Uncategorized

Futures Unchanged After Another Boring Overnight Session

Futures Unchanged After Another Boring Overnight Session

For the third day in a row, futures have gone nowhere in the overnight session, and…

Share this:

For the third day in a row, futures have gone nowhere in the overnight session, and are flat as a pancake with yields also barely changed and holding on to their sharp move higher from the previous day when they surged 14bps; the USD was down, commodities are mixed with oil outperforming again, and crypto and gold staged a modest rebound. At 8:00am ET, emini S&P futures were unchanged at 4,275 while Nasdaq futs were just fractionally in the green after the index yesterday posted its worst decline since April; concern that central banks will keep driving interest rates higher sent tech stocks in Europe to one of the worst performances among industries, with ASML Holding NV as the biggest drag on the Stoxx 600.

In premarket trading, GameStop plunged 18% after firing its chief executive and reporting sales that fell short of estimates. Manchester United is set to extend gains, after rising as much as 5.6% in premarket trading, as Qatar’s Sheikh Jassim submitted his fifth takeover offer for Premier League team. Here are some other notable premarket movers:

- Smartsheet shares fell as much as 18% in premarket trading, after the software company reported its first-quarter results and gave an outlook. Analysts noted a weaker-than-expected billings forecast as a potential point of concern. If losses hold, Smartsheet will be set for its biggest fall since Sept. 3, 2020.

- HashiCorp falls 23% after the infrastructure software company cut its full-year revenue forecast. Despite the beats in the first quarter, analysts were focused on the reduced guidance for FY24, with Piper Sandler saying it raises questions on sales execution issues.

- Rent the Runway shares fall as much as 11% in premarket trading after the clothing rental company gave a weaker-than-expected second-quarter sales outlook, hurt by a reduction in promotions to attract subscribers. The firm confirmed full-year guidance but stressed that its target hinges on a sales recovery in the second half, making the stock a “show-me story” amid macro uncertainties, according to Wells Fargo.

- Semtech shares soar as much as 29% in premarket trading after the semiconductor and internet-of-things company eked out positive 1Q earnings thanks to cost controls. Outgoing CEO Mohan Maheswaran said during a conference call that core operations probably have found a bottom in the previous quarter, with 2Q set for an improvement. Analysts say a strategy update by the new CEO Paul Pickle could serve as a key catalyst for the stock.

- Trip.com shares advance over 4% in premarket trading after the online travel agent reported first-quarter revenue that beat estimates. Analysts said the results were solid, noting that revenue was above pre-pandemic levels.

- Privia Health and eXp World Holdings (EXPI US) jumped in postmarket trading after S&P Dow Jones Indices said they would replace Heska and Ruth’s Hospitality Group in the S&P SmallCap 600 Index.

- Signet Jewelers tumbles 9% after slashing its fiscal year projections for sales and profit, citing slowing trends, including a softer-than-expected Mother’s Day.

- Torrid Holdings slumps 11% after cutting its full-year projections for net sales and adjusted Ebitda. Telsey Advisory Group downgrades the apparel retailer to market perform from outperform, also citing weaker-than-expected sales and gross margin in the fiscal first quarter.

- Clothing company Oxford Industries tumbles 7% postmarket after the owner of the Tommy Bahama brand cut its profit and sales guidance for the full year

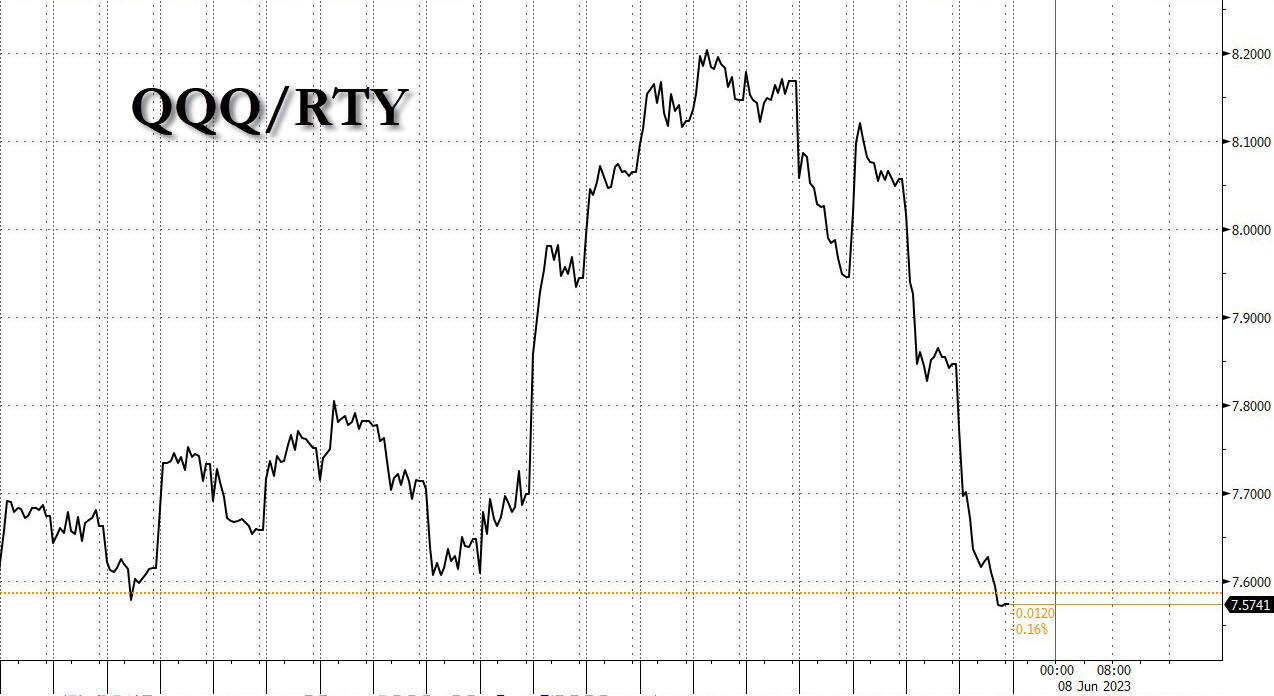

Yesterday, Russell 2000 was the clear standout as the +RTY/-NDX had another 3-sigma move (as discussed here), retracing the move since May 10.

Technology stocks, the most rate sensitive of all equities, have been feeling the pinch as investors consider the possibility that the Fed isn’t finished with its own tightening. Two major central banks this week — the Bank of Canada and the Reserve Bank of Australia — unexpectedly raised rates to bring inflation under control. Sure enough, the US yield curve reacted to the surprise Bank of Canada rate hike; the hike comes after skipping 2 meetings. The bond market is pricing ~80% chance of a 25bps hike by the July 26 meeting. Yields on two-year US Treasuries are hovering near 4.5%, the highest since March, although well below the 5.07% seen before banking turmoil gripped markets back then.

“The key thing to remember is that the fight against inflation isn’t over,” Helen Jewell, EMEA deputy CIO of BlackRock Fundamental Equities, said in an interview with Bloomberg Television. “We’re seeing the stickiness in inflation and concerns coming through from a rate hike perspective.”

Megacap tech companies have powered the S&P 500 to the brink of a bull market, before rate worries prompted Wednesday’s pullback. Policy decisions are due from the Fed and the ECB next week, with the Fed signaling it may pause rate hikes in June before resuming them later. The big question facing markets right now is whether the Fed decides to raise rates next Wednesday or holds after 10 straight increases, Deutsche Bank AG strategists including Jim Reid wrote in a note. Traders have boosted wagers on Fed rate increases, with swaps close to pricing in a quarter-point hike for the July meeting.

“While we still expect the Fed to skip the June meeting, this week’s policy decision which expressed more concern over persistent inflation risks makes us more wary,” said Lee Hardman, a strategist at MUFG Bank. “The hawkish policy updates from the RBA and BOC have injected fresh upward momentum into global yields.”

European tech stocks underperformed on concerns over the potential for central banks to keep raising interest rates. Stoxx 600 is steady with autos and banks outperforming. FTSE MIB outperforms peers, adding 0.7%; FTSE 100 lags, dropping 0.2%. Here are the most notable movers today:

- Evotec jumps as much as 9.1% after the German biotech was upgraded to buy by Citi, which also hiked its price target on the stock, calling it the “Tesla of biologics manufacturing”

- Orsted jumps as much as 6.3% as the lack of need for additional equity provides relief for the stock, according to Citi. The firm said late Wednesday it’s on track to outperform previous financial targets

- Wizz Air gains as much as 5.4% in London after the low-cost airline forecast net income for FY24 that exceeded estimates, with analysts saying the outlook outweighs the weaker FY23 figures

- Europe’s Stoxx 600 basic resources and energy subsectors led gains in the broader benchmark on Thursday as iron ore rises for a seventh day, on signs of Chinese government efforts to revive the economy

- Lottomatica gains as much as 5.1% after the gambling company was initiated with buy-equivalent ratings at six brokers, following its May 3 IPO. Analysts note the company’s leading position in Italy

- Clarkson rises as much as 5.9% after J.P. Morgan analyst Sam Bland raised the recommendation on the shipping company to overweight from neutral saying it’s heading in the right direction

- FirstGroup shares soar as much as 21% after the British transport company reported full-year revenue that beat estimates. Analysts noted the strength in the company’s bus margins

- RWS Holdings shares jump as much as 13% after the patent translations company gave a half-year update and said that it expects to see growth accelerate in the second half of the year

- Just Eat Takeaway shares drop as much as 3.7%, the worst performer in the Stoxx 600 Technology Index, after Bryan Garnier cut its rating to sell amid declines in market share and customer orders

- SBB falls as much as 12% after the beleaguered Swedish landlord saw its credit rating downgraded in two steps to BB- from BB+ by S&P Global Rating, pulling it deeper into junk territory

Earlier in the session, Asian shares ticked lower as investors boost bets that the Federal Reserve may continue to raise interest rates and keep them at elevated levels for longer, while the yen strengthened after data showing Japan’s economy grew faster than expected in the first quarter. The MSCI Asia Pacific Index dropped as much as 0.8%, dragged by info tech and communication services shares. Tech stocks including TSMC, Tencent and Samsung Electronics were among the biggest contributors to the gauge’s decline. Most markets in the region traded lower with Taiwan being the worst performer. Benchmarks in the region dropped for a second day after the Bank of Canada unexpectedly resumed hiking its rates, stoking concerns for a further tightening by the Federal Reserve. The move comes after a surprising hike earlier in the week by Australia’s central bank. Meanwhile, Chinese equities in Hong Kong snapped a four-day winning streak following disappointing export data. This has raised hopes for more stimulus measures from the government.

- Hang Seng and Shanghai Comp. were lacklustre amid the ongoing growth concerns surrounding the world’s second-largest economy although the losses stemmed after China's Big 4 banks reduced their deposit rates following calls from the government to help bolster the economy.

- Nikkei 225 was initially choppy but eventually retreated firmly beneath the 32,000 level despite the stronger-than-expected upward revisions to Japan's Q1 GDP.

- ASX 200 traded rangebound as gains in the commodity-related sectors were offset by underperformance in property and tech, while softer trade data from Australia added to the non-committal mood.

“If there are pressures that are too negative in the domestic economy, I really believe the government will come in with support measures but in a much more, I would say, delicate way” than what was seen earlier, Virginie Maisonneuve, global chief investment officer for equities at Allianz Global Investors, said in an interview with Bloomberg Television. Investors are also awaiting data on foreign buying of Japanese stocks due later this afternoon, given the recent market strength in the world’s third-largest economy

In FX, the Bloomberg dollar spot index fell 0.2%. SEK and CHF are the weakest performers in G-10 FX, NZD and AUD outperform. The Turkish lira continued its merry disintegration.

In rates, Treasuries are slightly cheaper across the curve. US yields cheaper by 1bp-2bp across the curve with 7-year sector underperforming, widening 5s7s10s fly by 1.5bp on the day; 10- year yields around 3.81%, cheaper by 1.5bp on the day with gilts underperforming by 3bp in the sector. Gilts underperform bunds and Treasuries, and lead core European rates lower with 30-year UK cheaper by more than 5bp on the day, while euro money markets cement bets on a 25bp ECB rate hike next week. US session includes weekly jobless claims data.

In commodities, WTI trades within Wednesday’s range, falling 0.4% to near $72.21. Spot gold rises roughly $8 to trade near $1,948/oz

To the day ahead now, it’s an incredibly quiet one on the calendar, with one of the few highlights being the US weekly initial jobless claims.

Market Snapshot

- S&P 500 futures little changed at 4,277.50

- MXAP down 0.3% to 163.31

- MXAPJ little changed at 516.75

- Nikkei down 0.9% to 31,641.27

- Topix down 0.7% to 2,191.50

- Hang Seng Index up 0.2% to 19,299.18

- Shanghai Composite up 0.5% to 3,213.59

- Sensex little changed at 63,141.77

- Australia S&P/ASX 200 down 0.3% to 7,099.66

- Kospi down 0.2% to 2,610.85

- STOXX Europe 600 little changed at 461.00

- German 10Y yield little changed at 2.45%

- Euro up 0.2% to $1.0718

- Brent Futures little changed at $76.97/bbl

- Gold spot up 0.4% to $1,947.72

- U.S. Dollar Index down 0.18% to 103.91

Top Overnight News

- US futures slipped and Treasuries held their sharp move from the previous session, after a surprise Bank of Canada rate increase led traders to reassess the risks from stubborn inflation.

- Global bonds are slumping after two shock interest-rate hikes this week served traders a reality check that central banks are far from done fighting inflation.

- After dominating bonds and equities investing for years, BlackRock Inc. is looking to become a one- stop destination for clients in private markets, a more lucrative area of finance.

- Most Europeans consider China a key economic partner despite seeing limits to the relationship, according to a survey that comes as the bloc tries to find a safe way to engage with Beijing.

- China’s economic recovery showed further signs of weakening in May, clouding the outlook for the rest of the year and fueling calls for more central bank stimulus.

A more detailed look at global markets courtesy of Newsquawk

Asia-Pac stocks were mostly subdued following the mixed handover from Wall St where tech underperformed as global yields climbed after the surprise BoC rate hike. ASX 200 traded rangebound as gains in the commodity-related sectors were offset by underperformance in property and tech, while softer trade data from Australia added to the non-committal mood. Nikkei 225 was initially choppy but eventually retreated firmly beneath the 32,000 level despite the stronger-than-expected upward revisions to Japan's Q1 GDP. Hang Seng and Shanghai Comp. were lacklustre amid the ongoing growth concerns surrounding the world’s second- largest economy although the losses stemmed after China's Big 4 banks reduced their deposit rates following calls from the government to help bolster the economy.

Top Asian News

- China National Financial Regulation Administration head Li said they will continue to support Shanghai as a financial centre and that China's economy is continuing its recovery, while the domestic economy is showing resilience and dynamism. Li added that they will step up support for high-tech sectors and comprehensively improve financial regulation, as well as improve private firms' financing environment, according to Reuters.

- China securities regulator chairman said they will support technology innovation in a more precise and effective manner, while they will further promote long-term capital to invest in equities and promote product innovation to support bond, equity and M&A financing, according to Reuters.

- RBI kept the key Repo Rate unchanged at 6.50%, as expected, with the decision on rates made unanimously and it also maintained the policy stance of remaining focused on the withdrawal of accommodation through a 5-1 vote. RBI Governor Das said the path ahead is now somewhat clearer and uncertainty on the horizon is comparatively less, while he added the MPC will remain vigilant on the evolving situation and growth outlook. Das also said they will take further action promptly and headline inflation is still above target and that being within the tolerance band is not enough.

European bourses are mixed/flat with newsflow limited and the region alongside broader assets largely struggling for direction into a sparse docket. Sectors are mixed overall; Basic Resources outperform as metals lift slightly and on a Rio Tinto upgrade while Tech and Healthcare names lag. Stateside, futures paint a similar picture but feature incremental underperformance in the NQ and outperformance in RTY which continues its recent strength amid a rotation into small caps. Tesla (TSLA) is asking several Chinese supply chain companies to build factories in Mexico to replicate a Giga Shanghai and its supply chain system there, according to a report cited by CnEVPost. Meta (META) voluntary child protection appears not to work, according to EU's Bretton via a Reuters exclusive; calls on CEO to explain and take immediate action.

Top European News

- US President Biden vetoed the lawmaker resolution against his student loan plan, according to Reuters.

- US federal prosecutors notified former President Trump that he is a target of a special counsel investigation over classified documents, according to ABC citing sources.

FX

- Dollar drifts ahead of US jobless claims, as DXY fades above 104.000 within 104.070-103.810 range.

- Aussie and Kiwi derive most from the latest Buck downturn, with AUD/USD and NZD/USD elevated above 0.6650 and around 0.6050 respectively.

- Loonie straddles 1.3350 vs Greenback post-BoC hike and pre-commentary from Beaudry before Canadian jobs on Friday.

- Euro and Yen firmer against Dollar around 1.0700 and 140.00 handles, but wary of very large option expiries nearby.

- Lira continues to collapse with no respite insight this side of 23.5000 vs Dollar.

- PBoC set USD/CNY mid-point at 7.1280 vs exp. 7.1282 (prev. 7.1196)

- PBoC Vice Governor said they have confidence, conditions and the capacity to maintain stable operations of the FX market, while the FX market, yuan market expectations and cross-border capital flows are relatively stable. Furthermore, the official stated as the Fed nears the end of its rate hike cycle, USD strength is hardly sustainable and the external impact on the yuan is expected to weaken, according to Reuters.

Fixed Income

- Debt still waning and after hawkish Central Bank turns, Bunds regained some poise after dipping below 133.00, but bounce curtailed bang on 133.50.

- Gilts lag within 95.94-61 range and T-note mostly sub-par between 113-07+/112-30 bounds pre-US jobless claims and Quarterly Refunding announcement.

- Orders for the new 4yr BTP Valore retail bond reach EUR 15bln since the commencement of the offer.

Commodities

- Crude benchmarks have spent the morning choppy but within particularly narrow parameters of sub-USD 1.00/bbl with specific newsflow exceptionally light and markets generally quiet ahead of US IJC during Fed blackout.

- Specifically, WTI and Brent are holding at the lower end of USD 72.07-72.88/bbl and USD 76.44-77.29/bbl parameters which themselves are well within the ranges of yesterday and by extension the more pronounced movement of last week.

- Spot gold is firmer but remains capped by the USD 1950/oz level with the 10-DMA just above at USD 1954/oz. To the downside, the sessions trough dipped just below the 100-DMA at USD 1940/oz; the current low is USD 1939/oz.

- Base metals are more of the same, with the main benchmarks rangebound and around familiar levels and following suit to the broader risk tone.

Crypto

- Bitcoin is essentially unchanged, in very narrow parameters and moving in-situ with broader asset classes in very quiet newsflow.

- G20 emerging nations are reportedly concerned that widespread use of stablecoins could threaten their monetary policy and as such are after stricter regulation, via CoinDesk citing officials.

Geopolitics

- Taiwan Defence Ministry said 37 Chinese aircraft entered Taiwan's air defence zone starting Thursday morning and some of the aircraft flew into the western Pacific, while Taiwan sent an aircraft to keep watch, according to Reuters.

- IAEA's Gross intends to rotate inspectors at the Zaporizhzhia nuclear plant next week, plans need to be agreed with Ukraine and Russia.

US Event Calendar

- 08:30: May Continuing Claims, est. 1.8m, prior 1.8m

- 08:30: June Initial Jobless Claims, est. 235,000, prior 232,000

- 10:00: April Wholesale Trade Sales MoM, est. 0.9%, prior -2.1%

- 10:00: April Wholesale Inventories MoM, est. -0.2%, prior -0.2%

- 12:00: 1Q US Household Change in Net Worth, prior $2.93t

DB's Jim Reid concludes the overnight wrap

With less than a week to go until the Fed’s next decision, yesterday offered another hawkish surprise for markets after the Bank of Canada delivered an unexpected 25bp rate hike. Now that might be just one central bank, but it comes on the back of a similar surprise hike from the Reserve Bank of Australia the previous day, so investors are starting to see a pattern emerging here and there was a significant bond selloff as a result. The latest developments have also run against the prevailing narrative that central banks are on the verge of pausing their rate hikes, particularly given Canada was one of the first to formally signal a pause back in January. The big question now is whether the Fed might follow up with a hike of their own next Wednesday, or whether they’ll finally keep rates on hold after 10 consecutive increases.

When it came to the Bank of Canada, they announced they were taking their overnight rate up to a post-2001 high of 4.75%, and their statement said that that “excess demand in the economy looks to be more persistent than anticipated”. In light of this, they wrote that “concerns have increased that CPI inflation could get stuck materially above the 2% target”, and they said they were hiking since “monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target.” Looking forward, they didn’t provide too much of a steer on future policy, but markets then moved to price in a further hike in July as the most likely outcome.

That surprise rate hike sparked a big selloff among sovereign bonds. Unsurprisingly, Canada was at the epicentre of this, and their 10yr government bond yield was up +16.3bps on the day to their highest level since early March. That was echoed among US Treasuries, where the 10yr yield (+13.5bps) rose to 3.80%, and the 2yr yield (+7.8bps) hit a post-SVB high of 4.56%. There was a strong rise in real yields too, with the 2yr real yield (+9.2bps) closing at a post-GFC high yesterday of 2.49%, and the 10yr real yield (+11.7bps) closing at a post-SVB high of 1.59%. So it’s clear that investors are pricing in the prospect of higher rates for longer.

When it comes to next week’s Fed decision, it’s hard to get a firm steer on things given that officials are now in their blackout period ahead of the meeting. Nevertheless, the decision from the Bank of Canada meant that futures moved to price in a 35% chance of a hike, up from 19% as of close on Tuesday. At the same time, investors also grew more sceptical that the Fed would end up cutting rates this year at all, with the rate priced in by the December meeting up to a post-SVB high at 5.03%. Bear in mind that after the Fed’s last meeting in May, that rate expected in December was priced at 4.18%. So in just over a month, we’ve had around 85bps of expected cuts for this year taken out of market pricing.

This selloff was evident in Europe as well, with yields on 10yr bunds (+8.3bps), OATs (+9.4bps) and BTPs (+15.1bps) all moving higher. That came as ECB speakers continued to signal another rate hike next week. For instance, Isabel Schnabel of the Executive Board said that “we have more ground to cover” in an interview with De Tijd that was conducted last week but released yesterday. Along these lines, Ireland’s Makhlouf said that “more work is needed from monetary policy in the short run” and the Netherlands’ Knot said that he was “not yet convinced that the current tightening is sufficient”. All this meant markets priced in more rate hikes over the rest of the year, with the rate priced in for the December meeting up +4.0bps on the day.

This backdrop meant that equities struggled, and the S&P 500 (-0.38%) saw a pullback that took it further away from bull market territory. For once, tech stocks actually underperformed, and the NASDAQ (-1.29%) came off its one-year high from the previous day, whilst the FANG+ index (-2.91%) saw even larger declines. On the other hand, energy stocks were the biggest outperformer, having been aided by a rebound in commodity prices over recent days. Indeed, Brent Crude closed up +0.87% to $76.95/bbl, marking its highest level in 8 trading sessions. Otherwise in Europe it was much the same story, and the STOXX 600 (-0.19%) posted a small decline.

Broadly speaking, this pattern has continued overnight in Asia, with some fresh momentum after data revisions showed that Japan’s Q1 GDP growth was faster than initially thought. Specifically, growth was revised up to an annualised rate of +2.7%, which was above the initial +1.6% estimate, as well as economists’ expectations of a +1.9% reading. That’s meant that bonds have continued to lose ground across the region, and yields on 10yr Australian (+15.0bps) and New Zealand (+12.1bps) government debt have seen some strong increases this morning. The major equity indices have experienced losses too, with the Nikkei (-0.96%), the KOSPI (-0.64%), the Hang Seng (-0.39%) and the Shanghai Comp (-0.12%) all falling back. The main exception is the CSI 300 (+0.09%) which has posted modest gains. Looking forward, US and European equities futures are pointing towards more losses today as well, with those on the S&P 500 currently down -0.18%.

There was little in the way of economic data yesterday. German industrial production saw a small rebound in April (+0.3% mom vs +0.6% expected) but with the March decline revised upward (from -3.4% to -2.1%). The OECD published their latest economic outlook, with a view that global growth would come in at 2.7% this year, before picking up slightly to 2.9% in 2024.

To the day ahead now, it’s an incredibly quiet one on the calendar, with one of the few highlights being the US weekly initial jobless claims.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire