Uncategorized

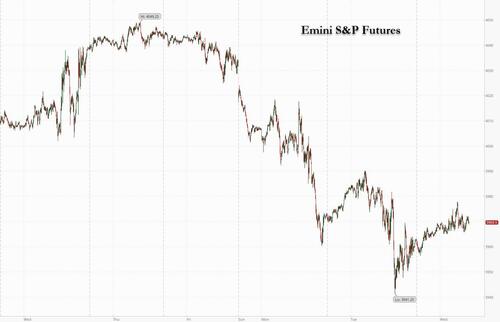

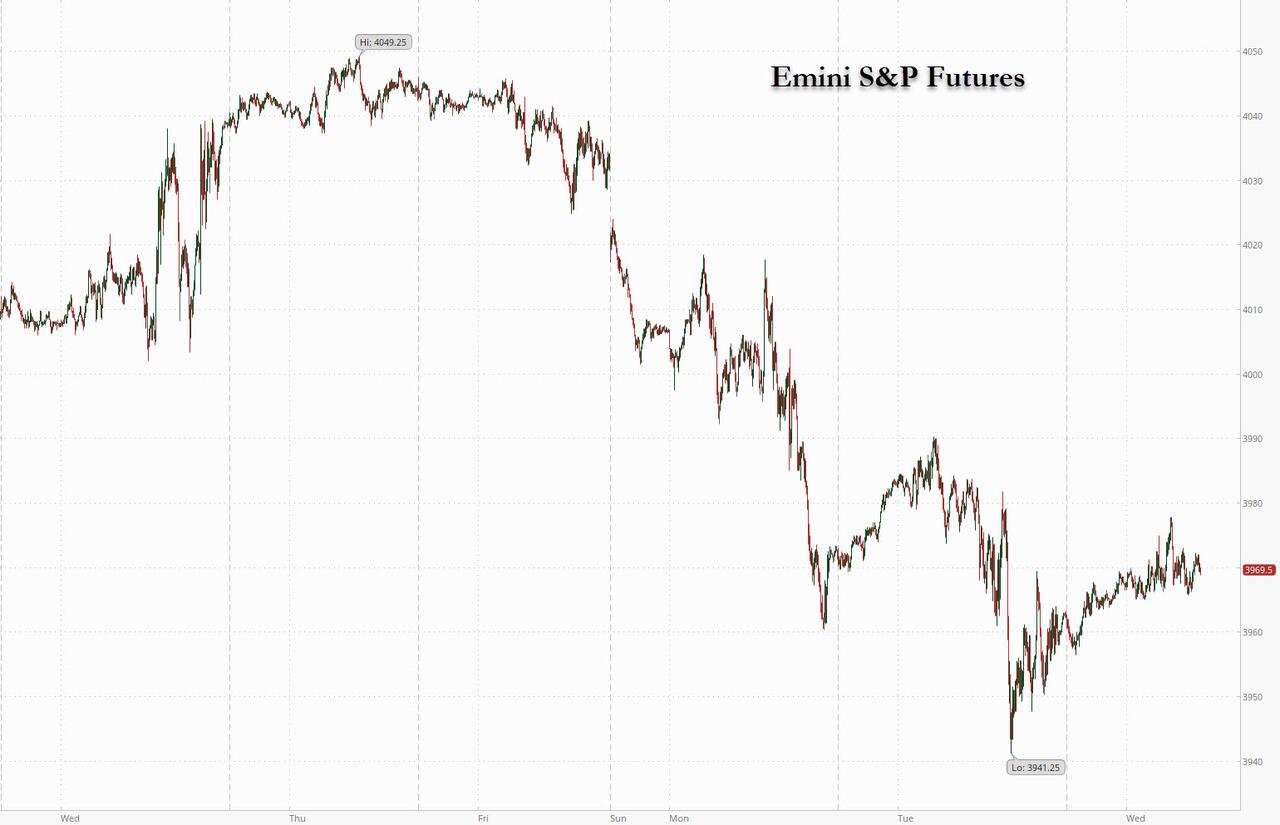

Futures Rise As Nervous Traders Await Powell Speech

Futures Rise As Nervous Traders Await Powell Speech

US futures rose on the last trading day of November as anxious investors awaited a potentially…

Share this:

US futures rose on the last trading day of November as anxious investors awaited a potentially monkey-hammering speech from Federal Reserve Chair Jerome Powell (although as JPM said, most of the downside is already priced in) and assessed a softer stance from China on Covid curbs. S&P 500 futures rose 0.2% by 745a.m. ET while Nasdaq 100 futures rose 0.3%. The underlying indexes have closed lower for three consecutive days amid Covid restrictions and unrest in China. In Europe, shares climbed the most in more than a week as data showed eurozone inflation slowed for the first time in 1-1/2 years. Benchmark Treasury 10-year yields slipped and are down more than 25 basis points in November.

In premarket trading, NetApp plunged 14% after the data-management company cut its guidance for earnings and revenue growth, while cybersecurity stocks fell after CrowdStrike’s forecast for fourth-quarter revenue fell short of estimates with analysts noting that macro headwinds have started catching up to the business as clients pull back on tech spending, while deals are taking longer to close amid an economic slowdown. HP Enterprise shares rose after sales beat forecasts on strong demand. Here are some other premarket movers:

- Cryptocurrency- exposed stocks climb as Bitcoin rose to a two-week high, before a keenly awaited speech by Fed Chair Jerome Powell that is expected to signal a slower pace of interest rate hikes in the US. Marathon Digital +4.8%, Riot Blockchain +5%, Coinbase +2.9% and Silvergate +2.4%

- Horizon Therapeutics stock rises 33% after the company confirmed it’s in “highly preliminary discussions” with Amgen, Johnson & Johnson and Sanofi about a possible sale. Such a deal would be accretive, analysts said, estimating a takeout price range between ~$110 and $135 a share.

- X4 Pharmaceuticals shares fall 18%, weakness that Stifel (buy) said is likely “balance-sheet driven” after the company disclosed in a presentation that it has sufficient cash to fund operations into 3Q next year.

- AST SpaceMobile shares decline 5.8% after offering of $65m of its Class A common stock via B. Riley, with net proceeds to be used for general corporate purposes.

- Keep an eye on LPL Financial stock as Morgan Stanley downgrades it to equal-weight and removes the broker-dealer from its ‘Financials’ Finest’ list, with private-equity group Blackstone (BX US) added.

- Watch Fisker stock as it was initiated with an outperform rating at Evercore ISI, with the broker positive on the firm’s “unique” business model. Lucid and Rivian which both gain in US premarket trading, are started at inline.

- Workday shares jumped 8.5% in US postmarket trading on Tuesday as the finance and human resources cloud software provider narrowed its subscription revenue guidance for the full year, with analysts saying that demand is holding up even against a tough macroeconomic backdrop.

US equities have been consolidating over the past 20 days, with the S&P 500 hovering around the 4,000 point-level, as volumes have collapsed heading into the year-end.

“The reality is that as we approach year-end, people’s appetite to add new risk will severely diminish,” said James Athey, investment director at Abrdn. “Indeed, with a recession the base case for 2023, investors who have made a quick profit on this recent rally are increasingly liable to want to book profit before liquidity dries up. That probably means we will continue to drift without much force in either direction.”

As previewed yesterday, Fed chair Jerome Powell is expected to speak about the state of the economy and the labor market at 1:30pm ET. Investors will pay attention to any clues about future policy, with the Fed Chair widely expected to signal lower rate hikes, but also warn that monetary tightening has further to run. He is widely expected to signal that the next Fed rate hike will step down to 50 basis points, though he will also likely warn that policy tightening has further to run. Those hopes of slower interest rate rises, alongside mounting optimism over China’s reopening, pushed the dollar lower and put the greenback on track for its worst month since 2009.

A degree of caution remains among traders before the Fed chair’s remarks, given still-high global inflation and a robust jobs market. “The market is hesitating a bit,” Societe Generale strategist Kenneth Broux said. “I would be very surprised if it is a dovish speech.” Some may hold the view that “the dollar has peaked and that the Fed Funds rate will peak at 5%, but I fear Powell will tell them it’s too soon,” he said.

“Where we think markets need to be cautious and where we would like to see a bit of tempering in optimism is over the pivot,” said Geoffrey Yu, senior strategist at Bank of New York Mellon. “What we are looking for is higher for longer.”

In Europe, the Stoxx 600 rose, led by consumer, auto, technology and energy shares. The benchmark is on course for a back-to-back monthly gain for the first time since August 2021. Here are the biggest European movers:

- Swedish biopharma company BioArctic jumps as much as 13% after its partner Eisai said the treatment for Alzheimer’s disease that they’re developing, lecanemab, isn’t to blame for two deaths involving brain bleeding of patients in a clinical trial.

- VGP gains as much as 6.6% after KBC Securities reinstated its buy recommendation, highlighting the Belgian real estate developer’s “strong management,” robust demand and good positioning in taking advantage of macro trends.

- Argenx rises as much as 7.4% after the biotech company agreed to purchase another FDA Priority Review Voucher, a move that KBC (buy) says can “significantly” accelerate regulatory review in the US, reducing times from about 12 months to six.

- Adyen climbs as much as 3.1% after New Street Research initiated with a buy rating, saying expectations over the payment firm’s margins have now been reset and it’s well positioned to create long-term value versus competitors that slowed investments amid macro uncertainties.

- Catena falls as much as 7.5% after the Swedish logistics property firm offered 4.5 million shares at SEK362, a 7.4% discount versus Tuesday’s closing price.

- Rexel falls as much as 6.9% in early Paris trading, the worst performance in the SBF 120 index, after the company was downgraded to underperform by Exane.

- Telenet slides as much as 5.3% after Oddo BHF downgraded to underperform just over a month after it cut the telecom operator to neutral, saying the company will face significant earnings pressure in 2023, while its fiber joint venture with Fluvius will take years to unlock the value.

- Pennon falls as much as 8.4% after the UK water company’s 1H results, which Jefferies said imply downside risk to earnings estimates.

- Sanofi declines as much as 3% after Horizon Therapeutics disclosed that the French company is among potential suitors it’s holding “highly preliminary discussions” with about a possible sale. Amgen and Johnson & Johnson are others.

Earlier in the session, Asian equities rose, supported by a rally in Chinese shares amid speculation that unrest in China would pressure authorities to speed up the loosening of Covid restrictions, while traders awaited a speech from Fed Chair Jerome Powell. Meanwhile, China’s economic activity contracted further in November amid a record Covid outbreak, with growth likely to remain weak and the central bank expected to add more stimulus to bolster the recovery. The MSCI Asia Pacific Index erased a drop of as much as 0.5% to rise 0.9% on Wednesday, led by consumer discretionary and technology shares. Benchmarks in South Korea and Taiwan gained while Japanese key gauges capped a fourth day of losses. Chinese equities rose for a second day, buoyed by optimism from the removal of lockdown curbs in some districts of Guangzhou which added to hopes that the nation is laying the ground for an eventual Covid-Zero exit. Economic data released earlier Wednesday showed China’s factory and services activity contracted further in November due to Covid curbs.

“I think the direction of reopening is quite clear,” said Vey-Sern Ling, managing director at Union Bancaire Privee. “Government is taking baby steps which is to be expected. It is also doing the right things, such as encouraging vaccination for the elderly.” Powell’s comments will provide traders with more clues on the Fed’s tightening path going forward. Market watchers recently have been expecting slower interest rate hikes, though hawkish remarks from some officials continue to temper optimism. Asian equities have seen stellar performances in November with multiple benchmarks capping their best months in years. The key MSCI Asian measure has jumped nearly 15%, set for its best month since 1998.

Japanese equities dropped, capping a fourth day of losses, as investors monitored the Covid situation in China and awaited Fed Chair Jerome Powell’s speech. The Topix fell 0.4% to close at 1,985.57, while the Nikkei declined 0.2% to 27,968.99. Keyence Corp. contributed the most to the Topix decline, decreasing 2.2%. Out of 2,165 stocks in the index, 573 rose and 1,496 fell, while 96 were unchanged. “Caution remains as the risk of inflation has not gone away, and with US stock prices having difficulty rising significantly, Japan’s stock prices have recently been moving sideways,” said Tomo Kinoshita, a global market strategist at Invesco Asset Management

Australian stocks rose: the S&P/ASX 200 index reversed an earlier loss to close 0.4% higher at 7,284.20 after data showed inflation unexpectedly decelerated in October. The print sent government bond yields lower and suggest the Reserve Bank may be approaching the peak of its policy tightening cycle. Mining and energy shares contributed the most to the benchmark’s rise, with a gauge of materials stocks notching its biggest monthly gain ever as iron ore eyed its own record surge. In New Zealand, the S&P/NZX 50 index rose 1.4% to 11,552.04

In FX, a gauge of the dollar fell for a second day. The Bloomberg Dollar Spot Index is poised to end this month around 4.5% lower, which would be its worst performance since May 2009. Investors continue to bet that China will reopen its economy after authorities on Tuesday adjusted virus restrictions in Zhengzhou, a city that’s home to Apple Inc.’s largest manufacturing site in China. Norway’s krone led gains as oil rose. The onshore yuan advanced 1% versus the dollar as hopes over a relaxation of China’s Covid curbs stoke optimism about the country’s economy. Onshore yuan rallies to 7.0830 vs dollar; offshore currency up 0.8% to 7.0840.

In rates, treasuries were slightly richer across the curve with gains led by belly out to long-end, flattening 2s10s and 2s5s spreads with 2-year yields little changed on the day. Treasuries are on pace for their third monthly gain of 2022 and the biggest since March 2020, as inflation moderated and Fed policymakers remained committed to additional rate increases to reinforce the trend. US 10-year yields around 3.72%, richer by 2bp on the day and outperforming bunds and gilts by 3bp and 4.5bp in the sector; after the data and Powell’s speech and Q&A at the Brookings Institution at 1:30pm in Washington, long-end could draw support into the month-end Treasury index rebalancing at 4pm New York time. Expected month-end duration extension is larger than average at 0.13yr for Dec. 1. Dollar issuance slate empty so far; 11 borrowers priced just over $17b Tuesday, led by Amazon multi-tranche offering. Focal points of month-end session include 3Q GDP revision, JOLTS job openings data and Fed’s Powell speaking on the economic outlook and labor market.

In commodities, OPEC and its allies are increasingly expected to hold production levels steady after the group opted to meet online amid an uncertain market outlook. Earlier this week, OPEC+ delegates signaled that Saudi Arabia and its partners would consider new output curbs at its gathering on Sunday, which was scheduled to take place at the cartel’s Vienna headquarters. But with the group’s decision to hold a virtual session, views are changing, and oil analysts and OPEC+ officials widely predict that the alliance will keep output unchanged. In futures, West Texas Intermediate rose for a third day, climbing above $80 a barrel after industry data pointed to a large decline in US crude stockpiles, while traders weighed the outlook for Chinese demand and the forthcoming OPEC+ meeting. For spot oil prices from around the world, see BOIL. IN THE NEWS The dilemma facing OPEC+ members is that the potential demand slowdown going into next year -- especially in China --coincides with an “exceptionally tight” crude market, according to Bank of America’s Karen Kostanian. Here’s what other analysts are saying we should expect from this weekend’s meeting. European diplomats trying to reach a deal to curb Russian oil prices are wrestling with an awkward truth: Moscow’s main benchmark crude is already trading below the levels proposed for the cap. Saudi Aramco may reduce the official selling price of its flagship Arab Light crude by $2.10 a barrel on-month to Asia for January, according to the median estimate in a Bloomberg survey. The Caspian Pipeline Consortium, which has already suffered two major stoppages this year, is warning of the potential for more because of a lack of spare parts. China’s ongoing battle with Covid-19, which sparked street protests and conciliatory moves from the government after citizens balked at the latest lockdowns, continues to crimp oil demand in the world’s biggest importer. Chevron Corp. found almost half of employees and contractors in Australia have been bullied in the past five years and a third experienced sexual harassment, according to a survey led by an external consultancy

Binance has acquired Sakura Exchange, entering the Japanese market as a JFSA regulated entity.

Looking to the day ahead now, one of the key highlights will be Fed Chair Powell’s speech at the Brookings Institution. Other central bank speakers include the Fed’s Bowman and Cook, the ECB’s Makhlouf and BoE chief economist Pill. The Fed will also be releasing their Beige Book. When it comes to data releases, today will we will get the November ADP employment change (8:15am), second estimate of 3Q GDP and October wholesale inventories (8:30am), November MNI Chicago PMI (9:45am), October pending home sales and JOLTS job openings (10am).

Market Snapshot

- S&P 500 futures up 0.2% to 3,969.25

- STOXX Europe 600 up 0.6% to 439.99

- MXAP up 0.9% to 156.52

- MXAPJ up 1.5% to 508.23

- Nikkei down 0.2% to 27,968.99

- Topix down 0.4% to 1,985.57

- Hang Seng Index up 2.2% to 18,597.23

- Shanghai Composite little changed at 3,151.34

- Sensex up 0.3% to 62,898.19

- Australia S&P/ASX 200 up 0.4% to 7,284.17

- Kospi up 1.6% to 2,472.53

- Brent Futures up 2.2% to $84.89/bbl

- Gold spot up 0.7% to $1,761.34

- U.S. Dollar Index down 0.36% to 106.44

- German 10Y yield up 0.4% to 1.92%

- Euro up 0.4% to $1.0371

Top Overnight News from Bloomberg

- Zhengzhou shuttered hundreds of buildings and apartment blocks hours after lifting broader lockdown measures, as officials strive to make their Covid controls more targeted in line with Beijing’s directives

- Strong demand for goods and services may be starting to overtake supply constraints -- from the pandemic and the war in Ukraine -- as the driver of US prices, according to new gauges built by Federal Reserve economists

- Currency traders hoping to enjoy a quiet run up to Christmas may be in for a shock. One-month implied volatility for major currency pairs -- a gauge of expectations for FX moves over that period -- are sitting well above their 10-year average for this time of year

- Jiang Zemin, the Chinese leader who presided over more than a decade of dramatic economic growth following the bloody 1989 crackdown on pro-democracy protesters in Tiananmen Square, has died. He was 96

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mostly higher at month-end although gains were capped following the subdued handover from Wall St and after disappointing Chinese PMI data. ASX 200 was positive with the index led by strength in the mining-related sectors and with initial losses pared alongside a slew of data releases including better-than-expected Construction Work and softer monthly Australian CPI. Nikkei 225 slipped beneath the 28,000 level after Industrial Production further deteriorated which prompted the government to cut its relevant assessment. Hang Seng and Shanghai Comp were indecisive as recent optimism from hopes of an easing of COVID controls was clouded by disappointing Chinese PMI data which slipped into a deeper contraction.

Top Asian News

- Fullerton Health Said to Mull Stake Sale at $1.1 Billion Value

- Hong Kong Dollar Strengthens Past Strong Half of Trading Band

- Asian Stocks Gain for Second Day on China Reopening Hopes

- NDTV Founders Resign From Holding Firm Board Amid Adani Takeover

- Chinese Stocks in Hong Kong Jump, Capping Best Month Since 2003

- Binance Re-Enters Japan With Sakura Exchange Purchase

- GoTo Shares Fall to Record Low as Major Holders’ Lock-Up Expires

European equities trade on a firmer footing following mixed leads from Wall St, with eyes set on Fed Chair Powell on month-end, Euro Stoxx 50 +0.5%. Sectors in Europe are mostly positive but to a lesser extent than at the cash open; Autos, Consumer Products and Energy outpace while Real Estate and Telecoms lag. US futures are trading a touch above unchanged following yesterday’s session which was characterised by notable tech selling amid a pick-up in US yields, ES +0.2%.

Top European News

- BoE Chief Economist Pill says inflation expected to decline rapidly in H2 2023, demand is easing as household incomes are squeezed, the labour market remains very tight.

- Hungary gets initial green light from the European Commission for its EUR 5.8bln recovery plan, according to Bloomberg; recommends withholding separate EUR 7.5bln in fund.

- Hungary’s Russia-Designed Nuclear Reactors Survive Legal Attack

- Viceroy Target Home REIT Hits Back at Latest Short Report

- Houseboats Get Fresh Look in London’s Brutal Real Estate Market

- Turkish Economy Stumbles, Risks Bigger Downswing Before Election

- Germany Nov. SA Unemployment Change +17K M/m; Est. +13.5K M/m

- BOE Chief Economist Assumes UK Inflation Will Fall Next Year

FX

- DXY is under pressure in early European hours after failing to top 107.00 overnight, having printed an APAC peak of 106.90, matching the Tuesday high.

- Antipodeans lead the charge amid the positive risk move and despite the softer-than-expected Aussie CPI overnight and weak PMIs from China.

- EUR gains were somewhat stalled after EZ headline CPI printed softer than expectations but the core metrics topped forecasts while Cable has managed to attain a foothold on 1.20.

- CNH is the EM outperformer on hopes of looser Chinese COVID restrictions.

- PBoC set USD/CNY mid-point at 7.1769 vs exp. 7.1790 (prev. 7.1989)

- Japanese FX intervention amounted to 0 between October 28th-November 28th, according to MoF.

Fixed Income

- Core bonds dented as core EZ inflation fails to decline, USTs directionally in-fitting but little changed overall pre-Powell.

- Bund Dec’22 slipped from 141.24 to 140.70 (vs 140.50 low) on the EZ inflation release, with market pricing between 50bp & 75bp remains on a knife-edge.

- Gilts are lower by circa 40 ticks on the session in sympathy and were unphased by largely familiar remarks from Chief Economist Pill.

Commodities

- WTI and Brent futures are firmer intraday as the risk tone remains constructive and the Dollar declines.

- Spot gold grinds higher as DXY softens and the risk tone turns less constructive, with the yellow metal rising north of USD 1,750/oz and towards Monday’s USD 1,763/oz peak.

- Base metals are firmer across the board on hopes China will ease its Zero-COVID parameters, with 3M LME copper extending on overnight gains to levels north of USD 8,100/t during the European morning.

- US Private Energy Inventory Data (bbls): Crude -7.9mln (exp. -2.8mln), Gasoline +2.9mln (exp. +1.7mln), Distillate +4.0mln (exp. +1.5mln), Cushing -0.2mln.

- OPEC+ decision to meet virtually on December 4th signals that there is little likelihood of a change in policy and the virtual meeting puts focus on the pending Russian oil price cap decision on December 5th, according to a source with direct knowledge cited by Reuters.

- OPEC+ cancelled the 2nd Dec JTC meeting, according to Argus sources.

China covid updates

- Beijing City reports 2,378 new local COVID cases (prev. 2,126) during 15 hours to 3pm on Wednesday.

- China's Guangzhou will gradually resume normal operations of subway stations and Haizhu trams as of November 30th, according to the Municipal government.

- Beijing is set to allow some residents to skip mass COVID testing, according to Bloomberg.

- China is reportedly mulling rolling out a 4th round of COVID vaccines, according to Bloomberg.

Geopolitics

- China and Russian warplanes temporarily entered South Korea's air defence zone, according to Yonhap.

- Russian Foreign Ministry says Moscow does not intend to discuss the New START treaty with Washington as long as it supplies Ukraine with weapons, via Al Jazeera.

US Event Calendar

- 07:00: Nov. MBA Mortgage Applications -0.8%, prior 2.2%

- 08:15: Nov. ADP Employment Change, est. 200,000, prior 239,000

- 08:30: 3Q GDP Annualized QoQ, est. 2.8%, prior 2.6%

- Personal Consumption, est. 1.6%, prior 1.4%

- PCE Core QoQ, est. 4.5%, prior 4.5%

- GDP Price Index, est. 4.1%, prior 4.1%

- 08:30: Oct. Advance Goods Trade Balance, est. -$90.5b, prior -$92.2b

- 08:30: Oct. Retail Inventories MoM, est. 0.5%, prior 0.4%

- Wholesale Inventories MoM, est. 0.5%, prior 0.6%

- 09:45: Nov. MNI Chicago PMI, est. 47.0, prior 45.2

- 10:00: Oct. JOLTs Job Openings, est. 10.3m, prior 10.7m

- 10:00: Oct. Pending Home Sales YoY, est. -35.2%, prior -30.4%

- Pending Home Sales (MoM), est. -5.7%, prior -10.2%

- 14:00: U.S. Federal Reserve Releases Beige Book

Central Bank speakers

- 08:50: Fed’s Bowman Discusses the Future of Small Banks

- 12:35: Fed’s Cook Discusses the Economic and Policy Outlook

- 13:30: Powell Discusses the Economic Outlook and the Labor Market

DB's Jim Reid concludes the overnight wrap

Markets bent a little yesterday but didn’t break as US stocks rallied around half a percent off their European closing lows into the NY final bell. The S&P 500 (-0.16%) still ultimately lost ground for a third day running though. Interestingly, that came in spite of several positive developments yesterday, with the latest European inflation data surprising on the downside, just as there were fresh signs pointing towards a potential reopening in China. However, the focus is now turning back to the Fed once again, with investors eagerly awaiting Chair Powell’s speech at the Brookings Institution later on today. That’s an important one since the Fed’s blackout period ahead of the next meeting begins this weekend, so this is the last chance Powell will have to give a steer on policy beforehand. In addition, today will bring the latest data on job openings and the quits rate for October, which have recently been cited by the Fed and others as a key gauge of inflationary pressures from the labour market.

With that in mind, it’ll be a big day for Fed watchers, but we shouldn’t forget the ECB as we’ll also get the flash CPI release for the Euro Area at 10am London time. Markets will be paying close attention, but European government bonds were already rallying ahead of that yesterday after the country-specific releases surprised on the downside. For instance, Spanish inflation came in at +6.6% in November using the EU-harmonised measure, which was down from +7.3% in October and also beneath the +7.1% reading expected. Later in the day, we got further signs that inflation might be moving lower, with German inflation down from +11.6% in October to +11.3% in November, whilst Belgian inflation was down from +12.3% in October to +10.6% in November. That trend has continued overnight as well, with Australia’s CPI for October unexpectedly falling to +6.9% (vs. +7.6% expected).

Those signs of decelerating inflation led investors to price in a growing chance that the ECB would slow down the pace of their hikes to 50bps in December. Indeed, the hike that overnight index swaps are pricing in for the next meeting came down by -5.2bps on the day to 56.5bps, suggesting that investors were pricing out the chances of another 75bps hike. In turn, European government bonds rallied across the continent, with yields on 10yr bunds (-6.6bps), OATs (-6.9bps) and BTPs (-8.3bps) all falling on the day.

When it comes to Fed Chair Powell’s speech today, he’s set to be giving remarks on the “economic outlook, inflation and the labor market”, so it should be relevant for policy. It’s widely expected the Fed will downshift their rate hikes to a 50bp pace in December, but our US economists expect Powell to shift the focus away from a downshift towards the Fed’s broader tightening campaign, and to reiterate the key messages from the November press conference. Ahead of that, we had some fresh signs that the Fed’s tightening cycle was impacting the economy, with the Case-Shiller index of 20-cities’ home prices down by a further -1.24% in September, building on its -1.30% decline in August. Bear in mind as well that all 20 cities in the index posted a monthly decline, so this is a very broad-based move lower. Elsewhere, the Conference Board’s consumer confidence numbers also fell back in November, falling to their lowest level since July at 100.2 (vs. 100.0 expected).

Ahead of Powell’s remarks, US Treasuries followed a very different path to their counterparts in Europe, with yields rising at all maturities. The 10yr yield was up +6.3bps on the day to 3.74%, with the move entirely driven by a +6.7bps rise in the real yield. And those moves have only slightly retraced overnight, with the 10yr yield down -2.1bps at 3.72%. With the pickup in real yields, equities were always going to struggle, even if the S&P did recover into the close. The rate-sensitive Nasdaq underperformed, falling -0.59%. Sentiment was similar in Europe, with the STOXX 600 (-0.13%) experiencing its third consecutive decline for the first time since early October.

Over in China, there were some important developments on the Covid situation shortly after we went to press yesterday. First, officials said that they would seek to raise vaccination rates among the elderly, which was good news for markets since stronger levels of immunity are seen as increasing the chances of the economy reopening. Second, there was also a comment that local officials should avoid excessive Covid restrictions, which again was seen as taking the direction of travel further in favour of reopening following the weekend protests. Chinese assets performed strongly on the back of these developments, and in US hours the NASDAQ Golden Dragon China index surged by +5.04%, building on its +2.83% gain over the previous session. The prospect of a future reopening in China offered further support to oil prices as well, with Brent crude up +0.61% to $83.70/bbl.

That boost has continued into Asian markets this morning, with the CSI 300 (+0.10%), the Shanghai Composite (+0.05%) and the Hang Seng (+0.69%) all seeing further gains. That’s in spite of some downbeat data on the economic situation in China, with the manufacturing PMI falling to its lowest level since April at 48.0 (vs. 49.0 expected). The non-manufacturing PMI also deteriorated to 46.7 (vs. 48.0 expected), and the composite PMI fell to a post-April low as well at 47.1. Markets elsewhere in the region are a bit more mixed however, with the Nikkei shedding -0.35%, whereas the KOSPI (+1.18%) has seen solid gains. Looking ahead, US and European equity futures are pointing to gains at the open, with those on the S&P 500 up +0.18%.

Elsewhere yesterday, UK gilts underperformed their European counterparts after comments from the BoE’s Catherine Mann, who’s been one of the more hawkish members on the MPC. Mann said that inflation expectations were becoming “increasingly embedded”, and 10yr gilt yields only fell -2.6bps on the day, a smaller fall than seen for the other big European economies. In the meantime, the latest data on mortgage approvals for October came through, which is the first release entirely after the UK’s mini-budget in late-September. That showed a dip in approvals to 59.0k (vs. 60.0k expected), which is their lowest level since the initial wave of the pandemic.

To the day ahead now, and one of the key highlights will be Fed Chair Powell’s speech at the Brookings Institution. Other central bank speakers include the Fed’s Bowman and Cook, the ECB’s Makhlouf and BoE chief economist Pill. The Fed will also be releasing their Beige Book. When it comes to data releases, today will bring the Euro Area flash CPI release and German unemployment for November, whilst in the US there’s the ADP’s report of private payrolls for November, the second estimate of Q3 GDP, the JOLTS job openings for October, pending home sales for October, and the MNI Chicago PMI for November.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

{kind=link}

{kind=link}

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex