ANN ARBOR, Mich. – As children head back to school, two issues have climbed higher on their parents’ list of concerns: the role of social media and the internet in kids’ lives.

Over half of parents also rate mental health issues as leading health concerns for children and teens, according to the University of Michigan Health C.S. Mott Children’s Hospital National Poll on Children’s Health.

Overall, emotional health and technology use dominated this year’s top 10 list of parent concerns about health-related issues for kids in the U.S.– surpassing childhood obesity, which parents rated the number one children’s health issue a decade ago.

“Parents still view problems directly impacting physical health, including unhealthy eating and obesity, as important children’s health issues. But these have been overtaken by concerns about mental health, social media and screen time,” said Mott Poll co-director and Mott pediatrician Susan Woolford, M.D., M.P.H.

Two-thirds of parents are worried about children’s increased time on devices, including overall screen time and use of social media, taking the No.1 and No.2 spots on the list of children’s health concerns this year, according to the nationally representative poll.

“Children are using digital devices and social media at younger ages, and parents may struggle with how to appropriately monitor use to prevent negative impacts on safety, self-esteem, social connections and habits that may interfere with sleep and other areas of health,” Woolford said.

Screen time became a growing concern for parents during the pandemic, previous reports suggest. Woolford encourages parents to regularly evaluate their children’s use of technology and consider limiting use if they notice signs of unhealthy interactions or behaviors. Certain social media and device settings can also help protect kids.

Mental, emotional health concerns top of mind

The poll findings, which are based on 2,099 responses collected in February, also demonstrate parents’ continued concern about children’s mental health. The majority of parents view depression, suicide, stress, anxiety, and related topics like bullying as big problems.

And nearly half of parents expressed concern with a lack of mental health services.

“The mismatch between the growing number of youth with mental health concerns and the limited access to mental health services has serious implications for children’s well-being,” Woolford said.

Parents also shared a high level of concern about school violence, which may reflect direct experience with school shootings or fights as well as media coverage about such events, Woolford says.

She adds that changes to the school environment, such as metal detectors, armed guards and locked doors, as well as active shooter drills may remind children and parents about the potential for school violence. Parents may struggle with how to manage their own stress and anxiety while they try to reassure their child.

“Parents may want to talk with their child periodically about how safe they feel at school and what they’ve heard about violent incidents,” Woolford said. “They should tailor the information to their child’s age and avoid sharing graphic details while offering reassurance about safety measures that their school has in place.”

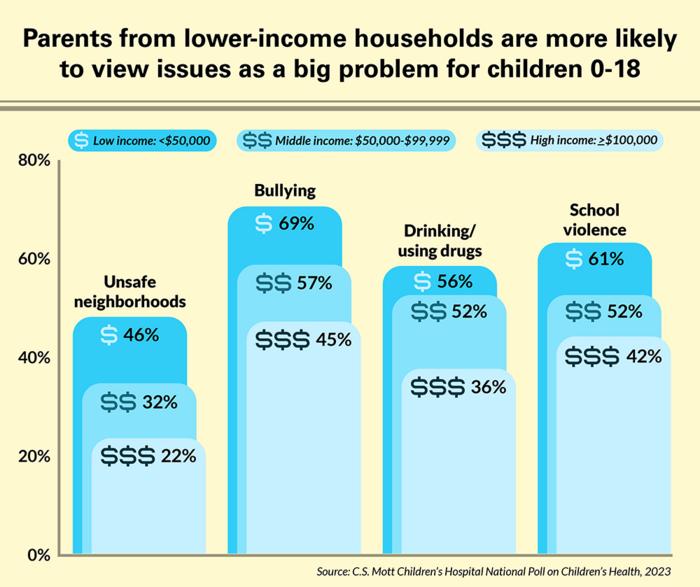

Parents in low-income households were more likely to view several children’s health issues as a major concern, including depression and suicide, bullying, school violence, unsafe neighborhoods, drinking and drugs, smoking and vaping, teen pregnancy and sexual activity, child abuse and neglect, parental stress, discrimination, COVID, and health risks from pollution.

Meanwhile, parents in middle and high-income homes are more likely to rate overuse of devices and social media as significant problems.

“Differences in how parents view children’s health problems may reflect their day-to-day experiences dealing with environmental challenges such as unsafe neighborhoods, as well as discrimination that may be more frequently experienced by children from low-income homes,” Woolford said.

Concern about a greater number of child health issues may be reflected in this group’s higher reports of parental stress as a big problem, Woolford adds.

But parents across income groups rated other topics similarly, including unhealthy diet, obesity, healthcare costs, and lack of mental health services.

Falling just outside the top 10 children’s health concerns are obesity (48%), guns/gun injuries (47%), lack of mental health services (47%), poverty (45%), drinking/using drugs (44%), child abuse/neglect (42%), followed by unequal access to health care (35%), parental stress (35%), inaccurate/misleading health information (31%), teen pregnancy/sexual activity (31%), discrimination (31%), unsafe neighborhoods (30%), gay/gender issues (LGBTQ) (29%), and health risks from polluted water and air (23%).

At the bottom of the list: safety of vaccines (16%), over-involved parents/parents doing too much (13%) and COVID (12%).

“Today’s school aged children have experienced dramatic shifts in classroom environments, technology norms and increased mental health challenges,” Woolford said.

“Parents should partner with schools, mentors and their child’s health care providers to address both ongoing and emerging health concerns. They should also regularly revisit conversations with their children and teens that encourage them to share any concerns they might be experiencing, both physically and emotionally.”