Soon, you’ll wake up to hear reports on CNBC and Twitter about ATM machines not working across the country.

JPMorgan Chase CEO Jamie Dimon will appear on CNBC, to explain that for the good of the country, his bank and all the other banks in the country are buying long-dated Treasury bonds. And, to protect America, it’s important that we all take a pause and stop withdrawing cash from the system, which means a “temporary” shutdown of other banking operations for a week or two.

It will happen. It’s unavoidable.

A couple of interesting facts…

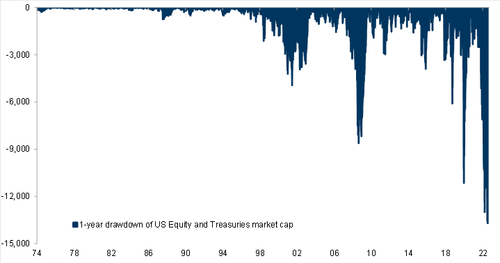

The price of U.S. Treasury bonds is collapsing. Since the end of July, the 10-year Treasury rate has risen sharply, from a yield of 2.65% to over 4.3% now. There haven’t been bigger losses in the U.S. Treasury bond market, EVER.

Signs of inflation are fading, and the American economy is obviously heading into a severe recession.

But rather than stabilizing – which is what usually happens – the selloff in longer-dated U.S. Treasury securities is intensifying, and liquidity is at its lowest levels since March 2020.

That suggests that the market doesn’t trust the dollar anymore. And that means the entire system is at risk.

Payback’s A Witch

The sell-off in long-dated Treasuries isn’t because of last year’s inflation. It’s because the market knows that the U.S. Treasury cannot possibly afford a real rate of interest on its massive $31 trillion in debt.

Think about it: this year’s increase in Social Security benefits payments is 8.7%. At even half that rate of inflation, a 2% real yield on a 10-year U.S. Treasury bond would be well above 6%. If the U.S. government has to pay anything like that rate of interest to roll over its debts (average duration is 5 years) in the coming years, it is already bankrupt.

There are $24 trillion worth of publicly traded U.S. Treasury securities. At 6% interest, that’s $1.4 trillion a year in payments. That’s roughly 40% of total federal tax receipts.

This same kind of panic struck last month in the long-dated bonds of Great Britain. Now, along with big declines in long-dated U.S. sovereign bonds, the Japanese yen is falling apart, and the Swiss National Bank is suddenly accessing currency swap loan facilities from the Federal Reserve.

Most worryingly, liquidity is disappearing in the U.S. Treasury market, the most liquid financial market in the world. Analysts at Bank of America wrote yesterday that “the [U.S. Treasury] market is fragile and potentially one shock away from functioning challenges.” That’s broker-speak for “we’re in uncharted territory here.”

We are on the cusp of a complete panic in the world’s bond markets. Like we explained last week, a global “Minsky Moment” is looming.

We think this crisis will be the largest the world has seen since World War II. That brought the end of sterling’s role as the world’s reserve currency. This will end the U.S. dollar’s reign as the world’s reserve currency.

What’s next is going to be incredibly painful. Most of the developed world is going to see its standard of living decline 30% to 50% over the next 4-6 years. There’s going to be a lot of anger and a lot of violence.

It’s worth remembering how we got here.

Lies, Damned Lies, And Printing Presses

I’m talking about Ben Bernanke. As the Chairman of the Federal Reserve from 2006-2014, he decided in the aftermath of the Global Financial Crisis that the banking system had to be saved, by any means necessary. To finance the massive losses – which were over $10 trillion in the U.S. alone – the world’s central banks began printing money and buying government bonds to finance massive bailouts.

Like squirrels watching a bank robbery, the members of the Nobel Committee – which recently awarded Bernanke the prize in economics – saw everything that happened and knew nothing about what it meant.

Printing money doesn’t cure economic problems: it simply skews who pays for them.

Printing trillions to paper over the financial system’s losses moved the egregious errors of Bank of America, Bear Stearns, Lehman Brothers, Goldman Sachs, AIG, Fannie Mae and Freddie Mac, General Electric, General Motors and others from their balance sheets, onto the balance sheet of the U.S. Treasury and the Federal Reserve.

Morally these actions are repugnant – much like requiring that taxpayers finance hundreds of billions’ worth of second-rate college educations for 10 million lazy, underachieving students – but on a vastly bigger scale.

The real problem isn’t financial. Printing money changes societies by giving the government virtually unlimited amounts of power. That warps the ambitions of politicians and gives socialists unlimited budgets. People soon believe every problem can be solved by the government and the printing press. Trade-offs are no longer required. Costs are no longer relevant. In this kind of environment, no problem is too big to solve through politics and the central bank. And if there isn’t a crisis, then one will soon be invented.

And, sure enough, as soon as the U.S. central bank began to sell assets and return to “normal” policies in 2018 and 2019, a new, even bigger crisis was “found.”

A novel coronavirus. Never mind that coronaviruses appear all the time and that most people will get and survive the flu a half dozen times in their lives… this time the world went completely nuts.

Everything was shut down for two years – except politics. Trillions were spent on vaccines – vaccines that don’t prevent you from getting Covid or from transmitting Covid. It was definitely a government vaccine: it cost trillions, everyone was forced to use it, and it didn’t work.

Nothing else worked during the Covid lockdown either. Kids don’t learn at home. Employees don’t work at home. Flimsy surgical masks don’t prevent you from contracting or spreading Covid – they don’t work, but they were required too. Fauci wore two masks, everywhere. He received four different shots of the “vaccine.” Guess who got Covid anyway?

Worst of all, the government spent unlimited sums of money on things like the ridiculous “paycheck protection program,” which might as well have been called “Fraud on a Federal Scale For You.”

The lie that we could print over the mortgage losses led directly to the lie that wearing a paper mask can stop a virus. Or that a vaccine created in a few weeks and tested only on a handful of people could stop a coronavirus that constantly mutates. With a printing press, there’s no problem that appears too big for the government to handle.

But, much like the “vaccine” and the paper masks, the printing press is just a lie too.

Altogether, the world’s central banks have printed over $25 trillion over the last 12 years.

In the United States, the printing was equal to more than 30% of our GDP. In the Eurozone, the printing was twice as large – over 60% of GDP. In Japan, the printing has been equal to over 100% of GDP.

You can think of these figures as being the size of the mirage we’ve been living in.

Reality looms.

Time to Opt-Out of “Money” Entirely

Our advice? Do everything you can to avoid holding the currency or the bonds of bankrupt western nations that have been trying to print their way to prosperity. And most importantly, do not let the current rally in the U.S. dollar fool you.

Yes, it’s the basis of the current monetary standard and, as such, in a crisis it is where all the banks will hide. It could continue to strengthen for several more weeks or months. But it has no more legitimacy than the euro or the yen. And it is only a matter of time – maybe only hours – before it will begin printing again, trying to keep the system from coming apart at the seams. Maybe it will work – but only after the value of the dollar (and the rest of the paper money) has fallen by 50% or more.

What will survive this crisis? Energy. Bitcoin. Land. Timber. Critical metals, like copper. High-quality, capital efficient businesses that aren’t in debt.

What will fail? Anything that has to refinance debt in the next 5-7 years.

In a new book, experts in a variety of fields explore nocebo effects – how negative expectations concerning health can make a person sick. It is the first time a book has been written on this subject.

“I think it’s the idea that words really matter. It’s fascinating that how we communicate can affect the outcome. Communication in health care is perhaps more important than the patient recognises,” says Charlotte Blease, who is a researcher at the Department of Women’s and Children’s Health at Uppsala University.

Along with colleagues at Brown University in the United States and the University of Zurich in Switzerland she has written the book “The Nocebo Effect: When Words Make You Sick”. Nocebo is sometimes called the placebo’s evil twin. A placebo effect occurs when a patient thinks they feel better because of receiving medicine and part of that perception is due not to the drug but to positive expectations. The concept of the nocebo effect means that harmful things can happen because a person expects it – unconsciously or consciously. This is the first time the phenomenon has been addressed in a scholarly book. Researchers in medicine, history, culture, psychology and philosophy have examined it, each in their own particular area.

Credit: Catherine Blease

In a new book, experts in a variety of fields explore nocebo effects – how negative expectations concerning health can make a person sick. It is the first time a book has been written on this subject.

“I think it’s the idea that words really matter. It’s fascinating that how we communicate can affect the outcome. Communication in health care is perhaps more important than the patient recognises,” says Charlotte Blease, who is a researcher at the Department of Women’s and Children’s Health at Uppsala University.

Along with colleagues at Brown University in the United States and the University of Zurich in Switzerland she has written the book “The Nocebo Effect: When Words Make You Sick”. Nocebo is sometimes called the placebo’s evil twin. A placebo effect occurs when a patient thinks they feel better because of receiving medicine and part of that perception is due not to the drug but to positive expectations. The concept of the nocebo effect means that harmful things can happen because a person expects it – unconsciously or consciously. This is the first time the phenomenon has been addressed in a scholarly book. Researchers in medicine, history, culture, psychology and philosophy have examined it, each in their own particular area.

“It’s a very new field, an emerging discipline. Even if the nocebo effect is documented far back in history, it perhaps became especially obvious during the coronavirus pandemic,” Blease says.

A previous study of patients during the pandemic (see below) shows that as many as three quarters of the reported side-effects of the coronavirus vaccine may be due to the nocebo effect. The study involved more than 45,000 participants, approximately half of whom were injected with a saline solution instead of the vaccine but despite this still experienced many side-effects such as nausea and headache. In the book, the authors highlight that one issue that disappeared in the discussion of side-effects during the coronavirus pandemic was that many of these were actually due to the nocebo effect.

“Whether this is due to expectations – the nocebo effect – remains to be understood. However, it is curious that so many participants reported side-effects after receiving no vaccine. Regardless, some people may have been put off by what they heard about side-effects,” Blease comments.

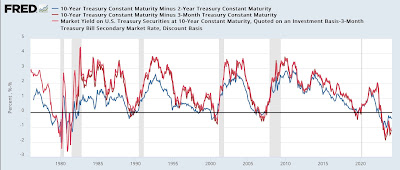

Prof. Menzie Chinn at Econbrowser makes the point that the yield curve is still inverted, and has not yet eclipsed the longest previous time between onset of such an inversion and a recession. So he believes the threat of recession is still on the table.

And he’s correct about the yield curve, although it is getting very long in the tooth. In the past half century, the shortest time between a 10 minus 2 year inversion (blue in the graph below) to recession has been 10 months (1980) and the longest 22 months (2007). For the 10 year minus 3 month inversion (red), the shortest time has been 8 months (1980 and 2001) and the longest has been 17 months (2007):

At present the former yield curve has been inverted for 20.5 months, and the latter for 16.5 months. So if there is no recession by May 1, we’re in uncharted territory as far as the yield curve indicator is concerned.

My view for the past half year or so has been much more cautious. While there has been nearly unprecedented Fed tightening (only the 1980-81 tightening was more severe), on the other hand there was massive pandemic stimulus, and what I described on some occasions as a “hurricane force tailwind” of supply chain unkinking. If the two positive forces have abated, does the negative force of the Fed tightening, which is still in place, now take precedence? Or because interest rates have plateaued in the past year, is it too something of a spent force? Since I confess not to know, because the situation is unprecedented in the modern era for which most data is available, I have highlighted turning to the short leading metrics. Do they remain steady or improve? Or do they deteriorate as they have before prior recessions?

First of all, let me show the NY Fed’s Global Supply Chain Index, which attempts to disaggregate supply sided information from demand side information. A positive value shows relative tightening, a negative loosening:

You can see the huge pandemic tightening in 2020 into 2022, followed by a similarly large loosening through 2023. For the past few months, the Index has been close to neutral, or shown very slight tightness.

Typically in the past Fed tightenings have operated through two main channels: housing and manufacturing, especially durable goods manufacturing.

Let’s take the two in reverse order.

Manufacturing has at very least stalled, and by some measures turned down to recessionary levels. Last week I discussed industrial production (not shown), which peaked in late 2022 and has continued to trend sideways to slightly negative right through February.

A very good harbinger with a record going back 75 years has been the ISM manufacturing index. Here’s its historical record through about 10 years ago (when FRED discontinued publishing it):

And here is its record for the past several years:

This index was frankly recessionary for almost all of last year. It is still negative, although not so much as before.

Two other metrics with lengthy records are the average hourly workweek in manufacturing (blue, right scale), which is one of the 10 “official” leading indicators, as well as real spending on durable goods (red, measured YoY for ease of comparison, left scale):

As a general rule, if real spending on durable goods turns negative YoY for more than an isolated month, a recession has started (with the peak in absolute terms coming before). Also, since employers generally cut hours before cutting jobs, a decline of about 0.8% of an hour in the average manufacturing workweek has typically preceded a recession - with the caveat in modern times that it must fall to at least roughly 40.5 hours:

The average manufacturing workweek has met the former criteria for the last 9 months, and the latter since November. By contrast, real spending on durable goods was up 0.7% YoY as of the last report for January, and in December had made an all-time record high.

But if some of the manufacturing data has met the historical criteria for a recession warning, it is important to note that manufacturing is less of US GDP than before the year 2000, and had been down more in 2015-16 without a recession occurring.

Further, housing construction has not meaningfully constricted at all. The below graph shows the leading metric of housing permits (another “official” component of the LEI, right scale), together with housing units under construction (gold, *1.2 for scale, right scale), and also real GDP q/q (red, left scale):

Housing permits declined -30% after the Fed began tightening, which has normally been enough to trigger a recession. *BUT* the actual measure of economic activity, housing units under construction, has barely turned down at all. In comparison to past downturns, where typically it had fallen at least 10%, and more often 20%, before a recession had begun, as of last month it was only 2% off peak!

The only other two occasions where housing permits declined comparably with no recession ensuing - 1966 and 1986 - real gross domestic product increased robustly. This was similarly the case in 2023.

An important reason is the other historical reason proppin up expansions: stimulative government spending. Here’s the historical record comparing fiscal surpluses vs. deficits:

Note the abrupt end of stimulative spending in 1937, normally thought to have been the prime driver of the steep 1938 recession. Note also the big “Great Society” stimulative spending in 1966-68, when a downturn was averted (indeed, although not shown in the first graph above, there was an inverted yield curve then as well). Needless to say, there as been a great deal of stimulative fiscal spending since 2020 as well.

Fed tightening typically works by constricting demand. Both government stimulus and the unkinking of supply chains work to stimulate supply.

All of which leads to the conclusion that, while manufacturing has reacted to the tightening, the *real* measure of construction activity has not, or not sufficiently to be recessionary.

Tomorrow housing permits, starts, and units under construction will all be updated. Unless there is a sharp decline in units under construction, there is no short term recession signal at all.

Confidential real estate information obtained by the Pittsburgh Post-Gazette estimates that 17 buildings are in “significant distress” and another nine are in “pending distress,” meaning they are either approaching foreclosure or at risk of foreclosure. Those properties represent 63% of the Downtown office stock and account for $30.5 million in real estate taxes, according to the data.

It also calculates the current office vacancy rate at 27% when subleases are factored in — one of the highest in the country.

And with an additional three million square feet of unoccupied leased space becoming available over the next five years, the vacancy rate could soar to 46% by 2028, based on the data.

Property assessments on 10 buildings, including U.S. Steel Tower, PPG Place, and the Tower at PNC Plaza, have been slashed by $364.4 million for the 2023 tax year, as high vacancies drive down their income.

Another factor has been the steep drop — to 63.5% from 87.5% — in the common level ratio, the number used to compute taxable value in county assessment appeal hearings.

The assessment cuts have the potential to cost the city, the county, and the Pittsburgh schools nearly $8.4 million in tax refunds for that year alone. Downtown represents nearly 25% of the city’s overall tax base.

In response Pittsburgh City Councilman Bobby Wilson wants to remove a $250,000 limit on the amount of tax relief available to a building owner or developer as long as a project creates at least 50 full-time equivalent jobs.

It’s unclear if the proposal will be enough. Annual interest costs to borrow $1 million have soared from $32,500 at the start of the pandemic in 2020 to $85,000 on March 1. Local construction costs have increased by about 30% since 2019.

But the city is doomed if it does nothing. Aaron Stauber, president of Rugby Realty said it will probably empty out Gulf Tower and mothball it once all existing leases expire.

“It’s cheaper to just shut the lights off,” he said. “At some point, we would move on to greener pastures.”

Where’s There’s Smoke There’s Unions

In addition to the commercial real estate woes, the city is also wrestling with union contracts.

It’s only March, and Pittsburgh’s 2024 house-of-cards operating budget is already falling down. That’s the clear implication of a letter sent by new City Controller Rachael Heisler to Mayor Ed Gainey and members of City Council on Wednesday afternoon.

The letter is a rare and welcome expression of urgency in a city government that has fallen in complacency — and is close to falling into fiscal disaster.

The approaching crisis was thrown into sharp relief this week, when City Council approved amendments to the operating budget accounting for a pricey new contract with the firefighters union. The Post-Gazette Editorial Board had predicted that this contract — plus two others yet to be announced and approved — would demonstrate the dishonesty of Mayor Ed Gainey’s budget, and that’s exactly what’s happening: The new contract is adding $11 million to the administration’s artificially low 5-year spending projections, bringing expected 2028 reserves to just barely the legal limit.

But there’s still two big contracts to go, with the EMS union and the Pittsburgh Joint Collective Bargaining Committee, which covers Public Works workers. Worse, there are tens — possibly hundreds — of millions in unrealistic revenues still on the books. On this, Ms. Heisler’s letter only scratched the surface.

Similarly, as we have observed, the budget’s real estate tax revenue projections are radically inconsistent with reality. Due to high vacancies and a sharp reduction in the common level ratio, a significant drop in revenues was predictable — but not reflected in the budget. Ms. Heisler’s estimate of a 20% drop in revenues from Downtown property, or $5.3 million a year, may even be optimistic: Other estimates peg the loss at twice that, or more.

Left unmentioned in the letter are massive property tax refunds the city will owe, as well as fanciful projections of interest income that are inconsistent with the dwindling reserves, and drawing-down of federal COVID relief funds, predicted in the budget itself. That’s another unrealistic $80 million over five years.

Pittsburgh exited Act 47 state oversight after nearly 15 years on Feb. 12, 2018, with a clean bill of fiscal health.

Pittsburgh’s tax structure was a much-complained-about topic leading up to the Act 47 declaration. The year following Pittsburgh’s designation as financially distressed under Act 47 it levied taxes on real estate, real estate transfers, parking, earned income, business gross receipts (business privilege and mercantile), occupational privilege and amusements. The General Assembly enacted tax reforms in 2004 giving the city authority to levy a payroll preparation tax in exchange for the immediate elimination of the mercantile tax and the phase out of the business privilege tax. The tax reforms increased the amount of the occupational privilege tax from $10 to $52 (this is today known as the local services tax and all municipalities outside of Philadelphia levy it and could raise it thanks to the change for Pittsburgh).

The coordinators recommended an increase in the deed transfer tax, which occurred in late 2004 (it was just increased again by City Council) and in the real estate tax, which increased in 2015.

Legacy costs, principally debt and underfunded pensions, were the primary focus of the 2009 amended recovery plan. The city’s pension funded ratio has increased significantly from where it stood a decade ago, rising from the mid-30 percent range to over 60 percent at last measurement.

The obvious question? Will the city stick to the steps taken to improve financially and avoid slipping back into distressed status? If Pittsburgh once stood “on the precipice of full-blown crisis,” as described in the first recovery plan, hopefully it won’t return to that position.

The Obvious Question

I could have answered the 2018 obvious question with the obvious answer. Hell no.

No matter how much you raise taxes, it will never be enough because public unions will suck every penny and want more.

On top of union graft, and insanely woke policies in California, we have an additional huge problem.

Hybrid Work Leaves Offices Empty and Building Owners Reeling

Hybrid work has put office building owners in a bind and could pose a risk to banks. Landlords are now confronting the fact that some of their office buildings have become obsolete, if not worthless.

Meanwhile, in Illinois …

Chicago Teachers’ Union Seeks $50 Billion Despite $700 Million City Deficit

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

{kind=link}

{kind=link}

{kind=link}