If Bitcoin Didn’t Exist, We’d Have To Invent It Right Now

If Bitcoin Didn’t Exist, We’d Have To Invent It Right Now

Authored by Mark Jeftovic via BombThrower.com,

The conventional take on Bitcoin and crypto-currencies in general from the mainstream skeptics is that it’s some sort of speculative…

Share this:

Authored by Mark Jeftovic via BombThrower.com,

The conventional take on Bitcoin and crypto-currencies in general from the mainstream skeptics is that it’s some sort of speculative bubble. The recent mania in NFTs seemingly adds credence to this argument. However, the NFT craze, as unfathomable as it is, even to somebody like myself, has precedents that show it doesn’t invalidate the crypto thesis.

Coming up in the domain and DNS business, I’ve seen this movie before. I’ve also made the point back in the 2017 crypto cycle that the Tulipmania analogy for Bitcoin was a bad one for many reasons, and that it was a more accurate comparison to the domain name aftermarket of the 2000’s era. When companies and speculators were paying millions of dollars for strings of words from the dictionary with “.com” appended to them, that was a speculative mania and it was akin to Tulipmania. And from our vantage point in the present we can draw the comparison to NFTs.

But when the .com aftermarket fizzled, the entire internet kept right on plugging along using DNS as the carrier tone, and domain names for endpoints. That didn’t change and to this day, without DNS you’ve basically got nothing. It’s part of the internet plumbing (yes, there are multiple projects seeking to supplant DNS via blockchain, separate convo for another day).

The overall point is, a seemingly speculative mania can erupt out of a relatively new protocol, be it the long defunct hedge fund that rang the bell at the top by purchasing “fund.com” for $10M USD, or an NFT selling today for $69M USD, and that doesn’t make the underlying protocol from which it sprang forth a speculative bubble (we discussed this along with attention markets and BAT on the latest AxisOfEasy Salon #40).

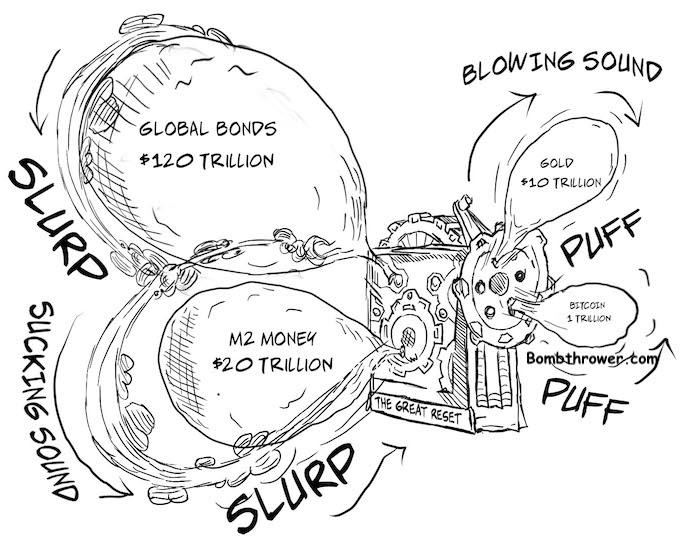

But if everything from NFTs to stonks to real estate and gold and cryptos are all hitting fresh all-time-highs, it seems to be that the obvious pattern here isn’t necessarily that “Everything is in a Bubble” as much as that the numéraire is collapsing.

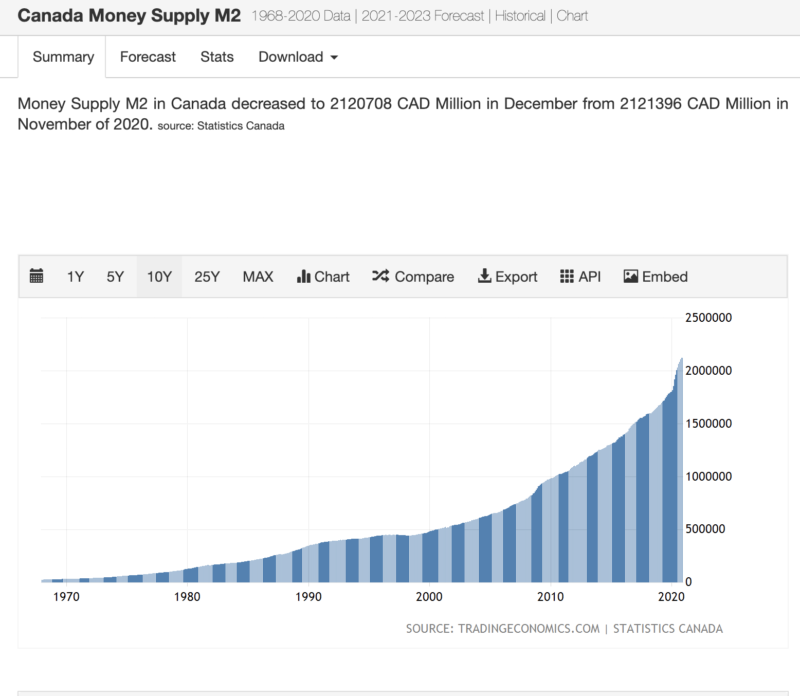

Most people reading these kinds of articles know that bonds are a dead man walking and M2 money supply is going up everywhere. I was going to pull in charts from multiple places (my home country of Canada’s is below). Japan, Eurozone, China, there’s no point, they all look the same, everything looks like this:

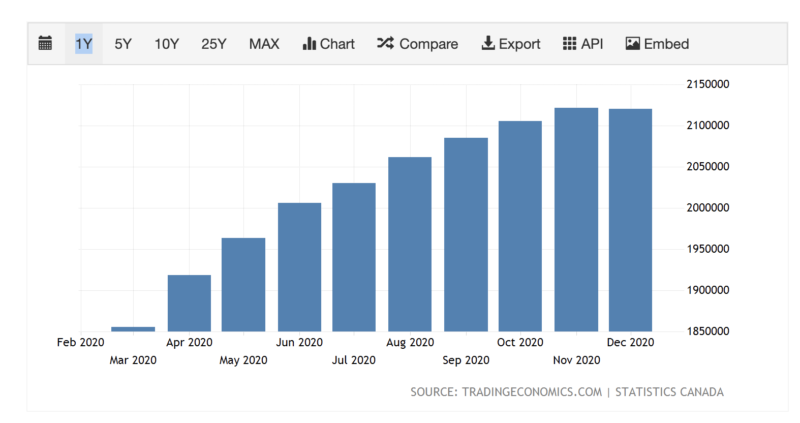

And if you zoom in on the last year, the Pandemic Year that will bisect modern history into The Beforetimes and The New Normal, they all look like this:

The Pandemic panic and the monetary response to it pulled forward what I’ve been calling The Great Bifurcation by decades.

That acceleration and its intensity is a big reason why everything that can be construed as an asset in the world is going like this:

We aren’t in a hyperinflation yet. Policy makers are still trying to pretend inflation is undershooting and they’re still trying like hell to ignite it. As Charles Hugh Smith noted recently, money velocity is plummeting, even as M2 is blasting off (hold that thought).

When you read about historical hyperinflationary episodes, you will find that what invariably happens is that capital flight occurs in all directions and people end up using some sort of “notgelt”. From Jens O. Parsson’s “Dying of Money”

“The seas of marks which had been stored up… flooded forth and fought to buy into other investments, foreign currencies, tangible goods, almost anything but marks

Germany’s money printing industry could not turn out enough trillions to keep up. States, towns, and companies got into the act by issuing their own “emergency money” (Notgeld). Barter became prevalent. Still money grew scarcer while prices continued to soar.”

“Notgeld” could be a peculiar word. It might connote “not money”, “geld” or “gelt” being the German for money. If the money is worthless, people would want what isn’t that. However that’s because we’re thinking in English. “Not money” in German would probably be nichtgeld. Notgeld actually does mean “emergency money”.

In Zimbabwe it was prepaid cellphone cards. In 90’s Yugoslavia things came somewhat full circle and everybody flocked to Deutsche Marks.

One time at easyDNS (in 2019), we found a customer who kept pre-funding his account with us and had enough of a balance in there to prepay his single website out to 2085. When I asked him what the hell he was doing, it turned out he was an Argentine trying to protect his savings through one of their incessant currency collapses. He was using us as a bank.

In all previous hyperinflations people just needed to get out of their local currencies and they’d come up with all manner of ways to do it. But when hyperinflation goes global, across all currencies in all nations, then what do you go into?

Bitcoin in particular and crypto currencies in general are this coming hyper-inflationary event’s “Notgeld”.

The recent institutional move into Bitcoin and cryptocurrencies is a reaction against systemic, global financial repression. What the naysayers like Peter Schiff and Nouriel Roubani don’t get about where we are in history is this:

If Bitcoin didn’t exist, we would have to invent it, right now.

Fortunately Bitcoin and the other crypto-currencies do exist, and they’ve enjoyed a spectacular debut onto the world stage and into monetary history.

Fortunately proof-of-concept has already occurred and countless FUD cycles surmounted.

Fortunately the decentralized crypto ecosystems are ready for prime time, exactly when humanity needs it the most. Necessity really was the mother of invention.

In my Crypto Capitalist Manifesto (30 pages), which is one of the documents subscribers receive after they sign up to my new Crypto Capitalist Letter, I lay out some scenarios which show the theoretical effect of an exodus from bonds and cash on the price of bitcoin, I’ll extract a couple below:

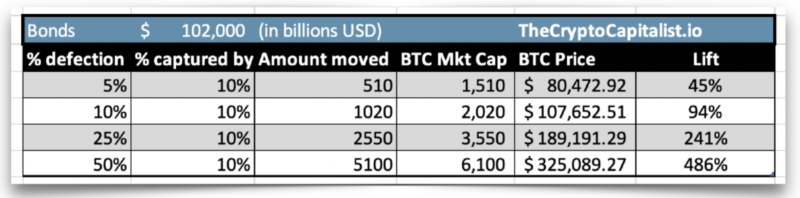

This one estimates the lift to the Bitcoin price in nominal terms based on capturing a fraction of a fraction of a secular exodus from the nearly $20 Trillion USD in negative yield bonds. If half of the capital fled negative yielding debt and of that, 10% moved into Bitcoin, it would push it up over $100K (extrapolating in linear terms of the price is where it is today when this happens).

There’s at least another $100 Trillion USD in nominally positive yield bonds, but mostly negative real returns that would also be good candidates for re-allocation. The second table tries to model Bitcoin capturing a fraction of a fraction of that as well. If there was a 25% exodus out of bonds and Bitcoin caught 10% of that, that alone would put Bitcoin up over $6 Trillion. Other alternative assets like other cryptos, and gold and silver and real estate would all experience similar lifts.

Of course those are all linear extrapolations based on the current price. In the manifesto I model out a bit more, such as Bitcoin capturing more of the exodus out of bonds as it accelerates. There would also be a generalized acceleration of the Bitcoin price once the market participants became increasingly aware of this dynamic.

In other words, this is what I think is happening, metaphorically….

The Crypto Capitalist Letter will (hopefully) be in the tradition of The Privateer, but with a tactical focus on investing in crypto stocks.

Given what has happened to asset prices and crypto in response to just an inkling of inflation, imagine if Charles Hugh Smith is right, looking at the collapse in money velocity occurring now, that this is one final deflationary “tide receding” before the inflationary tsunami hits. Then what happens to the price of Bitcoin, cryptos and gold?

* * *

To receive future posts in your mailbox join the Bombthrower mailing list or follow me on Twitter. We had to push the launch of The Crypto Capitalist Letter into the week of March 22nd, get on the invite list here for when that goes live.

International

TikTok Ban Obscures Chinese Stock Gold Rush

No one wants to invest in China right now. The country’s stock market is teetering on the brink of collapse. And it is about to lose its biggest foothold…

Share this:

No one wants to invest in China right now.

The country’s stock market is teetering on the brink of collapse.

And it is about to lose its biggest foothold in America — TikTok.

Yet, beneath its crumbling economy, military weather balloons and blatant propaganda tools lie some epic opportunities…

…if you have the stomach and the knowledge.

Because as Jim Woods wrote in his newsletter last month:

“China has been so battered for so long, that there is a lot of deep value here for the ‘blood in the ‘’red’’ streets’ investors.”

And boy was he right.

However, this battle-tested veteran didn’t recommend buying individual Chinese stocks.

He was more interested in the exchange-traded funds (ETFs) like the CHIQ.

And here’s why…

Predictable Manipulation

China’s heavy-handed approach creates gaping economic inefficiencies.

When markets falter, President Xi calls on his “national team” to prop up prices.

$17 billion flowed into index-tracking funds in January as the Hang Sang fell over 13% while the CSI dropped over 7%.

Jim Woods saw this coming from a mile away.

In late February, he highlighted the Chinese ETF CHIQ in late February, which has rallied rather nicely since then.

This ETF focuses on the Chinese consumer, a recent passion project for the central government.

You see, around 2018, when President Xi decided to smother his own economy, notable shifts were already taking place.

The once burgeoning retail market had slowed markedly. Developers left cities abandoned, including weird copies of Paris (Tianducheng) and England.

Source: Shutterstock

So, Xi and co. shifted the focus to the consumer… which went terribly.

For starters, a lot of the consumer wealth was tied up in real estate.

Then you had a growing population of unemployed younger adults who didn’t have any money to spend.

Once the pandemic hit, everything collapsed.

That’s why it took China far longer to recover even a sliver of its former economy.

While it’s not the growth engine of the early 2000s, the old girl still has some life left in it.

As Jim pointed out, China’s consumer spending rebounded nicely in Q4 2023.

Source: National Bureau of Statistics of China

Combined with looser central bank policy, it was only a matter of time before Chinese stocks caught a lift.

The resurgence may be largely tied to China’s desire to travel. After all, its people have been cooped up longer than any other country.

But make no mistake, this doesn’t make China a long-term investment.

Beyond what most people understand about China’s politics, there’s a little-known fact about how they treat foreign investors.

Money in. Nothing out.

When we buy a stock, we’re taking partial ownership in that company. This entitles us to a portion of the profits (or assets).

That doesn’t happen with Chinese companies.

American depository receipts (ADRs) aren’t actual shares of a company. It’s a note that the intermediary ties to shares of the company they own overseas.

So, we can only own Chinese companies indirectly.

But there’s another key feature you probably weren’t aware of.

Many of the Chinese companies we, as Americans invest in, don’t pay dividends. In fact, a much smaller percentage of Chinese companies pay any dividends.

Alibaba is a perfect example.

Despite generating billions of dollars in cash every year, it doesn’t pay dividends.

What do its managers do with the money?

Other than squirreling away $80 billion on its balance sheets, they do share buybacks.

Plenty of investors will tell you that’s even better than dividends.

But you have no legal ownership rights in China. So, what is that ADR in reality?

We’d argue nothing but paper profits at best, and air at worst.

That’s why it’s flat-out dangerous to own shares of individual Chinese companies long-term.

Any one of them can be nationalized at any moment.

Chinese ETFs reduce that risk through diversification, similar to junk bond funds.

Short of an all-out ban, like between the United States and Russia, the majority of the ETF holdings should remain intact.

Opportunistic Investing

If China is so unstable, and capable of changing at a moment’s notice, how can investors uncover pockets of value?

As Jim showed with his ETF selection, you can have some sector or thematic idea so long as you have the data to support it.

China, like any large institution, isn’t going to change its broad economic policies overnight.

As long as you study the general movements of the government, you can steer clear of the catastrophic zones and towards the diamond caves.

Because when things look THIS bad, you know the opportunities are even juicier.

But rather than try to run this maze solo, take this opportunity to check out Jim Woods’ latest report on China.

In it, he details the broad economic themes driving the Chinese government, and how to exploit them for gain.

Click here to explore Jim Woods’ report.

The post TikTok Ban Obscures Chinese Stock Gold Rush appeared first on Stock Investor.

stocks pandemic real estate etf consumer spending gold russia chinaInternational

The Great Escape… of UK Unemployment Reporting

https://bondvigilantes.com/wp-content/uploads/2024/03/1-the-great-escape-of-uk-unemployment-reporting-1024×576.pngThe Bank of England Monetary Policy Committee…

Share this:

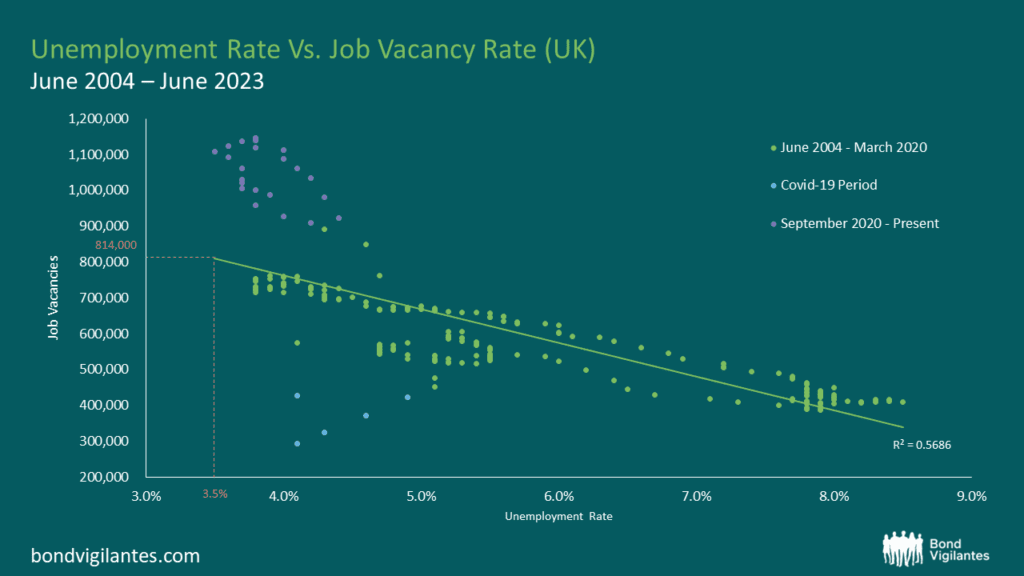

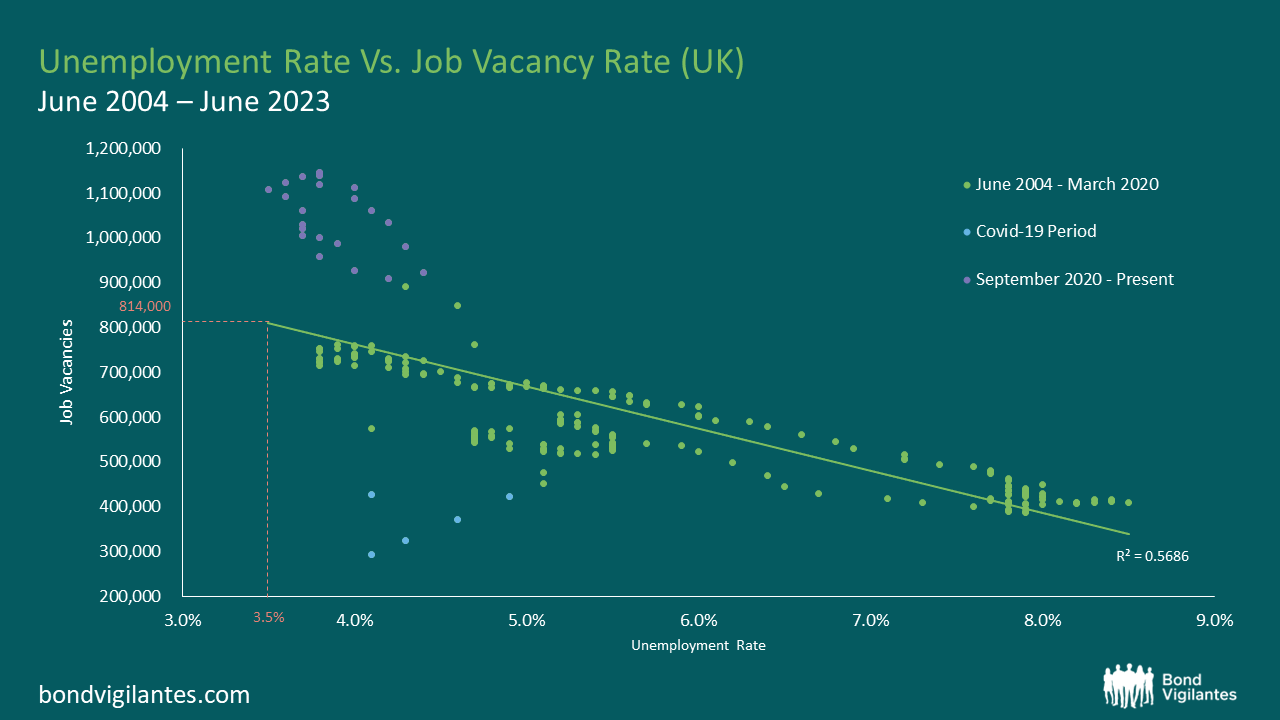

The Bank of England Monetary Policy Committee potentially has a problem: it requires data to make its labour market forecasts and assessments, but the unemployment statistics have become increasingly unreliable. This is because the Labour Force Survey participation rate (on which the unemployment figures are based) has fallen below 50% since 2018 and has been as low as 15% recently[1]. What is the solution to this difficult measurement problem? An answer can be found in the classic war film, The Great Escape.

In 1943, the Escape Committee of Stalag Luft III was tasked with digging a tunnel to freedom. Unfortunately, they had a problem. They needed to measure the distance between one of the prisoner’s huts and the forest beyond the prison perimeter, but they had no reliable tools to measure this critical variable. Fortunately they had two mathematicians within the group who came up with a method to gauge the distance to the forest so that the tunnel would be long enough to ensure escape without detection. The idea was to eyeball the distance using a 20 foot tree for scale (the tree was the one ‘accurate’ measurement around which they could work with). They got individual prisoners to gauge the distance from the hut to the tree and then averaged all of the estimates. The critical distance measure was therefore the average of a large sample size of guesstimates. Fortunately, it more or less worked. Happily, modern economists have an equivalent to rely on in the area of unemployment. Their version of the Stalag Luft III tree strategy is something called the Beveridge Curve.

The Beveridge Curve is simply an observed relationship between an economy’s unemployment rate and its job vacancy rate at the same point in time. An excellent exposition can be found in the Bond Vigilantes archive[2]. When you plot the two variables against one another over a given period, the data points disclose a curve. This curve shows us that when unemployment increases, job vacancies decrease and vice versa. I have plotted the current curve below using the available data from the Office for National Statistics (ONS)[3]. The bottom left quadrant of the graph (the blue dots) relate to the Covid-19 era and the top left quadrant (the purple dots) represent the last 2 years’ worth of data. The green dots represent the remaining data from July 2004 to June 2023.

Source: Office for National Statistics, Dataset JP9Z & UNEM

Source: Office for National Statistics, Dataset JP9Z & UNEM

From these charts and new data from the ONS, we can observe that in the UK, the level of unemployment is increasing and that the job vacancy rate is decreasing. At face value, this suggests that current Bank of England monetary policy is working and that the inflation rate is slowing as the economy cools. One could argue that we are on track for a reasonably soft landing. Nothing new so far.

Things become more interesting when we consider the Beveridge Curve in conjunction with the most recent job vacancy data. We are told that there are now 814,000 job vacancies as of the 31st December 2023[4]. Ordinarily, we would use the curve and clearly be able to extrapolate from the Job Vacancy data what our Unemployment figure might be. However, we also know that the current unemployment data is unreliable, which makes this harder. Using our model inclusive of data oddities, we could extrapolate that with 814,000 job vacancies, we might expect an unemployment rate of around 3.5%. Yet, we know that our unemployment figures are unreliable so the question therefore is, how big an increase in unemployment are we likely to see given what we know about job vacancies?

In order to estimate the magnitude of the rise in unemployment, we need to look further afield. If we study the levels of economic inactivity in the UK, we can observe that they have remained stationary at 22%[5] for the last decade. We can also see that the population of the UK has risen over the same period by around 5.91%[6]. Further, we know that the Labour Force Survey (LFS) samples 40,000 households per quarter to obtain its data, but of late has had a response rate of only 15% (6,000 households). Therefore a critical question for policy makers is what is happening with the 85%, the non-responders?

Given the small sample size, it is entirely possible that the LFS suffered survey bias that is being erroneously weighted away. In other words, the LFS compensates for the paucity of response data by accessing other regional population statistics as a legitimate part of their methodology. The problems of non-responders are being addressed in upcoming LFS releases but for the time being, the data is not as clear as it ought to be. With such a small sample size, it seems possible – indeed probable – that unemployment levels are being underreported. This would explain why the current unemployment rate of 3.8%[7] is dramatically lower than the historic average of 6.7% (1971-2023). We see further evidence for this in the forecasts of the UK’s unemployment rate on Bloomberg which have been consistently above the actual levels for the last few published data points. So whilst the published headline figures might be looking reasonable, the underlying story looks like it could be hiding something more sinister.

Through it all, the Beveridge Curve remains a reasonable template. Job vacancies are definitely falling, so we should expect to see unemployment rising. Like the Stalag Luft III measurement solution, the Beveridge Curve offers a constructive way out of our present statistical dilemma. That being said, analogies can only be taken so far. Unfortunately for the inmates of Stalag Luft III, the calculation didn’t quite work and the tunnel came up short. No one actually made a Great Escape. What does this mean for UK unemployment data? Time may tell.

[1] The UK’s ‘official’ labour data is becoming a nonsense (harvard.edu)

[2] https://bondvigilantes.com/blog/2013/11/a-shifting-beveridge-curve-does-the-us-have-a-long-term-structural-unemployment-problem/

[3] Unemployment – Office for National Statistics (ons.gov.uk)

[4] https://www.ons.gov.uk/employmentandlabourmarket/peopleinwork/employmentandemployeetypes/timeseries/jp9z/unem

[5] https://www.ethnicity-facts-figures.service.gov.uk/work-pay-and-benefits/unemployment-and-economic-inactivity/economic-inactivity/latest/#:~:text=data%20shows%20that%3A-,22%25%20of%20working%20age%20people%20in%20England%2C%20Scotland%20and%20Wales,for%20a%20job)%20in%202022

[6] https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/bulletins/annualmidyearpopulationestimates/mid2021

[7] https://www.ons.gov.uk/employmentandlabourmarket/peoplenotinwork/unemployment

unemployment covid-19 monetary policy unemployment ukInternational

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

By John Cody of Remix News

German Finance Minister…

Share this:

{kind=link}

By John Cody of Remix News

German Finance Minister Christian Lindner is warning his own government that state finances are quickly growing out of hand, and the government needs to change course and implement austerity measures. However, the dispute over spending is only expected to escalate, with budget shortfalls causing open clashes among the three-way left-liberal coalition running the country.

{kind=link}

With negotiations kicking off for the 2025 budget, much is at stake. However, the picture has been complicated after the country’s top court ruled that the government could not shift €60 billion in money earmarked for the coronavirus crisis to other areas of the budget, with the court noting that the move was unconstitutional.

Since then, the government has been in crisis mode, and sought to cut the budget in a number of areas, including against the country’s farmers. Those cuts already sparked mass protests, showcasing how delicate the situation remains for the government.

Lindner, whose party has taken a beating in the polls, is desperate to create some distance from his coalition partners and save his party from electoral disaster. The finance minster says the financial picture facing Germany is dire, and that the budget shortfall will only grow in the coming years if measures are not taken to rein in spending.

“In an unfavorable scenario, the increasing financing deficits lead to an increase in debt in relation to economic output to around 345 percent in the long term,” reads the Sustainability Report released by his office. “In a favorable scenario, the rate will rise to around 140 percent of gross domestic product by 2070.”

Under EU law, Germany has limited its debt levels to 60 percent of economic output, which requires dramatic savings. A huge factor is Germany’s rapidly aging population, with a debt explosion on the horizon as more and more citizens head into retirement while tax revenues shrink and the social welfare system grows — in part due to the country’s exploding immigrant population.

Lindner’s partners, the Greens and Social Democrats (SPD), are loath to cut spending further, as this will harm their electoral chances. In fact, Labor Minister Hubertus Heil is pushing for a new pension package that will add billions to the country’s debt, which remarkably, Lindner also supports.

Continue reading at rmx.news

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Women’s basketball is gaining ground, but is March Madness ready to rival the men’s game?

Gen Z, The Most Pessimistic Generation In History, May Decide The Election

“Extreme Events”: US Cancer Deaths Spiked In 2021 And 2022 In “Large Excess Over Trend”

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

Default: San Francisco Four Seasons Hotel Investors $3 Million Late On Loan As Foreclosure Looms

You can strike gold and silver investment opportunities at Costco

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex