International

Office Market Availability Rate Hits Record High In San Francisco

Office Market Availability Rate Hits Record High In San Francisco

Authored by Travis Gillmore via The Epoch Times,

A confluence of factors…

Share this:

Authored by Travis Gillmore via The Epoch Times,

A confluence of factors continues to impact San Francisco’s office market, with vacancy and availability rates reaching record highs in the first quarter of 2024, according to commercial real estate analysts at global companies Avison Young and CBRE.

Availability - the combination of vacancy and sublease opportunities in the market - reached 36.7 percent of all office square footage from January to April, according to recently released market analyses from the leading commercial real estate firms.

“We’re at mostly record levels, and I say that kind of cautiously optimistic,” Dina Gouveia, west region market intelligence manager for Avison Young, told The Epoch Times April 25.

According to Ms. Gouveia vacancies only saw a “slight uptick” during the first quarter which might mean such is slowing.

“[I]f we can continue that slower velocity of additional vacancies ... then it would be a very good indicator of us being near a bottom,” she said.

Much of the issue, experts say, is the city’s reliance on the tech industry, with more than 44 percent of its office space housing technology companies.

Additionally, tech firms lead the list of upcoming lease expirations—accounting for 45.8 percent, according to Avison Young.

San Francisco’s office market was deeply affected as the number of work-from-home employees skyrocketed during the pandemic, though recent trends show a slight return to the office.

Remote job postings fell more than 5 percent to 22.2 percent in the first quarter compared to the end of last year, according to the Avison Young report.

Job postings increased 22.7 percent in the first quarter following seven consecutive quarters of decline. The listings were led by legal services, engineering, consulting, research, accounting, and recruiting companies. Media and tech industries, however, both experienced declines, according to the report.

Unemployment, however, ticked up to 4.4 percent in the first quarter, a sharp increase from its low of 2.3 percent in June 2022.

According to the report, slightly less than 1 million total square footage was leased in the first quarter—a 63.3 percent drop from the five-year pre-pandemic average.

Analysts noted signs they deemed optimistic, including Netherlands-based payment company Adyen’s sublease of space at 505 Brannan Street—in the city’s South of Market district—and multinational accounting company KPMG’s lease renewal at 55 2nd Street, in the city’s financial district. Combined, those leases total 300,000 square feet, experts said.

Sublease opportunities offer lower rents than signing new leases that require build outs and significant capital to develop properties, which is spurring the sector of the market, while also allowing businesses with existing leases to rent out some of their vacant space.

“The amount of sublease activity that we’ve seen has increased a lot because tenants are looking for plug-and-play opportunities,” Ms. Gouveia said. “A lot more activity is happening because tenants ... want to take advantage of pre-built spaces and lower rents.”

High interest rates are making it harder for companies with limited cash to refinance loans. At the same time, rates are also slowing down new purchases, according to analysts.

With an uncertain market—in part due to conflicting signals from the Federal Reserve about the future of interest rates—prospective tenants are seeking flexibility when looking to renew leases or relocate.

“Interest rates are a huge catalyst,” Ms. Gouveia said. “We’re hearing a little bit of two different stories that interest rates are going down and then they’re not. If the interest rates do come down ... that will stimulate the commercial market quite a bit.”

In response, the highest quality properties have seen lease term lengths decrease from quarter-to-quarter to make them less risky.

Such wariness from tenants is forcing some landlords to lower rents and offer concession packages to attract business, though a disparity still remains between what tenants want to pay and what landlords can offer given their current debt load.

Many landlords are working with their lenders to restructure debt before loans come due, and analysts expect rent prices to become more favorable for tenants once such is realized.

“Rents will definitely come down,” Ms. Gouveia said. “And once that debt workout happens, there’s going to be a larger reset.”

Distressed properties at risk of default are creating buying opportunities of which private buyers are increasingly taking advantage. Industrial investors and real estate investment trusts, however, are on the sidelines, with 100 percent of all investment activity coming from private buyers in the first quarter, according to the report.

On the other hand, the percentage of private sellers also increased to begin the year compared to prior years, with analysts pointing to uncertainty that their debt can be restructured due to high interest rates and limited financing opportunities.

Refinancing has proven challenging because lenders are reluctant to write loans for office buildings because defaults are looming and valuations are plummeting, with true market values unclear, according to analysts.

A pending election is also slowing activity, as many firms want more certainty before making large capital decisions.

“Because we’re coming up on an election year, a lot of companies go dormant on their expansion plans, and servicers are also in that wait-and-see mode,” Ms. Gouveia said.

Another global commercial real estate leader, CBRE, found that San Francisco’s office market is facing unique challenges given crime and homelessness impacting the city.

According to Colin Yasukochi, executive director of CBRE’s Tech Insights Center, more office tenants are signing new leases, showing a willingness to recommit to the city, but are still somewhat tentative when doing so.

“This dynamic is still somewhat tenuous as employers and their employees still have concerns about public safety and the cost of doing business,” he told The Epoch Times by email.

Noting that some workers are returning to the office for more days a week he suggested such is not enough for a recovery, which, he said, will require a desire to compete in a robust economic environment.

“Additional mandates are unlikely to increase office attendance materially at this point, but rather a booming economy will compel more people to want to be in the office and be better connected to the next growth cycle,” Mr. Yasukochi said.

While artificial intelligence could play a significant role in buoying the tech sector that the city relies on, a fast recovery, he said, is not anticipated.

“The San Francisco office market is beginning to transition out of its four-year downturn,” Mr. Yasukochi said. “While it will take many years to rebalance supply and demand, we are starting to see positive signs.”

International

From Bird Flu To Climate Snakes

From Bird Flu To Climate Snakes

Authored by Breeauna Sagdal via The Brownstone Institute,

Seasoned veterinarians and livestock producers…

Share this:

Authored by Breeauna Sagdal via The Brownstone Institute,

Seasoned veterinarians and livestock producers alike have been scratching their heads trying to understand the media’s response to the avian flu.

Headlines across every major news outlet warn of humans becoming infected with the “deadly” bird flu after one reported case of pink-eye in a human.

The entire narrative is predicated upon a long-disputed claim that Covid-19 was the result of a zoonotic jump—the famed Wuhan bat wet-market theory.

While the source of Covid is hotly contested within the scientific community, the policy vehicle at the center of this dialectic began years prior to Sars-CoV-2 and is quite resolute in force and effect.

In 2016, the Gates Foundation donated to the World Health Organization to create the OneHealth Initiative. Since 2020, the CDC has adopted and implemented the OneHealth Initiative to build a “collaborative, multisectoral, and transdisciplinary approach—working at the local, regional, national, and global levels—with the goal of achieving optimal health outcomes recognizing the interconnection between people, animals, plants, and their shared environment.”

In the aftermath of Covid-19, the OneHealth Initiative began taking shape, due largely in part to millions of tax dollars appropriated through ARP (American Rescue Plan) funding.

Through its APHIS (Animal and Plant Health Investigation System) the USDA (United States Department of Agriculture) was given $300 million in 2021 to begin implementing “a risk-based, comprehensive, integrated disease monitoring and surveillance system domestically…to build additional capacity for zoonotic disease surveillance and prevention,” globally.

“The One Health concept recognizes that the health of people, animals, and the environment are all linked,” said USDA Under Secretary for Marketing and Regulatory Programs Jenny Lester Moffitt.

According to the USDA’s press release, the Biden-Harris administration’s OneHealth approach will also help to ensure “new markets and streams of income for farmers and producers using climate smart food and forestry practices,” by “making historic investments in infrastructure and clean energy capabilities in rural America.”

In other words, the federal government is using regulatory enforcement to intervene in the marketplace, in addition to subsidizing corporations with tax dollars to direct a planned economic outcome—ending meat consumption.

Climate-Smart Commodities – Planning the Economy through Subsidized Intervention

Under the recently announced Climate-Smart Commodities program, the USDA has appropriated $3.1 billion in tax subsidies to one hundred and forty-one new private Climate-Smart projects, ranging from carbon sequestration to Climate-Smart meat and forestry practices.

Private investors such as Amazon founder Jeff Bezos – who just committed $1 billion to the development of lab cultured meat-like molds, and meat grown in petri dishes, to

Ballpark, formerly known for its hot dogs but is now harvesting python meat, is rushing to cash in on this new industry, and the OneHealth/USDA certification program.

Culling The Herd – Regulatory Intervention in the Marketplace

Meanwhile, the last vestiges of America’s food freedom and decentralized food sources are quietly being targeted by the full force of the federal government.

The once voluntary APHIS System is poised to become the mandatory APHIS-15, which among many other changes, “the system will be renamed Animal Health, Disease, and Pest Surveillance and Management System, USDA/APHIS-15. This system is used by APHIS to collect, manage, and evaluate animal health data for disease and pest control and surveillance programs.”

Among those “many changes” that APHIS-15 is undergoing, one should be of particular interest to the public—the removal of all references to the voluntary* Bovine Johne’s Disease Control Program.

“Updating the authority for maintenance of the system to remove reference to the Bovine Johne’s Disease Control Program.”

In addition to removing references to the once-voluntary herd culling program, the USDA is also implementing mandatory RFID ear tags in cattle and bison.

According to the USDA/APHIS-15, expanded authority places disease tracing in their jurisdiction and the radio frequency ear tags are necessary for the “rapid and accurate recordkeeping for this volume of animals and movement,” which they say “is not achievable without electronic systems.”

The notice clearly spells out that RFID tags “may be read without restraint as the animal goes past an electronic reader.”

“Once the reader scans the tag, the electronically collected tag number can be rapidly and accurately transmitted from the reader to a connected electronic database.”

However, industry leaders and lawmakers alike have said the database will be used to track vaccination history and movement, and that this data may be used to impact the market rate of cattle and bison at the time of processing.

Centralized Control of Processing/Production via Public-Private Partnership Agreements

In addition to the vast new authority of the USDA funded through the OneHealth Initiative, and the ARP, the EPA has also created its own unique set of regulatory burdens upon the entire meat industry.

On March 25, 2024, the EPA finalized a new set of Clean Water Act rule changes to limit nitrogen and phosphorus “pollutants” in downstream water treatment facilities from processing facilities. While the EPA’s interpretation of authority and jurisdiction over wastewater is concerning long-term, the broader context of consolidated processing under four multinational meat-packing companies is of much greater concern for the immediate future.

With few exceptions, in the United States it is illegal to sell meat without a USDA certification. Currently, the only way to access USDA certification is through a USDA-certified processing facility.

According to the EPA, the new rules will impact up to 845 processing facilities nationwide, unless facilities drastically limit the amount of meat they process each year.

With processing capabilities being the number one barrier to market for livestock producers, and billions of dollars in grants being awarded to Climate-Smart food substitutes, the amount of government intervention into the marketplace becomes very clear.

The Rise of Authoritarianism and Economic Fascism – Control the Supply

The United States, once a consumer-demand free market society, is currently witnessing the use of government force, and intervention tactics to steer and manipulate the marketplace. Similar to 1930’s Italy, this is being achieved by the state within the state, through the use of selectionism, protectionism, and economic planning between public-private partnership agreements.

The long-term and unavoidable problem with economic fascism is that it leads to authoritarian and centralized control, from which escape is impossible.

As each industry becomes centralized and consolidated under the few, consumer choice simultaneously disappears. As choice disappears, so does the ability of the individual to meet their specific and unique needs.

Eventually, the individual no longer serves a role outside of its usefulness to the state—the final exhale before the last python squeeze.

International

“Bye Bye, Babies… Bye Bye, Workers”: Can Europe Slow The Impact Of Its Aging Society

"Bye Bye, Babies… Bye Bye, Workers": Can Europe Slow The Impact Of Its Aging Society

By Erik-Jan van Harn and Maartje Wijffelaars of Rabobank

Summary

Europe’s…

Share this:

By Erik-Jan van Harn and Maartje Wijffelaars of Rabobank

Summary

- Europe’s population is aging and this will stunt economic growth in the coming decades.

- Challenges are arising for social welfare, debt sustainability, and even strategic autonomy.

- Potential remedies for the declining workforce differ per country, but overall, there are no easy solutions.

- To protect the welfare state, maintain sustainable public finances, and support Europe’s quest for strategic autonomy, higher productivity growth seems essential.

The demographic transition

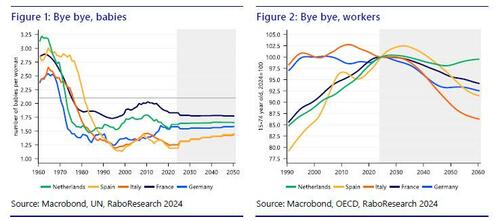

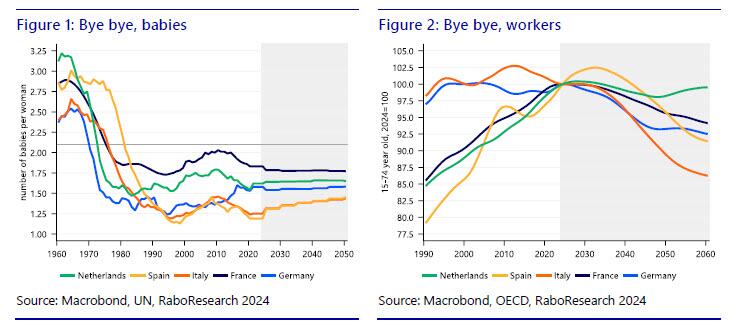

Change is often accompanied by difficulty and discomfort. Most of us are focused on the transitions that are most visible to us: the energy transition, a changing world order, or technological progress. However, there exists another, less conspicuous transition: that of demographics. Over the past six decades, fertility rates have plummeted, while life expectancy has surged to unprecedented levels. These shifts have fundamentally altered Europe’s demographic landscape and, consequently, its workforce.

Although Europe isn’t unique in this matter, it faces a pressing demographic challenge. Despite government efforts to boost fertility rates, progress remains limited. Cultural, sociological, and economic factors stubbornly outweigh incentives offered by governments. As we grapple with this persistent issue, what can we expect?

In this report, we delve into three key questions:

- How will demographics impact the structural economic growth of major member states?

- What challenges arise from this demographic shift?

- What strategies can be employed to address these challenges?

Assessing the current landscape

The labor market has been significantly strong in recent years. Unemployment rates have reached historic lows and more people have entered the workforce. But as we assess the current landscape, Europe’s long-term demographic prospects appear less than optimistic.

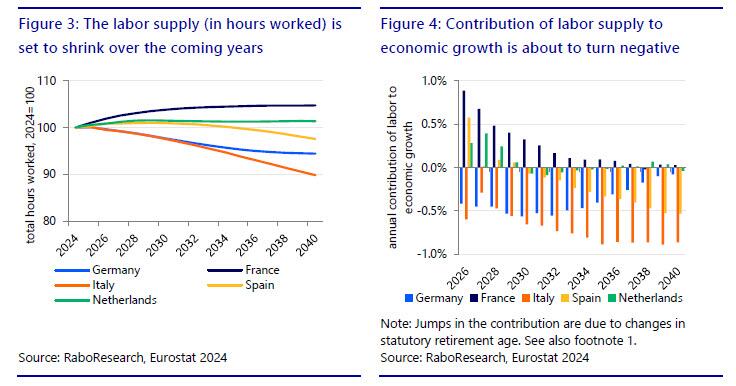

Demographics are shifting across the continent, although the impact on labor supply varies across countries. While some nations, like France, are projected to experience relatively benign demographic effects, others – such as Germany and Italy – face a less rosy outlook. For Germany, the annual labor contribution to economic growth is projected to average around -0.5% until 2035, due to the departure of baby boomers and Generation X from the workforce (see figure 4). In Italy, the challenge persists after 2035, as fertility rates and net migration are expected to remain lower than in Germany.

Spain and the Netherlands find themselves in an intermediate position. They also grapple with an aging population and its implications for the economy, but less so than Italy and Germany in the coming two decades. In both Spain and the Netherlands, it will take until 2030 before labor supply – in hours – will start to contract. But whereas labor’s annual negative contribution will remain very small for the Netherlands, it is set to grow for Spain as time progresses.

Age is just a number, but numbers do matter

Over the past decade, a growing supply of labor has played a pivotal role in driving economic growth, especially given the relatively modest productivity gains. Any decline in or negative impact on labor’s contribution could significantly impede overall economic growth. While weaker growth in the short-term may not pose an immediate crisis, sustained challenges could emerge with respect to public services, debt sustainability, and Europe’s strategic autonomy.

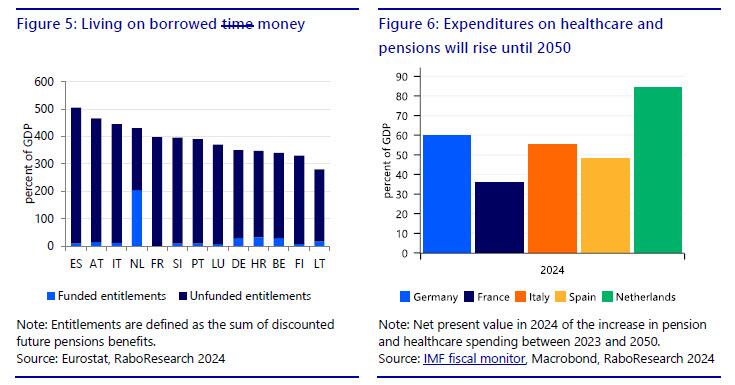

Public services and pensions

As demographic projections unfold, the number of workers available declines, and the balance between retirees and active workers shifts. Currently, there is about one retiree for every three workers in the Eurozone, but this is projected to decline to two workers by 2040. This change could strain the affordability of public services. For instance, healthcare costs are expected to rise as the population ages (see figure 6), while tax revenues may stagnate or grow at a slower pace. Another concerning issue is the sustainability of pension systems. Across most European countries, pensions operate on a pay-as-you-go model, where retirees’ benefits are funded by the contributions of the currently employed. In theory, this system functions smoothly. But as the proportion of retirees increases relative to the workforce, the burden on today’s contributors becomes substantial.

Some countries have included automatic changes to the contribution, benefits, or statutory retirement age to alleviate some of the strain on public finances when needed. In the Netherlands and Italy, for example, the statutory retirement age is linked to life expectancy. While these measures dampen the blow to some extent, the burden for public finances will likely remain large and is still projected to grow in multiple countries. This burden is especially problematic if wide access to early retirement lowers the effective retirement age, as is the case in Italy.

The Netherlands stands out from its European counterparts. Approximately half of its pension entitlements are privately funded, offering a unique approach to addressing this challenge

Debt sustainability and strategic autonomy

An aging society also poses challenges to public debt sustainability. Without substantial increases in productivity growth, we can expect a slowdown in economic growth and, consequently, a decrease in tax revenues. Simultaneously, expenditures on healthcare and pensions will rise, as illustrated in Figure 6. These trends, all else being equal, will lead to a rise in the primary budget deficit and a decrease in the affordability of debt, measured by the ratio of interest payments to revenues. A growing part of revenues will be allocated to servicing interest costs on existing debt. Corrective spending in other areas and/or tax measures will likely be necessary to prevent the overall budget balance from spiralling out of control, which would simultaneously raise financing needs and public debt. Higher productivity growth may lessen the need for austerity, as it would generate higher tax revenues with the same amount of labor, but that’s not a given. It is certain, however, that higher productivity growth makes higher taxes less painful. Furthermore, productivity and efficiency gains in the health sector could dampen the increase in healthcare spending. As such, faster productivity growth could actually be crucial to prevent a negative downward spiral between austerity measures and growth in some countries.

The demographic decline will also have implications for the geopolitical aspirations of the European Union. Firstly, it will directly impact the deterioration of debt sustainability just when the EU's strategic agenda requires substantial investments in military capabilities, the energy transition, and industrial development. Beyond the direct effects on debt servicing capacity, the demographic decline in Europe will also result in a shift in the EU's relative geopolitical power. The EU currently boasts the world's largest single market, and companies conform to EU product standards as a consequence. Therefore, the EU holds a position as a regulatory superpower. However, as Europe's consumer market shrinks in the coming decades, likely so will the power derived from it. This obviously also holds for the other forms of soft power that Europe (still) commands, such as its cultural and democratic values.

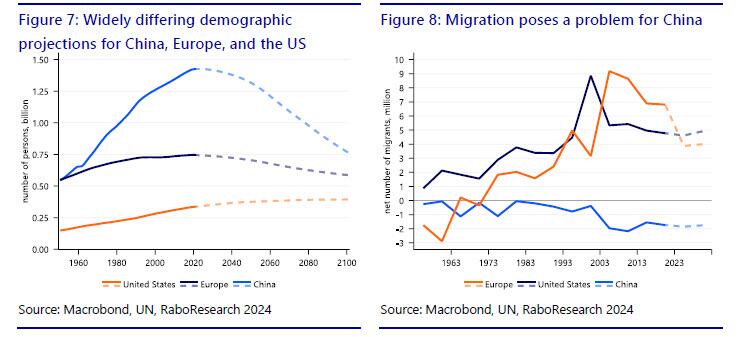

The good news for the EU with respect to its relative power on the world stage is that Europe’s problems aren’t unique and that low fertility rates and aging societies are prevalent in many countries worldwide. For instance, if current trends continue, China’s population is expected to halve in the coming decades. These long term projections are inherently uncertain, but it’s easy to argue that the demographic situation is even worse in China than it is in Europe. In addition to lower fertility rates, China also suffers from emigration. On the other hand, the United States experiences a relatively higher influx of migrants and notably higher fertility rates than Europe. With respect to demographics, the United States have the advantage.

Can we avert the decline in labor supply?

The future doesn’t look too rosy for some countries, but luckily, the changes are predictable and relatively slow. This leaves room for policy intervention. But what can governments do to avert or at least slow the projected decline in labor supply (in hours)? In broad terms, three key factors shape the total labor supply within an economy: the working age population, the participation rate, and the hours worked per worker.

Working age population

First, we consider the working-age population. In the long term, the primary drivers are the fertility rate and net migration. Recent campaigns in countries such as Denmark, Italy, and China have underscored the challenge of increasing fertility rates. You simply cannot force people to have babies and decisions are determined by multiple factors including nature, culture, and economics. Even if successful, the effects of such campaigns may take up to two decades to materialize.

Migration represents another avenue to bolster the working-age population. Spain is a good example of a country where migration mitigates the effect of an aging population. However, this path is not without hurdles. Populist sentiments in some countries have made foreign workers less welcome. Furthermore, to fully counteract the decline in the working-age population, a substantial influx of migrants would be necessary. For Germany, this could mean accommodating between 200,000 and 400,000 workers annually over the coming decades. It is no given that European countries will be able to find qualified workers abroad so easily, as language and cultural barriers further complicate things.

An alternative approach involves redefining the concept of “working age” by raising the statutory retirement age. France, for instance, elevated its retirement age from 62 to 64 last year. While this strategy proves highly effective, recent experience also highlights the contentious nature of such adjustments. French President Emmanuel Macron had to water down his initial proposal to raise the retirement age to 65, when nationwide protests crippled the country. In Italy, a 2011 pension reform linked the retirement age to life expectancy, leading to a statutory retirement age of 67 as of 2019. Yet the age at which workers actually retire is quite some years earlier, as subsequent governments have opened a door to early retirement.

Participation rate

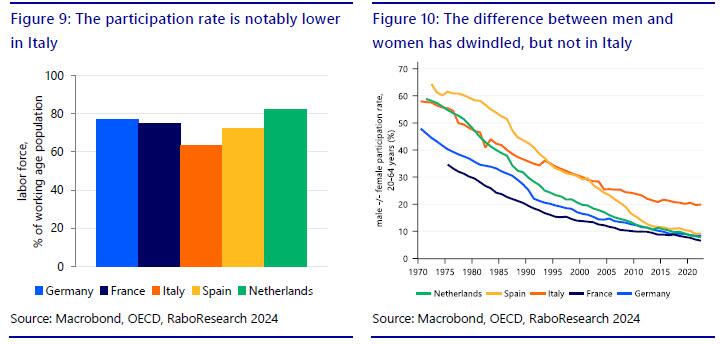

What if we could harness a larger share of our working-age population, i.e. raise the participation rate? The truth is that for most large member states, there appears to be limited room for improvement, as participation rates are high and relatively comparable. Italy is a notable outlier, however. Coincidentally, Italy also faces significant challenges. The key lies in the participation of Italian women in the labor force. Where the participation rate for Italian men closely mirrors that of other major European economies, the participation rate for Italian women is much lower. The gap in the participation rate between men and women is around 10% for most European countries, but for Italy it’s more than double that figure. If Italy can encourage more women to join the workforce, it may partially mitigate the pressing issue of its declining working age population.

Average hours worked

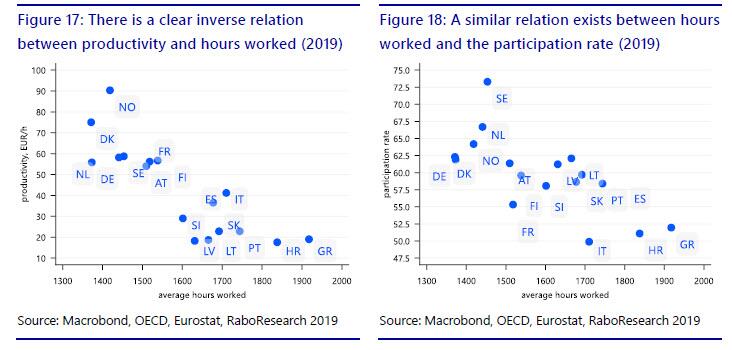

What if workers simply worked more? In comparison to Asia or North America, Europeans are often both ridiculed and envied for their extended summer holidays and nine-to-five work mentality. While there is some truth to this perception, significant variations exist within the Eurozone.

Consider Greece, where workers log an average of over 1,900 hours per year – approximately 8% more than their counterparts in the United States. Conversely, in Germany for example, employees annually work around 500 hours less than in Greece. However, convincing European workers to increase their hours isn’t easy, as the trend currently leans in the opposite direction – though Italy has bucked that trend since the pandemic. While composition effects of the workforce play a role, there also appears to be a structural shift in Europeans’ work-life balance. If anything, the tightness of the labor market and historically low share of people wanting to work more hours than they do, suggests it is more an issue of supply rather than demand. So encouraging Europeans to work more hours will require robust incentives. Governments are exploring how to reverse the current trend, but haven’t had much success yet.

Which measures would have the biggest impact?

Thankfully, the demographic changes unfolding across Europe are both predictable and quantifiable. This foresight grants governments a crucial window of opportunity to take action before challenges escalate. Our analysis has delved into the three factors determining the labor supply: working-age population, participation rates, and average hours worked per worker. To assess what can be done, we tune each variable separately. While isolating these effects may be unrealistic, it does clearly show which areas countries can improve in.

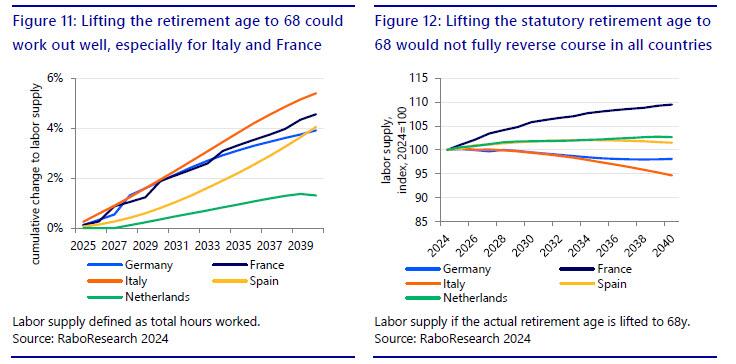

Increase the statutory retirement age

Let’s look at the impact of changes to the working-age population. Raising the retirement age will certainly not be a popular measure. Yet given Europe’s current political climate, it might be more feasible than significantly increasing net migration. We’ve raised the statutory retirement age to 68 by 2034 across all countries in this exercise.

This adjustment would particularly benefit Italy and France. While Italy boasts a relatively high statutory retirement age (67 years and 3 months), only a fraction of Italians work until that age due to early retirement provisions. Given the size of this cohort, a higher actual retirement age could make an impact, but would still fall short in fully reversing the demographic challenges.

France stands in a different position. The country would largely benefit from the fact that its current retirement age falls well below 68, and its relatively positive demographic prospects could further improve.

For the Netherlands, Germany, and Spain, the effect is more modest. These countries already maintain higher participation rates for the specific age cohort compared to others. Unsurprisingly, adjusting the retirement age alone won’t fully counteract the demographic decline in Germany either.

Increase the participation rate

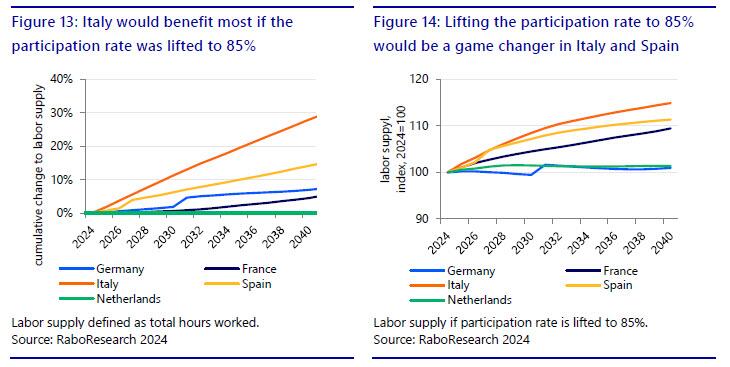

Another approach worth considering is boosting labor participation rates. Our analysis assumes a gradual improvement in the participation rate for the working-age population, aiming for an ambitious target of 85%, which is in line with the participation rate in the Netherlands.

As anticipated, this adjustment would yield remarkable results for Italy. The participation rate is projected to surge by over 20%-points (or more than 30% in relative terms), providing a much-needed boost. Remarkably, this increase could even reverse the anticipated decline in the labor supply, fostering growth. Spain would also benefit, albeit to a lesser extent. Since we raised the participation rate to the Dutch level, there’s no impact for the Netherlands. But of course, and in contrast to the statutory retirement age, governments cannot simply “press a button” to raise the activity rate. It may require a host of measures and incentives that work both on the demand and supply side of the labor market.

Increase the average hours worked

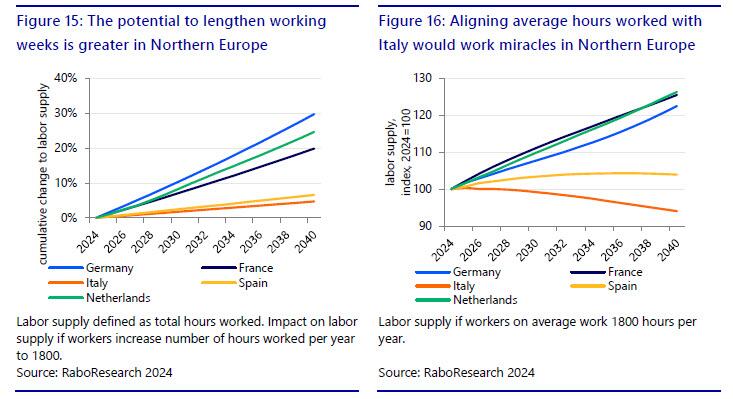

During the pandemic, average hours worked per worker in the Eurozone experienced a significant decline and in many countries, they haven’t returned to pre-pandemic levels. In some countries, the decline follows a trend that already started (long) before the pandemic. In others, a clear intensification or “new” trend is visible. In our scenario, we assume that average hours worked rises to 1800, just above the average hours worked in Italy.

The impact would be most pronounced in Western Europe, where workers currently log fewer hours. For instance, in Germany, this change would lead to a 30% increase in the labor supply. In Southern Europe, where workers already put in more hours on average, the effect would be less pronounced. Such a dramatic increase in hours worked in Western European countries would very likely lead to a worsening of other parameters, like the participation rate, as we will show in the next paragraph. Still, it underscores the potential for improvement from this perspective.

No silver bullet, just a silver tsunami

While the data above appears promising, we can hardly expect these factors to improve in isolation. There is a strong correlation between productivity, hours worked, and labor participation rates. However, the causal relationship is not entirely clear. Improved productivity could translate to fewer hours worked as the necessity for longer workweeks to sustain a certain lifestyle diminishes, for example. On the other hand, working less hours could also lead to higher productivity because of diminishing returns. Similarly, a reciprocal relationship exists between participation rates and hours worked. Individuals entering the labor force when participation rates are already high tend to work fewer hours. This likely results from maintaining an adequate worklife balance at the household level, especially when children are involved.

This sobering reality suggests that there is no silver bullet for these challenges, unless workers can be persuaded to make changes independently. Whether it’s working more hours, extending their careers, or maintaining full-time contracts even as productivity and participation rates improve, each scenario requires serious effort to convince workers. The Italians have recently demonstrated that such a thing is indeed possible. Average hours worked have risen compared to pre-pandemic years, despite the fact that the participation rate has continued to increase. Going against the usual current will require some extra commitment though.

Productivity growth remains an open question

In addition to addressing the demographic decline by encouraging increased workforce participation, another crucial factor to consider is enhancing productivity levels. Higher productivity growth could mitigate the negative impact of declining labor supply on the economy. However, achieving this goal is far from straightforward. Despite numerous attempts to revive it, productivity growth in the Eurozone has essentially halved since the Global Financial Crisis (GFC). While there are high expectations for technological advancements in AI to turn the tide, the current level of uncertainty makes it too challenging to make any definitive conjectures about the potential breadth and significance of such a productivity boost. The same holds for the impact of reforms and investments spurred with the EU’s Recovery and Resilience Facility, especially in Southern Eurozone member states. This is also true initiatives to strengthen Europe’s strategic autonomy by focusing more investment in sustainable energy, the semi-conductor sector, etc. These questions, however, are beyond the scope of this research note.

Conclusion

Decades ago, it was already clear that Europe would have to face the problems of its aging population at some point. Although governments have prepared themselves to some extent, it is unlikely to be enough to turn the tide. A shrinking (working) population will put a dent in Europe’s economic outlook, even if the potential of the working-age population is stretched to its limits. Lower economic growth does not automatically imply lower welfare to the same extent, given that you have to share the pie with fewer people. That said, it will have a profound impact on factors such as the affordability of public services and social benefits, debt sustainability, and on the Europe’s relative power compared to both its allies and rivals. In order to maintain the welfare state and prevent a negative spiral of austerity and economic growth, governments will likely have to both incentivize labor supply and find ways to improve the productivity of its workforce. This is easier said than done.

Full pdf available here.

Government

Bird-Flu, Censorship, & 100 Day Vaccines: 7 Predictions For “The Next Pandemic”

Bird-Flu, Censorship, & 100 Day Vaccines: 7 Predictions For "The Next Pandemic"

Authored by Kit Knightly via Off-Guardian.org,

Earlier…

Share this:

{kind=link}

{kind=link}

{kind=link}

Authored by Kit Knightly via Off-Guardian.org,

Earlier this month the White House published its new “Pandemic Preparedness” targets.

{kind=link}

They are far from alone in covering this. Back in March, Sky News was asking: “Next pandemic is around the corner,’ expert warns – but would lockdown ever happen again?”

On April 3rd, the Financial Times asked something similar: “The next pandemic is coming. Will we be ready?”

Less than an hour ago, the Daily Mail invited us inside “the world’s deadliest cave that could cause the next pandemic”.

Just two days ago a professional panic spreader wrote for CNN:

The next pandemic threat demands action now!!!

OK, I added the exclamation points, but they are very much implied in the original text.

So, while Iran and Israel rattle their sabres on the front pages, I thought we should take a look at the quieter back pages to see what we can learn, and help us predict how “the next pandemic” will unfold.

WHAT IS “THE NEXT PANDEMIC”?

I mean…I feel like that’s fairly self-explanatory.

Seriously though, it’s the one they’ve been predicting from pretty much the moment Covid started. First it was going to be monkey pox – sorry MPox – but that fizzled.

Of course by “pandemic”, we really mean “psy-op”, because nothing about the next pandemic will be any more real than the last pandemic. Hell, given the leaps forward in AI technology, it could be considerably less real next time.

We don’t know any of the details yet, but there’s enough vague coverage to tease out some guesstimates.

WHAT DISEASE WILL THEY USE?

Probably the most important question. We already mentioned monkey pox, but that doesn’t look likely anymore.

Right now they are mostly talking about “disease X” – a term which caused a little panic in certain sections when it first appeared on the scene – but that isn’t some top secret gain of function super disease, it’s literally a place holder name.

And it’s a placeholder name which does its job, for the time being.

After all, they don’t really need an actual name yet, any more than they need an actual disease, they just need the idea of a disease to hold over people’s heads while they construct the legislative rules of their health-based tyranny.

Indeed, the vagueness “Disease X” provides is helpful, as it keeps the legislation vague too.

That said, they will likely want and/or need to produce an actual disease at some point.

When that time comes around, it will almost certainly be another respiratory disease, because they are easy to “fake” using pre-existing endemic diseases and their uniform symptoms.

The prime candidate is bird flu, which has been slow-boiling in the news for two years now and has recently got a big uptick in coverage due to it allegedly passing to people from cows.

The UN reports “pandemic experts” are “concerned over avian influenza spread to humans”. Just yesterday, Jeremy Farrar of the World Health Organization (WHO) warned that “[the] threat Of Bird Flu spreading to Humans is a great concern”

Prompting gleefully sensationalist headlines like this from the Daily Star:

New pandemic ‘expected’ as human-to-human bird flu of ‘great concern’ to WHO

Bird flu is a convenient pick because it enables them to push their health tyranny and their food transition at the same time. They can claim that dairy, beef, chicken and eggs have become “dangerous” as an excuse to ration them or at least force scarcity while they drive the prices up.

They will then push the idea that veganism and/or lab grown meat “prevents pandemics”. Something they’ve been claiming since at least 2021.

The Daily Mail reported just a few hours ago:

H5N1 strain of bird flu is found in MILK for first time in ‘very high concentrations,’ World Health Organization warns

The downside to bird flu is that it’s hard to work the climate change angle into the narrative, so maybe they’ll go with something else.

WHEN WILL IT HAPPEN?

Probably not until the winter, I would guess January 2025 at the earliest, for two reasons:

- They need it to be flu season so they can co-opt normal seasonal deaths into their “pandemic” narrative.

- I think they’ll want to wait until after the “big election year” is over so there are fresh governments in place.

That second point is not just a hunch, but based on the article from Sky I mentioned above. It asks “would lockdown ever happen again?”, and an “expert” answers [emphasis added]:

…if another lockdown was needed, the current Tory government would either have to minimise scandals over their own rule-breaking – or change hands completely to keep the public on board. If we had a new government, people would be far more likely to have faith in them because they would be less likely to say, ‘it’s the same bunch as before – why should we do it again?’

Which I think is correct.

That would also explain the raft of sudden political resignations – including Covid stars Angela Merkel and Jacinda Ardern – which swept the world in Covid’s wake. They were aware then, and are still aware now, their players were spent and they needed a fresh roster before coming back for the second leg.

So, elections first – with all the nonsense that entails – then maybe the “next pandemic”.

HOW WILL IT BE DIFFERENT FROM “COVID”?

Any future pandemic psy-op will be unlikely to follow the covid pattern beat-for-beat, for one thing the Covid narrative spent itself before achieving everything it was meant to achieve.

You can bet the farm that, in the four years since, there have been working groups and researchers poring over the pandemic data to figure out what went wrong and how they can fix it next time.

There seem to be three recurring themes.

1. Vaccines not lockdowns There will be a focus on securing vaccines rather than lockdowns. Indeed, part of the whole “aw shucks lockdowns were damaging who’d have thunk it” rigmarole is about setting up the dynamic that “next time” we need to do anything we can to avoid lockdowns.

Lockdowns will become a threat rather than a fact.

“We HAVE to mandate vaccines, because the economy can’t afford another lockdown.”

“Take the vaccine, you don’t want to have another lockdown do you?”

So there will be more testing, more masks and more vaccine mandates…and/or quarantine camps for the unvaccinated. And if they DO have lockdowns, they will be entirely blamed on the “anti-vaxxers”, of course.

2. Speed speed speed The main failing of the Covid narrative was that it ran out of steam. By the time the vaccines rolled out in early 2021 the pandemic fatigue was already setting in. And by the time the third boosters and fourth waves were in the headlines nobody really cared.

The propaganda blitzkrieg of early 2020 was arguably the greatest and most wide-reaching misinformation campaign of all time – and it was almost overwhelmingly effective. But it slowed, stalled, stopped and staled.

Next time, they know now, they need to be faster. Bill Gates said as much at the 2022 Munich Security Conference. They need to get the disease out the deaths up and vaccines in before people even realise what happened.

Hence the “100 day vaccines” plan. As the ever-reliably-hysterical Devi Shridar writes for the Guardian:

most governments are working towards the 100-day challenge: that is, how to contain a virus spreading while a scientific response, such as a vaccine, diagnostic or treatment, can be approved, manufactured and delivered to the public.

The “100 Day Mission” is the brainchild of CEPI, the Gates and WHO-backed NGO. Its main aim is to make it possible to produce new vaccines for previously unknown pathogens in 100 days.

In the US, the target is 130 days from pathogen discovery to nation-wide vaccine coverage.

It should go without saying that real, reliable, “safe and effective” vaccines cannot be produced in 100 days. Whatever they make, sell and force you to inject in that time…it won’t be a vaccine

3. Free Speech is Dangerous. The slow development of the narrative post-2020 may have hindered the health tyranny agenda, but it was the independent media that really hurt it. The impromptu network of dissident experts, independent researchers and social media movements spread “misinformation” faster than the powers-that-be could fact-check it.

We have seen perpetual messaging about the dangers of “misinformaion and disinformation” since then, including prominently at the most recent DAVOS summit earlier this year, where it was labelled one of the “three greatest dangers” facing the planet.

Last week, a UK Parliamentary Committee published “recommendations” headlined:

Government should learn lessons from pandemic to improve communications and counter misinformation

Only a few days ago, Gordon Brown was quoted in the news “warning” that:

“fake news’ risks preparations for next pandemic”

Which heavily implies they will move to counter this “fake news” before the “next pandemic” begins.

WILDCARD PREDICTION: The multipolar angle. Whatever form the “next pandemic” takes, they will likely avoid the monolithic messaging of 2020, where total global conformity to “the message” was one of the real telltale signs of deception. Next time prepare for countries like India, China and Russia to forge their own pandemic strategy – focusing on some new treatment or technology that the West refuses to endorse.

There are no sources to back this one, yet. It’s just a gut feeling.

*

So what am I officially predicting for the “next pandemic”?

- It will won’t be launched until after the major elections this year, because they want new politic faces untarnished by Covid

- It will likely be bird flu or some other respiratory disease, launched in the winter to hijack the real flu season again

- The chosen disease will fit into one or more pre-existing agenda – either impacting food or originating from some forced “climate change” connection or both

- They will move faster, producing “vaccines” in 100 days to stop people getting wise to the deception as they did with Covid

- They will try and avoid lockdowns, but use them as a threat to enforce vaccine mandates more rigorously

- They will clamp down harder on “mis- and dis-information” before launching the new narrative.

- The next pandemic will have a multipolarity angle to establish a fake binary

That’s how I see it. Feel free to bookmark this post for future reference.

Even if I’ve guessed the details wrong here, there’s no question they are planning to roll out another pandemic at some point in near future. A covid sequel that learns from past mistakes.

While, in some ways, it will likely be worse than Covid was – the good news is that this time we can be ready for it.

Ryanair CEO goes on tirade about frequent flyer loyalty

From Bird Flu To Climate Snakes

Excess Deaths In Japan Hit 115,000 Following 3rd COVID Shot; New Study Explains Why

The CEO of a major airline is a former flight attendant

Mobile device location data is already used by private companies, so why not for studying human-wildlife interactions, scientists ask

Ryanair CEO goes on frequent flyer tirade: ‘If you want loyalty, get a dog’

‘For Your Own Safety’: USC Cancels Commencement To Avoid Pro-Palestinian Protesters

Food insecurity is significant among inhabitants of the region affected by the Belo Monte dam in Brazil

Ryanair CEO thinks frequent flyers should get no perks

Bird-Flu, Censorship, & 100 Day Vaccines: 7 Predictions For “The Next Pandemic”

-

Government3 weeks ago

Government3 weeks agoClimate-Con & The Media-Censorship Complex – Part 1

-

Spread & Containment1 week ago

Spread & Containment1 week agoJ&J’s AI head jumps to Recursion; Doug Williams resigns as Sana’s R&D chief

-

Government4 days ago

Government4 days agoCOVID-19 Vaccine Emails: Here’s What The CDC Hid Behind Redactions

-

Spread & Containment2 weeks ago

Spread & Containment2 weeks agoWHO Official Admits Vaccine Passports May Have Been A Scam

-

Spread & Containment3 weeks ago

Spread & Containment3 weeks agoFDA Finally Takes Down Ivermectin Posts After Settlement

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoVaccinated People Show Long COVID-Like Symptoms With Detectable Spike Proteins: Preprint Study

-

Uncategorized1 day ago

Uncategorized1 day agoPopular fast-food restaurant chain files Chapter 11 bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCan language models read the genome? This one decoded mRNA to make better vaccines.