Uncategorized

Luongo: BRICS Summit Proves Geography Trumps Currency

Luongo: BRICS Summit Proves Geography Trumps Currency

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

The older I get the more time…

Share this:

Authored by Tom Luongo via Gold, Goats, 'n Guns blog,

The older I get the more time I spend asking the question, “Why does someone want me to know this?” Our media is so compromised that questioning the editorial bias of every issue is a full time job.

And I know that it is done on purpose to distract us from the real issues in some instances while advancing an agenda in others.

In 2023, the topic of de-dollarization has been all the rage. It’s been a non-stop barrage of hype and hyperbole. The din of de-dollarization talk became so loud in the lead up to the recent BRICS Summit that it drowned out what was really on the agenda for those few days.

This talk came from all sides, from the BRICS leaders themselves as well as the western press dominated by both British and Davos interests.

People fell all over themselves talking up the “BRICS gold-backed currency” trying to edge each other out in being ahead of the curve on this issue. After a while it became another moment to ask who benefits from all of this amplification?

I’ve been writing about these things for years, knowing that those who control the production of commodities would ultimately get tired of the wealth extraction schemes operated by the financialization masters in New York, London, and Zurich.

It was only a matter of time before they would make their move.

And I can tell you for real that I’ve never been amplified on any subject like this until such time as people in Moscow, Brussels and Beijing wanted this commentary out there.

Don’t take this for grousing, because it isn’t. It’s just an observation born of years of experience. I’ve come to understand what a lack of amplification means; that this is the story no one wants to be told.

So, this begs the question, why do they want it told now?

In many ways this is how I know I’m usually on the right track with respect to a particular issue. It’s my forever internalizing the baseball great Wee Willy Keeler who famously said that baseball is an easy game, “Just hit ’em where they ain’t.”

So, a lot of important someones wanted us to know about de-dollarization this year.

They had their reasons to promote this concept. And, as always, it has to do with influencing global capital flow while distracting the commentary from what was really on the agenda.

For Davos de-dollarization is just another attack vector on the United States.

By playing up the problems the US has domestically as well as geopolitically they create uncertainty. Capital hates uncertainty.

Throw in a purposefully-belligerent and incompetent “Biden” administration and you have a perfect cocktail of uncertainty which keeps capital markets globally distrustful of both the near-term policy mixed with the long-term trends.

Conclusion? The US is FUBAR.

Russia is at war with the West, so, of course, Vladimir Putin will talk his book on de-dollarization. He is the point man on the BRICS being “anti-dollar.”

There’s only this one little problem with all of this: The US dollar itself and the lack of alternative infrastructure for ditching it. Despite all of the jawboning and, frankly, propaganda on this subject, the reality is far, far different.

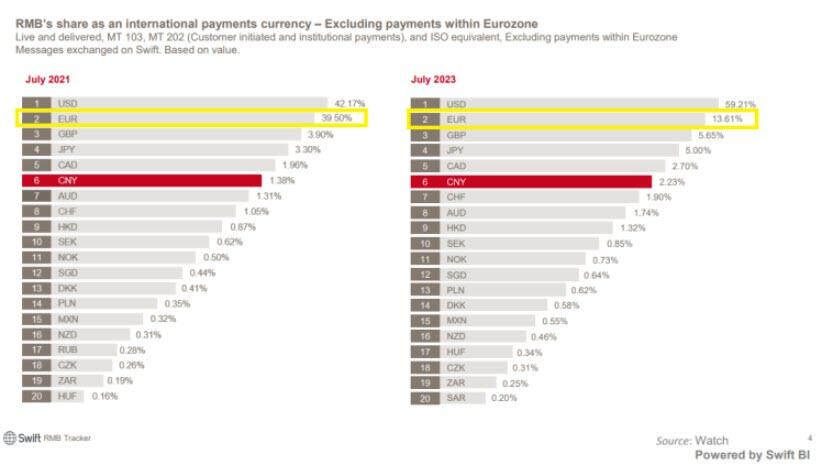

While everyone is talking de-dollarization, the real currency losing it’s position in global trade is the euro. But no one is talking about de-eruoization. I guess it doesn’t roll off the tongue as well?

According to the latest data from the SWIFT RMB Tracker, there is no currency that has lost more ground in global trade than the euro. In just over two years the euro has fallen from 39.5% of global payments outside the euro-zone to just 13.6%.

The dollar absorbed most of those payments with the British pound, Japanese yen and, yes, the Chinese renminbi taking up the rest.

So, the great distraction about de-dollarization is, in part, about paying no attention to the rapid demise of the euro and the emerging sovereign bond crisis that ECB President Christine Lagarde works everyday to paper over.

I’ve talked about this so much people are getting sick of it. (Here, Here, Here, and Here)

Eventually, however, no matter how hard they try to game the math, paint the tape and make deals to keep up appearances, markets are simply smarter than central planners.

So, with this in mind I fully expect over the next couple of months for the bond vigilantes to return with a vengeance now that Jerome Powell has everyone’s attention. He can further up his street cred with another 25 basis point raise in September, but honestly, he may not have to.

BRICS in the Wall

But, back to the BRICS. If de-dollarization wasn’t the point of the Summit this year, then what was?

Expansion.

And not just expansion for the sake of expansion, but geographically strategic expansion.

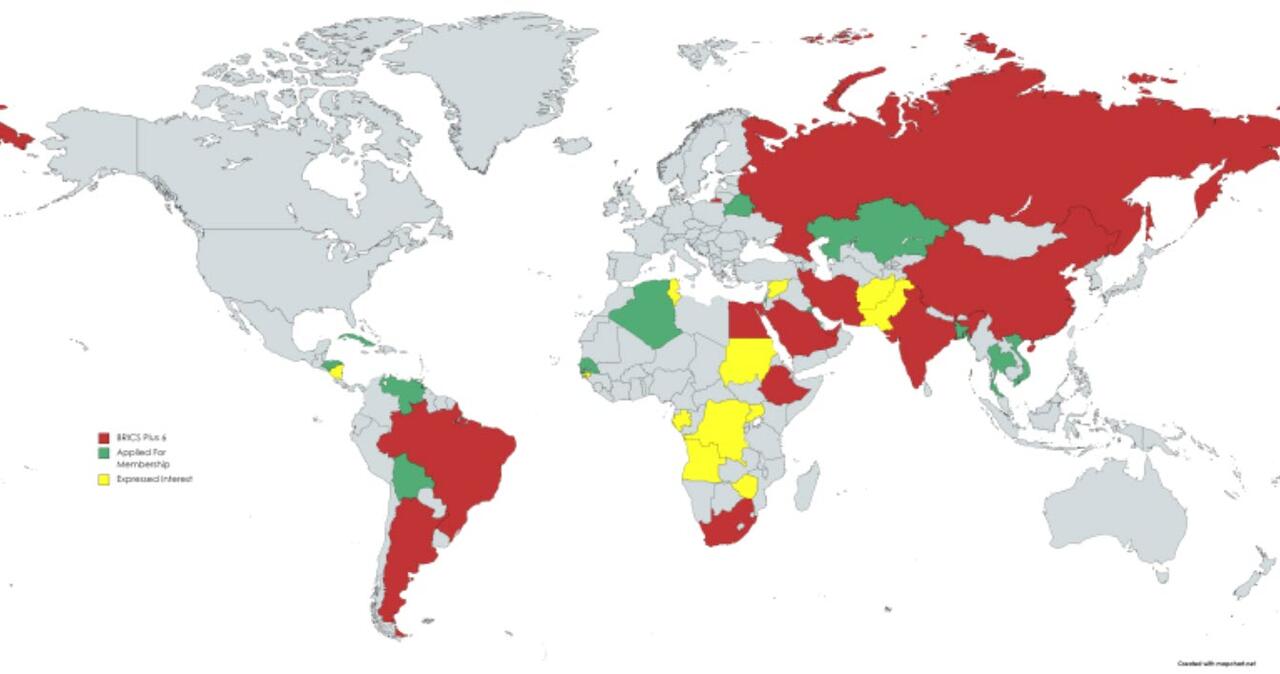

The BRICS formally added six countries — Iran, Saudi Arabia, United Arab Emirates, Argentina, Egypt and Ethiopia. They could have added others and almost added Algeria if not for a last-minute veto by India on behalf of France.

Algeria is symbolic of the fight between Italy and France for access to African oil and gas. There can be no Ital-exit from the EU without Italy minimizing France’s influence in North Africa, shoring up its energy needs as collateral for a return to the lira.

Thankfully, with the help of Russia and China, the Africans are taking care of the Italians’ French Problem all on their own.

If there is one common theme beyond the geography (more on that in a bit) with all six of these countries it is their relationship with the supposedly former British empire. From the Arab states and Egypt to those that defied the Brits in the past — e.g. Iran and Argentina — these additions represent a power shift that is profound.

One look at the world map should make this point crystal clear.

Countries in Red are members of the alliance. Those in green have formally applied for membership and yellow are those that have openly expressed interest.

But it is the 5 countries clustered around the center of global trade that should grab your attention.

Because all talk of a BRICS common currency are nothing more than theatre if there isn’t a fully developed alternative financial supply chain to capture the profits and minimize currency risks and friction for all the members.

Taking them one by one let’s discuss.

Iran

So, let’s start with the easy one. Iran, in my book, has been the “I” in BRICS for years. Because with India constantly keeping everyone off-balance, much like Erdogan in Turkey, that incentivized Russia and China to invest heavily in Iran, as a counterpoint, making it the key to both China’s Belt and Road Initiative (BRI) and Russia’s long-desired International North-South Transport Corridor (INSTC).

India dragged their feet for so long on their contracted work on the Iranian port at Chabahar, that Iran nullified the contract, handed it to China, who then finished the work in less time than it took for Iran to get India on the phone to complain about it.

This is the kind of pivot that gets results. China and Russia have pledged hundreds of billions in investment and sales to Iran, supporting them after Former President Trump tore up the JCPOA and put on sanctions which didn’t work, unless Trump’s goal was to ensure what has transpired since.

This is further proof Trump doesn’t play 4-d chess.

Both the ports at Chabahar and Bandar Abbas now serve to get Asian trade, especially coming from Russia, exits beyond the choke points around the Mediterranean, Red, and Black Seas.

So, Iran was always going to be the first country added to the bloc. It quickly put India on notice to stop playing games.

Saudi Arabia

Adding Saudi Arabia and the UAE weren’t on anyone’s radar back during the Trump Interregnum, because Trump understood how important the Saudis were to the US maintaining its presence in the region.

The problem for Trump was that the Saudis knew he wasn’t a long-term solution in the US. All during his presidency events occurred that trace a line straight back to Obama’s foreign policy. Undermining Trump was the sole focus of Obama’s shadow government, especially our relationship with the Saudis.

With the successful intervention by Russia in Syria, and their own disastrous results in the War in Yemen, it was only a matter of time before Crown Prince Mohammed bin Salman (MbS) came to his senses.

Saudi Arabia’s future was with the BRICS not the remnants of the British empire. As an aside here, I talk about Neocons all the time and the best way to think of them, beyond their hatred of pretty much the rest of the world, is to see them as the inheritors of the British empire’s foreign policy.

The US adopted this foreign policy a century ago under Woodrow Wilson (see my podcast with Richard Poe). Since then it’s been the one thing, aside from ruinous spending, that unites the Uniparty on Capitol Hill. Empire or bust. Looking at the ruin of our finances and domestic politics, “Bust” was the obvious outcome.

Saudi Arabia had no other option than to go along with its OPEC+ partner, Russia, if MbS wants the country to survive the end of its oil reserves.

UAE

The UAE addition is definitely part of the currency discussion. Dubai and Abu Dhabi have rapidly become centers for strategic commodities trading with very successful and deepening gold and oil trading. Dubai has its own crude oil benchmark. Even Moscow doesn’t have one of those (yet).

As Vince Lanci and I talked about at length in a recent appearance on Palisades Gold Raio (parts I and II here), in order to even talk about some form of gold-backed trade settlement system, there has to be a deep and liquid supply chain and financial industry in place to facilitate both that settlement and minimize the storage risks to gold and currency risks of the alliance members trading bilaterally without the dollar as the intermediate.

So, adding Dubai as one node in that network outside of China’s control was important to building trust there. Having multiple exchanges, vaults, and refineries simplifies everything. And, with that, minimizes the ‘convenience premium’ of using the US dollar and maximizing members’ use of local currencies with gold acting as the universal trust layer and a blockchain for back office and auditing functions.

So, first, you add the financial center, then you start really talking the whole “Gold-Backed BRICS Currency.” Order of operations matters folks.

The UAE was necessary to get India to even consider going along with Russia and China on this idea, which is why the UAE dirham will be the settlement currency between India and Russia on oil sales, and not the ruble. It both creates validity for a third party while also keeps India free from directly contravening US sanctions on buying Russian energy.

Argentina

It shouldn’t be underestimated how much the IMF and European corruption have wreaked havoc in Argentina over the years. This is another resource-rich country that has been kept under constant upheaval which now has the opportunity, like Egypt, to get out from underneath the IMF’s thumb, depriving vulture capitalists all across the west the opportunity to plunder the country one more time.

Adding Argentina should see the development money necessary to build out its significant shale reserves at Vaca Muerta make its way into the country. This stabilizes its foreign exchange reserves and access to the BRICS New Development Bank (NDB) gives it an alternative to the IMF loan sharks.

The upcoming elections could quickly become a referendum on IMF requirements and capital controls.

Egypt and Ethiopia

Egypt is a fascinating turn of events, because Egypt’s financial weakness was the very thing to create a strategic opportunity for Russia and China to make President Al-Sisi a great offer. Use our New Development Bank and stiff the International Monetary Fund if they won’t negotiate a debt write-down.

Like what’s in front of Argentina, Egypt now has leverage in negotiations they didn’t have before.

Either way the IMF loses here, because Egypt has an alternative lender it can force a write-down by the IMF for the first time ever or they can just default. China is already willing to forgive $8 billion in Egypt’s debt while the IMF is holding fast only to restructuring.

And if you think Egypt doesn’t have this leverage here let’s not forget that the Suez Canal still handles 12% of global trade daily. The BRICS bloc now have a political ally that controls the Suez.

With Ethiopia, along with Russia’s deft diplomacy with both Eretria and China’s with Djibouti where they have port access, the BRICS now has effectively unfettered access to the Red Sea. The pressure will mount for Eretria and Djibouti to make peace with Ethiopia, thus opening up trade in eastern Africa.

Access to or circumventing the historic chokepoints to global trade has been a long-held goal of both Russia and China. And it looks like with these additions to the BRICS bloc, they have finally achieved that.

Meet the New Boss?

In my last article on geopolitics, I brought up the importance of physical collateral for the future of the West’s financial dominance, especially that of Europe. The main reason why I keep harping on why Europe is in such trouble is because it’s obvious now that those with physical collateral, including the US, are no longer interested in selling that collateral to a colonial-minded Europe at cut-rate prices.

Russia, under Putin, was happy to court the EU as energy partners because he thought it would secure Russia’s future from potential war with Europe. He was willing to sell Europe cheap gas to maximize the total profit to Russia, not directly measurable in things like GDP or trade balances.

Some capital is political. Some profits are social, despite crappy Marxist commentary to the contrary.

This is why he went along with Former German Chancellor Angela Merkel’s plea to build Nordstream 2, knowing it would incense the US/UK Neocons.

The peace dividend to Russia was just too big not to make a run at. Merkel’s betrayal of Putin over NS2 and the Minsk agreements are why we are in the mess we’re in today.

The Neocons struck geopolitical gold with blowing up Nordstream, depriving Germany and France of much needed gas. Things are so bad in Germany that they are now quietly dismantling their wind farms to rebuild coal-fired plants, going back to the one energy source they have in abundance in Europe.

Now Africa is in revolt against France. Last month it was Niger. This month it is Gabon. There is no way France can respond to all of these revolts on their own. They need outside intervention and it doesn’t look like it’s coming.

Queen Warmonger Vicky Nudelman went to Niger and was rebuffed. Reports are now circulating that she and her staff were caught completely by surprise with events in Africa and had no solutions, offers or even credible threats to bring to bear.

Pretoria was well aware of Nuland’s hawkish reputation, but when she arrived in Pretoria, the official described her as “totally caught off guard” by winds of change engulfing the region. The July putsch that saw a popular military junta come to power in Niger followed military coups in Mali and Burkina Faso that were similarly inspired by mass anti-colonial sentiment.

Though Washington has so far refused to characterize developments in the Nigerien capital of Niamey as a coup, the South African source confirmed that Nuland sought South Africa’s assistance in responding to regional conflicts, including in Niger, where she emphasized that Washington not only held significant financial investments, but also maintained 1,000 of its own troops. For Nuland, the realization that she was negotiating from a position of weakness was likely a rude awakening.

If you map Nuland to the UK/US Neocons who are not necessarily aligned with Davos then this report should shock you, because it tells us that neither are capable of moving into the power vacuum left by these juntas seizing power.

It says, with little equivocation, that all of the colonial powers of Europe are paper tigers. What started in Burkina Faso and Mali is spreading like wildfires set by Climate Change arsonists in Canada across Africa.

French President Emmanuel Macron can only scream impotently in Paris, Nuland can shake her fist screaming, “You’ll rue the day…,” and the US Dept. of Defense stands by and says exactly nothing.

At the same time clashes between Syrian Arab Army troops and US occupying forces east of the Euphrates River are back under the headlines.

Do you get the picture yet?

The fight for physical collateral is dovetailing perfectly with capturing control of the major trade routes. While the UK and their Neocon quislings are hell bent on starting WWIII over Ukraine, c.f. drone strikes on Russia’s Pskov airport from Latvia, the BRICS bloc understands that their best course of action is to continue building new relationships, networks, and pressuring the centuries-old colonial networks that have financed their power.

Staying out of a direct hot war simply makes good strategic sense. Attrition is a bitch, energetically.

Now they are being forced to expend their seed capital built up over these centuries on influencing events to their liking, and it’s clear they really don’t have the resources to do so for very long.

Against that backdrop, de-dollarization is the least of their worries.

It will be the thing that grinds away in the background, like Powell’s shrinking the Fed’s balance sheet, and will just emerge out of these events.

The choice the West is now facing is at what point do they stop fighting this and finally come to the negotiating table. Some factions, like the US military and the banking sector, have already made their intentions clear.

The others? Not so much.

When facing extinction, that’s when you find out where someone’s true loyalties are.

* * *

Join my Patreon if you value loyalty

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex