Spread & Containment

How to use statistics to prepare for the next pandemic

Many governments, including the US, already collect and make public population statistics that could help them prepare for the next pandemic.

Share this:

The Research Brief is a short take about interesting academic work.

The big idea

Publicly available statistics about population demographics and culture can help governments prepare for the next pandemic. We have found that by using existing socio-demographic data from early COVID-19 hot spots, where there was a lot of information, officials could have predicted how COVID-19 would spread through society. The next time there is a global health crisis governments can use our techniques to figure out how a disease will likely move beyond hot spots to regions that are not yet affected.

With a computational social scientist and a librarian for science, technology and mathematics research, we study the socio-cultural drivers of public health crises, such as obesity. In two peer-reviewed papers that we published in early 2021, which build on our previous research, we analyzed these drivers at the scale of U.S. counties and at scale of nations. Both studies connected socio-cultural variables to the impact of COVID-19.

For our U.S. study, we collected data from 3,088 U.S. counties on 31 factors that could affect the spread of COVID-19. These factors included population density and ethnicity, commuting habits for work, voting patterns, social connectivity, underlying health conditions and economic information. We collected this information from the U.S. Census Bureau and a variety of other sources.

Using these factors, we built a predictive model of COVID-19 prevalence. We found that just five risk factors can predict between 47% and 60% of variation in COVID-19 prevalence in U.S. counties: population size, population density, public transport, voting patterns and percent African American population. We validated our model by showing that counties which reported fewer COVID-19 cases in April than expected in our model tended to have more cases in July. The results thus provide a new way of discerning when a U.S. county is under-reporting the actual number of infections present in the community.

In the second paper we sought to explain why certain countries, like the U.S., have death tolls in the hundreds of thousands, while other nations had very few deaths. Using international data from a large survey, measuring cultural values in 88 countries, we found demographic factors like population size and obesity levels were important. But more surprising, we found culture was also important, in that open and tolerant societies, as well as those with low trust in institutions, tended to fare the worst.

This analysis made some surprising predictions about the spread of COVID-19 around the world. For example, while many believed in early 2020 that African countries would be heavily affected by COVID-19, our model predicted that they would not. So far this has been true.

In the U.S., which scored high on many of the socio-cultural risk factors – including low trust in institutions, high tolerance toward minorities and high levels of obesity – COVID-19 has hit very hard. Nearly 583,000 people in the U.S. had died from COVID-19 as of May 12, 2021. That is the highest absolute number of deaths in any nation so far, and roughly 17.5% of global deaths from the virus, in a country where only 4% of the world population lives.

Why it matters

Governments struggle to predict and plan for the location and extent of disease outbreaks. With so many moving parts, from local mandates like economic shutdowns and face mask recommendations, to international travel bans or restrictions, it seems almost impossible to project the number of cases in different counties or regions. In the average week, how many cases might you expect to have? Should the U.S. expect more cases than Ghana? Why might one city or region be hit harder than another?

We show that additional planning based upon cultural and demographic factors can help predict how outbreaks could progress. It can also reveal which people may be most vulnerable. Properly applied, this data-driven approach might save hundreds of thousands of lives when the next pandemic hits.

What still isn’t known

Our goal is to use the predictive power of cultural and demographic data to anticipate the spread of future pandemics. But neither of our studies specify a relationship between cause and effect.

[Over 100,000 readers rely on The Conversation’s newsletter to understand the world. Sign up today.]

For example, when looking at the U.S., one of the five predictive factors is the proportion of the population that is African American: Higher proportions predicted higher infection and death rates. Our analysis, however, did not determine whether this one factor might subsume many other truly causal factors. The social science and public health literature posits reasons why African American populations have suffered more from COVID-19, including bigger households, underlying health conditions and a tendency to work in sectors with greater risk of exposure.

R. Alexander Bentley received funding from the U.S. National Science Foundation.

spread deaths pandemic covid-19Spread & Containment

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

Two years ago, we first said that it’s only a matter…

Share this:

Two years ago, we first said that it's only a matter of time before the Fed admits it is unable to rsolve the so-called "last mile" of inflation and that as a result, the old inflation target of 2% is no longer viable.

At some point Fed will concede it has no control over supply. That's when we will start getting leaks of raising the inflation target

— zerohedge (@zerohedge) June 21, 2022

Then one year ago, we correctly said that while everyone was paying attention elsewhere, the inflation target had already been hiked to 2.8%... on the way to even more increases.

The new inflation target has been set to 2.8%. The rest is just narrative fill for the next 2 years. https://t.co/X1xYkecyPy

— zerohedge (@zerohedge) February 21, 2023

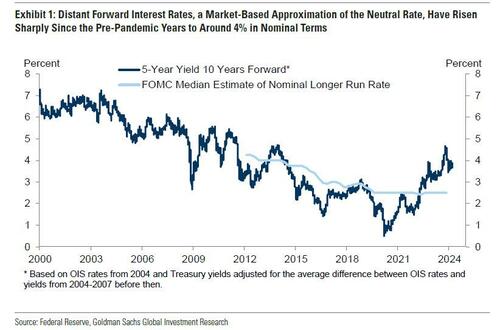

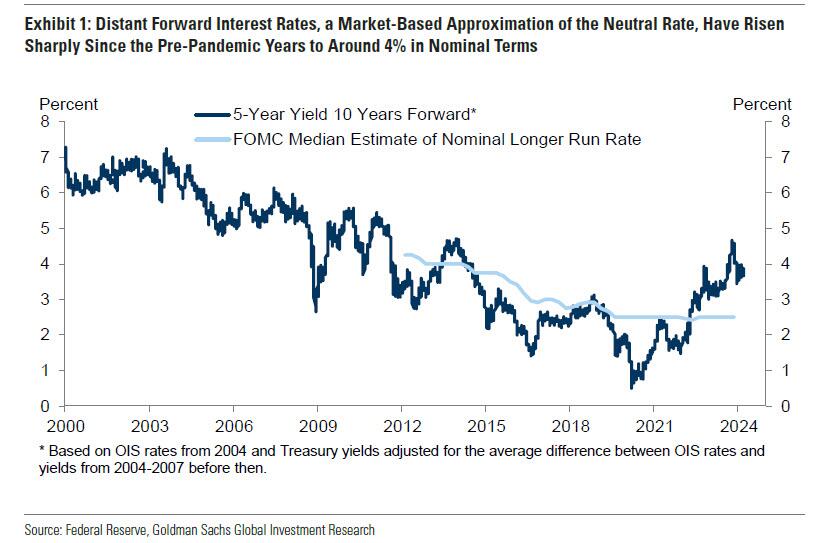

And while the Fed still pretends it can one day lower inflation to 2% even as it prepares to cut rates as soon as June, moments ago Goldman published a note from its economics team which had to balls to finally call a spade a spade, and concluded that - as party of the Fed's next big debate, i.e., rethinking the Neutral rate - both the neutral and terminal rate, a polite euphemism for the inflation target, are much higher than conventional wisdom believes, and that as a result Goldman is "penciling in a terminal rate of 3.25-3.5% this cycle, 100bp above the peak reached last cycle."

There is more in the full Goldman note, but below we excerpt the key fragments:

We argued last cycle that the long-run neutral rate was not as low as widely thought, perhaps closer to 3-3.5% in nominal terms than to 2-2.5%. We have also argued this cycle that the short-run neutral rate could be higher still because the fiscal deficit is much larger than usual—in fact, estimates of the elasticity of the neutral rate to the deficit suggest that the wider deficit might boost the short-term neutral rate by 1-1.5%. Fed economists have also offered another reason why the short-term neutral rate might be elevated, namely that broad financial conditions have not tightened commensurately with the rise in the funds rate, limiting transmission to the economy.

Over the coming year, Fed officials are likely to debate whether the neutral rate is still as low as they assumed last cycle and as the dot plot implies....

...Translation: raising the neutral rate estimate is also the first step to admitting that the traditional 2% inflation target is higher than previously expected. And once the Fed officially crosses that particular Rubicon, all bets are off.

... Their thinking is likely to be influenced by distant forward market rates, which have risen 1-2pp since the pre-pandemic years to about 4%; by model-based estimates of neutral, whose earlier real-time values have been revised up by roughly 0.5pp on average to about 3.5% nominal and whose latest values are little changed; and by their perception of how well the economy is performing at the current level of the funds rate.

The bank's conclusion:

We expect Fed officials to raise their estimates of neutral over time both by raising their long-run neutral rate dots somewhat and by concluding that short-run neutral is currently higher than long-run neutral. While we are fairly confident that Fed officials will not be comfortable leaving the funds rate above 5% indefinitely once inflation approaches 2% and that they will not go all the way back to 2.5% purely in the name of normalization, we are quite uncertain about where in between they will ultimately land.

Because the economy is not sensitive enough to small changes in the funds rate to make it glaringly obvious when neutral has been reached, the terminal or equilibrium rate where the FOMC decides to leave the funds rate is partly a matter of the true neutral rate and partly a matter of the perceived neutral rate. For now, we are penciling in a terminal rate of 3.25-3.5% this cycle, 100bps above the peak reached last cycle. This reflects both our view that neutral is higher than Fed officials think and our expectation that their thinking will evolve.

Not that this should come as a surprise: as a reminder, with the US now $35.5 trillion in debt and rising by $1 trillion every 100 days, we are fast approaching the Minsky Moment, which means the US has just a handful of options left: losing the reserve currency status, QEing the deficit and every new dollar in debt, or - the only viable alternative - inflating it all away. The only question we had before is when do "serious" economists make the same admission.

Meanwhile, nothing changes: total US debt jumps $57BN on March 15, to a record $34.543 trillion.

— zerohedge (@zerohedge) March 19, 2024

Three ways this ends: inflate it away, QE it all, or reserve status collapse

They now have.

And while we have discussed the staggering consequences of raising the inflation target by just 1% from 2% to 3% on everything from markets, to economic growth (instead of doubling every 35 years at 2% inflation target, prices would double every 23 years at 3%), and social cohesion, we will soon rerun the analysis again as the implications are profound. For now all you need to know is that with the US about to implicitly hit the overdrive of dollar devaluation, anything that is non-fiat will be much more preferable over fiat alternatives.

Much more in the full Goldman note available to pro subs in the usual place.

Spread & Containment

Household Net Interest Income Falls As Rates Spike

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical…

Share this:

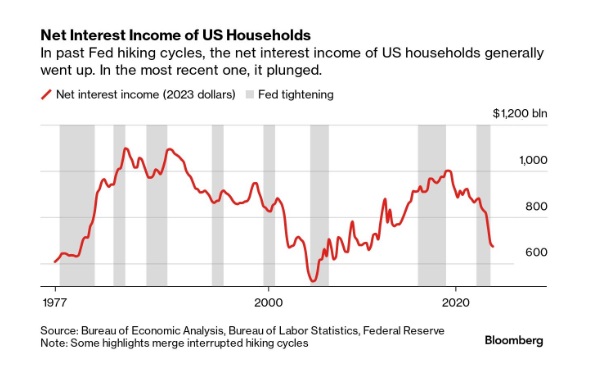

A Bloomberg article from this morning offered an excellent array of charts detailing the shifts in interest payment flows amid rising rates. The historical anomaly was both surprising and contradicted our priors.

10 Key Points:

- Historical Anomaly: This is the first time in the last fifty years that a Federal Reserve rate hike cycle has led to a significant drop in household net interest income.

- Interest Expense Increase: Since the Fed began raising rates in March 2022, Americans’ annual interest expenses on debts like mortgages and credit cards have surged by nearly $420 billion.

- Interest Income Lag: The increase in interest income during the same period was only about $280 billion, resulting in a net decline in household interest income, a departure from past trends.

- Consumer Debt Influence: The recent rate hikes impacted household finances more because of a higher proportion of consumer credit, which adjusts more quickly to rate changes, increasing interest costs.

- Banks and Savers: Banks have been slow to pass on higher interest rates to depositors, and the prolonged period of low rates before 2022 may have discouraged savers from actively seeking better returns.

- Shift in Wealth: There’s been a shift from interest-bearing assets to stocks, with dividends surpassing interest payments as a source of unearned income during the pandemic.

- Distributional Discrepancy: Higher interest rates benefit wealthier individuals who own interest-earning assets, whereas lower-income earners face the brunt of increased debt servicing costs, exacerbating economic inequality.

- Job Market Impact: Typically, Fed rate hikes affect households through the job market, as businesses cut costs, potentially leading to layoffs or wage suppression, though this hasn’t occurred yet in the current cycle.

- Economic Impact: The distribution of interest income and debt servicing means that rate increases transfer money from those more likely to spend (and thus stimulate the economy) to those less likely to increase consumption, potentially dampening economic activity.

- No Immediate Relief: Expectations for the Fed to reduce rates have diminished, indicating that high-interest expenses for households may persist.

Spread & Containment

TJ Maxx and Marshalls follow Costco and Target on upcoming closures

Many of these stores have information customers need to know.

Share this:

{kind=link}

U.S. consumers have come to increasingly rely on the near ubiquity of convenience stores and big-box retailers.

Many of us depend on these stores being open practically all day, every day, even during some of the biggest holidays. After all, Black Friday beckons retail stores to open just hours after a Thanksgiving Day dinner in hopes of attracting huge crowds of shoppers in search of early holiday sales.

Related: Walmart announces more store closures for 2024

And it's largely true that before the covid pandemic most of our favorite stores were open all the time. Practically nothing — from inclement weather to bad news to holidays — could shut down a major operation like Walmart (WMT) or Target (TGT) .

Then the pandemic hit, and it turned everything we thought we knew about retail operations upside down.

Everything from grocery stores to shopping malls shut down in an effort to contain potential spread. And when they finally reopened to the public, different stores took different precautionary measures. Some monitored how many shoppers were inside at once, while others implemented foot-traffic rules dictating where one could enter and exit an aisle. And almost every one of them mandated wearing masks at one point or another.

Though these safety measures seem like a distant memory, one relic from the early 2020s remains firmly a part of our new American retail life.

Store closures announced for spring 2024

Many retailers have learned to adapt after a volatile start to this third decade, and in many ways this requires serving customers better and treating employees better to retain a workforce.

In some cases, the changes also reflect a change in shopping behavior, as more customers order online and leave more breathing room for brick-and-mortar operations. This also means more time for employees.

Thanks to this, big retailers have recently changed how they operate, especially during holiday hours, with Walmart recently saying it would close during Thanksgiving to give employees more time to spend with loved ones.

"I am delighted to share that once again, we'll be closing our doors for Thanksgiving this year," Walmart U.S. CEO John Furner told associates in a video posted to Twitter in November. "Thanksgiving is such a special day during a very busy season. We want you to spend that day at home with family and loved ones."

Other retailers have now followed suit, with Costco (COST) , Aldi, and Target all saying they would close their doors for 24 hours on Easter Sunday, March 31.

Now, the stores that operate under TJX Cos. (TJX) will also shut down during the holiday, including HomeGoods, TJ Maxx and Marshalls.

Though it closed on Thanksgiving, Walmart says it will remain open for shoppers on Easter.

Here's a list of stores that are closing for Easter 2024:

- Target

- Costco

- Aldi

- TJ Maxx

- Marshalls

- HomeGoods

- Publix

- Macy's

- Best Buy

- Apple

- ACE Hardware

Others are expected to remain open, including:

- Walmart

- Ikea

- Petco

- Home Depot

Most of the stores closing on Sunday will reopen for regular business hours on Monday.

spread pandemic

Google’s A.I. Fiasco Exposes Deeper Infowarp

Report Criticizes ‘Catastrophic Errors’ Of COVID Lockdowns, Warns Of Repeat

There Goes The Fed’s Inflation Target: Goldman Sees Terminal Rate 100bps Higher At 3.5%

Gates-backed PhIII study tuberculosis vaccine study gets underway

AI vs. elections: 4 essential reads about the threat of high-tech deception in politics

Supreme Court To Hear Arguments In Biden Admin’s Censorship Of Social Media Posts

Household Net Interest Income Falls As Rates Spike

Artificial mucus identifies link to tumor formation

Supreme Court’s questions about First Amendment cases show support for ‘free trade in ideas’

Choosing over the counter drugs for COVID 19? It’s complicated

-

Spread & Containment7 days ago

Spread & Containment7 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International2 weeks ago

International2 weeks agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized1 month ago

Uncategorized1 month agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized1 month ago

Uncategorized1 month agoIndustrial Production Decreased 0.1% in January

-

International2 weeks ago

International2 weeks agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized1 month ago

Uncategorized1 month agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex