Uncategorized

Housing Market Tracker: Inventory drops as mortgage rates move higher

The housing market experienced more volatility last week, with housing inventory dropping as mortgage rates moved higher.

Share this:

The housing market experienced more volatility last week, with housing inventory dropping as mortgage rates moved higher.

Here is a quick rundown from last week:

- Purchase application data had a 3% week-to-week increase. The start of 2023 has been good, considering mortgage rates have stayed above 6% most of the time.

- Weekly housing inventory continues to decline, as we saw a decrease of 13,238 units, double the amount we had this time last year. However, we are working from a higher level in 2023.

- The 10-year yield jumped aggressively, continuing the decisive move from jobs Friday, and mortgage rates have moved from the recent lows of 5.99% back to 6.50%.

Purchase application data

We saw a weekly increase of 3% in purchase applications and the year-over-year data is improving, although it is still down 37% from last year. The extremely high comps that we had to deal with from October 2022 to January 2023 are coming to an end, which means that every month we should see the year-over-year declines move lower, even if the data just stay flat.

Last year, we had a historical dive in purchase application data, but recently we found a bottom and purchase apps have bounced from the lows. Since Nov. 9, when this data line started to get better, and excluding the traditional extreme slowdown the last and first week of the year, it’s been positive outside of one week. I am keeping an eye on how much growth we can get with mortgage rates over 6%.

This week, we will get a good test with the purchase application data as mortgage rates have risen recently. I am looking forward to seeing how the data reacts to higher rates. Unlike the COVID-19 recovery, which was fast and sharp, we are now dealing with a much different backdrop. Morgage rates are higher and we’re working from much higher home prices as well.

The one benefit of the housing market now is that days on the market are no longer teenagers, which means we are getting closer to a more balanced marketplace. This means buyers have more say now in the home-buying process. Finally, all the positive data we have seen since Nov. 9 looks forward 30-90 days, so the existing home sales will show better data coming up.

Weekly housing inventory

When I saw a slight increase in housing inventory in January, I got very excited because some of the demand collapse we saw in the second half of 2022 was from people choosing not to list their homes because of their fear of buying another. So, when I saw the slight inventory increase, I thought this was a good trend.

Before 2020, weekly housing inventory bottomed out in the January/February timeframe, and then the seasonal spring increase would start. From 2014 to 2016, housing inventory bottomed out in January. From 2017 to 2019, the inventory levels in January and February were very close to each other before the seasonal push higher.

However, since 2020, this hasn’t been the case — inventory has tended to bottom out a little later in the year. In 2021, inventory bottomed out in April, and in 2022 inventory bottomed out in March.

In the last two weeks, housing inventory has been declining significantly and I hope we are coming closer to the bottom of the seasonal inventory decline. Unfortunately, last week we saw a bigger decline in inventory than the previous week, as units fell by 13,238 according to Altos Research.

So I am crossing my fingers that we are getting closer to the end of the seasonal inventory decline because the last thing we want to see is bidding wars again, especially with demand working from much lower levels than what we saw in 2020/2021, and the early months of 2022. The positive aspect is that inventory is still higher than last year

- Weekly inventory change (Feb. 3-Feb. 10): Fell From 456,990 to 443,416

- Same week last year (Feb. 4-Feb. 11): Fell from 255,662 to 249,161

Because I could see that housing demographics were going to be good in the years 2020-2024, I really didn’t want to see inventory break to all-time lows during this period. This reality created my fear of home prices overheating, which they did, and once mortgage rates rose, the housing market took an extreme affordability hit. Last year, we had a historical dive in housing demand and didn’t get much inventory.

Unfortunately, we have a good shot of the next existing home sales report showing even lower inventory levels than the 970,000 level we are dealing with today. This means 2022 and 2023 are the only times in recent history where the NAR active listing data is under 1 million.

10-year yield and mortgage rates

In my 2023 forecast, if the economy stayed firm my 10-year yield range was between 3.21% and 4.25%, equating to mortgage rates staying in a range of 5.75% to 7.25%. For some time now, I have discussed how it would be hard to break under 3.42% with follow-through bond buying, meaning mortgage rates would fall further. The market made a few attempts to break that level, but now bond yields have reversed higher.

The question this week with the CPI report data being released, is whether we will see a W forming in this chart, which would mean bond yields head back to 4.25%, or whether the downtrend continues. Over time, the growth rate of inflation will cool down once rents get accounted for in a more real-time fashion.

Also, part of the 2023 forecast is that if the labor market breaks, the 10-year yield could get to 2.72%, which would mean mortgage rates in the low 5% range. And if the spreads get better, we could even have a 4-handle on mortgage rates. For now, though, the labor market is still solid.

The week ahead

This will be an exciting week for economic data, bonds and housing. First and most important, this week’s purchase application data is vital. It will be the first apps data amid a half a percentage move higher in mortgage rates, and the next few weeks will be critical, too, if rates stay at 6.50% or head higher. Remember, you should prioritize numbers over people; if the tracker data goes negative, you go with data rather than a personal belief.

The big move for rates should be the Consumer Price Index report this week. If it’s hotter than expected, we could see bonds act negatively to that report. Also, this week we have jobless claims, retail sales, Producer Price Index inflation, the homebuilders’ confidence survey, housing starts and the Leading Economic Index!

It’s going to be a busy week with economic data that can move the bond market and mortgage rates. One thing is certain from the data: mortgage rates heading lower, even to just 5.99%, shifted the housing market, which is something to remember as we go forward

Uncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

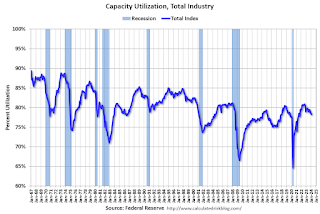

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Uncategorized

Southwest and United Airlines have bad news for passengers

Both airlines are facing the same problem, one that could lead to higher airfares and fewer flight options.

Share this:

{kind=link}

Airlines operate in a market that's dictated by supply and demand: If more people want to fly a specific route than there are available seats, then tickets on those flights cost more.

That makes scheduling and predicting demand a huge part of maximizing revenue for airlines. There are, however, numerous factors that go into how airlines decide which flights to put on the schedule.

Related: Major airline faces Chapter 11 bankruptcy concerns

Every airport has only a certain number of gates, flight slots and runway capacity, limiting carriers' flexibility. That's why during times of high demand — like flights to Las Vegas during Super Bowl week — do not usually translate to airlines sending more planes to and from that destination.

Airlines generally do try to add capacity every year. That's become challenging as Boeing has struggled to keep up with demand for new airplanes. If you can't add airplanes, you can't grow your business. That's caused problems for the entire industry.

Every airline retires planes each year. In general, those get replaced by newer, better models that offer more efficiency and, in most cases, better passenger amenities.

If an airline can't get the planes it had hoped to add to its fleet in a given year, it can face capacity problems. And it's a problem that both Southwest Airlines (LUV) and United Airlines have addressed in a way that's inevitable but bad for passengers.

Image source: Kevin Dietsch/Getty Images

Southwest slows down its pilot hiring

In 2023, Southwest made a huge push to hire pilots. The airline lost thousands of pilots to retirement during the covid pandemic and it needed to replace them in order to build back to its 2019 capacity.

The airline successfully did that but will not continue that trend in 2024.

"Southwest plans to hire approximately 350 pilots this year, and no new-hire classes are scheduled after this month," Travel Weekly reported. "Last year, Southwest hired 1,916 pilots, according to pilot recruitment advisory firm Future & Active Pilot Advisors. The airline hired 1,140 pilots in 2022."

The slowdown in hiring directly relates to the airline expecting to grow capacity only in the low-single-digits percent in 2024.

"Moving into 2024, there is continued uncertainty around the timing of expected Boeing deliveries and the certification of the Max 7 aircraft. Our fleet plans remain nimble and currently differs from our contractual order book with Boeing," Southwest Airlines Chief Financial Officer Tammy Romo said during the airline's fourth-quarter-earnings call.

"We are planning for 79 aircraft deliveries this year and expect to retire roughly 45 700 and 4 800, resulting in a net expected increase of 30 aircraft this year."

That's very modest growth, which should not be enough of an increase in capacity to lower prices in any significant way.

United Airlines pauses pilot hiring

Boeing's (BA) struggles have had wide impact across the industry. United Airlines has also said it was going to pause hiring new pilots through the end of May.

United (UAL) Fight Operations Vice President Marc Champion explained the situation in a memo to the airline's staff.

"As you know, United has hundreds of new planes on order, and while we remain on path to be the fastest-growing airline in the industry, we just won't grow as fast as we thought we would in 2024 due to continued delays at Boeing," he said.

"For example, we had contractual deliveries for 80 Max 10s this year alone, but those aircraft aren't even certified yet, and it's impossible to know when they will arrive."

That's another blow to consumers hoping that multiple major carriers would grow capacity, putting pressure on fares. Until Boeing can get back on track, it's unlikely that competition between the large airlines will lead to lower fares.

In fact, it's possible that consumer demand will grow more than airline capacity which could push prices higher.

Related: Veteran fund manager picks favorite stocks for 2024

bankruptcy pandemic stocks

Key shipping company files for Chapter 11 bankruptcy

Pharma industry reputation remains steady at a ‘new normal’ after Covid, Harris Poll finds

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Tight inventory and frustrated buyers challenge agents in Virginia

Part 1: Current State of the Housing Market; Overview for mid-March 2024

The Question You Should Ask Whenever You’re Wrong

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Key shipping company files Chapter 11 bankruptcy

The best real estate coaching programs for 2024

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment2 days ago

Spread & Containment2 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex