Uncategorized

Futures Rise, Bank Stocks Soar On Report Private Equity Firms Circle SVB Loan Book

Futures Rise, Bank Stocks Soar On Report Private Equity Firms Circle SVB Loan Book

Market mood recovered from yesterday’s bank rout as contagion…

Share this:

Market mood recovered from yesterday's bank rout as contagion fears from the collapse of SIVB and SBNY appear to have subsided for the time being, despite a hiccup earlier in the session when Credit Suisse stock hit a new record low after the Swiss bank said it had identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021. The mood was lifted by a Bloomberg report that Apollo Global and Blackstone have expressed interest in snapping up a book of loans held by Silicon Valley Bank, suggesting the collapsed bank contagion may be contained after bigger buyers step in.

S&P futures were up 0.8% to 3,920 and Nasdaq 100 futures rise 0.7% ahead of US CPI later today (full CPI preview here). Major US banks were broadly higher in the premarket as regional lender First Republic Bank surged 39% after plunging on Monday. This has led to a rebound in short end yields with US two-year up 27bps on the day to 4.22% (still down around 85bps from last week’s peak). Plunging rates gripped Wall Street’s attention yesterday, when the yield dropped more than a half-percentage point in the biggest move since the 1980s. The 10-year yield rose three basis points to 3.60%, while a gauge of the dollar snapped three days of losses.

In premarket trading, financial stocks traded higher, alongside the broader market as banks rally off a historically bad Monday; the mood was lifted by the aforementioned BBG report that Apollo and Blackstone, two of the world’s largest alternative asset managers, are among investors looking to buy pieces of Silicon Valley Bank. First Republic Bank jumped 44% in premarket trading, while PacWest Bancorp rose 34% and Western Alliance Bancorp added more than 20%. Bigger lenders were also in the green, with Bank of America Corp advancing 3% and Citigroup Inc. adding 1.3%. Here are some other notable premarket movers:

- United Airlines shares drop 6.1% after the carrier slashed its 1Q outlook and now expects to post a loss for the period. Analysts said that the revised guidance was due to the change in timing for pilot contract accrual, though note other aspects of the 2023 outlook remain unchanged.

- Uber and Lyft advanced after a California appeals court upheld the current law classifying gig workers as independent contractors instead of employees. Analysts noted that this would allow the companies to avoid any negative impact to their business. Uber rose as much as 5.8% and Lyft jumped 6.4%

- Cryptocurrency-exposed stocks rose after Bitcoin extends its gains as US authorities stepped in to stem spreading concerns about the health of the nation’s financial system after Silicon Valley Bank’s collapse. Bitfarms (BITF US) +8.5%, Stronghold Digital (SDIG US) +8.5%, Marathon Digital (MARA US) +2.1%, Riot Platforms (RIOT US) +1.3%, Coinbase (COIN US) +0.6%

- Momentive Global rose 18% to $9.13 per share, after the SurveyMonkey owner said it had agreed to be acquired by a consortium led by Symphony Technology Group for $9.46/share cash.

- Gitlab fell 33% after the software company gave a full-year revenue forecast that was weaker than expected. Analysts note that the management’s outlook seems conservative amid a tough macro environment.

- Amylyx Pharmaceuticals the maker of a drug for amyotrophic lateral sclerosis, rose 20% in after-market after posting 4Q revenue that easily topped estimates.

- Watch Apple stock as Evercore ISI said it deserves to trade at a premium valuation compared to its big tech peers, citing the iPhone maker’s higher operating efficiency, large share repurchase program and consistent execution.

The S&P 500 closed Monday down 0.2%, after bouncing between gains and losses amid a rout in bank shares while the policy-sensitive Nasdaq climbed 0.8%, the most in over a week. The fallout from SVB’s collapse prompted President Joe Biden to promise stronger regulation of US lenders, while reassuring depositors that their money is safe.

Treasuries had been whipsawed in recent days — with a measure of volatility climbing to the highest since 2009 — and banking shares plunged as the collapse of Silicon Valley Bank and two other US lenders prompted wagers the Federal Reserve will pause its hiking cycle and even cut interest rates to stabilize the financial system. But a hot inflation reading later today could muddy that outlook and spark a fresh wave of volatility in fixed-income markets.

“A policy mistake is hands down the biggest risk in the market,” Mary Manning, global portfolio manager for Alphinity Investment Management, said on Bloomberg Television. “Controlling inflation but also addressing the fact there is some instability in the banking system is difficult.”

As BBG notes, swap contracts referencing Fed policy meetings slashed the odds of any increase to less than one-in-two. Meanwhile, contracts for the rest of 2023 suggest that the Fed could cut rates by almost a full percentage point from the peak in May before the year is out. Goldman economists as well as asset managers from PIMCO said the Fed could take a breather on the policy rate following the collapse of SVB. Nomura economists took it one step further, saying the Fed could cut its target rate next week.

“Niggling concerns that mild recessions could be on the way have been replaced by a wall of worry about runs on smaller banks,” as well as the risk that larger ones may turn more risk averse to lending, according to Susannah Streeter, head of money and markets at Hargreaves Lansdown. Inflation data will be closely watched “as another hot reading will reinforce expectations that a rate rise, albeit smaller, will be on the cards next week,” she said.

Then there is CPI to look forward to: traders are looking to the US consumer price index report later in the day for cues that may trigger further shifts in the outlook for monetary policy. Our full CPI preview can be found here.

The bank selloff “certainly creates a headwind for aggressive Fed action, if any action,” said Gary Schlossberg, a senior economist at Wells Fargo. “But there is that very important data coming out which may not ease concerns over inflation. It means the Fed has even more of a balancing act.”

European stocks are also ahead, albeit slightly, with the Stoxx 600 adding 0.2%. European real estate shares jump the most in a month on bets central banks will slow the pace of interest-rate hikes, with the Stoxx 600 Real Estate subindex outpacing all others; elsewhere, utilities and industrials were among the best-performing sectors while the FTSE 100 underperforms, down 0.2%. Credit Suisse shares slide to new record lows, shedding as much as 5.6%, after the lender said it had found “material weaknesses” in its reporting and control procedures for the past years. Here are the most notable European movers:

- Generali shares rise as much as 2.5% and are the top performers on the FTSE MIB index, after the Italian insurer reported full-year operating results that were ahead of estimates

- Icade shares jump as much as 10%, their biggest gain since November 2020, after the real estate investment trust entered a pact with Primonial REIM to sell its stake in Icade Santé

- Wojas surge as much as 33% to a record high after the Polish footwear producer said it had received a 138.6m zloty contract to make military shoes for the country’s army.

- Close Brothers shares fall as much as 7.5% after the UK financial services firm posted 1H pretax operating profit that missed the average analyst estimate

- PolyPeptide falls as much as 22% to a record low, after the biotech reported full- year results that were once again weaker than expected even after two profit warnings, according to ZKB

- TP ICAP falls as much as 8.9% after dark pool unit Liquidnet saw “subdued” block trading activity last year, amid a broader equity-market rout, according to the firm’s results

- Fraport shares fall as much as 7%. Warburg notes free cash flow levels are still “deep in negative territory,” even as the German airport operator posted a good set of FY results

Earlier in the session, shares of Asian financial firms decline after Treasury yields dropped and US bank stocks slid amid continued concerns related to bank failures. The MSCI Asia Pacific Financials Index falls as much as 2.7% to the lowest since Nov. 29. Investors questioned whether the US government’s rescue plan for the banking system will prevent more fallout from SVB’s collapse. The KBW Bank Index dropped nearly 12% Monday, the most since March 2020. The 10-year Treasury yield shed about 13 basis points to 3.57%; two-year yields plunged 61 bps

Japanese stocks fell for a third day as investors continued to assess the fallout from the collapse of Silicon Valley Bank and rethink expectations for Federal Reserve monetary policy. The Topix Index fell 2.7% to 1,947.54 as of the market close in Tokyo, while the Nikkei 225 declined 2.2% to 27,222.04. The yen weakened slightly after strengthening 1.4% Monday to 133.21 per dollar. Mitsubishi UFJ Financial Group Inc. contributed the most to the Topix’s decline, decreasing 8.6%. Out of 2,159 stocks in the index, 66 rose and 2,081 fell, while 12 were unchanged. The Topix’s gauge for banks and insurers dragged the broader index down, both tumbling at least 6%, as the SVB trouble has driven investor attention to the heavy investment in US bonds by Japan’s lenders. The uncertain sentiment toward financial institutions also set off a plunge in bond yields in the US and Japan. The US two-year Treasury yield dropped on Monday, logging the biggest three-day retreat since Black Monday of October 1987, as market participants continued to flee US bank shares even after US regulators announced a rescue plan Sunday evening. Japan’s five-year yield also tumbled to lowest since Dec. 2 earlier today. Bond Yields’ Plunge Is Biggest Since Volcker Era on Bank Worries “News around US banks had a major impact creating the ‘flight to safety’ sentiment,” said Mamoru Shimode, chief strategist at Resona Asset Management. “Investors are leveraging and taking out loans, and their money is connected to the financial system, so they are reducing their positions due to a sense of uncertainty.”

South Korea’s Kospi dropped 2.6%, the most since Sept. 26, as foreign investors sell equities in Kospi futures and cash markets amid worries about repercussions from the SVB crisis. “Emerging markets are vulnerable every time there are worries about financial risks in developed markets,” Seo Jung-Hun, an analyst at Samsung Securities said by phone “It appears that foreign investors are hedging their risks through South Korea” by heavily selling Kospi 200 futures. Foreigners cut 1.4 trillion won worth of futures in the Kospi 200 Index, the most since August 2021, while selling net 638 billion won in the Kospi cash markets

In Australia, the S&P/ASX 200 index fell 1.4% to 7,008.90, its lowest close since Jan. 3. The benchmark extended losses to a third day, as all sectors declined. Equities across Asia fell, led by weakness in financial stocks as the collapse of Silicon Valley Bank continued to reverberate across global markets. In New Zealand, the S&P/NZX 50 index fell 0.7% to 11,595.47

In India, major equity indexes plunged for a fourth consecutive session as most Asian markets extended their declines, triggered by the continued selloff in financials. Indian software makers were the worst performers on worries over the banking sector in the US, their biggest revenue generator. The S&P BSE Sensex fell 0.6% to 57,900.19 in Mumbai, while the NSE Nifty 50 Index declined by a similar measure as the guages come within 2% of entering a so-called correction from their record peaks in early December. Asia’s benchmark stock index erased all of its gains for the year as financials extended the rout following the implosion of Silicon Valley Bank. “Markets are likely to remain under pressure in the near term,” Siddhartha Khemka, head of retail research at Mumbai-based Motilal Oswal Financial Services said. US inflation data to be released later Tuesday will be a key factor to watch, he added. Tata Consultancy Services contributed the most to the Sensex’s decline, decreasing 2%. Out of 30 shares in the Sensex index, 7 rose and 23 fell

In FX, a gauge of the greenback rebounded from a three-week low as Treasury yields rose before the release of US inflation data. The Japanese yen was the weakest of the G-10 currencies, while the Dollar Index adds 0.2%. Traders may take their next cue from US inflation data to gauge if the Federal Reserve will halt its tightening campaign to limit the fallout from higher interest rates

In rates, Treasuries are cheaper across front-end and belly of the curve, unwinding a portion of Monday’s aggressive bull-steepening rally. Long-end yields slightly richer on the day, re-flattening 2s10s and 5s30s spreads ahead of February inflation data, Tuesday’s main calendar event. Yields cheaper by as much as 24bp across front-end of the curve with 2s10s, 5s30s spreads flatter by ~21bp and ~10bp on the day; 10-year yields around 3.59%, cheaper by ~2bp vs Monday’s close, with bunds and gilts lagging by 7bp and 6bp in the sector. Early gains in Treasuries during Asia session were spurred by report that Credit Suisse Group AG said it found “material weaknesses” in its reporting and control procedures for the past two years. UK and German two-year yields rise 12bps and 10bps respectively. Ahead of CPI, Fed-dated OIS price in around 19bp of rate-hike premium for the March policy meeting, up from 13bp at Monday’s close.

In commodities, oil extended a decline ahead of the inflation data with WTI futures declining down 2.7% to trade near $72.80. Bitcoin rises 1.0% while spot was gold down 0.6% after rising in the three previous sessions as traders turned to haven assets.

To the day ahead now, and data releases include the US CPI release for February, the NFIB small business optimism index for February and the UK unemployment rate for January. Otherwise, central bank speakers include Fed Governor Bowman.

Market Snapshot

- S&P 500 futures up 0.4% to 3,873.50

- MXAP down 2.2% to 155.29

- MXAPJ down 1.7% to 500.30

- Nikkei down 2.2% to 27,222.04

- Topix down 2.7% to 1,947.54

- Hang Seng Index down 2.3% to 19,247.96

- Shanghai Composite down 0.7% to 3,245.31

- Sensex down 0.7% to 57,817.37

- Australia S&P/ASX 200 down 1.4% to 7,008.88

- Kospi down 2.6% to 2,348.97

- STOXX Europe 600 little changed at 443.15

- German 10Y yield little changed at 2.26%

- Euro down 0.4% to $1.0693

- Brent Futures down 1.5% to $79.58/bbl

- Brent Futures down 1.5% to $79.56/bbl

- Gold spot down 0.4% to $1,906.05

- U.S. Dollar Index up 0.36% to 103.97

Top Overnight News

- China said its embassy in Washington would once again permit foreign tourists to visit the country, the latest example of Beijing lifting its COVID restrictions. WSJ

- Just 1 week ago it would have been hard to imagine anyone asking if the CPI print even matters. Oh how quickly things change. This makes me believe risk is skewed to the downside post CPI print. Unless we get a shockingly hot number mkt will remain more focused on unfolding banks drama ( a soft print will be disregarded as not relevant). For headline print GIR look for +.4% MoM ( vs +.4% cons and +.5% prior) and +6.08% YoY (vs +6% cons and +6.4% prior). For core MoM GIR looking for +.45% (vs +.4% consensus and +.4% prior) and YoY of +5.56% (vs 5.5% cons and 5.6% prior). GS GBM

- Gov. Ron DeSantis of Florida has sharply broken with Republicans who are determined to defend Ukraine against Russia’s invasion, saying in a statement made public on Monday night that protecting the European nation’s borders is not a vital U.S. interest and that policymakers should instead focus attention at home. NYT

- U.S. regulators are likely to let emergency measures announced Sunday to shore up investor confidence in the banking sector sink in and increase scrutiny of the industry before intervening with any further steps, regulatory experts said. RTRS

- Biden was apparently “highly skeptical” of intervening in the bank industry over the weekend but was finally brought on board by fears about contagion. WaPo

- FDIC is concerned that it is now expected to guarantee all depositors every time a bank fails, something it is not designed to do. Politico

- The FHLB system, a key source of cash for regional lenders, raised $88.7 billion through the sale of short-term notes, according to people with knowledge of the matter, more than the $64 billion initially planned. BBG

- Moody’s placed First Republic Bank, Western Alliance Bancorp., Intrust Financial Corp., UMB Financial Corp., Zions Bancorp. and Comerica Inc. on review for downgrade, the latest sign of concern over the health of regional financial firms following the collapse of Silicon Valley Bank.

- The DOJ is probing last year's collapse of the TerraUSD stablecoin, raising the risk of criminal charges against its fugitive creator Do Kwon, the WSJ reported. Separately, US prosecutors are looking at Telegram chats among employees at Jump, Jane Street and the now-bankrupt Alameda about a potential bailout of the TerraUSD project, and whether market manipulation was involved, a person familiar said. BBG

- One year after the Federal Reserve started frantically raising interest rates, the collapse of Silicon Valley Bank answered what had become perhaps the hottest question on Wall Street: When is something going to break? BBG

- Credit Suisse says it has identified material weaknesses in its internal control over financial reporting as of December 31, 2022 and 2021, according to the annual report: BBG

- Some of the world’s top money managers are sitting on a windfall after the collapse of Silicon Valley Bank spurred the biggest rally in US Treasuries since the early 1980s: BBG

A more detailed look at global markets courtesy of Newqsuawk

Asia-Pac stocks declined amid a continuation of the selling in financials and with risk appetite constricted amid the fallout from the recent US bank collapses. ASX 200 spent most of the session beneath the 7,000 level with the index pressured by substantial losses in nearly all sectors and amid headwinds from weak data releases in which Westpac consumer sentiment remained near historic lows and NAB business surveys deteriorated. Nikkei 225 slumped due to heavy losses in financial stocks which occupied the list of the 10 worst performers, while the Tokyo Stock Exchange banking index suffered its worst day in over three years. Hang Seng and Shanghai Comp. retreated albeit with less aggressive selling in the mainland on reopening news as China is to resume the issuance of all types of visas for foreigners from March 15th.

Top Asian News

- US President Biden said he will talk to Chinese President Xi soon but didn't specify when. Furthermore, National Security Adviser Sullivan said President Biden anticipates a call opportunity with Chinese President Xi once China's government returns to work after the NPC, while Sullivan added the US had communicated with China over the AUKUS submarine pact and China's military build-up.

- EU seeks new controls to limit China acquiring high-tech and is exploring ways to police how European companies invest in production facilities overseas, according to FT.

- The Great Hiking Cycle Is Seen as Done as Yields Drop Below Cash

- SVB Crisis Puts Focus on Chinese Tech IPOs in the US: ECM Watch

- China Assets Stand Out as Oasis of Calm Amid SVB Fallout

- Germany, Brazil Plan High-Level Meetings as Ties Strengthen

- Japan Yield Falls Past Previous BOJ Ceiling as US Hike Bets Ease

- Global Financial Stocks Lose $465 Billion as SVB Fallout Spreads

European bourses are posting tentative gains, Euro Stoxx 50 +0.2%, as the risk tone remains fragile given financial stability concerns. Banking names in Europe remain softer, with Credit Suisse lagging after finding material weakness in its 2021/22 financial reporting; for the sector more broadly, GS highlights there is a limited risk of direct contagion to Europe. Stateside, futures are modestly firmer but have been unable to claw back any of Monday's marked downside, ES +0.4%, ahead of February's CPI. CATL's (3007540 CH) at least USD 5bln Swiss IPO is said to be delayed amid regulatory concern, according to Reuters sources; no new timetable for Swiss listing.

Top European News

- UK PM Sunak invited US President Biden to visit Northern Ireland for the anniversary of the Good Friday Agreement, while President Biden said that he intends to go to Northern Ireland

- UK Chancellor Hunt is to set out plans for 12 new investment zones in the Budget to "supercharge" growth in hi-tech industries, while the scheme is to be backed by GBP 80mln of investment over five years in each of the new high-growth zones, according to Sky News.

- Germany has reportedly made last-minute demands on the reform of EU fiscal rules, according to Bloomberg, casting doubts on a draft proposal agreed by EU members. Follows reports that EU Finance Ministers are to discuss the Growth and Stability Pact on 14th March, draft conclusions show general support for the switch from a one-rule-fits-all approach to debt reduction to multi-year plans tailored to each nation, via Politico; Germany said to seek to ensure nations bring down debt by a common quantitative benchmark/target.

SVB/Bank Bailout update

- Top Senate and top House Democrats said Congress will be looking closely at the causes behind the run on SVB and other banks, as well as how a similar crisis can be prevented in the future.

- Silicon Valley Bank N.A. CEO said they are conducting business as usual within the US and expect to resume cross-border transactions in the coming days, while the CEO added the FDIC transferred all deposits and all assets of former Silicon Valley Bank to the newly created, full-service FDIC-operated 'bridge bank' and all depositors have full access to their money with deposits protected.

- FDIC is still looking to sell SVB (SIVB) and told GOP senators it is planning another auction, according to WSJ sources.

- Moody's withdrew Signature Bank's (SBNY) long-term and short-term local currency bank deposit ratings, while it downgraded its subordinate debt to C from BAA3 and will withdraw ratings. Furthermore, Moody's placed multiple US banks under review for downgrade including Zions Bancorporation (ZION), Comerica (CMA), UMB (UMBF), Western Alliance (WAL), First Republic (FRC), Signature Bank (SBNY) and Intrust.

- Large US banks are reportedly inundated with new depositors as smaller lenders face turmoil with JPMorgan (JPM), Citigroup (C) and other large financial institutions trying to accommodate customers wanting to move deposits quickly, according to FT.

- Credit Suisse (CSGN SW) found material weakness in financial reporting for 2021 and 2022, though the reports fairly present the situation. Co. at its AGM is to discuss the proposal for a distribution of a dividend to shareholders of CHF 0.05 gross per registered share for the financial year 2022. Adding, it could require significant resources to correct the material deficiencies within report, developing a remediation plan to address this. Note, this update is not in relation to the SVB situation. On SVB, CEO adds credit exposure is not material.

FX

- The DXY is firmer and benefitting from some consolidation/corrective price action in yields, with the index briefly surmounting 104.00 as the US 2 & 10yr yields convincingly reclaimed 4.00% and 3.50% respectively.

- Given the action in yields and the USD's recovery, the JPY is the clear underperformer giving back much of Monday's haven-premium; USD/JPY above 134.00 from a 133.04 base.

- As such, G10 peers are lower across the board though with the magnitude of downside less pronounced than the JPY move with EUR and GBP relatively unreactive to data prints; around 1.07 and 1.215 respectively vs the USD.

- Antipodeans are more rangebound with AUD and NZD around 0.665 and 0.621 respectively while the SEK as perhaps derived some incremental support from familiar Riksbank commentary.

- PBoC set USD/CNY mid-point at 6.8949 vs exp. 6.8933 (prev. 6.9375)

Fixed Income

- Core benchmarks have experienced a marked turnaround, after an initial move higher around Credit Suisse's update, with USTs now below 114.00 from a 115.07+ peak.

- Amidst this, yields are elevated across the curve with the US experiencing marked bear-flattening with US CPI due and potential remarks from Fed's Bowman.

- Within Europe, Bunds peaked just above 137 and have since reversed to below 135.00 while the UK sale was well-received and seemingly helped to lift Gilts off lows ahead of German Bobl supply.

Commodities

- WTI and Brent have been declining throughout the European morning after settling lower by around USD 2.0/bbl, with the front month futures below USD 73/bb; and USD 79/bbl respectively.

- Nat Gas experiences some modest divergence with Henry Hub firmer and Dutch TTF softer, with ING highlighting renewable generation and milder forecasts for northern Europe as factors.

- Metals are mixed, spot gold is slightly softer but is holding above USD 1900/oz while base metals continue to slip given the broader tone.

- Indian oil ministry says there are no discussions on payments of Russian oil in CNY, according to Reuters sources; India has no obligation to purchase Russian oil below the price cap.

- Black Sea grain deal has been extended according to Tass citing the Russian Deputy Foreign Minister; under prior conditions. Ukraine will adhere to the terms of the prior 120-day corridor, via Reuters citing a senior gov't official. However, Turkey and the UN subsequently clarified that talks are ongoing on an extension.

Geopolitics

- US President Biden said alongside Australian PM Albanese that he doesn't view what they are doing as a challenge to anybody but is more about stability in the Indo-Pacific after AUKUS leaders met and agreed on a plan to deliver nuclear-powered submarines to Australia.

- North Korea fired two short-range ballistic missiles into the East Sea. South Korea said the missiles flew 620km and the repeated launches are a grave act of provocation threatening peace and security in the region. South Korea also said it will carry out combined drills with the US as planned and maintain readiness based on overwhelming capability, while the US military said North Korean missile launches do not pose an immediate threat to US personnel or territory or to their allies.

- Russian Deputy Foreign Minister says Washington seeks to create flashpoints for geopolitical confrontation with Russia in Moldova and Georgia, via Al Jazeera.

Crypto

- US DoJ is probing the collapse of Do Kwon's TerraUSD stablecoin and FBI and New York officials have questioned former Terraform Labs team members, according to WSJ.

- Crypto conglomerate Digital Currency Group (DCG) is reportedly trying to find new banking partners for portfolio companies following the collapse of SVB (SIVB), Signature Bank (SBNY), and Silvergate (SI), according to messages viewed by CoinDesk

US Event Calendar

- 06:00: Feb. SMALL BUSINESS OPTIMISM 90.9, est. 90.3, prior 90.3

- 08:30: Feb. CPI MoM, est. 0.4%, prior 0.5%; Feb. CPI YoY, est. 6.0%, prior 6.4%

- CPI Ex Food and Energy MoM, est. 0.4%, prior 0.4%; CPI Ex Food and Energy YoY, est. 5.5%, prior 5.6%

- Real Avg Hourly Earning YoY, prior -1.8%, revised -1.9%

- Real Avg Weekly Earnings YoY, prior -1.5%, revised -1.9%

DB's Jim Reid concludes the overnight wrap

In late summer 1998 I went on holiday for 2 weeks. Before I went, a Mexico 2002 maturity bond traded at around +150-200bps over DM government bonds. After a relaxing two weeks in the sun with no mobile phones etc and no financial news flow I ambled back into the office to the shock of finding that same Mexico bond that I’d been involved in launching as a salesman a few months earlier was now trading at around +900bps. I was dumbfounded. Since then, I've learnt not to be too shocked by anything in financial markets even if yesterday was up there with some of the wilder days I can remember. In some benchmark assets (e.g. US 2yr yields) we saw far bigger moves that even during the GFC. However if you just looked at the S&P 500 (-0.15%) you'll be forgiven for thinking yesterday was a big fuss about nothing.

Overall, I came out of yesterday even more convinced of our long-standing H2 2023 US hard landing view but with absolutely no idea at the moment what the Fed and ECB are going to do at their meetings over the next week and even beyond. I always thought that with inflation where it was, that central banks would keep hiking until they broke something, which was especially likely with the yield curve so inverted. Now they have broken something, is that enough for a pause? Much will depend on whether markets and contagion risk can calm quickly enough. If the FOMC meeting was today I strongly suspect they wouldn't hike but a week is a long time in these markets. For the recession call it's simpler. As per last month's chart book we were just "Waiting for the lag" (link here). It's fair to say that the lag has well and truly arrived and it’s unlikely now that a key part of our macro story, namely lending standards, are going to get looser given all that's gone on. So no change to our very bearish year end 2023 credit spread targets through all this crisis.

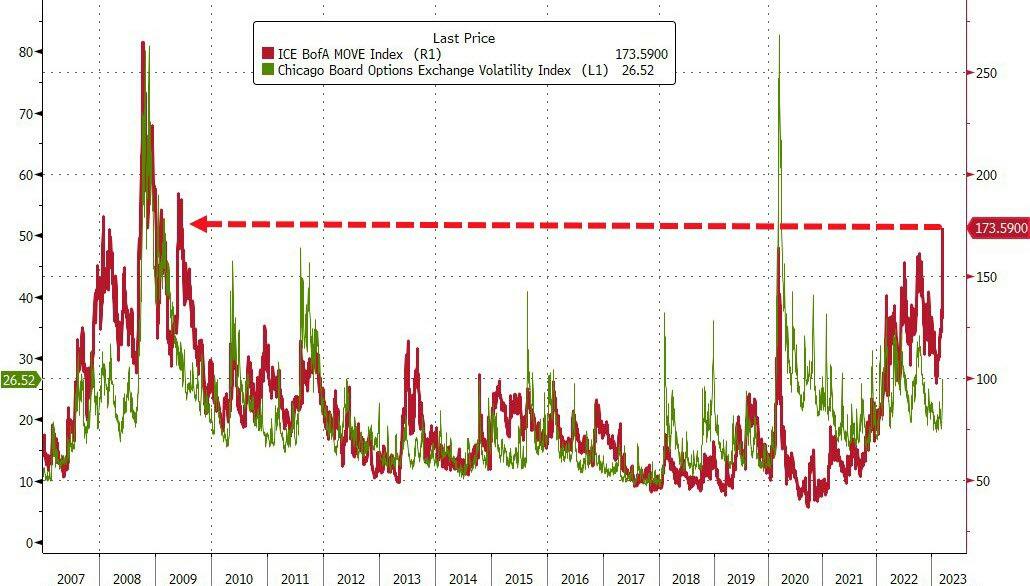

Back to current markets, let's first run through some of the astonishing stats from yesterday. The most remarkable was that we saw the biggest daily decline in the 2yr Treasury yield (-61.0bps) since October 7 1982 when the 2yr yield fell -75bps to 10.469% in what was a very different rate environment. In Europe, the 2yr German yield saw its biggest decline (-40.7bps) in available data back to reunification in 1990. And for equities, the KBW Banks Index (-11.66%) saw its worst performance since the height of the pandemic in March 2020 even if there was a big divide between big and small banks (see below). In the meantime, there are now serious questions being asked about whether the Fed might even call it a day on their current hiking cycle, and pricing for the Fed funds rate by the end of the year has now collapsed by over -140bps since last Wednesday. Meanwhile the MOVE index of bond volatility hit 14-year highs.

After all that, there’ve been few signs of any letup in Asian markets this morning, with banks leading a further round of equity declines. For instance, the TOPIX Banks index in Japan is down another -7.21%, which builds on its -9.17% decline over the previous two sessions. That has meant all the major equity indices have lost ground, including the Nikkei (-2.20%), the KOSPI (-2.37%), the Hang Seng (-1.59%), the Shanghai Comp (-0.77%) and the CSI 300 (-0.67%). Sovereign bond yields have moved lower in Asia too, with Japan’s 10yr government bond yield (-7.8bps) moving down to 0.24% this morning, which interestingly is beneath the Bank of Japan’s previous ceiling of 0.25% for the 10yr yield, which they moved up to 0.5% back in December.

Whilst markets in Asia have continued yesterday’s trend, those in the US this morning are showing signs of stabilising. Equity futures are pointing higher, with those on the S&P 500 up +0.31% after the index’s run of three consecutive declines. Furthermore, we’ve even seen a sharp rebound in the 2yr Treasury yield, which is up +18.4bps this morning to 4.16%, following its largest daily decline since 1982 over the previous session. The only thing to remember is that we have been here before to some extent, since 24 hours ago futures were pointing to an even sharper equity rebound before we ended up with the S&P seeing a modest decline, so this story could still have plenty of twists and turns remaining.

In terms of the latest on the SVB situation, concerns about potential contagion to other banks remain prominent, in spite of the moves we mentioned in yesterday’s edition from the FDIC and the Fed. We did hear from President Biden, who reassured the public that “the banking system is safe” and proposed new regulation that would “strengthen the rules for banks to make it less likely this kind of bank failure would happen again”. But he didn’t outline any specific proposals, and any new legislation would have to get past the Republican majority in the House of Representatives. After the US close the Fed announced that they would be launching an internal investigation into the supervision of Silicon Valley Bank, led by Vice Chair for Supervision Michael Barr.

In a move that highlights the current need for funding in financial markets, the US Federal Home Loan Banks raised $88.7bn in a bond sale yesterday, exceeding their initial target. The FHLB system is a Depression-era tool designed to be a lender of short-term funding to private banks in order to lessen the load on the Fed and make it not seem like banks are reaching for their “lender of last resort”. Silicon Valley Bank had tapped the FHLB last Thursday before the Fed stepped in and took control of the situation. Given the large bond sale it is likely that other regional banks are still looking for liquidity.

The lingering contagion concerns and fears about further outflows meant that bank stocks plummeted yesterday, particularly among some of the US regional banks. For instance, First Republic ended the day down -61.93%, which was actually a recovery from its intraday low of -78.56%. Another was Western Alliance Bancorp, which fell -47.06% having been as low as -84.88%. Both experienced trading halts during the day, and overnight Moody’s has placed the ratings of both on review for a downgrade. By contrast, the biggest banks were relatively unscathed, with JPMorgan only down -1.80%, whilst Bank of America (-5.81%) and Citigroup (-7.45%) also outperformed the wider KBW Banks Index.

Aside from contagion fears, the other big question moving forward is how central banks react to this turmoil. Up until Thursday of last week, investors had little doubt that the Fed would keep on hiking rates for some months, and a larger 50bps hike was seen as the most likely outcome for the next meeting. But the view now is that the SVB collapse has torpedoed any chance they might accelerate to 50bps, and even a 25bps move is now seen as questionable depending on what happens over the coming days. We’ve also seen financial conditions tighten with astonishing speed, with Bloomberg’s index seeing its largest move tighter over 3 days since March 2020 at the height of the pandemic.

Looking at market pricing, a 17.6bps hike is now priced in for the Fed’s meeting next week, which is down from 42.8bps last Wednesday. So that implies a roughly +71% chance they’ll follow through with a 25bps hike next week. Andif you look at pricing for the terminal rate there’s been an even more dramatic shift, since by the close yesterday it had fallen to 4.76% (-54bps yesterday) for the May meeting and only 6bps above March suggesting that the market isn’t pricing in a full 25bps hike anymore and a long way down from the intraday peak of 5.695% we saw for the September meeting last week. And overnight, terminal pricing has only seen a very partial rebound to 4.84%. Further out, there are nearly three 25bp rate cuts priced in for 2023 now, but for what it’s worth, the Fed haven’t started cutting rates with CPI or core CPI this high since 1981. And remember that was also when unemployment was running at 7.5% (rather than 3.6% today), so a cut was far easier to justify given their dual mandate for maximum employment alongside stable prices. So for the Fed to cut with this combination of above-target inflation whilst unemployment is around its lowest in half a century would be unprecedented.

As discussed at the top, the prospect that the Fed might already be done with its hiking cycle triggered a massive sovereign bond rally. This was most pronounced at the front-end, where the 2yr Treasury yield came down -60.98bps, with 10yr yields down “just” -12.5bps after intraday being down as much as -28.7bps in what would have been its largest decline on the year. This meant that the 2s10s curve steepened substantially on the day, finishing +48.2bps steeper to close -41.1bps inverted – that’s the least inverted the curve has been since late October and the largest amount of steepening since 9/11.

Interestingly, the declines in the 10yr portion of the rate curve were even bigger in Europe, despite the fact that they face far less exposure to SVB. That meant yields on 10yr bunds (-24.9bps) saw their largest daily decline since Mario Draghi became ECB President in 2011, whilst yields on 10yr OATs (-21.2bps) and gilts (-27.0bps) also tumbled. Much as happened in the US, a driving factor behind the European rates rally was the prospect of fewer rate hikes from the ECB. Their next meeting is only on Thursday, but markets are only pricing in a +38.7bps move despite their pre-existing commitment to a 50bp hike. And to be fair, back in June the ECB pre-committed to their initial hike being 25bps move in July, but they went onto deliver a 50bps one, so these clearly aren’t set in stone. Further out, there’s been a similar collapse in terminal rate pricing over recent days, with the deposit rate only expected to get to roughly 3.25%-3.50%, which is a big shift from the 4%-plus rates that had recently been expected.

Sticking with fixed income, credit widened further yesterday with Europe wider on the day as it caught up somewhat to the large moves in the US on Friday night. EUR HY Xover was +50bps wider to 476bps, while the EUR IG CDS index was +12bps wider to 94bps. On the other side of the Atlantic, the USD IG CDS was 8bps wider to 91bps and the USD HY CDS index was 36bps wider to 534bps – both of which are the widest levels since November.

When it came to equities, there was a much more divergent performance across regions and sectors. Bank stocks really suffered as mentioned above, but the broader S&P 500 recovered from an intraday low of -1.37% shortly after the open to post a modest -0.15% decline. Even with the recovery, volatility remained elevated, and the VIX index shot up further to end the day at a new high for 2023 of 26.5pts. By contrast in Europe, the STOXX 600 (-2.42%) had its worst day so far this year, with other major declines for the DAX (-3.04%), the CAC 40 (-2.90%) and the FTSE MIB (-4.03%).

With all that’s happening, today’s US CPI release suddenly feels like a second-tier concern. But it still could have an impact at the margins as the Fed decide whether to proceed with a hike next week, particularly if inflation comes in on the upside. In terms of what to expect, our US economists are looking for headline CPI to come in +0.37%, whilst core CPI should be pretty similar at +0.36%. If those are correct, that would take the year-on-year numbers down to +6.0% for headline CPI and +5.4% for core CPI. As ever, keep an eye out on the components, since if the stickier ones like core services are remaining persistent, then that would be a concern.

To the day ahead now, and data releases include the US CPI release for February, the NFIB small business optimism index for February and the UK unemployment rate for January. Otherwise, central bank speakers include Fed Governor Bowman.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

COVID-19 May Lead To Persistent Cognitive Impairment, Brain Fog, And Lower IQ Scores

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire