- Kospi up 1.3% to 2,472.74

- German 10Y yield little changed at 2.34%

- Euro little changed at $1.0882

- Brent Futures up 0.6% to $79.61/bbl

- Gold spot up 0.3% to $2,028.90

- U.S. Dollar Index down 0.16% to 103.37

Top Overnight News

- China’s largest brokerage has suspended short selling for some clients in mainland markets amid a deepening rout in the nation’s stocks. State-owned Citic Securities Co. has stopped lending stocks to individual investors and raised the requirements for institutional clients earlier this week after so-called window guidance from regulators. BBG

- China has said it will rein in expansion of the country’s electric vehicle sector, as Beijing responds to western criticism of its industrial and trade policies that have contributed to a wave of Chinese car exports. FT

- Japan’s core CPI cooled to +3.7% in Dec, inline with expectations and down from +3.8% in Nov, a number that removes pressure from the BOJ. RTRS

- British retailers suffered the biggest drop in sales for almost three years during December, raising the risk that the economy slipped into recession late last year, official data showed on Friday.

- The Office for National Statistics (ONS) said people doing Christmas shopping earlier than usual - especially for food - contributed to retail sales volumes shrinking 3.2% between December and November. It was the biggest monthly drop since January 2021 and left the level of sales at its lowest ebb since May 2020. RTRS

- Germany’s construction union has demanded a pay rise of more than 20 per cent for many of the sector’s 930,000 workers, which economists warn could stoke inflation fears and delay interest rate cuts by the European Central Bank. FT

- Blackstone’s Steve Schwarzman says inflation is already near 2%, lower than what the formal gov’t statistics signal (“I think they’re the wrong numbers…the numbers that the Fed are using are overstated”). Barron's

- Congress passes legislation shifting the gov’t shutdown dates to Mar 1 and May 8 (from Jan 19 and Feb 2). WaPo

- Arab states are working on an initiative to secure a ceasefire and the release of hostages in Gaza as part of a broader plan that could offer Israel a normalization of relations if it agrees to “irreversible” steps towards the creation of a Palestinian state. FT

- META CEO Mark Zuckerberg said the company will have 350,000 Nvidia H100 graphics processing units and overall almost 600,000 H100 compute equivalent GPUs by the end of this year. Barrons

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly took impetus from the tech-led advances on Wall St where sentiment was underpinned after initial jobless claims fell to the lowest since September 2022 and with tech encouraged by TSMC's earnings which lifted the Co.'s shares by over 6% and underpinned other chipmakers including Samsung Electronics. ASX 200 climbed back above 7,400 with the advances led by tech after similar outperformance stateside. Nikkei 225 was underpinned and briefly climbed above 36,000 after Japanese CPI data continued to soften and a source report noted there was no pressure for the BoJ to rush towards the exit. Hang Seng and Shanghai Comp were subdued amid the lingering concerns surrounding an uneven recovery in the Chinese economy, while a restriction on short sales by China's largest brokerage did little to spur a recovery.

Top Asian News

- China's MOFCOM said it hopes all parties concerned will restore and ensure the security of shipping lanes in the Red Sea and it hopes all parties jointly safeguard the smooth flow of global production, supply chains and normal order of international trade. Furthermore, it stated that China will strengthen coordination with relevant departments, closely track developments and provide timely support and assistance to foreign trade enterprises.

- Japanese Finance Minister Suzuki said forex moves are driven by various factors and the government is watching forex developments carefully, while he reiterated it is important for FX to move stably reflecting fundamentals. Suzuki also stated that he won't comment in advance about what the government expects the BoJ to do but hopes the BoJ guides policy appropriately, working closely with the government to sustainably achieve the 2% inflation target.

- Moody's cuts Huarong Asset Management to Junk, according to Bloomberg

- China's cabinet has reportedly instructed heavily indebted governments to halt some unfinished infrastructure projects, according to Reuters sources; Beijing is said to be concerned about potential default due to local governments' large debts.

- China securities regulator said will strengthen supervision over stock index futures trading to safeguard market stability. No signs yet of the intensive build-up of short positions in stock index futures.

European bourses are modestly firmer but with price action contained amid a lack of pertinent catalysts; the FTSE 100 (+0.5%) leads amid the softer Pound and lower yields. European sectors hold a slight positive tilt; Travel & Leisure outperforms, Tech continues to build on the prior day's advances whilst Consumer Products is hampered as Luxury gives back some of yesterday's gains. US equity futures are firmer across the board to varying degrees. The NQ (+0.7%) continues yesterday’s outperformance. BASF (BAS GY) FY Prelim (EUR): adj. EBIT 3.81bln (exp. 3.85bln); Sales 68.90bln (exp. 70.58bln); Miss in forecasts "primarily attributable to non-cash-effective impairments in the amount of EUR 1.1bln".

Top European News

- UK Chancellor Hunt has given strong hints that he wants to cut taxes in the spring budget, according to the BBC. He did not offer any further detail on the scale of potential future tax cuts, as the government awaits an assessment from the Office for Budget Responsibility (OBR). It is widely expected that the chancellor will focus on income tax in the budget on 6 March, BBC said.

- SNB's Jordan said that additional rate hikes from the Bank are not necessary to maintain price stability, according to Aargauer Zeitung

FX

- A contained session for the Dollar thus far in narrow 103.31-51 ranges amid a lack of pertinent catalysts and a light docket ahead; DXY resides within yesterday's 103.14-63 range on either side of its 200 DMA (103.45).

- A flat session for the EUR amidst a quiet morning with little price action seen on the sub-forecast German PPI metrics; EUR/USD trades within yesterday's 1.0845-1.0906 parameter.

- GBP is the G10 underperformer (albeit narrowly) in the aftermath of the dismal UK Retail Sales data; Cable found resistance just above its 21 DMA (1.2708) and matched yesterday's high.

- Antipodeans are mixed trade across the antipodeans with the AUD propped by a rise in base metals whilst NZD is subdued following a further contraction in Manufacturing PMI.

- PBoC set USD/CNY mid-point at 7.1167 vs exp. 7.1972 (prev. 7.1174).

Fixed Income

- USTs are flat following yesterday's bear-steepened as the long end failed to recover from the larger-than-expected drop in US jobless claims; Resistance at 111-21 and support at the 38.2% Fibonacci retracement level from Oct 19 at 110-14.

- Gilts saw a marginal gap higher at the resumption of trade following the dismal UK Retail Sales metrics, which saw the contract open at 98.90 (vs yesterday's 98.71 close).

- Another choppy morning within narrow ranges for Bunds with horizontal trade seen in APAC hours following yesterday's fall under 134.00 after yesterday's US data.

Commodities

- WTI and Brent continue to extend on gains after settling higher by over USD 1/bbl apiece yesterday; Brent Mar resides above USD 79/bbl and found resistance just before USD 79.50/bbl.

- Modest upside bias in precious metals as the DXY remains caged whilst geopolitics could be underpinning the yellow metal as prices were largely unfazed by yesterday's US data; XAU found support at near its 50 DMA (USD 2,019.74/oz).

- Base metals are firmer across the board despite relatively muted price action elsewhere, with copper continuing to edge higher.

- Russia's Kremlin said there is no prospect of reviving Black Sea Grain deal, said alternative routes to ship Ukrainian grain carry huge risks

- Saudi Finance Minister said Saudi Arabia is not worried about the oil price, via BBG interview

Geopolitics

- Yemen's Houthis military spokesman said naval forces carried out an operation against the American ship Chem Ranger in the Gulf of Aden with naval missiles, while the US military later stated Houthis launched two anti-ship ballistic missiles at a US-owned tanker ship and that there was no reported damage or injuries.

- North Korea said it conducted a test of an underwater nuclear weapons system and that the test was in response to joint military drills involving South Korea, the US and Japan, according to KCNA.

- Belarusian Defence Minister said Belarusian new defence doctrine defines actions in case of aggression against CSTO allies, according to Tass

US Event Calendar

- 10:00: Jan. U. of Mich. Sentiment, est. 70.1, prior 69.7

- Jan. U. of Mich. Current Conditions, est. 73.0, prior 73.3

- Jan. U. of Mich. Expectations, est. 67.0, prior 67.4

- Jan. U. of Mich. 1 Yr Inflation, est. 3.1%, prior 3.1%

- Jan. U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 2.9%

- 10:00: Dec. Existing Home Sales MoM, est. 0.3%, prior 0.8%

- 10:00: Dec. Home Resales with Condos, est. 3.83m, prior 3.82m

- 16:00: Nov. Total Net TIC Flows, prior -$83.8b

Central bank speakers

- 08:30: Fed’s Goolsbee Speaks on CNBC

- 11:15: Fed’s Daly Speaks on Fox Business

- 13:00: Fed’s Barr Speaks About Bank Regulation

DB's Jim Reid concludes the overnight wrap

Risk assets found a firmer footing over the last 24 hours, with the S&P 500 (+0.88%) posting a solid recovery as an upbeat 2024 outlook by chipmaker TSMC drove an outperformance from tech stocks that saw the Magnificent 7 (+1.35%) reach a new all-time high. By contrast, bonds continued to struggle, and the 1 0yr Treasury yield (+3.9bps) hit a one-month high of 4.14% after US data continued to surprise on the upside, and overnight it’s risen further to 4.16%. That was mainly driven by positive data, including the weekly initial jobless claims which fell to just 187k over the week ending January 13 (205k expected), marking their lowest level since September 2022. So that offered yet more evidence of US economic resilience, and the data increasingly looks like a trend, since the release also pushed the 4-week average to its lowest since February.

But it was renewed tech optimism rather than the positive data that helped equities post solid gains yesterday, and the S&P 500’s advance (+0.88%) means the index is now less than half a percent away from its all-time high at the start of 2022. Europe’s STOXX 600 also rose +0.59%. That optimism was driven by an upbeat outlook by the world’s largest chip manufacturer TSMC, which expects revenue growth of at least 20% in 2024. TSMC’s shares are more than +6% up in trading this morning, while its American Depositary Receipts gained +9.87% in US trading yesterday. The news boosted other chipmakers – with the Philadelphia semiconductor index up +3.36% – as well as tech stocks more broadly with the NASDAQ advancing +1.35%, whilst the STOXX Technology index in Europe was up +3.24% in its best daily performance since July. Outside of tech, equities posted more moderate gains though, and the equal weighted version of the S&P 500 (+0.52% yesterday) is still down -2.04% YTD, in contrast to a slight +0.23% gain for the regular index. So the theme of mega caps propping up the equity performance has again played out since the start of the year.

Meanwhile, bond markets continued to see the pattern of positive data pushing up longer-dated bond yields. For instance, t he 30yr Treasury yield was up another +5.4bps yesterday to 4.37%, which is its highest level in over 6 weeks. Similarly in the Euro Area, 10yr bund yields were up +3.3bps yesterday to 2.35%, up more than +45bps from their low less than a month ago. And in the near-term, the robust data meant that investors continued to dial back the prospect of a Q1 rate cut. Indeed, the prospect of a Fed cut by the March meeting was down to 56% yesterday and has moved down further to 55% overnight, its lowest since the Fed’s last meeting in December. Meanwhile at the ECB, the prospect of a cut by March is down to 19% overnight, the lowest since late November.

This pushback on rate cuts was echoed by comments from Atlanta Fed President Bostic (a voter on the FOMC this year), who said that his “outlook right now is for our first cut to be sometime in the third quarter this year”, so that’s a contrast with market pricing, which is still fully pricing in a cut by the May meeting. Remember that today is the last day before the Fed’s blackout period ahead of the next meeting, so the next scheduled remarks are Fed Chair Powell’s press conference on January 31.

For the ECB, their next meeting is now less than a week away, and yesterday saw the release of the December minutes, which showed a concern about the recent easing in financial conditions. It said that “Concern was expressed that the sharp market repricing threatened to loosen financial conditions excessively, which could derail the disinflationary process.” Nevertheless, the accounts also mentioned that “it was argued that the December staff projections for growth in the near term might be too optimistic overall”. So while at least some on the Governing Council are wary of the downside risks to the ECB’s view, the overall reaction function was still focused on ensuring disinflation continues, as seen also in recent comments pushing back at pricing of cuts. See our European economists’ full reaction to the accounts here.

Looking back at the key data yesterday, the decline in US jobless claims was a surprise for markets, and the 187k reading was beneath every economist’s estimate on Bloomberg. And on similar lines, continuing claims fell to 1.806m in the week ending January 6, which was the lowest since October (1.840m expected). That positivity was echoed in the housing data too, where housing starts only fell to an annualised rate of 1.460m in December (vs. 1.425m expected), and building permits were up to an annualised rate of 1.495m (vs. 1.477m expected).

Overnight in Asia, equity markets are mostly up this morning following the rally on Wall Street yesterday. The Nikkei (+1.19%) has posted strong gains, along with the S&P/ASX 200 (+1.02%) and the KOSPI (+0.81%). However, the Shanghai Composite (-0.68%) has lost further ground and is now at its lowest since May 2020, whilst the CSI 300 (-0.37%) and the Hang Seng (-0.28%) are also down. Otherwise overnight, Japan’s headline CPI inflation rate fell to +2.6% in December (vs. +2.5% expected), which is the lowest it’s been since July 2022. In addition, core inflation slowed to +2.3% as expected, and core-core inflation was down to +3.7% as expected, which helped to cement expectations that the Bank of Japan won’t be rushing to end its negative interest rate policy.

In US policy news, last night Congress averted a partial government shutdown that would have started this weekend, with both the Senate and the House approving the latest stopgap spending bill. T he temporary measure pushes out the deadlines into early March, giving six weeks for officials to try and agree a long-term funding bill. Another short-term continuing resolution is also possible, with the harder deadline being 30 April, when automatic sequestration spending cuts would take place if no annual funding bill is passed.

Elsewhere, data yesterday showed fresh evidence that the rise in shipping costs was continuing, with Drewry’s WCI composite index up by +23% to $3,777 for a 40ft container, marking its 6th consecutive weekly advance. That follows the attacks on commercial shipping in the Red Sea by the Houthi rebels, which has led to big diversions as container ships go round the Cape of Good Hope instead. Yesterday also saw further US strikes in response to the Houthis, and President Biden said that they would continue. The news also contributed to upside for oil, with both Brent (+1.57% to $79.10/bbl) and WTI (+2.09% to $74.08/bbl) crude prices rising to YTD highs.

To the day ahead now, and data releases include German PPI and UK retail sales, and US existing home sales for December. Otherwise in the US, there’s also the University of Michigan’s preliminary consumer sentiment index for January. From central banks, we’ll hear from ECB President Lagarde, along with the Fed’s Daly and Barr.

Uncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

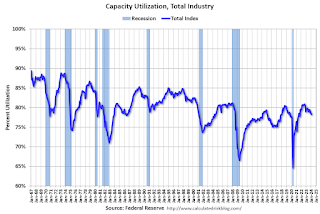

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

{kind=link}

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

{kind=link}

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

The Question You Should Ask Whenever You’re Wrong

Tight inventory and frustrated buyers challenge agents in Virginia

Futures Rise To New Record High Ahead Of Data Deluge

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex