Uncategorized

It’s Deja Vu All Over Again: Futures Tumble As Yields Surge

It’s Deja Vu All Over Again: Futures Tumble As Yields Surge

In a deja vu repeat of Monday’s open, and really a carbon copy of most mornings…

Share this:

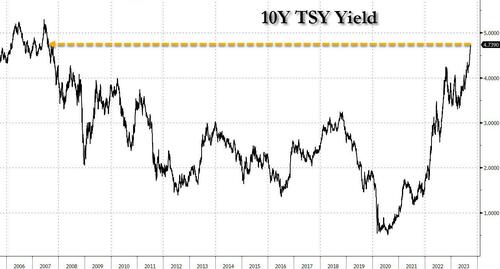

In a deja vu repeat of Monday's open, and really a carbon copy of most mornings in the past month, what was a modest attempt to push futures higher has crashed and burned with US equity futures sliding to session lows as yields resumed their surge once again, the 10Y rising up to a new 16 year high of 4.74%, with 30Ys also rising to the highest since 2007, hitting 4.856%.

As a result what was a modest 0.3% gain in spoos turned into a 0.4% loss as S&P futures dropped to session lows of 4,307 as of 7:35am with Nasdaq futures dragged 0.5% lower. The Bloomberg Dollar Spot Index followed yields tick for tick and rose to an 10-month high, pressuring most Group-of-10 currencies. The selloff rippled across equity and commodity markets, with Europe’s Stoxx 600 sliding to a six-month low as WTI traded near $89 a barrel and gold and Bitcoin fell.

In US premarket trading, HP gained after BofA double upgraded its rating on the PC maker to buy from underperform, with positive commentary expected at next week’s analyst day. MSP Recovery rose as much as 26% in premarket trading on Tuesday as its Chief Legal Officer Frank Carlos Quesada reported a purchase of stock to the US Securities and Exchange Commission. Here are some other notable premarket movers:

- ALX Oncology surges as much as 149% in premarket trading Tuesday, erasing an earlier drop, after reporting interim mid-stage data from a trial of its drug evorpacept for the treatment of advanced gastric cancer.

- McCormick slides 3% in premarket trading, after the spice maker reported net sales that trailed the average analyst estimate and a larger-than-expected decline in product volume. Sales in the consumer segment in the Asia-Pacific region were particularly weak, which the company attributed to a slower-than-expected economic recovery in China.

- Oddity Tech Ltd. rallied 18% in premarket trading after Truist Securities analyst Youssef Squali raised the recommendation to buy from hold based on the firm’s preliminary third quarter results and its “compelling” valuation.

- Point Biopharma surges 85% in premarket trading Tuesday after Eli Lilly & Co. agreed to buy the biotech firm for $12.50 per share in cash in a bid to expand its oncology capabilities into radioligand therapies.

Wall Street strategists are warning about the impact that elevated interest rates on equities, with Goldman Sachs, Morgan Stanley and JPMorgan all saying there’s a risk of further stock-market declines. Currently, traders are pricing roughly a one-in-three chance of a rate hike in November.

“We had not anticipated such an increase in rates,” said Vincent Juvyns, global market strategist at JPMorgan Asset Management. “This is something which will at least slow down, or even reverse the progress of equity markets.”

And indeed all eyes are on rates this morning, as Treasury yields extend to fresh cycle highs in 5-year out to long-end of the curve, as the selloff gathers pace in early US session. Futures volumes pick up as 10-year tenor breaks through earlier session lows and through the 107-00 level. In the long-end of the curve 30-year yields breach 4.855% and onto highest levels since 2007.

- In Treasury options demand seen for bearish plays targeting higher yields, matching the early price action.

- US yields cheaper by up to 6.5bp on the day across long-end of the curve; breaking through 4.856% in 30-year tenor and onto highest yield to highest since 2007

- Selloff extended as 10-year futures breached 107-00 level to the downside reaching as low as 106-30+; into the move around 22,000 Dec23 contracts traded over a one-minute period, highest volumes of the session

- In Treasury options early demand seen for downside protection as yields continue to climb higher; flows have included TY Nov23 107.00/106.00 put spread bought in 3,500 at 24 ticks says London trader

- Some information comes from rates traders familiar with the transactions, who asked not to be identified because they are not authorized to speak publicly

This week’s Treasury selloff came after US lawmakers managed to avert a government shutdown, prompting traders to increase bets that the Fed could raise rates in November. Comments from two Fed policymakers reinforced that view, with Cleveland Fed president Loretta Mester saying on Monday that one more rate hike was likely needed and Governor Michelle Bowman urging multiple increases.

“The market is probably evenly split on whether central banks will need to continue raising rates or not so the bond marker is testing investors,” said Brian O’Reilly, head of market strategy at Mediolanum International Funds. “With 10-year yields around 4.6%, the asset allocation decision for equities is getting quite difficult.”

European stocks were also lower, spooked by the surge in rates. The Stoxx 600 is down 0.7% at session lows, led by declines in the utility sector; retail stocks were dragged down on a warning from online retailer Boohoo Group Plc, which fell 10%. Here are the biggest European movers:

- AstraZeneca shares rise as much as 1.1% after the drugmaker agreed to pay $425 million to settle US product liability lawsuits related to heartburn and stomach acid treatments Nexium and Prilosec

- Novo Nordisk shares rise as much as 2.8% after the drugmaker won denial of a challenge to two US patents backing semaglutide

- Sika shares gain as much as 1.1% after Swiss chemicals company raised its annual sales growth and Ebitda margin targets for medium term

- Burberry falls as much as 4.7% in London to hit the lowest level since Nov. 2022, after the luxury stock was cut to sell from neutral at UBS

- Greggs shares slip as much as 3.2% after Tuesday’s third-quarter trading statement, with analysts taking an overall positive view but noting the lack of any guidance upgrade

- Eramet lost as much as 4.5% in early Paris trading on Tuesday after AlphaValue/Baader cut its rating for the French mining group, arguing there is further downward potential for the stock

- Boohoo shares tumble as much as 11%, to the lowest since August 2015, after the online fast fashion retailer cut its revenue forecast for the year

- Aker Carbon Capture drops as much as 7%, to lowest in almost five months, after Citi cuts to neutral due to perceived risks

Earlier in the session, Asian stocks declined as hawkish signals from the Federal Reserve spurred risk-off sentiment, while losses in Hong Kong intensified as traders returned from a holiday. The MSCI Asia Pacific Index fell as much as 1.6% to reach its lowest since late December. The Hang Seng China Enterprises Index fell more than 3% in the region’s worst performance among major gauges, dragged lower by tech stocks Meituan and Alibaba. Mainland China remains shut for Golden Week holiday, while South Korean markets are also closed. The broad selloff came as the latest commentary from Fed officials stirred concerns that the central bank will continue to raise interest rates. Traders boosted bets on a November rate hike to a roughly one-in-three chance, up from the 25% likelihood priced on Friday. Positive Chinese travel data did little to lift sentiment as investors focus on uncertainties lingering in the world’s second-largest economy.

- Hang Seng was the worst hit on return from holiday amid losses in property, tech and energy with developers suffering despite an early spike in Evergrande shares by around 35% on resumption of trade.

- Nikkei 225 weakened with all industries pressured and energy firms leading the broad declines.

- ASX 200 was dragged lower by underperformance in the mining-related sectors due to the recent declines in commodity prices and with headwinds from the rising yields after Australia’s 10yr yield rose to its highest since 2011, while the RBA decision to keep rates steady provided no major fireworks.

- In India, key stock gauges in India slid, tracking weakness in regional peers, with lenders and energy sector companies leading the selloff. The S&P BSE Sensex fell 0.5% to 65,512.10 in Mumbai, while the NSE Nifty 50 Index declined 0.6% to 19,528.75. The MSCI Asia Pacific Index was down 1.5%. Banks, energy and automakers were among the worst sectoral performers during the session. HDFC Bank contributed the most to the Sensex’s decline, decreasing 1.2%. Out of 30 shares in the Sensex index, 11 climbed, while 19 fell.

In FX, the Bloomberg Dollar Spot Index rises 0.1%, hitting a fresh 10-month high and the euro falling to its lowest against the dollar since last December at 1.049.

- The Australian dollar extended declines after the Reserve Bank of Australia held its cash rate; AUD/USD dropped as much as 0.9% to 0.6306, weakest since November

- The euro and the pound were also little changed after erasing earlier losses against the greenback

- The yen swung between gains and losses, staying near cycle lows amid intervention speculation

- USD/JPY is hovering just below 150.

In rates, Treasuries are trading at the lows of the day, with 10-year yields rising 6bps to 4.74%, while gilts outperform their German counterparts after data showed UK shop price-inflation fell to a one-year low in September. UK two-year yields fall 3bps to 4.95%. Treasury yields once again rose to session highs across the curve with futures under or near Monday’s lows; 10- to 30-year yields reached fresh multiyear highs. Gilts outperform Treasuries on the back of supportive food inflation data. US 10-year yields around 4.75%, cheaper by ~5bps on the day near session high; gilts outperform by nearly 5bp in the sector as they unwind a portion of Monday’s losses. US 2s10s curve steeper by 4bp on the day with front-end slightly outperforming; spread breached -41bp, least inverted since May 5. Fed-dated OIS continues to price around 35% odds of a 25bp rate hike for the November policy meeting; Cleveland Fed President Loretta Mester said late Monday that one more rate hike may be needed this year. Dollar IG issuance slate empty so far after five names priced $5b Monday; a slow week is expected with many companies entering earnings blackout periods. US session highlights include August JOLTS job openings data and comments from Fed’s Bostic.

In commodities, crude futures are little changed with WTI trading near $88.90. Spot gold falls 0.1%.

Bitcoin is under pressure after experiencing a marked upside in recent sessions, which took BTC to near USD 29k. Currently, residing around the USD 27.5k mark but well within recent ranges.

Looking to the day ahead now, and the main data highlight will be the US JOLTS release of job openings for August. Otherwise, central bank speakers include the ECB’s Simkus, Lane and Villeroy, along with the Fed’s Bostic.

Market Snapshot

- S&P 500 futures up 0.2% to 4,332.75

- MXAP down 1.4% to 154.63

- MXAPJ down 1.3% to 485.09

- Nikkei down 1.6% to 31,237.94

- Topix down 1.7% to 2,275.47

- Hang Seng Index down 2.7% to 17,331.22

- Shanghai Composite up 0.1% to 3,110.48

- Sensex down 0.4% to 65,585.91

- Australia S&P/ASX 200 down 1.3% to 6,943.42

- Kospi little changed at 2,465.07

- STOXX Europe 600 up 0.1% to 446.12

- German 10Y yield little changed at 2.90%

- Euro little changed at $1.0485

- Brent Futures down 0.3% to $90.45/bbl

- Gold spot up 0.0% to $1,828.42

- U.S. Dollar Index little changed at 106.99

Top Overnight News

- Several Taiwanese companies are helping Huawei build infrastructure for a secret network of chip plants across southern China, a Bloomberg investigation found. At a time when China regularly threatens Taiwan with military action, the island's tech firms risk spurring a backlash by potentially helping US-sanctioned Huawei effectively break an American blockade. BBG

- India has told Canada to withdraw dozens of diplomats from the country, in an escalation of the crisis that erupted when Prime Minister Justin Trudeau said New Delhi may have been linked to the murder of a Canadian Sikh. FT

- ECB’s Chief Economist Philip Lane warned that there is still work needed to be done to fully tackle the EU’s inflation problem. BBG

- Switzerland’s core CPI for Sept dips to +1.3%, down from +1.5% in Aug and below the Street’s +1.5% forecast (headline inflation ticked up to +2% from +1.9% in Aug. BBG

- British shoppers enjoyed the first monthly drop in food prices in more than two years as retailers cut the cost of dairy products, fish and vegetables amid “fierce competition” between stores, a survey found. BBG

- Federal Reserve Bank of Cleveland President Loretta Mester said the US central bank will likely need to raise rates once more this year and then hold them at higher levels for some time to get inflation back to its 2% target. BBG

- Rep. Matt Gaetz (R-Fla.) on Monday night filed a formal motion to eject the speaker Kevin McCarthy, a maneuver last attempted in 1910 and never successfully completed. The House must act by Wednesday on the matter — and while McCarthy may yet survive depending on how Democrats vote, even a failed challenge to his speakership weakens him going forward. Politico

- The slide in Treasuries has been excessive given recent economic data and Federal Reserve policy, suggesting it’s instead being driven by fears over the swelling US deficit. BBG

- America’s shale pioneers have vowed to keep a lid on drilling even if oil hits $100 a barrel, citing a need to maintain capital discipline and what they claim is a “war” on fossil fuels waged by the Joe Biden administration. FT

- In the new ‘higher for longer’ rates environment, the key risk for S&P 500 ROE will be higher interest expenses and lower leverage. Our rates strategists recently raised their forecast for the nominal 10Y UST and now expect rates to end 2023 at 4.3% and then rise to 4.6% in 1H 2024 before receding back to 4.3% at the end of 2024. Although the long-maturity, fixed-rate debt structures of S&P 500 companies generally insulate them from higher rates, borrow costs for S&P 500 companies have ticked up on a year/year basis by the largest amount in nearly two decades. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks declined amid the rising global yield environment and the continued absence of some key markets, while the focus turned to central bank announcements beginning with the RBA. ASX 200 was dragged lower by underperformance in the mining-related sectors due to the recent declines in commodity prices and with headwinds from the rising yields after Australia’s 10yr yield rose to its highest since 2011, while the RBA decision to keep rates steady provided no major fireworks. Nikkei 225 weakened with all industries pressured and energy firms leading the broad declines. Hang Seng was the worst hit on return from holiday amid losses in property, tech and energy with developers suffering despite an early spike in Evergrande shares by around 35% on resumption of trade.

Top Asian News

- RBA kept the Cash Rate Target unchanged at 4.10%, as expected, while it reiterated that some further tightening of monetary policy may be required and that the Board remains resolute in its determination to return inflation to the target. Furthermore, it stated that returning inflation to the target within a reasonable timeframe remains the Board’s priority and recent data are consistent with inflation returning to the 2–3% target range over the forecast period but also noted significant uncertainties around the outlook..

- "(China) has seen a recovery in consumer spending in terms of trips and transportation, with market confidence and vitality both on the continuous rise" following the first four days of the Chinese holiday, according to Global Times.

European bourses have been mixed but are currently a touch softer, Euro Stoxx 50 -0.2%; newsflow is relatively light and markets remain focused on yields. Sectors are similarly mixed, featuring outperformance in Banks and Insurance names while Utilities and Basic Resources are the relative laggards. Stateside, futures are modestly firmer, ES +0.2%, with recent pressure being attributed to yields but action comparably more contained thus far in today's session ahead of JOLTS and Fed's Bostic & Mester. For reference, APAC trade remains limited given mass holiday closures though the return of the Hang Seng saw it experience marked pressure and close with downside of circa. 3.0%, with the move similarly attributed to recent yield action.

Top European News

- EU is to assess risks of four critical technologies being used by third countries such as semiconductors, AI, quantum technologies and biotechnologies, while the EU aims to take measures next year to mitigate risks to these technologies, according to an EU official cited by Reuters.

- Brussels will unfreeze about EUR 13bln in EU funding to Hungary as it seeks help for Ukraine, according to FT.

- ECB's Lane says they have reached the interest rate level that will help tame inflation; the key is to maintain this rate level for as long as needed; seeing wage data coming in lower is very important. Would not focus on December as a critical decision; December is not the end of the inflation challenge. Says he welcomes September inflation data, but we need to see further progress.

- ECB's Valimaki (sitting in for ECB's Rehn) says further rate hikes cannot be ruled out, appears as if a wage-price spiral can be avoided.

- ECB's Simkus says rates need to stay restrictive to tame prices; prompt response of monetary policy was effective; inflation still faces many lines of resistance; inflation shock is not over.

FX

- Dollar resumes bull run before running into chart and round number resistance, DXY probes Fib at 107.170 and fades within 107.210-106.930 range.

- Yen continues to defend 150.00 vs. Buck, but barely and with 1.1bln option expiries helping, Euro eyes expiry interest at 1.0495 against Greenback after a bounce from 1.0461 and Sterling pivots Fib retracement between 1.2062-96 parameters.

- Aussie lags post-on hold RBA and Kiwi down in sympathy awaiting RBNZ to follow suit, AUSD/USD and NZD/USD cling to 0.6300 and 0.5900 handles respectively.

- Franc deflated after softer than forecast Swiss CPI, USD/CHF hovers above 0.9200.

- Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals and they will take appropriate steps on FX moves with a sense of urgency, while he added that they will stand ready to respond while closely watching FX moves. Furthermore, he said currency interventions are not targeting FX levels and whether to carry out FX intervention is determined by volatility, according to Reuters.

Fixed Income

- EGB underperformance gradually spills over as Bunds retreat from 127.95 to 127.45 and BTPs reverse through 109.00 within a 109.49-108.86 range.

- Gilts and T-note suffer contagion between 93.18-92.68 and 107-14/06 respective parameters ahead of Fed's Bostic and JOLTS US job openings.

- Orders for the new 5-year BTP Valore have reached EUR 5bln since the beginning of the offer, via Reuters citing Bourse data.

Commodities

- Crude benchmarks are little changed overall having lifted incrementally off initial lows as the USD moves below the 107.00 mark while crude specifics have been light as attention turns to this week's JMMC.

- Currently, WTI and Brent are trading in USD 87.76-88.71/bbl and USD 89.50-90.46/bbl respective ranges.

- Spot gold is essentially flat intraday with the yellow metal holding around USD 1825/oz while spot silver is a touch firmer after Monday's pronounced pressure, finally base metals have seen similar directional action to crude with the metals off lows as the USD eases a touch.

- Spain's Energy Minister showed support for the Dutch call to phase out fossil fuel subsidies.

- India's petroleum minister says an oil price above USD 100/bbl is not going to be in anyone's interest.

- Poland and Ukraine announced a breakthrough on Ukrainian grain transit, according to AFP.

Geopolitics

- Israel carried out an air attack on Syrian armed forces positions in the vicinity of Deir al Zor, according to Syrian state media.

- India told Canada to withdraw dozens of diplomatic staff whereby it must repatriate around 40 diplomats by October 10th, according to FT.

US Event Calendar

- Sept. Wards Total Vehicle Sales, est. 15.4m, prior 15m

- 10:00: Aug. JOLTs Job Openings, est. 8.82m, prior 8.83m

Central bank speakers

- 08:00: Fed’s Bostic Speaks on Economic Outlook, Inflation

DB's Jim Reid concludes the overnight wrap

It might have been a brand new quarter, but yesterday was another challenging day for markets, especially with the bond sell-off showing no sign of letting up. In fact, the 10yr Treasury yield (+10.8bps) closed at a post-2007 high of 4.68%, whilst the 10yr real yield (+9.7bps) closed at a post-GFC high of 2.33%. And despite some better-than-expected data, risk assets came under pressure alongside WTI crude (-2.17%) falling back beneath $90/bbl. Equities were weak in Europe and down for much of the day in the US but a late rally left the S&P 500 (+0.01%) flat by the close. Europe’s STOXX 600 (-1.03%) fell to a 6-month low, and the German 10yr real yield (+12.1bps) hit a post-2011 high of 0.58%. The main event today is the US JOLTS data as we see how tight the labour market still is under the surface.

Starting with markets and there were several factors driving the latest sell-off. First up, the lack of a US government shutdown over the weekend was seen in a more bearish light as the day progressed, as it removed a tangible risk for the economy and was seen as raising the likelihood of more rate hikes. For instance, futures raised the likelihood of a hike at the next meeting in November from 19% on Friday to 28% yesterday. And looking at the prospect of a hike by December, the likelihood rose from 39% last Friday to 51% by yesterday’s close.

Second, the sell-off then got added fuel from the latest ISM manufacturing print for September, which was notably better than expected. The headline print came in at 49.0 (vs. 47.6 expected), which was the highest since November 2022. And there was lots of good news at the component level as well, with new orders (49.2) at a 13-month high and employment (51.2) back in expansionary territory. That was echoed by the final manufacturing PMI as well, where the final reading was revised up to 49.8 (vs. flash 48.9). So there were several signs that the economy was proving more resilient than expected.

Third, comments from numerous Fed speakers reiterated the higher-for-longer narrative. Governor Bowman, one of the more hawkish FOMC members, suggested that multiple further rate hikes may be needed while Cleveland Fed President Mester saw another hike this year as likely. Comments from Vice Chair of Supervision Barr erred on the more cautious side, saying that the more important question was “how long we will need to hold rates at a sufficiently restrictive level”. Overall, despite the more encouraging recent inflation data, the latest Fed commentary shows no signs of a downshift from the September median dot plot view of another rate hike by year-end.

Speaking of US economic resilience, our own US economists have just released an updated set of forecasts overnight. Their baseline still sees a recession taking place, but they now see that starting a bit later in Q1 2024, and only lasting two quarters. Their view is that the soft landing case has strengthened over recent months, but there are still plenty of headwinds, including depleted savings, tightening credit conditions, and a return of student debt payments. For the Fed, they continue to see the tightening cycle as over now, albeit with the risk of another hike. And they now expect the Fed to start cutting rates from June 2024, with 175bps of cuts next year. See their full update here.

With some more positivity about the economy, bonds continued to sell off throughout the day, with yields on 10yr Treasuries up +10.8bps to a post-2007 high of 4.68%. The 30yr yield (+8.9bps) also pushed higher to close at 4.79%. It was real yields that drove the increase in rates, with the 2yr real yield (+7.3bps) at a new post-GFC high of 3.07%, and the 10yr real yield (+9.7bps) at 2.33%. At the same time, the 2s10s curve continued to steepen, with a +4.9bps increase to -42.8bps. On one level, that might be seen as a positive sign given the 2s10s is a classic recessionary indicator, but then again, the last 4 cycles saw it move out of inversion territory just before the recession began.

Over in Europe, there was a similarly strong bond sell-off, with yields on 10yr bunds (+8.2bps), OATs (+7.8bps) and BTPs (+2.6bps) all moving higher. But it was gilts that led the moves, with the 10yr yield up +12.7bps to 4.56%, whilst the 30yr gilt yield (+11.4bps) surpassed its mini-budget peak yesterday to close above 5% for the first time since 2002. Similarly to the US, it was real yields that led those moves, and the German 10yr real yield (+12.1bps) hit a post-2011 high of 0.58%.

The bond sell-off created a tough backdrop for equities. The S&P 500 traded around half a percent lower for most of the day, but a rally in the last hour of the US session left it flat on the day (+0.01%). Tech stocks were a big winner though, with the FANG+ Index (+1.38%) going against the broader trend to advance for a 4th consecutive session. The breadth of losses outside of tech was highlighted by the equal weight index declining -1.11% with only 22% of the S&P 500 constituents up on the day despite its flat headline performance. Small caps also underperformed with the Russell 2000 index down -1.58%. Back in Europe there were larger losses, leaving the STOXX 600 (-1.03%), the DAX (-0.91%), the CAC 40 (-0.94%) and FTSE 100 (-1.28%) lower on the day.

Across other asset classes, the dollar was a key beneficiary, with the broad index (+0.69%) rising to a 10-month high and the euro falling to its lowest against the dollar since last December at 1.049. Meanwhile, oil declined for third day in a row, with WTI crude falling back below $90/bl (-2.17% to $88.82/bl). Both WTI (-5%) and Brent (-6%) have seen their sharpest 3-day decline since the oil price rally started in June. So some evidence that uncertainty over the demand outlook is weighing on the strong recent oil rally.

Overnight in Asia, regional equities are also selling off with the Nikkei 225 down -1.43%. The Hang Seng is down -2.98% after reopening post Monday's holiday. Many other markets remain closed in this holiday week. There was also an RBA decision overnight, with the central bank keeping rates at 4.10% with much of the statement identical to the last one. S&P 500 futures are almost unchanged (-0.06%), with Treasury yields up less than a basis point across the curve.

Elsewhere yesterday, the main data highlight came from the final manufacturing PMIs, although they mostly echoed the initial impressions from the flash reading. Indeed, the Euro Area PMI was exactly in line with the flash print at 43.4, and Germany’s was revised down slightly to 39.6 (vs. flash 39.8). Otherwise, the Euro Area unemployment rate was back at its recent low of 6.4% in August, which is its joint-lowest level since the formation of the single currency.

To the day ahead now, and the main data highlight will be the US JOLTS release of job openings for August. Otherwise, central bank speakers include the ECB’s Simkus, Lane and Villeroy, along with the Fed’s Bostic.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire