Government

How to use ventilation and air filtration to prevent the spread of coronavirus indoors

How to use ventilation and air filtration to prevent the spread of coronavirus indoors

Share this:

The vast majority of SARS-CoV-2 transmission occurs indoors, most of it from the inhalation of airborne particles that contain the coronavirus. The best way to prevent the virus from spreading in a home or business would be to simply keep infected people away. But this is hard to do when an estimated 40% of cases are asymptomatic and asymptomatic people can still spread the coronavirus to others.

Masks do a decent job at keeping the virus from spreading into the environment, but if an infected person is inside a building, inevitably some virus will escape into the air.

I am a professor of mechanical engineering at the University of Colorado Boulder. Much of my work has focused on how to control the transmission of airborne infectious diseases indoors, and I’ve been asked by my own university, my kids’ schools and even the Alaska State Legislature for advice on how to make indoor spaces safe during this pandemic.

Once the virus escapes into the air inside a building, you have two options: bring in fresh air from outside or remove the virus from the air inside the building.

It’s all about fresh, outside air

The safest indoor space is one that constantly has lots of outside air replacing the stale air inside.

In commercial buildings, outside air is usually pumped in through heating, ventilating and air-conditioning (HVAC) systems. In homes, outside air gets in through open windows and doors, in addition to seeping in through various nooks and crannies.

Simply put, the more fresh, outside air inside a building, the better. Bringing in this air dilutes any contaminant in a building, whether a virus or a something else, and reduces the exposure of anyone inside. Environmental engineers like me quantify how much outside air is getting into a building using a measure called the air exchange rate. This number quantifies the number of times the air inside a building gets replaced with air from outside in an hour.

While the exact rate depends on the number of people and size of the room, most experts consider roughly six air changes an hour to be good for a 10-foot-by-10-foot room with three to four people in it. In a pandemic this should be higher, with one study from 2016 suggesting that an exchange rate of nine times per hour reduced the spread of SARS, MERS and H1N1 in a Hong Kong hospital.

Many buildings in the U.S., especially schools, do not meet recommended ventilation rates. Thankfully, it can be pretty easy to get more outside air into a building. Keeping windows and doors open is a good start. Putting a box fan in a window blowing out can greatly increase air exchange too. In buildings that don’t have operable windows, you can change the mechanical ventilation system to increase how much air it is pumping. But in any room, the more people inside, the faster the air should be replaced.

Using CO2 to measure air circulation

So how do you know if the room you’re in has enough air exchange? It’s actually a pretty hard number to calculate. But there’s an easy-to-measure proxy that can help. Every time you exhale, you release CO2 into the air. Since the coronavirus is most often spread by breathing, coughing or talking, you can use CO2 levels to see if the room is filling up with potentially infectious exhalations. The CO2 level lets you estimate if enough fresh outside air is getting in.

Outdoors, CO2 levels are just above 400 parts per million (ppm). A well ventilated room will have around 800 ppm of CO2. Any higher than that and it is a sign the room might need more ventilation.

Last year, researchers in Taiwan reported on the effect of ventilation on a tuberculosis outbreak at Taipei University. Many of the rooms in the school were underventilated and had CO2 levels above 3,000 ppm. When engineers improved air circulation and got CO2 levels under 600 ppm, the outbreak completely stopped. According to the research, the increase in ventilation was responsible for 97% of the decrease in transmission.

Since the coronavirus is spread through the air, higher CO2 levels in a room likely mean there is a higher chance of transmission if an infected person is inside. Based on the study above, I recommend trying to keep the CO2 levels below 600 ppm. You can buy good CO2 meters for around $100 online; just make sure that they are accurate to within 50 ppm.

Air cleaners

If you are in a room that can’t get enough outside air for dilution, consider an air cleaner, also commonly called air purifiers. These machines remove particles from the air, usually using a filter made of tightly woven fibers. They can capture particles containing bacteria and viruses and can help reduce disease transmission.

The U.S. Environmental Protection Agency says that air cleaners can do this for the coronavirus, but not all air cleaners are equal. Before you go out and buy one, there are few things to keep in mind.

The first thing to consider is how effective an air cleaner’s filter is. Your best option is a cleaner that uses a high-efficiency particulate air (HEPA) filter, as these remove more than 99.97% of all particle sizes.

The second thing to consider is how powerful the cleaner is. The bigger the room – or the more people in it – the more air needs to be cleaned. I worked with some colleagues at Harvard to put together a tool to help teachers and schools determine how powerful of an air cleaner you need for different classroom sizes.

The last thing to consider is the validity of the claims made by the company producing the air cleaner.

The Association of Home Appliance Manufacturers certifies air cleaners, so the AHAM verified seal is a good place to start. Additionally, the California Air Resources Board has a list of air cleaners that are certified as safe and effective, though not all of them use HEPA filters.

Keep air fresh or get outside

Both the World Health Organization and U.S. Centers for Disease Control and Prevention say that poor ventilation increases the risk of transmitting the coronavirus.

If you are in control of your indoor environment, make sure you are getting enough fresh air from outside circulating into the building. A CO2 monitor can help give you a clue if there is enough ventilation, and if CO2 levels start going up, open some windows and take a break outside. If you can’t get enough fresh air into a room, an air cleaner might be a good idea. If you do get an air cleaner, be aware that they don’t remove CO2, so even though the air might be safer, CO2 levels could still be high in the room.

If you walk into a building and it feels hot, stuffy and crowded, chances are that there is not enough ventilation. Turn around and leave.

By paying attention to air circulation and filtration, improving them where you can and staying away from places where you can’t, you can add another powerful tool to your anti-coronavirus toolkit.

[Understand new developments in science, health and technology, each week. Subscribe to The Conversation’s science newsletter.]

Shelly Miller receives funding from the National Science Foundation, Environmental Protection Agency, Centers for Disease Control, National Institutes of Health, and additional nonprofit organizations. She is affiliated with American Association of Aerosol Research and the International Society of Indoor Air Quality and Climate.

International

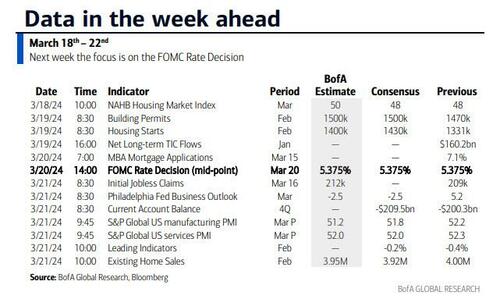

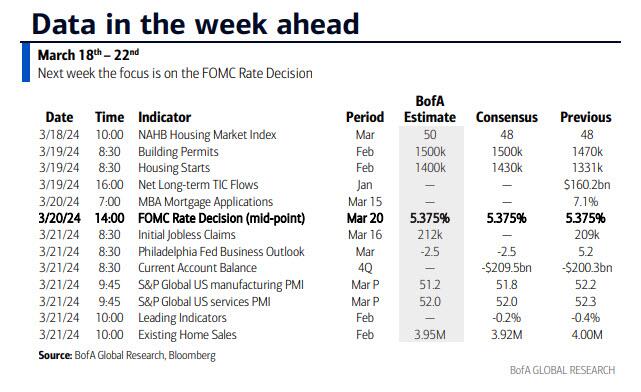

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

According to DB’s Jim Reid, "this could be a landmark…

Share this:

According to DB's Jim Reid, "this could be a landmark week in markets as the last global holdout on negative rates looks set to be removed as the BoJ likely hikes rates from -0.1% tomorrow." That will likely overshadow the FOMC that concludes on Wednesday that will have its own signalling intrigue given recent strong inflation. We also have the RBA meeting tomorrow and the SNB and BoE meetings on Thursday to close out a big week for global central bankers with many EM countries also deciding on policy. We’ll preview the main meetings in more depth below but outside of this we have the global flash PMIs on Thursday as well as inflation reports in Japan (Thursday) and the UK (Wednesday). US housing data also permeates through the week as you'll see in the full global day-by-day week ahead at the end as usual.

Let’s go into detail now, starting with the BoJ tomorrow. We’ve had negative base rates now for 8 years which if is the longest run ever seen for any country in the history of mankind. In fact it is doubtful that pre-historic man was as generous as to charge negative interest rates on lending money prior to this! It also might be one of the longest global runs without any interest rate hikes given the 17 year run that could end tomorrow. So, as Reid puts it, a landmark event.

DB's Chief Japan economist expects the central bank to revise its policy and abandon both NIRP and the multi-tiered current account structure and set rates on all excess reserves at 0.1%. He also sees both the yield curve control (YCC) and the inflation-overshooting commitment ending, replaced by a benchmark for the pace of the bank’s JGB purchasing activity. The house view forecast of 50bps of hikes through 2025 is more hawkish than the market but risks are still tilted to the upside. On Friday, the Japan Trade Union Confederation (Rengo) announced the first tally of the results of this year's shunto spring wage negotiation. The wage increase rate, including the seniority-based wage hike, is 5.28%, which was significantly higher than expected. This year will probably see the highest wage settlements since 1991 which given Japan’s recent history is an incredible turnaround. This wage data news has firmed up expectations for tomorrow.

With regards to the FOMC which concludes on Wednesday, DB economists expect only minor revisions to the meeting statement that saw an overhaul last meeting. With regards to the SEP, the growth and unemployment forecasts are unlikely to change but the 2024 inflation forecasts potentially could; elsewhere, expect the Fed to revise up their 2024 core PCE inflation forecast by a tenth to 2.5%, although they see meaningful risks that it gets revised up even higher to 2.6%. In our economists' view, a 2.5% core PCE reading would allow just enough wiggle room to keep the 2024 fed funds rate at 4.6% (75bps of cuts). However, if core PCE inflation were revised up to 2.6%, it would likely entail the Fed moving their base case back to 50bps of cuts, as this would essentially reflect the same forecasts as the September 2023 SEP.

Beyond 2024, DB expect officials to build in less policy easing due to a higher r-star. If two of the eight officials currently at 2.5% move up by 25bps, then the long-run median forecast would edge up to 2.6%. This could be justified by a one-tenth upgrade to the long-run growth forecast. After all this information is released the presser from Powell will of course be heavily scrutinised, especially on how Powell sees recent inflation data. Powell should also provide an update on discussions around QT but it is unlikely they are ready yet to release updated guidance.

One additional global highlight this week might be a big fall in UK inflation on Wednesday, suggesting that headline CPI will slow to 3.4% (vs 4% in January) and core to 4.5% (5.1%). Elsewhere there is plenty of ECB speaker appearances including President Lagarde on Wednesday. They are all highlighted in the day-by-day guide at the end.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 18

- Data: US March New York Fed services business activity, NAHB housing market index, China February retail sales, industrial production, property investment, Eurozone January trade balance, Canada February raw materials, industrial product price index, existing home sales

Tuesday March 19

- Data: US January total net TIC flows, February housing starts, building permits, Japan January capacity utilization, Germany and Eurozone March Zew survey, Eurozone Q4 labour costs, Canada February CPI

- Central banks: BoJ decision, ECB's Guindos speaks, RBA decision

- Auctions: US 20-yr Bond ($13bn, reopening)

Wednesday March 20

- Data: UK February CPI, PPI, RPI, January house price index, China 1-yr and 5-yr loan prime rates, Japan February trade balance, Italy January industrial production, Germany February PPI, Eurozone March consumer confidence, January construction output

- Central banks: Fed's decision, ECB's Lagarde, Lane, De Cos, Schnabel, Nagel and Holzmann speak, BoC summary of deliberations

- Earnings: Tencent, Micron

Thursday March 21

- Data: US, UK, Japan, Germany, France and Eurozone March PMIs, US March Philadelphia Fed business outlook, February leading index, existing home sales, Q4 current account balance, initial jobless claims, UK February public finances, Japan February national CPI, Italy January current account balance, France March manufacturing confidence, February retail sales, ECB January current account, EU27 February new car registrations

- Central banks: BoE decision, SNB decision

- Earnings: Nike, FedEx, Lululemon, BMW, Enel

- Auctions: US 10-yr TIPS ($16bn, reopening)

- Other: European Union summit, through March 22

Friday March 22

- Data: UK March GfK consumer confidence, February retail sales, Germany March Ifo survey, January import price index, Canada January retail sales

* * *

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the Philadelphia Fed manufacturing index and existing home sales reports on Thursday. The March FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM. There are several speaking engagements from Fed officials this week, including Chair Powell, Vice Chair for Supervision Barr, and President Bostic.

Monday, March 18

- There are no major economic data releases scheduled.

Tuesday, March 19

- 08:30 AM Housing starts, February (GS +9.4%, consensus +7.4%, last -14.8%); Building permits, February (consensus +2.0%, last -0.3%)

Wednesday, March 20

- 02:00 PM FOMC statement, March 19 – March 20 meeting: As discussed in our FOMC preview, we continue to expect the committee to target a first cut in June, but we now expect 3 cuts in 2024 in June, September, and December (vs. 4 previously) given the slightly higher inflation path. We continue to expect 4 cuts in 2025 and now expect 1 final cut in 2026 to an unchanged terminal rate forecast of 3.25-3.5%. The main risk to our expectation is that FOMC participants might be more concerned about the recent inflation data and less convinced that inflation will resume its earlier soft trend. In that case, they might bump up their 2024 core PCE inflation forecast to 2.5% and show a 2-cut median.

Thursday, March 21

- 08:30 AM Current account balance, Q4 (consensus -$209.5bn, last -$200.3bn)

- 08:30 AM Philadelphia Fed manufacturing index, March (GS 3.2, consensus -1.3, last 5.2): We estimate that the Philadelphia Fed manufacturing index fell 2pt to 3.2 in March. While the measure is elevated relative to other surveys, we expect a boost from the rebound in foreign manufacturing activity and the pickup in US production and freight activity.

- 08:30 AM Initial jobless claims, week ended March 16 (GS 210k, consensus 215k, last 209k): Continuing jobless claims, week ended March 9 (consensus 1,815k, last 1,811k)

- 09:45 AM S&P Global US manufacturing PMI, March preliminary (consensus 51.8, last 52.2): S&P Global US services PMI, March preliminary (consensus 52.0, last 52.3)

- 10:00 AM Existing home sales, February (GS +1.2%, consensus -1.6%, last +3.1%)

- 02:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair Michael for Supervision Barr will participate in a fireside chat in Ann Arbor, MI with students and faculty. A moderated Q&A is expected. On February 14, Barr said the Fed is “confident we are on a path to 2% inflation,” but the recent report showing prices rose faster than anticipated in January “is a reminder that the path back to 2% inflation may be a bumpy one.” Barr also noted that “we need to see continued good data before we can begin the process of reducing the federal funds rate.”

Friday, March 22

- 09:00 AM Fed Reserve Chair Powell speaks: The Federal Reserve Board will host a Fed Listens event in Washington D.C. on “Transitioning to the Post-Pandemic Economy.” Chair Powell will deliver opening remarks. Vice Chair Phillip Jefferson and Fed Governor Michelle Bowman will moderate conversations with leaders from various organizations. On March 6, Chair Powell noted in his congressional testimony that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.

- 12:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair for Supervision Michael Barr will participate in a virtual event on “International Economic and Monetary Design.” A moderated Q&A is expected.

- 04:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will participate in a moderated conversation at the 2024 Household Finance Conference in Atlanta. On March 4, Bostic said, “I need to see more progress to feel fully confident that inflation is on a sure path to averaging 2% over time.” Bostic also noted, “I expect the first interest rate cut, which I have penciled in for the third quarter, will be followed by a pause in the following meeting.”

Source: DB, Goldman, BofA

International

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

Key Events This Week: Central Banks Galore Including A Historic Rate Hike By The BOJ

According to DB’s Jim Reid, "this could be a landmark…

Share this:

According to DB's Jim Reid, "this could be a landmark week in markets as the last global holdout on negative rates looks set to be removed as the BoJ likely hikes rates from -0.1% tomorrow." That will likely overshadow the FOMC that concludes on Wednesday that will have its own signalling intrigue given recent strong inflation. We also have the RBA meeting tomorrow and the SNB and BoE meetings on Thursday to close out a big week for global central bankers with many EM countries also deciding on policy. We’ll preview the main meetings in more depth below but outside of this we have the global flash PMIs on Thursday as well as inflation reports in Japan (Thursday) and the UK (Wednesday). US housing data also permeates through the week as you'll see in the full global day-by-day week ahead at the end as usual.

Let’s go into detail now, starting with the BoJ tomorrow. We’ve had negative base rates now for 8 years which if is the longest run ever seen for any country in the history of mankind. In fact it is doubtful that pre-historic man was as generous as to charge negative interest rates on lending money prior to this! It also might be one of the longest global runs without any interest rate hikes given the 17 year run that could end tomorrow. So, as Reid puts it, a landmark event.

DB's Chief Japan economist expects the central bank to revise its policy and abandon both NIRP and the multi-tiered current account structure and set rates on all excess reserves at 0.1%. He also sees both the yield curve control (YCC) and the inflation-overshooting commitment ending, replaced by a benchmark for the pace of the bank’s JGB purchasing activity. The house view forecast of 50bps of hikes through 2025 is more hawkish than the market but risks are still tilted to the upside. On Friday, the Japan Trade Union Confederation (Rengo) announced the first tally of the results of this year's shunto spring wage negotiation. The wage increase rate, including the seniority-based wage hike, is 5.28%, which was significantly higher than expected. This year will probably see the highest wage settlements since 1991 which given Japan’s recent history is an incredible turnaround. This wage data news has firmed up expectations for tomorrow.

With regards to the FOMC which concludes on Wednesday, DB economists expect only minor revisions to the meeting statement that saw an overhaul last meeting. With regards to the SEP, the growth and unemployment forecasts are unlikely to change but the 2024 inflation forecasts potentially could; elsewhere, expect the Fed to revise up their 2024 core PCE inflation forecast by a tenth to 2.5%, although they see meaningful risks that it gets revised up even higher to 2.6%. In our economists' view, a 2.5% core PCE reading would allow just enough wiggle room to keep the 2024 fed funds rate at 4.6% (75bps of cuts). However, if core PCE inflation were revised up to 2.6%, it would likely entail the Fed moving their base case back to 50bps of cuts, as this would essentially reflect the same forecasts as the September 2023 SEP.

Beyond 2024, DB expect officials to build in less policy easing due to a higher r-star. If two of the eight officials currently at 2.5% move up by 25bps, then the long-run median forecast would edge up to 2.6%. This could be justified by a one-tenth upgrade to the long-run growth forecast. After all this information is released the presser from Powell will of course be heavily scrutinised, especially on how Powell sees recent inflation data. Powell should also provide an update on discussions around QT but it is unlikely they are ready yet to release updated guidance.

One additional global highlight this week might be a big fall in UK inflation on Wednesday, suggesting that headline CPI will slow to 3.4% (vs 4% in January) and core to 4.5% (5.1%). Elsewhere there is plenty of ECB speaker appearances including President Lagarde on Wednesday. They are all highlighted in the day-by-day guide at the end.

Courtesy of DB, here is a day-by-day calendar of events

Monday March 18

- Data: US March New York Fed services business activity, NAHB housing market index, China February retail sales, industrial production, property investment, Eurozone January trade balance, Canada February raw materials, industrial product price index, existing home sales

Tuesday March 19

- Data: US January total net TIC flows, February housing starts, building permits, Japan January capacity utilization, Germany and Eurozone March Zew survey, Eurozone Q4 labour costs, Canada February CPI

- Central banks: BoJ decision, ECB's Guindos speaks, RBA decision

- Auctions: US 20-yr Bond ($13bn, reopening)

Wednesday March 20

- Data: UK February CPI, PPI, RPI, January house price index, China 1-yr and 5-yr loan prime rates, Japan February trade balance, Italy January industrial production, Germany February PPI, Eurozone March consumer confidence, January construction output

- Central banks: Fed's decision, ECB's Lagarde, Lane, De Cos, Schnabel, Nagel and Holzmann speak, BoC summary of deliberations

- Earnings: Tencent, Micron

Thursday March 21

- Data: US, UK, Japan, Germany, France and Eurozone March PMIs, US March Philadelphia Fed business outlook, February leading index, existing home sales, Q4 current account balance, initial jobless claims, UK February public finances, Japan February national CPI, Italy January current account balance, France March manufacturing confidence, February retail sales, ECB January current account, EU27 February new car registrations

- Central banks: BoE decision, SNB decision

- Earnings: Nike, FedEx, Lululemon, BMW, Enel

- Auctions: US 10-yr TIPS ($16bn, reopening)

- Other: European Union summit, through March 22

Friday March 22

- Data: UK March GfK consumer confidence, February retail sales, Germany March Ifo survey, January import price index, Canada January retail sales

* * *

Finally, looking at just the US, Goldman notes that the key economic data releases this week are the Philadelphia Fed manufacturing index and existing home sales reports on Thursday. The March FOMC meeting is on Wednesday. The post-meeting statement will be released at 2:00 PM ET, followed by Chair Powell’s press conference at 2:30 PM. There are several speaking engagements from Fed officials this week, including Chair Powell, Vice Chair for Supervision Barr, and President Bostic.

Monday, March 18

- There are no major economic data releases scheduled.

Tuesday, March 19

- 08:30 AM Housing starts, February (GS +9.4%, consensus +7.4%, last -14.8%); Building permits, February (consensus +2.0%, last -0.3%)

Wednesday, March 20

- 02:00 PM FOMC statement, March 19 – March 20 meeting: As discussed in our FOMC preview, we continue to expect the committee to target a first cut in June, but we now expect 3 cuts in 2024 in June, September, and December (vs. 4 previously) given the slightly higher inflation path. We continue to expect 4 cuts in 2025 and now expect 1 final cut in 2026 to an unchanged terminal rate forecast of 3.25-3.5%. The main risk to our expectation is that FOMC participants might be more concerned about the recent inflation data and less convinced that inflation will resume its earlier soft trend. In that case, they might bump up their 2024 core PCE inflation forecast to 2.5% and show a 2-cut median.

Thursday, March 21

- 08:30 AM Current account balance, Q4 (consensus -$209.5bn, last -$200.3bn)

- 08:30 AM Philadelphia Fed manufacturing index, March (GS 3.2, consensus -1.3, last 5.2): We estimate that the Philadelphia Fed manufacturing index fell 2pt to 3.2 in March. While the measure is elevated relative to other surveys, we expect a boost from the rebound in foreign manufacturing activity and the pickup in US production and freight activity.

- 08:30 AM Initial jobless claims, week ended March 16 (GS 210k, consensus 215k, last 209k): Continuing jobless claims, week ended March 9 (consensus 1,815k, last 1,811k)

- 09:45 AM S&P Global US manufacturing PMI, March preliminary (consensus 51.8, last 52.2): S&P Global US services PMI, March preliminary (consensus 52.0, last 52.3)

- 10:00 AM Existing home sales, February (GS +1.2%, consensus -1.6%, last +3.1%)

- 02:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair Michael for Supervision Barr will participate in a fireside chat in Ann Arbor, MI with students and faculty. A moderated Q&A is expected. On February 14, Barr said the Fed is “confident we are on a path to 2% inflation,” but the recent report showing prices rose faster than anticipated in January “is a reminder that the path back to 2% inflation may be a bumpy one.” Barr also noted that “we need to see continued good data before we can begin the process of reducing the federal funds rate.”

Friday, March 22

- 09:00 AM Fed Reserve Chair Powell speaks: The Federal Reserve Board will host a Fed Listens event in Washington D.C. on “Transitioning to the Post-Pandemic Economy.” Chair Powell will deliver opening remarks. Vice Chair Phillip Jefferson and Fed Governor Michelle Bowman will moderate conversations with leaders from various organizations. On March 6, Chair Powell noted in his congressional testimony that if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year.

- 12:00 PM Federal Reserve Vice Chair for Supervision Barr speaks: Federal Reserve Vice Chair for Supervision Michael Barr will participate in a virtual event on “International Economic and Monetary Design.” A moderated Q&A is expected.

- 04:00 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will participate in a moderated conversation at the 2024 Household Finance Conference in Atlanta. On March 4, Bostic said, “I need to see more progress to feel fully confident that inflation is on a sure path to averaging 2% over time.” Bostic also noted, “I expect the first interest rate cut, which I have penciled in for the third quarter, will be followed by a pause in the following meeting.”

Source: DB, Goldman, BofA

International

AI vs. elections: 4 essential reads about the threat of high-tech deception in politics

Using disinformation to sway elections is nothing new. Powerful new AI tools, however, threaten to give the deceptions unprecedented reach.

Share this:

{kind=link}

It’s official. Joe Biden and Donald Trump have secured the necessary delegates to be their parties’ nominees for president in the 2024 election. Barring unforeseen events, the two will be formally nominated at the party conventions this summer and face off at the ballot box on Nov. 5.

It’s a safe bet that, as in recent elections, this one will play out largely online and feature a potent blend of news and disinformation delivered over social media. New this year are powerful generative artificial intelligence tools such as ChatGPT and Sora that make it easier to “flood the zone” with propaganda and disinformation and produce convincing deepfakes: words coming from the mouths of politicians that they did not actually say and events replaying before our eyes that did not actually happen.

The result is an increased likelihood of voters being deceived and, perhaps as worrisome, a growing sense that you can’t trust anything you see online. Trump is already taking advantage of the so-called liar’s dividend, the opportunity to discount your actual words and deeds as deepfakes. Trump implied on his Truth Social platform on March 12, 2024, that real videos of him shown by Democratic House members were produced or altered using artificial intelligence.

The Conversation has been covering the latest developments in artificial intelligence that have the potential to undermine democracy. The following is a roundup of some of those articles from our archive.

1. Fake events

The ability to use AI to make convincing fakes is particularly troublesome for producing false evidence of events that never happened. Rochester Institute of Technology computer security researcher Christopher Schwartz has dubbed these situation deepfakes.

“The basic idea and technology of a situation deepfake are the same as with any other deepfake, but with a bolder ambition: to manipulate a real event or invent one from thin air,” he wrote.

Situation deepfakes could be used to boost or undermine a candidate or suppress voter turnout. If you encounter reports on social media of events that are surprising or extraordinary, try to learn more about them from reliable sources, such as fact-checked news reports, peer-reviewed academic articles or interviews with credentialed experts, Schwartz said. Also, recognize that deepfakes can take advantage of what you are inclined to believe.

2. Russia, China and Iran take aim

From the question of what AI-generated disinformation can do follows the question of who has been wielding it. Today’s AI tools put the capacity to produce disinformation in reach for most people, but of particular concern are nations that are adversaries of the United States and other democracies. In particular, Russia, China and Iran have extensive experience with disinformation campaigns and technology.

“There’s a lot more to running a disinformation campaign than generating content,” wrote security expert and Harvard Kennedy School lecturer Bruce Schneier. “The hard part is distribution. A propagandist needs a series of fake accounts on which to post, and others to boost it into the mainstream where it can go viral.”

Russia and China have a history of testing disinformation campaigns on smaller countries, according to Schneier. “Countering new disinformation campaigns requires being able to recognize them, and recognizing them requires looking for and cataloging them now,” he wrote.

3. Healthy skepticism

But it doesn’t require the resources of shadowy intelligence services in powerful nations to make headlines, as the New Hampshire fake Biden robocall produced and disseminated by two individuals and aimed at dissuading some voters illustrates. That episode prompted the Federal Communications Commission to ban robocalls that use voices generated by artificial intelligence.

AI-powered disinformation campaigns are difficult to counter because they can be delivered over different channels, including robocalls, social media, email, text message and websites, which complicates the digital forensics of tracking down the sources of the disinformation, wrote Joan Donovan, a media and disinformation scholar at Boston University.

“In many ways, AI-enhanced disinformation such as the New Hampshire robocall poses the same problems as every other form of disinformation,” Donovan wrote. “People who use AI to disrupt elections are likely to do what they can to hide their tracks, which is why it’s necessary for the public to remain skeptical about claims that do not come from verified sources, such as local TV news or social media accounts of reputable news organizations.”

4. A new kind of political machine

AI-powered disinformation campaigns are also difficult to counter because they can include bots – automated social media accounts that pose as real people – and can include online interactions tailored to individuals, potentially over the course of an election and potentially with millions of people.

Harvard political scientist Archon Fung and legal scholar Lawrence Lessig described these capabilities and laid out a hypothetical scenario of national political campaigns wielding these powerful tools.

Attempts to block these machines could run afoul of the free speech protections of the First Amendment, according to Fung and Lessig. “One constitutionally safer, if smaller, step, already adopted in part by European internet regulators and in California, is to prohibit bots from passing themselves off as people,” they wrote. “For example, regulation might require that campaign messages come with disclaimers when the content they contain is generated by machines rather than humans.”

Read more: How AI could take over elections – and undermine democracy

This story is a roundup of articles from The Conversation’s archives.

This article is part of Disinformation 2024: a series examining the science, technology and politics of deception in elections.

You may also be interested in:

Misinformation, disinformation and hoaxes: What’s the difference?

trump pandemic testing iran european russia china

Mistakes Were Made

Home buyers must now navigate higher mortgage rates and prices

Supreme Court Rules Public Officials May Block Their Constituents On Social Media

Gen Z, The Most Pessimistic Generation In History, May Decide The Election

“Extreme Events”: US Cancer Deaths Spiked In 2021 And 2022 In “Large Excess Over Trend”

Harvard Medical School Professor Was Fired Over Not Getting COVID Vaccine

Germany Is Running Out Of Money And Debt Levels Are Exploding, Finance Minister Warns

You can strike gold and silver investment opportunities at Costco

TikTok Ban Obscures Chinese Stock Gold Rush

Supreme Court To Hear Arguments In Biden Admin’s Censorship Of Social Media Posts

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Spread & Containment5 days ago

Spread & Containment5 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex