Uncategorized

Futures, Global Stocks Tumble As Markets Reel After Fed’s Hawkish Pause

Futures, Global Stocks Tumble As Markets Reel After Fed’s Hawkish Pause

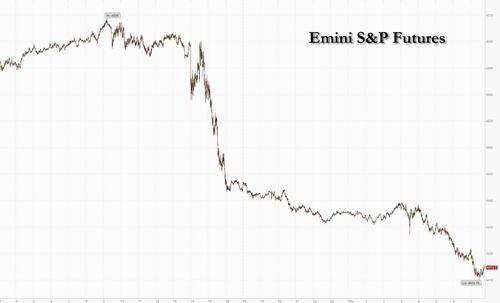

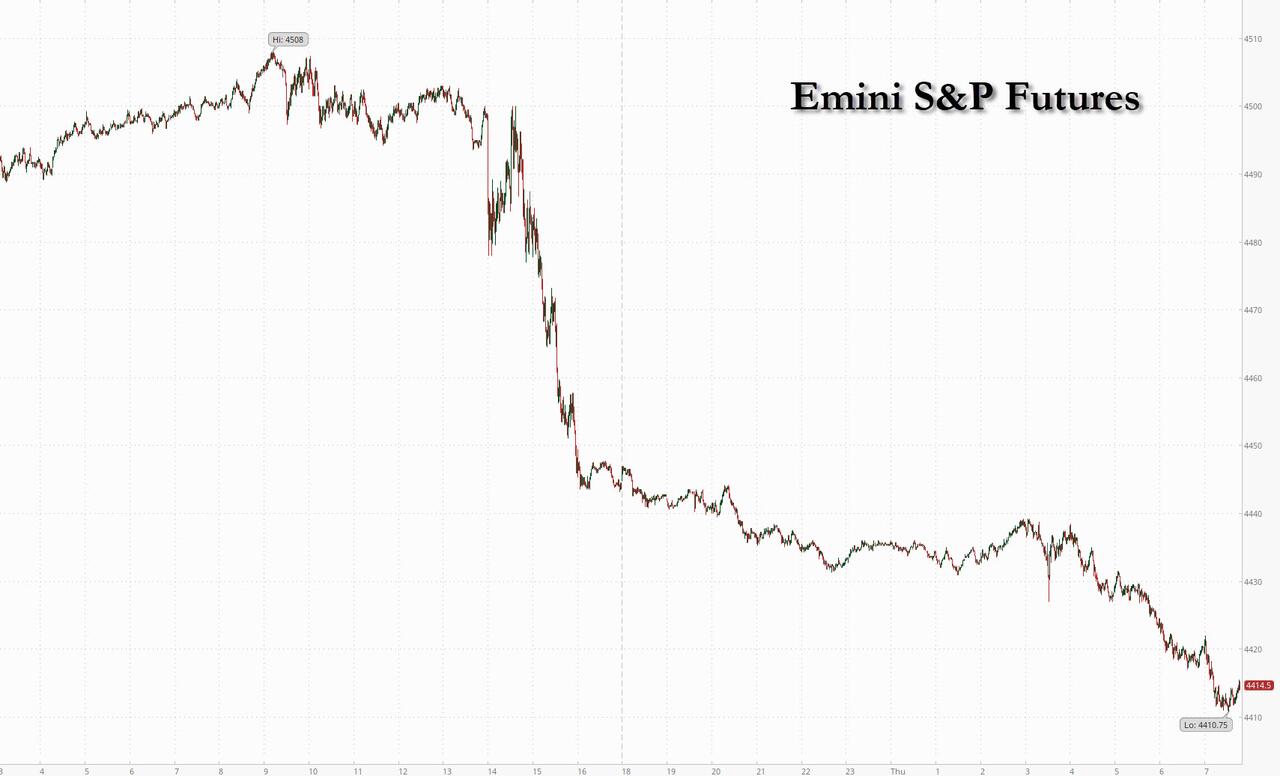

Futures are sharply lower, extending yesterday’s steep losses after…

Share this:

Futures are sharply lower, extending yesterday's steep losses after the Fed’s hawkish pause. The Fed wasn't alone in keeping rates unchanged: it was followed by both the SNB and BOE, both of which surprised markets by not raising rates and sending the franc and sterling sliding. On the other hand, the inflation-ridden Riksbank and Norges both hiked, telling investors to expect more such moves. Hyperinflating basket case Turkey hiked by 500bps, in line with expectations. As of 7:45am, S&P futures tumbled 0.7% to 4,415, while Nasdaq 100 futures were down 1% briefly dipping below the key 15,000 level. Most Treasury yields climbed apart from two-year rates, which edged lower. The Bloomberg Dollar Spot Index traded near the day’s highs, pressuring most other Group-of-10 currencies. Brent crude fell for a third-straight day, trading below $93. Gold slid and Bitcoin declined 1%. Today’s macro data focus is on Jobless Claims, Existing Home Sales, Leading Index, and Philly Fed.

In premarket trading, Splunk was set to open sharply higher after Cisco announced it would purchase the company for $157/share (it closed just below $120). Broadcom slumped after a report by The Information that Google has discussed dropping the company as an AI chips supplier as early as 2027. FedEx shares rise as much as 5.4% after the courier raised the lower end of its fiscal 2024 adjusted EPS forecast, thanks to cost cutting, strong pricing and customers who switched to the courier from its main rival on concern over a potential strike, and prompting analysts to hike their price targets on the stock. Analysts were positive on the company’s cost reduction progress and highlighted the strong performance at its Ground unit and said that guidance is still conservative. Here are the other notable premarket movers:

- ARM Holdings shares fall 2.3%, with the chip designer nearing its $51 IPO price, as rising bond yields put pressure on growth stocks, with tech peers down too.

- Broadcom shares drop as much as 4.6%, following a report from The Information that Google executives “extensively” discussed dropping the semiconductor maker as an AI chips supplier as early as 2027, citing a person familiar with the matter.

- CrowdStrike shares rise as much as 3.4%, as analysts hike their price targets on the stock following the Fal.Con cybersecurity conference and investor briefing, at which it set out new targets. Analysts said the company’s margin outlook was especially strong, and new products such should help boost growth.

- Film and entertainment stocks rise, after Hollywood Studios and writers came a step closer to reaching a deal to end months of strikes. Warner Bros (WBD US) +3.1% and Paramount (PARA US) +3%.

The Fed on Wednesday held its target range, while updated quarterly projections showed most officials favored another rate hike in 2023. Policymakers also see less easing next year, with the median forecast for the federal funds rate at 5.1% by year-end, up from 4.6% when projections were last updated in June.

“People did expect a hawkish hold from the Fed, but it’s the extent of the hawkishness that surprised,” said Lee Hardman, a strategist at MUFG Bank Ltd. “We thought they may take one cut out of next year’s forecasts — instead they took two out. So it was much more hawkish than markets were pricing in.”

Some non-Fed headlines came from BAC’s CFO who says, “It’s difficult to see a US recession when the consumer is spending 4% more year-over year.” Axios reported that the US Chamber of Commerce’s Small Business Index, a confidence indicator, has reached its highest level since COVID struck US markets in early 2020. The survey includes 751 business, each that have fewer than 500 people; 71% say they expect revenue to increase next year. Spoiler alert: it won't.

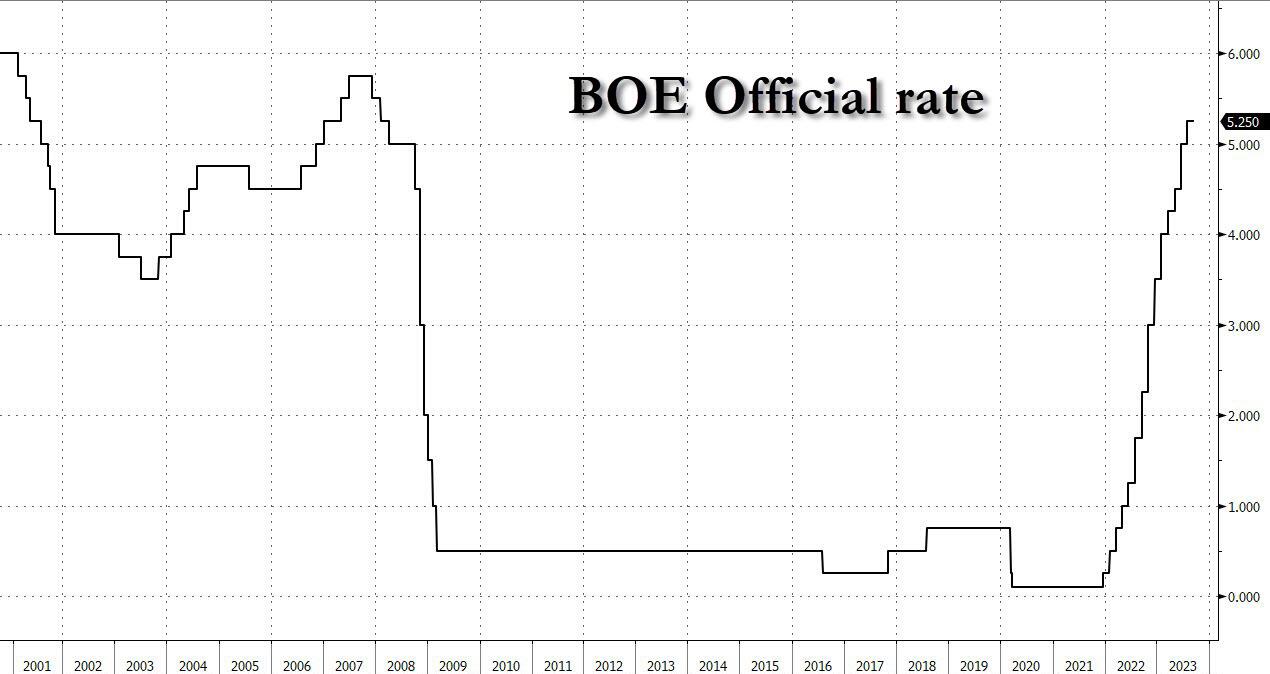

Europe's Stoxx 600 Index declined 1% but was off session lows, with all sectors in the red, as traders digested the Fed’s higher-for-longer message. Travel and leisure stocks fell the most, while miners and industrial stocks also underperformed. Swiss equities were higher after the SNB unexpectedly paused rate hikes, while the BOE is due to announce its rate decision later Shares in UK banks and home builders rose as traders slashed their bets on further rate hikes with UBS saying the BOE hiking cycle is now over. The central bank held its key rate at 5.25%, ending a series of 14 successive hikes since December 2021, after a surprise drop in August inflation this week.

“Inflation has fallen a lot in recent months and we think it will continue to do so,” BOE Governor Andrew Bailey said in a written statement. “That’s welcome news. But there is no room for complacency. We need to be sure inflation returns to normal and we will continue to take the decisions necessary to do just that.”

A day after the Federal Reserve’s meeting, Europe had its own frenetic flurry of central bank decisions. Before the BOE, Swiss National Bank surprised investors by holding interest rates, causing the franc’s steepest drop since May against the euro. Sweden’s Riksbank increased its key rate as expected and said more hikes were possible, while Norway’s central bank said more tightening may come in December after raising rates to the highest in more than 14 years. Here are Europe's top movers:

- Merck shares gain as much as 2.2% after Citi raised its recommendation on the German biotech group to buy, predicting performance in the firm’s Life Science and Semiconductor segments will recover in the near future.

- JD Sports shares rise as much as 8.6% after reporting results that Peel Hunt analysts said reflected a “surprisingly strong” performance in the US following recent guidance cuts from peers Foot Locker and Dick’s Sporting Goods.

- Next shares gain as much as 2.5% after the UK retailer boosted its pretax profit outlook for the full year, following other guidance raises in August and June. The third guidance update in three months is impressive, with the sales outlook suggesting resilience in the first half, Jefferies said.

- Safilo shares rise as much as 8.1%, the most intraday since August 2022, after the Italian eyewear company said it’s launching its Carrera Smart Glasses with Amazon.com’s Alexa technology, according to a statement late on Wednesday.

- Valneva shares rise as much as 4.7% after the French pharmaceutical firm reported better-than-expected first-half earnings. Van Lanschot Kempen sees a “strong set” of figures with beats across the board.

- CVS Group shares gain as much as 4.4% after the veterinary services firm reports better-than-expected profit. The stock plummeted earlier this month as UK antitrust regulators announced a probe of the sector.

- Delivery Hero rises as much as 2%, adding to Wednesday’s 7.1% gain, as the food delivery company confirmed that it’s mulling a sale of some businesses in Southeast Asia. Analysts said a potential deal could boost the company’s balance sheet and profit by shaking off some unprofitable operations that are currently involved in intensive competition.

- Ocado shares drop as much as 9.3% after being downgraded to underperform from neutral at BNP Paribas Exane, which cited the British online grocer’s share price rally in recent months.

- SSP Group shares fall as much as 8.7% after the food services company gave a trading update saying it expects full-year EPS toward the lower end of its guidance range. Analysts at Goodbody and Shore Capital noted the FX headwinds apparent in the update, but were encouraged by the opportunity from new business.

- Engcon shares drop as much as 8.9% after an editorial column on Swedish retail-trading website Placera.se recommended its users sell the Swedish industrial firm’s shares, citing a high valuation and slowing growth prospects.

- Quadient shares fall as much as 8.7% after the French postal- and document-services company reported first-half results that Oddo said were slightly below estimates.

Earlier in the session, Asian stocks fell the most in nearly a month after the Fed signaled that interest rates will remain higher for longer amid renewed economic strength, while Chinese equities slumped on persistent pessimism. The MSCI Asia Pacific Index dropped as much as 1.4%, set for a fourth day of losses, led by health-care and technology shares. Most markets in the region were down, with South Korea’s Kospi Index slumping more than 1% as large-cap chip and battery stocks dragged. The Fed left its benchmark interest rate unchanged as expected, while indicating that borrowing costs will likely stay higher for longer after one more hike this year. The message triggered overnight losses in Wall Street, gains in Treasury yields and strength in the dollar.

- Hang Seng and Shanghai Comp declined alongside the downbeat mood across regional peers, although the losses in the mainland were initially cushioned following the Chinese Cabinet’s pledge to speed up the development of the advanced manufacturing sector and amid resilience in developers after Guangzhou adjust purchase rules for several districts.

- Japan's Nikkei 225 retreated below the 33,000 level as Japanese yields climbed to decade highs and with the BoJ kickstarting its 2-day policy meeting.

- Australia's ASX 200 was lower with the top-weighted financial industry leading the broad declines.

- India’s benchmark stocks gauge dropped for a third consecutive session to its two-week low as US Federal Reserve’s signal to keep interest rates higher for longer spooked equities in Asia. The S&P BSE Sensex fell 0.9% to 66,230.24 in Mumbai, its lowest close since Sept. 6. The NSE Nifty 50 Index declined 0.8% to 19,742.35. ICICI Bank contributed the most to the Sensex’s decline, decreasing 2.8%. Out of 30 shares in the Sensex index, 6 rose and 20 fell, while 4 were unchanged.

In FX, the dollar gained against most major currencies, aside from the yen, which traded around 148 per dollar after weakening on Wednesday to the lowest level since November.

- EUR/CHF rises as much as 0.8% to 0.9656, the biggest daily jump since June

- EUR/SEK drops as much as 0.9% to 11.7687; it rose earlier to 11.9381 after the Riskbank announced a quarter-point interest rate increase

- EUR/NOK drops as much as 0.4% to 11.4573 before halving losses; Wednesday’s low is 11.4560

- GBP/USD falls as much as 0.4% to 1.2265, after the BOE unexpectedly ended its hiking cycle

With most central banks out of the way, attention now turns to Friday's BOJ announcement. There are heightened prospects of official support for the Japanese currency, said John Vail, chief global strategist for Nikko Asset Management Co. in Tokyo. “Japan’s Ministry of Finance is likely to intervene in large fashion at 150 per dollar because it is hard to tolerate more inflationary pressure.”

The value of the yen has slumped to the lowest on record, as measured against a broad basket of its peers and adjusted for inflation, according to data from the Bank for International Settlements. This underscores the pressure to address yen weakness at the Bank of Japan, which is where this week’s series of central bank policy meetings wraps up on Friday.

In rates, treasury yields were broadly higher after the rate on the two-year note, which is more sensitive to imminent Fed moves, hit the highest since 2006 on Wednesday. After resuming post-Fed selloff in early Asia session, front-end of the Treasuries curve trades richer on the day into early US, outperforming belly and long-end as steepening move extends. US yields richer by 2bp across front-end of the curve while belly out to long-end trades cheaper by 1.5bp to 4bp on the day; 10-year yields around 4.45% the highest level since 2007, underperforming bunds and gilts by 1.5bp and 5bp in the sector. Gilts were supported after Bank of England keeps rates unchanged. Long-end Treasury yields also reach new cycle highs, joining rest of the curve after Wednesday’s Fed decision. Dollar IG issuance slate includes IBK 5Y; issuance paused Wednesday for the Fed decision and is expected to remain quiet for Thursday. US economic data slate includes 2Q current account balance, September Philadelphia Fed business outlook and weekly initial jobless claims (8:30am), August existing home sales and leading index (10am); no Fed speakers scheduled.

In commodities, oil’s breakneck rally is taking a breather as a smaller-than-expected drop in US crude stockpiles bolstered technical resistance to further gains; crude futures declined with WTI falling 1% to trade near $88.80. Spot gold drops 0.4%.

To the day ahead, and we’ll get the Bank of England’s latest policy decision, and also hear remarks from the ECB’s Schnabel and Lane. Otherwise, data releases include the US weekly initial jobless claims, existing home sales for August, the Conference Board’s leading index for August, and the Philadelphia Fed’s business outlook for September. In the Euro Area, we’ll get the preliminary consumer confidence reading for September, whilst in the UK there’s the public finances for August.

Market Snapshot

- S&P 500 futures down 0.4% to 4,430.50

- Brent Futures down 1.3% to $92.35/bbl

- Gold spot down 0.2% to $1,926.07

- U.S. Dollar Index up 0.13% to 105.46

- STOXX Europe 600 down 0.7% to 457.60

- MXAP down 1.5% to 159.24

- MXAPJ down 1.6% to 492.56

- Nikkei down 1.4% to 32,571.03

- Topix down 0.9% to 2,383.41

- Hang Seng Index down 1.3% to 17,655.41

- Shanghai Composite down 0.8% to 3,084.70

- Sensex down 0.9% to 66,197.17

- Australia S&P/ASX 200 down 1.4% to 7,065.23

- Kospi down 1.7% to 2,514.97

- German 10Y yield little changed at 2.73%

- Euro little changed at $1.0657

- Brent Futures down 1.3% to $92.35/bbl

Top Overnight News

- Japan may be nearing a point where it can declare victory in its battle against deflation, paving the way for further BOJ policy normalization. Nikkei

- As China's stock market struggles to recover, regulators have started to probe some hedge funds and brokerages on quantitative trading strategies amid a growing outcry against a sector able to profit from share price falls and volatility. RTRS

- Natural gas prices sink in Europe as Chevron seems close to resolving a strike in Australia while flows recover in Norway. BBG

- Norway’s central bank hikes rates by 25bp to 4.25%, as expected, and provides hawkish forward guidance by signaling another increase in Dec (most assumed today’s hike would be the last one). Switzerland’s SNB surprises markets by leaving rates unchanged (economists were anticipating a 25bp hike). BBG

- Poland looks to downplay remarks from its PM about no longer supplying weapons to Ukraine, insisting that the country remains a committed to helping Kyiv achieve victory. FT

- Google has talked “extensively” about dropping Broadcom as its AI chip supplier as soon as 2027 as the internet giant looks to cut costs and utilize proprietary silicon (in addition, Google is working to replace Broadcom with Marvell for network interface chips). The Information

- House Republicans reported major progress charting a path forward on a partisan bill to avert a government shutdown and a Department of Defense spending bill — two measures that suffered public setbacks just a day before — after Speaker Kevin McCarthy (R-Calif.) hashed out a new framework for a GOP-only stopgap proposal in a House Republican conference meeting that lasted more than two hours on Wednesday. The Hill

- AMZN is abandoning plans to impose a new fee on merchants that don’t use its shipping services amid increased regulatory/antitrust scrutiny on the company from the gov’t. BBG

- FDX reported very strong FQ1 earnings, with EPS of 4.55 (vs. the Street 3.73), thanks to aggressive cost cutting, and the full-year EPS outlook was increased (although by less than the Q1 beat). RTRS

A more detailed look at global markets courtesy of Newquawk

Asia-Pac stocks were pressured in the aftermath of the FOMC’s hawkish pause. ASX 200 was lower with the top-weighted financial industry leading the broad declines. Nikkei 225 retreated below the 33,000 level as Japanese yields climbed to decade highs and with the BoJ kickstarting its 2-day policy meeting. Hang Seng and Shanghai Comp declined alongside the downbeat mood across regional peers, although the losses in the mainland were initially cushioned following the Chinese Cabinet’s pledge to speed up the development of the advanced manufacturing sector and amid resilience in developers after Guangzhou adjust purchase rules for several districts.

Top Asian News

- Japanese PM Kishida said he will instruct people to pull together the pillars of an economic package early next week, while they will include measures to counter inflation and social measures to counter declining population, according to Reuters.

- Chinese Commerce Ministry says some firms have obtained export licenses for gallium and germanium; willing to seek a basket of solutions for the Australian wine dispute.

- China's 2023 nat gas demand seen at 396.4BCM, +8% Y, via CNOOC; LNG imports 70.79mln/T, +10.9% YY. Nat gas demand from China seen peaking in 2040 at 700BCM.

European bourses are pressured as the region reacts to Wednesday's FOMC where a hawkish hold was delivered, Euro Stoxx 50 -1.1%. Action which continues the tone of APAC trade but with the region conscious of a Chinese cabinet pledge around manufacturing and also beginning to look ahead to Friday's BoJ. Sectors are primarily in the red with the exception of Retail post-earnings from JD Sports and Next which reside towards the top of the Stoxx 600; Travel/Leisure and Basic Resources lag, latter on benchmark activity and numerous price target cuts. US futures are lower across the board but with action slightly more contained when compared to European peers, ES -0.4%, NQ -0.6%; today's docket has a handful of data points before Friday's Fed speak resumption with Cook, Daly & Kashkari. Google (GOOG) reportedly wants to ditch Broadcom (AVGO) as its TPU sever chip supplier to reduce AI costs, according to The Information; Since last year has been working to replace Broadcom with Marvell Technology (MRVL). Pre-market: GOOG -0.7%, AVGO -5.2%, MRVL +3.5%

Top European News

- Sunak Gambles on Voters Focusing More on Costs Than Climate

- Next Raises Guidance Again as Wage Gains Boost Shoppers

- SNB Surprises With Rate Pause as Tightening Tames Inflation

- Riksbank Hikes Swedish Rate With Door Kept Open to Act Again

- Norway Raises Rate Again and Signals Another Move in December

- Swiss Stocks Outshine Peers as SNB Pauses; Fed Weighs on Region

FX

- The Fed revives Greenback fortunes via more hawkish dot plots, DXY firmly back above 105.000 within a 105.400-680 range.

- Franc collapses as SNB defies expectations for a 25bp hike and bases new forecasts on steady 1.75% rate, EUR/CHF and USD/CHF spike circa 100 pips to 0.9677 and 0.9078 respectively.

- Pound flounders in the dark about BoE prospects for midday as markets remain split between pause and 1/4 point rate rise, Cable sub-1.2300 from just over 1.2350 at best.

- Yen and Euro pare declines vs. Dollar ahead of 148.50 and 1.0600, with EUR/USD propped up by a Fib and option expiries.

- Norwegian Crown underpinned around 11.5000 vs. Euro after hawkish Norges Bank hike, Swedish Krona choppy on either side of 11.9000 as Riksbank reaches a peak and hedges 25% FX reserves.

- PBoC set USD/CNY mid-point at 7.1730 vs exp. 7.3052 (prev. 7.1732)

- The European Commission has sent a letter to Poland listing 11 questions to determine the scope of the visa-for-bribes scandal and the EU security impact, via Politico; the letter warns that Poland could be violating EU law

Fixed Income

- Bonds off worst levels, but still heavy in wake of hawkish FOMC and through slew of other Central Bank pronouncements.

- Bunds below par between 129.69-23 parameters, Gilts sub-96.00 within 96.41-95.81 range and T-note nearer base of 108-16/25+ bounds pre-BoE, IJC, Philly Fed and ECB speakers

Commodities

- Crude benchmarks are softer intraday given broader risk sentiment post-Fed, WTI below USD 89.00/bbl and Brent down to a test of USD 92.00/bbl respectively at worst; currently off these lows.

- Dutch TTF pressured as Offshore Alliance members at Woodside have overwhelmingly voted to endorse a deal with the company.

- Spot gold is under modest pressure as the USD remains bid with base metals similarly pressured on the broader risk tone.

- Saudi Crown Prince MBS responded that output reductions are purely based on supply and demand to the market when asked about criticism that oil output cuts help Russia.

- Australian industrial arbitrator said Chevron (CVX) and unions are on the precipice of achieving the first enterprise agreements for LNG facilities and discussions have resulted in widespread agreement on the majority of provisions of proposals. The arbitrator made recommendations on pay and working conditions for Chevron and unions to consider but noted that a failure to settle all outstanding issues would result in the agreed provisions simply evaporating, while parties are required to advise the commission of their acceptance or rejection of recommendations by 09:00 Sydney time on Friday.

- Offshore Alliance members at Woodside (WDS AT) have overwhelmingly voted to endorse a deal with the company while members at Chevron (CVX) will meet tonight to consider a recommendation made by the Fair Work Commission, according to a statement.

- Natural Gas Pipeline Co. declared a force majeure on the M&M line near compressor station 158 located in Dewey County, Oklahoma.

- Russia is mulling an additional tax on exports for some commodities including metals, according to sources cited by Reuters.

Geopolitics

- Russian Foreign Ministry said NATO drills near Russian borders are increasingly provocative and aggressive in nature, as well increase risks of incidents, according to RIA.

- Saudi Arabia said solving the Palestinian issue is critical to a deal with Israel, according to FT. In relevant news, Saudi Crown Prince MBS said he is prepared to work with whoever is leading Israel if there is a breakthrough in negotiations for normalisation with Israel, while he had also commented that Saudis will get a nuclear weapon if Iran does first, according to AFP and Fox News.

- Iranian President Raisi said Iran has no problem with IAEA inspections of its nuclear sites.

- Qatar held separate bilateral meetings with the US and Iran this week, touching on nuclear and drone issues, according to sources cited by Reuters.

- Kuwait's PM said the Iraqi ruling on regulating navigation in Khor Abdullah Waterway includes historical fallacies and Iraq needs to take concrete, decisive and urgent measures to address the ruling, according to Reuters.

- Nagorno-Karabakh ethnic Armenians say Azerbaijani forces have violated the ceasefire; Azerbaijan denies its forces violated the ceasefire.

US Event Calendar

- 08:30: Sept. Initial Jobless Claims, est. 225,000, prior 220,000

- 08:30: Sept. Continuing Claims, est. 1.69m, prior 1.69m

- 08:30: Sept. Philadelphia Fed Business Outl, est. -1.0, prior 12.0

- 08:30: 2Q Current Account Balance, est. -$220b, prior -$219.3b

- 10:00: Aug. Existing Home Sales MoM, est. 0.7%, prior -2.2%

- 10:00: Aug. Leading Index, est. -0.5%, prior -0.4%

DB's Jim Reid concludes the overnight wrap

As widely expected, the FOMC kept the fed funds rate on hold yesterday, but this pause was accompanied by clear hawkish undertones and both bonds and equities sold off notably in the aftermath. 10yr US yields are at 4.43% as I type this morning, +12bps above where they were prior to the meeting. The starting point for the hawkishness came from the updated dot plot in the new Summary of Economic Projections. The end-2023 median dot was unchanged at 5.6%, but the median dot for 2024 moved 50bps higher to 5.1% (our US economists had expected 2024 to move up by 25bps). So the median FOMC member is pencilling in only two rate cuts in 2024, after one more hike this year. Interestingly, the newly published projections for 2026 showed the median dot at 2.9%, still above the long-term projection of 2.5%, so pointing to a persistently "tight" policy stance. The higher 2024-25 dot plot came as the SEP moved further towards a soft landing view, lowering unemployment projections for both 2024 and 2025 by 0.4pp to 4.1%. That would be only a slight uptick from the latest 3.8% level.

In the press conference Powell actually said that he “would not” have a soft landing as a baseline expectation, though later adding that soft landing is a primary objective for the FOMC. A little bit of a confusing message but overall, Powell reinforced a higher-for-longer message. Echoing the dot plot, he noted that the neutral rate may have risen and it was “certainly possible that the neutral rate...at this moment is higher than (the long-run rate)”. He also downplayed the prospects of cuts, saying that the FOMC was “never intending to send a signal” about timing of rate cuts with its dot plot and that “there’s so much uncertainty around” this.

Powell’s comments did see some moderation of the near-term tightening bias. He noted several times that the Fed is now in a position to “proceed carefully”. The prepared remarks struck a softer tone on labour market tightness and Powell highlighted that the last three inflation prints were “very good” readings, though not yet enough for the Fed to be confident they have reached a “sufficiently restrictive” stance. Our US economists note that with the FOMC end-2023 projections being likely too high on inflation and too low on unemployment, these set a relatively low bar for skipping the final projected hike. Correspondingly, our economists continue to expect no further rate increases – see the reaction note here for their full take.

So overall, the Fed sent a clear message that they think rates will stay high for longer, and the markets took this on board. Fed fund futures saw the chances of another hike by the end of the year move up to 54% from 45% the day before, with the peak rate now priced for January 2024 (with a 58% chance of a hike by then). Fed funds pricing for end-24 rose by +13.3bps on the day, and 20bps from its earlier intra-day lows, to a new cycle high of 4.76% (this is still more than 30bps below the Fed’s new median dot). My CoTD yesterday looked the implications of this pricing. Although it reflects the market pricing in a soft landing, the high levels probably increase the risk of a hard one. See the short note here.

In the bond market, the 2yr Treasury yield had been trading a few bps lower prior to the Fed decision but spiked by nearly 10bps in its immediate aftermath and closed +8.5bps up on the day at 5.18%, the highest level since 2006. The 10yr yield was up by +4.9bps to 4.41%, a new post-2007 high and is above 4.43% as I type. Meanwhile, the 10yr real yield closed above 2% for the first time since early 2009 (+6.6bps to 2.05%). Equities also lost ground in response to the Fed’s hawkish signal. The S&P 500 was down -0.94% by the close, with the decline coming during and after Powell’s press conference. Tech stocks lagged, with the NASDAQ down -1.53% and the Magnificent Seven mega caps down -2.20%. In FX, the dollar index gained about half a percent following the Fed event, closing up +0.19% on the day after trading lower earlier on. This morning in Asia, the trend continues with the dollar index rising another +0.2% and to fresh 14-year highs. The Yen has drifted to the lowest level since last November since the FOMC with this being an interesting set up ahead of the BoJ tomorrow morning.

Equity markets across Asia are also tumbling this morning with the KOSPI (-1.44%) leading losses followed by the Hang Seng (-1.21%), the Nikkei (-1.14%), the Shanghai Composite (-0.58%) and the CSI (-0.52%). S&P 500 (-0.25%) and NASDAQ 100 (-0.35%) futures are also moving lower again as the FOMC message continues to reverberate.

With the Fed out of the way, attention will now turn to the Bank of England, who are announcing their latest policy decision at 12:00 London time. Up until yesterday morning, it had been widely expected that the BoE would deliver another 25bp hike. But we then got a strong downside surprise from the August CPI print, where headline inflation unexpectedly fell to +6.7% (vs. +7.0% expected). So markets are now only pricing in a 46% chance of a rate hike today, and it’s very finely balanced as we approach the decision.

Our own UK economist at DB has also changed his call following the CPI data (link here), and now thinks that the BoE will skip a rate hike at this meeting. He thinks that the CPI print offers the MPC more optionality to pause, and there were also positive signs beyond the headline number. For instance, core CPI fell to +6.2% (vs. +6.8% expected), whilst the closely-watched services CPI rate fell to +6.8% as well. However, he still sees this decision as finely balanced, with the big miss in inflation and weaker growth momentum now in stark contrast to elevated wage growth. The growing chance of a pause has been evident among gilts as well, with 10yr yields experiencing a sharp decline of -13.0bps yesterday. In addition, the 2yr yield (-16.2bps) closed at a 3-month low of 4.82%.

Elsewhere in Europe, markets put in a strong performance ahead of the Fed’s decision, with the STOXX 600 (+0.91%) recovering from its rough start to the week. That was echoed across the major indices, with the DAX (+0.75%), the CAC 40 (+0.67%) and the FTSE 100 (+0.93%) posting solid gains of their own. It was the same story on the bond side too, as yields on 10yr bunds (-3.6bps), OATs (-4.4bps) and BTPs (-6.6bps) moved off their highs from the previous day. All before the FOMC of course.

Looking at yesterday’s other data, German PPI continued to plunge, with the latest reading for August at -12.6% (vs. -12.5% expected). That’s the fastest decline in recorded data back to 1948, although that is down from a record peak one year earlier of almost +46%.

To the day ahead, and we’ll get the Bank of England’s latest policy decision, and also hear remarks from the ECB’s Schnabel and Lane. Otherwise, data releases include the US weekly initial jobless claims, existing home sales for August, the Conference Board’s leading index for August, and the Philadelphia Fed’s business outlook for September. In the Euro Area, we’ll get the preliminary consumer confidence reading for September, whilst in the UK there’s the public finances for August.

Uncategorized

February Employment Situation

By Paul Gomme and Peter Rupert The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000…

Share this:

By Paul Gomme and Peter Rupert

The establishment data from the BLS showed a 275,000 increase in payroll employment for February, outpacing the 230,000 average over the previous 12 months. The payroll data for January and December were revised down by a total of 167,000. The private sector added 223,000 new jobs, the largest gain since May of last year.

Temporary help services employment continues a steep decline after a sharp post-pandemic rise.

Average hours of work increased from 34.2 to 34.3. The increase, along with the 223,000 private employment increase led to a hefty increase in total hours of 5.6% at an annualized rate, also the largest increase since May of last year.

The establishment report, once again, beat “expectations;” the WSJ survey of economists was 198,000. Other than the downward revisions, mentioned above, another bit of negative news was a smallish increase in wage growth, from $34.52 to $34.57.

The household survey shows that the labor force increased 150,000, a drop in employment of 184,000 and an increase in the number of unemployed persons of 334,000. The labor force participation rate held steady at 62.5, the employment to population ratio decreased from 60.2 to 60.1 and the unemployment rate increased from 3.66 to 3.86. Remember that the unemployment rate is the number of unemployed relative to the labor force (the number employed plus the number unemployed). Consequently, the unemployment rate can go up if the number of unemployed rises holding fixed the labor force, or if the labor force shrinks holding the number unemployed unchanged. An increase in the unemployment rate is not necessarily a bad thing: it may reflect a strong labor market drawing “marginally attached” individuals from outside the labor force. Indeed, there was a 96,000 decline in those workers.

Earlier in the week, the BLS announced JOLTS (Job Openings and Labor Turnover Survey) data for January. There isn’t much to report here as the job openings changed little at 8.9 million, the number of hires and total separations were little changed at 5.7 million and 5.3 million, respectively.

As has been the case for the last couple of years, the number of job openings remains higher than the number of unemployed persons.

Also earlier in the week the BLS announced that productivity increased 3.2% in the 4th quarter with output rising 3.5% and hours of work rising 0.3%.

The bottom line is that the labor market continues its surprisingly (to some) strong performance, once again proving stronger than many had expected. This strength makes it difficult to justify any interest rate cuts soon, particularly given the recent inflation spike.

unemployment pandemic unemploymentUncategorized

Mortgage rates fall as labor market normalizes

Jobless claims show an expanding economy. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

Share this:

Everyone was waiting to see if this week’s jobs report would send mortgage rates higher, which is what happened last month. Instead, the 10-year yield had a muted response after the headline number beat estimates, but we have negative job revisions from previous months. The Federal Reserve’s fear of wage growth spiraling out of control hasn’t materialized for over two years now and the unemployment rate ticked up to 3.9%. For now, we can say the labor market isn’t tight anymore, but it’s also not breaking.

The key labor data line in this expansion is the weekly jobless claims report. Jobless claims show an expanding economy that has not lost jobs yet. We will only be in a recession once jobless claims exceed 323,000 on a four-week moving average.

From the Fed: In the week ended March 2, initial claims for unemployment insurance benefits were flat, at 217,000. The four-week moving average declined slightly by 750, to 212,250

Below is an explanation of how we got here with the labor market, which all started during COVID-19.

1. I wrote the COVID-19 recovery model on April 7, 2020, and retired it on Dec. 9, 2020. By that time, the upfront recovery phase was done, and I needed to model out when we would get the jobs lost back.

2. Early in the labor market recovery, when we saw weaker job reports, I doubled and tripled down on my assertion that job openings would get to 10 million in this recovery. Job openings rose as high as to 12 million and are currently over 9 million. Even with the massive miss on a job report in May 2021, I didn’t waver.

Currently, the jobs openings, quit percentage and hires data are below pre-COVID-19 levels, which means the labor market isn’t as tight as it once was, and this is why the employment cost index has been slowing data to move along the quits percentage.

3. I wrote that we should get back all the jobs lost to COVID-19 by September of 2022. At the time this would be a speedy labor market recovery, and it happened on schedule, too

Total employment data

4. This is the key one for right now: If COVID-19 hadn’t happened, we would have between 157 million and 159 million jobs today, which would have been in line with the job growth rate in February 2020. Today, we are at 157,808,000. This is important because job growth should be cooling down now. We are more in line with where the labor market should be when averaging 140K-165K monthly. So for now, the fact that we aren’t trending between 140K-165K means we still have a bit more recovery kick left before we get down to those levels.

From BLS: Total nonfarm payroll employment rose by 275,000 in February, and the unemployment rate increased to 3.9 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, in government, in food services and drinking places, in social assistance, and in transportation and warehousing.

Here are the jobs that were created and lost in the previous month:

In this jobs report, the unemployment rate for education levels looks like this:

- Less than a high school diploma: 6.1%

- High school graduate and no college: 4.2%

- Some college or associate degree: 3.1%

- Bachelor’s degree or higher: 2.2%

Today’s report has continued the trend of the labor data beating my expectations, only because I am looking for the jobs data to slow down to a level of 140K-165K, which hasn’t happened yet. I wouldn’t categorize the labor market as being tight anymore because of the quits ratio and the hires data in the job openings report. This also shows itself in the employment cost index as well. These are key data lines for the Fed and the reason we are going to see three rate cuts this year.

recession unemployment covid-19 fed federal reserve mortgage rates recession recovery unemploymentUncategorized

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Inside The Most Ridiculous Jobs Report In History: Record 1.2 Million Immigrant Jobs Added In One Month

Last month we though that the January…

Share this:

{kind=link}

Last month we though that the January jobs report was the "most ridiculous in recent history" but, boy, were we wrong because this morning the Biden department of goalseeked propaganda (aka BLS) published the February jobs report, and holy crap was that something else. Even Goebbels would blush.

What happened? Let's take a closer look.

On the surface, it was (almost) another blockbuster jobs report, certainly one which nobody expected, or rather just one bank out of 76 expected. Starting at the top, the BLS reported that in February the US unexpectedly added 275K jobs, with just one research analyst (from Dai-Ichi Research) expecting a higher number.

{kind=link}

Some context: after last month's record 4-sigma beat, today's print was "only" 3 sigma higher than estimates. Needless to say, two multiple sigma beats in a row used to only happen in the USSR... and now in the US, apparently.

Before we go any further, a quick note on what last month we said was "the most ridiculous jobs report in recent history": it appears the BLS read our comments and decided to stop beclowing itself. It did that by slashing last month's ridiculous print by over a third, and revising what was originally reported as a massive 353K beat to just 229K, a 124K revision, which was the biggest one-month negative revision in two years!

Of course, that does not mean that this month's jobs print won't be revised lower: it will be, and not just that month but every other month until the November election because that's the only tool left in the Biden admin's box: pretend the economic and jobs are strong, then revise them sharply lower the next month, something we pointed out first last summer and which has not failed to disappoint once.

In the past month the Biden department of goalseeking stuff higher before revising it lower, has revised the following data sharply lower:

— zerohedge (@zerohedge) August 30, 2023

- Jobs

- JOLTS

- New Home sales

- Housing Starts and Permits

- Industrial Production

- PCE and core PCE

To be fair, not every aspect of the jobs report was stellar (after all, the BLS had to give it some vague credibility). Take the unemployment rate, after flatlining between 3.4% and 3.8% for two years - and thus denying expectations from Sahm's Rule that a recession may have already started - in February the unemployment rate unexpectedly jumped to 3.9%, the highest since February 2022 (with Black unemployment spiking by 0.3% to 5.6%, an indicator which the Biden admin will quickly slam as widespread economic racism or something).

And then there were average hourly earnings, which after surging 0.6% MoM in January (since revised to 0.5%) and spooking markets that wage growth is so hot, the Fed will have no choice but to delay cuts, in February the number tumbled to just 0.1%, the lowest in two years...

... for one simple reason: last month's average wage surge had nothing to do with actual wages, and everything to do with the BLS estimate of hours worked (which is the denominator in the average wage calculation) which last month tumbled to just 34.1 (we were led to believe) the lowest since the covid pandemic...

... but has since been revised higher while the February print rose even more, to 34.3, hence why the latest average wage data was once again a product not of wages going up, but of how long Americans worked in any weekly period, in this case higher from 34.1 to 34.3, an increase which has a major impact on the average calculation.

While the above data points were examples of some latent weakness in the latest report, perhaps meant to give it a sheen of veracity, it was everything else in the report that was a problem starting with the BLS's latest choice of seasonal adjustments (after last month's wholesale revision), which have gone from merely laughable to full clownshow, as the following comparison between the monthly change in BLS and ADP payrolls shows. The trend is clear: the Biden admin numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is far more accurate), shows an accelerating slowdown.

But it's more than just the Biden admin hanging its "success" on seasonal adjustments: when one digs deeper inside the jobs report, all sorts of ugly things emerge... such as the growing unprecedented divergence between the Establishment (payrolls) survey and much more accurate Household (actual employment) survey. To wit, while in January the BLS claims 275K payrolls were added, the Household survey found that the number of actually employed workers dropped for the third straight month (and 4 in the past 5), this time by 184K (from 161.152K to 160.968K).

This means that while the Payrolls series hits new all time highs every month since December 2020 (when according to the BLS the US had its last month of payrolls losses), the level of Employment has not budged in the past year. Worse, as shown in the chart below, such a gaping divergence has opened between the two series in the past 4 years, that the number of Employed workers would need to soar by 9 million (!) to catch up to what Payrolls claims is the employment situation.

There's more: shifting from a quantitative to a qualitative assessment, reveals just how ugly the composition of "new jobs" has been. Consider this: the BLS reports that in February 2024, the US had 132.9 million full-time jobs and 27.9 million part-time jobs. Well, that's great... until you look back one year and find that in February 2023 the US had 133.2 million full-time jobs, or more than it does one year later! And yes, all the job growth since then has been in part-time jobs, which have increased by 921K since February 2023 (from 27.020 million to 27.941 million).

Here is a summary of the labor composition in the past year: all the new jobs have been part-time jobs!

But wait there's even more, because now that the primary season is over and we enter the heart of election season and political talking points will be thrown around left and right, especially in the context of the immigration crisis created intentionally by the Biden administration which is hoping to import millions of new Democratic voters (maybe the US can hold the presidential election in Honduras or Guatemala, after all it is their citizens that will be illegally casting the key votes in November), what we find is that in February, the number of native-born workers tumbled again, sliding by a massive 560K to just 129.807 million. Add to this the December data, and we get a near-record 2.4 million plunge in native-born workers in just the past 3 months (only the covid crash was worse)!

The offset? A record 1.2 million foreign-born (read immigrants, both legal and illegal but mostly illegal) workers added in February!

Said otherwise, not only has all job creation in the past 6 years has been exclusively for foreign-born workers...

... but there has been zero job-creation for native born workers since June 2018!

This is a huge issue - especially at a time of an illegal alien flood at the southwest border...

... and is about to become a huge political scandal, because once the inevitable recession finally hits, there will be millions of furious unemployed Americans demanding a more accurate explanation for what happened - i.e., the illegal immigration floodgates that were opened by the Biden admin.

Which is also why Biden's handlers will do everything in their power to insure there is no official recession before November... and why after the election is over, all economic hell will finally break loose. Until then, however, expect the jobs numbers to get even more ridiculous.

Wendy’s has a new deal for daylight savings time haters

Mortgage rates fall as labor market normalizes

Racial and Ethnic Wealth Inequality in the Post‑Pandemic Era

Wealth Inequality by Age in the Post‑Pandemic Era

Interest rates, the best it gets. It’s time to deploy cash

Is the biotech market rally real? Data suggest comeback in private, public markets

February Employment Situation

People Who Received Ivermectin Were Better Off, Study Finds

Shipping company files surprise Chapter 7 bankruptcy, liquidation

Wendy’s teases new $3 offer for upcoming holiday

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoAll Of The Elements Are In Place For An Economic Crisis Of Staggering Proportions

-

Uncategorized1 month ago

Uncategorized1 month agoCathie Wood sells a major tech stock (again)

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoCalifornia Counties Could Be Forced To Pay $300 Million To Cover COVID-Era Program

-

Uncategorized2 weeks ago

Uncategorized2 weeks agoApparel Retailer Express Moving Toward Bankruptcy

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoIndustrial Production Decreased 0.1% in January

-

International2 days ago

International2 days agoWalmart launches clever answer to Target’s new membership program

-

Uncategorized3 weeks ago

Uncategorized3 weeks agoRFK Jr: The Wuhan Cover-Up & The Rise Of The Biowarfare-Industrial Complex

-

International2 days ago

International2 days agoEyePoint poaches medical chief from Apellis; Sandoz CFO, longtime BioNTech exec to retire