Uncategorized

HOME BANCORP, INC. ANNOUNCES 2023 FIRST QUARTER RESULTS AND DECLARES QUARTERLY DIVIDEND

HOME BANCORP, INC. ANNOUNCES 2023 FIRST QUARTER RESULTS AND DECLARES QUARTERLY DIVIDEND

PR Newswire

LAFAYETTE, La., April 18, 2023

LAFAYETTE, La., April 18, 2023 /PRNewswire/ — Home Bancorp, Inc. (Nasdaq: “HBCP”) (the “Company”), the parent compan…

Share this:

HOME BANCORP, INC. ANNOUNCES 2023 FIRST QUARTER RESULTS AND DECLARES QUARTERLY DIVIDEND

PR Newswire

LAFAYETTE, La., April 18, 2023

LAFAYETTE, La., April 18, 2023 /PRNewswire/ -- Home Bancorp, Inc. (Nasdaq: "HBCP") (the "Company"), the parent company for Home Bank, N.A. (the "Bank") (www.home24bank.com), reported financial results for the first quarter of 2023. For the quarter, the Company reported net income of $11.3 million, or $1.39 per diluted common share ("diluted EPS"), up $544,000 from $10.8 million, or $1.32 diluted EPS, for the fourth quarter of 2022.

"The headlines for the quarter focused on two well publicized bank failures which don't tell the whole story," said John W. Bordelon, President and Chief Executive Officer of the Company and the Bank. "Home Bancorp is well capitalized and has appropriate liquidity to meet our customer needs. We continue to attract outstanding commercial talent in various markets throughout our footprint while maintaining a strong credit discipline. Loan growth moderated in the first quarter of 2023 due in part to market volatility. Loans increased approximately 1.5% in 2023 resulting in a net loan growth, excluding PPP, for the seventh consecutive quarter. As we move forward in 2023, we remain committed to providing exceptional service to our new and existing customers. The Company is well positioned for the remainder of 2023."

First Quarter 2023 Highlights

- Loans totaled $2.5 billion at March 31, 2023, up $35.6 million, or 1.5%, or 6% annualized, from December 31, 2022.

- Net interest income totaled $31.6 million, down $1.7 million, or 5% from the prior quarter.

- The net interest margin ("NIM") decreased 20 basis points from 4.38% for the fourth quarter of 2022 to 4.18%.

- The Company recorded a $814,000 provision to the allowance for loan losses primarily due to loan growth.

- Nonperforming assets totaled $11.3 million, or 0.35% of total assets, up $336,000, or 3%, from $11.0 million, or 0.34% of total assets, at December 31, 2022 primarily due to one credit relationship being downgraded to substandard.

Loans

Loans totaled $2.5 billion at March 31, 2023, up $35.6 million, or 1%, from December 31, 2022. PPP loans, included in commercial and industrial loans, decreased $466,000, or 7%, from December 31, 2022. The following table summarizes the changes in the Company's loan portfolio, net of unearned income, from December 31, 2022 to March 31, 2023.

(dollars in thousands) | 3/31/2023 | 12/31/2022 | Increase (Decrease) | |||||

Real estate loans: | ||||||||

One- to four-family first mortgage | $ 405,638 | $ 389,616 | $ 16,022 | 4 % | ||||

Home equity loans and lines | 64,107 | 61,863 | 2,244 | 4 | ||||

Commercial real estate | 1,162,367 | 1,152,537 | 9,830 | 1 | ||||

Construction and land | 318,622 | 313,175 | 5,447 | 2 | ||||

Multi-family residential | 102,604 | 100,588 | 2,016 | 2 | ||||

Total real estate loans | 2,053,338 | 2,017,779 | 35,559 | 2 | ||||

Other loans: | ||||||||

Commercial and industrial | 379,119 | 377,894 | 1,225 | — | ||||

Consumer | 33,935 | 35,077 | (1,142) | (3) | ||||

Total other loans | 413,054 | 412,971 | 83 | — | ||||

Total loans | $ 2,466,392 | $ 2,430,750 | $ 35,642 | 1 % | ||||

The average loan yield was 5.67% for the first quarter of 2023, up 24 basis points from the fourth quarter of 2022. Loan growth during the first quarter of 2023 was across all loan types with the exception of consumer. One- to four-family first mortgage loan growth for the current quarter was primarily in our Acadiana, New Orleans and Southwest Louisiana markets. The growth in commercial real estate and construction loans was primarily within our Houston and Northshore markets.

Credit Quality and Allowance for Credit Losses

Nonperforming assets ("NPAs") totaled $11.3 million, or 0.35% of total assets, at March 31, 2023, up $336,000, or 3%, from $11.0 million, or 0.34% of total assets, at December 31, 2022. During the first quarter of 2023, the Company recorded net loan recoveries of $5,000, compared to net loan charge-offs of $39,000 during the fourth quarter of 2022.

The Company provisioned $814,000 to the allowance for loan losses in the first quarter of 2023. At March 31, 2023, the allowance for loan losses totaled $30.1 million, or 1.22% of total loans, compared to $29.3 million, or 1.21% of total loans, at December 31, 2022. Provisions to the allowance for loan losses are based upon, among other factors, our estimation of current expected losses in our loan portfolio, which we evaluate on a quarterly basis. Changes in expected losses consider various factors including the changing economic activity, potential mitigating effects of governmental stimulus, borrower specific information impacting changes in risk ratings, projected delinquencies and the impact of industry-wide loan modification efforts, among other factors.

The following tables present the Company's loan portfolio by credit quality classification as of March 31, 2023 and December 31, 2022.

March 31, 2023 | ||||||||

(dollars in thousands) | Pass | Special | Substandard | Total | ||||

One- to four-family first mortgage | $ 401,296 | $ 1,224 | $ 3,118 | $ 405,638 | ||||

Home equity loans and lines | 64,076 | — | 31 | 64,107 | ||||

Commercial real estate | 1,148,828 | 340 | 13,199 | 1,162,367 | ||||

Construction and land | 311,638 | 5,431 | 1,553 | 318,622 | ||||

Multi-family residential | 99,221 | — | 3,383 | 102,604 | ||||

Commercial and industrial | 374,364 | 2,783 | 1,972 | 379,119 | ||||

Consumer | 33,672 | — | 263 | 33,935 | ||||

Total | $ 2,433,095 | $ 9,778 | $ 23,519 | $ 2,466,392 | ||||

December 31, 2022 | ||||||||

(dollars in thousands) | Pass | Special | Substandard | Total | ||||

One- to four-family first mortgage | $ 385,199 | $ 1,194 | $ 3,223 | $ 389,616 | ||||

Home equity loans and lines | 61,830 | — | 33 | 61,863 | ||||

Commercial real estate | 1,138,584 | 524 | 13,429 | 1,152,537 | ||||

Construction and land | 312,008 | 520 | 647 | 313,175 | ||||

Multi-family residential | 97,202 | 3,312 | 74 | 100,588 | ||||

Commercial and industrial | 372,775 | 1,533 | 3,586 | 377,894 | ||||

Consumer | 34,543 | — | 534 | 35,077 | ||||

Total | $ 2,402,141 | $ 7,083 | $ 21,526 | $ 2,430,750 | ||||

Investment Securities

The Company's investment securities portfolio totaled $467.6 million at March 31, 2023, a decrease of $20.0 million, or 4% from December 31, 2022. During the first quarter 2023, the Company recorded a net loss of $249,000 related to the sale of available-for-sale investment securities totaling $14.0 million of securities. At March 31, 2023, the Company had a net unrealized loss position on its investment securities of $47.1 million, compared to a net unrealized loss of $54.8 million at December 31, 2022. The Company's investment securities portfolio had an effective duration of 4.5 years at March 31, 2023 and December 31, 2022.

The following table summarizes the composition of the Company's investment securities portfolio at March 31, 2023.

(dollars in thousands) | Amortized Cost | Fair Value | ||

Available for sale: | ||||

U.S. agency mortgage-backed | $ 341,049 | $ 307,381 | ||

Collateralized mortgage obligations | 88,800 | 84,887 | ||

Municipal bonds | 56,426 | 48,556 | ||

U.S. government agency | 20,301 | 19,322 | ||

Corporate bonds | 6,980 | 6,360 | ||

Total available for sale | $ 513,556 | $ 466,506 | ||

Held to maturity: | ||||

Municipal bonds | $ 1,070 | $ 1,069 | ||

Total held to maturity | $ 1,070 | $ 1,069 |

Approximately 38% of the investment securities portfolio was pledged as of March 31, 2023. As of March 31, 2023 and December 31, 2022, the Company had $146.5 million and $170.0 million, respectively, of securities pledged to secure public deposits.

Deposits

Total deposits were $2.6 billion at March 31, 2023, down $75.4 million, or 3%, from December 31, 2022. Non-maturity deposits decreased $111.9 million, or 5% during the first quarter of 2023 to $2.2 billion. The following table summarizes the changes in the Company's deposits from December 31, 2022 to March 31, 2023.

(dollars in thousands) | 3/31/2023 | 12/31/2022 | Increase (Decrease) | |||||

Demand deposits | $ 854,736 | $ 904,301 | $ (49,565) | (5) % | ||||

Savings | 288,788 | 305,871 | (17,083) | (6) | ||||

Money market | 384,809 | 423,990 | (39,181) | (9) | ||||

NOW | 657,499 | 663,574 | (6,075) | (1) | ||||

Certificates of deposit | 371,912 | 335,445 | 36,467 | 11 | ||||

Total deposits | $ 2,557,744 | $ 2,633,181 | $ (75,437) | (3) % | ||||

The average rate on interest-bearing deposits increased 33 basis points from 0.44% for the fourth quarter of 2022 to 0.77% for the first quarter of 2023. At March 31, 2023, certificates of deposit maturing within the next 12 months totaled $305.1 million.

We obtain most of our deposits from individuals, small businesses and public funds in our market areas. The following table presents our deposits per customer type for the periods indicated.

March 31, 2023 | December 31, 2022 | |||

Individuals | 51 % | 51 % | ||

Small businesses | 39 | 40 | ||

Public funds | 8 | 7 | ||

Broker | 2 | 2 | ||

Total | 100 % | 100 % | ||

The total amounts of our uninsured deposits (deposits in excess of $250,000, as calculated in accordance with FDIC regulations) were $778.0 million at March 31, 2023 and $830.9 million at December 31, 2022. Public funds in excess of the FDIC insurance limits are fully collateralized.

Net Interest Income

The net interest margin ("NIM") decreased 20 basis points from 4.38% for the fourth quarter of 2022 to 4.18% for the first quarter of 2023 primarily due to an increase in the average cost of interest-bearing liabilities, which was partially offset with an increase in the average yield on interest-earning assets. The increase in average cost of interest-bearing liabilities was primarily due to the higher costs on short-term FHLB borrowings and deposits in the first quarter of 2023.

The average loan yield was 5.67% for the first quarter of 2023, up 24 basis points from the fourth quarter of 2022 primarily reflecting increased market rates of interest on variable loans coupled with new loan originations at higher market rates during the period.

Average other interest-earning assets were $53.5 million for the first quarter of 2023, down $8.8 million, or 14%, from the fourth quarter of 2022 primarily due to a reallocation of certain other interest-earning assets to partially fund the increase in loans.

Unrecognized PPP lender fees totaled $84,000 at March 31, 2023. Loan accretion income from acquired loans totaled $668,000 for the first quarter of 2023, down $82,000, or 11% from the fourth quarter of 2022.

The following table summarizes the Company's average volume and rate of its interest-earning assets and interest-bearing liabilities for the periods indicated. Taxable equivalent ("TE") yields on investment securities have been calculated using a marginal tax rate of 21%.

Quarter Ended | ||||||||||||

3/31/2023 | 12/31/2022 | |||||||||||

(dollars in thousands) | Average | Interest | Average | Average | Interest | Average | ||||||

Interest-earning assets: | ||||||||||||

Loans receivable | $ 2,437,770 | $ 34,498 | 5.67 % | $ 2,374,065 | $ 32,826 | 5.43 % | ||||||

Investment securities (TE) | 535,195 | 3,142 | 2.38 | 549,961 | 3,214 | 2.37 | ||||||

Other interest-earning assets | 53,456 | 475 | 3.60 | 62,240 | 555 | 3.54 | ||||||

Total interest-earning assets | $ 3,026,421 | $ 38,115 | 5.05 % | $ 2,986,266 | $ 36,595 | 4.82 % | ||||||

Interest-bearing liabilities: | ||||||||||||

Deposits: | ||||||||||||

Savings, checking, and money market | $ 1,349,185 | $ 2,048 | 0.62 % | $ 1,431,577 | $ 1,463 | 0.41 % | ||||||

Certificates of deposit | 349,683 | 1,192 | 1.38 | 338,389 | 486 | 0.57 | ||||||

Total interest-bearing deposits | 1,698,868 | 3,240 | 0.77 | 1,769,966 | 1,949 | 0.44 | ||||||

Other borrowings | 5,539 | 53 | 3.89 | 5,539 | 53 | 3.80 | ||||||

Subordinated debt | 54,041 | 851 | 6.30 | 53,984 | 851 | 6.30 | ||||||

FHLB advances | 215,478 | 2,376 | 4.41 | 54,620 | 456 | 3.28 | ||||||

Total interest-bearing liabilities | $ 1,973,926 | $ 6,520 | 1.33 % | $ 1,884,109 | $ 3,309 | 0.70 % | ||||||

Net interest spread (TE) | 3.72 % | 4.12 % | ||||||||||

Net interest margin (TE) | 4.18 % | 4.38 % | ||||||||||

Noninterest Income

Noninterest income for the first quarter of 2023 totaled $3.3 million, down $28,000, or 1%, from the fourth quarter of 2022. The decrease was related primarily to a net loss on sale of securities totaling $249,000 during the first quarter of 2023, which was partially offset by an increase in bank card fees of $221,000 for the first quarter of 2023 compared to the fourth quarter of 2022.

Noninterest Expense

Noninterest expense for the first quarter of 2023 totaled $19.9 million, down $1.2 million, or 6%, from the fourth quarter of 2022. The decrease was primarily related to lower expenses in foreclosed assets ($769,000 primarily due to a recovery of a previous loss), compensation and benefits expense (down $441,000), marketing and advertising expenses (down $243,000) and franchise and shares tax expense (down $152,000), which were offset with an increase in provision for unfunded commitments.(up $380,000) during the first quarter of 2023.

Capital and Liquidity

At March 31, 2023, shareholders' equity totaled $345.1 million, up $15.1 million, or 5%, compared to $330.0 million at December 31, 2022. The increase was primarily due to the Company's earnings of $11.3 million in the quarter and a $5.5 million reduction in the accumulated other comprehensive loss on available for sale investment securities during the first quarter of 2023. The market value of the Company's available for sale securities at March 31, 2023 increased $7.7 million, or 14%, compared to $54.8 million at December 31, 2022. Preliminary Tier 1 leverage capital and total risk-based capital ratios were 10.69% and 14.00%, respectively, at March 31, 2023, compared to 10.43% and 13.63%, respectively, at December 31, 2022.

The following table summarizes the Company's primary and secondary sources of liquidity which were available at March 31, 2023.

(dollars in thousands) | March 31, 2023 | |

Cash and cash equivalents | $ 107,171 | |

Unpledged investment securities, amortized cost(1) | 352,077 | |

FHLB advance availability(1) | 913,921 | |

Amounts available from unsecured lines of credit | 55,000 | |

Federal Reserve discount window availability(1) | 500 | |

Total primary and secondary sources of available liquidity | $ 1,428,669 |

____________________ | |

(1) | Approximately $148.2 million of securities were moved in April 2023 from Federal Home Loan Bank to the Federal Reserve for future discount window availability at the Federal Reserve. |

Dividend and Share Repurchases

The Company announced that its Board of Directors declared a quarterly cash dividend on shares of its common stock of $0.25 per share payable on May 12, 2023, to shareholders of record as of May 1, 2023.

The Company repurchased 10,199 shares of its common stock during the first quarter of 2023 at an average price per share of $32.81. An additional 185,519 shares remain eligible for purchase under the 2021 Repurchase Plan. The book value per share and tangible book value per share of the Company's common stock was $41.66 and $31.09, respectively, at March 31, 2023.

Non-GAAP Reconciliation

This news release contains financial information determined by methods other than in accordance with generally accepted accounting principles ("GAAP"). The Company's management uses this non-GAAP financial information in its analysis of the Company's performance. In this news release, information is included which excludes intangible assets, PPP loans and certain acquisition related metrics. Management believes the presentation of this non-GAAP financial information provides useful information that is helpful to a full understanding of the Company's financial position and operating results. This non-GAAP financial information should not be viewed as a substitute for financial information determined in accordance with GAAP, nor is it necessarily comparable to non-GAAP financial information presented by other companies. A reconciliation on non-GAAP information included herein to GAAP is presented below.

Quarter Ended | ||||||

(dollars in thousands, except per share data) | 3/31/2023 | 12/31/2022 | 3/31/2022 | |||

Reported net income | $ 11,320 | $ 10,776 | $ 4,401 | |||

Add: Core deposit intangible amortization, net tax | 352 | 350 | 199 | |||

Non-GAAP tangible income | $ 11,672 | $ 11,126 | $ 4,600 | |||

Total assets | $ 3,266,970 | $ 3,228,280 | $ 3,332,228 | |||

Less: Intangible assets | 87,527 | 87,973 | 87,569 | |||

Non-GAAP tangible assets | $ 3,179,443 | $ 3,140,307 | $ 3,244,659 | |||

Total shareholders' equity | $ 345,100 | $ 329,954 | $ 337,504 | |||

Less: Intangible assets | 87,527 | 87,973 | 87,569 | |||

Non-GAAP tangible shareholders' equity | $ 257,573 | $ 241,981 | $ 249,935 | |||

Return on average equity | 13.53 % | 13.23 % | 5.08 % | |||

Add: Average intangible assets | 5.29 | 5.52 | 1.39 | |||

Non-GAAP return on average tangible common equity | 18.82 % | 18.75 % | 6.47 % | |||

Common equity ratio | 10.56 % | 10.22 % | 10.13 % | |||

Less: Intangible assets | 2.46 | 2.51 | 2.43 | |||

Non-GAAP tangible common equity ratio | 8.10 % | 7.71 % | 7.70 % | |||

Book value per share | $ 41.66 | $ 39.82 | $ 39.93 | |||

Less: Intangible assets | 10.57 | 10.62 | 10.36 | |||

Non-GAAP tangible book value per share | $ 31.09 | $ 29.20 | $ 29.57 | |||

This news release contains certain forward-looking statements. Forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. They often include the words "believe," "expect," "anticipate," "intend," "plan," "estimate" or words of similar meaning, or future or conditional verbs such as "will," "would," "should," "could" or "may."

Forward-looking statements, by their nature, are subject to risks and uncertainties. A number of factors - many of which are beyond our control - could cause actual conditions, events or results to differ significantly from those described in the forward-looking statements. Home Bancorp's Annual Report on Form 10-K for the year ended December 31, 2022 describes some of these factors, including risk elements in the loan portfolio, the level of the allowance for credit losses, the impact of the COVID-19 pandemic, risks of our growth strategy, geographic concentration of our business, dependence on our management team, risks of market rates of interest and of regulation on our business and risks of competition. Forward-looking statements speak only as of the date they are made. We do not undertake to update forward-looking statements to reflect circumstances or events that occur after the date the forward-looking statements are made or to reflect the occurrence of unanticipated events.

HOME BANCORP, INC. AND SUBSIDIARY | ||||||||

CONDENSED STATEMENTS OF FINANCIAL CONDITION | ||||||||

(Unaudited) | ||||||||

(dollars in thousands) | 3/31/2023 | 12/31/2022 | % | 3/31/2022 | ||||

Assets | ||||||||

Cash and cash equivalents | $ 107,171 | $ 87,401 | 23 % | $ 548,019 | ||||

Interest-bearing deposits in banks | 349 | 349 | — | 349 | ||||

Investment securities available for sale, at fair value | 466,506 | 486,518 | (4) | 415,260 | ||||

Investment securities held to maturity | 1,070 | 1,075 | — | 2,094 | ||||

Mortgage loans held for sale | 473 | 98 | 383 | 4,187 | ||||

Loans, net of unearned income | 2,466,392 | 2,430,750 | 1 | 2,157,969 | ||||

Allowance for loan losses | (30,118) | (29,299) | 3 | (26,731) | ||||

Total loans, net of allowance for loan losses | 2,436,274 | 2,401,451 | 1 | 2,131,238 | ||||

Office properties and equipment, net | 42,844 | 43,560 | (2) | 43,929 | ||||

Cash surrender value of bank-owned life insurance | 46,528 | 46,276 | 1 | 40,575 | ||||

Goodwill and core deposit intangibles | 87,527 | 87,973 | (1) | 87,569 | ||||

Accrued interest receivable and other assets | 78,228 | 73,579 | 6 | 59,008 | ||||

Total Assets | $ 3,266,970 | $ 3,228,280 | 1 | $ 3,332,228 | ||||

Liabilities | ||||||||

Deposits | $ 2,557,744 | $ 2,633,181 | (3) % | $ 2,941,179 | ||||

Other Borrowings | 5,539 | 5,539 | — | 5,539 | ||||

Subordinated debt, net of issuance cost | 54,073 | 54,013 | — | — | ||||

Federal Home Loan Bank advances | 276,727 | 176,213 | 57 | 25,671 | ||||

Accrued interest payable and other liabilities | 27,787 | 29,380 | (5) | 22,335 | ||||

Total Liabilities | 2,921,870 | 2,898,326 | 1 | 2,994,724 | ||||

Shareholders' Equity | ||||||||

Common stock | 83 | 83 | — | 85 | ||||

Additional paid-in capital | 165,470 | 164,942 | — | 164,830 | ||||

Common stock acquired by benefit plans | (1,969) | (2,060) | 4 | (2,332) | ||||

Retained earnings | 215,290 | 206,296 | 4 | 188,386 | ||||

Accumulated other comprehensive loss | (33,774) | (39,307) | 14 | (13,465) | ||||

Total Shareholders' Equity | 345,100 | 329,954 | 5 | 337,504 | ||||

Total Liabilities and Shareholders' Equity | $ 3,266,970 | $ 3,228,280 | 1 | $ 3,332,228 | ||||

HOME BANCORP, INC. AND SUBSIDIARY | ||||||||||

CONDENSED STATEMENTS OF INCOME | ||||||||||

(Unaudited) | ||||||||||

Quarter Ended | ||||||||||

(dollars in thousands, except per share data) | 3/31/2023 | 12/31/2022 | % | 3/31/2022 | % | |||||

Interest Income | ||||||||||

Loans, including fees | $ 34,498 | $ 32,826 | 5 % | $ 22,671 | 52 % | |||||

Investment securities | 3,142 | 3,214 | (2) | 1,618 | 94 | |||||

Other investments and deposits | 475 | 555 | (14) | 277 | 71 | |||||

Total interest income | 38,115 | 36,595 | 4 | 24,566 | 55 | |||||

Interest Expense | ||||||||||

Deposits | 3,240 | 1,949 | 66 % | 893 | 263 % | |||||

Other borrowings | 53 | 53 | — | 53 | — | |||||

Subordinated debt expense | 851 | 851 | — | — | — | |||||

Federal Home Loan Bank advances | 2,376 | 456 | 421 | 109 | 2080 | |||||

Total interest expense | 6,520 | 3,309 | 97 | 1,055 | 518 | |||||

Net interest income | 31,595 | 33,286 | (5) | 23,511 | 34 | |||||

Provision for loan losses | 814 | 1,987 | (59) | 3,215 | (75) | |||||

Net interest income after provision for loan losses | 30,781 | 31,299 | (2) | 20,296 | 52 | |||||

Noninterest Income | ||||||||||

Service fees and charges | 1,250 | 1,198 | 4 % | 1,165 | 7 % | |||||

Bank card fees | 1,787 | 1,566 | 14 | 1,454 | 23 | |||||

Gain on sale of loans, net | 57 | 22 | 159 | 299 | (81) | |||||

Income from bank-owned life insurance | 253 | 257 | (2) | 214 | 18 | |||||

Loss on sale of securities, net | (249) | — | — | — | — | |||||

(Loss) gain on sale of assets, net | (17) | 9 | (289) | 5 | (440) | |||||

Other income | 230 | 287 | (20) | 249 | (8) | |||||

Total noninterest income | 3,311 | 3,339 | (1) | 3,386 | (2) | |||||

Noninterest Expense | ||||||||||

Compensation and benefits | 12,439 | 12,880 | (3) % | 10,159 | 22 % | |||||

Occupancy | 2,350 | 2,261 | 4 | 1,803 | 30 | |||||

Marketing and advertising | 307 | 550 | (44) | 407 | (25) | |||||

Data processing and communication | 2,321 | 2,295 | 1 | 2,195 | 6 | |||||

Professional fees | 364 | 392 | (7) | 542 | (33) | |||||

Forms, printing and supplies | 187 | 182 | 3 | 146 | 28 | |||||

Franchise and shares tax | 541 | 693 | (22) | 391 | 38 | |||||

Regulatory fees | 539 | 511 | 5 | 446 | 21 | |||||

Foreclosed assets, net | (739) | 30 | (2563) | 402 | (284) | |||||

Amortization of acquisition intangible | 446 | 443 | 1 | 252 | 77 | |||||

Provision for credit losses on unfunded commitments | 210 | (170) | 224 | 302 | (30) | |||||

Other expenses | 975 | 1,114 | (12) | 1,195 | (18) | |||||

Total noninterest expense | 19,940 | 21,181 | (6) | 18,240 | 9 | |||||

Income before income tax expense | 14,152 | 13,457 | 5 | 5,442 | 160 | |||||

Income tax expense | 2,832 | 2,681 | 6 | 1,041 | 172 | |||||

Net income | $ 11,320 | $ 10,776 | 5 | $ 4,401 | 157 | |||||

Earnings per share - basic | $ 1.40 | $ 1.33 | 5 % | $ 0.53 | 164 % | |||||

Earnings per share - diluted | $ 1.39 | $ 1.32 | 5 % | $ 0.53 | 162 % | |||||

Cash dividends declared per common share | $ 0.25 | $ 0.24 | 4 % | $ 0.23 | 9 % | |||||

HOME BANCORP, INC. AND SUBSIDIARY | ||||||||||

SUMMARY FINANCIAL INFORMATION | ||||||||||

(Unaudited) | ||||||||||

Quarter Ended | ||||||||||

(dollars in thousands, except per share data) | 3/31/2023 | 12/31/2022 | % Change | 3/31/2022 | % Change | |||||

EARNINGS DATA | ||||||||||

Total interest income | $ 38,115 | $ 36,595 | 4 % | $ 24,566 | 55 % | |||||

Total interest expense | 6,520 | 3,309 | 97 | 1,055 | 518 | |||||

Net interest income | 31,595 | 33,286 | (5) | 23,511 | 34 | |||||

Provision for loan losses | 814 | 1,987 | (59) | 3,215 | (75) | |||||

Total noninterest income | 3,311 | 3,339 | (1) | 3,386 | (2) | |||||

Total noninterest expense | 19,940 | 21,181 | (6) | 18,240 | 9 | |||||

Income tax expense | 2,832 | 2,681 | 6 | 1,041 | 172 | |||||

Net income | $ 11,320 | $ 10,776 | 5 | $ 4,401 | 157 | |||||

AVERAGE BALANCE SHEET DATA | ||||||||||

Total assets | $ 3,219,856 | $ 3,173,676 | 1 % | $ 2,977,559 | 8 % | |||||

Total interest-earning assets | 3,026,421 | 2,986,266 | 1 | 2,783,614 | 9 | |||||

Total loans | 2,437,770 | 2,374,065 | 3 | 1,862,616 | 31 | |||||

PPP loans | 6,386 | 6,883 | (7) | 31,326 | (80) | |||||

Total interest-bearing deposits | 1,698,868 | 1,769,966 | (4) | 1,779,832 | (5) | |||||

Total interest-bearing liabilities | 1,973,926 | 1,884,109 | 5 | 1,811,166 | 9 | |||||

Total deposits | 2,578,369 | 2,707,823 | (5) | 2,576,378 | — | |||||

Total shareholders' equity | 339,311 | 323,102 | 5 | 351,337 | (3) | |||||

PER SHARE DATA | ||||||||||

Earnings per share - basic | $ 1.40 | $ 1.33 | 5 % | $ 0.53 | 164 % | |||||

Earnings per share - diluted | 1.39 | 1.32 | 5 | 0.53 | 162 | |||||

Book value at period end | 41.66 | 39.82 | 5 | 39.93 | 4 | |||||

Tangible book value at period end | 31.09 | 29.20 | 6 | 29.57 | 5 | |||||

Shares outstanding at period end | 8,284,130 | 8,286,084 | — | 8,453,014 | (2) | |||||

Weighted average shares outstanding | ||||||||||

Basic | 8,087,524 | 8,070,734 | — % | 8,270,209 | (2) % | |||||

Diluted | 8,136,583 | 8,119,481 | — | 8,336,561 | (2) | |||||

SELECTED RATIOS (1) | ||||||||||

Return on average assets | 1.43 % | 1.35 % | 6 % | 0.60 % | 138 % | |||||

Return on average equity | 13.53 | 13.23 | 2 | 5.08 | 166 | |||||

Common equity ratio | 10.56 | 10.22 | 3 | 10.13 | 4 | |||||

Efficiency ratio (2) | 57.12 | 57.83 | (1) | 67.81 | (16) | |||||

Average equity to average assets | 10.54 | 10.18 | 4 | 11.80 | (11) | |||||

Tier 1 leverage capital ratio (3) | 10.69 | 10.43 | 2 | 8.67 | 23 | |||||

Total risk-based capital ratio (3) | 14.00 | 13.63 | 3 | 12.28 | 14 | |||||

Net interest margin (4) | 4.18 | 4.38 | (5) | 3.39 | 23 | |||||

SELECTED NON-GAAP RATIOS (1) | ||||||||||

Tangible common equity ratio (5) | 8.10 % | 7.71 % | 5 % | 7.70 % | 5 % | |||||

Return on average tangible common equity (6) | 18.82 | 18.75 | — | 6.47 | 191 | |||||

(1) | With the exception of end-of-period ratios, all ratios are based on average daily balances during the respective periods. |

(2) | The efficiency ratio represents noninterest expense as a percentage of total revenues. Total revenues is the sum of net interest income and noninterest income. |

(3) | Capital ratios are preliminary end-of-period ratios for the Bank only and are subject to change. |

(4) | Net interest margin represents net interest income as a percentage of average interest-earning assets. Taxable equivalent yields are calculated using a marginal tax rate of 21%. |

(5) | Tangible common equity ratio is common shareholders' equity less intangible assets divided by total assets less intangible assets. See "Non-GAAP Reconciliation" for additional information. |

(6) | Return on average tangible common equity is net income plus amortization of core deposit intangible, net of taxes, divided by average common shareholders' equity less average intangible assets. See "Non-GAAP Reconciliation" for additional information. |

HOME BANCORP, INC. AND SUBSIDIARY | ||||||||||||||||||

SUMMARY CREDIT QUALITY INFORMATION | ||||||||||||||||||

(Unaudited) | ||||||||||||||||||

3/31/2023 | 12/31/2022 | 3/31/2022 | ||||||||||||||||

(dollars in thousands) | Originated | Acquired | Total | Originated | Acquired | Total | Originated | Acquired | Total | |||||||||

CREDIT QUALITY (1) | ||||||||||||||||||

Nonaccrual loans(2) | $ 5,546 | $ 5,686 | $ 11,232 | $ 4,336 | $ 6,177 | $ 10,513 | $ 5,515 | $ 15,598 | $ 21,113 | |||||||||

Accruing loans 90 days or more past | — | — | — | 2 | — | 2 | — | — | — | |||||||||

Total nonperforming loans | 5,546 | 5,686 | 11,232 | 4,338 | 6,177 | 10,515 | 5,515 | 15,598 | 21,113 | |||||||||

Foreclosed assets and ORE | — | 80 | 80 | 151 | 310 | 461 | 536 | 729 | 1,265 | |||||||||

Total nonperforming assets | 5,546 | 5,766 | 11,312 | 4,489 | 6,487 | 10,976 | 6,051 | 16,327 | 22,378 | |||||||||

Performing troubled debt restructurings | 4,230 | 1,583 | 5,813 | 4,600 | 1,605 | 6,205 | 3,797 | 1,100 | 4,897 | |||||||||

Total nonperforming assets and | $ 9,776 | $ 7,349 | $ 17,125 | $ 9,089 | $ 8,092 | $ 17,181 | $ 9,848 | $ 17,427 | $ 27,275 | |||||||||

Nonperforming assets to total assets | 0.35 % | 0.34 % | 0.67 % | |||||||||||||||

Nonperforming loans to total assets | 0.34 | 0.33 | 0.63 | |||||||||||||||

Nonperforming loans to total loans | 0.46 | 0.43 | 0.98 | |||||||||||||||

(1) | It is our policy to cease accruing interest on loans 90 days or more past due, with certain limited exceptions. Nonperforming assets consist of nonperforming loans, foreclosed assets and surplus real estate (ORE). Foreclosed assets consist of assets acquired through foreclosure or acceptance of title in-lieu of foreclosure. ORE consists of closed or unused bank buildings. |

(2) | Nonaccrual loans include originated restructured loans placed on nonaccrual totaling $3.0 million, $3.1 million and $3.6 million at March 31, 2023, December 31, 2022 and March 31, 2022, respectively. Acquired restructured loans placed on nonaccrual totaled $3.2 million, $3.7 million and $3.0 million at March 31, 2023, December 31, 2022 and March 31, 2022, respectively. |

HOME BANCORP, INC. AND SUBSIDIARY | ||||||||||||||||||

SUMMARY CREDIT QUALITY INFORMATION - CONTINUED | ||||||||||||||||||

(Unaudited) | ||||||||||||||||||

3/31/2023 | 12/31/2022 | 3/31/2022 | ||||||||||||||||

Collectively | Individually | Total | Collectively | Individually | Total | Collectively | Individually | Total | ||||||||||

ALLOWANCE FOR CREDIT | ||||||||||||||||||

One- to four-family first mortgage | $ 3,356 | $ — | $ 3,356 | $ 2,883 | $ — | $ 2,883 | $ 2,056 | $ — | $ 2,056 | |||||||||

Home equity loans and lines | 753 | — | 753 | 624 | — | 624 | 539 | — | 539 | |||||||||

Commercial real estate | 13,344 | 450 | 13,794 | 13,264 | 550 | 13,814 | 12,878 | 2,324 | 15,202 | |||||||||

Construction and land | 4,921 | — | 4,921 | 4,680 | — | 4,680 | 4,112 | — | 4,112 | |||||||||

Multi-family residential | 608 | — | 608 | 572 | — | 572 | 554 | — | 554 | |||||||||

Commercial and industrial | 5,831 | 143 | 5,974 | 5,853 | 171 | 6,024 | 3,200 | 440 | 3,640 | |||||||||

Consumer | 712 | — | 712 | 702 | — | 702 | 628 | — | 628 | |||||||||

Total allowance for credit losses | $ 29,525 | $ 593 | $ 30,118 | $ 28,578 | $ 721 | $ 29,299 | $ 23,967 | $ 2,764 | $ 26,731 | |||||||||

Unfunded lending commitments(3) | 2,303 | — | 2,303 | 2,093 | — | 2,093 | 2,117 | — | 2,117 | |||||||||

Total allowance for credit losses | $ 31,828 | $ 593 | $ 32,421 | $ 30,671 | $ 721 | $ 31,392 | $ 26,084 | $ 2,764 | $ 28,848 | |||||||||

Allowance for loan losses to | 266.25 % | 266.94 % | 119.45 % | |||||||||||||||

Allowance for loan losses to | 268.14 % | 278.64 % | 126.61 % | |||||||||||||||

Allowance for loan losses to total | 1.22 % | 1.21 % | 1.24 % | |||||||||||||||

Allowance for credit losses to total | 1.31 % | 1.29 % | 1.34 % | |||||||||||||||

Year-to-date loan charge-offs | $ 93 | $ 1,398 | $ 316 | |||||||||||||||

Year-to-date loan recoveries | 98 | 704 | 465 | |||||||||||||||

Year-to-date net loan recoveries | $ 5 | $ (694) | $ 149 | |||||||||||||||

Annualized YTD net loan recoveries | — % | (0.03) % | 0.03 % | |||||||||||||||

(3) | The allowance for unfunded lending commitments is recorded within accrued interest payable and other liabilities on the Consolidated Statements of Financial Condition. |

View original content to download multimedia:https://www.prnewswire.com/news-releases/home-bancorp-inc-announces-2023-first-quarter-results-and-declares-quarterly-dividend-301799616.html

SOURCE Home Bancorp, Inc.

Uncategorized

One city held a mass passport-getting event

A New Orleans congressman organized a way for people to apply for their passports en masse.

Share this:

While the number of Americans who do not have a passport has dropped steadily from more than 80% in 1990 to just over 50% now, a lack of knowledge around passport requirements still keeps a significant portion of the population away from international travel.

Over the four years that passed since the start of covid-19, passport offices have also been dealing with significant backlog due to the high numbers of people who were looking to get a passport post-pandemic.

Related: Here is why it is (still) taking forever to get a passport

To deal with these concurrent issues, the U.S. State Department recently held a mass passport-getting event in the city of New Orleans. Called the "Passport Acceptance Event," the gathering was held at a local auditorium and invited residents of Louisiana’s 2nd Congressional District to complete a passport application on-site with the help of staff and government workers.

'Come apply for your passport, no appointment is required'

"Hey #LA02," Rep. Troy A. Carter Sr. (D-LA), whose office co-hosted the event alongside the city of New Orleans, wrote to his followers on Instagram (META) . "My office is providing passport services at our #PassportAcceptance event. Come apply for your passport, no appointment is required."

More Travel:

- A new travel term is taking over the internet (and reaching airlines and hotels)

- The 10 best airline stocks to buy now

- Airlines see a new kind of traveler at the front of the plane

The event was held on March 14 from 10 a.m. to 1 p.m. While it was designed for those who are already eligible for U.S. citizenship rather than as a way to help non-citizens with immigration questions, it helped those completing the application for the first time fill out forms and make sure they have the photographs and identity documents they need. The passport offices in New Orleans where one would normally have to bring already-completed forms have also been dealing with lines and would require one to book spots weeks in advance.

These are the countries with the highest-ranking passports in 2024

According to Carter Sr.'s communications team, those who submitted their passport application at the event also received expedited processing of two to three weeks (according to the State Department's website, times for regular processing are currently six to eight weeks).

While Carter Sr.'s office has not released the numbers of people who applied for a passport on March 14, photos from the event show that many took advantage of the opportunity to apply for a passport in a group setting and get expedited processing.

Every couple of months, a new ranking agency puts together a list of the most and least powerful passports in the world based on factors such as visa-free travel and opportunities for cross-border business.

In January, global citizenship and financial advisory firm Arton Capital identified United Arab Emirates as having the most powerful passport in 2024. While the United States topped the list of one such ranking in 2014, worsening relations with a number of countries as well as stricter immigration rules even as other countries have taken strides to create opportunities for investors and digital nomads caused the American passport to slip in recent years.

A UAE passport grants holders visa-free or visa-on-arrival access to 180 of the world’s 198 countries (this calculation includes disputed territories such as Kosovo and Western Sahara) while Americans currently have the same access to 151 countries.

stocks pandemic covid-19 grantsUncategorized

Fast-food chain closes restaurants after Chapter 11 bankruptcy

Several major fast-food chains recently have struggled to keep restaurants open.

Share this:

Competition in the fast-food space has been brutal as operators deal with inflation, consumers who are worried about the economy and their jobs and, in recent months, the falling cost of eating at home.

Add in that many fast-food chains took on more debt during the covid pandemic and that labor costs are rising, and you have a perfect storm of problems.

It's a situation where Restaurant Brands International (QSR) has suffered as much as any company.

Related: Wendy's menu drops a fan favorite item, adds something new

Three major Burger King franchise operators filed for bankruptcy in 2023, and the chain saw hundreds of stores close. It also saw multiple Popeyes franchisees move into bankruptcy, with dozens of locations closing.

RBI also stepped in and purchased one of its key franchisees.

"Carrols is the largest Burger King franchisee in the United States today, operating 1,022 Burger King restaurants in 23 states that generated approximately $1.8 billion of system sales during the 12 months ended Sept. 30, 2023," RBI said in a news release. Carrols also owns and operates 60 Popeyes restaurants in six states."

The multichain company made the move after two of its large franchisees, Premier Kings and Meridian, saw multiple locations not purchased when they reached auction after Chapter 11 bankruptcy filings. In that case, RBI bought select locations but allowed others to close.

Image source: Chen Jianli/Xinhua via Getty

Another fast-food chain faces bankruptcy problems

Bojangles may not be as big a name as Burger King or Popeye's, but it's a popular chain with more than 800 restaurants in eight states.

"Bojangles is a Carolina-born restaurant chain specializing in craveable Southern chicken, biscuits and tea made fresh daily from real recipes, and with a friendly smile," the chain says on its website. "Founded in 1977 as a single location in Charlotte, our beloved brand continues to grow nationwide."

Like RBI, Bojangles uses a franchise model, which makes it dependent on the financial health of its operators. The company ultimately saw all its Maryland locations close due to the financial situation of one of its franchisees.

Unlike. RBI, Bojangles is not public — it was taken private by Durational Capital Management LP and Jordan Co. in 2018 — which means the company does not disclose its financial information to the public.

That makes it hard to know whether overall softness for the brand contributed to the chain seeing its five Maryland locations after a Chapter 11 bankruptcy filing.

Bojangles has a messy bankruptcy situation

Even though the locations still appear on the Bojangles website, they have been shuttered since late 2023. The locations were operated by Salim Kakakhail and Yavir Akbar Durranni. The partners operated under a variety of LLCs, including ABS Network, according to local news channel WUSA9.

The station reported that the owners face a state investigation over complaints of wage theft and fraudulent W2s. In November Durranni and ABS Network filed for bankruptcy in New Jersey, WUSA9 reported.

"Not only do former employees say these men owe them money, WUSA9 learned the former owners owe the state, too, and have over $69,000 in back property taxes."

Former employees also say that the restaurant would regularly purchase fried chicken from Popeyes and Safeway when it ran out in their stores, the station reported.

Bojangles sent the station a comment on the situation.

"The franchisee is no longer in the Bojangles system," the company said. "However, it is important to note in your coverage that franchisees are independent business owners who are licensed to operate a brand but have autonomy over many aspects of their business, including hiring employees and payroll responsibilities."

Kakakhail and Durranni did not respond to multiple requests for comment from WUSA9.

bankruptcy pandemicUncategorized

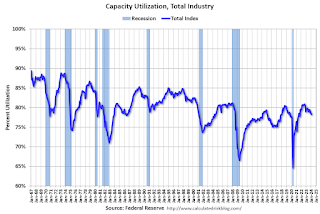

Industrial Production Increased 0.1% in February

From the Fed: Industrial Production and Capacity Utilization

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 p…

Share this:

Industrial production edged up 0.1 percent in February after declining 0.5 percent in January. In February, the output of manufacturing rose 0.8 percent and the index for mining climbed 2.2 percent. Both gains partly reflected recoveries from weather-related declines in January. The index for utilities fell 7.5 percent in February because of warmer-than-typical temperatures. At 102.3 percent of its 2017 average, total industrial production in February was 0.2 percent below its year-earlier level. Capacity utilization for the industrial sector remained at 78.3 percent in February, a rate that is 1.3 percentage points below its long-run (1972–2023) average.Click on graph for larger image.

emphasis added

{kind=link}

This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.3% is 1.3% below the average from 1972 to 2022. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 102.3. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Key shipping company files for Chapter 11 bankruptcy

These Cities Have The Highest (And Lowest) Share Of Unaffordable Neighborhoods In 2024

Tight inventory and frustrated buyers challenge agents in Virginia

The Question You Should Ask Whenever You’re Wrong

Walmart and Target make key self-checkout changes to fight theft

Industrial Production Increased 0.1% in February

Your financial plan may be riskier without bitcoin

Key shipping company files Chapter 11 bankruptcy

One city held a mass passport-getting event

Futures Rise To New Record High Ahead Of Data Deluge

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

International1 week ago

International1 week agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoIndustrial Production Decreased 0.1% in January

-

International1 week ago

International1 week agoWalmart launches clever answer to Target’s new membership program

-

Spread & Containment3 days ago

Spread & Containment3 days agoIFM’s Hat Trick and Reflections On Option-To-Buy M&A

-

Uncategorized4 weeks ago

Uncategorized4 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex